how to get governments to like bitcoin (without ruining bitcoin in the process)

TRANSCRIPT

© Promontory Financial Group, LLC. All rights reserved.

WASHINGTON, D.C. ATLANTA BRUSSELS DENVER DUBAI HONG KONG LONDON MILAN NEW YORK PARIS SAN FRANCISCO SINGAPORE SYDNEY TOKYO TORONTO

How to get Governments to Like Bitcoin(Without Ruining Bitcoin in the Process)

Adam Shapiro Promontory Financial Group

Inside Bitcoins – New YorkApril 29, 2015

2© Promontory Financial Group, LLC. All rights reserved.

The Important Prior Question

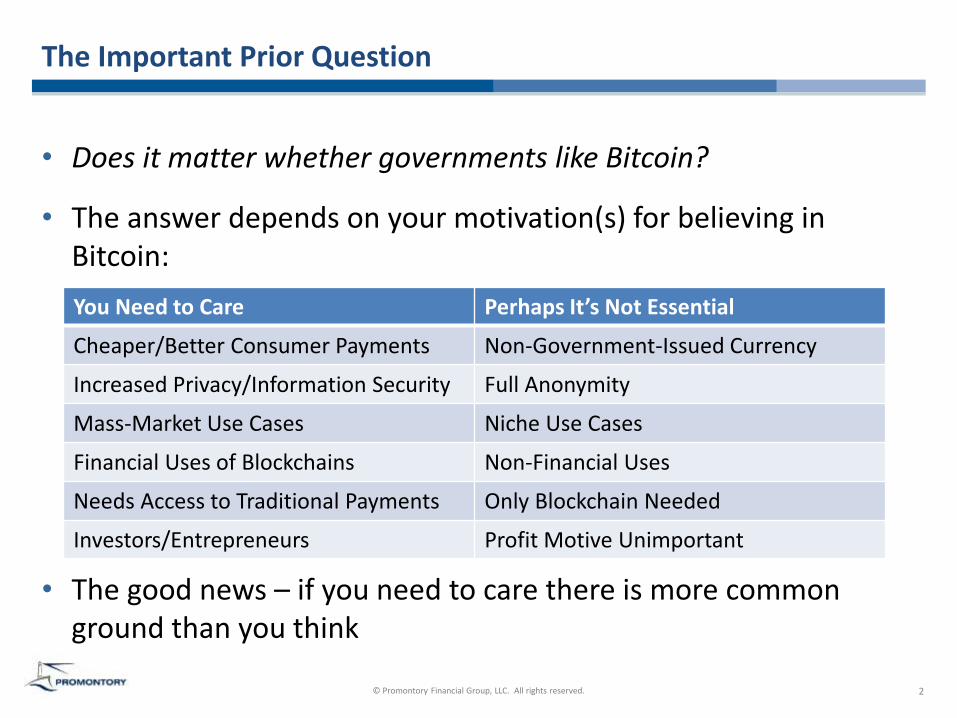

• Does it matter whether governments like Bitcoin?

• The answer depends on your motivation(s) for believing in Bitcoin:

• The good news – if you need to care there is more common ground than you think

You Need to Care Perhaps It’s Not Essential

Cheaper/Better Consumer Payments Non-Government-Issued Currency

Increased Privacy/Information Security Full Anonymity

Mass-Market Use Cases Niche Use Cases

Financial Uses of Blockchains Non-Financial Uses

Needs Access to Traditional Payments Only Blockchain Needed

Investors/Entrepreneurs Profit Motive Unimportant

3© Promontory Financial Group, LLC. All rights reserved.

Why Do Governments Care About Financial Services?

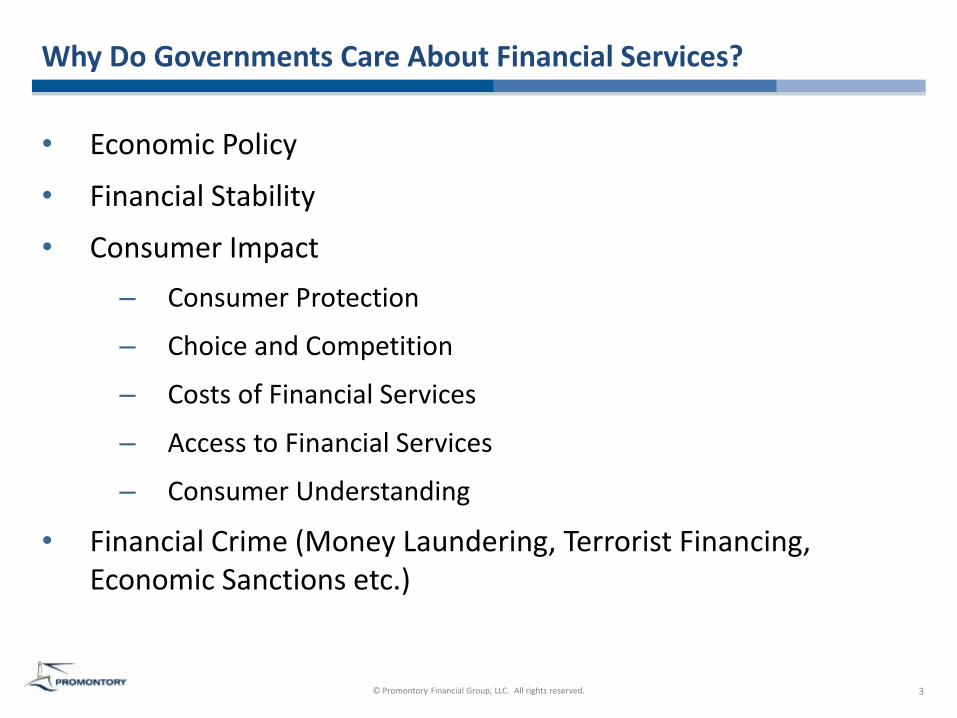

• Economic Policy

• Financial Stability

• Consumer Impact

– Consumer Protection

– Choice and Competition

– Costs of Financial Services

– Access to Financial Services

– Consumer Understanding

• Financial Crime (Money Laundering, Terrorist Financing, Economic Sanctions etc.)

4© Promontory Financial Group, LLC. All rights reserved.

Good Reasons For Governments Like Bitcoin

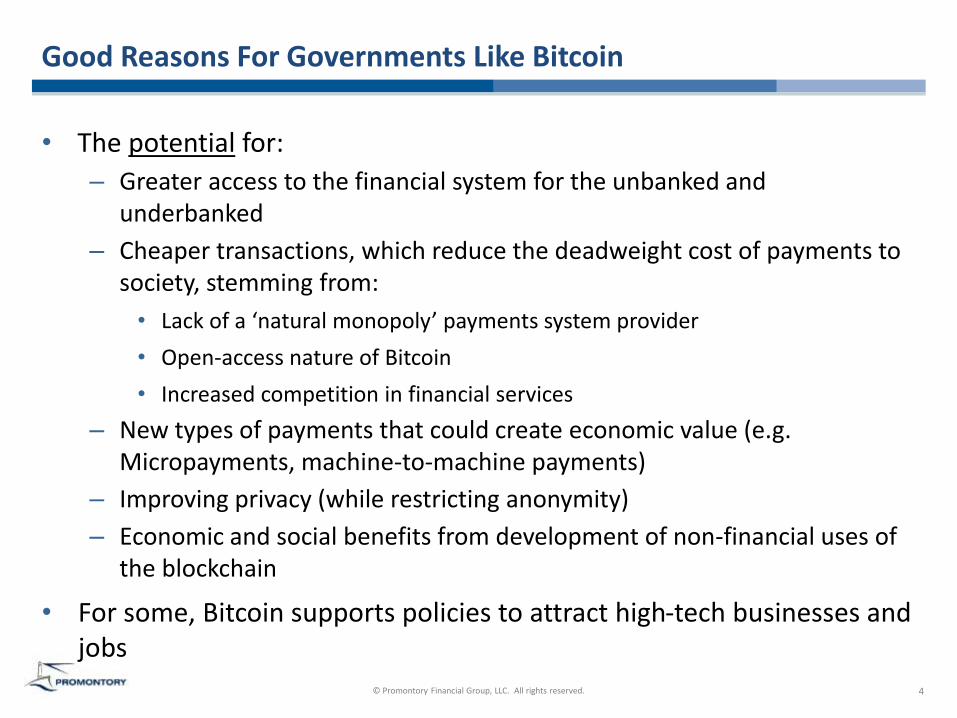

• The potential for:

– Greater access to the financial system for the unbanked and underbanked

– Cheaper transactions, which reduce the deadweight cost of payments to society, stemming from:

• Lack of a ‘natural monopoly’ payments system provider

• Open-access nature of Bitcoin

• Increased competition in financial services

– New types of payments that could create economic value (e.g. Micropayments, machine-to-machine payments)

– Improving privacy (while restricting anonymity)

– Economic and social benefits from development of non-financial uses of the blockchain

• For some, Bitcoin supports policies to attract high-tech businesses and jobs

5© Promontory Financial Group, LLC. All rights reserved.

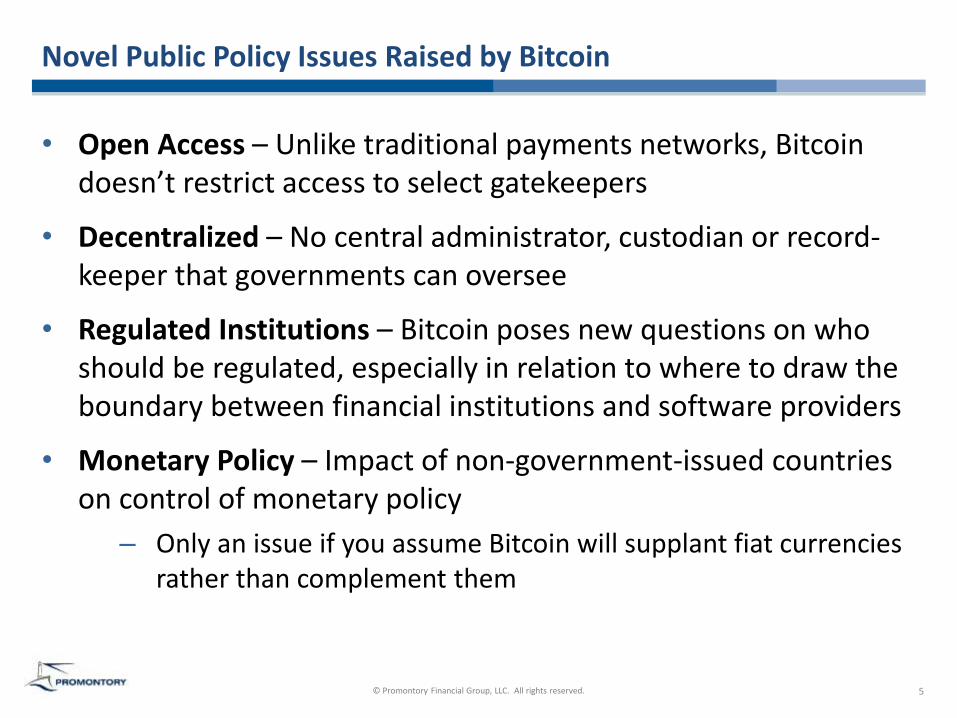

Novel Public Policy Issues Raised by Bitcoin

• Open Access – Unlike traditional payments networks, Bitcoin doesn’t restrict access to select gatekeepers

• Decentralized – No central administrator, custodian or record-keeper that governments can oversee

• Regulated Institutions – Bitcoin poses new questions on who should be regulated, especially in relation to where to draw the boundary between financial institutions and software providers

• Monetary Policy – Impact of non-government-issued countries on control of monetary policy

– Only an issue if you assume Bitcoin will supplant fiat currencies rather than complement them

6© Promontory Financial Group, LLC. All rights reserved.

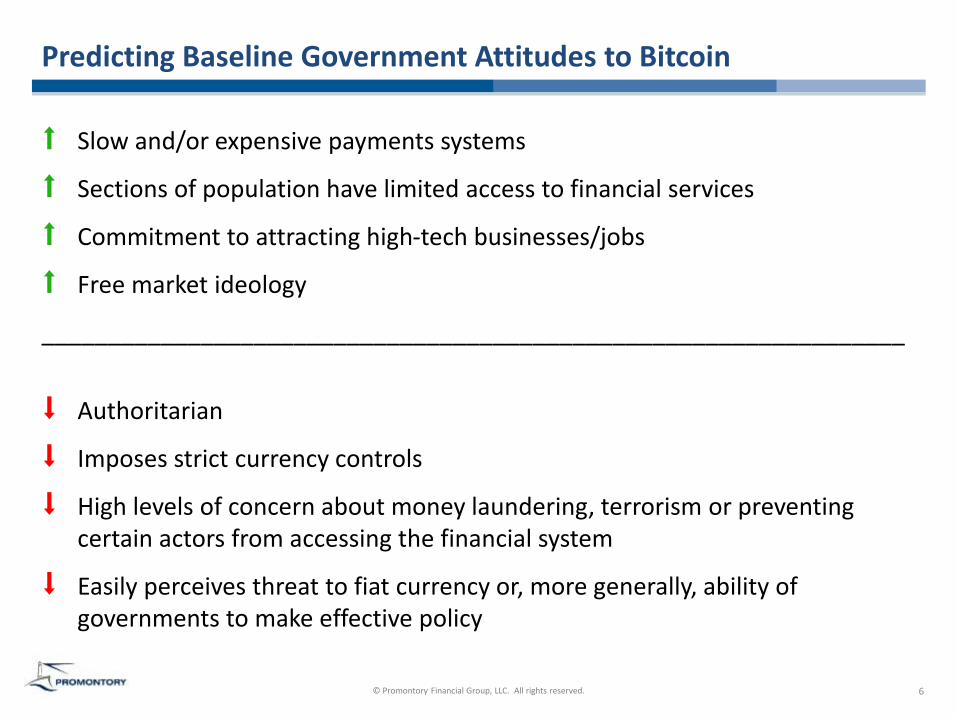

Predicting Baseline Government Attitudes to Bitcoin

⬆ Slow and/or expensive payments systems

⬆ Sections of population have limited access to financial services

⬆ Commitment to attracting high-tech businesses/jobs

⬆ Free market ideology

_________________________________________________________________

⬇ Authoritarian

⬇ Imposes strict currency controls

⬇ High levels of concern about money laundering, terrorism or preventing certain actors from accessing the financial system

⬇ Easily perceives threat to fiat currency or, more generally, ability of governments to make effective policy

7© Promontory Financial Group, LLC. All rights reserved.

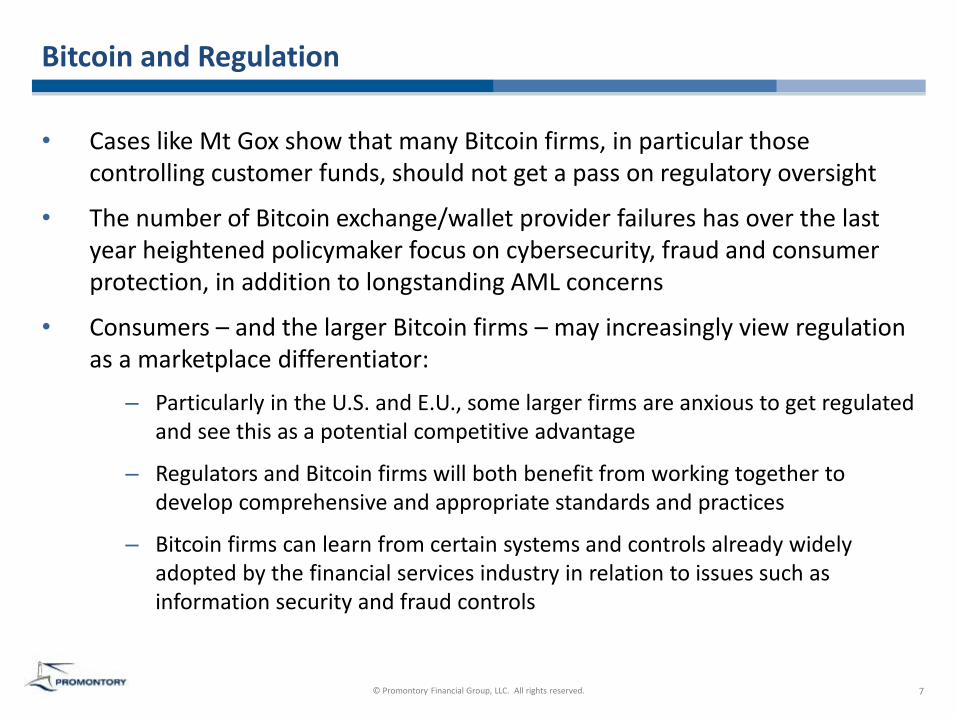

Bitcoin and Regulation

• Cases like Mt Gox show that many Bitcoin firms, in particular those controlling customer funds, should not get a pass on regulatory oversight

• The number of Bitcoin exchange/wallet provider failures has over the last year heightened policymaker focus on cybersecurity, fraud and consumer protection, in addition to longstanding AML concerns

• Consumers – and the larger Bitcoin firms – may increasingly view regulation as a marketplace differentiator:

– Particularly in the U.S. and E.U., some larger firms are anxious to get regulated and see this as a potential competitive advantage

– Regulators and Bitcoin firms will both benefit from working together to develop comprehensive and appropriate standards and practices

– Bitcoin firms can learn from certain systems and controls already widely adopted by the financial services industry in relation to issues such as information security and fraud controls

8© Promontory Financial Group, LLC. All rights reserved.

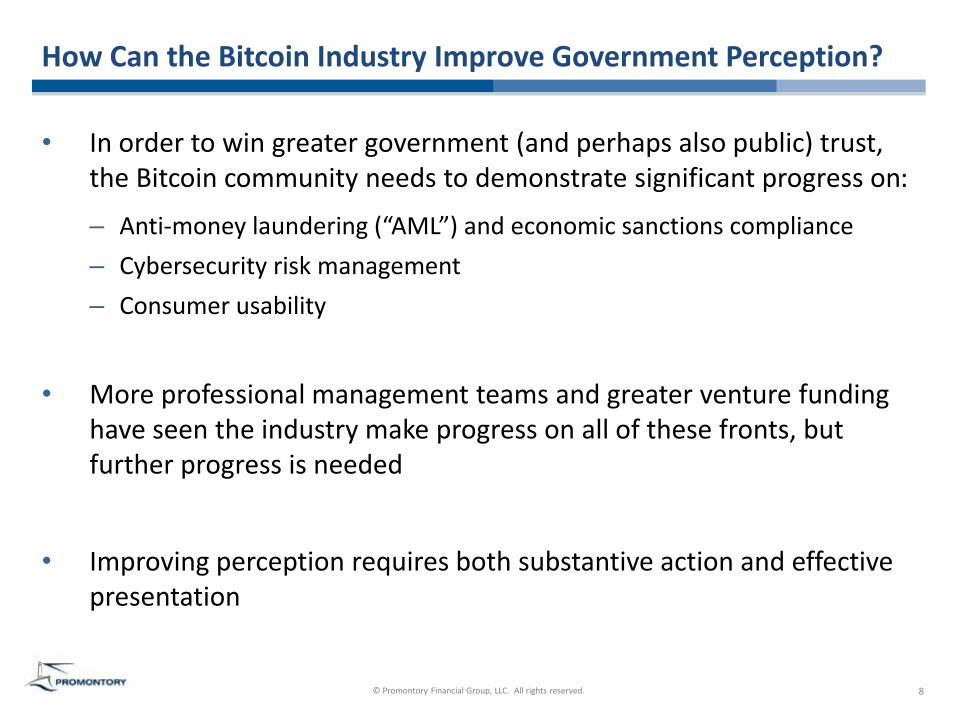

How Can the Bitcoin Industry Improve Government Perception?

• In order to win greater government (and perhaps also public) trust, the Bitcoin community needs to demonstrate significant progress on:

– Anti-money laundering (“AML”) and economic sanctions compliance

– Cybersecurity risk management

– Consumer usability

• More professional management teams and greater venture funding have seen the industry make progress on all of these fronts, but further progress is needed

• Improving perception requires both substantive action and effective presentation

9© Promontory Financial Group, LLC. All rights reserved.

AML/Sanctions Challenges

• The quasi-anonymity of Bitcoin raises AML and economic sanctions risks

• Bitcoin exchange and hosted wallet firms (in most respects) have no more difficulty getting Know Your Customer information than other online financial services firms

• However, these firms have no effective way to know the identity of their customers’ counterparties for digital currency to digital currency transactions. This inhibits their ability to:

– Conduct fully-effective sanctions screening

– Implement transaction monitoring rules based on counterparties (e.g., by country risk of counterparties)

– Comply with the Financial Action Task Force Recommendation 16 (and national government implementations thereof, such as the Travel Rule)

• This “Know Your Counterparty” issue does not simply reflect unwillingness by the industry to address this issue. Rather, open-access financial protocols such as Bitcoin cannot use the ‘closed-shop’ nature of traditional financial networks to enforce compliance

10© Promontory Financial Group, LLC. All rights reserved.

AML – Current Situation and Potential Solutions

• Increased focus of policymakers discussions (e.g. FATF, recent negotiations on the E.U. 4th AML directive, U.S. starting examinations of Bitcoin firms)

• Recently-hired compliance officers in the better-funded firms are partially mitigating these risks by strengthening individual firm’s AML Programs

• However, full resolution of these issues requires industry-wide solutions, such as:

– The ability for firms to establish if another financial institution controls a specific Bitcoin address. This will allow firms to identify when they have a Travel Rule obligation and which firm(s) need to receive Travel Rule information

– Better ability for firms to identify with confidence where to return funds where they have AML concerns or are required to reject transactions

– Automated transaction monitoring that incorporates blockchain analysis

– Decentralized mechanisms by which Bitcoin users operating their own wallets can verify their own identity – and, where appropriate, elect to share that information with certain other transaction parties

• These solutions will, with the best will in the world, take time to implement

11© Promontory Financial Group, LLC. All rights reserved.

Cybersecurity Challenges

• At a protocol level, Bitcoin has to date proven (relatively) robust. However:

– Cases like Heartbleed shows the importance of the industry addressing governance and

funding to prevent industry-wide issues

– Some smaller digital currencies have failed to maintain protocol-level integrity (e.g.

Auroracoin)

• Many of the first generation of firms offering Bitcoin services suffered significant losses as a result of internal or external fraud - Mt. Gox is the most prominent example but many others

• Bitcoin also presents a problem of maintaining access to funds – many firms and consumers have also lost funds as a result of losing access to private keys (or computer hardware storing private keys)

• Leading firms have made significant progress in dealing with these issues –but further work remains

12© Promontory Financial Group, LLC. All rights reserved.

Cybersecurity - Current Situation and Potential Solutions

• Leading firms have made significant progress in addressing the security challenges that affected early adopters:

– Use of multi-signature wallets

– Cold storage retrieval that requires access to secure locations

– Better physical security for offices and key executives

– Increasing redundancy to reduce risk of losing access to funds

– Stronger controls to prevent – and promptly detect – internal fraud

• However, best practices for management of private keys remain a work in progress – and sophistication of attackers will inevitably increase as the industry grows

• The problem of private key management is not unique to Bitcoin. Firms –and those evaluating their cybersecurity arrangements – can use proven frameworks such as NIST to help manage risk

13© Promontory Financial Group, LLC. All rights reserved.

Consumer Usability - Challenges

• Irrespective of cybersecurity issues, current iterations of digital currencies are not yet ready for mass adoption:

– Levels of volatility make digital currencies too risky to be a mass-market asset class

– Without holding digital currencies, consumers currently have limited (albeit growing) ability to take advantage of their payments efficiency

– Difficult for consumers to understand and complicated for them to use

– Some digital currency firms have consumer facing materials that overstate consumer benefits relative to risks

– Lack of clarity for consumers about which firms they should trust

– No consensus about whether digital currency customers need the types of consumer protections associated with many traditional financial networks

• Bottom line – Bitcoin and other current digital currencies are not (yet) ready for the mass market. In their current form, they pose too much risk to (most) consumers and require too much consumer effort to use

14© Promontory Financial Group, LLC. All rights reserved.

Consumer Usability – Current Situation and Potential Solutions

• Leading firms are seeking to reduce current consumer risks through:

– Well-designed fee disclosures, receipts and online transaction records

– Fair and balanced marketing materials and consumer-facing materials, including disclosures of the key risks

– Strong privacy controls around customer information

– A well-defined complaints process

– Startup-friendly new product approval processes

• Firms are working on better options for consumers to hold balances in fiat currencies and facilitate more efficient payments through ‘instant exchange’ akin to currently-available merchant services. Bitcoin may need to become invisible to facilitate mass adoption

• Is adoption by traditional retail financial services firms necessary for mass adoption? (Arguably mass adoption of internet financial services relied more on traditional firms than startups)

• The ‘killer app’ could turn out to be an enterprise or B2B solution

15© Promontory Financial Group, LLC. All rights reserved.

Tips for Engaging with Governments

• Engage – Like everyone else, policymakers and regulators are more sympathetic when they can put a human face on an issue

• Encourage – Give recognition when policymakers and regulators engage constructively with the industry and avoid taking premature action

• Eliminate Exaggeration – Avoid claiming that Bitcoin has solved problems that it really hasn’t (e.g. remittance fees, blockchain transaction monitoring)

• Edit – Avoid language that policymakers and regulators will find off-putting (e.g. “The right hack to be disruptive”)

• Empathize – Show you understand and care about the public policy issues raised by Bitcoin. And understand what the particular interests are of the person you are talking to – law enforcement and consumer regulators have different priorities

• Explain – Articulate why these policy issues relate to the potential benefits of Bitcoin – and what you are doing to address them

• Examples – Offer alternative suggestions rather than criticism. For example, if a regulator proposes subjecting software companies to financial regulation the offer alternative language rather than criticism

© Promontory Financial Group, LLC. All rights reserved.

Questions?

Adam Shapiro

Director – Promontory Financial Group

+1 415 321 6404