iamai - aml mobile vas report - launch presentation - 2011-07

DESCRIPTION

Analysys Mason in collaboration with IAMAI has developed a Vision Document on Mobile VAS industry in India, titled “Evolution of Mobile VAS in India”. This report was released on 27th July, 2011 in New Delhi at a full day conference hosted jointly by Analysys Mason and IAMAI. The key findings of the report were released by Shri Sachin Pilot, Minister of State, Communications and IT, Government of India. Commenting upon the report, Shri Sachin Pilot said “The mobile value added services is miniscule at present in comparison to its potential and the government would make appropriate efforts to put the industry on an equitable and sustainable growth path.” However, in order for the industry to be a success, he suggested that service providers should provide locally relevant services in local languages. The inaugural session comprised of renowned industry delegates: Rajan Anandan, Managing Director, Google India; Dr. Kiran Karnik, Former President, NASSCOM; Hitesh Oberoi, Chairman, IAMAI & Managing Director & Chief Executive Officer, Infoedge India Ltd; Sandeep Sawhney, Chief Product & Innovation Officer, Aircel; D.P Venkatesh, CEO, mPortal. Kunal Bajaj, Partner & Director India, Analysys Mason gave a presentation on the launch of this report and stated: “Carriers are under tremendous pressure from competition and declining ARPUs, which have stunted revenue growth. Recent trends in the sector indicate that now is the right time for them to increase their focus on the VAS space to find new opportunities for differentiation and earnings.” Besides the inaugural session, the conference comprised of four panel discussions on current themes in the Mobile VAS industry: Mobile Entertainment, Livelihood Enhancement Services, Mobile Applications and Mobile Money. Each of these panels comprised of speakers (CXO level) from a cross-section representation of the industry and included leading carriers, technology platforms, mobile value added services providers and the government. The conference saw a turn out of over 200 leading industry delegates.TRANSCRIPT

Evolution of Mobile VAS in India Evolution of Mobile VAS in India

Imperatives for Exponential Growth Imperatives for Exponential Growth

July 2011 | A joint report by IAMAI and Analysys Mason

Launch Presentation Launch Presentation

2

List of Sponsors

Platinum Sponsor

Gold Sponsors

3

Peer Review / Acknowledgements

• Peer Review Steering Committee

We would like to thank the peer review steering committee for dedicating their time to this initiative and helping to identify the key issues to focus on. Producing this report would not have been possible without their inputs and feedback

Parag Kar VP, Government Affairs, Qualcomm (India & South Asia)

PG Ponnapa Chief Executive Officer- India/Asia Pac, MPortal

Sanjay K Goyal Founder & CEO, ACL Wireless

Dr. Subho Ray President, IAMAI

Vijay Shekhar Sharma Chairman & MD, One97

• Acknowledgements

We would like to acknowledge the following people for their extraordinary contributions

Anand Virani Business Development Lead, Services Ecosystem, Qualcomm (India & South Asia)

Chirag Jain Vice President - Marketing & Business Development, Webaroo

Mohit Narain Business Director, ACL Wireless

Rakesh Mahajan Independent Consultant

4

Global experience suggests that India has an opportunity to be a leading

‘mobile first’ market for data

Global Experience

Source: Analysys Mason, © Wireless Intelligence 2011, Telegeography

0%

15%

30%

45%

60%

Q1

2005

Q2

2005

Q3

2005

Q4

2005

Q1

2006

Q2

2006

Q3

2006

Q4

2006

Q1

2007

Q2

2007

Q3

2007

Q4

2007

Q1

2008

Q2

2008

Q3

2008

Q4

2008

Q1

2009

Q2

2009

Q3

2009

Q4

2009

Q1

2010

China Unicom, China Vivo, Brazil Globe, Philippines

Smart, Philippines Maxis, Malaysia AIS, Thailand

Telkomsel, Indonesia MTN, South Africa Vodacom, South Africa

Share of Non-Voice Revenues1 by Carrier, Country (%)

Launch of 3G Services

Messaging Driven Market

• Messaging dominant markets with

high base of non-voice revenues

• Philippines

High Growth post 3G

• Markets that have witnessed an

average change3 of ~4% per year

since 3G

• Malaysia, Brazil

Moderate Growth post 3G

• Markets that have witnessed an

average change3 of ~2.5% per year

since 3G

• Large potential for long term growth

due to the lack of alternate access

mechanism

• S Africa, Indonesia, Thailand & China

1

2

3

S Africa: 8.2%, 8.7%

Malaysia: 21.8%, 64.1%

Brazil: ~16%, 45.0%

China: ~4.8%, 28.2%

Note: 1. Non-voice revenues includes revenue from messaging, data usage and other non voice related activities; 2. PC penetration figures are

for 2005 and Internet Penetration figures are as of 2006; 3. Average yearly change in share of non voice revenues (within total revenues);

4. China Unicom was considered rather than China Mobile, because the latter launched 3G with TD-SCDMA while the former did so

with W-CDMA / HSPA; 5. Smart launched 3G services in Q1’06; 6. Vodacom launched 3G services in Q4’04

4

6

5

Legend2: Country: PC Penetration, Internet Penetration

5

Source: Analysys Mason, FICCI Frames 2010, Company Reports

Structural enablers in the market also indicate that the MVAS industry is at

an inflexion point

Mobile VAS Overview

51%

65%

2009 2010

Share of GPRS Enabled Handsets

in Total Handset Sales

DEVICE

• The device landscape in India

has changed significantly with

the entry of local Indian

handset OEMs

• Data enabled devices (both

GPRS and 3G) now constitute

~70-80% of the installed

handset base

ACCESS

• Mobile data is now widely

accessible with carriers

launching 3G services

• Low sachet pricing and pay-

per-site are encouraging

penetration of data services

adoption

Data (2.5G) Plan Tariffs (INR)1

CONTENT

• Wider variety of VAS content

and services available to

Indian user today; carriers

have become significant

distribution partners

• App stores with inventories

into the millions across

multiple categories and

genres are being launched by

carriers, handset OEMs and

third party stores

DEMAND

• The complete ecosystem

across devices, access and

content is resulting in

growing demand from

consumers for mobile

internet services 30

75

CY2008 CY2010

Active Mobile Data (GPRS)

Users in India

450

90

2008 20101

Indian Music Industry Revenues

by Component (2010)

41%

49%

10%

Digital Music

Physical Music

Others

Note: 1. Estimated price for entry level plan with unlimited monthly data usage

6

However, key market and policy enablers in the on-deck, off-deck and SMS

markets will be imperative for growth

Second Order Impact

Affordability

Price points for VAS remains flat,

due to lack of competitive offerings

Ecosystem Evolution

Lack of innovative product and

service offerings, with VAS providers

focusing on mass market services

Investments for Scalability

Limited investment in this sector due

to perceived risk around carrier

control on revenue shares and billing

Consumer Welfare

Lack of consumer interest protection,

with no clarity on data charges and

pricing for SMS/calls to short codes

Mobile VAS: Challenges

Challenges for On-Deck VAS1

1. Carrier control

2. MIS reconciliation

3. Dispute redressal

Key Issues

• Perceived scalability and profitability

constraints for D2C models, due to

high % of billing share, and lack of

alternate billing models

• Companies focusing on basic mass

market offerings which can drive

volumes in alignment with carriers

• Market inefficiencies resulting in

perceived scalability constraints for

VAS providers

• Focus of platform providers shifting to

international markets to drive higher

revenue from their offerings

First Order Impact

Challenges for Off-Deck VAS2

1. Lack of alternate payment channels

2. No control over end user pricing

3. Skewed revenue shares when

using carrier billing

Source: Analysys Mason, Industry Inputs

• Addressable base of SMS limited,

with only 47% penetration

• Mobile marketing / advertising on

SMS also constrained

Challenges for SMS adoption

1. Limited understanding of English /

Roman characters

Note: 1. On-Deck VAS: Value added services which are available through the carrier; 2. Off-Deck VAS: Value added services which are available through D2C models

7

Global experience suggests that a policy framework without licensing and

market determined revenue shares is the right way forward

1. Policy Framework without

Licensing

2. Licensing with Market Determined

Revenue Share

3. Licensing with Policy

Determined Revenue Share

• No separate VAS license needs to

be issued – but a policy framework

to support VAS providers is required

• A broader licensing framework, which

leaves revenue shares to be driven by

market forces

• A focused licensing regime needs to

be in place for VAS, including

regulation recommending minimum

revenue shares

• Revenue shares should be left to

market forces, as that will help drive

innovation

• Creating licenses will increase the

costs of the MVASPs and innovation

will suffer as smaller VAS providers

will not be able to bear the attendant

costs of a license

• Licensing will ensure that the VAS

industry gets support on critical issues

such as MIS reconciliation and dispute

redressal

• Revenue share is a commercial

agreement between entities and cannot

be mandated by the Government

• Once off-deck services gain traction,

market forces will drive revenue shares

without intervention

• Revenue shares remain a critical

element in the mobile VAS ecosystem

and are currently hampering growth

and investment in the industry because

of their low levels

• Once revenue shares are regulated,

other operational issues such as MIS

would also get addressed

• Formation of a self governed

industry forum to formally represent

the VASPs

• Formation of a premium number

policy which will govern the

operation of short codes

• A VAS licensing framework that will

regulate MIS, dispute redressal and

other issues, but will leave revenue

shares to market participants

• A VAS license framework that will

regulate revenue shares, and

recommend measures for

implementation and monitoring

Source: Analysys Mason, Industry Inputs

Mobile VAS: Recommended Solutions

Ration

ale

P

ote

ntia

l S

olu

tion

P

ositio

n

8

For on-deck, an industry self-governing board that can act as a formal

forum for participants in the MVAS ecosystem can be beneficial

On-Deck VAS

Source: Analysys Mason

Mobile VAS: On-Deck VAS Providers (Recommended Solutions)

MVAS Industry

Governing Board

IAMAI COAI / AUSPI

MVAS Services

Providers

Technology

Platform Providers Carriers

Formation of an MVAS Authority

Members From Stakeholders Across

the Value Chain

Formation of an Industry Association for Mobile VAS Providers in India

1. Self governing VAS forum

2. Board can draft guidelines for MIS

reconciliation between mobile VAS

providers and carriers

3. Act as a forum for grievance redressal

and issue directives for action

4. The functioning / structure of the board

can be modeled after the ASCI1

Handset

Manufacturers

Note: 1. ASCI stands for Advertising Standards Council of India

9

However, billing remains a major issue in addition to carrier control over

end user pricing of off-deck services

Source: Analysys Mason, Wireless Intelligence, Industry Inputs

10

3

10

15

10

30

3 3

10

15

10

30

0

10

20

30

Voice PremiumSMS

Mono Tone Poly Tone WallpaperDownload

CRBTSubscription

2007 2010

End user Price for Voice and Non-Voice

Offerings in India (2007 & 2010)1

Note: 1. For a 10 minute call; 2007 rate assumed at INR 1 per minute, 2009 rate at INR 0.5 paisa per second, Cost of per transaction for SMS,

monotone, polytone and wallpaper, monthly subscription for CRBT; 2. India (Paid game on Indiatimes), USA, UK, China (Paid game

on Apple Apps Store), Malaysia (GamesUnlimited; Maxis games site); Most games in China are cracked and available for free.

Number in parenthesis indicates the cost of game as a % of ARPU

161.6

2171.7

1507.5

444.6

722.3

54.0 44.6 42.8 44.6 119.7

0

500

1000

1500

2000

2500

India USA UK China Malaysia

ARPU Game Price

(33%)

(2%)

(3%)

(10%)

(17%)

INR INR

(10 mins call)1

Off-Deck VAS

Mobile VAS: Off-Deck Providers (Challenges)

ARPU vs. Price of Popular Game in Different Countries (INR)2

10

A policy framework (without licensing) that will mandate a premium

number policy can potentially address the challenges for off-deck billing

Mobile VAS: Off-Deck Providers (Recommended Solutions)

Source: Analysys Mason

Proposed Framework for Premium Number Policy

Central Short Code (CSC) Agency

Created & Mandated by TRAI

Carrier

1

Carrier

n

Carrier

2 ….

VAS Provider

• Short codes

allocated and

maintained by

this central

agency

• Pan India access

across all

carriers

• Mandated

turnaround time

of activation

across carriers

• VAS Provider Offers

Services to Users

Across Carriers

User Billed

by carrier

for service

Short Code Operational

Across Carriers

Host carrier pays

VASP; Keeps share

to cover

interconnection and

other costs

Revenue Flow Service Flow

• CSC agency to be set up as a

licensed entity under TRAI

• Licensing of CSC agency allows it to

enter into agreements with other

licensed entities

• TRAI to mandate a ‘Rate Card’ under

IUC regulations, which includes billing,

origination and termination charges for

carriers whose customer originates

service access request

• This policy will guarantee pan India

access across all carriers

Off-Deck VAS

11

Mandating the incorporation of a standards based local language solution

on all handsets can help drive SMS penetration

Mobile VAS: SMS (Challenges and Recommendation)

Source: Analysys Mason, Centre of Excellence in Wireless Technology (CEWiT) India Reports

Enablers: Local Language Support on Handsets

• Mandate standardization of character set of local

language fonts

Partnering with an organization like CEWiT and others

to get key standards in place for:

– Indic 7-bit encoding (improves text payload in a SMS)

– Simplified Indic keypad design (to make user adoption

easy)

– Memory efficient font libraries (critical for distribution

and field support)

• Mandate incorporation of local language

standards on all handsets sold in India

Partnering with top handset vendors to motivate

adoption of new standards by mid-2012 and launch of

an industry-wide education campaign

SMS Penetration

SMS Penetration, 2010

100%

80%

47%

0%

25%

50%

75%

100%

Philippines China India

• Apart from lower SMS pricing in Philippines and China than

in India, the ability to message in local language is the key

driver for high SMS penetration

• Different handset OEMs use their own proprietary standards

for Indian language text, creating interoperability issues

12

In the future, emerging areas of m-commerce & advertising, and changes

in the VAS value chain will modify the way services are consumed

Content Aggregators

Carriers

Technology Platform Enablers

Product/ Apps

Retail

Advertising/Profiling/Relevance Platform

Mobile Commerce Platform

Content Repurposing / ISV4

Online

Handset OEM

3rd Party VASP WAP SMS

Content Developer

UGC Device Integration

Carrier

Cash/ CC/ DC

MPG2 / Ad3 Voice

• Backward integration across the three segments e.g. TPE moving into content aggregation

• UGC gaining adoption

• Easy integration of VAS products on to the carrier SDP / network

• With initiatives like START/STOP, focus is on enabling users to experiment with multiple products

• Carriers offering ad-based services for secondary revenue streams

• Partnering with payment companies for additional revenue from mobile shopping and remittance

• M-commerce solution provider with one or more capabilities such as mobile payment, mobile banking, money transfer and mobile shopping

• Carriers deploying profiling / relevance platform for better targeting

• Ad-networks forming dedicated sales force to sell branded inventory

Managed Services / Network OEM /VAS SI

• Network OEMs are providing technology platform for carriers, e.g. Network OEM CRBT platform integration in carrier network

Carrier Billing

MPG2

Ad3

• Handset OEM is offering VAS under its brand on multiple sales channel: online, retail and mobile

• D2C players using alternate payment channels

Voice

SMS1

Online

WAP

Source: Analysys Mason, Industry Inputs

Note: 1. STK embedded content is included in SMS; 2. Mobile Payment Gateway; 3. Ad based revenues; 4. Independent Software Vendor

Mobile VAS Trends

13

Based on these structural changes and market trends, we have identified

nine themes which will have a significant role in shaping MVAS in India

Themes Introduction

Source: Analysys Mason

Category Current Situation Key Trends

Category Themes

1

Consumer

VAS

• Commerce • Current scalable models use prepaid cards, and not

mobile; pilots by carriers, banks, D2C • UID accepted as KYC will increase share of G2C; carriers

pushing financial inclusion also a key driver (banking,

domestic remittances)

2 • Entertainment

Services • Services around music and gaming has seen early

adoption among mid ARPU segment • New products such as streaming music, full song download

and mobile games

3 • Utility Services • Multiple pilots, with few scalable models (e.g. RML,

IKSL), Location based services • Utility apps and affordable feature-phones to drive adoption

of productivity and livelihood enhancement services

4 • Community Services • Carrier promoted SNCs (e.g. AirtelFrenz)

aggregating audience on an ad monetization model • Emergence of new monetization models based on micro

transactions, content sales (e.g. Rocketalk) with carrier

marketing support, and increased off-deck usage

5 • Mobile Video • Limited services on EDGE with very poor user

experience • Launch of 3G services by 2011 by all major carriers, with a

strong video services portfolio (e.g. mobile TV, video calling)

6 • Device Apps and App

Stores • Carrier app stores dominate; D2C app stores facing

issues of billing as credit card penetration is low • Emergence of affordable android based phones, app store

push by handset OEMs, launch of 3G, utility apps (e.g.

railway booking)

7 Network

VAS • Network Services

• Among all the network services such as CRBT, CMS,

Roaming, Recharging, Location Enablement, CRBT

contributes significant share to total MVAS market

• CRBT has reached a mature level of adoption, while few

network services such as voice mail is limited by cultural and

price points

8

Enterprise

VAS

• Mobile Ad / Marketing • SMS / display ads used for lead generation and

digital content sale; poor user experience • 3G and better device form factors expected to enhance

effectiveness of display advertising and help ecosystem

growth

9 • Enterprise Solutions • Enterprise messaging solutions (e.g. Valuefirst) ,

Sales force management • Emergence of enterprise mobility providers with vertical

specific, carrier / software agnostic middleware solutions

(e.g. Mobien)

14

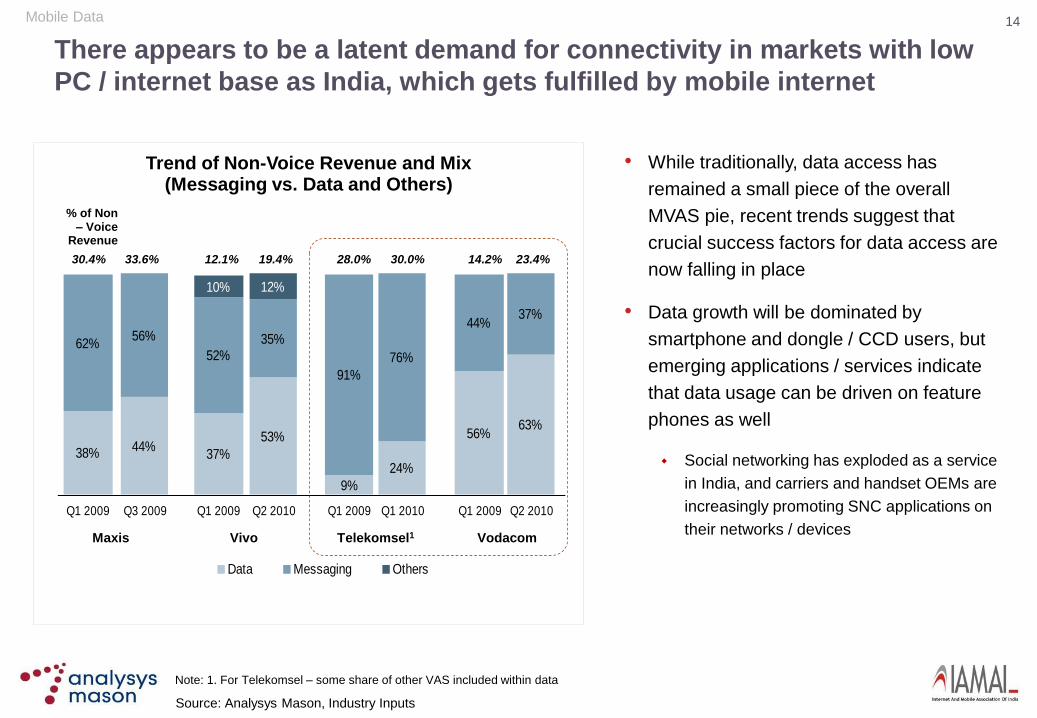

There appears to be a latent demand for connectivity in markets with low

PC / internet base as India, which gets fulfilled by mobile internet

• While traditionally, data access has

remained a small piece of the overall

MVAS pie, recent trends suggest that

crucial success factors for data access are

now falling in place

• Data growth will be dominated by

smartphone and dongle / CCD users, but

emerging applications / services indicate

that data usage can be driven on feature

phones as well

Social networking has exploded as a service

in India, and carriers and handset OEMs are

increasingly promoting SNC applications on

their networks / devices

Mobile Data

Note: 1. For Telekomsel – some share of other VAS included within data

38% 37%

9%

56%

62%52%

91%

44%

10%

Q1 2009 Q1 2009 Q1 2009 Q1 2009

Data Messaging Others

44%53%

24%

63%

56% 35%

76%

37%

12%

Q3 2009 Q2 2010 Q1 2010 Q2 2010

30.4% 33.6% 28.0% 30.0% 14.2% 23.4% 12.1% 19.4%

% of Non – Voice

Revenue

Maxis Vivo Telekomsel1 Vodacom

Source: Analysys Mason, Industry Inputs

Trend of Non-Voice Revenue and Mix (Messaging vs. Data and Others)

15

It appears that a scalable model for app stores in India would be carrier

app stores in partnership with OEM / OS companies

Source: Analysys Mason, Industry Inputs

Carrier App Store

Ap

p S

tore

OEM / OS App Store

Third Party App Store

Developer

Community

User

Experience /

Relevance

Monetization /

Billing

Carrier OEM / OS Third Party

Current Mapping of App stores and CSF1

Critical S

ucce

ss F

acto

rs

App Stores

• Revenue share is less

• No developer forum, except Airtel

• Better profiling of its subscriber

• Poor user interface

High Medium Low Favourability of CSF1:

• High rev share • Provides

continuous support to developers

• Provides high revenue share to developers

• Profiling based on handset model

• Better user interface

• Better user interface

• Seamless billing

• Ability to implement subscription model

• Unable to implement single click checkout and subscription plan

• Unable to implement single click checkout and subscription plan

Note: 1. CSF stands for Critical Success Factors

App Store

• Carriers have a strong hold in

the value chain of mobile

applications. They provide

seamless billing and multiple

business model

• OEM / OS with their better

relationship with developers

provide rich portfolio of mobile

applications

• Third party app stores such as

by Getjar have the lowest share

today of overall revenues in the

apps market in India

Three Kinds of App Store

16

Emerging services within mobile VAS also include social networking,

instant messaging and microblogging

Classification of Mobile Community Services based on Primary Service

Business Models for Mobile Community Services

Source: Analysys Mason, Industry Inputs

Primary

Service Description Key Service Providers

Social

Networking

Community

• Includes sharing of

multimedia content

along with posting

status messages to

a group of friends

Instant

Messaging

• Includes real time

P2P communication

over mobile internet

Micro-

blogging

• Includes sharing of

status messages

only

Mobile Community Services

Mobile Extension of Online Community Services

• These communities are feature rich platforms that

allows a wide range of activities including sharing of

text, photos and videos in addition to playing games

• Broadband connection and a wide screen is required

for taking advantage of the features available

• Mobile version, usually an application, is a strip down

version in terms of features and allowed activities

Custom Built for Mobile (Mobile Only Services)

• These communities have mobile as the primary

access channel and the platforms are highly

optimized for mobile usage

• Features offered through these communities are

customized to work on slow 2G data channel, as well

as other bearer channels

• The primary target users are ‘mobile first’ data users

17

Livelihood enhancement services, especially in rural areas, will play a key

role in the development of this sector

Source: Analysys Mason, Industry Inputs

Utility Services

Case

Study Description User base Pricing

RML

Information

Alert

Services

• Provides

agricultural and

commodity pricing

information service

via SMS

~ 0.3 mn farmers

have subscribed to

RML (Q1 2010)

So far, the service

has reached more

than 1 mn farmers

across 15K villages

(Nov 2010)

• Price: INR 175

(USD 3.8) for 3

months; INR 75

(USD ) per

month by Idea

Cellular

Behtar

Zindagi

Mobile

health

• Voice based rural

information services

on livestock, mandi

prices, fishery

advisory and others

Launched in March

2011

• Subscription

fee: INR 2 for 1

day and INR 30

for 30 days and

INR 1 per

minute

LifeLines –

Education

Mobile

Education

• Connects teachers

in rural areas with

education experts

whom they can

consult on

educational queries

via IVR

More than 25,000

academic query-

answer sets have

been facilitated

under this service in

2010

• Transaction

charge of INR 5

(USD 0.1) per

call

Eko

Financial

Inclusion

• Provides financial

services to the un-

banked population

in urban as well as

rural areas

Over 180,000 customers across Delhi-NCR and

Bihar-Jharkhand till October 2010

• Free

Access to Information

Uti

lity

Se

rvic

es

Access to Opportunity

Access to Infrastructure

• Alerts related to crop price,

weather updates

• Stocks and news alerts

• Location based services and

maps

• Push email

• Mobile education, tutorials for

English in multiple language

• Job listings on mobile

• Health support on mobile,

including regular health tips

• Mobile governance services

such as tracking passport

application, details of utility

payments

• Financial inclusions via mobile

and mobile ticketing

Use Case of Utility Services

18

Source: Analysys Mason, FICCI Frames 2010, Company Reports

M-Commerce will be another critical growth driver with carriers and D2C

providers experimenting with multiple models

Mobile Commerce

Payments

• Under the current regulations, there are two models for payment

using mobile: linked payment instruments and stored wallets

model

• The linked payment model has witnessed some traction for utility

bill payments and some small value shopping

• The stored wallets model is relatively new, and has the potential

to gain traction for small ticket items and eventually as an

alternative to credit cards for digital payment

• However, regulations do not allow cash out, which can potentially

slow adoption as users are reluctant to lock in cash

Banking

• Mobile banking reduces the transaction cost for banks and

provides a convenient channel for account holders

• Mobile will add relatively higher value for serving the needs of the

un-banked segment for banking and remittance

• BC based banking is expected to be popular amongst the un-

banked segment

• However, given low deposits this does not translate into a

significant market opportunity

MGNREGA Project FY-09 FY-101

Districts covered 615 619

Total Issued Job

Cards (mn) 100 109

Number of

households

benefited (mn)

45 43

Budget outlay

(USD bn) 6.5 8.5

G2C Payouts

• BC accounts opened with UIDs

will enable the unbanked

population to receive benefits

from government

• Government gives a lot of cash

benefits like old age pension,

disability pension, widows

pension and MGNREGA

payment

• Under the current regulations,

mobile enablement is possible

only for domestic remittance

• BC based remittance will form

the dominant portion, driven

by urban to rural channels.

Users will shift to mobile

remittance for convenience

and cost

Inter-state Remittance (2009)

Domestic Remittance Size

(Migrants) ~USD 12 bn

Via Post Office ~USD 1.8 bn1

Via ‘Friends & Family’ ~USD 10.2 bn

Informal (non-migrant) ~USD 13 bn

Average Annual Transaction

Value per Worker ~USD 150

Domestic Remittance

19

Mobile VAS Market Potential (INR bn) & Its Share of Telecom Revenue

Source: Analysys Mason, Industry Inputs

With the above market and policy initiatives, MVAS revenues is expected

to account for as much as 51% of incremental industry revenues in 2015

Forecasts: MVAS Industry

Note: 1. Others include m-commerce and CMS

• Indian MVAS industry will reach contribution

levels seen in other emerging markets such as

Malaysia and China

• Data access will be the biggest revenue driver

based on handset based access and CCD /

dongles

• CRBT will decline in revenue contribution due to

poor per unit economics for carriers and end

user affordability

• SMS penetration is expected to stabilize at the

current levels due to consumer behaviour and

literacy issues unless local language can be

introduced

25 49 88

150 201 215

48 58

62

81

123 148

13 16

19

23

28 34

96

132

159

182

202

219

28

32

34

34

35

37

2

4

6

9

14

19

213

291

368

480

603

671

16% 18%

22%

27%

31% 31%

2010 2011 2012 2013 2014 2015

Mobile Internet (Handset) Dongles / CCD Data Access

IVR Messaging

CRBT Others1

Share of MVAS

20

Data Users (mn)

Source: Analysys Mason, Industry Inputs

This growth is driven primarily by a forecasted 534 mn data users in 2015

across 2.5G, 3G and 4G, contributing 54% of total mobile VAS revenue

76 125

183

275

372

468

7

12

18

28

48

66

83

137

201

303

420

534

2010 2011 2012 2013 2014 2015

Handset Data Users Dongles & CCDs

Forecasts: MVAS Industry – Data Users

• Of an estimated active base of 1.1 bn

subscribers in 2015, 154 mn subscribers are

expected to access data on 2.5G and 314 mn

subscribers on 3G

• Adoption of mobile handset data will continue to

grow, with reduction in price per MB for HSPA

data, increasing penetration of feature-phones

and smartphones, as well as availability of

content and applications

• User base of 22 mn is expected on 3G handsets

in 2011, contributing a data ARPU of INR 133 in

2011 going down to INR 49 in 2015, with access

accounting for a major share of the revenues

• EVDO dongles are expected to dominate the

mobile broadband access market from PCs, as

they provide relatively better capacity and cost

per MB than HSPA

• 4G / LTE dongle and CCD base is expected to

reach 21 mn by 2015

21

www.iamai.in www.amalysysmason.com

To access the report, please visit:

www.iamai.in

www.analysysmason.com/india

www.slideshare.net/analysysmason