iais global insurance capital standards update - soa · session 169 pd - iais global insurance...

TRANSCRIPT

Session 169 PD - IAIS Global Insurance Capital Standards Update

Moderator: David Sherwood

Presenters: Elizabeth K. Dietrich, FSA, CERA, MAAA

David Sherwood

SOA Antitrust Compliance Guidelines SOA Presentation Disclaimer

IAIS Global Insurance Capital Standards UpdateSOA Annual Meeting, Session 169October 18, 2017Boston, MA

Liz Dietrich, FSA, CERA, MAAAVice President & ActuaryRetirement Valuation & ReportingPrudential Financial, Inc.

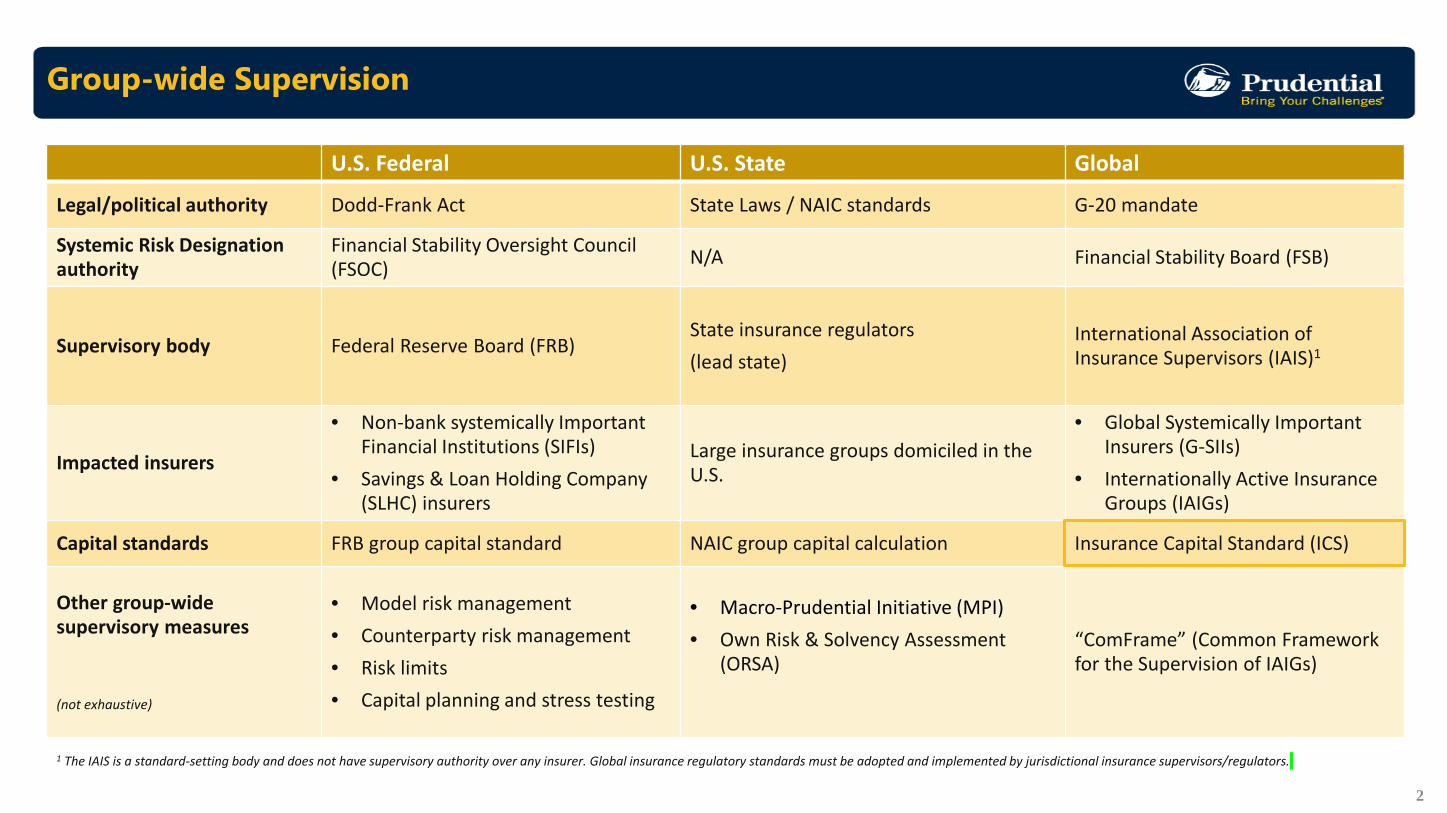

Group-wide Supervision

2

U.S. Federal U.S. State Global

Legal/political authority Dodd-Frank Act State Laws / NAIC standards G-20 mandate

Systemic Risk Designation authority

Financial Stability Oversight Council (FSOC) N/A Financial Stability Board (FSB)

Supervisory body Federal Reserve Board (FRB)State insurance regulators(lead state)

International Association of Insurance Supervisors (IAIS)1

Impacted insurers

• Non-bank systemically Important Financial Institutions (SIFIs)

• Savings & Loan Holding Company (SLHC) insurers

Large insurance groups domiciled in the U.S.

• Global Systemically Important Insurers (G-SIIs)

• Internationally Active Insurance Groups (IAIGs)

Capital standards FRB group capital standard NAIC group capital calculation Insurance Capital Standard (ICS)

Other group-wide supervisory measures

(not exhaustive)

• Model risk management• Counterparty risk management• Risk limits • Capital planning and stress testing

• Macro-Prudential Initiative (MPI)• Own Risk & Solvency Assessment

(ORSA)“ComFrame” (Common Framework for the Supervision of IAIGs)

1 The IAIS is a standard-setting body and does not have supervisory authority over any insurer. Global insurance regulatory standards must be adopted and implemented by jurisdictional insurance supervisors/regulators.

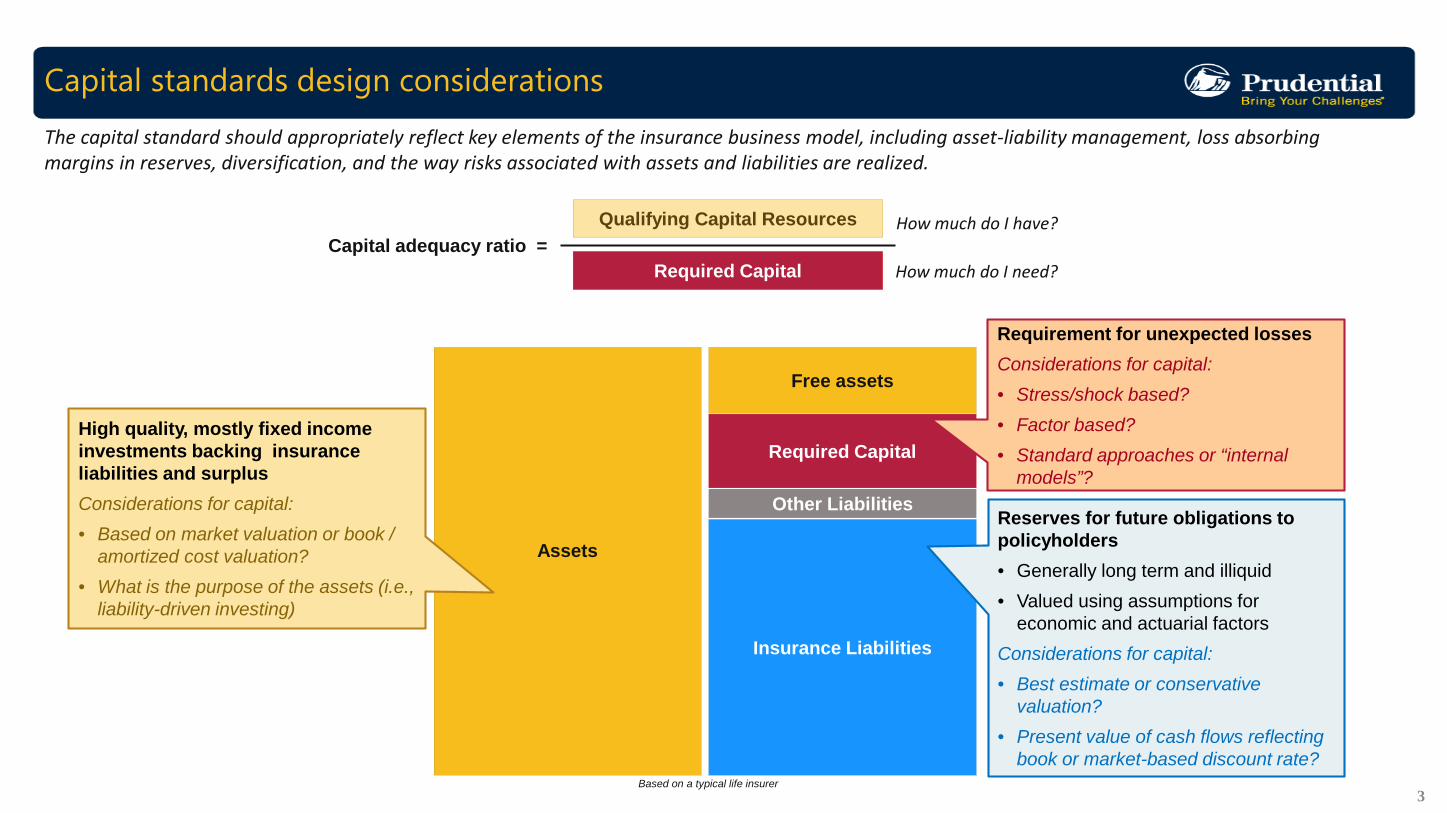

Capital standards design considerations

Assets

Insurance Liabilities

Other Liabilities

Required Capital

Free assets

Reserves for future obligations to policyholders• Generally long term and illiquid• Valued using assumptions for

economic and actuarial factorsConsiderations for capital:• Best estimate or conservative

valuation?• Present value of cash flows reflecting

book or market-based discount rate?

Requirement for unexpected lossesConsiderations for capital:• Stress/shock based?• Factor based?• Standard approaches or “internal

models”?

High quality, mostly fixed income investments backing insurance liabilities and surplusConsiderations for capital:• Based on market valuation or book /

amortized cost valuation?• What is the purpose of the assets (i.e.,

liability-driven investing)

Qualifying Capital Resources

Required CapitalCapital adequacy ratio =

3

The capital standard should appropriately reflect key elements of the insurance business model, including asset-liability management, loss absorbing margins in reserves, diversification, and the way risks associated with assets and liabilities are realized.

How much do I have?

How much do I need?

Based on a typical life insurer

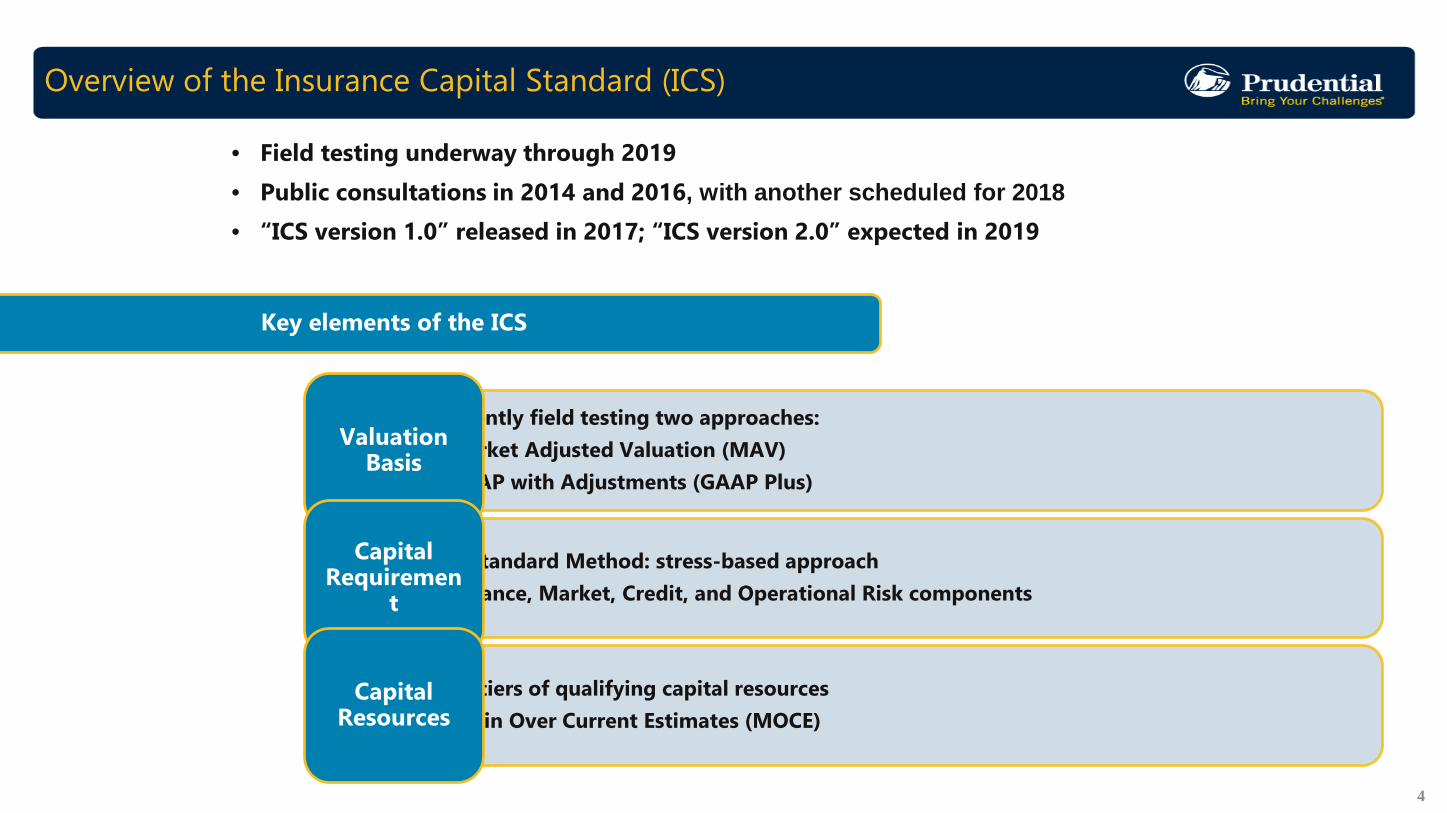

Overview of the Insurance Capital Standard (ICS)

•Currently field testing two approaches:•Market Adjusted Valuation (MAV)•GAAP with Adjustments (GAAP Plus)

•ICS Standard Method: stress-based approach•Insurance, Market, Credit, and Operational Risk components

•Two tiers of qualifying capital resources•Margin Over Current Estimates (MOCE)

Key elements of the ICS

Valuation Basis

Capital Requiremen

t

Capital Resources

4

• Field testing underway through 2019• Public consultations in 2014 and 2016, with another scheduled for 2018• “ICS version 1.0” released in 2017; “ICS version 2.0” expected in 2019

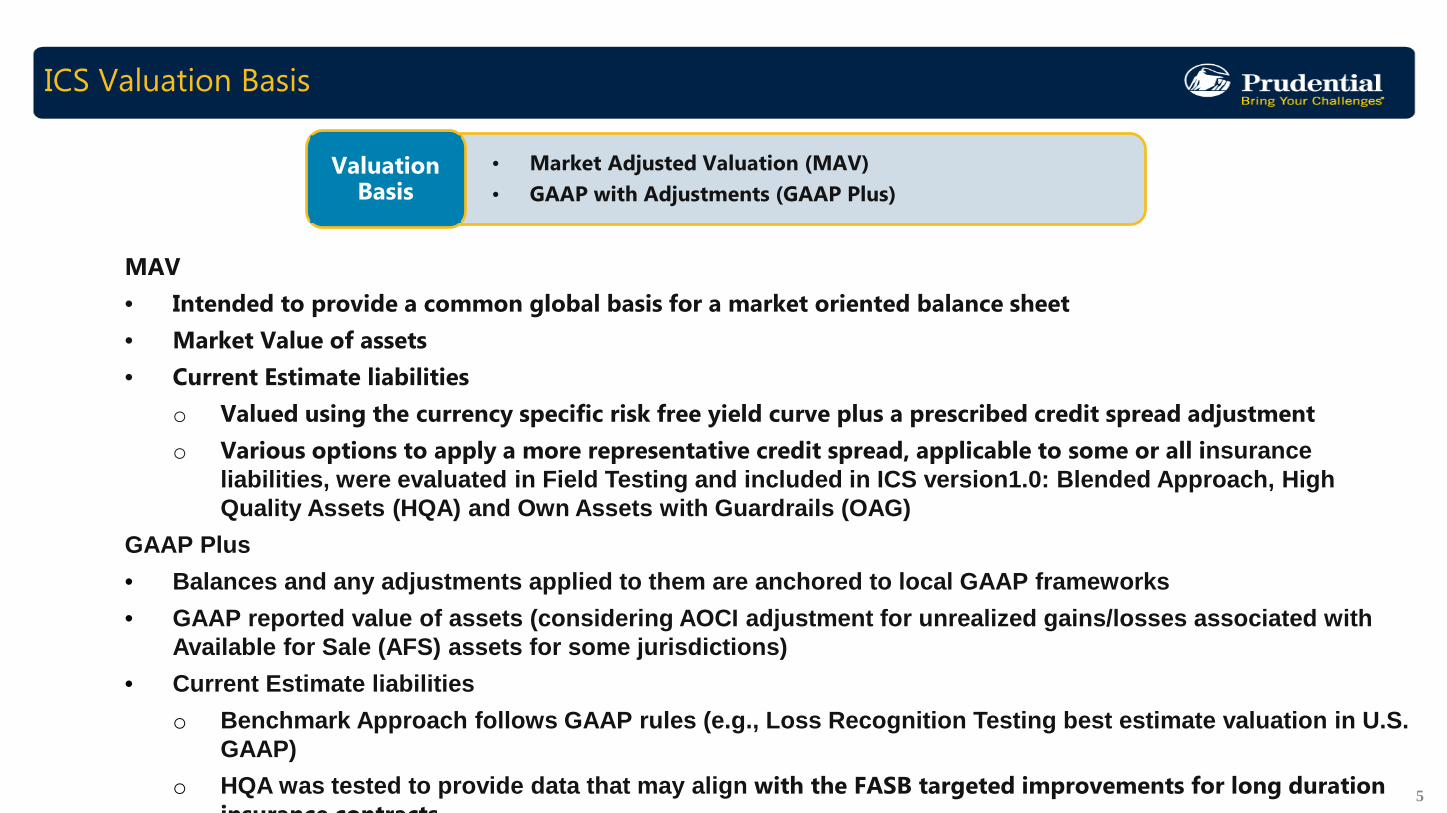

ICS Valuation Basis

MAV• Intended to provide a common global basis for a market oriented balance sheet• Market Value of assets• Current Estimate liabilities

o Valued using the currency specific risk free yield curve plus a prescribed credit spread adjustmento Various options to apply a more representative credit spread, applicable to some or all insurance

liabilities, were evaluated in Field Testing and included in ICS version1.0: Blended Approach, High Quality Assets (HQA) and Own Assets with Guardrails (OAG)

GAAP Plus• Balances and any adjustments applied to them are anchored to local GAAP frameworks • GAAP reported value of assets (considering AOCI adjustment for unrealized gains/losses associated with

Available for Sale (AFS) assets for some jurisdictions)• Current Estimate liabilities

o Benchmark Approach follows GAAP rules (e.g., Loss Recognition Testing best estimate valuation in U.S. GAAP)

o HQA was tested to provide data that may align with the FASB targeted improvements for long duration insurance contracts

• Market Adjusted Valuation (MAV)• GAAP with Adjustments (GAAP Plus)

Valuation Basis

5

ICS Capital Requirement

Stresses for Insurance, Market, Credit, and Operational risksCapital

Requirement

6

Insurance Market Risk Credit Risk Operational Risk

• Mortality (base rates)

• Longevity (base rates)

• Morbidity and disability (incidence and recovery rates)

• Lapse (level and trend, mass lapse)

• Expense (level and expense inflation)

• Catastrophe (terrorism, pandemic)

• Interest Rate (up, down, flattening, steepening, mean reversion)

• Equity (equity returns and volatility)

• Real Estate

• Currency

• Asset concentration

• Stresses to credit assets, evaluated with and without consideration of NAIC ratings • Factor-based

Correlation matrices applied in aggregation (intra- and cross-risk)

ICS Capital Resources

Tier 1 and Tier 2 considerations• Loss absorbing capacity• Level of subordination• Permanence• Availability • Absence of both encumbrances and mandatory servicing costsItems for consultation include:• Structural vs. contractual subordination• Capital composition limits• Treatment of AOCI• Treatment of DTAs and other deductions from Tier 1 capitalMOCE • 2 options currently being tested: Cost of Capital MOCE and Prudence MOCE

• Tier 1 and Tier 2 qualifying capital resources• Margin Over Current Estimates (MOCE) treatment

Capital Resources

7

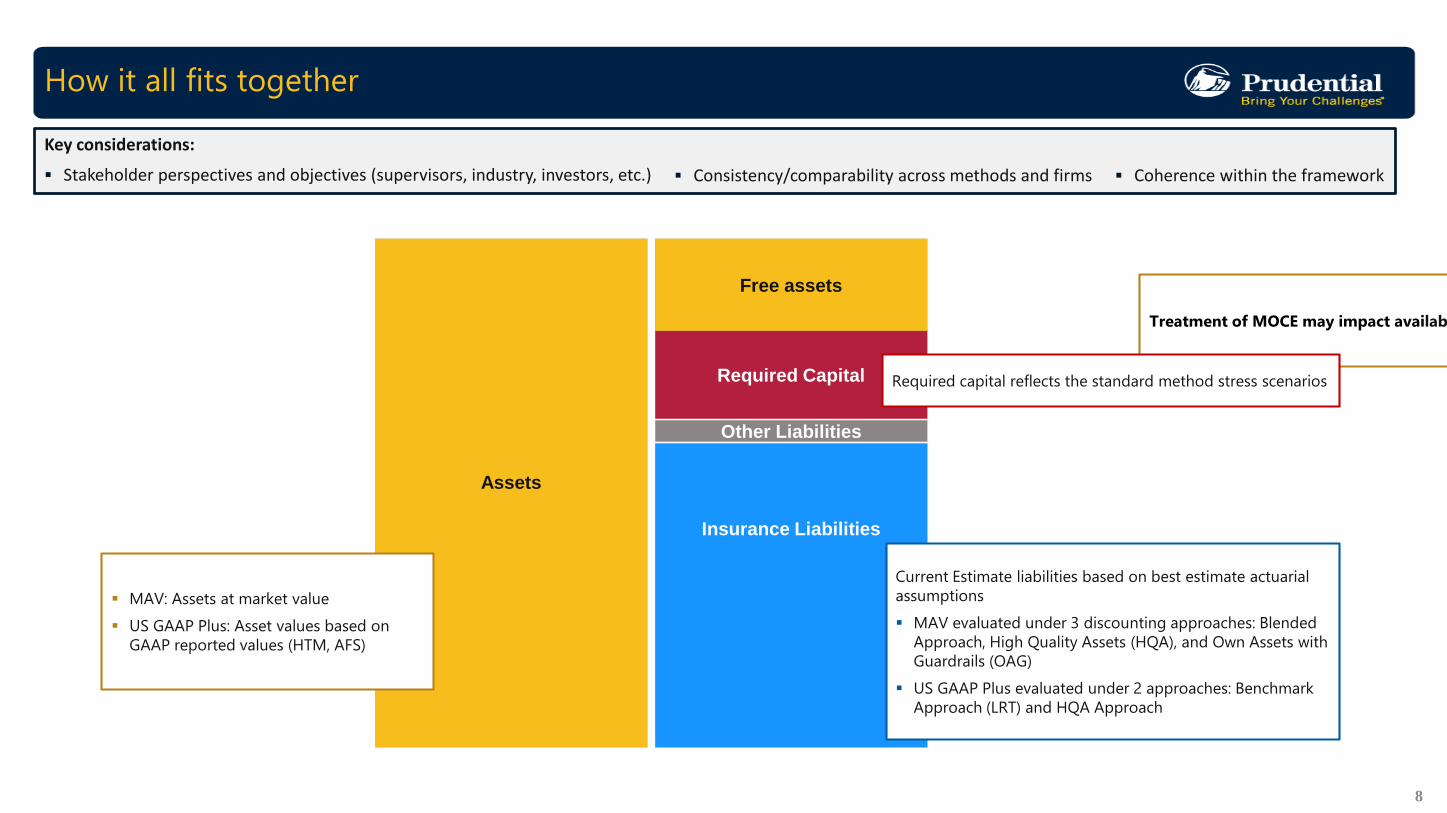

How it all fits together

8

Assets

Insurance Liabilities

Other Liabilities

Required Capital

Free assets

MAV: Assets at market value US GAAP Plus: Asset values based on

GAAP reported values (HTM, AFS)

Current Estimate liabilities based on best estimate actuarial assumptions MAV evaluated under 3 discounting approaches: Blended

Approach, High Quality Assets (HQA), and Own Assets with Guardrails (OAG)

US GAAP Plus evaluated under 2 approaches: Benchmark Approach (LRT) and HQA Approach

Treatment of MOCE may impact availab

Required capital reflects the standard method stress scenarios

Key considerations:

Stakeholder perspectives and objectives (supervisors, industry, investors, etc.) Consistency/comparability across methods and firms Coherence within the framework

1) Volatility – asymmetric treatment of assets and liabilities in the valuation basis creates artificial volatility and pro-cyclicality

2) Excessive conservatism – improper design and calibration understates Available Capital and overstates Required Capital

The above issues are especially impactful for long term protection and retirement products.

MAV

The IAIS is considering discounting options to address asymmetry between the valuation of assets and liabilities

MV of Assets Current Estimate Liabilities based on prescribed discount curve

GA

The IAIS is asymmetry

GAAP Value of Assets (mostly MV)

Current Estimate Liabilities based on GAAP LRT rules (asset earned rate)

Required CapitalIntended as a 1-in-200 level of stress over one year (99.5% one-year VaR)

Improper design & overly punitive calibration overstates Required Capital

Available CapitalCapital resources should include all tangible loss absorbing resources (including margins in reserves)

MOCE do

Observed concerns with the ICS

9

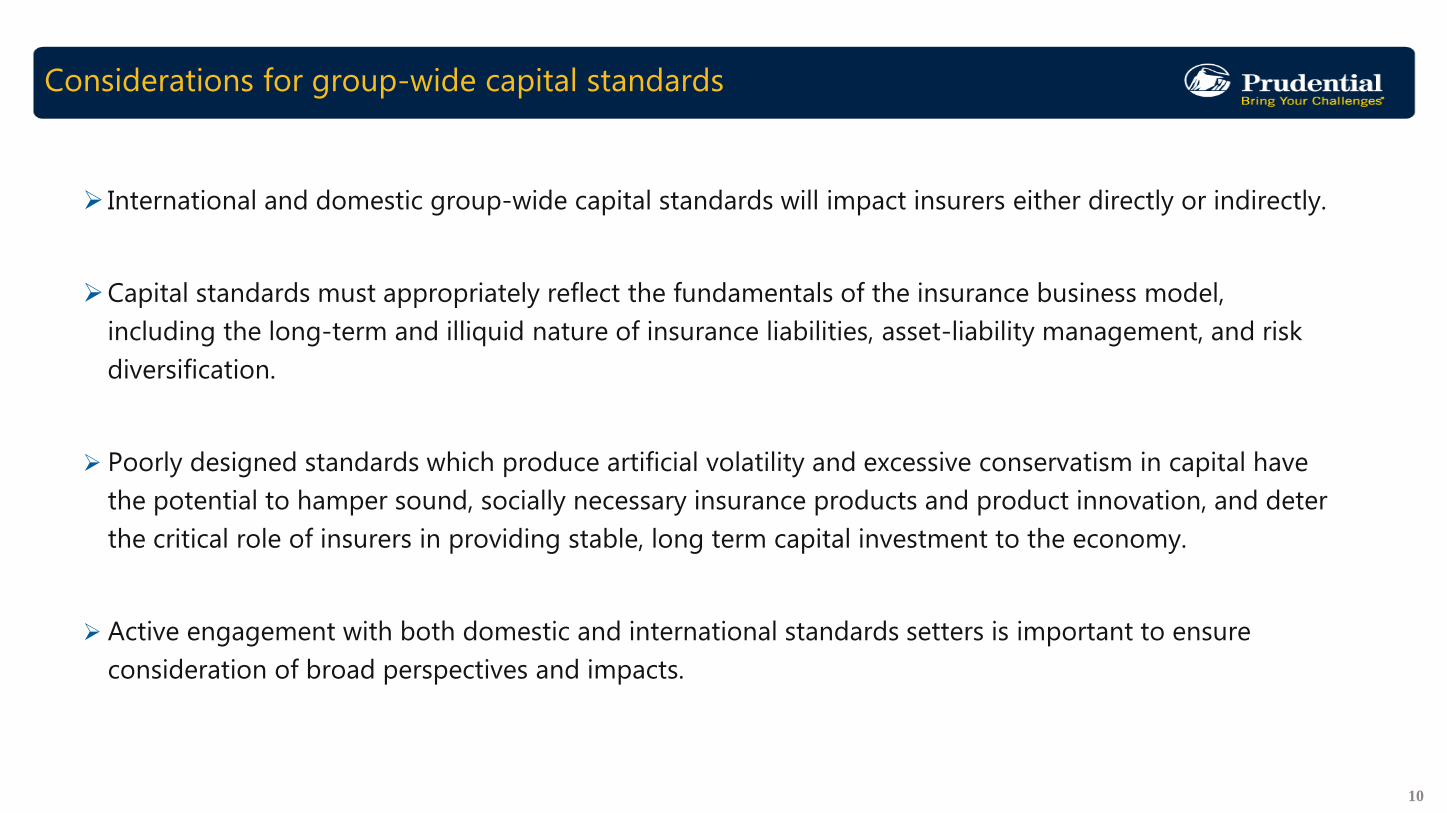

Considerations for group-wide capital standards

International and domestic group-wide capital standards will impact insurers either directly or indirectly.

Capital standards must appropriately reflect the fundamentals of the insurance business model, including the long-term and illiquid nature of insurance liabilities, asset-liability management, and risk diversification.

Poorly designed standards which produce artificial volatility and excessive conservatism in capital have the potential to hamper sound, socially necessary insurance products and product innovation, and deter the critical role of insurers in providing stable, long term capital investment to the economy.

Active engagement with both domestic and international standards setters is important to ensure consideration of broad perspectives and impacts.

10

2017 SOA Annual Meeting & ExhibitSession 169 PD - IAIS Global Insurance Capital Standards UpdateOctober 18, 2017

DAVID SHERWOOD

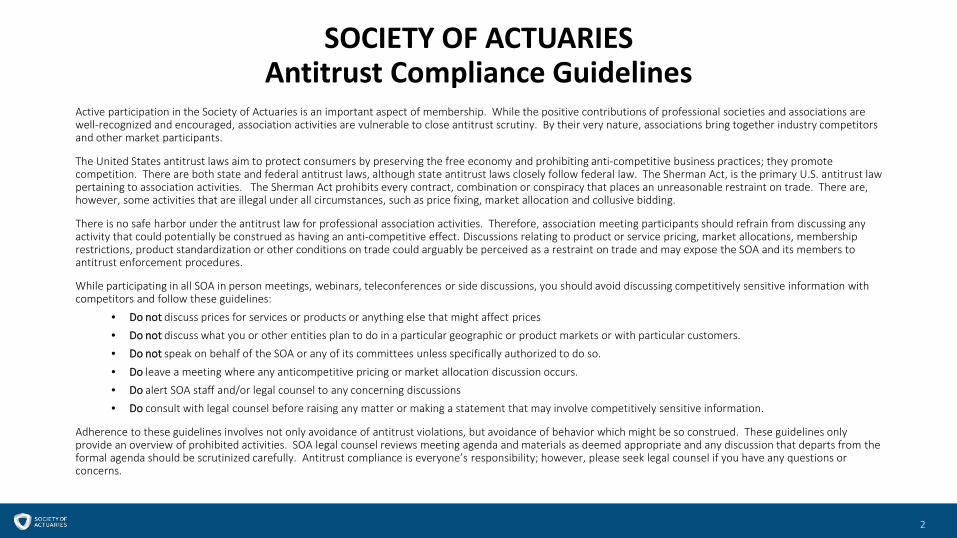

SOCIETY OF ACTUARIESAntitrust Compliance Guidelines

Active participation in the Society of Actuaries is an important aspect of membership. While the positive contributions of professional societies and associations are well-recognized and encouraged, association activities are vulnerable to close antitrust scrutiny. By their very nature, associations bring together industry competitors and other market participants.

The United States antitrust laws aim to protect consumers by preserving the free economy and prohibiting anti-competitive business practices; they promote competition. There are both state and federal antitrust laws, although state antitrust laws closely follow federal law. The Sherman Act, is the primary U.S. antitrust law pertaining to association activities. The Sherman Act prohibits every contract, combination or conspiracy that places an unreasonable restraint on trade. There are, however, some activities that are illegal under all circumstances, such as price fixing, market allocation and collusive bidding.

There is no safe harbor under the antitrust law for professional association activities. Therefore, association meeting participants should refrain from discussing any activity that could potentially be construed as having an anti-competitive effect. Discussions relating to product or service pricing, market allocations, membership restrictions, product standardization or other conditions on trade could arguably be perceived as a restraint on trade and may expose the SOA and its members to antitrust enforcement procedures.

While participating in all SOA in person meetings, webinars, teleconferences or side discussions, you should avoid discussing competitively sensitive information with competitors and follow these guidelines:

• Do not discuss prices for services or products or anything else that might affect prices• Do not discuss what you or other entities plan to do in a particular geographic or product markets or with particular customers.• Do not speak on behalf of the SOA or any of its committees unless specifically authorized to do so.

• Do leave a meeting where any anticompetitive pricing or market allocation discussion occurs.• Do alert SOA staff and/or legal counsel to any concerning discussions• Do consult with legal counsel before raising any matter or making a statement that may involve competitively sensitive information.

Adherence to these guidelines involves not only avoidance of antitrust violations, but avoidance of behavior which might be so construed. These guidelines only provide an overview of prohibited activities. SOA legal counsel reviews meeting agenda and materials as deemed appropriate and any discussion that departs from the formal agenda should be scrutinized carefully. Antitrust compliance is everyone’s responsibility; however, please seek legal counsel if you have any questions or concerns.

2

Industry ObservationsICS Participation:

• Global• United States

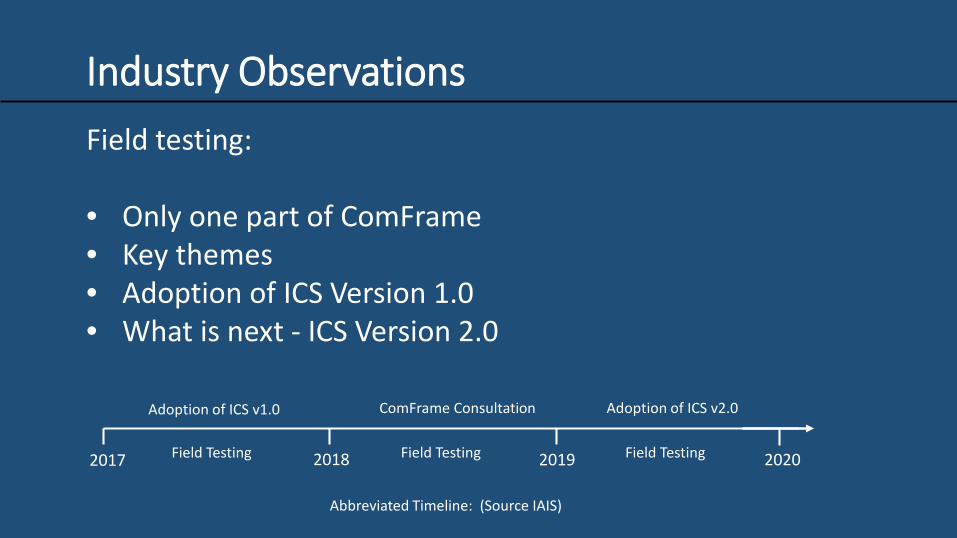

Industry ObservationsField testing:

• Only one part of ComFrame• Key themes• Adoption of ICS Version 1.0• What is next - ICS Version 2.0

2018 20192017 2020

Adoption of ICS v1.0 Adoption of ICS v2.0

Field Testing Field TestingField Testing

ComFrame Consultation

Abbreviated Timeline: (Source IAIS)

Industry ObservationsUnanswered questions:

• Field testing helps explore differing approaches – only so much can be achieved in any one year

• Focus has been technical content not implementation• Many other areas remain unknown• Benefits of participation

Industry ObservationsMoving from project to process

Current field testing allows for discretion

Some considerations for reliable ICS production:• Governance• Process and controls• Systems and data

Industry ObservationsWider considerations:

• Linkage to other regulatory aspects e.g. ORSA

• Other emerging group capital calculations / standards

• Impact on business strategy