hr/payroll concepts

TRANSCRIPT

HR/Payroll Concepts

November 17, 2021

Session 2 of 3

Friendly Reminders

• Please Mute Audio, Video optional

• Use the Chat Box for Questions

• Q&A to follow

Agenda

• Payroll Deductions• Tax Withholdings• Templates for FIT & SIT Withholdings• Calculate FIT & SIT Withholdings

Three main types of payroll deductionsPayroll Deductions

• Involuntary

• Voluntary

• Statutory

Page 3

Payroll DeductionsVoluntary Deductions

• When an employee chooses – gives written permission to – the district to withhold money for certain purposes

• Written authorization should be received before setting up the deduction

• First to be removed if it causes negative net pay

Page 3

Voluntary

Health FSA

Life Insurance

Dependent Care FSA

Tax Shelter Annuity

403b/457

What are some examples?

Page 3

Payroll DeductionsStatutory Deductions

• Required by Law according to federal and state laws or collective bargaining unit

• Statutory deductions guarantee the employee pays what is owed, whether they want to or not

• Districts do not have the choice of allowing or disallowing statutory deductions

Page 3

Statutory

FIT & SIT

OASDI

MEDICARE

RETIREMENT

What are some examples?

Page 3

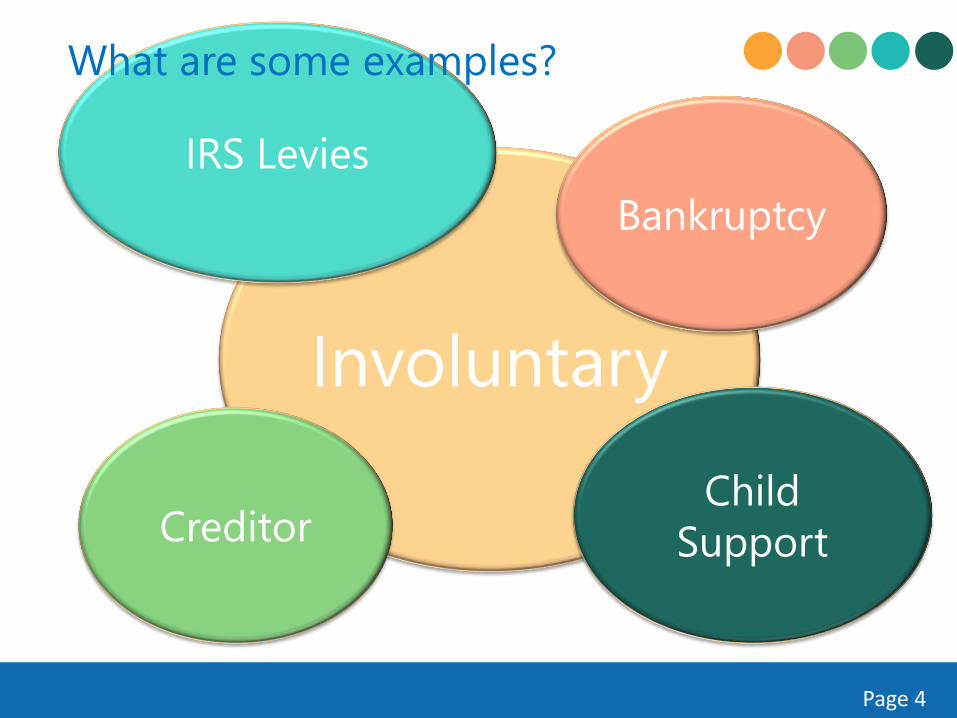

Payroll DeductionsInvoluntary Deductions

• Regulated by state and federal laws in order to deduct and remit monies to various government agencies or authorities in order to satisfy certain types of unpaid debts

• Districts and county offices that do not process the involuntary deductions correctly are liable for any payments due

Page 4

Involuntary

Creditor

Bankruptcy

Child Support

IRS Levies

What are some examples?

Page 4

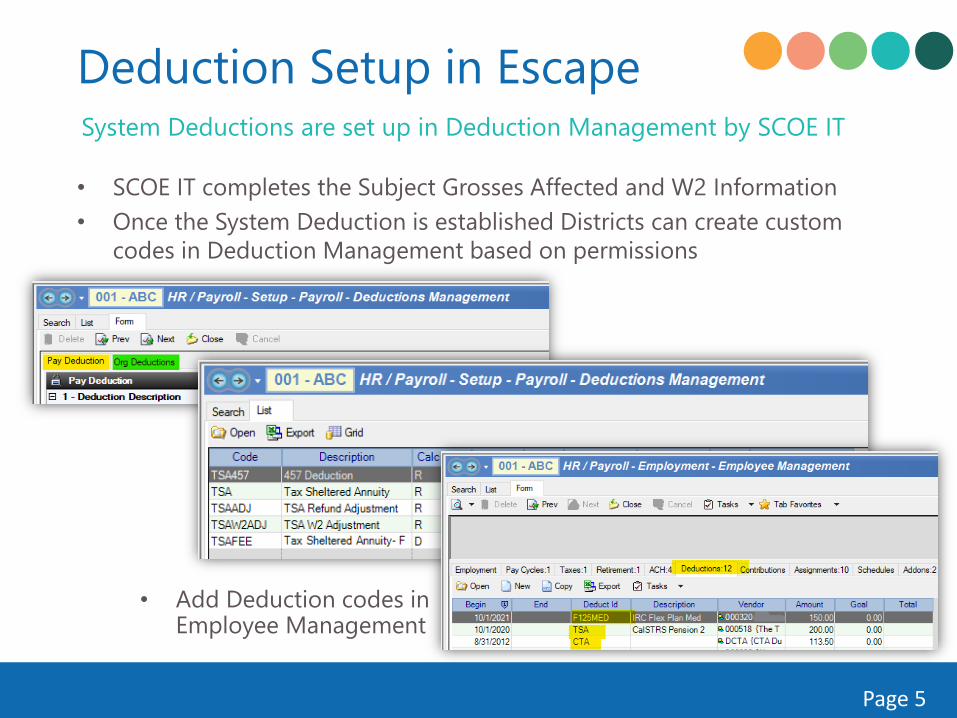

Deduction Setup in EscapeSystem Deductions are set up in Deduction Management by SCOE IT

• SCOE IT completes the Subject Grosses Affected and W2 Information• Once the System Deduction is established Districts can create custom

codes in Deduction Management based on permissions

Page 5

• Add Deduction codes in Employee Management

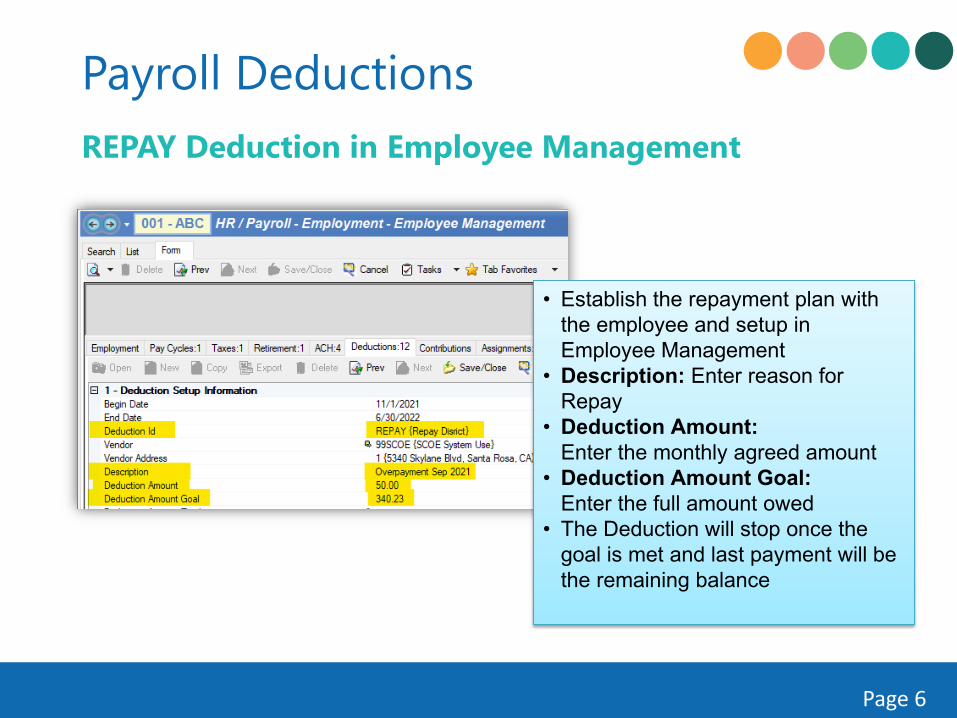

Payroll DeductionsREPAY Deduction

• When an employee owes money to the District

• CA Labor code along with court decisions set the requirements for when an employer can deduct money owed to them through a deduction in the employee’s paycheck. CA Labor Code 224

• Recommended that the District meet and discuss a repayment plan with the employee and obtain written authorization

Page 6

Payroll DeductionsREPAY Deduction in Employee Management

Page 6

• Establish the repayment plan with the employee and setup in Employee Management

• Description: Enter reason for Repay

• Deduction Amount:Enter the monthly agreed amount

• Deduction Amount Goal:Enter the full amount owed

• The Deduction will stop once the goal is met and last payment will be the remaining balance

Income Tax Withholdings

Statutory tax withholdings are mandatory taxes that are contributed by the employee and employer to the taxing agency

Taxes Required Employee Employer

Federal Yes X

State Yes X

Social Security (OASDI) Yes X X

Medicare Yes X X

State Unemployment Ins Yes X

State Disability Ins No X

Income Tax Withholding

Page 7

• Withholdings are reported annually on the W-2 Form

• Districts match Social Security and Medicare Contributions

• Districts are responsible for State Unemployment Insurance

• Districts are not required to participate in State Disability Insurance

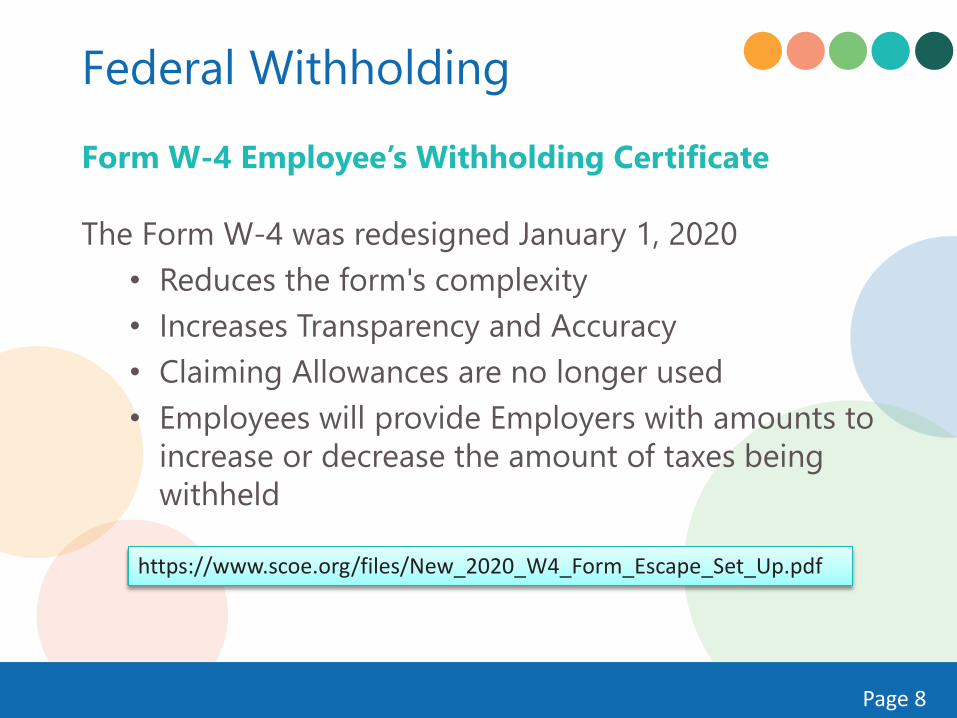

Form W-4 Employee’s Withholding Certificate

The Form W-4 was redesigned January 1, 2020• Reduces the form's complexity• Increases Transparency and Accuracy• Claiming Allowances are no longer used• Employees will provide Employers with amounts to

increase or decrease the amount of taxes being withheld

Federal Withholding

Page 8

https://www.scoe.org/files/New_2020_W4_Form_Escape_Set_Up.pdf

Form W-4• Form W-4 continuing employee received prior to

January 1, 2020 will remain in effect until a new form is received

• New employees must use the current 2021 Form• Effective with employee’s first pay period• Employers responsibility not to accept and withhold

on invalid Forms W-4

Federal Withholdings

https://www.irs.gov/pub/irs-pdf/fw4.pdf

Page 8

Step 1: RequiredEmployees: name, address, social security number, and filing status

Important Reminder: Do NOT provide tax

advice. Recommend they seek advice from the IRS

or their Tax Advisor.

Steps 2, 3, and/or 4: Only if relevant to the employees personal situation

Step 5: RequiredThe form is invalid if not signed and dated by the employee

If a new employees fails to furnish a Form W-4 will be treated as if they had checked the box for:

Single or Married filing separately in Step 1(c) and made no entries in Step 2, Step 3, or Step 4 of the W-4

Employee Fails to Furnish W-4 Form

Page 10

The W-4 Form no longer has check box for Exempt

Employees can write “Exempt” on Form W-4 in the space below Step 4(c) shall have no federal income tax withheld from their earnings

Withholdings Exemption

Page 10

When Claiming Exempt a new form must be submitted each year by February 15

Lock-In Letter• IRS Notice to the Employer• Employee must challenge at IRS• Disregard new W-4 until new letter• Applies to DE-4 CA State Withholdings

“Employee Notice” from IRS • Send to employee within 10 days of receipt• Notify IRS in writing if no longer an employee

Withholdings

Page 11

OASDI (Old Age Survivor Disability Insurance• If an employee qualifies for Social Security, they

must also pay into Medicare• All employees who are not participating in a

qualified retirement system are subject to Social Security and Medicare (Non-Members)

• Exception for employees hired prior to 1986 who made a one-time election to be exempt from MC

Social Security & Medicare

Page 13

• CalPERS Members are subject to both• CalSTRS Members only subject to Medicare

Voluntary Section 218 Agreement

• A written voluntary agreement between the State and Social Security Administration to provide Social Security and Medicare coverage for state and local government employees

• Section 218 Agreements are irrevocable• CalPERS is the State Social Security Administrator for

School Employees

Social Security (OASDI)

Page 13

COBRA 1986 Medicare• Mandated Mandatory Medicare coverage if hired

after March 31,1986• Retiree returning to work, mandatory Medicare• PERS/STRS, mandatory Medicare coverage• No PERS, No Social Security, mandatory Medicare

Rehire Annuitant

Page 13

Retirees

• Subject to Medicare tax withholding regardless of Age OR if they were exempt before they retired

• Applies even if they are eligible to receive Medicare• OBRA 90 specifically excludes a qualified member

from mandatory social security if they are rehired with an employer that participates in the same retirement plan from which they retired

Rehire Annuitant

Page 14

Student Workers• Exempt from Social Security/Medicare if their

services are performed in an educational institution where they are enrolled and attending classes

• Summer work is subject to SS/MC when not enrolled in classes

Social Security/Medicare

Page 14

SSA 1945 FormSocial Security Administration

• Districts must provide a statement to new employees (except students) hired in a job that is not covered by Social Security

• Best practice include this form in the new hire information

https://www.socialsecurity.gov/forms/ssa-1945.pdf

Page 14

DE-4 Form Employee’s Withholding Allowance Certificate

• Form must be submitted, can no longer use W-4 for both

• If an employee claims Exempt, then a new form must be submitted each year by February 15 and must claim exempt on W-4

• An employee can file a new form anytime with the most current being the one in effect until a new form is submitted

• IRS Lock-In Letter applies to CA DE-4

CA State Withholding

Page 15

https://www.edd.ca.gov/pdf_pub_ctr/de4.pdf

CA State Withholding DE-4 Form

Page 15

Important Reminder: Do NOT provide tax

advice. Recommend they seek advice from the IRS

or their Tax Advisor.

CA State Withholding DE-4 Form

Page 15https://www.scoe.org/files/Military_EDD_Exemption_2020.pdf

Military Spouse not

subject to CA Withholdings

Additional steps needed

The California Unemployment Insurance is an employer paid tax and the rate is set annually through the School Employers Fund

• Paid by Employer • Schools do not pay into the

Federal Unemployment System• Rate is determined with rate formula specified by

Section 823(b) of the California Unemployment Insurance Code

• Established annually• Pooled rate for schools

State Unemployment Insurance (SUI)

Page 16

Applies to all wages except:

• Board Members• Elected Officials • Students enrolled and regularly attending classes

where employed• Students under 22 years old enrolled in a non-

profit/public education institution which combines academic instruction with work experience

State Unemployment Insurance (SUI)

Page 16

State Disability Insurance (SDI)Optional Insurance Program for government entities to help protect employee wage loss because of non-occupational illness or injury

• Each District may or may not offer the coverage• Typically employee paid• An application has to be completed and filed with EDD

Page 16

Payroll Rates

https://www.scoe.org/files/Payroll_Rates_20210701-rev9-20-2021.pdf

SCOE IT updates the rates the beginning of

the Fiscal Year and Calendar Year

Page 16

Employee Management Taxes TabBe mindful of the system Defaults and update based on the employee information

Important: If there is No Active Tax Record, the system Default is YES and will Report SDI Wages, but not deduct from the employee

{Defaults}

Gross Wages are taxed when paid to an employee and is considered constructively received

• Wages become taxable when Paid not Earned• Considered paid when

– Employee receives paycheck– Money is constructively received– When the employee has the ability to have access

to funds– ACH based on Paid Date

Taxable Income

Page 16

Taxable Income

Page 16

Gross Wages can exclude benefits such as Tax Deferred and Pre-Tax Benefits to reduce taxable wages

Pop Quiz

Which form is new for

2020? DE-4 or W-4

True or False?Wages become taxable when

paid not earned.

If an employee claims Exempt

when must they submit a

new form?

Can an employee opt

out of Statutory

Taxes? NO!Statutory

are required by

law

True!Based on

constructive receipt

2020 W-4

By Feb 15 each year

Tax Withholding Calculations

Tax Withholding CalculationsDetermine Gross Pay

• Salary Schedule Salary Placement

• Number of Paid Days

• Number of Pay Periods

Payroll Concepts 1 of 2 workshop slides

Calculating Tax WithholdingsDetermine Taxable Wages

• Reduce Gross by any Pre-Tax/Tax Deferred Deductions

Tax Deferred and Pre-Tax DeductionsFederal Tax WageReduction

State TaxWageReduction

Social Security/MedicareWage Reduction

CalSTRS (Tax-deferred) Yes Yes No

CalPERS (Tax-deferred) Yes Yes No

403(b) & 457(b) (Tax-deferred) Yes Yes No

Pre-Tax Medical Insurance Premiums Yes Yes Yes

Section 125 Flex Plan (Medical) Yes Yes Yes

Section 125 Flex Plan (Dependent Care) Yes Yes Yes

Health Savings Account Yes No Yes

Calculate Federal Tax WithholdingsSalary Salary Schedule Cell $ 88,146.00 Master Stipend $ 850.00 Total Salary $ 88,996.00 Number of Pay Periods 10Monthly Gross $ 8,899.60

Pre-Tax ReductionsSTRS $ 912.21 Flex125 Medical $ 150.00 TSA $ 200.00 Total Pre-Tax Reductions $ 1,262.21

Monthly Taxable Gross $ 7,637.39Number of Pay Periods 10Annual Taxable Wages $ 76,373.90

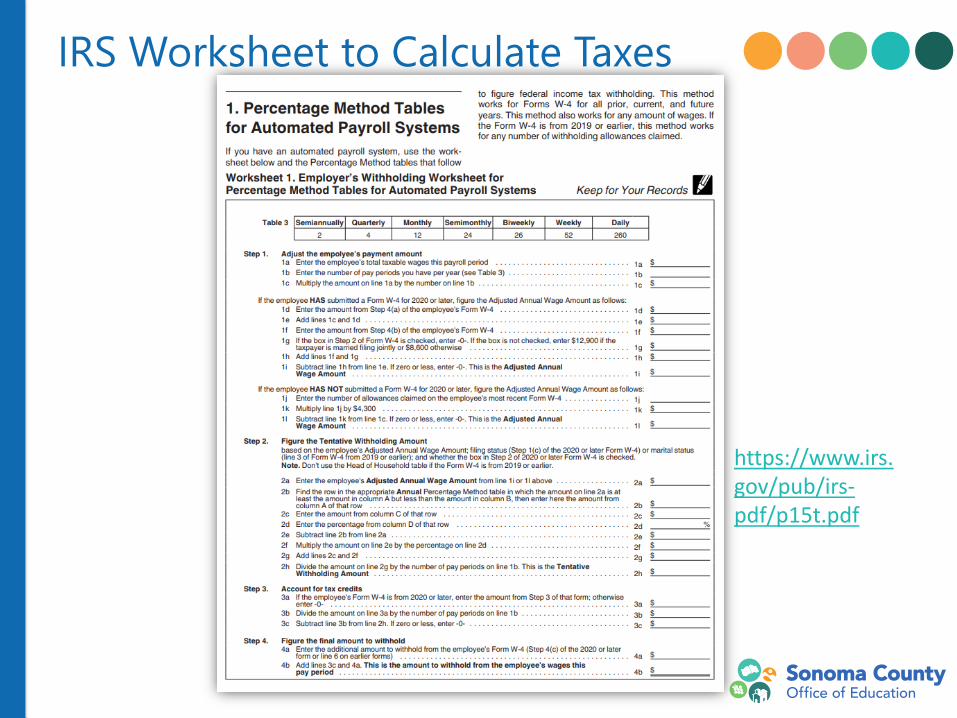

Federal Withholding Calculations

● There are several ways to figure income tax withholding ● Most County Offices use the Percentage Method

● See IRS – 2021 Percentage Method Tables for Automated Systems – Publication 15-T

https://www.irs.gov/pub/irs-pdf/p15t.pdf

Calculating Tax Withholdings

Calculating Tax Withholdings

• The IRS recommends that Employers who use an automated payroll software, such as Escape, use the Percentage Method Tables for Automated Payroll Systems worksheet and the Percentage Method tables to manually calculate District Employees federal income tax withholding monthly amounts

Federal Withholding Calculations – Percentage Method

IRS Worksheet to Calculate Taxes

https://www.irs.gov/pub/irs-pdf/p15t.pdf

Worksheet Template Created by SCOE IT

Dept.

Calculating Tax Withholdings

• This method works for Forms W-4 from 2019 or earlier and Forms W-4 from 2020 or later

• This method also works for any amount of wages

Federal Withholding Calculations – Percentage Method

Federal Withholding Calculations

Calculating Tax Withholdings

Is the Employee W4 form prior to 2020 OR after January 1, 2020?

2021 Percentage Method Tables for Automated Payroll Systems

Now let’s manually calculate Federal Tax Withholdings

Calculating CA State Withholdings

California Withholding Schedules

● CA Provides two methods for determining the amount of wages and salaries to be withheld for state personal income tax● Method A – Wage Bracket Table Method

● Method B – Exact Calculation Method

● Most COE’s and Districts use Method B

Calculating State Tax Withholdings

https://www.edd.ca.gov/pdf_pub_ctr/21methb.pdf

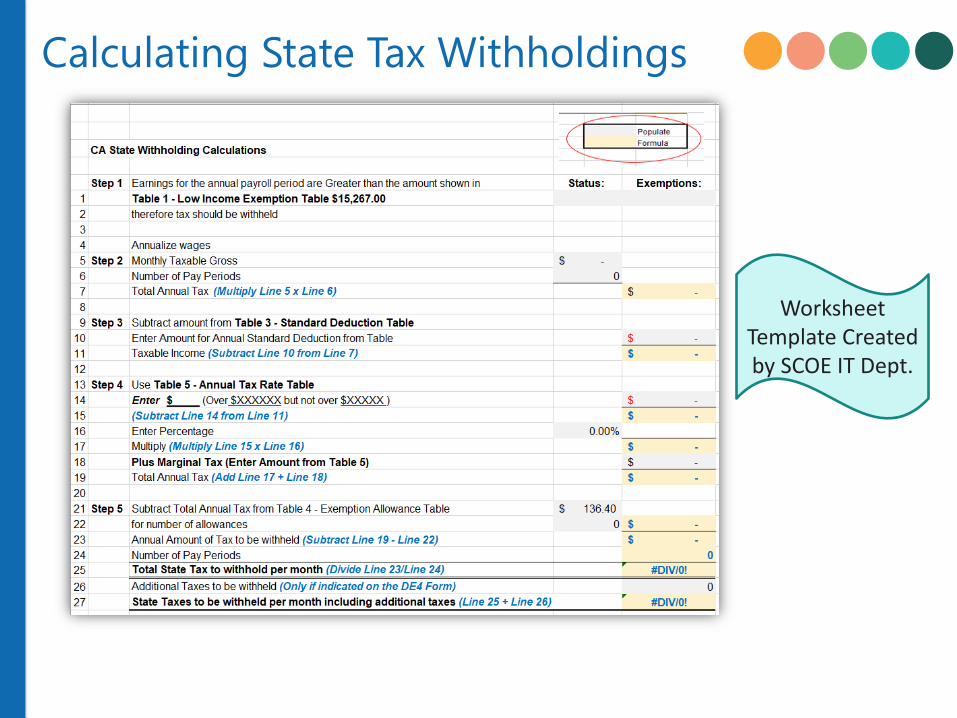

Calculating State Tax WithholdingsMethod B – Exact Calculation Method

Calculating State Tax Withholdings

Table 1 – Low Income Exemption Table

Calculating State Tax WithholdingsTable 3 – Standard Deduction Table

Calculating State Tax Withholdings

Table 4 – Exemption Allowance Table

Calculating State Tax Withholdings

Calculating State Tax Withholdings

Worksheet Template Created by SCOE IT Dept.

Now let’s manually calculate CA State Tax Withholdings

California Ed Code

California Labor Code

California Government Code

Employment Development Department - State of California

(EDD)

Internal Revenue Service (IRS)

Bargaining Unit Agreements/MOU

Resources