how to understand and use the key drivers and trends in ... pharmed session...partner at accenture...

TRANSCRIPT

Christelle GOBLET Partner at Accenture Managment Consulting

How to understand and use the key drivers and

trends in today’s pharmaceutical market?

PHARMED ULB – Module 8: Health marketplace

June 20th , 2012

SHORT VERSION

Copyright © 2012 Accenture. All rights reserved. 2 Copyright © 2012 Accenture. All rights reserved. 2

Agenda

Welcome and Introduction A

What are the key trends reshaping the Life Sciences industry? B

The emergence of an alternative commercial model D

The use of market research and analytics to drive performance C

The growing importance of digital & mobility E

The new opportunities in supply chain F

Break

Conclusion G

Copyright © 2012 Accenture. All rights reserved. 3 Copyright © 2012 Accenture. All rights reserved. 3

Welcome and Introduction Welcome and Introduction

Christelle Goblet Partner

Life Sciences

Commercial

Birgit Matthé Manager

Life Sciences

Analytics

Laureline Vansteenkiste Senior Manager

Life Sciences

Supply Chain

Copyright © 2012 Accenture. All rights reserved. 4 Copyright © 2012 Accenture. All rights reserved. 4

Agenda

Welcome and Introduction A

What are the key trends reshaping the Life Sciences industry? B

The emergence of an alternative commercial model D

The use of market research and analytics to drive performance C

The growing importance of digital & mobility E

The new opportunities in supply chain F

Break

Conclusion G

Copyright © 2012 Accenture. All rights reserved. 5 Copyright © 2012 Accenture. All rights reserved. 5

The industry is at a tipping point…

Copyright © 2012 Accenture. All rights reserved. 6 Copyright © 2012 Accenture. All rights reserved. 6

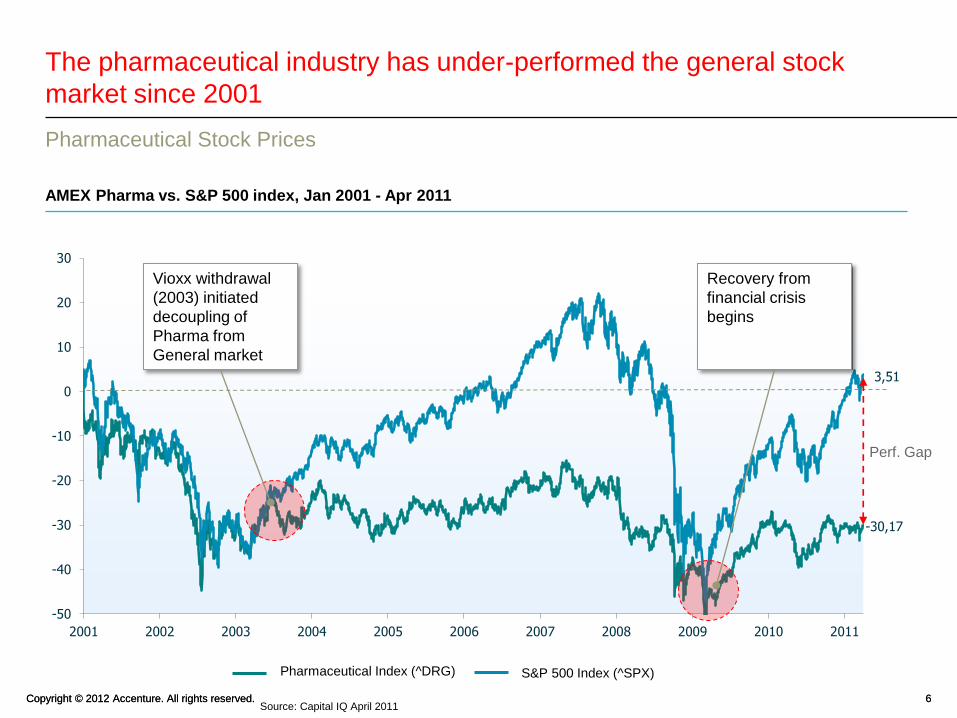

-30,17

3,51

-50

-40

-30

-20

-10

0

10

20

30

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

The pharmaceutical industry has under-performed the general stock

market since 2001

Pharmaceutical Stock Prices

Perf. Gap

Vioxx withdrawal

(2003) initiated

decoupling of

Pharma from

General market

Recovery from

financial crisis

begins

AMEX Pharma vs. S&P 500 index, Jan 2001 - Apr 2011

Pharmaceutical Index (^DRG) S&P 500 Index (^SPX)

Source: Capital IQ April 2011

Copyright © 2012 Accenture. All rights reserved. 7 Copyright © 2012 Accenture. All rights reserved. 7

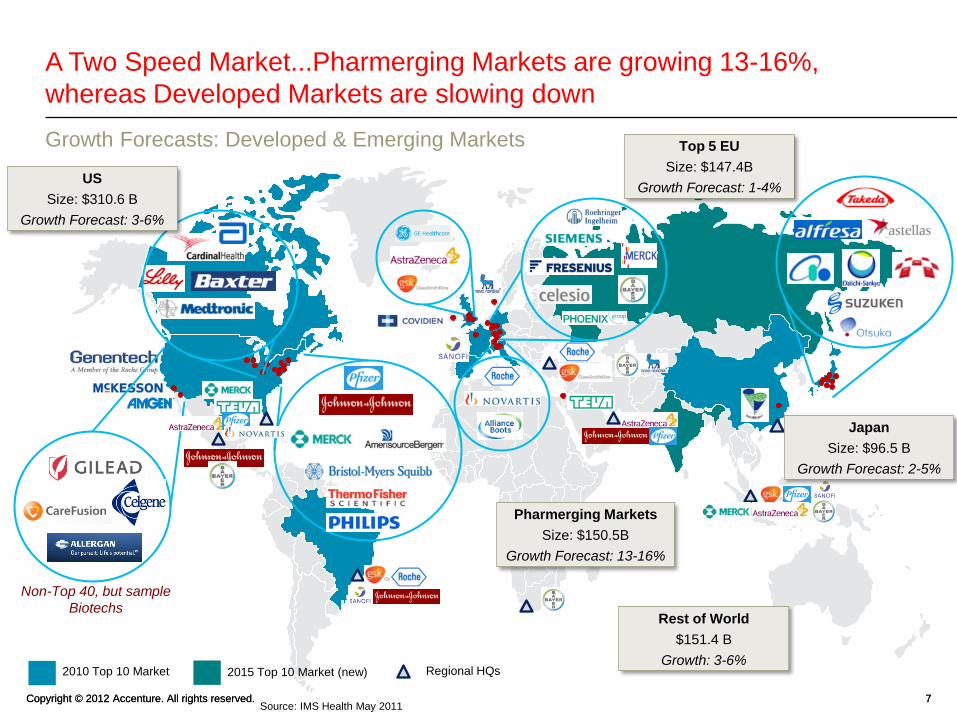

A Two Speed Market...Pharmerging Markets are growing 13-16%,

whereas Developed Markets are slowing down

Growth Forecasts: Developed & Emerging Markets

2010 Top 10 Market

Non-Top 40, but sample

Biotechs

2015 Top 10 Market (new) Regional HQs

Source: IMS Health May 2011

Top 5 EU

Size: $147.4B

Growth Forecast: 1-4%

Japan

Size: $96.5 B

Growth Forecast: 2-5%

Pharmerging Markets

Size: $150.5B

Growth Forecast: 13-16%

Rest of World

$151.4 B

Growth: 3-6%

US

Size: $310.6 B

Growth Forecast: 3-6%

Copyright © 2012 Accenture. All rights reserved. 8 Copyright © 2012 Accenture. All rights reserved. 8

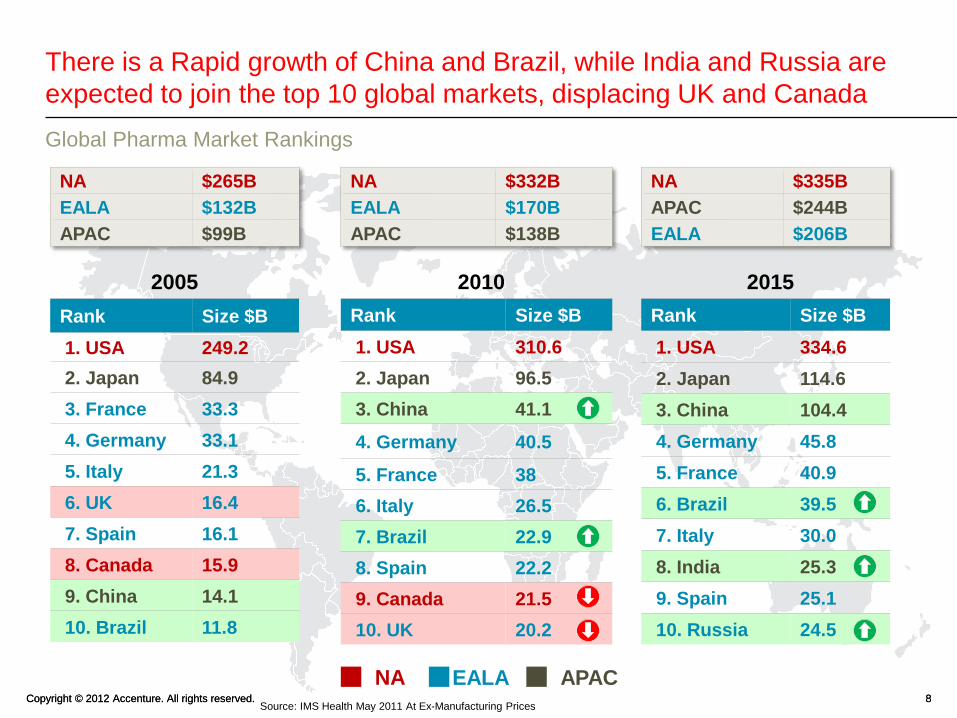

There is a Rapid growth of China and Brazil, while India and Russia are

expected to join the top 10 global markets, displacing UK and Canada

Global Pharma Market Rankings

Source: IMS Health May 2011 At Ex-Manufacturing Prices

2005

Rank Size $B

1. USA 249.2

2. Japan 84.9

3. France 33.3

4. Germany 33.1

5. Italy 21.3

6. UK 16.4

7. Spain 16.1

8. Canada 15.9

9. China 14.1

10. Brazil 11.8

2010

Rank Size $B

1. USA 310.6

2. Japan 96.5

3. China 41.1

4. Germany 40.5

5. France 38

6. Italy 26.5

7. Brazil 22.9

8. Spain 22.2

9. Canada 21.5

10. UK 20.2

2015

Rank Size $B

1. USA 334.6

2. Japan 114.6

3. China 104.4

4. Germany 45.8

5. France 40.9

6. Brazil 39.5

7. Italy 30.0

8. India 25.3

9. Spain 25.1

10. Russia 24.5

NA $265B

EALA $132B

APAC $99B

NA $332B

EALA $170B

APAC $138B

NA $335B

APAC $244B

EALA $206B

NA EALA APAC

Copyright © 2012 Accenture. All rights reserved. 9 Copyright © 2012 Accenture. All rights reserved. 9

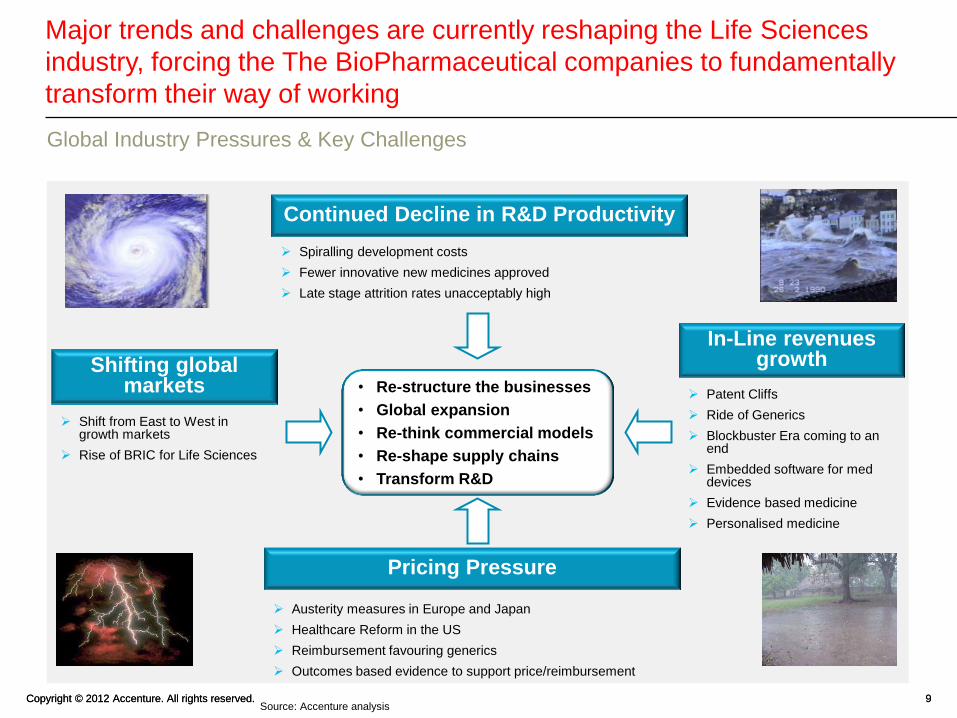

Major trends and challenges are currently reshaping the Life Sciences

industry, forcing the The BioPharmaceutical companies to fundamentally

transform their way of working

Global Industry Pressures & Key Challenges

Source: Accenture analysis

Shift from East to West in growth markets

Rise of BRIC for Life Sciences

Shifting global markets

Patent Cliffs

Ride of Generics

Blockbuster Era coming to an end

Embedded software for med devices

Evidence based medicine

Personalised medicine

In-Line revenues growth

Spiralling development costs

Fewer innovative new medicines approved

Late stage attrition rates unacceptably high

Continued Decline in R&D Productivity

Austerity measures in Europe and Japan

Healthcare Reform in the US

Reimbursement favouring generics

Outcomes based evidence to support price/reimbursement

Pricing Pressure

• Re-structure the businesses

• Global expansion

• Re-think commercial models

• Re-shape supply chains

• Transform R&D

Copyright © 2012 Accenture. All rights reserved. 10 Copyright © 2012 Accenture. All rights reserved. 10

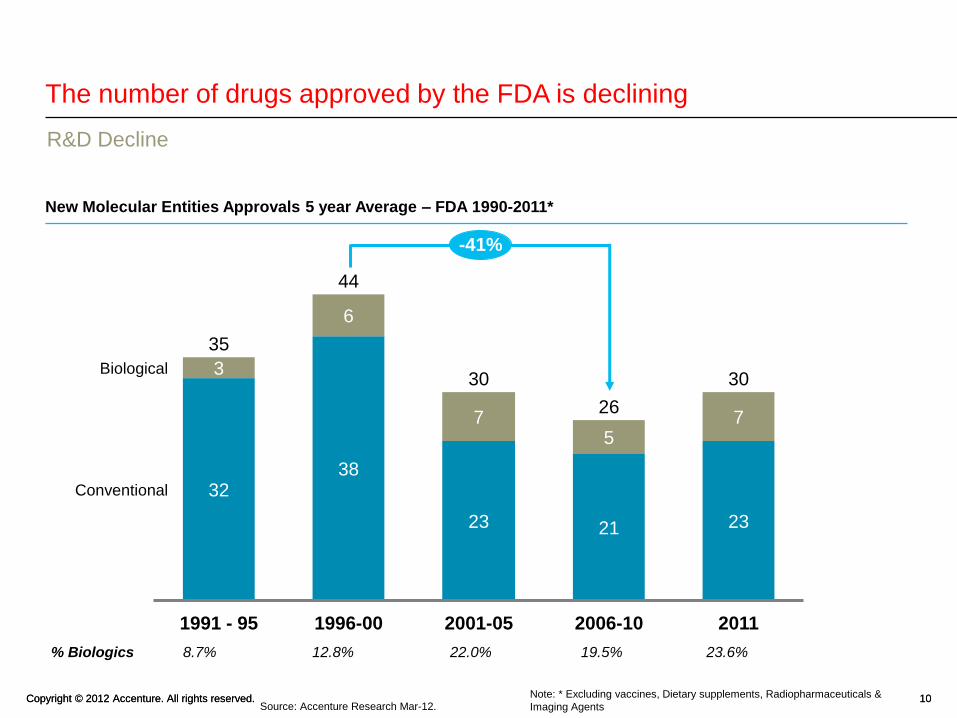

The number of drugs approved by the FDA is declining

R&D Decline

Source: Accenture Research Mar-12.

1991 - 95 2011

Biological 3

35

7

30

6

44

1996-00

Conventional

2001-05

32

23 21 23

38

5

26 7

30

2006-10

8.7% 12.8% 22.0% 19.5% 23.6% % Biologics

-41%

New Molecular Entities Approvals 5 year Average – FDA 1990-2011*

Note: * Excluding vaccines, Dietary supplements, Radiopharmaceuticals &

Imaging Agents

Copyright © 2012 Accenture. All rights reserved. 11 Copyright © 2012 Accenture. All rights reserved. 11

2010 Global Pharma Sales estimated $163B already off patent, and an

additional $211B were due to go off-patent in the coming 5 years

2011-15. That’s 53% of Global Sales “At Risk”

Patent Expiry

Source: Accenture Research Mar-12.

70441

2010 2011

62

2013

19 31

2012 2015 2014

58

186

144

163

211

23%

30%

20%

2010

26%

IP Exposure Pharma Industry 2010-15(E)

Already

Off Patent

Patent Expiry in

5 years 2011-15 Safe Sales Unclassified

Copyright © 2012 Accenture. All rights reserved. 12 Copyright © 2012 Accenture. All rights reserved. 12

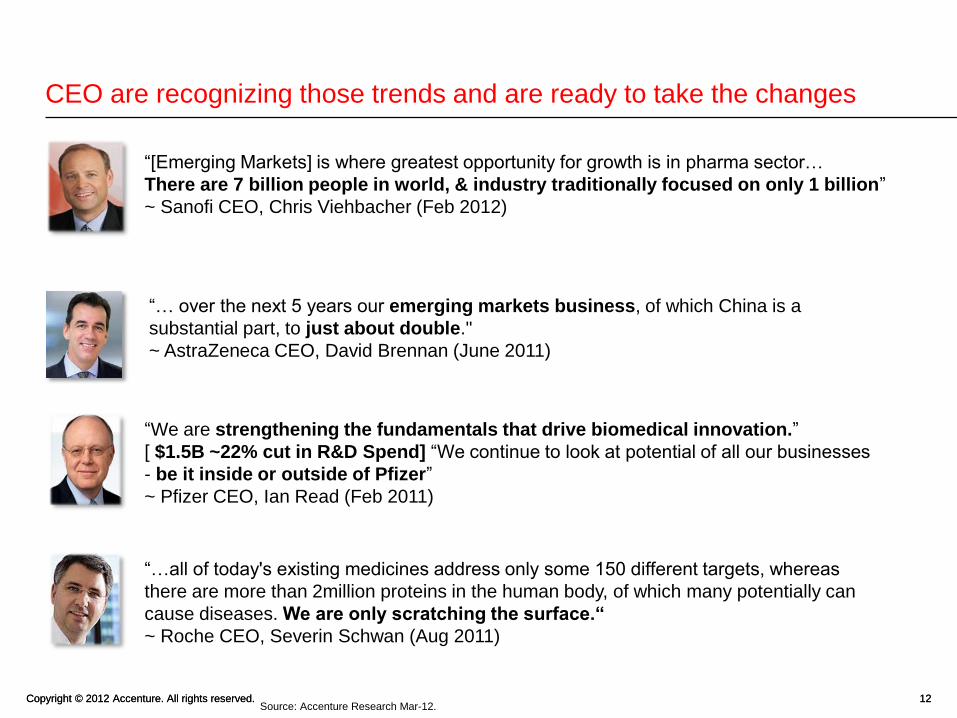

CEO are recognizing those trends and are ready to take the changes

Source: Accenture Research Mar-12.

“…all of today's existing medicines address only some 150 different targets, whereas

there are more than 2million proteins in the human body, of which many potentially can

cause diseases. We are only scratching the surface.“

~ Roche CEO, Severin Schwan (Aug 2011)

“[Emerging Markets] is where greatest opportunity for growth is in pharma sector…

There are 7 billion people in world, & industry traditionally focused on only 1 billion”

~ Sanofi CEO, Chris Viehbacher (Feb 2012)

“… over the next 5 years our emerging markets business, of which China is a

substantial part, to just about double."

~ AstraZeneca CEO, David Brennan (June 2011)

“We are strengthening the fundamentals that drive biomedical innovation.”

[ $1.5B ~22% cut in R&D Spend] “We continue to look at potential of all our businesses

- be it inside or outside of Pfizer”

~ Pfizer CEO, Ian Read (Feb 2011)

Copyright © 2012 Accenture. All rights reserved. 13 Copyright © 2012 Accenture. All rights reserved. 13

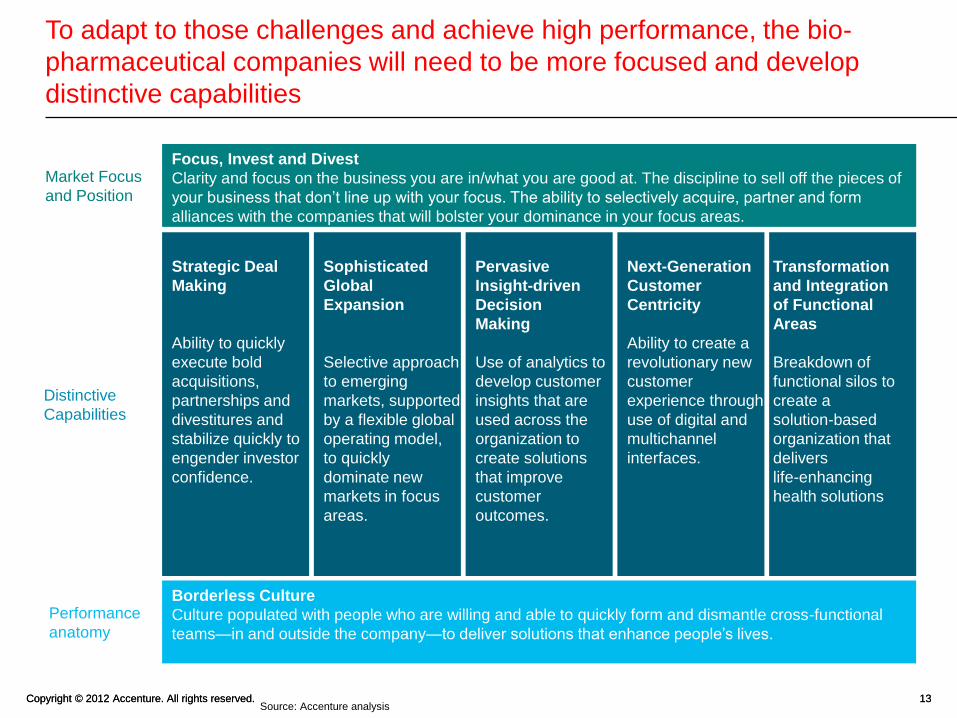

To adapt to those challenges and achieve high performance, the bio-

pharmaceutical companies will need to be more focused and develop

distinctive capabilities

Source: Accenture analysis

Strategic Deal

Making

Ability to quickly

execute bold

acquisitions,

partnerships and

divestitures and

stabilize quickly to

engender investor

confidence.

Sophisticated

Global

Expansion

Selective approach

to emerging

markets, supported

by a flexible global

operating model,

to quickly

dominate new

markets in focus

areas.

Pervasive

Insight-driven

Decision

Making

Use of analytics to

develop customer

insights that are

used across the

organization to

create solutions

that improve

customer

outcomes.

Next-Generation

Customer

Centricity

Ability to create a

revolutionary new

customer

experience through

use of digital and

multichannel

interfaces.

Transformation

and Integration

of Functional

Areas

Breakdown of

functional silos to

create a

solution-based

organization that

delivers

life-enhancing

health solutions

Focus, Invest and Divest

Clarity and focus on the business you are in/what you are good at. The discipline to sell off the pieces of

your business that don’t line up with your focus. The ability to selectively acquire, partner and form

alliances with the companies that will bolster your dominance in your focus areas.

Borderless Culture

Culture populated with people who are willing and able to quickly form and dismantle cross-functional

teams—in and outside the company—to deliver solutions that enhance people’s lives.

Market Focus

and Position

Performance

anatomy

Distinctive

Capabilities

Copyright © 2012 Accenture. All rights reserved. 14 Copyright © 2012 Accenture. All rights reserved. 14

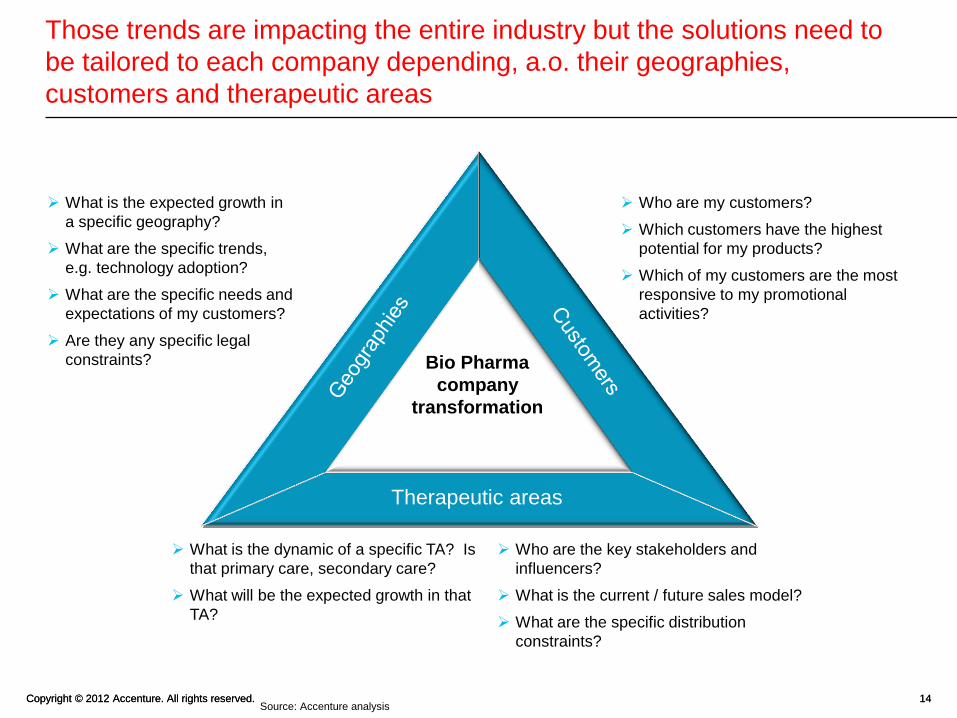

Those trends are impacting the entire industry but the solutions need to

be tailored to each company depending, a.o. their geographies,

customers and therapeutic areas

Source: Accenture analysis

What is the expected growth in

a specific geography?

What are the specific trends,

e.g. technology adoption?

What are the specific needs and

expectations of my customers?

Are they any specific legal

constraints?

Who are my customers?

Which customers have the highest

potential for my products?

Which of my customers are the most

responsive to my promotional

activities?

What is the dynamic of a specific TA? Is

that primary care, secondary care?

What will be the expected growth in that

TA?

Therapeutic areas

Bio Pharma

company

transformation

Who are the key stakeholders and

influencers?

What is the current / future sales model?

What are the specific distribution

constraints?

Copyright © 2012 Accenture. All rights reserved. 15 Copyright © 2012 Accenture. All rights reserved. 15

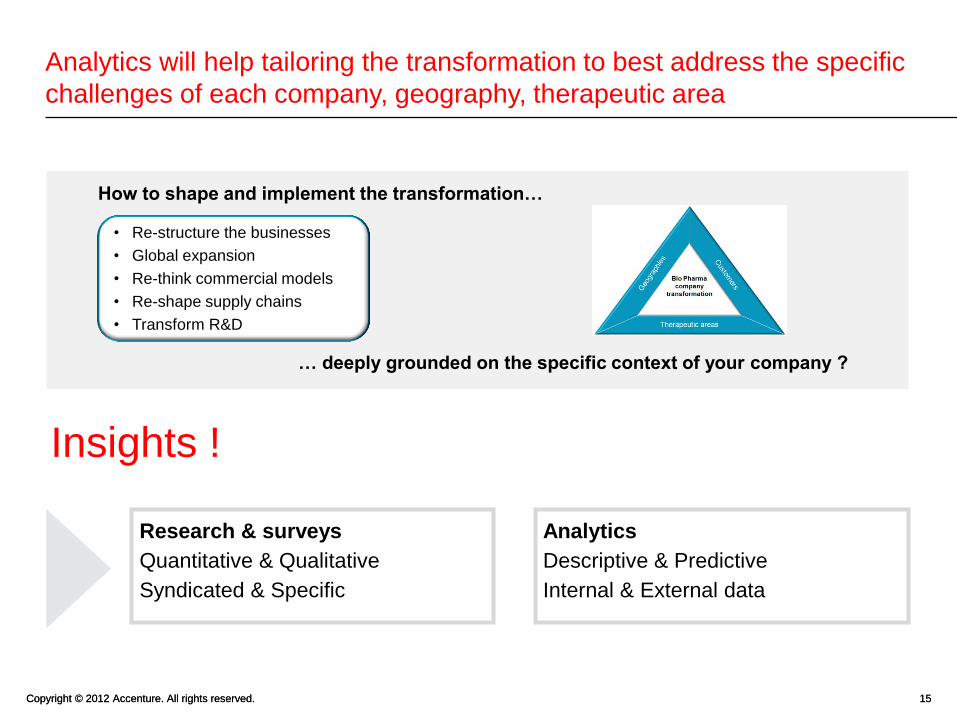

Analytics will help tailoring the transformation to best address the specific

challenges of each company, geography, therapeutic area

• Re-structure the businesses

• Global expansion

• Re-think commercial models

• Re-shape supply chains

• Transform R&D

How to shape and implement the transformation…

… deeply grounded on the specific context of your company ?

Insights !

Research & surveys

Quantitative & Qualitative

Syndicated & Specific

Analytics

Descriptive & Predictive

Internal & External data

Copyright © 2012 Accenture. All rights reserved. 16 Copyright © 2012 Accenture. All rights reserved. 16

Agenda

Welcome and Introduction A

What are the key trends reshaping the Life Sciences industry? B

The emergence of an alternative commercial model D

The use of market research and analytics to drive performance C

The growing importance of digital & mobility E

The new opportunities in supply chain F

Break

Conclusion G

Copyright © 2012 Accenture. All rights reserved. 17 Copyright © 2012 Accenture. All rights reserved. 17

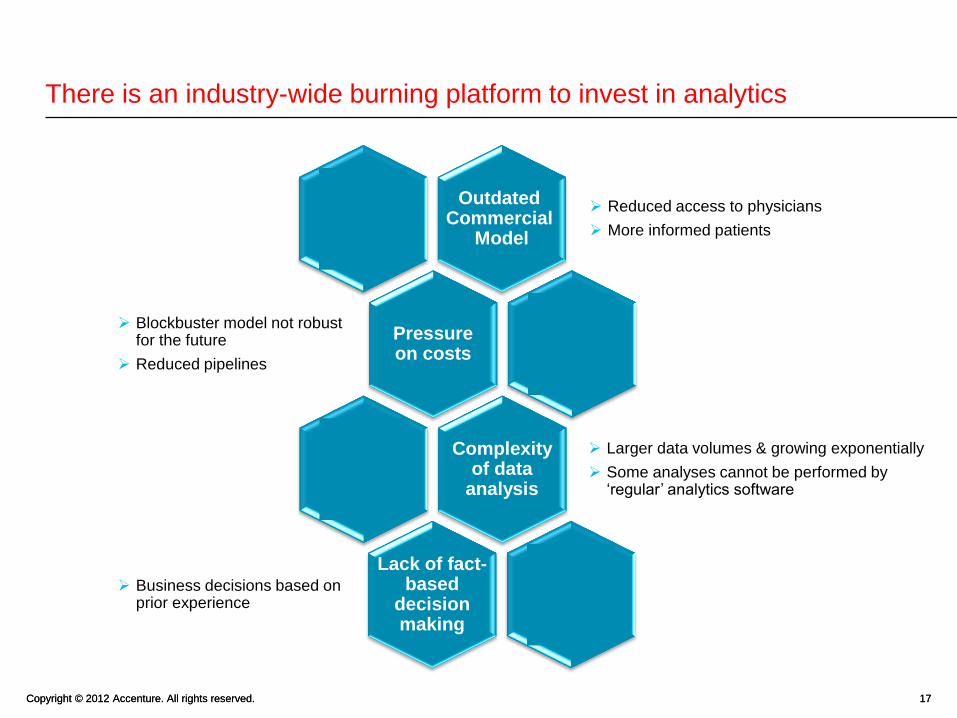

There is an industry-wide burning platform to invest in analytics

Outdated Commercial

Model

Reduced access to physicians

More informed patients

Pressure on costs

Blockbuster model not robust for the future

Reduced pipelines

Complexity of data

analysis

Larger data volumes & growing exponentially

Some analyses cannot be performed by ‘regular’ analytics software

Lack of fact-based

decision making

Business decisions based on prior experience

Copyright © 2012 Accenture. All rights reserved. 18 Copyright © 2012 Accenture. All rights reserved. 18

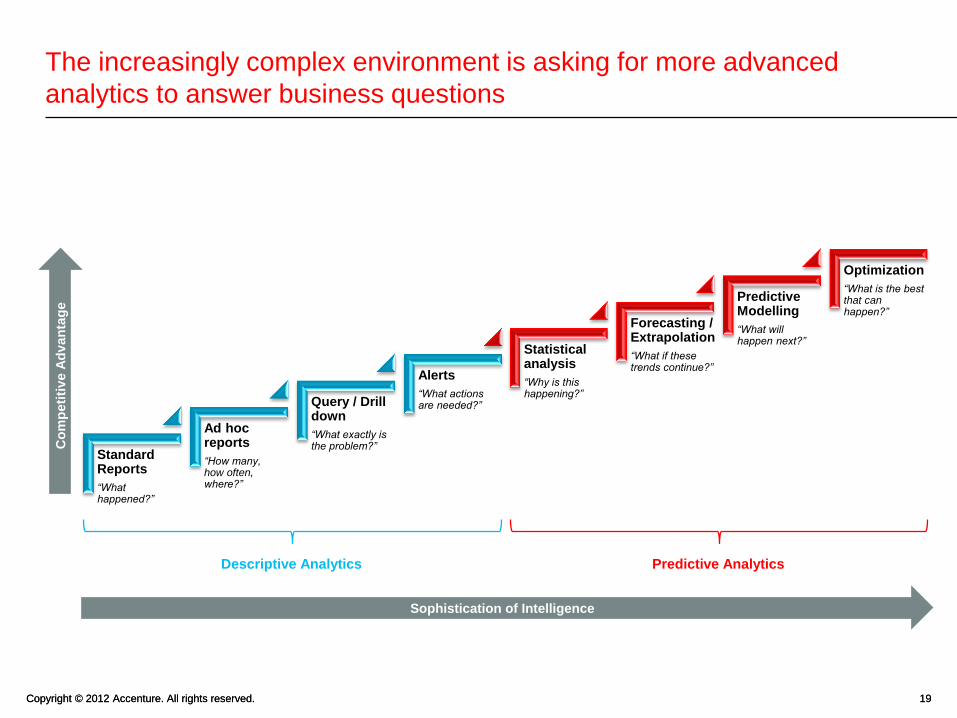

The increasingly complex environment is asking for more advanced

analytics to answer business questions

Outcomes

Information

Data

Solutions focus on

performance dashboards

Incomplete view of physicians,

patients, effectiveness

Primarily data

Solutions have to become

holistic and predictive

Mandatory to connect market,

activities & financial data

New channels & customers,

digitized clinical information

Yesterday Today

Copyright © 2012 Accenture. All rights reserved. 19 Copyright © 2012 Accenture. All rights reserved. 19

The increasingly complex environment is asking for more advanced

analytics to answer business questions

Sophistication of Intelligence

Co

mp

eti

tiv

e A

dv

an

tag

e

Standard Reports

“What happened?”

Ad hoc reports

“How many, how often, where?”

Query / Drill down

“What exactly is the problem?”

Alerts

“What actions are needed?”

Statistical analysis

“Why is this happening?”

Forecasting / Extrapolation

“What if these trends continue?”

Predictive Modelling

“What will happen next?”

Optimization

“What is the best that can happen?”

Descriptive Analytics Predictive Analytics

Copyright © 2012 Accenture. All rights reserved. 20 Copyright © 2012 Accenture. All rights reserved. 20

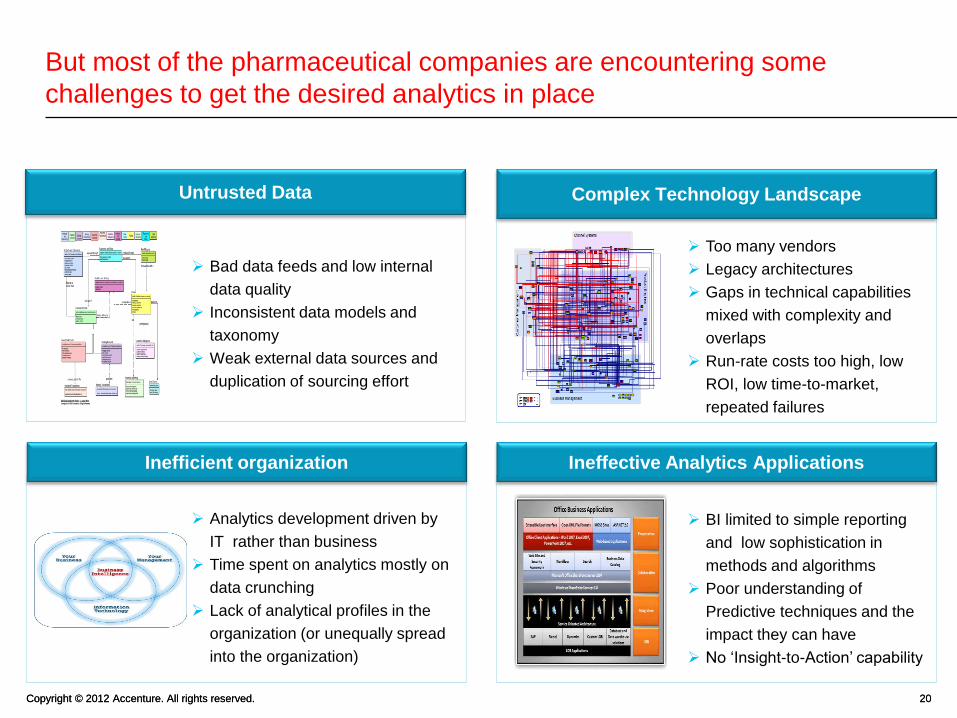

But most of the pharmaceutical companies are encountering some

challenges to get the desired analytics in place

Complex Technology Landscape

Too many vendors

Legacy architectures

Gaps in technical capabilities

mixed with complexity and

overlaps

Run-rate costs too high, low

ROI, low time-to-market,

repeated failures

Untrusted Data

Bad data feeds and low internal

data quality

Inconsistent data models and

taxonomy

Weak external data sources and

duplication of sourcing effort

Ineffective Analytics Applications

BI limited to simple reporting

and low sophistication in

methods and algorithms

Poor understanding of

Predictive techniques and the

impact they can have

No ‘Insight-to-Action’ capability

Inefficient organization

Analytics development driven by

IT rather than business

Time spent on analytics mostly on

data crunching

Lack of analytical profiles in the

organization (or unequally spread

into the organization)

Copyright © 2012 Accenture. All rights reserved. 21 Copyright © 2012 Accenture. All rights reserved. 21

Agenda

Welcome and Introduction A

What are the key trends reshaping the Life Sciences industry? B

The emergence of an alternative commercial model D

The use of market research and analytics to drive performance C

The growing importance of digital & mobility E

The new opportunities in supply chain F

Break

Conclusion G

Copyright © 2012 Accenture. All rights reserved. 22 Copyright © 2012 Accenture. All rights reserved. 22

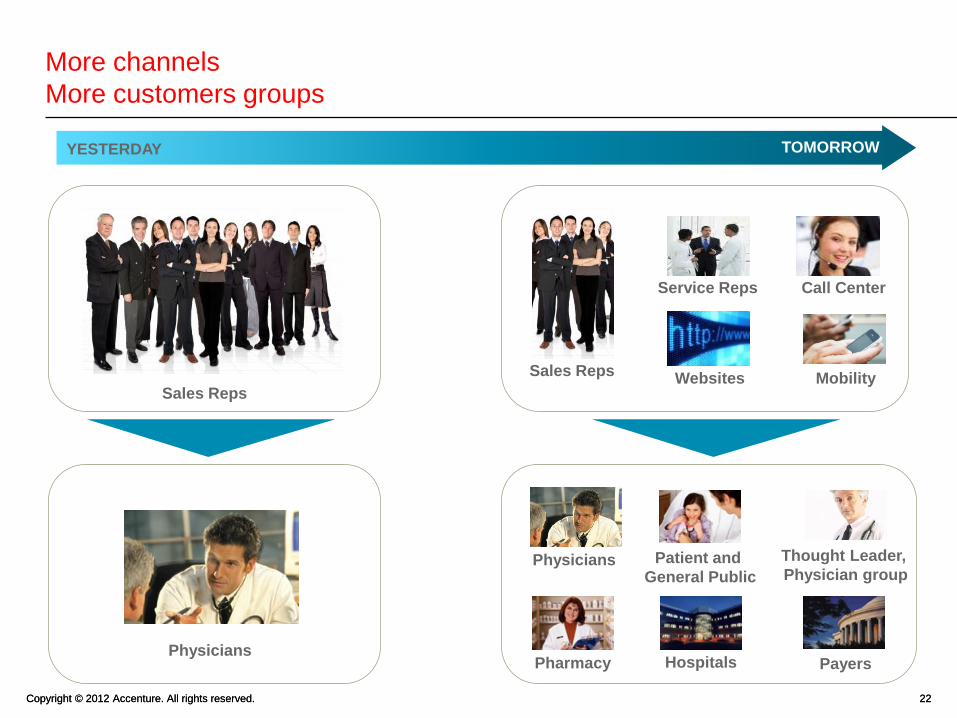

More channels

More customers groups

Physicians

Sales Reps

Thought Leader,

Physician group

Payers

Pharmacy

Patient and

General Public

Hospitals

Physicians

Sales Reps

Service Reps Call Center

Websites Mobility

YESTERDAY TOMORROW

Copyright © 2012 Accenture. All rights reserved. 23 Copyright © 2012 Accenture. All rights reserved. 23

Overview of options to align the traditional pharmaceutical sales model

Copyright © 2012 Accenture. All rights reserved. 24 Copyright © 2012 Accenture. All rights reserved. 24

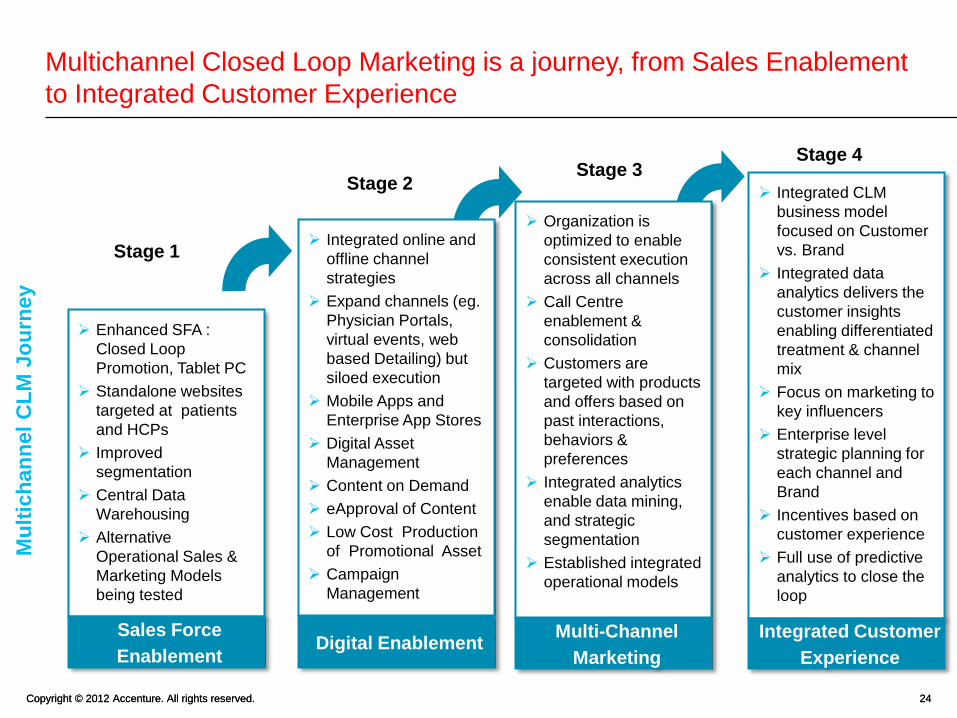

Integrated CLM

business model

focused on Customer

vs. Brand

Integrated data

analytics delivers the

customer insights

enabling differentiated

treatment & channel

mix

Focus on marketing to

key influencers

Enterprise level

strategic planning for

each channel and

Brand

Incentives based on

customer experience

Full use of predictive

analytics to close the

loop

Multichannel Closed Loop Marketing is a journey, from Sales Enablement

to Integrated Customer Experience

Mu

ltic

han

nel

CL

M J

ou

rney

Enhanced SFA :

Closed Loop

Promotion, Tablet PC

Standalone websites

targeted at patients

and HCPs

Improved

segmentation

Central Data

Warehousing

Alternative

Operational Sales &

Marketing Models

being tested

Stage 1 Integrated online and

offline channel

strategies

Expand channels (eg.

Physician Portals,

virtual events, web

based Detailing) but

siloed execution

Mobile Apps and

Enterprise App Stores

Digital Asset

Management

Content on Demand

eApproval of Content

Low Cost Production

of Promotional Asset

Campaign

Management

Stage 2

Organization is

optimized to enable

consistent execution

across all channels

Call Centre

enablement &

consolidation

Customers are

targeted with products

and offers based on

past interactions,

behaviors &

preferences

Integrated analytics

enable data mining,

and strategic

segmentation

Established integrated

operational models

Stage 3 Stage 4

Sales Force

Enablement Digital Enablement

Multi-Channel

Marketing

Integrated Customer

Experience

Copyright © 2012 Accenture. All rights reserved. 25 Copyright © 2012 Accenture. All rights reserved. 25

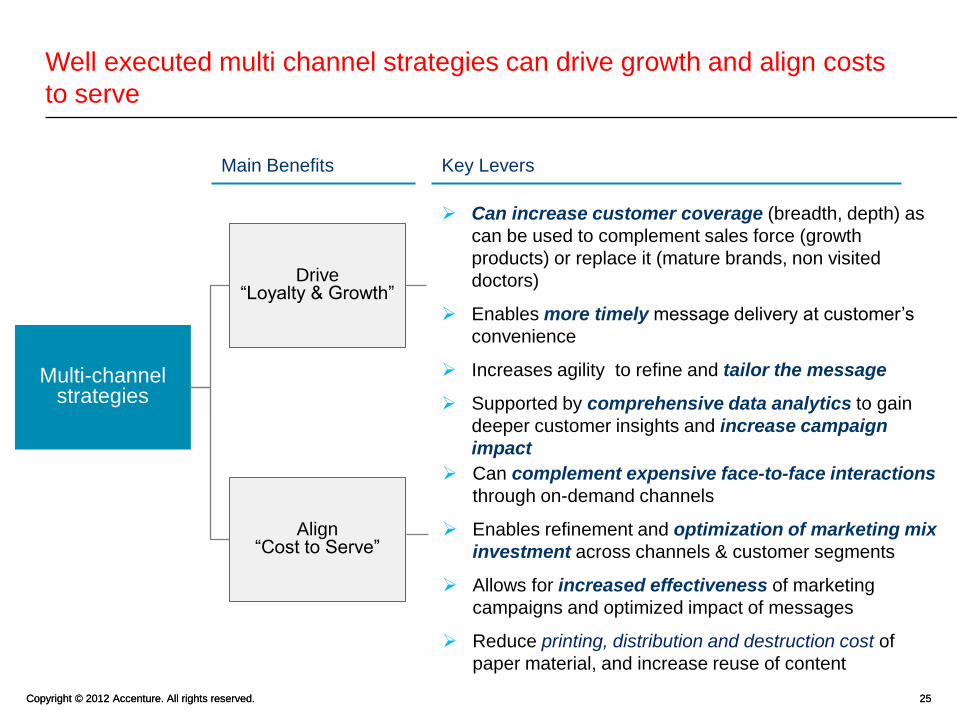

Well executed multi channel strategies can drive growth and align costs

to serve

Can increase customer coverage (breadth, depth) as

can be used to complement sales force (growth

products) or replace it (mature brands, non visited

doctors)

Enables more timely message delivery at customer’s

convenience

Increases agility to refine and tailor the message

Supported by comprehensive data analytics to gain

deeper customer insights and increase campaign

impact

Can complement expensive face-to-face interactions

through on-demand channels

Enables refinement and optimization of marketing mix

investment across channels & customer segments

Allows for increased effectiveness of marketing

campaigns and optimized impact of messages

Reduce printing, distribution and destruction cost of

paper material, and increase reuse of content

Drive “Loyalty & Growth”

Align “Cost to Serve”

Multi-channel strategies

Main Benefits Key Levers

Copyright © 2012 Accenture. All rights reserved. 26 Copyright © 2012 Accenture. All rights reserved. 26

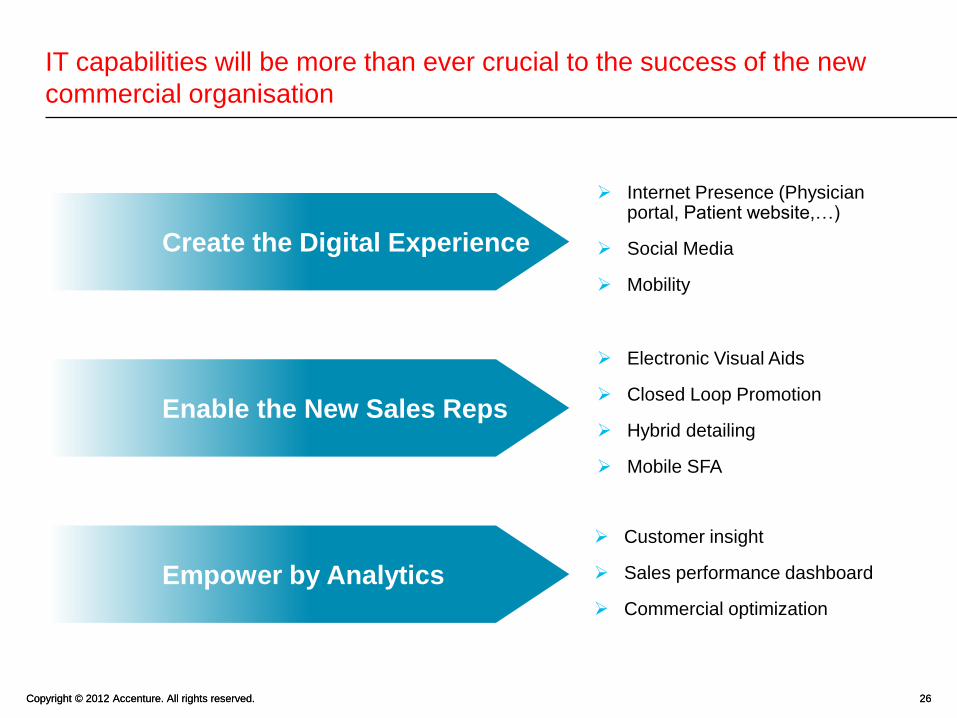

IT capabilities will be more than ever crucial to the success of the new

commercial organisation

Create the Digital Experience

Enable the New Sales Reps

Empower by Analytics

Internet Presence (Physician portal, Patient website,…)

Social Media

Mobility

Electronic Visual Aids

Closed Loop Promotion

Hybrid detailing

Mobile SFA

Customer insight

Sales performance dashboard

Commercial optimization

Copyright © 2012 Accenture. All rights reserved. 27 Copyright © 2012 Accenture. All rights reserved. 27

Agenda

Welcome and Introduction A

What are the key trends reshaping the Life Sciences industry? B

The emergence of an alternative commercial model D

The use of market research and analytics to drive performance C

The growing importance of digital & mobility E

The new opportunities in supply chain F

Break

Conclusion G

Copyright © 2012 Accenture. All rights reserved. 28 Copyright © 2012 Accenture. All rights reserved. 28

Agenda

Welcome and Introduction A

What are the key trends reshaping the Life Sciences industry? B

The emergence of an alternative commercial model D

The use of market research and analytics to drive performance C

The growing importance of digital & mobility E

The new opportunities in supply chain F

Break

Conclusion G

Copyright © 2012 Accenture. All rights reserved. 29 Copyright © 2012 Accenture. All rights reserved. 29

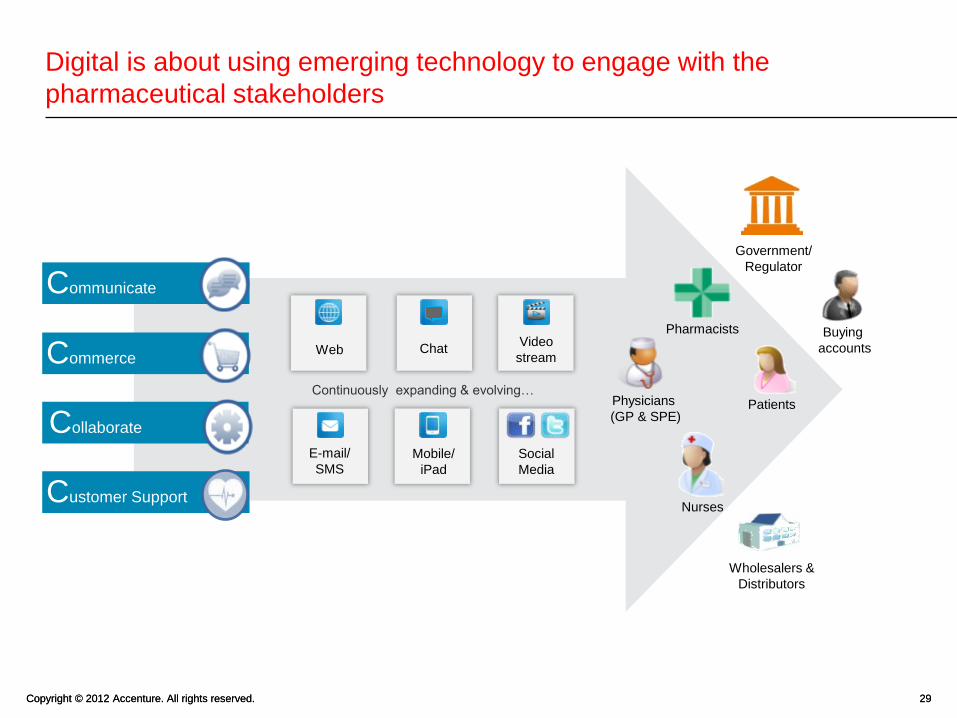

Digital is about using emerging technology to engage with the

pharmaceutical stakeholders

Collaborate

Commerce

Customer Support

Communicate

Government/

Regulator

E-mail/

SMS Mobile/

iPad

Social

Media

Web Chat Video

stream

Continuously expanding & evolving… Patients

Pharmacists

Nurses

Buying

accounts

Wholesalers &

Distributors

Physicians

(GP & SPE)

Copyright © 2012 Accenture. All rights reserved. 30 Copyright © 2012 Accenture. All rights reserved. 30

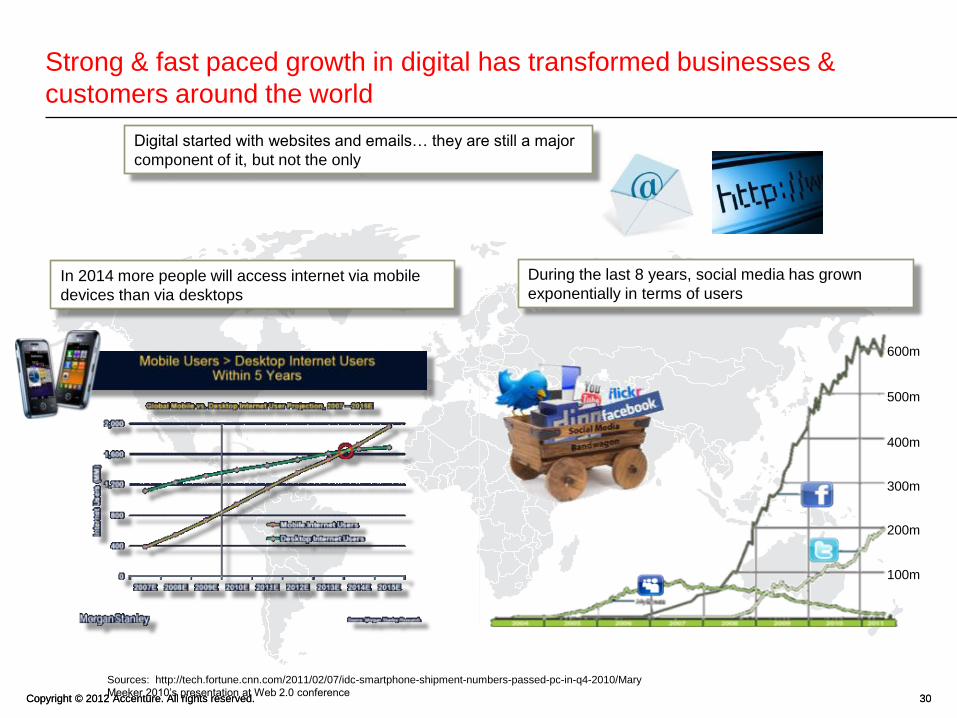

Strong & fast paced growth in digital has transformed businesses &

customers around the world

In 2014 more people will access internet via mobile

devices than via desktops

Sources: http://tech.fortune.cnn.com/2011/02/07/idc-smartphone-shipment-numbers-passed-pc-in-q4-2010/Mary

Meeker 2010’s presentation at Web 2.0 conference

During the last 8 years, social media has grown

exponentially in terms of users

100m

200m

300m

400m

500m

600m

Digital started with websites and emails… they are still a major

component of it, but not the only

Copyright © 2012 Accenture. All rights reserved. 31 Copyright © 2012 Accenture. All rights reserved. 31

Customers have dramatically changed the way they access information,

communicate and interact

Customers are in control of information…

10bn monthly Google searches – Health is the most searched topic on Google

According to an Accenture survey, 68% of US customers are using internet to research health issues, of those 46% use WebMD, 26% use Wikipedia

…they connect and interact through social media

859m Social Media users worldwide

> 600m Facebook active users (January 2011)

> 50% of US & EU online customers participate in social media and spend nearly 6 hours a month

…they are increasingly mobile

800m mobile Internet users (2010)

200m active users currently accessing Facebook through their mobile devices (2011)

…and show new shopping behaviors (eCommerce Market is growing fast)

+15% growth rate in North America

+26% growth in France in 2010, 20% in Europe

+90% growth in China in 2009, +20% in Brazil (in 2010)

Sources: Internet Stats Compendium, Jan. 2010/ eConsultancy Digital Marketers United (1bis) ACN research, April 2010/ Gartner, March 2009/ Morgan Stanley Research/ ACN Consumer

Survey: “The Evolving Consumer and The Pharmaceutical Company Relationship”, Nov 2010/ Euromonitor 2010/ Taking the Pulse® Asia v9.0/ http://www.macworld.co.uk/ipod-

itunes/news/index.cfm?RSS&NewsID=22296/ msnbc.com – JDN - http://www.sramanamitra.com/2011/04/12/strong-and-steady-e-commerce-growth-in-latin-america/ -

http://www.permuto.com/blog/2010/01/18/e-commerce-in-china-expected-to-double-in-2010/

Copyright © 2012 Accenture. All rights reserved. 32 Copyright © 2012 Accenture. All rights reserved. 32

Digital has become an essential source of information for physicians and

patients

Physicians Patients

• 9 out of 10 physicians agree that the Internet is

“essential to my practice”

• 61% of adults look online for health information

• Combined Internet sources exceeds TV or pharmacist

as initial source of information

Health is the most searched topic on the web

• 90% trust online medical information

• 50% say it impacts their prescription

Online information impacts dialogue

• 60% say information found online affected a treatment

decision

• 53% asked a doctor new questions

• Physician spend < 2.5 hours per wk seeing reps vs

8hrs per wk online

• 93% want personalized content

• 78% expect online services

Customers want to interact differently

• > 80m adults use social media for health-related

matters

• 41% read other patients comments

Patients Doctors

Copyright © 2012 Accenture. All rights reserved. 33 Copyright © 2012 Accenture. All rights reserved. 33

Digital offers a multitude of opportunities to connect with your customers

Cu

sto

me

rs

Physicians &

HCPs

Patients

& Care givers

KOLs Hospitals Payers &

Regulators

Pharmacists

De

live

ry

Ch

an

ne

ls

Web Mobile

Mobile Web SMS

Other channels

Mobile App Social media

Physical channels

Call Center

Sales Force 3rd party

Sites / Portals

Owned Sites

/ Portals

Feeds Email Social

Media

Web App Tablet PC

Game

Consoles

Video Immersive

Platforms

Devices Digital

Displays

Patients Employees

Communicate Collaborate Customer

Support Commerce

Copyright © 2012 Accenture. All rights reserved. 34 Copyright © 2012 Accenture. All rights reserved. 34

Each pharma company should assess the relevance of digital by

reviewing a set of key questions

Why

Why do we want to position

Digital as a key channel within

the new commercial model?

Who

Who do we want to reach

through Digital?

How

How will we engage our target

customers?

What

Services offered to engage the

customers through Digital?

Enablers What enablers do we need for

a successful implementation

of a digital strategy? Digital

Strategic

Intent

Digital Strategy Framework

Copyright © 2012 Accenture. All rights reserved. 35 Copyright © 2012 Accenture. All rights reserved. 35

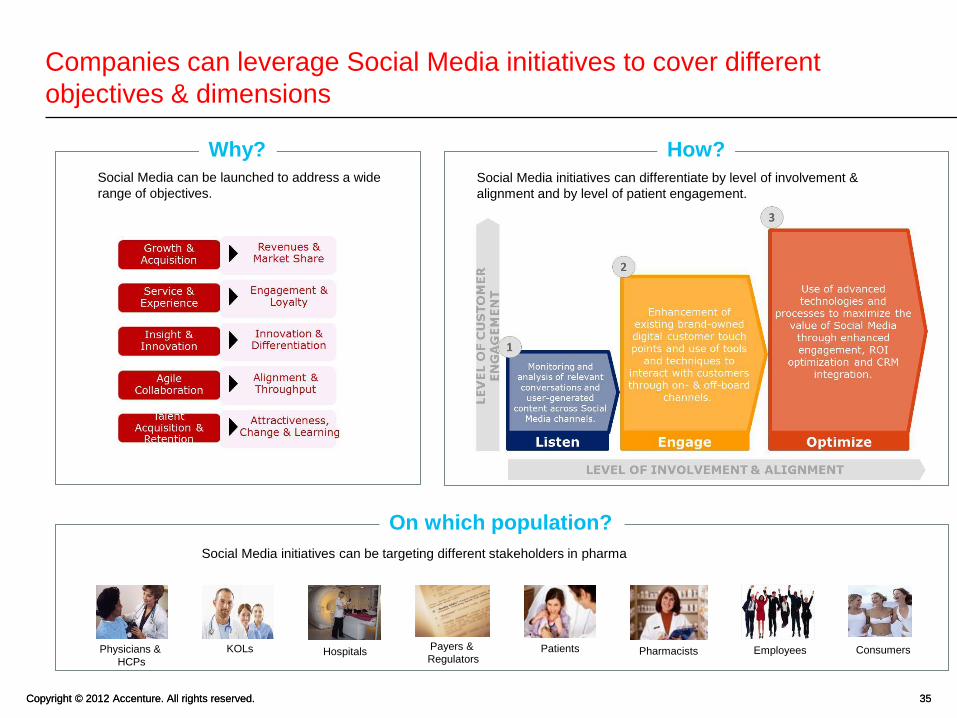

Companies can leverage Social Media initiatives to cover different

objectives & dimensions

Why?

How?

Physicians &

HCPs

Patients KOLs Hospitals Payers &

Regulators Pharmacists Consumers Employees

On which population?

Social Media can be launched to address a wide

range of objectives.

Social Media initiatives can differentiate by level of involvement &

alignment and by level of patient engagement.

Social Media initiatives can be targeting different stakeholders in pharma

Copyright © 2012 Accenture. All rights reserved. 36 Copyright © 2012 Accenture. All rights reserved. 36

Mobility is gaining in importance within pharma, to reach customers and

to enable employees

excite engage

efficiency

Mobile Marketing & Customer

Services Sales Force Enablement

Mobile

CRM/SFA

Reporting &

KPI Tracking

Admin

enablement e.g. time reporting,

PO approval

Other gadgets,

widgets &

utilities

Mobile SaaS

Solutions

SMS/MMS

Marketing

Medical

Education Behaviour

Support e.g. Treatment

trackers, community

Other mobile

services

Diagnostic

Tools Mobile

Transactions

Productivity

Solutions e.g. GPS/Learning on

the Move

enable Illustrative Examples

Copyright © 2012 Accenture. All rights reserved. 37 Copyright © 2012 Accenture. All rights reserved. 37

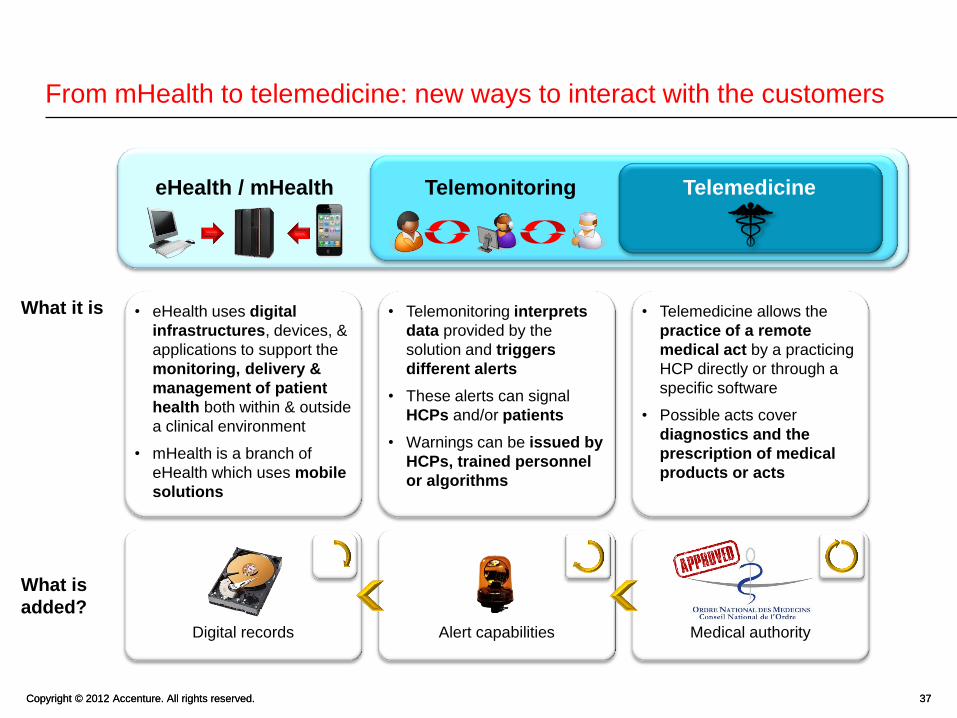

From mHealth to telemedicine: new ways to interact with the customers

eHealth / mHealth Telemonitoring Telemedicine

What it is

What is

added?

• eHealth uses digital

infrastructures, devices, &

applications to support the

monitoring, delivery &

management of patient

health both within & outside

a clinical environment

• mHealth is a branch of

eHealth which uses mobile

solutions

• Telemonitoring interprets

data provided by the

solution and triggers

different alerts

• These alerts can signal

HCPs and/or patients

• Warnings can be issued by

HCPs, trained personnel

or algorithms

• Telemedicine allows the

practice of a remote

medical act by a practicing

HCP directly or through a

specific software

• Possible acts cover

diagnostics and the

prescription of medical

products or acts

Medical authority Alert capabilities Digital records

Copyright © 2012 Accenture. All rights reserved. 39 Copyright © 2012 Accenture. All rights reserved. 39

Serious games in the healthcare environment, a few examples

Walk with me

Pedometer + Wii turns

walking into a game

Heartlands

Exploration via GPS in

phone inc. heart

monitoring

sg2: cabg

Breaking a complex procedure down step

by step to reduce risk in the real world

ReMission

Helps young people positively deal with

cancer treatment processes and recognize

symptoms

What Should We Tell The Children?

A sexual health communication tool to help

parents discuss these issues with their

children

Copyright © 2012 Accenture. All rights reserved. 40 Copyright © 2012 Accenture. All rights reserved. 40

Agenda

Welcome and Introduction A

What are the key trends reshaping the Life Sciences industry? B

The emergence of an alternative commercial model D

The use of market research and analytics to drive performance C

The growing importance of digital & mobility E

The new opportunities in supply chain F

Break

Conclusion G

Copyright © 2012 Accenture. All rights reserved. 41 Copyright © 2012 Accenture. All rights reserved. 41

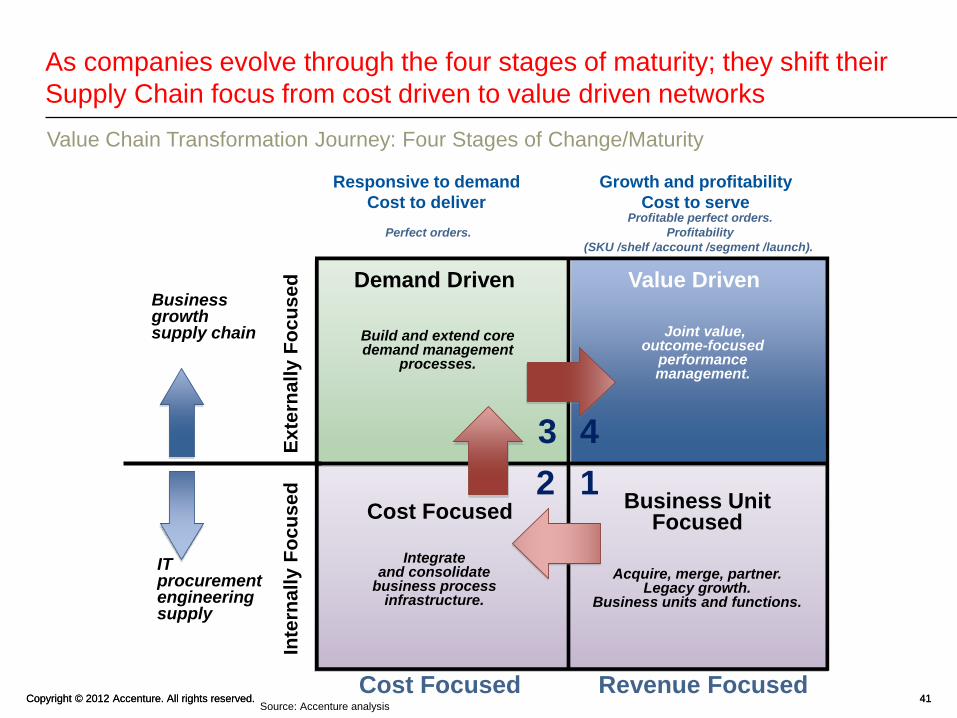

As companies evolve through the four stages of maturity; they shift their

Supply Chain focus from cost driven to value driven networks

Value Chain Transformation Journey: Four Stages of Change/Maturity

Source: Accenture analysis

Inte

rna

lly F

oc

us

ed

Ex

tern

all

y F

oc

us

ed

Cost Focused Revenue Focused

Growth and profitability

Cost to serve

Responsive to demand

Cost to deliver

Acquire, merge, partner.Legacy growth.

Business units and functions.

Joint value, outcome-focused

performance management.

Value Driven

Business UnitFocused

Integrate and consolidate

business process infrastructure.

Build and extend core demand management

processes.

Demand Driven

Cost Focused12

3 4

Profitable perfect orders.

Profitability

(SKU /shelf /account /segment /launch).

Perfect orders.

ITprocurement engineeringsupply

Business growth supply chain

Copyright © 2012 Accenture. All rights reserved. 42 Copyright © 2012 Accenture. All rights reserved. 42

In the Pharmaceutical industry, the key is to be right, fast & efficient and

endorse a customer centric mindset throughout the entire Supply Chain

Life Sciences Speed to Customer

↑ Revenues through innovative, customer-centric products and services and efficient new product launches

↑ Margins through operational excellence and optimal utilization of resources

↑ Perfect Order Performance with supply chain speed, responsiveness and improved forecasting accuracy

↑ Agility & Security by positioning the right supply chain model to meet quality & regulatory requirements

↑ Building Collaborative Networks to improve speed and efficiency across the value chain

↓ Costs by streamlining processes and eliminating inefficiencies

S2C Outcomes with Leaders

BEING RIGHT

• Ensuring safe, secure and compliantproduct supply globally

BEING FAST

• Delivering the right products to the right markets & customers when they want it and faster than the competition

BEING EFFICIENT

• Streamlining the organization to operate in the leanest, most cost appropriate manner possible

Copyright © 2012 Accenture. All rights reserved. 43 Copyright © 2012 Accenture. All rights reserved. 43

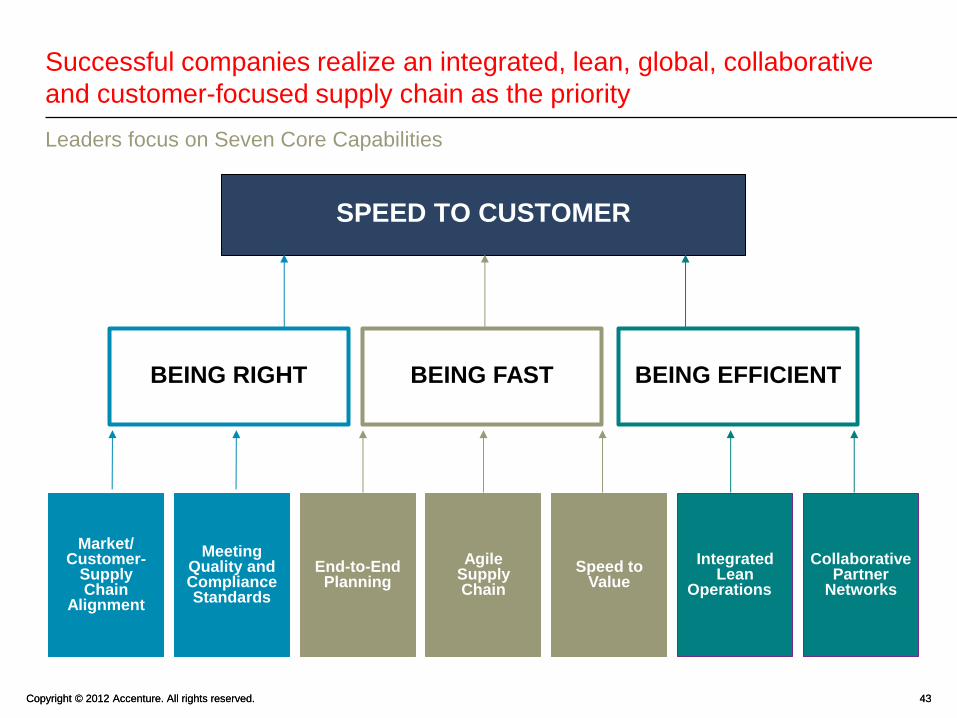

Successful companies realize an integrated, lean, global, collaborative

and customer-focused supply chain as the priority

Leaders focus on Seven Core Capabilities

Market/ Customer-

Supply Chain

Alignment

Meeting Quality and Compliance Standards

End-to-End Planning

Agile Supply Chain

Speed to Value

Integrated Lean

Operations

Collaborative Partner

Networks

BEING RIGHT BEING FAST BEING EFFICIENT

SPEED TO CUSTOMER

Copyright © 2012 Accenture. All rights reserved. 44 Copyright © 2012 Accenture. All rights reserved. 44

Agenda

Welcome and Introduction A

What are the key trends reshaping the Life Sciences industry? B

The emergence of an alternative commercial model D

The use of market research and analytics to drive performance C

The growing importance of digital & mobility E

The new opportunities in supply chain F

Break

Conclusion G

Copyright © 2012 Accenture. All rights reserved. 45 Copyright © 2012 Accenture. All rights reserved. 45

Appendix