hsm @lhy -puhujphs 9lwvy[ - indesit company - lem€¦ · net working capital 159.3 (10.0) ......

TRANSCRIPT

2014�/HSM�@LHY�-

PUHUJPHS�9LWVY[

^^ �̂PUKLZP[JVTWHU �̀JVT

1

2014 Half Year

Financial Report

2

Contents

Financial highlights for the first half of 2014 and the second

quarter of 2014 3

Interim report on operations 4

Introduction 4

Market trends 5

Currency movements 5

Consolidated results 6

Results by geographical segment 8

Cash flows 17

Balance Sheet 18

Financial position 19

Significant events during the first half of 2014 and subsequent to

period end 20

Reconciliation with the equity and results for the period of the

Parent 20

Intercompany and related party transactions, and significant,

atypical or unusual transactions 21

Corporate governance and ownership structure 21

Outlook for 2014 and forecast for operations 22

Company bodies 23

Interim condensed consolidated financial statements at 30 June

2014 24

Consolidated financial statements 25

Explanatory notes 31

Attachments 62

2014 Half Year Financial Report - Interim report on operations

3

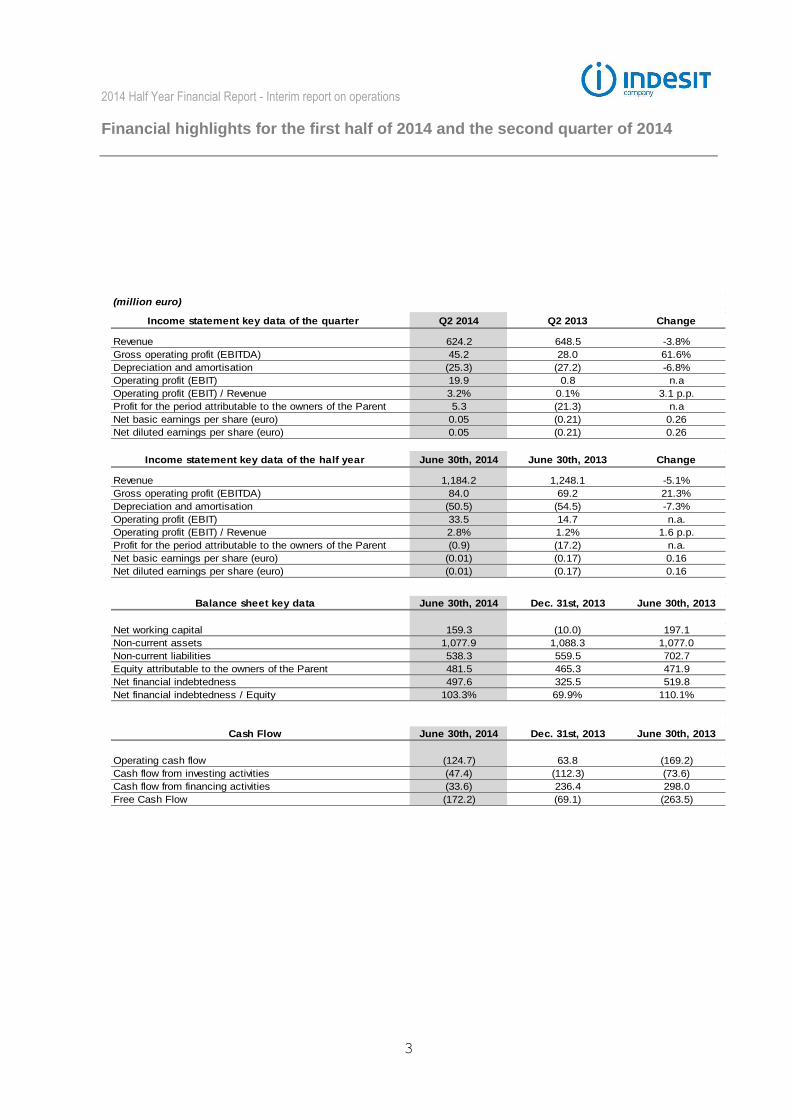

Financial highlights for the first half of 2014 and the second quarter of 2014

(million euro)

Income statement key data of the quarter Q2 2014 Q2 2013 Change

Revenue 624.2 648.5 -3.8%

Gross operating profit (EBITDA) 45.2 28.0 61.6%

Depreciation and amortisation (25.3) (27.2) -6.8%

Operating profit (EBIT) 19.9 0.8 n.a

Operating profit (EBIT) / Revenue 3.2% 0.1% 3.1 p.p.

Profit for the period attributable to the owners of the Parent 5.3 (21.3) n.a

Net basic earnings per share (euro) 0.05 (0.21) 0.26

Net diluted earnings per share (euro) 0.05 (0.21) 0.26

Income statement key data of the half year June 30th, 2014 June 30th, 2013 Change

Revenue 1,184.2 1,248.1 -5.1%

Gross operating profit (EBITDA) 84.0 69.2 21.3%

Depreciation and amortisation (50.5) (54.5) -7.3%

Operating profit (EBIT) 33.5 14.7 n.a.

Operating profit (EBIT) / Revenue 2.8% 1.2% 1.6 p.p.

Profit for the period attributable to the owners of the Parent (0.9) (17.2) n.a.

Net basic earnings per share (euro) (0.01) (0.17) 0.16

Net diluted earnings per share (euro) (0.01) (0.17) 0.16

Balance sheet key data June 30th, 2014 Dec. 31st, 2013 June 30th, 2013

Net working capital 159.3 (10.0) 197.1

Non-current assets 1,077.9 1,088.3 1,077.0

Non-current liabilities 538.3 559.5 702.7

Equity attributable to the owners of the Parent 481.5 465.3 471.9

Net financial indebtedness 497.6 325.5 519.8

Net financial indebtedness / Equity 103.3% 69.9% 110.1%

Cash Flow June 30th, 2014 Dec. 31st, 2013 June 30th, 2013

Operating cash flow (124.7) 63.8 (169.2)

Cash flow from investing activities (47.4) (112.3) (73.6)

Cash flow from financing activities (33.6) 236.4 298.0

Free Cash Flow (172.2) (69.1) (263.5)

2014 Half Year Financial Report - Interim report on operations

4

Introduction

The Half year financial report at 30 June 2014, prepared pursuant to para. 2 of Art. 154-ter of the Consolidated Finance Law, comprises this interim report on operations, the condensed interim consolidated financial statements and the statement required by para. 5 of Art. 154-bis of the Consolidated Finance Law. The condensed interim consolidated financial statements, prepared in accordance with International Financial Reporting Standards (IFRS) and, more specifically, with IAS 34 – Interim Financial Reporting, have been subjected to a limited examination by Reconta Ernst & Young S.p.A. The consolidation principles and measurement criteria are consistent with those reported in the consolidated financial statements at 31 December 2013. All the amounts presented below are stated in millions of euro, and the comparisons made (in brackets) relate to information for the corresponding period in the prior year. Percentages (margins and changes) are determined with reference to amounts stated in thousands of euro. Totals are calculated with reference to amounts stated in euro. The Group reporting to Indesit Company S.p.A. is hereafter referred to as “Indesit Company” or "Indesit" or simply the “Group”; when the commentary relates to the parent company or individual subsidiaries, their names and legal form are stated in full. The amounts presented at constant exchange rates with respect to 2013 were estimated by taking account of the transaction effects and the effect of translating to euro (the Group's functional currency) the operations reported in foreign currency financial statements. Certain economic information presented below by the Group makes reference to intermediate indicators of profitability, such as EBITDA (gross operating profit). Management believes that this indicator is an important parameter for monitoring and measuring the Group's operating performance, since it is not influenced by the effects of differing criteria for the determination of taxable income, or by the related depreciation policies. Nevertheless, EBITDA is not identified as an accounting measure in the IFRS endorsed by the European Commission. Consequently, the criteria applied for determining this indicator might not be consistent with those adopted by other groups or companies and, accordingly, its value might not be comparable with that determined by them.

2014 Half Year Financial Report - Interim report on operations

5

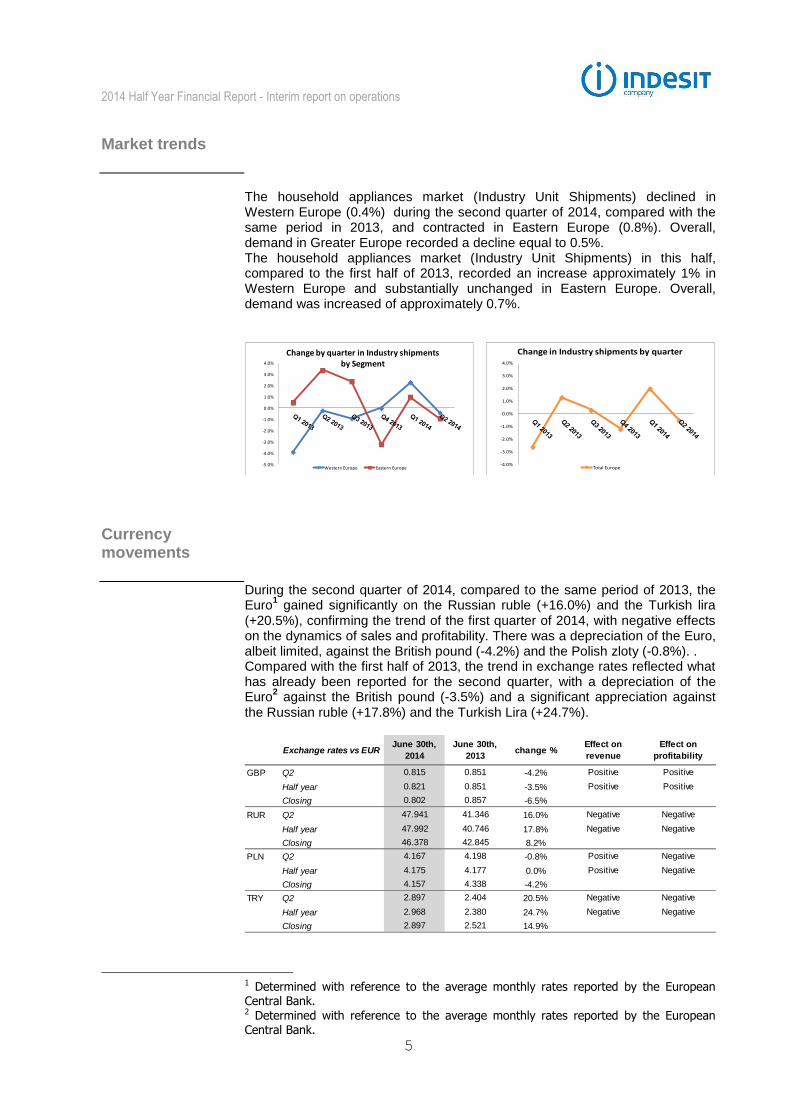

Market trends

The household appliances market (Industry Unit Shipments) declined in Western Europe (0.4%) during the second quarter of 2014, compared with the same period in 2013, and contracted in Eastern Europe (0.8%). Overall, demand in Greater Europe recorded a decline equal to 0.5%. The household appliances market (Industry Unit Shipments) in this half, compared to the first half of 2013, recorded an increase approximately 1% in Western Europe and substantially unchanged in Eastern Europe. Overall, demand was increased of approximately 0.7%.

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

Change by quarter in Industry shipments by Segment

Western Europe Eastern Europe

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

Change in Industry shipments by quarter

Total Europe

Currency movements

During the second quarter of 2014, compared to the same period of 2013, the Euro

1 gained significantly on the Russian ruble (+16.0%) and the Turkish lira

(+20.5%), confirming the trend of the first quarter of 2014, with negative effects on the dynamics of sales and profitability. There was a depreciation of the Euro, albeit limited, against the British pound (-4.2%) and the Polish zloty (-0.8%). . Compared with the first half of 2013, the trend in exchange rates reflected what has already been reported for the second quarter, with a depreciation of the Euro

2 against the British pound (-3.5%) and a significant appreciation against

the Russian ruble (+17.8%) and the Turkish Lira (+24.7%).

GBP Q2 0.815 0.851 -4.2% Positive Positive

Half year 0.821 0.851 -3.5% Positive Positive

Closing 0.802 0.857 -6.5%

RUR Q2 47.941 41.346 16.0% Negative Negative

Half year 47.992 40.746 17.8% Negative Negative

Closing 46.378 42.845 8.2%

PLN Q2 4.167 4.198 -0.8% Positive Negative

Half year 4.175 4.177 0.0% Positive Negative

Closing 4.157 4.338 -4.2%

TRY Q2 2.897 2.404 20.5% Negative Negative

Half year 2.968 2.380 24.7% Negative Negative

Closing 2.897 2.521 14.9%

Exchange rates vs EUREffect on

profitability

Effect on

revenuechange %

June 30th,

2013

June 30th,

2014

1 Determined with reference to the average monthly rates reported by the European Central Bank. 2 Determined with reference to the average monthly rates reported by the European Central Bank.

2014 Half Year Financial Report - Interim report on operations

6

Consolidated results

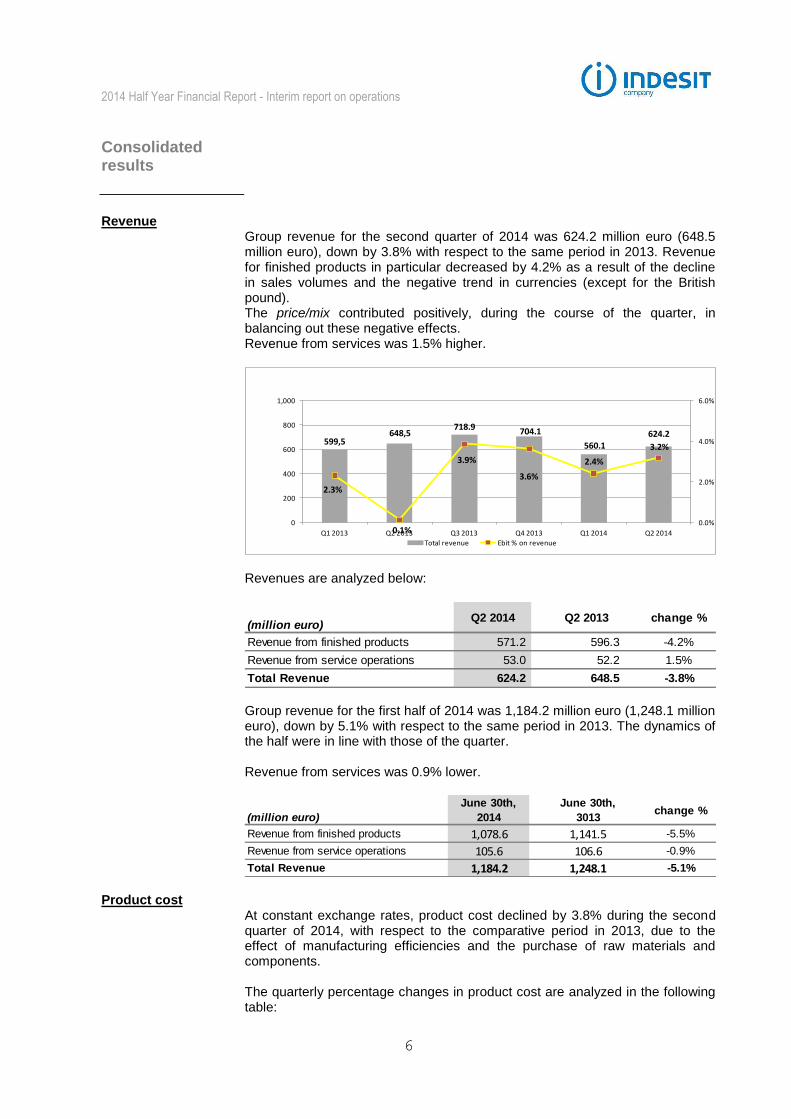

Revenue

Group revenue for the second quarter of 2014 was 624.2 million euro (648.5 million euro), down by 3.8% with respect to the same period in 2013. Revenue for finished products in particular decreased by 4.2% as a result of the decline in sales volumes and the negative trend in currencies (except for the British pound). The price/mix contributed positively, during the course of the quarter, in balancing out these negative effects. Revenue from services was 1.5% higher.

599,5 648,5

718.9 704.1

560.1 624.2

2.3%

0.1%

3.9%

3.6%

2.4%

3.2%

0.0%

2.0%

4.0%

6.0%

0

200

400

600

800

1,000

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

Total revenue Ebit % on revenue

Revenues are analyzed below:

(million euro)Q2 2014 Q2 2013 change %

Revenue from finished products 571.2 596.3 -4.2%

Revenue from service operations 53.0 52.2 1.5%

Total Revenue 624.2 648.5 -3.8% Group revenue for the first half of 2014 was 1,184.2 million euro (1,248.1 million euro), down by 5.1% with respect to the same period in 2013. The dynamics of the half were in line with those of the quarter. Revenue from services was 0.9% lower.

(million euro)

June 30th,

2014

June 30th,

3013change %

Revenue from finished products 1,078.6 1,141.5 -5.5%

Revenue from service operations 105.6 106.6 -0.9%

Total Revenue 1,184.2 1,248.1 -5.1% Product cost

At constant exchange rates, product cost declined by 3.8% during the second quarter of 2014, with respect to the comparative period in 2013, due to the effect of manufacturing efficiencies and the purchase of raw materials and components. The quarterly percentage changes in product cost are analyzed in the following table:

2014 Half Year Financial Report - Interim report on operations

7

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

Sourcing cost 0.7% 0.4% -0.9% -0.2% -0.6% -2.3%

Manufacturing cost -2.0% -0.8% 0.0% 0.5% -1.8% -1.4%

Total product cost -1.3% -0.4% -0.9% 0.3% -2.5% -3.8% At constant exchange rates, product cost was 3.1% lower in the first half of 2014 than in the comparative period of 2013, as a result of savings in production and supply costs.

Other operating costs At current exchange rates, advertising and promotion expenses totaled 15.9 million euro in the second quarter of 2014 (13.9 million euro). At current exchange rates, advertising and promotion expenses totaled 21.5 million euro in the first half of 2014 (18.8 million euro).

4.8

13.913.0 12.6

5.5

15.9

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

Advertising and Promo

0.8%

2.1%1.8% 1.8%

1.0%

2.8%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

Advertising and Promo incidence on revenue

Operating profitability

EBIT, with reference both to the quarterly and to the Half yearly figures, reveals similar evolutionary dynamics. The significant improvement compared to 2013 is due to the considerable performance of the price/mix and the incessant activity of reducing the purchasing and production costs, in addition to the lesser impact of the recorded non-recurring net expenses compared to 2013. Negative effects on the operating margin were determined by the reduction in sales volumes in some significant markets for Indesit and by the unfavorable trend of the major currencies in which the Group operates. Operating profit (EBIT), gross of non-recurring items, is analyzed by quarter in the following chart:

12.3 13.0

29.6 29.0

13.920.8

2.0%

2.0%

4.1%4.1%

2.5%

3.7%

0

20

40

60

80

100

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Q12013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

EBIT gross of non recurring items EBIT % gross of non recurring items

2014 Half Year Financial Report - Interim report on operations

8

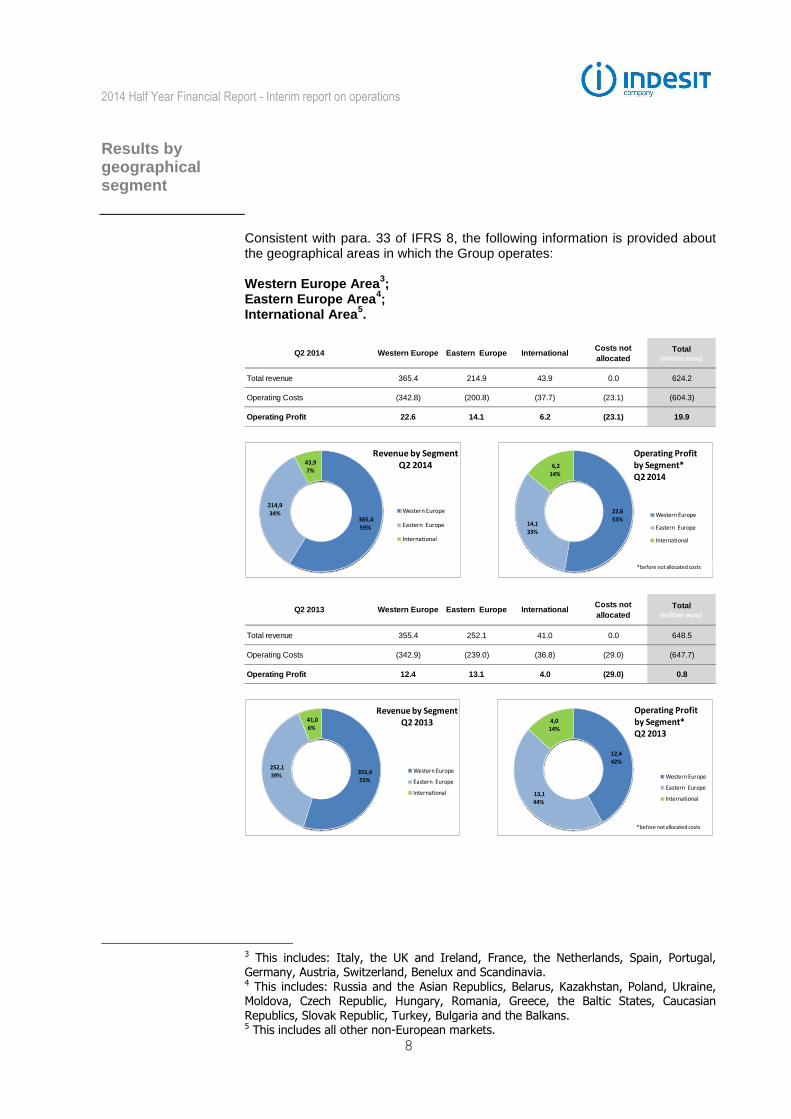

Results by geographical segment

Consistent with para. 33 of IFRS 8, the following information is provided about the geographical areas in which the Group operates: Western Europe Area

3;

Eastern Europe Area4;

International Area5.

Q2 2014 Western Europe Eastern Europe InternationalCosts not

allocated

Total(million euro)

Total revenue 365.4 214.9 43.9 0.0 624.2

Operating Costs (342.8) (200.8) (37.7) (23.1) (604.3)

Operating Profit 22.6 14.1 6.2 (23.1) 19.9

365,4 59%

214,9

34%

43,9

7%

Revenue by Segment Q2 2014

Western Europe

Eastern Europe

International

22,653%

14,1

33%

6,214%

Operating Profit by Segment*Q2 2014

Western Europe

Eastern Europe

International

*before not allocated costs

Q2 2013 Western Europe Eastern Europe InternationalCosts not

allocated

Total(million euro)

Total revenue 355.4 252.1 41.0 0.0 648.5

Operating Costs (342.9) (239.0) (36.8) (29.0) (647.7)

Operating Profit 12.4 13.1 4.0 (29.0) 0.8

355,4

55%

252,1

39%

41,0 6%

Revenue by Segment Q2 2013

Western Europe

Eastern Europe

International

12,4

42%

13,144%

4,014%

Operating Profit by Segment*Q2 2013

Western Europe

Eastern Europe

International

*before not allocated costs

3 This includes: Italy, the UK and Ireland, France, the Netherlands, Spain, Portugal, Germany, Austria, Switzerland, Benelux and Scandinavia. 4 This includes: Russia and the Asian Republics, Belarus, Kazakhstan, Poland, Ukraine, Moldova, Czech Republic, Hungary, Romania, Greece, the Baltic States, Caucasian Republics, Slovak Republic, Turkey, Bulgaria and the Balkans. 5 This includes all other non-European markets.

2014 Half Year Financial Report - Interim report on operations

9

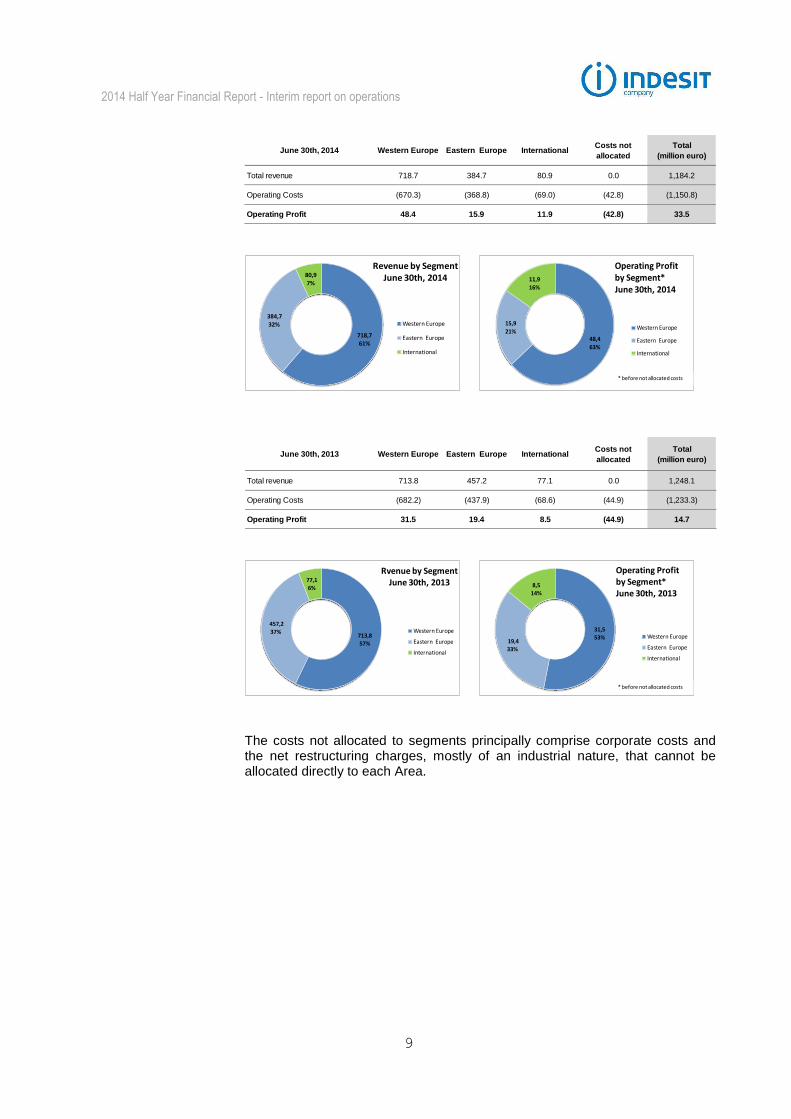

June 30th, 2014 Western Europe Eastern Europe InternationalCosts not

allocated

Total

(million euro)

Total revenue 718.7 384.7 80.9 0.0 1,184.2

Operating Costs (670.3) (368.8) (69.0) (42.8) (1,150.8)

Operating Profit 48.4 15.9 11.9 (42.8) 33.5

718,7

61%

384,7 32%

80,97%

Revenue by SegmentJune 30th, 2014

Western Europe

Eastern Europe

International

48,463%

15,921%

11,9 16%

Operating Profit by Segment*June 30th, 2014

Western Europe

Eastern Europe

International

* before not allocated costs

June 30th, 2013 Western Europe Eastern Europe InternationalCosts not

allocated

Total

(million euro)

Total revenue 713.8 457.2 77.1 0.0 1,248.1

Operating Costs (682.2) (437.9) (68.6) (44.9) (1,233.3)

Operating Profit 31.5 19.4 8.5 (44.9) 14.7

713,8

57%

457,2

37%

77,1

6%

Rvenue by SegmentJune 30th, 2013

Western Europe

Eastern Europe

International

31,553%

19,4

33%

8,5 14%

Operating Profit by Segment*June 30th, 2013

Western Europe

Eastern Europe

International

* before not allocated costs

The costs not allocated to segments principally comprise corporate costs and the net restructuring charges, mostly of an industrial nature, that cannot be allocated directly to each Area.

2014 Half Year Financial Report - Interim report on operations

10

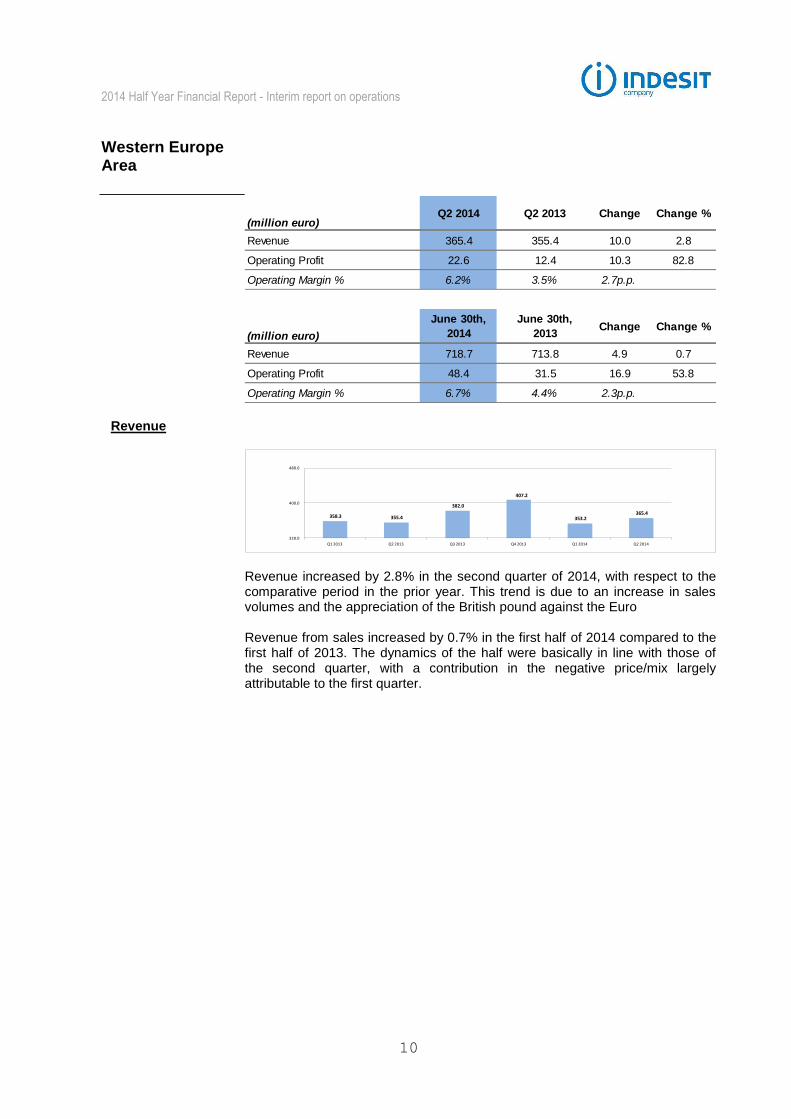

Western Europe Area

(million euro)Q2 2014 Q2 2013 Change Change %

Revenue 365.4 355.4 10.0 2.8

Operating Profit 22.6 12.4 10.3 82.8

Operating Margin % 6.2% 3.5% 2.7p.p.

(million euro)

June 30th,

2014

June 30th,

2013Change Change %

Revenue 718.7 713.8 4.9 0.7

Operating Profit 48.4 31.5 16.9 53.8

Operating Margin % 6.7% 4.4% 2.3p.p.

Revenue

358.3 355.4

382.0

407.2

353.2 365.4

320.0

400.0

480.0

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

Revenue increased by 2.8% in the second quarter of 2014, with respect to the comparative period in the prior year. This trend is due to an increase in sales volumes and the appreciation of the British pound against the Euro Revenue from sales increased by 0.7% in the first half of 2014 compared to the first half of 2013. The dynamics of the half were basically in line with those of the second quarter, with a contribution in the negative price/mix largely attributable to the first quarter.

2014 Half Year Financial Report - Interim report on operations

11

Profitability

19.1

12.4

18.5

30.6 25.7

22.6

5.3%

3.5%

4.9%

7.5% 7.3%

6.2%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014Operating Profit

Operating Margin % Profitability in Western Europe in the second quarter of 2014 almost doubled compared with the same period in 2013. This result was helped by major savings in the costs of goods sold, in addition to the positive trend recorded by the British pound. Negative affects on the profitability of the Area were caused substantially by the price/mix. The profitability of the Area during the first half of 2014 was basically in line with that for the second quarter.

2014 Half Year Financial Report - Interim report on operations

12

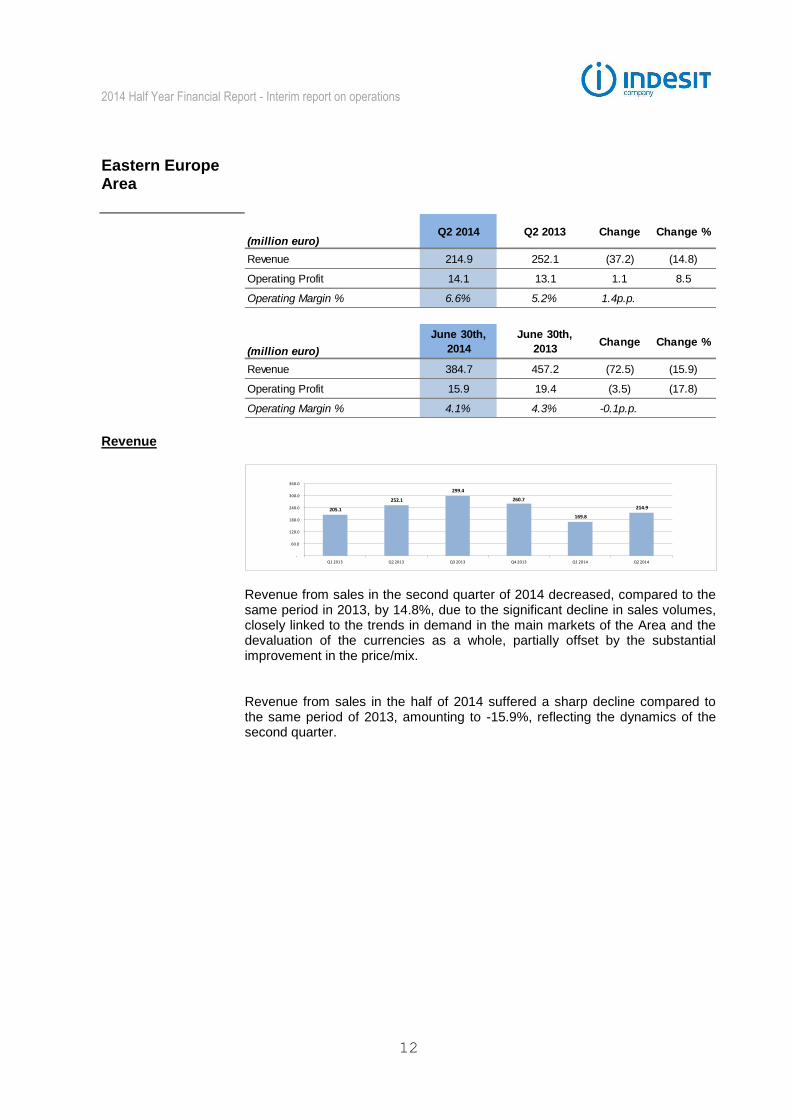

Eastern Europe Area

(million euro)Q2 2014 Q2 2013 Change Change %

Revenue 214.9 252.1 (37.2) (14.8)

Operating Profit 14.1 13.1 1.1 8.5

Operating Margin % 6.6% 5.2% 1.4p.p.

(million euro)

June 30th,

2014

June 30th,

2013Change Change %

Revenue 384.7 457.2 (72.5) (15.9)

Operating Profit 15.9 19.4 (3.5) (17.8)

Operating Margin % 4.1% 4.3% -0.1p.p. Revenue

205.1

252.1

299.4

260.7

169.8

214.9

-

60.0

120.0

180.0

240.0

300.0

360.0

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

Revenue from sales in the second quarter of 2014 decreased, compared to the same period in 2013, by 14.8%, due to the significant decline in sales volumes, closely linked to the trends in demand in the main markets of the Area and the devaluation of the currencies as a whole, partially offset by the substantial improvement in the price/mix. Revenue from sales in the half of 2014 suffered a sharp decline compared to the same period of 2013, amounting to -15.9%, reflecting the dynamics of the second quarter.

2014 Half Year Financial Report - Interim report on operations

13

Profitability

6.3

13.1

20,1

5,0 1.7

14.1

3.1%

5.2%

6.7%

1.9% 1.0%

6.6%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

-

5.0

10.0

15.0

20.0

25.0

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014Operating Profit

Operating Margin % The operating profit generated by the Area in the second quarter of 2014 is basically in line, in absolute value, with the same period in 2013 and an improvement in percentage terms. Positive effects such as the improvement in the price/mix, savings in the cost of goods sold and lower non-recurring costs were offset by the negative effect caused by the currencies and by lower sales volumes. The operating profit generated by the Area in the half of 2014, compared to 2013, experienced a slight decrease in absolute value and is stable in percentage terms due to lower volumes while, as well as in the first quarter, the heavy negative currency effect was completely offset by a positive price mix.

2014 Half Year Financial Report - Interim report on operations

14

International Area

(million euro)Q2 2014 Q2 2013 Change Change %

Revenue 43.9 41.0 2.9 7.0

Operating Profit 6.2 4.0 2.2 53.3

Operating Margin % 14.1% 9.7% 4.4p.p.

(million euro)

June 30th,

2014

June 30th,

2013Change Change %

Revenue 80.9 77.1 3.8 4.9

Operating Profit 11.9 8.5 3.4 40.4

Operating Margin % 14.8% 11.1% 3.7p.p. Revenue

36.1 41.0

37.5 36.2 37.1

43.9

-

10.0

20.0

30.0

40.0

50.0

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

In the second quarter of 2014, revenues were broadly stable in absolute terms. The Area recorded a significant increase in sales volumes, offset by the negative impact of the currencies (in particular the Argentine Peso) and the price/mix. In the first half, revenues were up 4.9% compared to 2013, with the same factors present in the second quarter.

2014 Half Year Financial Report - Interim report on operations

15

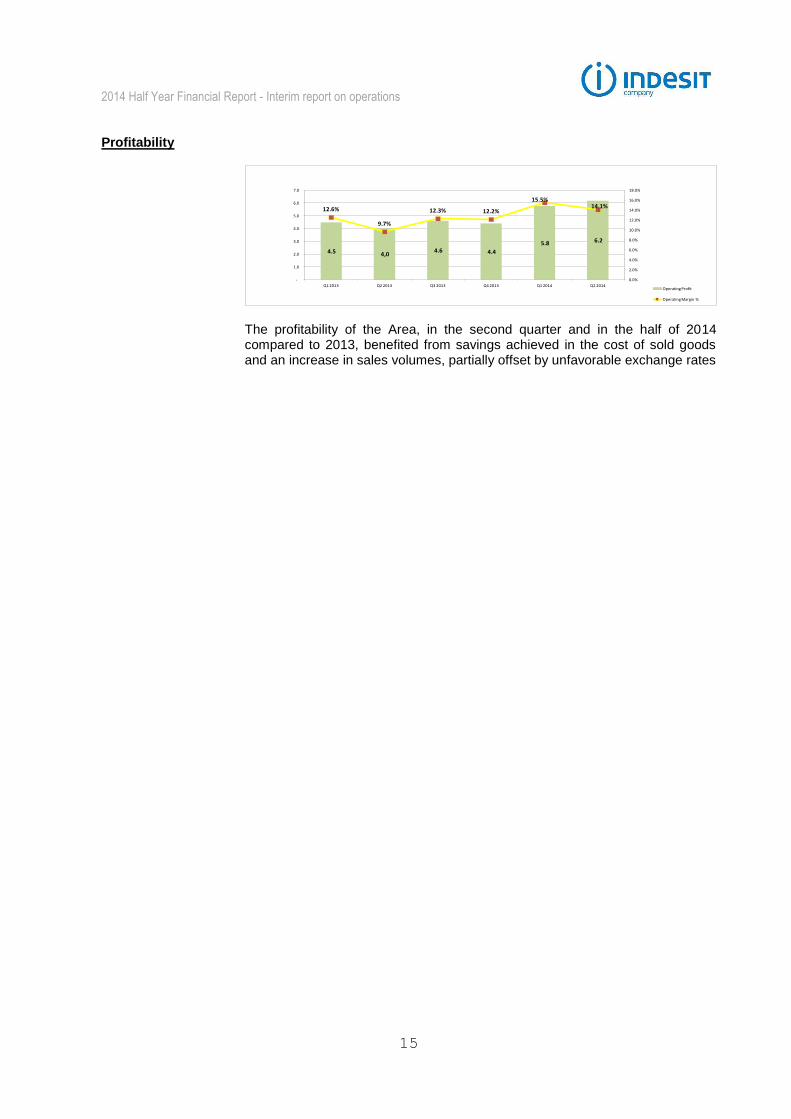

Profitability

4.5 4,0 4.6 4.4

5.8 6.2

12.6%

9.7%

12.3% 12.2%

15.5%14.1%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014Operating Profit

Operating Margin % The profitability of the Area, in the second quarter and in the half of 2014 compared to 2013, benefited from savings achieved in the cost of sold goods and an increase in sales volumes, partially offset by unfavorable exchange rates

2014 Half Year Financial Report - Interim report on operations

16

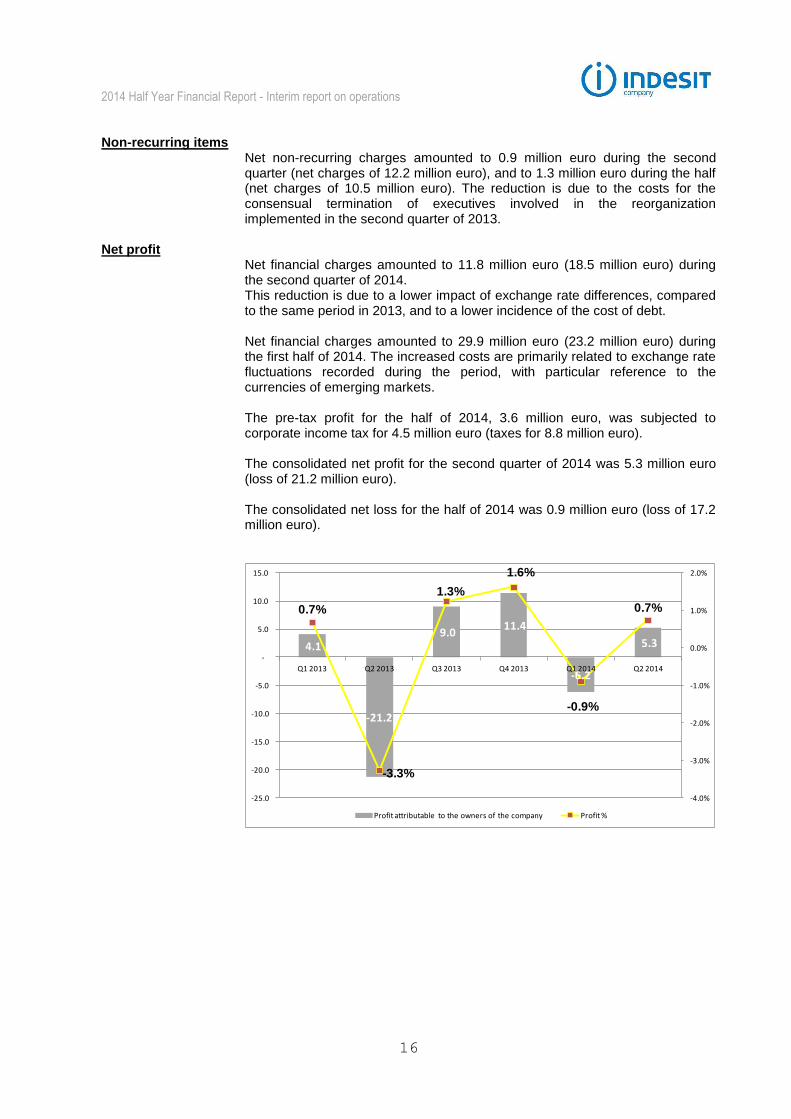

Non-recurring items

Net non-recurring charges amounted to 0.9 million euro during the second quarter (net charges of 12.2 million euro), and to 1.3 million euro during the half (net charges of 10.5 million euro). The reduction is due to the costs for the consensual termination of executives involved in the reorganization implemented in the second quarter of 2013.

Net profit Net financial charges amounted to 11.8 million euro (18.5 million euro) during the second quarter of 2014. This reduction is due to a lower impact of exchange rate differences, compared to the same period in 2013, and to a lower incidence of the cost of debt. Net financial charges amounted to 29.9 million euro (23.2 million euro) during the first half of 2014. The increased costs are primarily related to exchange rate fluctuations recorded during the period, with particular reference to the currencies of emerging markets. The pre-tax profit for the half of 2014, 3.6 million euro, was subjected to corporate income tax for 4.5 million euro (taxes for 8.8 million euro). The consolidated net profit for the second quarter of 2014 was 5.3 million euro (loss of 21.2 million euro). The consolidated net loss for the half of 2014 was 0.9 million euro (loss of 17.2 million euro).

4.1

-21.2

9.0 11.4

-6.2

5.3

0.7%

-3.3%

1.3%

1.6%

-0.9%

0.7%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

-25.0

-20.0

-15.0

-10.0

-5.0

-

5.0

10.0

15.0

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

Profit attributable to the owners of the company Profit %

2014 Half Year Financial Report - Interim report on operations

17

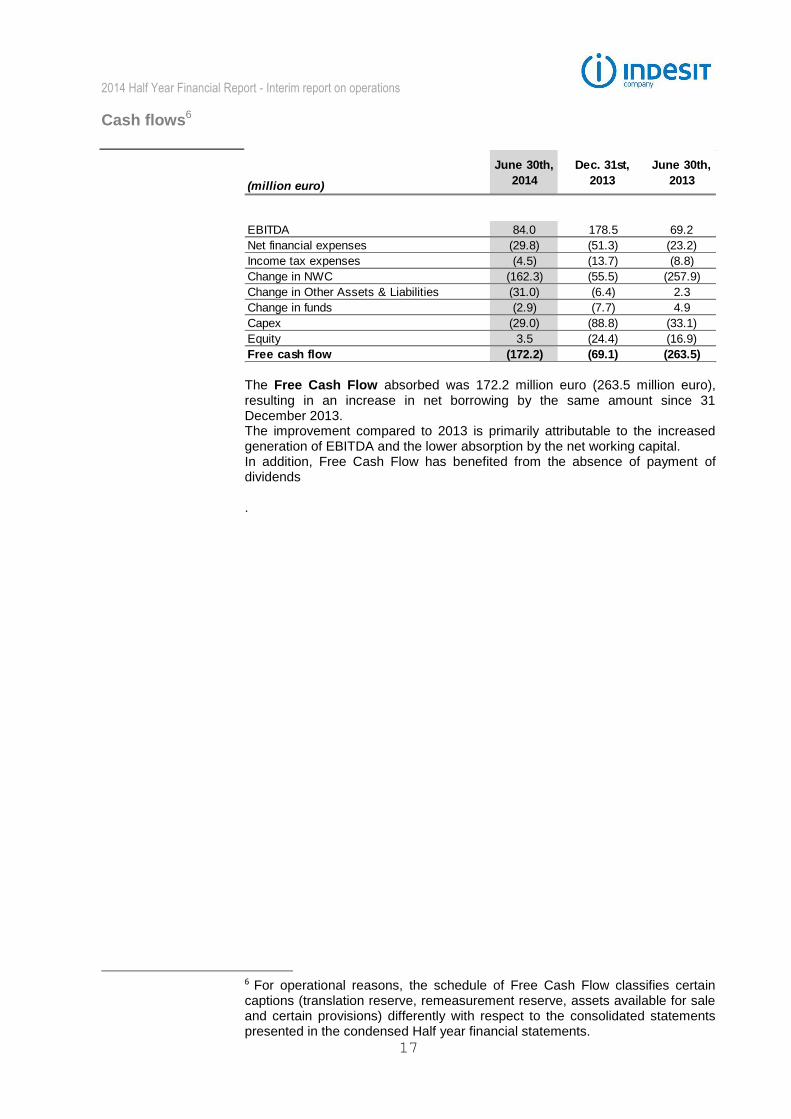

Cash flows6

(million euro)

June 30th,

2014

Dec. 31st,

2013

June 30th,

2013

EBITDA 84.0 178.5 69.2

Net financial expenses (29.8) (51.3) (23.2)

Income tax expenses (4.5) (13.7) (8.8)

Change in NWC (162.3) (55.5) (257.9)

Change in Other Assets & Liabilities (31.0) (6.4) 2.3

Change in funds (2.9) (7.7) 4.9

Capex (29.0) (88.8) (33.1)

Equity 3.5 (24.4) (16.9)

Free cash flow (172.2) (69.1) (263.5)

The Free Cash Flow absorbed was 172.2 million euro (263.5 million euro), resulting in an increase in net borrowing by the same amount since 31 December 2013. The improvement compared to 2013 is primarily attributable to the increased generation of EBITDA and the lower absorption by the net working capital. In addition, Free Cash Flow has benefited from the absence of payment of dividends .

6 For operational reasons, the schedule of Free Cash Flow classifies certain captions (translation reserve, remeasurement reserve, assets available for sale and certain provisions) differently with respect to the consolidated statements presented in the condensed Half year financial statements.

2014 Half Year Financial Report - Interim report on operations

18

Balance sheet7

(million euro)

June 30th,

2014

Dec. 31st,

2013

June 30th,

2013

Trade receivables 490.2 426.5 529.2

Inventories 378.4 302.4 403.0

Trade payables (709.2) (738.9) (735.1)

Net working capital 159.3 (10.0) 197.1

Non-current assets 940.2 954.2 956.3

Other current assets and liabilities and non-current liabilities (120.5) (153.4) (161.7)

Net invested capital 979.1 790.7 991.7

Net financial indebtedness 497.6 325.5 519.8

Equity attributable to the owners of the Parent 481.5 465.3 471.9

Non-controlling interests 0.0 0.0 0.0

Equity and financial liabilities 979.1 790.7 991.7 The decrease in net working capital since 30 June 2013 mainly reflects the improvement in the credit rating and efficient inventory management. Certain trade receivables in the UK and Poland have been sold without recourse. The amounts sold but not collected at 30 June 2014 total 28.4 million euro.

(% on revenue)

June 30th,

2014

Dec. 31st,

2013

June 30th,

2013

Trade receivables 18.8% 16.0% 18.7%

Inventories 14.5% 11.3% 14.2%

Trade payables 27.2% 27.7% 26.0%

Net working capital 6.1% -0.4% 7.0% The Shareholders' equity attributable to the shareholders of the parent company increased compared to 31 December 2013 by 16.2 million euro in particular due to the positive effect of the currency conversion and the positive trend of the Cash Flow Hedge reserve.

7 The trade receivables and payables, inventories and equity reported in the above reclassified statement of financial position are the same as the amounts reported in the consolidated statement of financial position. Net financial indebtedness is analyzed in the

following table. “Non-current assets” and “Other current assets and liabilities and non-

current liabilities” comprise the captions of the consolidated statement of financial

position that are not mentioned above or included as part of net financial indebtedness.

2014 Half Year Financial Report - Interim report on operations

19

Financial position

(million euro)

June 30th,

2014

Dec. 31st,

2013

June 30th,

2013

Current financial assets 11.0 17.9 31.2

Cash and cash equivalents 125.0 330.8 197.9

Banks and other financial payables (294.8) (307.4) (232.5)

Net financial indebtedness position - short term (158.8) 41.3 (3.3)

Medium/long-term financial payables (340.8) (368.6) (518.4)

Net financial position (*) (499.6) (327.4) (521.7)

Other non-current financial assets 2.0 1.9 1.9

Net financial indebtedness (497.6) (325.5) (519.8)

(*) As defined in CONSOB Communication DEM /6064293 dated 28 July 2006, applying the CESR recommendations dated 10 February

2005

Net financial indebtedness amounts to 497.6 million euro (519.8 million euro). Gross financial indebtedness totals 635.6 million euro (750.8 million euro), of which 53.6% is classified as long term (69.0% at 30 June 2013). The maturity profile of gross long-term financial payables is presented below:

2015 2016 2017 2018 TOTAL

EUROBOND 296.8 0.0 0.0 0.0 296.8 296.8

DUE TO BANKS AND OTHER FINANCIAL PAYABLES 44.0 6.1 12.5 12.8 12.8 44.0

Total 340.8 6.1 12.5 12.8 309.5 340.8

Medium/long-term

financial payables

2014 Half Year Financial Report - Interim report on operations

20

Significant events during the first half of 2014 and subsequent to period end

Starting from 1/1/2014 the Group as a result of the revision of the invoice flows and the evolution of functional and risk profiles of the various companies of the group, has adopted a new transfer pricing policy to adjust intercompany transactions and ensure that these continue to be regulated at market conditions, ie conditions similar to those offered to non-related parties. In June 2014 the Group repaid the bond (USPP) in full and in advance, including the installments due in September 2014 and in September 2016, for an amount of approx. 145 million euro. On 10 July 2014, Whirlpool Corporation and Fineldo S.p.A. (a holding company whose holdings include a controlling stake in Indesit Company SpA) announced that they had signed an agreement for the sale of the stake held by Fineldo in Indesit Company SpA. Whirlpool Corporation also signed further agreements with some members of the Merloni family for the purchase of the shares they held in Indesit. Under these agreements, Whirlpool would acquire a total number of shares representing 66.8% of the voting rights. The acquisition of the control of Indesit is subject to the authorization of the Court of Ancona and the antitrust authorities and is expected to be concluded by the end of 2014. At present, and based on the information available to the Board of Directors such agreements do not produce effects that should be reflected in the financial and economic situation of the Indesit Group as at 30 June 2014. There have not been any other significant events subsequent to the end of the period.

Reconciliation with the equity and results for the period of the Parent

In accordance with Consob Communication DEM/6064293 dated 28 July 2006, the equity and results for the period of the parent company are reconciled below with the related consolidated amounts. (million euro)

Profit (Loss) Equity Profit (Loss) Equity

Financial statements of the parent company (12.1) 482.7 2.3 489.9

Consolidated adjustments

Difference between carrying amount and equity of group

companies17.2 14.0 13.3 (3.0)

Dividends received from subsidiaries 0.0 0.0 (30.0) -

Effect of aligning separate financial statements with group 1.2 4.3 2.4 5.3

Elimination of intercompany profits (6.5) (18.0) (1.3) (15.3)

Other effects (0.7) (1.5) (3.9) (5.0)

Total consolidation adjustments 11.2 (1.2) (19.5) (18.0)

Consolidated financial statements (0.9) 481.5 (17.2) 471.9

June 30th, 2014 June 30th, 2013

2014 Half Year Financial Report - Interim report on operations

21

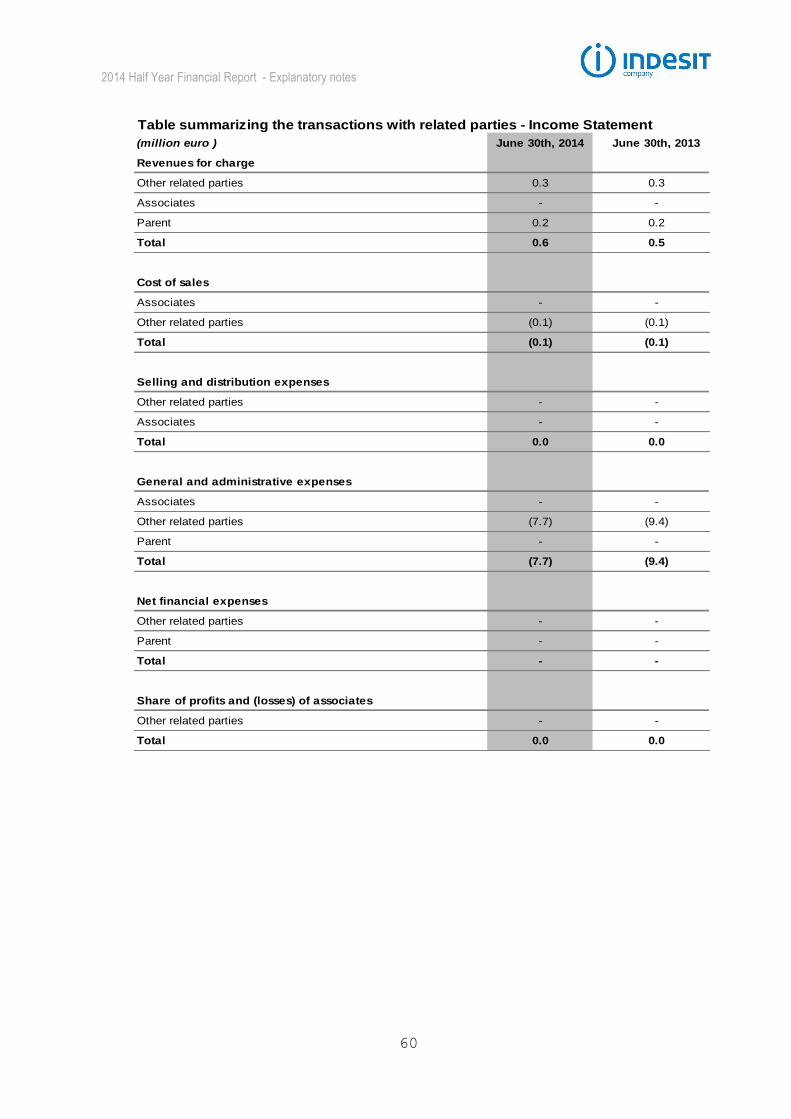

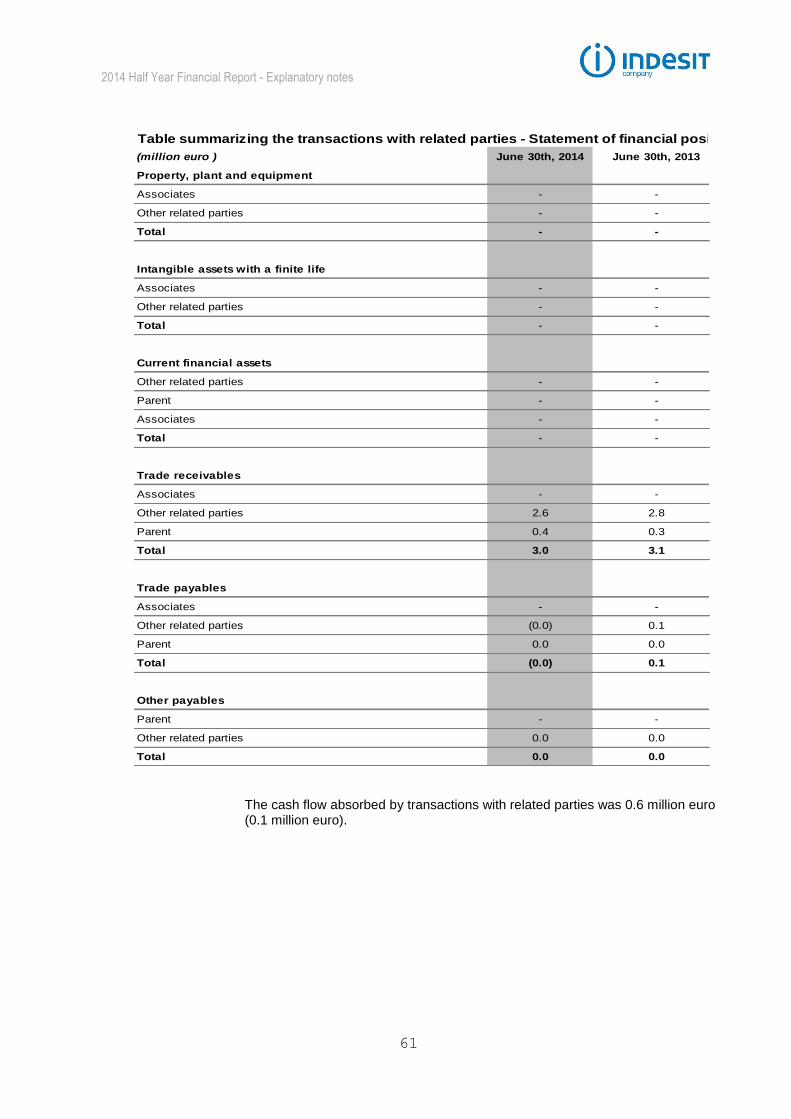

Intercompany and related party transactions, and significant, atypical or unusual transactions

Transactions between Group companies are settled on arms'-length terms, having regard for the quality of the goods and services provided. The notes to the condensed interim consolidated financial statements describe the nature of the principal transactions arranged by the parent and other Group companies with related parties. They also contain the detailed information required by Consob regulations and IAS 24. Pursuant to Consob regulations

8, Attachments

3 and 4 to the condensed interim consolidated financial statements present the consolidated income statement and statement of financial position, showing non-recurring items and transactions with related parties separately, together with their percentage incidence with respect to each account caption. Starting from 1 January 2014, the Group's intercompany transfer prices are determined using the Transactional Net Margin Method (TNMM), as required by the regulations, normal practice in Italy and the OECD Guidelines (or Directives). This method was applied using as an indicator of profit, the producers of the Group, the ratio of operating profit and total costs, and for the Group's distributors, the ratio of operating profit and sales revenues. Transactions with related parties are not significant to the economic and financial position of the Group. There were no unusual or non-business transactions during the first half of 2014.

Corporate governance and ownership structure

The system of Corporate Governance adopted by Indesit Company S.p.A. is essentially consistent with the principles established in the Code of Conduct for Listed Companies (the Code) and with international best practice. On 21 March 2014, the Board of Directors approved the 2013 Annual report on corporate governance and the ownership structure, prepared pursuant to art. 123-bis of the consolidated law on financial intermediation (TUIF). This report is published on the Company's website in the “Company” section, sub-section “Governance”

9. Reference is made to this report for the disclosures

required by law. Indesit Company S.p.A. has adopted the ordinary model of administration and control (envisaged under Italian law), with the presence of a Shareholders'

8 Consob Decision 15519 dated 27 July 2006 and Consob Communication DEM/6064293 dated 28 July 2006.

9 At the address http://www.indesitcompany.com/inst/en/vision/corporate_governance/cGHome.action

2014 Half Year Financial Report - Interim report on operations

22

Meeting, a Board of Directors, a Board of Statutory Auditors and Independent Auditors. The directors and officers are appointed at the Shareholders' Meeting and remain in office for a period of three years. The significant presence of Independent Directors, as defined in the Code, and the important role they play on both the Board and Board Committees (Human Resources Committee, Audit Committee, Strategic Development Committee and Related-party transactions Committee), ensures that the interests of all shareholders are appropriately balanced and guarantees a high level of discussion at Board meetings.

Outlook for 2014 and forecast for operations

Although during the first half of the year, the Euro has appreciated significantly against the Russian ruble, Hryvna and Turkish lira, the actions of selective increase in prices should allow Indesit undertaken to achieve, in the current year, a level of sales in line with 2013. The Group, in the light of the above the activity of containment of production costs, is estimated to achieve an operating profit (Operating Margin net of non recurring items and EBIT adjusted), which stands at around 3.5%. Milan, 30 July 2014 for the Board of Directors The Chairman Marco Milani

2014 Half Year Financial Report - Interim report on operations

23

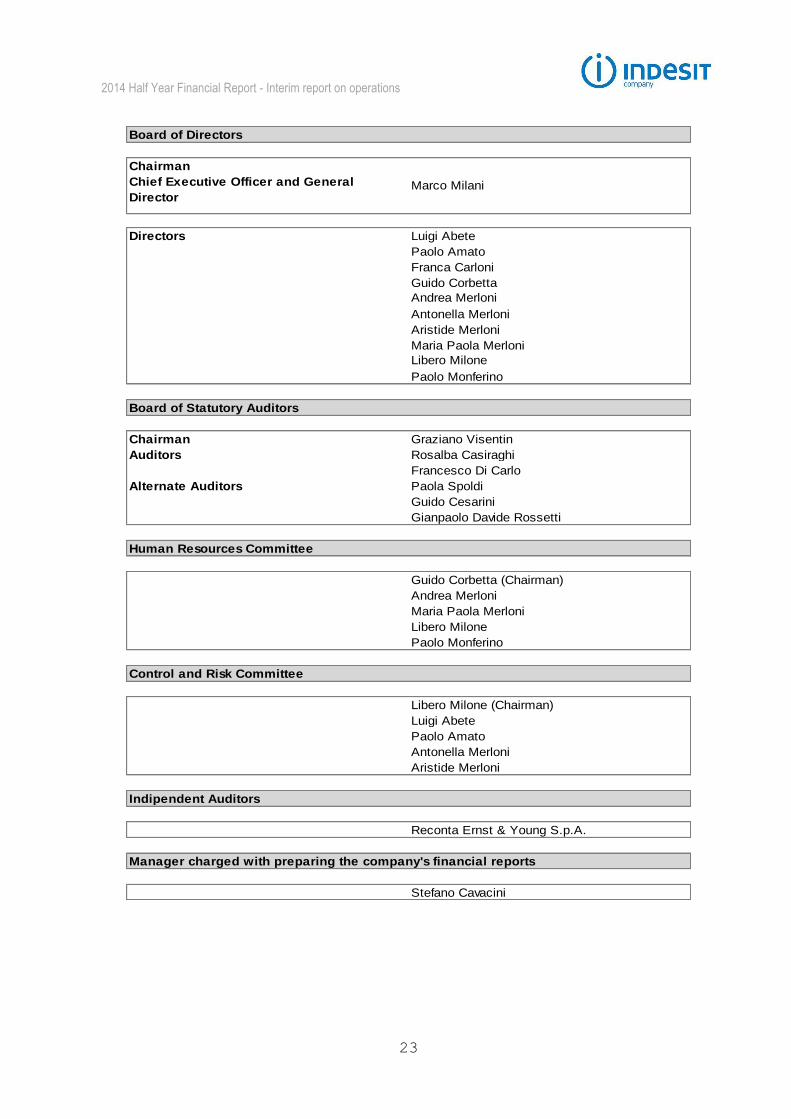

Chairman

Chief Executive Officer and General

Director

Directors Luigi Abete

Paolo Amato

Franca Carloni

Guido Corbetta

Andrea Merloni

Antonella Merloni

Aristide Merloni

Maria Paola Merloni

Libero Milone

Paolo Monferino

Board of Statutory Auditors

Chairman Graziano Visentin

Auditors Rosalba Casiraghi

Francesco Di Carlo

Alternate Auditors Paola Spoldi

Guido Cesarini

Gianpaolo Davide Rossetti

Human Resources Committee

Guido Corbetta (Chairman)

Andrea Merloni

Maria Paola Merloni

Libero Milone

Paolo Monferino

Control and Risk Committee

Libero Milone (Chairman)

Luigi Abete

Paolo Amato

Antonella Merloni

Aristide Merloni

Reconta Ernst & Young S.p.A.

Stefano Cavacini

Manager charged with preparing the company's financial reports

Board of Directors

Marco Milani

Indipendent Auditors

2014 Half Year Financial Report - Interim report on operations

24

Interim condensed consolidated

financial statements at 30 June 2014

2014 Half Year Financial Report - Interim report on operations

25

Consolidated financial statements

2014 Half Year Financial Report - Consolidated financial statements

26

Consolidated income statement for the first half of 201410

(million euro) NoteJune 30th,

2014

June 30th,

2013

Revenue 8.1 1,184.2 1,248.1

Cost of sales 8.2 (893.2) (954.0)

Selling and distribution expenses 8.3 (209.3) (218.4)

General and administrative expenses 8.4 (48.3) (60.9)

Operating profit 8.5 33.5 14.7

Net interest (12.8) (12.7)

Exchange rate 8.6 (14.9) (8.2)

Fees and other net financial expenses 8.6 (2.2) (2.3)

Share of profit (losses) of associates and other 8.6 0.0 0.0

Profit before tax 3.6 (8.4)

Income taxes 8.7 (4.5) (8.8)

Profit for the year (0.9) (17.2)

Attributable to non-controlling interests 0.0 (0.0)

Attributable to the owners of the Parent (0.9) (17.2)

Basic earnings per share (euro) 8.14 (0.01) (0.17)

Diluted earnings per share (euro) 8.14 (0.01) (0.17)

10

Pursuant to Consob Resolution no. 15519 dated 27 July 2006, the effects of related-party and non-recurring

transactions on the consolidated income statement are reported in Attachment 3 and in notes 8.5 and 10, respectively.

2014 Half Year Financial Report - Consolidated financial statements

27

Consolidated Statement of Comprehensive Income for the first half of 2014

(million euro)

Note June 30th, 2014 June 30th, 2013

Profit (loss) for the year (A) (0.9) (17.2)

Effects with possible future impact on the income statement 18.1 (51.0)

Profit / (loss) on the cash flow hedge 8.14 4.6 5.0

Tax effect 8.14 (1.0) (1.3)

Total profit / (loss) on the cash flow hedge 8.14 3.5 3.7

Total profit / (loss) arising from the translation of foreign operations 8.14 14.6 (54.6)

Effects that do not have future impact on the income statement (0.9) 2.2

Profit / (loss) from the effects of remeasurement 8.14 (1.4) 3.3

Tax effect 8.14 0.5 (1.1)

Total profit / (loss) from the effects of remeasurement 8.14 (0.9) 2.2

Total other comprehensive income/(loss), net of tax (B) 17.2 (48.8)

Total comprehensive income/(loss) (A+B) 16.2 (66.0)

Attributable to non-controlling interests (0.0) 0.0

Attributable to owners of the Parent 16.2 (66.0)

2014 Half Year Financial Report - Consolidated financial statements

28

Consolidated balance sheet as of 30 June 201411

(million euro) Note June 30th, 2014 Dec. 31st, 2013 June 30th, 2013

Assets

Property, plant and equipment 8.8 594.6 615.4 624.4

Goodwill and other intangible assets with an indefinite

useful life8.9 249.6 240.1 233.6

Other intangible assets with a finite useful life 8.10 96.0 98.7 98.3

Investments in associates 0.5 0.5 0.5

Other non-current assets 2.2 2.3 1.5

Deferred tax assets 133.0 129.5 116.8

Other non-current financial assets 8.15.5 2.0 1.9 1.9

Total non-current assets 1,077.9 1,088.3 1,077.0

Inventories 8.11 378.4 302.4 403.0

Trade receivables 8.12 490.2 426.5 529.2

Current financial assets 8.15.1 11.0 17.9 31.2

Tax receivables 17.5 14.1 14.8

Other receivables and current assets 8.13 87.2 63.2 75.1

Cash and cash equivalents 8.15.2 125.0 330.8 197.9

Assets held for sale - 2.1 2.9

Total current assets 1,109.2 1,157.0 1,254.1

Total assets 2,187.1 2,245.4 2,331.2

Equity

Share capital 8.14 92.9 92.8 92.8

Reserves 8.14 (173.8) (190.9) (162.6)

Retained earnings 8.14 563.4 560.2 558.9

Profit attributable to owners of the Parent 8.14 (0.9) 3.2 (17.2)

Equity attributable to owners of the Parent 481.5 465.3 471.9

Non-controlling interests 0.0 0.0 0.0

Total equity 481.5 465.3 471.9

Liabilities

Medium and long-term loans and borrowings 8.15.4 340.8 368.6 518.4

Employee benefits 8.16 79.5 81.0 72.3

Provisions for risks and charges 8.17 59.0 56.7 54.8

Deferred tax liabilities 41.1 30.5 32.3

Other non-current liabilities 8.18 17.8 22.6 24.9

Total non-current liabilities 538.3 559.5 702.7

Banks and other short-term loans and borrowings 8.15.3 294.8 307.4 232.5

Provisions for risks and charges 8.17 48.8 52.3 52.7

Trade payables 709.2 738.9 735.1

Tax payables 10.5 25.3 23.7

Other payables 8.19 104.1 96.8 112.6

Total current liabilities 1,167.4 1,220.6 1,156.6

Total liabilities 1,705.7 1,780.1 1,859.2

Total equity and liabilities 2,187.1 2,245.4 2,331.2

11

Pursuant to Consob Resolution no. 15519 dated 27 July 2006, the effects of related-party transactions on the

separate statement of financial position are reported in Attachment 4 and in note 10.

2014 Half Year Financial Report - Consolidated financial statements

29

Consolidated Cash Flow Statement for the period ended 30 June 201412

(million euro) Note June 30th, 2014 Dec. 31st, 2013 June 30th, 2013

Profit for the year 8.20 (0.9) 3.2 (17.2)

Income taxes 8.20 4.5 13.7 8.8

Depreciation and amortisation 8.20 50.5 110.3 54.5

Other non-monetary income and expenses, net 8.21 27.2 10.7 18.5

Change in trade receivables 8.22 (63.7) 38.8 (63.9)

Change in inventories 8.22 (76.0) 29.4 (71.2)

Change in trade payables 8.22 (11.3) (81.8) (68.6)

Change in other assets and liabilities 8.23 (21.7) (26.9) (11.4)

Taxes paid 8.20 (12.1) (18.4) (10.6)

Interest paid 8.21 (32.9) (27.7) (14.2)

Interest received 8.21 11.5 12.5 6.1

Cash flows from/(used in) operating activities (124.7) 63.8 (169.2)

Acquisition of property, plant and equipment 8.24 (34.6) (82.7) (61.2)

Proceeds from sale of property, plant and equipment 8.24 0.1 1.4 1.3

Acquisition of intangible assets 8.25 (12.9) (31.0) (14.1)

Proceeds from sale of intangible assets 8.25 0.0 0.0 0.5

Cash flows from/(used in) investing activities (47.4) (112.3) (73.6)

Increase in share capital - - -

Dividends paid 8.26 (0.0) (20.6) (20.6)

New medium/long-term financial liabilities - - -

Repayments of medium/long-term financial liabilities and bond issue 8.27 (6.4) (14.1) (6.4)

Change in short, medium and long-term financial liabilities 8.28 (27.2) 271.1 324.9

Cash flows from/(used in) financing activities (33.6) 236.4 298.0

Net cash flows from/(used in) (205.7) 188.0 55.1

Cash and cash equivalents, start of year 8.15.2 330.8 142.8 142.8

Cash and cash equivalents, end of year 8.15.2 125.0 330.8 197.9

Total change in cash and cash equivalents (205.7) 188.0 55.1

12

Pursuant to Consob Resolution no. 15519 dated 27 July 2006, the financial effects of related-party transactions

are reported in note 10. In addition, the financial effects of non-recurring transactions are described in note 8.5.

2014 Half Year Financial Report - Consolidated financial statements

30

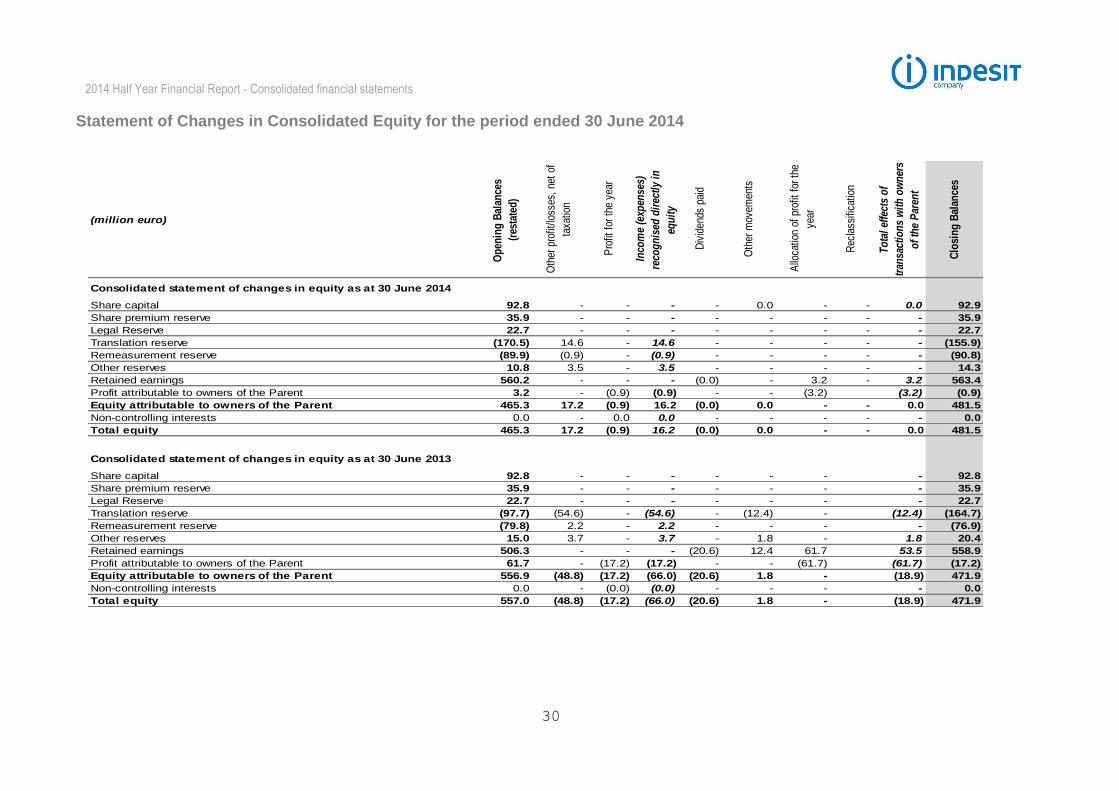

Statement of Changes in Consolidated Equity for the period ended 30 June 2014

(million euro)

Op

enin

g B

alan

ces

(res

tate

d)

Oth

er p

rofit

/loss

es,

net

of

taxa

tion

Pro

fit f

or t

he y

ear

Inco

me

(exp

ense

s)

reco

gn

ised

dir

ectl

y in

equ

ity

Div

iden

ds p

aid

Oth

er m

ovem

ents

Allo

catio

n of

pro

fit f

or t

he

year

Rec

lass

ifica

tion

To

tal

effe

cts

of

tran

sact

ion

s w

ith

ow

ner

s

of

the

Par

ent

Clo

sin

g B

alan

ces

Consolidated statement of changes in equity as at 30 June 2014

Share capital 92.8 - - - - 0.0 - - 0.0 92.9

Share premium reserve 35.9 - - - - - - - - 35.9

Legal Reserve 22.7 - - - - - - - - 22.7

Translation reserve (170.5) 14.6 - 14.6 - - - - - (155.9)

Remeasurement reserve (89.9) (0.9) - (0.9) - - - - - (90.8)

Other reserves 10.8 3.5 - 3.5 - - - - - 14.3

Retained earnings 560.2 - - - (0.0) - 3.2 - 3.2 563.4

Profit attributable to owners of the Parent 3.2 - (0.9) (0.9) - - (3.2) (3.2) (0.9)

Equity attributable to owners of the Parent 465.3 17.2 (0.9) 16.2 (0.0) 0.0 - - 0.0 481.5

Non-controlling interests 0.0 - 0.0 0.0 - - - - - 0.0

Total equity 465.3 17.2 (0.9) 16.2 (0.0) 0.0 - - 0.0 481.5

Consolidated statement of changes in equity as at 30 June 2013

Share capital 92.8 - - - - - - - 92.8

Share premium reserve 35.9 - - - - - - - 35.9

Legal Reserve 22.7 - - - - - - - 22.7

Translation reserve (97.7) (54.6) - (54.6) - (12.4) - (12.4) (164.7)

Remeasurement reserve (79.8) 2.2 - 2.2 - - - - (76.9)

Other reserves 15.0 3.7 - 3.7 - 1.8 - 1.8 20.4

Retained earnings 506.3 - - - (20.6) 12.4 61.7 53.5 558.9

Profit attributable to owners of the Parent 61.7 - (17.2) (17.2) - - (61.7) (61.7) (17.2)

Equity attributable to owners of the Parent 556.9 (48.8) (17.2) (66.0) (20.6) 1.8 - (18.9) 471.9

Non-controlling interests 0.0 - (0.0) (0.0) - - - - 0.0

Total equity 557.0 (48.8) (17.2) (66.0) (20.6) 1.8 - (18.9) 471.9

2014 Half Year Financial Report – Explanatory notes

31

Explanatory notes

2014 Half Year Financial Report – Explanatory notes

32

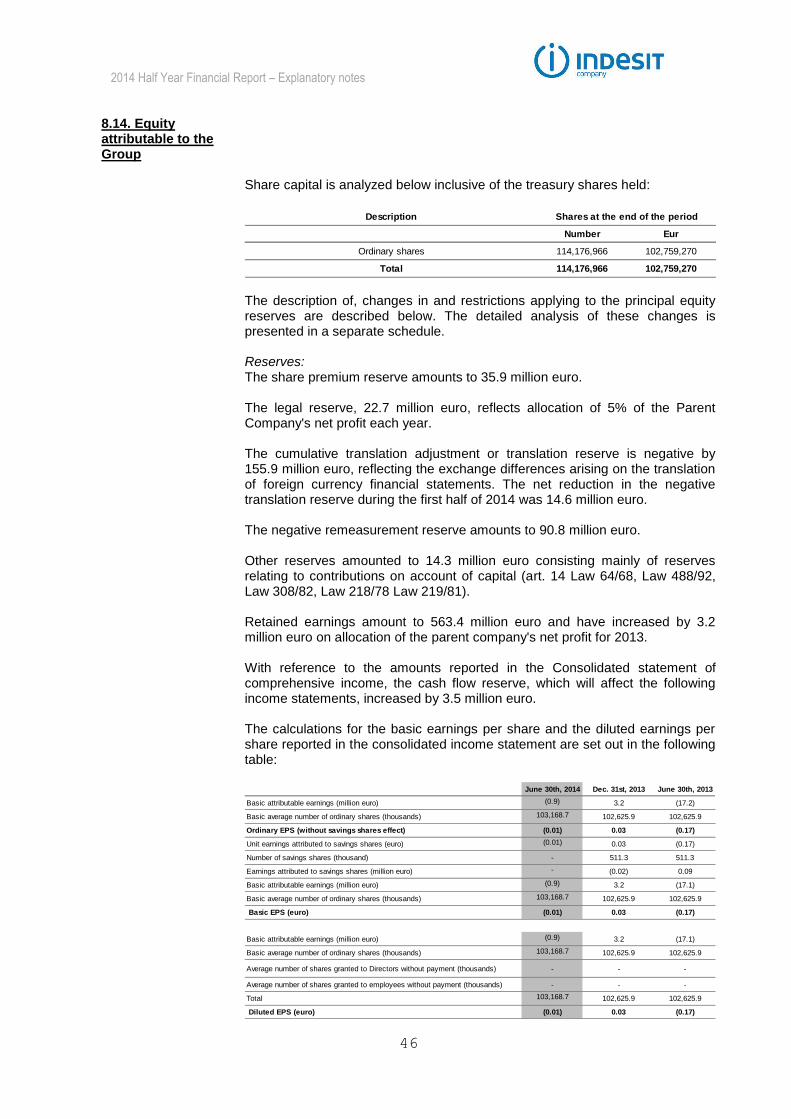

1. Group structure and activities

Indesit Company is a Group led by Indesit Company S.p.A., an Italian company based in Fabriano (Italy) that is listed on the Milan Stock Exchange. The Group is active in the production and sale of white goods, namely household appliances for the cooking sector (cookers, ovens and hobs), the cooling sector (refrigerators and freezers), and the washing sector (washing machines, combined washer-dryers, dryers and dishwashers). From 2013, the Group also sells small domestic appliances. Indesit identifies the Group as its sole operating segment pursuant to IFRS 8. Consistent with para. 33 of IFRS 8, information is provided about the geographical areas in which the Group operates. It should be noted that due to the cyclical nature of the Household Appliance sector, revenues and operating profit are higher in the second half of the year.

2. Approval of the consolidated Half year financial report at 30 June 2014

The consolidated Half year financial report at 30 June 2014 was approved by the Board of Directors on 30 July 2014. The attached condensed interim consolidated financial statements have been subjected to a limited examination by the auditing firm.

3. Declaration of compliance with international accounting standards and basis of presentation

These condensed interim consolidated financial statements have been prepared in compliance with IAS 34 and the requirements of art.154-ter of Decree 58 dated 24 February 1998 (Consolidated Finance Law) and subsequent amendments. They do not include all the information required for annual financial statements and should be read together with the consolidated financial statements as of 31 December 2013. In particular, the income statement, the statement of comprehensive income, the statement of financial position, the cash flow statement and the statement of changes in equity are presented in extended form, using the formats adopted for the consolidated financial statements at 31 December 2013. On the other hand, the following notes are presented in summary form and, accordingly, do not include all the information required for annual financial statements. In particular, as envisaged by IAS 34 in order to avoid repeating the information already published, the explanatory notes relate solely to those elements of the income statement, the statement of comprehensive income, the statement of financial position, the cash flow statement and the statement of changes in equity whose content or change, in terms of nature or amount or because unusual, must be known in order to understand the economic and financial position of the Group. The condensed interim consolidated financial statements at 30 June 2014 comprise the income statement, the statement of comprehensive income, the

2014 Half Year Financial Report – Explanatory notes

33

statement of financial position, the cash flow statement, the statement of changes in equity and these notes. The comparative figures presented in the statement of financial position and the cash flow statement include those at 30 June 2013 for the statement of financial position and at 31 December 2013 for the cash flow statement, together with those required by IAS 34 (31 December 2013 for the statement of financial position and 30 June 2013 for the cash flow statement). This decision was made to permit the consistent comparison of data that is significantly affected by the seasonality of the sector. The income statement presents figures for the first half of 2014 and the first half of 2013, since the Group has adopted the six-month period for interim reference purposes. The consolidated income statement is classified with reference to the reasons for which costs were incurred, the statement of financial position distinguishes between current and non-current assets and liabilities, the cash flow statement is presented using the indirect method, and the Statement of Changes in Equity format has been adopted. In addition, a separate consolidated statement of comprehensive income is presented. This statement comprises the various components forming the results for the period, together with the income and charges deriving from transactions not carried out with owners that were recognized directly in equity. The transactions carried out with owners are presented in the statement of changes in equity, together with the equity transactions reported in the statement of comprehensive income. The format adopted for the classification of the consolidated income statement was chosen to help the market understand more clearly the profitability of the Group; in particular, performance can be measured better with reference to the profit and cost centers used for the allocation of income and expenses. Additionally, this format assures the provision of precise segment information that is consistent with the way results are normally measured for management accounting purposes. This approach also ensures greater comparability with direct competitors and the multinationals operating in related sectors, since classification of the income statement by purpose is the format most widely used in international practice. In addition, the notes provide information on the nature of expenditure and the other disclosures necessary for the market, investors and all stakeholders. With reference to the calculation of taxes in interim financial statements, the Group uses the criterion of calculation according to the effective year to date as the best estimate of the actual annual taxation.

4. Accounting policies 4.1 Basis of preparation and accounting policies adopted

The consolidation principles and measurement criteria are consistent with those reported in the consolidated financial statements at 31 December 2013.

Basis of preparation The currency of presentation of the condensed interim consolidated financial statements is the euro, and the financial statement balances are expressed in millions of euro (except where stated otherwise). The condensed interim consolidated financial statements are prepared on an historical cost basis, except for derivative financial instruments, financial assets held for sale and financial instruments classified as available for sale, which are stated at their fair value. They also presume business continuity, which the Group believes to be reasonably certain. The accounting policies are applied on a consistent basis by all Group

2014 Half Year Financial Report – Explanatory notes

34

companies. There are no financial assets held to maturity. Financial transactions are recorded with reference to the trade date. The accounting policies adopted for the preparation of the condensed interim consolidated financial statements at 30 June 2014 have also been applied on a consistent basis to all the comparative financial information.

Accounting estimates

The preparation of the condensed interim consolidated financial statements involves making assumptions and estimates that affect the value of assets and liabilities and the related explanatory information, as well as the value of contingent assets and liabilities at the reporting date. These estimates are used to measure the property, plant and equipment and intangible assets subject to impairment, as well as to recognize provisions for doubtful accounts, inventory obsolescence, depreciation and amortization and the write-down of assets, employee benefits, taxation, and risks and charges. The estimates and underlying assumptions are based on historical experience and various other factors believed reasonable at the time. Estimates and assumptions are reviewed regularly and, if later estimates differ from those made initially, the effects - which obviously cannot be estimated or forecast at this time - are immediately reflected in the income statement. If the changes in estimate relate to both the current and future periods, their effects are reflected in the income statements for the periods concerned.

4.2 Amendments and revised accounting standards applied for the first time by the Group

Investment entities - Amendments to IFRS 10, IFRS 12 and IAS 27

These amendments provide an exception to the consolidation for entities that fall within the definition of investment entities pursuant to IFRS 10 - Consolidated Financial Statements. This exception to the consolidation requires that the investment entities evaluate subsidiaries at their fair value acknowledged in the income statement. These amendments have had no impact on the Group. Offsetting financial assets and financial liabilities - Amendments to IAS 32 These amendments clarify the meaning of "currently has a legally enforceable right to compensate" and the criterion of compensation in the case of settlement systems (such as central clearing houses) which apply non-simultaneous gross settlement mechanisms. These amendments have had no effect on the financial statements of the Group. Novation of derivatives and continuation of hedge accounting - Amendments to IAS 39 These amendments allow the continuation of hedge accounting when the novation of a hedge derivative meets certain criteria. These amendments have had no impact as the Group has not replaced its derivatives either in the current year or in prior years. IFRIC 21 Taxes IFRIC 21 is effective for annual periods beginning on or after 1 January 2014 and applies retrospectively. It is applicable to all payments imposed by law by the Government other than those already covered by other standards (eg IAS 12 income taxes) and those for fines or other penalties for breaches of the law. The interpretation clarifies that an entity recognizes a liability at the earliest

2014 Half Year Financial Report – Explanatory notes

35

upon occurrence of the event that is related to the payment, in accordance with applicable law. The interpretation also clarifies that the liability matures gradually only if the event to which the payment is related occurs over a period of time provided for by the law. For payments that are due only on exceeding a certain minimum threshold, the liability is recorded only on reaching this threshold. The interpretation requires these principles to be applied also to interim financial statements. Additional information on the recoverable value of non-financial assets - Amendments to IAS 36 These amendments remove the consequences inadvertently introduced by IFRS 13 about the disclosures required by IAS 36. Moreover, these changes require information on the recoverable amount of the asset or CGU to which was recognized during the year or "reversed" impairment (impairment losses).

5. Reclassifications

In 2013, the current and the non-current portions of the tax credits relating to the Polish Special Economic Zone (incentives for the construction of factories) have been reallocated among the deferred tax assets, with an according reclassification of the opening financial position. It should also be noted that, in order to provide a better economic representation, the costs of installation and the special consumption tax referring to the turkish market have been reclassified within the income statement. The increase in sales and cost of sales for the SCT, in relation to the first two quarters of 2013, respectively, equal to 1.4 million euro and 2.0 million euro. The decrease in cost of sales and the increase in selling and distribution expenses for the cost of installation, in relation to the first two quarters of 2013 amounted respectively to 0.5 million euro and 0.8 million euro.

6. Changes in the scope of consolidation

Except for the above, there were no other changes in the scope of consolidation during the first semester.

2014 Half Year Financial Report – Explanatory notes

36

7. Operating segments

Indesit Company identifies the Group as its sole operating segment. Consistent with IFRS 8 para. 33, the following information is provided about the geographical areas in which the Group operates: Western Europe Area

13;

Eastern Europe Area

14;

International Area

15.

Segment revenue is calculated based on the final destination of the products and segment results take account of all expenses that can be directly allocated to the geographical areas concerned. The costs not allocated to geographical areas include non-recurring industrial charges and corporate costs. Similarly, financial income and expenses and taxation are not allocated to the various geographical areas. Except for trade receivables, assets, liabilities and investments are not allocated to geographical areas and are examined by senior management on a combined basis. The trade receivables allocated to geographical areas and reviewed by the most senior decision makers comprise those deriving from the sale of finished products. They do not include receivables deriving from the provision of services (with the exception of UK service activities), advances to suppliers or the effects of any disposals of receivables. The following tables present the Group's operating information analyzed by geographical area based on the final destination of the products.

Analysis by operating segment at 30 June 2014

June 30th, 2014 Western Europe Eastern Europe InternationalCosts not

allocated

Total(million euro)

Total revenue 718.7 384.7 80.9 0.0 1,184.2

Cost of sales (525.6) (304.1) (60.5) (3.0) (893.2)

Selling and distribution expenses (129.6) (56.5) (7.8) (15.4) (209.3)

General and administrative expenses (15.0) (8.1) (0.7) (24.4) (48.3)

Operative costs (670.3) (368.8) (69.0) (42.8) (1,150.8)

Operating Profit 48.4 15.9 11.9 (42.8) 33.5

Interest expenses (12.8)

Interest income (14.9)

Exchange rate differences and other net financial expenses (2.2)

Share of profit (losses) of associates 0.0

Income taxes (4.5)

Profit attribuable to owners of the company (0.9)

13 This includes: Italy, the UK and Ireland, France, the Netherlands, Spain, Portugal, Germany, Austria, Switzerland, Benelux, Scandinavia. 14 This includes: Russia and the Asian Republics, Belarus, Kazakhstan, Poland, Ukraine, Moldova, Czech Republic,

Hungary, Romania, Greece, the Baltic States, Caucasian Republics, Slovak Republic, Turkey, Bulgaria and the Balkans.

15 This includes all other non-European markets.

2014 Half Year Financial Report – Explanatory notes

37

Analysis by operating segment at 30 June 2013

June 30th, 2013 Western Europe Eastern Europe InternationalCosts not

allocated

Total(million euro)

Total revenue 713.8 457.2 77.1 0.0 1,248.1

Cost of sales (539.6) (362.1) (58.2) 5.9 (954.0)

Selling and distribution expenses (127.1) (66.6) (9.5) (15.1) (218.4)

General and administrative expenses (15.5) (9.2) (0.6) (35.6) (60.9)

Operative costs (682.2) (437.9) (68.3) (44.9) (1,233.3)

Operating Profit 31.5 19.4 8.5 (44.9) 14.7

Interest expenses (12.7)

Interest income (8.2)

Exchange rate differences and other net financial expenses (2.3)

Share of profit (losses) of associates 0.0

Income taxes (8.8)

Profit attribuable to owners of the company (17.2)

Trade receivables analyzed by operating segment

(million euro)

June 30th, 2014

% of rolling

sales (12

months)

Dec. 31st, 2013

% of rolling

sales (12

months)June 30th, 2013

% of rolling

sales (12

months)

Western Europe 224.0 8.6% 218.5 8.2% 223.4 7.9%

Eastern Europe 197.0 7.6% 157.0 5.9% 217.9 7.7%

International 32.6 1.3% 19.0 0.7% 30.9 1.1%

Not allocated trade receivables 36.5 - 32.0 - 57.0 -

Total 490.2 18.8% 426.5 15.6% 529.2 18.7%

2014 Half Year Financial Report – Explanatory notes

38

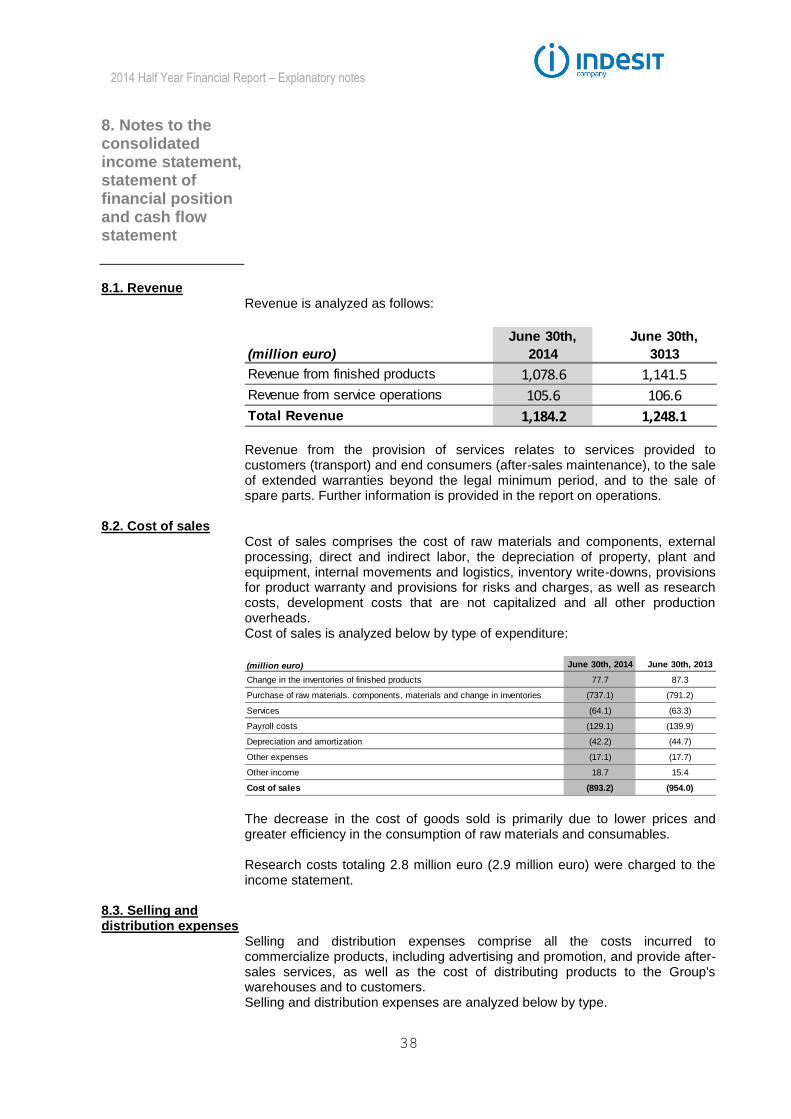

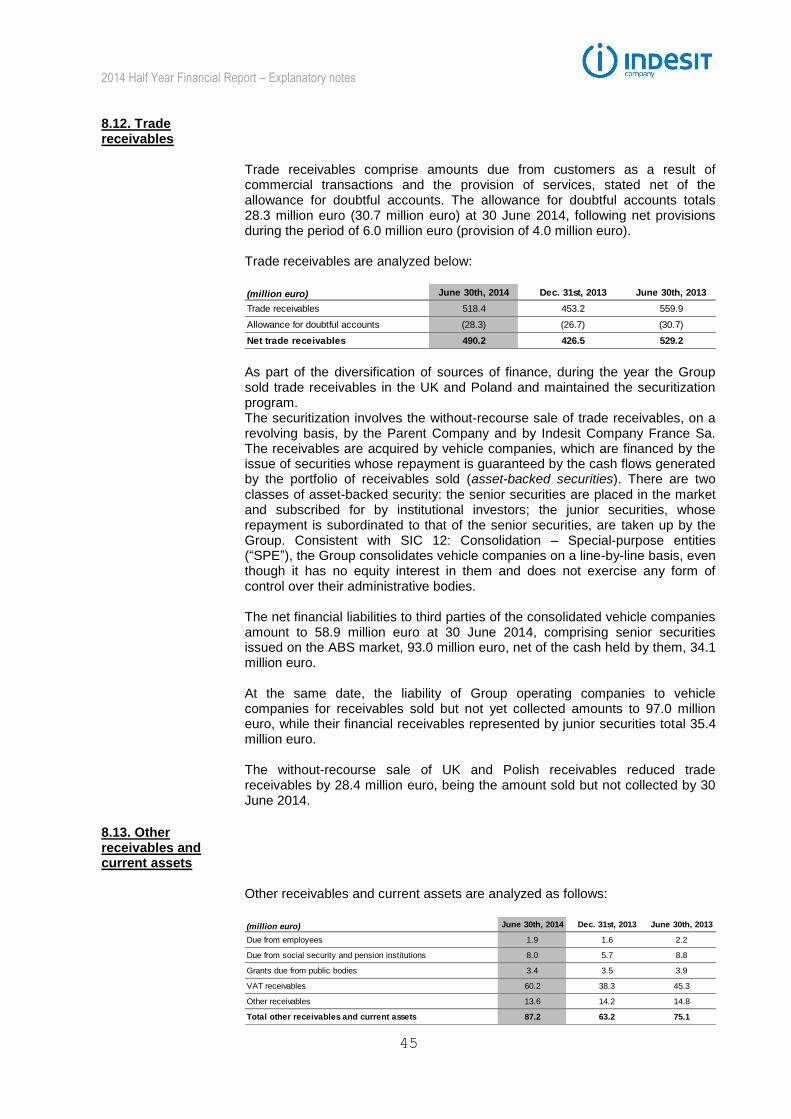

8. Notes to the consolidated income statement, statement of financial position and cash flow statement 8.1. Revenue

Revenue is analyzed as follows:

(million euro)

June 30th,

2014

June 30th,

3013

Revenue from finished products 1,078.6 1,141.5

Revenue from service operations 105.6 106.6

Total Revenue 1,184.2 1,248.1 Revenue from the provision of services relates to services provided to customers (transport) and end consumers (after-sales maintenance), to the sale of extended warranties beyond the legal minimum period, and to the sale of spare parts. Further information is provided in the report on operations.

8.2. Cost of sales Cost of sales comprises the cost of raw materials and components, external processing, direct and indirect labor, the depreciation of property, plant and equipment, internal movements and logistics, inventory write-downs, provisions for product warranty and provisions for risks and charges, as well as research costs, development costs that are not capitalized and all other production overheads. Cost of sales is analyzed below by type of expenditure:

(million euro) June 30th, 2014 June 30th, 2013

Change in the inventories of finished products 77.7 87.3

Purchase of raw materials. components, materials and change in inventories (737.1) (791.2)

Services (64.1) (63.3)

Payroll costs (129.1) (139.9)

Depreciation and amortization (42.2) (44.7)

Other expenses (17.1) (17.7)

Other income 18.7 15.4

Cost of sales (893.2) (954.0) The decrease in the cost of goods sold is primarily due to lower prices and greater efficiency in the consumption of raw materials and consumables. Research costs totaling 2.8 million euro (2.9 million euro) were charged to the income statement.

8.3. Selling and distribution expenses

Selling and distribution expenses comprise all the costs incurred to commercialize products, including advertising and promotion, and provide after-sales services, as well as the cost of distributing products to the Group's warehouses and to customers. Selling and distribution expenses are analyzed below by type.

2014 Half Year Financial Report – Explanatory notes

39

(million euro) June 30th, 2014 June 30th, 2013

Change in the inventories of finished products 0.4 (0.0)

Purchase of raw materials. components, materials and change in inventories (2.9) (3.1)

Services (141.7) (143.9)

Payroll costs (54.1) (56.6)

Depreciation and amortization (3.1) (3.7)

Other expenses (11.2) (12.8)

Other income 3.2 1.8

Selling and distribution expenses (209.3) (218.4)

Selling expenses decreased slightly during the half. 8.4. General and administrative expenses

General and administrative expenses include all general management and administrative costs, and all expenditure not directly attributable to production or sales units or to research and development. General and administrative expenses are analyzed below by type:

(million euro) June 30th, 2014 June 30th, 2013

Purchase of raw materials. components, materials and change in inventories (0.1) 0.0

Services (21.9) (22.7)

Payroll costs (24.5) (22.2)

Depreciation and amortization (5.3) (6.1)

Other expenses (5.2) (19.2)

Other income 8.7 9.2

General and administrative expenses (48.3) (60.9) Other costs have decreased by 14.0 million euro as a consequence of the lower redundancy expenses incurred compared to 2013.

8.5. Operating profit Operating profit is analyzed below by type of cost:

(million euro) June 30th, 2014 June 30th, 2013

Revenue 1,184.2 1,248.1

Change in the inventories of finished products 78.1 87.3

Purchase of raw materials. components, materials and change in inventories (740.1) (794.3)

Services (227.8) (230.0)

Payroll costs (207.6) (218.7)

Depreciation and amortization (50.5) (54.5)

Other income and expenses (2.8) (23.2)

Operating profit 33.5 14.7

Operating profit is analyzed further in the Report on operations. The number of employees at 30 June 2014 is 15,451 (16,270). As required by Consob Communication DEM/6064293 dated 28 July 2006, non-operating income and expenses are detailed in the following table. They mainly comprise restructuring charges.

2014 Half Year Financial Report – Explanatory notes

40

(million euro)

Cost of sales

Selling and

distribution

expenses

General and

administrative

expenses

June 30th, 2014

Restructuring expenses (0.6) (0.4) (0.5) (1.5)

Other non-recurring income and expenses 0.3 (0.0) (0.0) 0.2

Total non-recurring income and expenses (0.3) (0.4) (0.5) (1.3)

(million euro)

Cost of sales

Selling and

distribution

expenses

General and

administrative

expenses

June 30th, 2013

Restructuring expenses (0.3) (1.7) (12.9) (14.9)

Other non-recurring income and expenses (0.9) 0.0 5.3 4.4

Total non-recurring income and expenses (1.3) (1.7) (7.6) (10.5) Total payables and provisions for non-recurring transactions at 30 June 2014 amount to 16.3 million euro (25.5 million euro) and the cash flow effect was 1.1 million euro (absorption of 12.6 million euro).

8.6. Net interest, commissions, exchange differences and other financial expenses and share of profit/loss of associates and others

Interest expense comprises:

(million euro) June 30th, 2014 June 30th, 2013

Bond interests (8.3) (3.3)

Interest on medium-and long-term bank loans (0.4) (0.4)

Interest on short–term bank, loan and borrowings (3.9) (5.6)

Other interest expenses (2.0) (2.1)

Mark–to–market derivatives related to loans 0.4 (0.9)

Interest expenses on TFR and pension fund UK (1.4) (1.2)

Interest expenses (15.6) (13.6) Interest expense is primarily in line with 2013, recording higher USPP interest in relation to its early settlement and recording lower costs relating to derivatives for hedging the risk associated with interest rates. Interest income is analyzed below:

(million euro) June 30th, 2014 June 30th, 2013

Interest income on deposits 2.8 0.9

Interest income on pension fund UK 0.0 0.0

Interest income 2.8 0.9 Exchange differences are analyzed as follows:

(million euro) June 30th, 2014 June 30th, 2013

Net realised exchange rate differences (13.0) (6.6)

Net unrealised exchange rate differences (1.9) (1.6)

Exchange rate differences and other financial expenses (14.9) (8.2) The increase in exchange losses was almost entirely due to the unfavorable trend of Ukraine Hryvna. . See note 9 for information about the derivatives outstanding at 30 June 2014. Financial fees were 2.2 million euro (2.3 million euro). In line with 2013.

2014 Half Year Financial Report – Explanatory notes

41

8.7. Income tax Income taxes were 4.5 million euro (8.8 million euro).

8.8. Property, plant and equipment

Property, plant and equipment are analyzed as follows:

(million euro) June 30th, 2014 Dec. 31st, 2013 June 30th, 2013

Land and buildings 228.3 236.7 240.7

Plant and machinery 223.5 240.6 238.2

Industrial and commercial equipment 87.9 96.2 94.6

Assets under construction 34.0 20.4 29.0

Other assets 20.8 21.5 22.0

Total property, plant and equipment 594.6 615.4 624.4 The ownership of property is not restricted by liens and charges.

The change in the historical cost of property, plant and equipment is shown below:

(million euro)Dec. 31st, 2013 Additions Decreases

Exchange rate

differencesReclassifications June 30th, 2014

Land and buildings 369.0 0.9 (0.1) (1.6) (3.0) 365.2

Plant and machinery 732.3 3.7 (12.7) (22.6) 4.3 705.0

Industrial and commercial equipment 432.9 2.7 (5.5) (4.5) 2.6 428.1

Assets under construction 20.4 9.5 - 8.0 (3.9) 34.0

Other assets 91.5 1.2 (0.7) 0.1 0.0 92.2

Total 1,646.1 17.9 (18.9) (20.6) (0.0) 1,624.4

(million euro)Dec. 31st, 2012 Additions Decreases

Exchange rate

differencesReclassifications June 30th, 2013

Land and buildings 406.7 0.2 (1.3) (14.7) (20.2) 370.8

Plant and machinery 738.3 2.6 (0.7) (33.4) 14.6 721.4

Industrial and commercial equipment 418.1 4.2 (1.2) (13.9) 15.7 422.9

Assets under construction 50.1 11.8 - 1.1 (34.0) 29.0

Other assets 93.1 1.3 (1.1) (2.3) 0.7 91.7

Total 1,706.2 20.1 (4.3) (63.2) (23.1) 1,635.7 The changes in the related accumulated depreciation were as follows:

(million euro)

Dec. 31st, 2013

Depreciation

and Impairment

losses

DecreasesExchange rate

differencesReclassifications June 30th, 2014

Land and buildings (132.3) (5.1) 0.1 0.4 (0.0) (136.9)

Plant and machinery (491.7) (16.4) 12.7 14.0 (0.0) (481.5)

Industrial and commercial equipment (336.6) (12.8) 5.3 3.9 0.0 (340.2)

Other assets (70.1) (1.8) 0.7 (0.1) 0.0 (71.3)

Total (1,030.7) (36.2) 18.8 18.2 (0.0) (1,029.9)

(million euro)

Dec. 31st, 2012

Depreciation

and Impairment

losses

DecreasesExchange rate

differencesReclassifications June 30th, 2013

Land and buildings (151.2) (5.6) 0.2 4.3 22.3 (130.1)

Plant and machinery (487.2) (18.0) 0.7 21.4 0.0 (483.2)

Industrial and commercial equipment (324.2) (13.3) 1.2 7.5 0.3 (328.4)

Other assets (70.6) (1.9) 0.9 1.8 0.0 (69.7)

Total (1,033.2) (38.8) 3.0 35.1 22.6 (1,011.3)

The changes in the net carrying amount of property, plant and equipment are summarized in the following table:

2014 Half Year Financial Report – Explanatory notes

42

(million euro)

Dec. 31st, 2013 Additions

Depreciation

and Impairment

losses

DecreasesExchange rate

differencesReclassifications June 30th, 2014

Land and buildings 236.7 0.9 (5.1) - (1.2) (3.0) 228.3

Plant and machinery 240.6 3.7 (16.4) (0.0) (8.6) 4.3 223.5

Industrial and commercial equipment 96.2 2.7 (12.8) (0.1) (0.6) 2.6 87.9

Assets under construction 20.4 9.5 - - 8.0 (3.9) 34.0

Other assets 21.5 1.2 (1.8) (0.0) (0.0) 0.0 20.8

Total 615.6 17.9 (36.2) (0.1) (2.4) (0.0) 594.6

(million euro)

Dec. 31st, 2012 Additions

Depreciation

and Impairment

losses

DecreasesExchange rate

differencesReclassifications June 30th, 2013

Land and buildings 255.5 0.2 (5.6) (1.1) (10.4) 2.1 240.7

Plant and machinery 251.0 2.6 (18.0) 0.0 (12.0) 14.6 238.2

Industrial and commercial equipment 93.9 4.2 (13.3) (0.0) (6.4) 16.0 94.6

Assets under construction 50.1 11.8 - - 1.1 (34.0) 29.0

Other assets 22.5 1.3 (1.9) (0.2) (0.5) 0.7 22.0

Total 673.1 20.1 (38.8) (1.3) (28.1) (0.5) 624.4

The additions to property, plant and equipment principally involved the replacement of plant and investment in new production lines.

8.9. Goodwill and other intangible assets with an indefinite useful life

Goodwill and other intangible assets with an indefinite useful life are analyzed as follows:

(million euro) June 30th, 2014 Dec. 31st, 2013 June 30th, 2013

Goodwill 137.9 132.6 128.9

Brands with an indefinite useful life 111.7 107.6 104.7

Total goodwill and other intangible assets with an indefinite useful life 249.6 240.1 233.6

The changes in the net carrying amount of goodwill and other intangible assets with an indefinite useful life are summarized in the following table:

(million euro)Dec. 31st, 2013 Investments

Exchange rate

differencesJune 30th, 2014

Goodwill 132.6 5.3 137.9

Brands with an indefinite useful life 107.6 4.2 111.7

Total 240.1 - 9.5 249.6

(million euro)Dec. 31st, 2012 Investments

Exchange rate

differencesJune 30th, 2013

Goodwill 135.4 - (6.5) 128.9

Brands with an indefinite useful life 106.8 3.0 (5.1) 104.7

Total 242.2 3.0 (11.6) 233.6

The Hotpoint brand name with an indefinite useful life and the goodwill derive from the purchase of General Domestic Appliances Holding Ltd. It should be noted that 30 June 2014 Indesit has not seen any internal or external trigger events to draw up such that an impairment test on that date.

2014 Half Year Financial Report – Explanatory notes

43

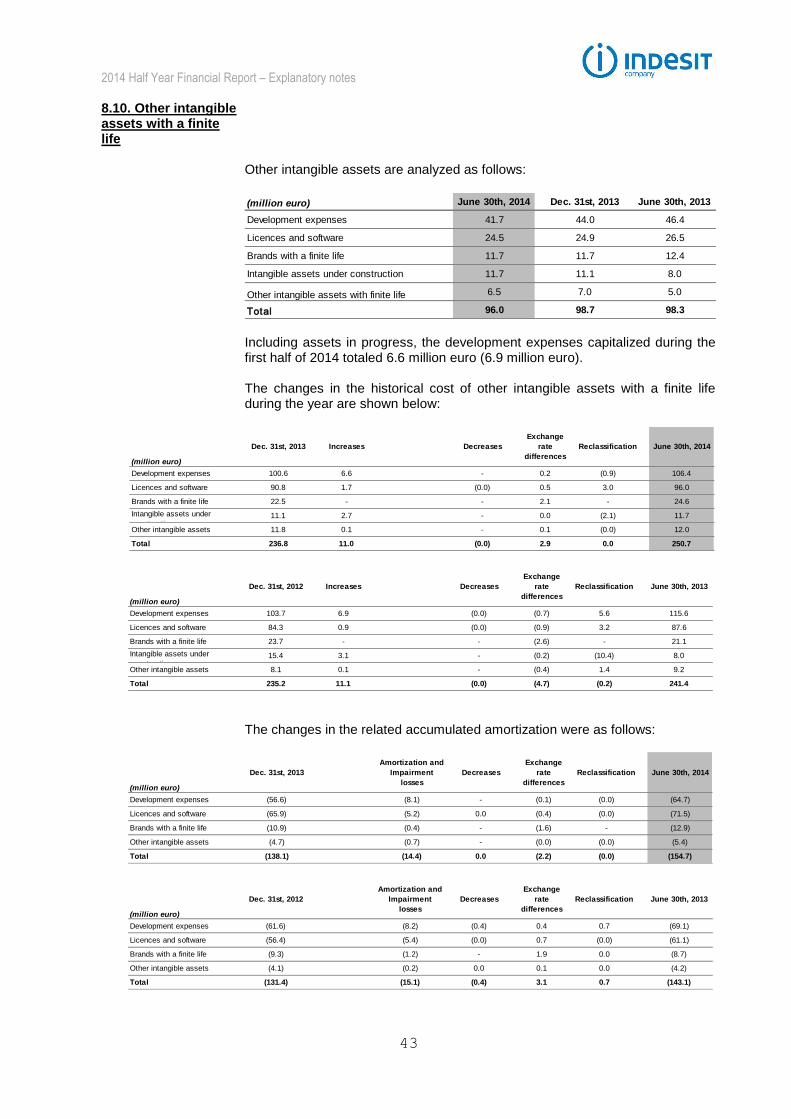

8.10. Other intangible assets with a finite life

Other intangible assets are analyzed as follows:

(million euro) June 30th, 2014 Dec. 31st, 2013 June 30th, 2013

Development expenses 41.7 44.0 46.4

Licences and software 24.5 24.9 26.5

Brands with a finite life 11.7 11.7 12.4

Intangible assets under construction 11.7 11.1 8.0

Other intangible assets with finite life 6.5 7.0 5.0

Total 96.0 98.7 98.3

Including assets in progress, the development expenses capitalized during the first half of 2014 totaled 6.6 million euro (6.9 million euro). The changes in the historical cost of other intangible assets with a finite life during the year are shown below:

(million euro)

Dec. 31st, 2013 Increases Decreases

Exchange

rate

differences

Reclassification June 30th, 2014

Development expenses 100.6 6.6 - 0.2 (0.9) 106.4

Licences and software 90.8 1.7 (0.0) 0.5 3.0 96.0

Brands with a finite life 22.5 - - 2.1 - 24.6

Intangible assets under

construction11.1 2.7 - 0.0 (2.1) 11.7

Other intangible assets 11.8 0.1 - 0.1 (0.0) 12.0

Total 236.8 11.0 (0.0) 2.9 0.0 250.7

(million euro)

Dec. 31st, 2012 Increases Decreases

Exchange

rate

differences

Reclassification June 30th, 2013

Development expenses 103.7 6.9 (0.0) (0.7) 5.6 115.6

Licences and software 84.3 0.9 (0.0) (0.9) 3.2 87.6

Brands with a finite life 23.7 - - (2.6) - 21.1

Intangible assets under

construction15.4 3.1 - (0.2) (10.4) 8.0

Other intangible assets 8.1 0.1 - (0.4) 1.4 9.2

Total 235.2 11.1 (0.0) (4.7) (0.2) 241.4

The changes in the related accumulated amortization were as follows:

(million euro)

Dec. 31st, 2013

Amortization and

Impairment

losses

Decreases

Exchange

rate

differences

Reclassification June 30th, 2014

Development expenses (56.6) (8.1) - (0.1) (0.0) (64.7)

Licences and software (65.9) (5.2) 0.0 (0.4) (0.0) (71.5)

Brands with a finite life (10.9) (0.4) - (1.6) - (12.9)

Other intangible assets (4.7) (0.7) - (0.0) (0.0) (5.4)

Total (138.1) (14.4) 0.0 (2.2) (0.0) (154.7)

(million euro)

Dec. 31st, 2012

Amortization and

Impairment

losses

Decreases

Exchange

rate

differences

Reclassification June 30th, 2013

Development expenses (61.6) (8.2) (0.4) 0.4 0.7 (69.1)

Licences and software (56.4) (5.4) (0.0) 0.7 (0.0) (61.1)

Brands with a finite life (9.3) (1.2) - 1.9 0.0 (8.7)

Other intangible assets (4.1) (0.2) 0.0 0.1 0.0 (4.2)

Total (131.4) (15.1) (0.4) 3.1 0.7 (143.1)

2014 Half Year Financial Report – Explanatory notes

44

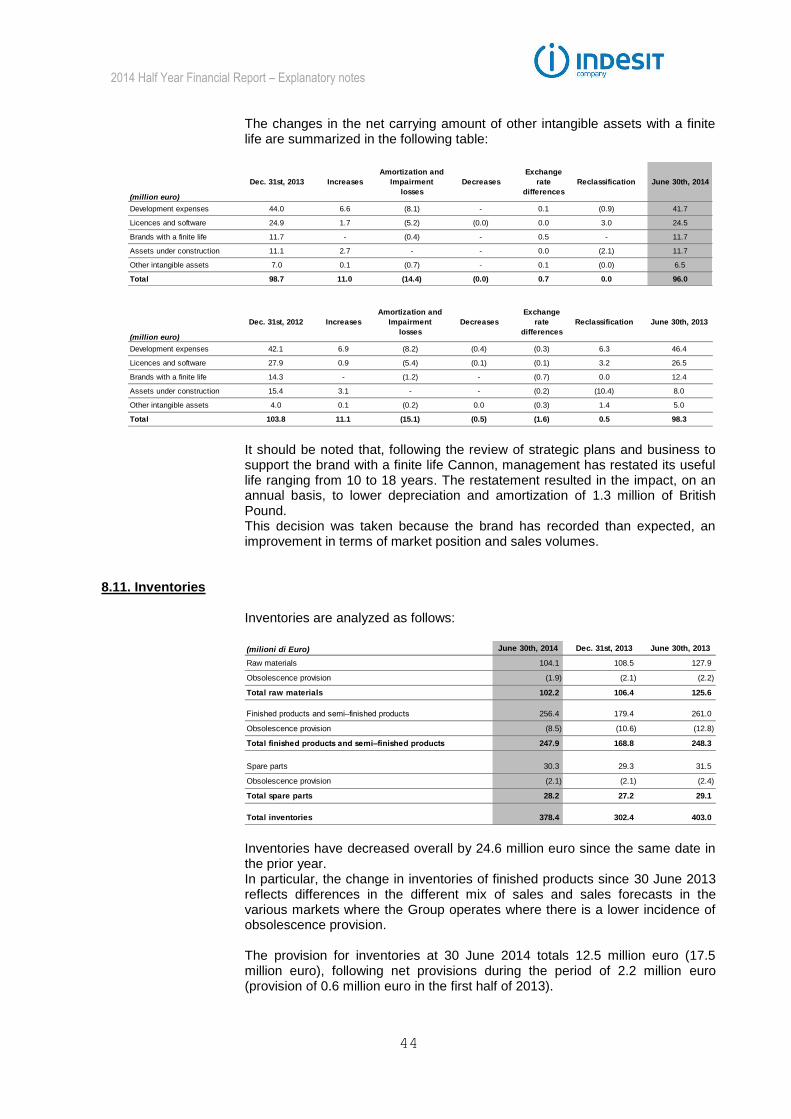

The changes in the net carrying amount of other intangible assets with a finite life are summarized in the following table:

(million euro)

Dec. 31st, 2013 Increases

Amortization and

Impairment

losses

Decreases

Exchange

rate

differences

Reclassification June 30th, 2014

Development expenses 44.0 6.6 (8.1) - 0.1 (0.9) 41.7

Licences and software 24.9 1.7 (5.2) (0.0) 0.0 3.0 24.5

Brands with a finite life 11.7 - (0.4) - 0.5 - 11.7

Assets under construction 11.1 2.7 - - 0.0 (2.1) 11.7

Other intangible assets 7.0 0.1 (0.7) - 0.1 (0.0) 6.5

Total 98.7 11.0 (14.4) (0.0) 0.7 0.0 96.0

(million euro)

Dec. 31st, 2012 Increases

Amortization and

Impairment

losses

Decreases

Exchange

rate

differences

Reclassification June 30th, 2013

Development expenses 42.1 6.9 (8.2) (0.4) (0.3) 6.3 46.4

Licences and software 27.9 0.9 (5.4) (0.1) (0.1) 3.2 26.5

Brands with a finite life 14.3 - (1.2) - (0.7) 0.0 12.4

Assets under construction 15.4 3.1 - - (0.2) (10.4) 8.0

Other intangible assets 4.0 0.1 (0.2) 0.0 (0.3) 1.4 5.0

Total 103.8 11.1 (15.1) (0.5) (1.6) 0.5 98.3