how to maximise the potential of buying or selling a business in today's economic climate...

TRANSCRIPT

Planning is everything:

How to maximise the potential of buying or selling a business in today’s

economic climate

Thursday 13 September 2012

How to maximise the potential of buying or selling a business in today’s economic climate

Rowan Andrews Team Leader, Shirlaws UK

Agenda

• Your business journey • The economic cycle• Timing• Building the value of your business

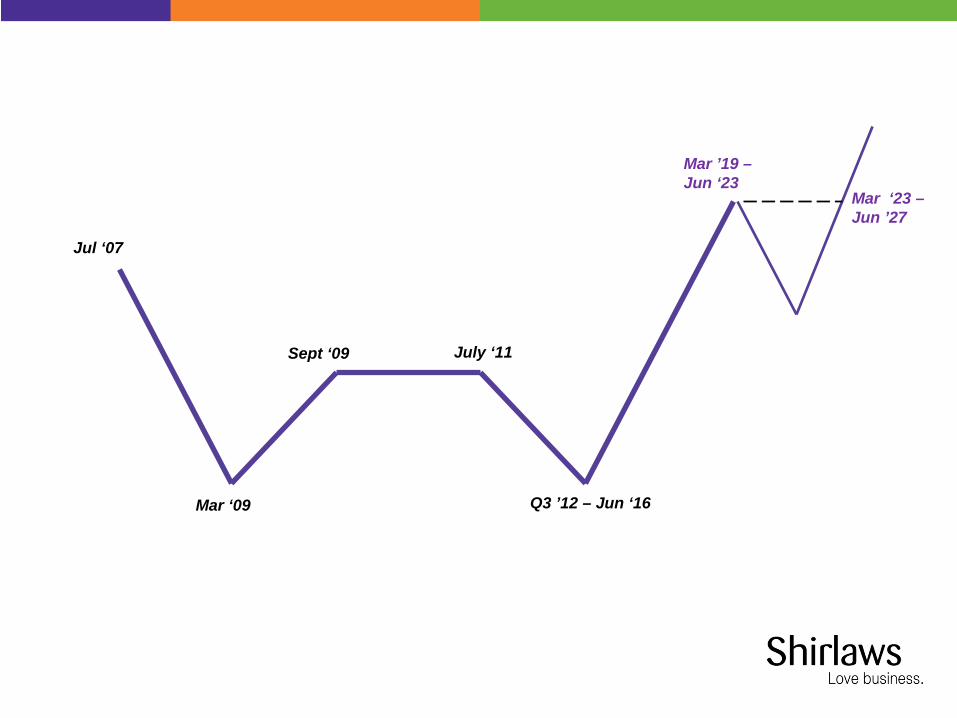

Mar ‘23 –Jun ’27

Jul ‘07

Mar ‘09

Sept ‘09

Q3 ’12 – Jun ‘16

Mar ’19 –Jun ‘23

July ‘11

Mar ‘21 - Jun ‘25

Mar ‘23 –Jun ’27

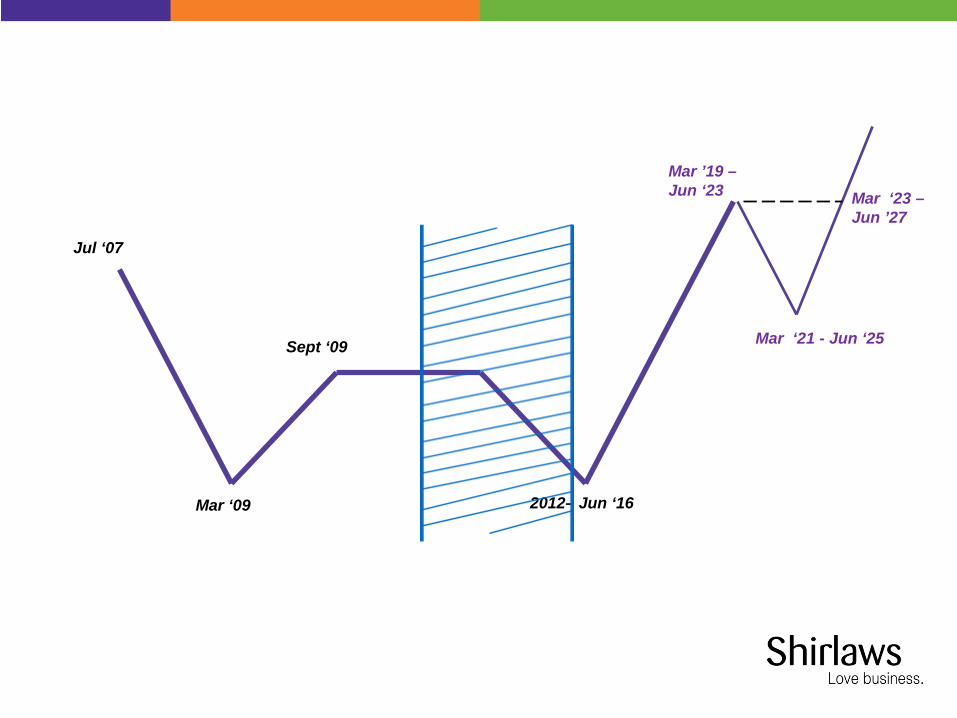

Jul ‘07

Mar ‘09

Sept ‘09

2012– Jun ‘16

Mar ’19 –Jun ‘23

Mar ‘21 - Jun ‘25

Mar ‘23 –Jun ’27

Jul ‘07

Mar ‘09

Sept ‘09

Mar ’12 – Jun ‘16

Mar ’19 –Jun ‘23

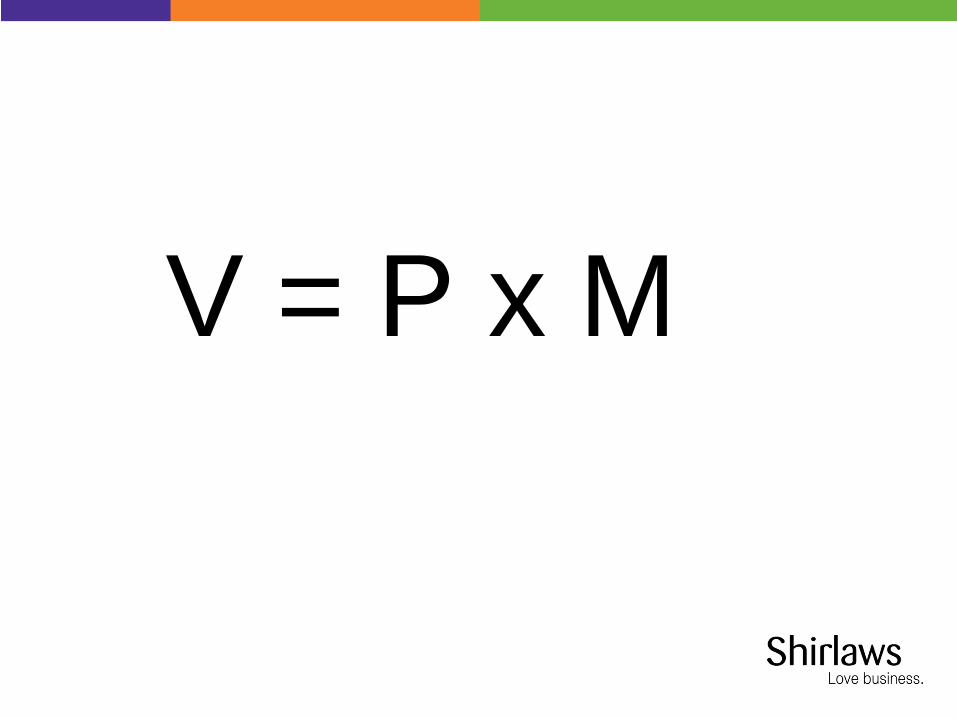

V = P x M

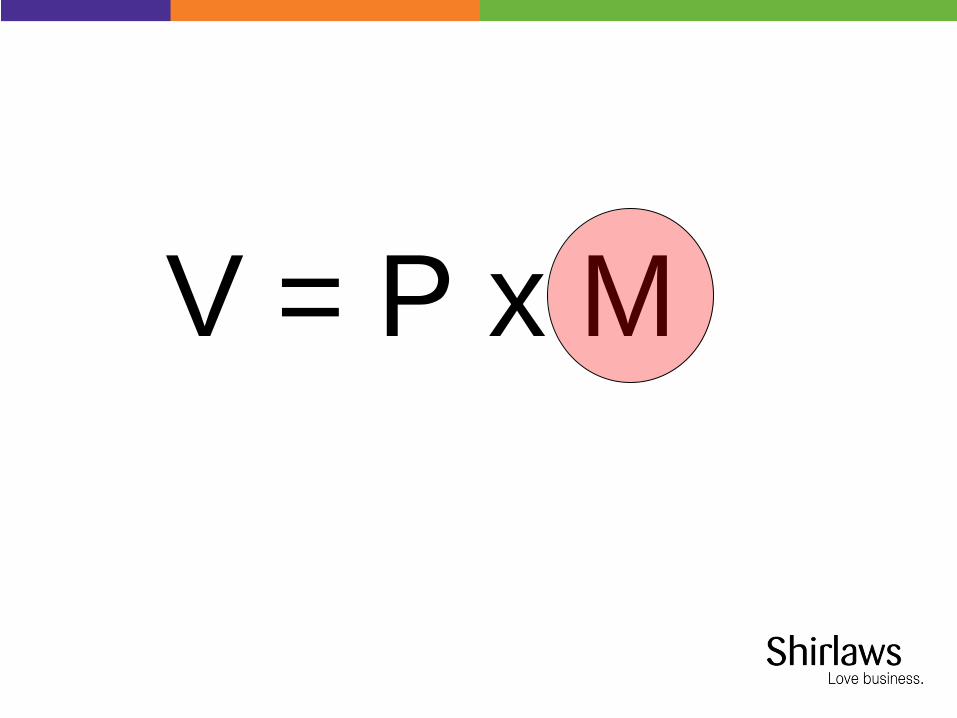

V = P x M

How to maximise the potential of buying or selling a Business in today’s Economic Climate 13 Sept 2012

Justin Ray Head of Corporate Finance

Critchleys is a trading name of Critchleys LLP

© Critchleys 2012 Content is for information only. No action should be taken without seeking professional advice.

© Critchleys 2012

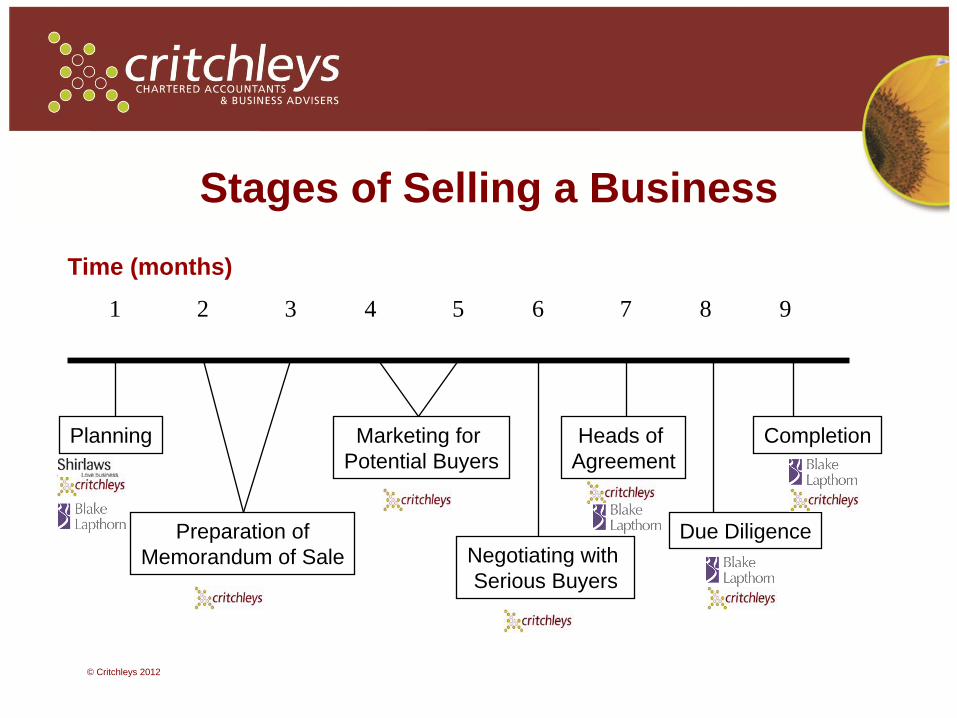

Stages of Selling a Business

© Critchleys 2012

Preparation of Memorandum of Sale

Time (months)

1 2 3 4 5 6 7 8 9

Planning Marketing for Potential Buyers

Negotiating with Serious Buyers

Heads of Agreement

Due Diligence

Completion

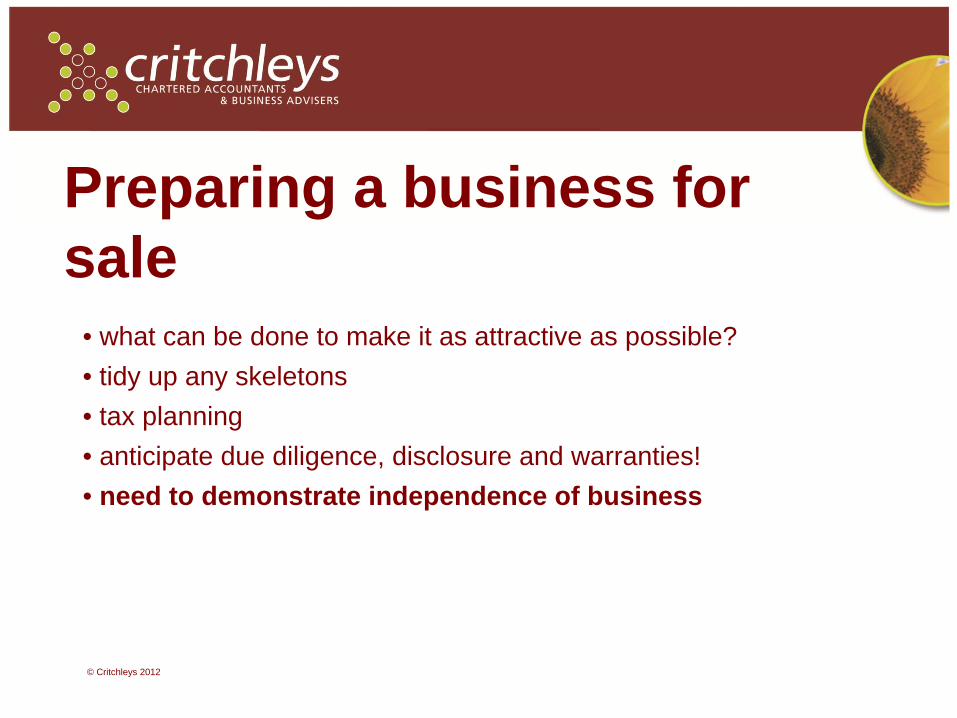

Preparing a business for sale

© Critchleys 2012

• what can be done to make it as attractive as possible?• tidy up any skeletons• tax planning• anticipate due diligence, disclosure and warranties!• need to demonstrate independence of business

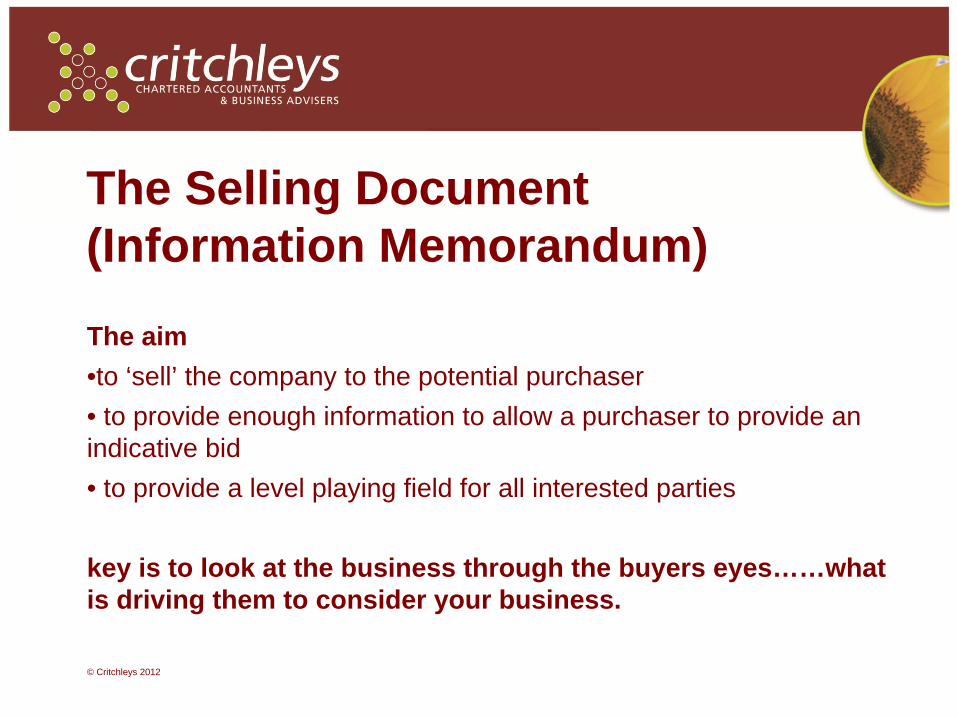

The Selling Document (Information Memorandum)

© Critchleys 2012

• first impression! • preserves market sensitive information• identifies advantages to purchaser• identifies opportunities for the business• highlights strengths of the business• describes people and business in commercial terms

The Selling Document (Information Memorandum)

© Critchleys 2012

The aim•to ‘sell’ the company to the potential purchaser• to provide enough information to allow a purchaser to provide an indicative bid• to provide a level playing field for all interested parties

key is to look at the business through the buyers eyes……what is driving them to consider your business.

The Process - making approaches

© Critchleys 2012

• depends on circumstances- small market/obvious acquirers – “confidential approaches” - directly by phone - approach the right person!- don’t blanket mail - commercial risk- non disclosure agreement prior to issuing information document

The Process - receipt of offers

© Critchleys 2012

• inevitable flexibility in timetable

• offers will not be formulated in the same way - need to clarify and evaluate

• highest price not automatically best deal

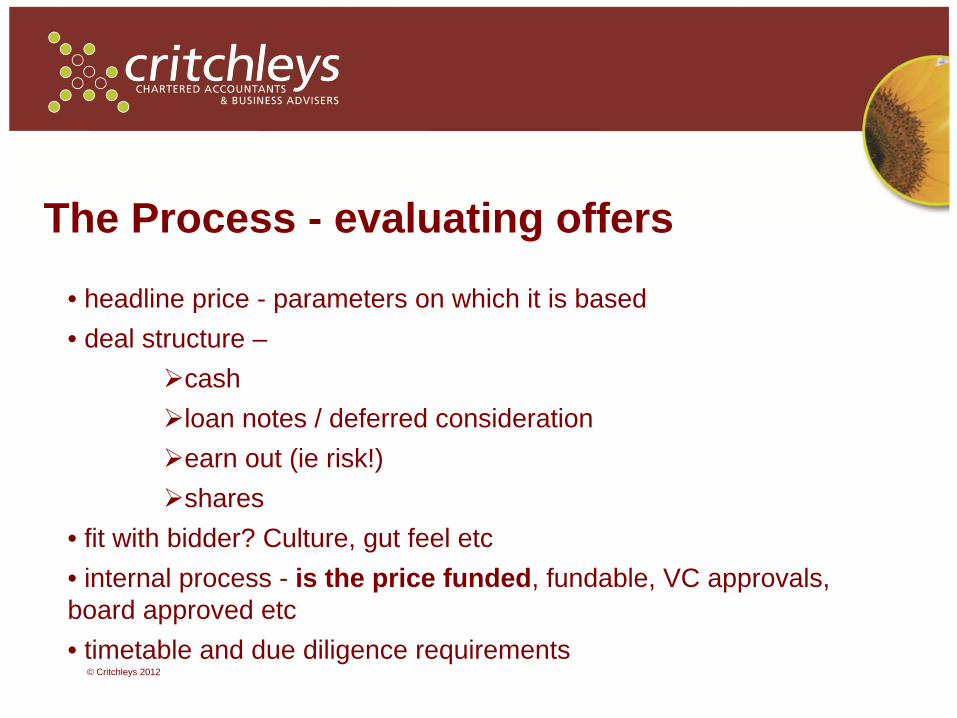

The Process - evaluating offers

© Critchleys 2012

• headline price - parameters on which it is based• deal structure –

cashloan notes / deferred considerationearn out (ie risk!)shares

• fit with bidder? Culture, gut feel etc• internal process - is the price funded, fundable, VC approvals, board approved etc• timetable and due diligence requirements

The Process - moving towards Heads of Terms

© Critchleys 2012

• may be one clear preferred bidder• if not - need to be clear with bidders where process is at?• seek clarification, seek second round bids• keep the playing field level• tax!• get to acceptable offer and then strike heads

The Process – managing due diligence

© Critchleys 2012

• know the likely problems up front

• aim for no surprises – surprises lead to price adjustments!

Legals –

© Critchleys 2012

• complex process that involves specialist corporate lawyers

Valuation and Structure

© Critchleys 2012 Content is for information only. No action should be taken without seeking professional advice.

© Critchleys 2012

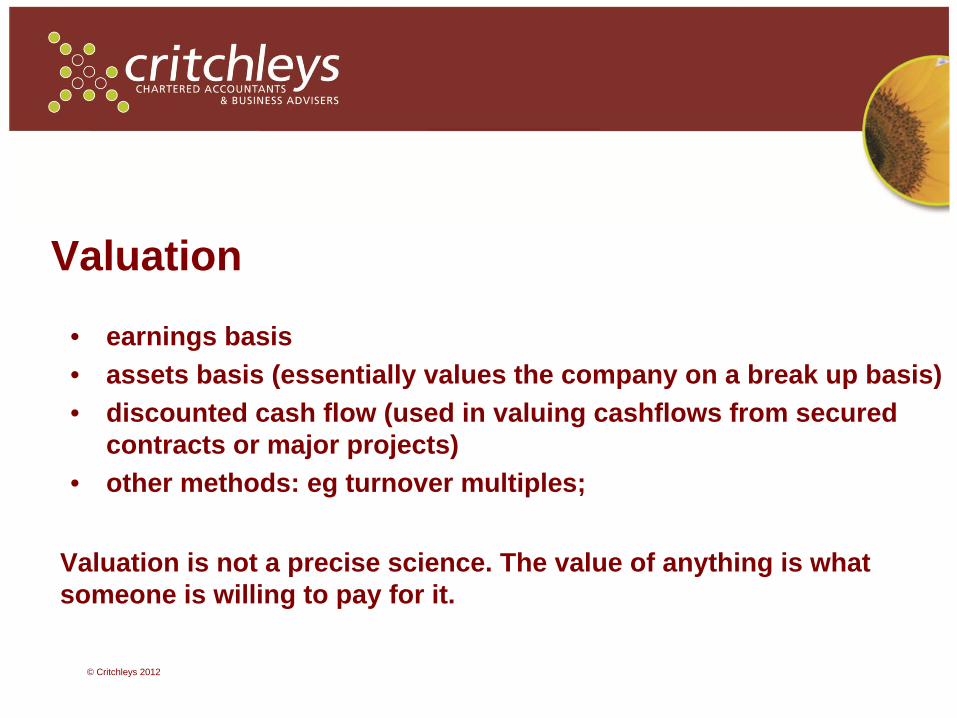

Valuation

• earnings basis• assets basis (essentially values the company on a break up basis)• discounted cash flow (used in valuing cashflows from secured

contracts or major projects)• other methods: eg turnover multiples;

Valuation is not a precise science. The value of anything is what someone is willing to pay for it.

© Critchleys 2012

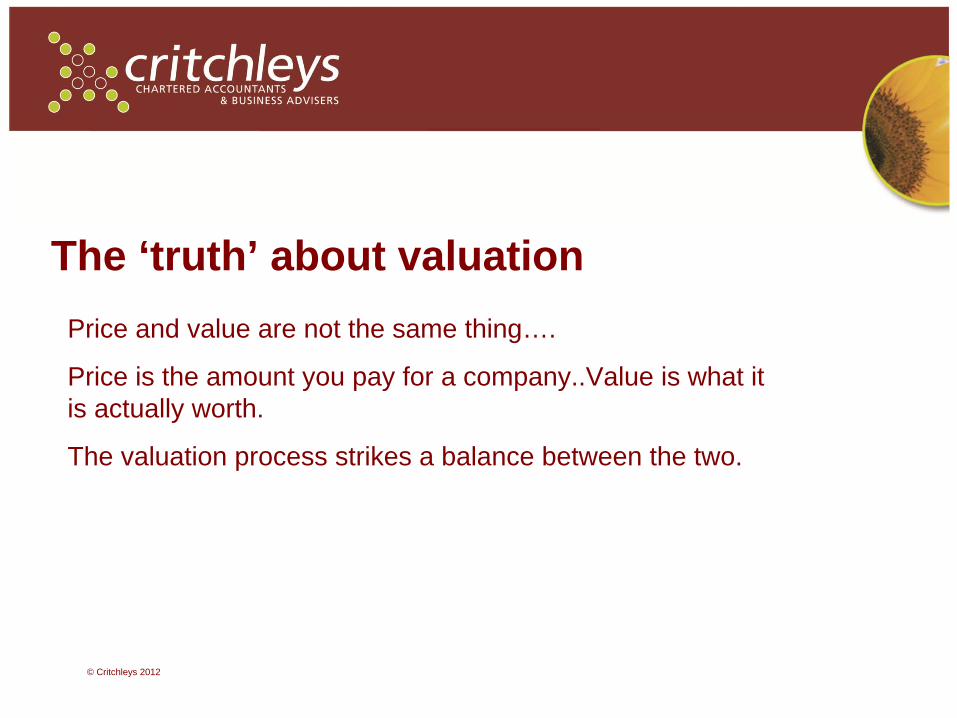

The ‘truth’ about valuationPrice and value are not the same thing….

Price is the amount you pay for a company..Value is what it is actually worth.

The valuation process strikes a balance between the two.

Enterprise Value, Equity Value and Asset Value

Enterprise Value

Value of Debt

Equity Value

Net Book Value of Assets

Goodwill

Net Book Value of Assets

Enterprise Value

Value of excess cash

Equity Value

Goodwill

Or....

Either...

© Critchleys 2012

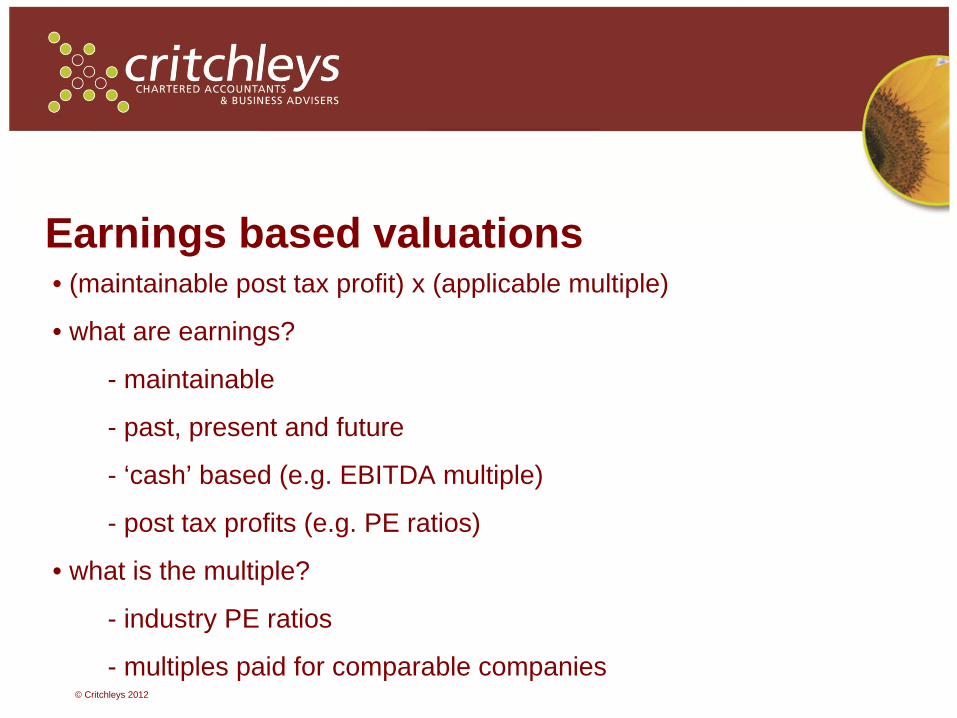

Earnings based valuations• (maintainable post tax profit) x (applicable multiple)

• what are earnings?

- maintainable

- past, present and future

- ‘cash’ based (e.g. EBITDA multiple)

- post tax profits (e.g. PE ratios)

• what is the multiple?

- industry PE ratios

- multiples paid for comparable companies© Critchleys 2012

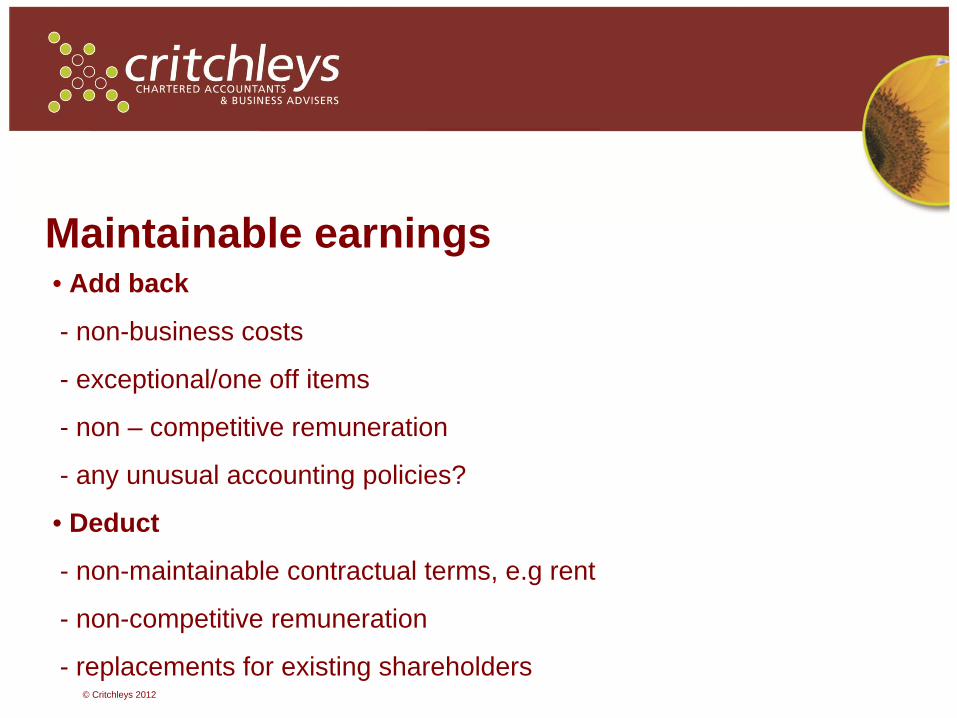

Maintainable earnings• Add back

- non-business costs

- exceptional/one off items

- non – competitive remuneration

- any unusual accounting policies?

• Deduct

- non-maintainable contractual terms, e.g rent

- non-competitive remuneration

- replacements for existing shareholders© Critchleys 2012

Maintainable earnings

• past, present, future or a mix of the three

• growth profile of the company

• structure of consideration

© Critchleys 2012

Multiples - Comparable companies• similarity of operations

• asset base

• gearing

• flexibility of workforce

• tax

© Critchleys 2012

Multiples - Comparable companies• for listed companies a discount to the adjusted PE is required to take account of the following in particular

- marketability of shares

- size of organisation

• discount 40-60% depending on quality of company

•.....but can your company attract a premium due to key USP’s or competitive advantage.

• P/E arbitrage

© Critchleys 2012

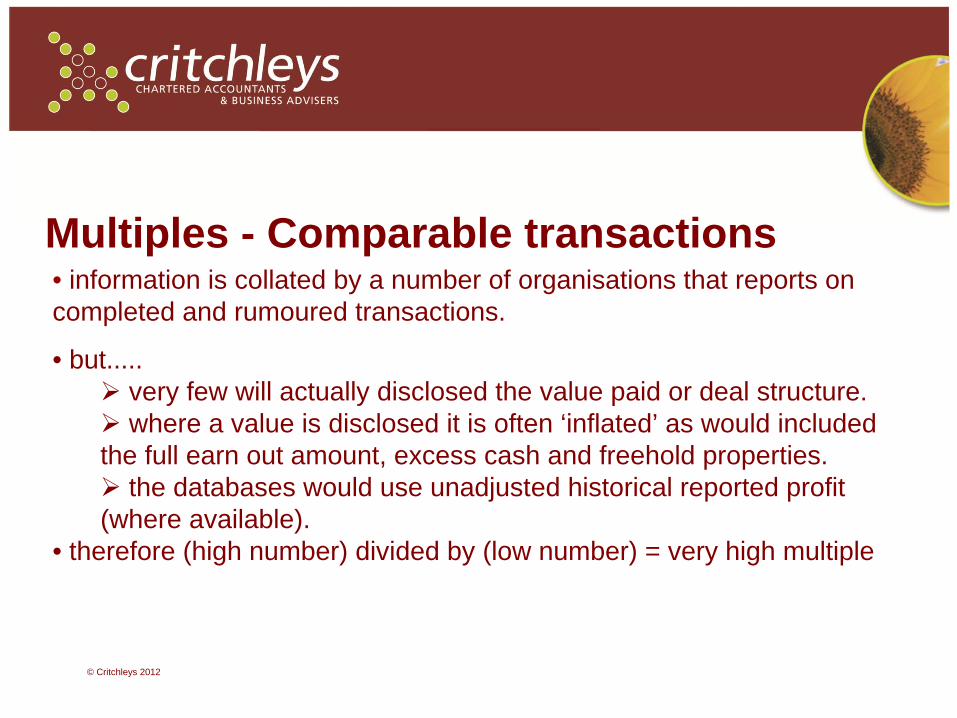

Multiples - Comparable transactions• information is collated by a number of organisations that reports on completed and rumoured transactions.

• but.....very few will actually disclosed the value paid or deal structure.where a value is disclosed it is often ‘inflated’ as would included

the full earn out amount, excess cash and freehold properties.the databases would use unadjusted historical reported profit

(where available).• therefore (high number) divided by (low number) = very high multiple

© Critchleys 2012

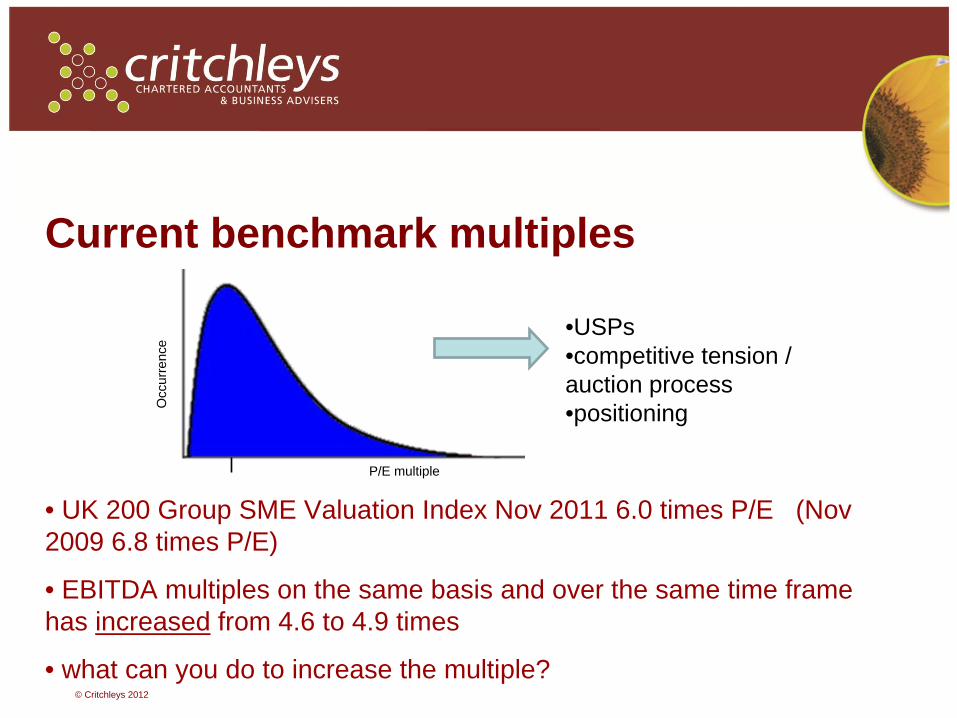

Current benchmark multiples

P/E multiple

Occ

urre

nce

• UK 200 Group SME Valuation Index Nov 2011 6.0 times P/E (Nov 2009 6.8 times P/E)

• EBITDA multiples on the same basis and over the same time frame has increased from 4.6 to 4.9 times

• what can you do to increase the multiple?© Critchleys 2012

•USPs•competitive tension / auction process•positioning

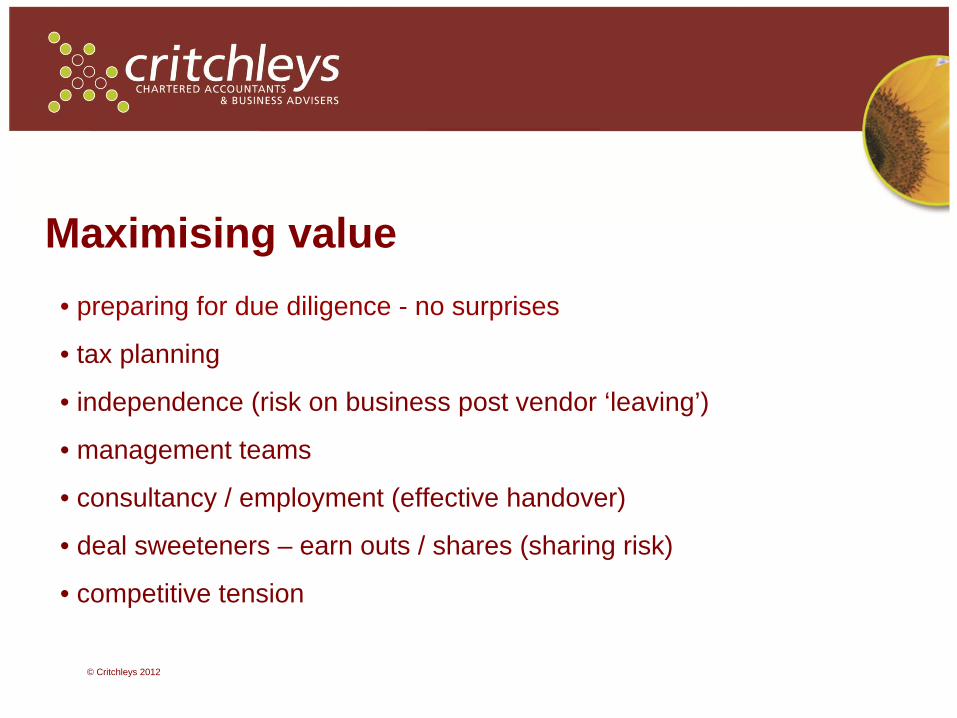

Maximising value

© Critchleys 2012

• preparing for due diligence - no surprises

• tax planning

• independence (risk on business post vendor ‘leaving’)

• management teams

• consultancy / employment (effective handover)

• deal sweeteners – earn outs / shares (sharing risk)

• competitive tension

www.critchleys.co.uk

Planning is everything:

How to maximise the potential of buying or selling a business in today’s economic

climate

Edward LeeHead of Corporate Finance

[email protected]: 01865 254222

Who is the buyer likely to be and why?

Private Equity– Very active?– What excites them?– Scaleability?

Trade Buyer– How has your sector faired?– Market noise?– Exit strategy?

MBO– Known entity?– Lower price = less risk?– Funding?

Who is the buyer likely to be and why?

Consolidator– The cycle– The “King maker”

Overseas interest– What are we seeing?– Why are we seeing it?

First impressions count!

Legal audit– It’s like buying a house– Good and bad seen in context

How do you make a good first impression?– Pre sale grooming– Tidy up!– Review contracts

2nd tier management– How good are they?– Why is it important?

Documents

Confidentiality and Exclusivity Agreements– Confidentiality

How to keep a secret?At what stage?

– ExclusivityOnly game in town or auctionTimetabling and get out of jail free cards

Heads– A summary– A moral stick– Time well spent?

Documents

SPA– Shares v assets– Narrative– Warranties/Disclosure– Tax Deed

Disclosure Letter– The more the merrier– Detail is everything

RiskDD– There is always a risk– Information is the key– Start process early

Warranty Insurance– What is it?– How much?– Why use it?

Limitations on warranties– All sellers?– Whole of price?– How long?– Cap, collars and floors

Buyer tactics

Paper overload– Adding pressure– Bodies required

Divide and conquer– Questioning quality of advice– The wedge

Non lawyer heads– Experienced buyer tactic– Importance of early involvement of lawyers

Buyer tactics

Tight timetables– More pressure– Late nights

Good cop bad cop– Letting the lawyers take the blame– Prophets of doom!

Industry specific tactics

Multiple4.0 Scale2.0 Brand – Brand Architecture1.5 Channel Extension1.4 Product Extension1.3 Product Innovation1.2 Systems & Infrastructure1.1 Culture & Talent1.0 Industry Benchmark0.9 Costs

0.8 Revenues0.7 Assets0.6 Liabilities

0.5 Management Team0.4 External Factors

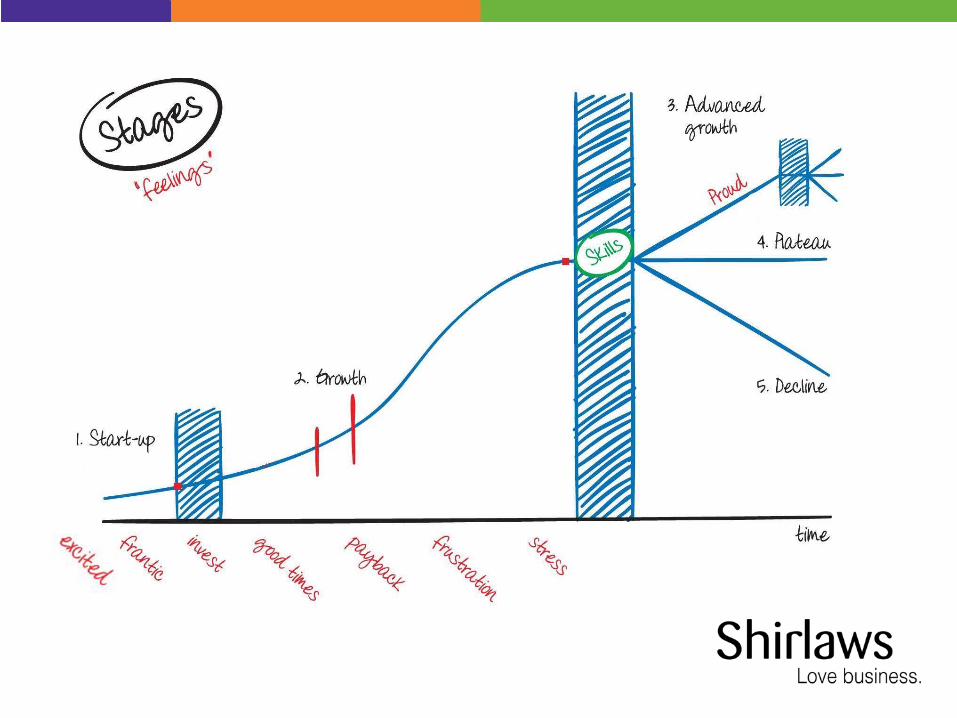

• Business cycle – Know where you are in the cycle – take the Stages test: http://www.shirlawscoaching.co.uk/stages

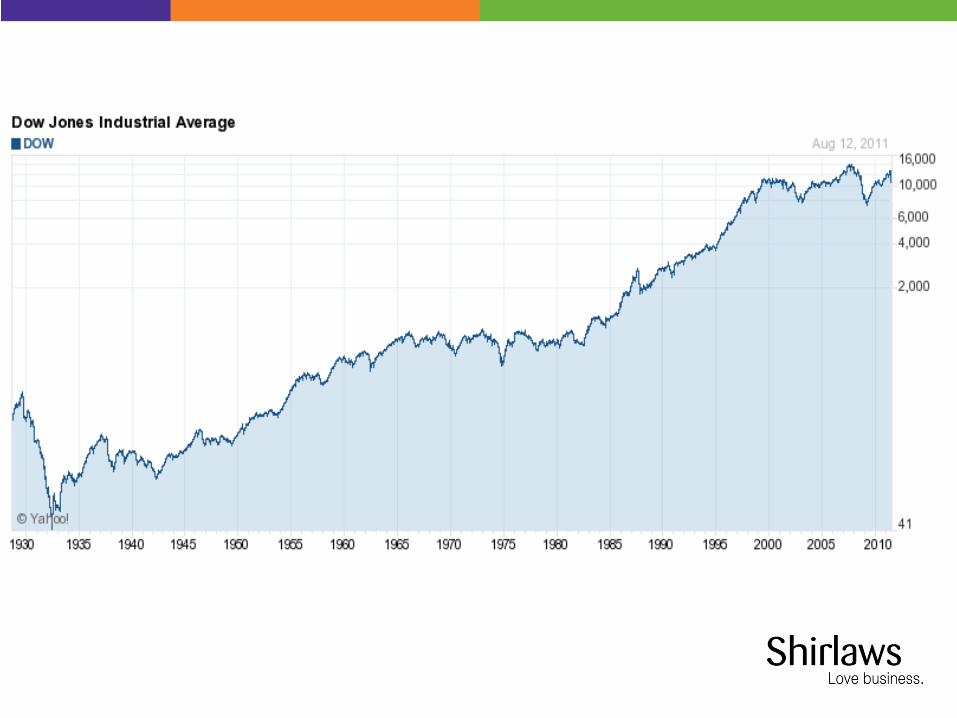

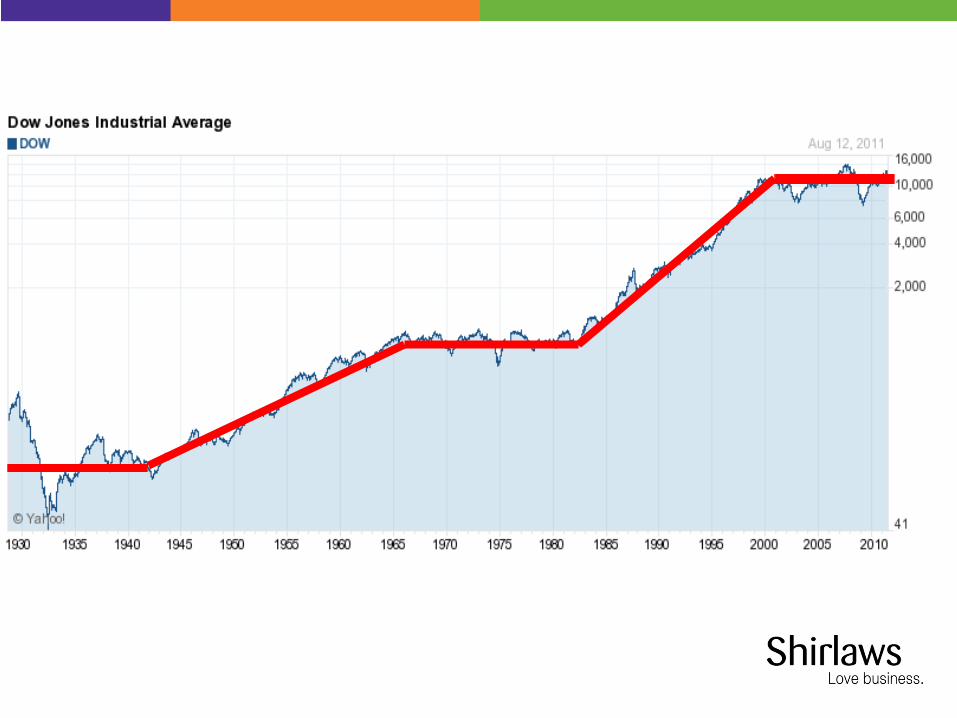

• Timing – Invest in your business now and plan to exit ahead of the market!

• Valuation = profit x multiple. Work on both to build value.

Summary