how opening a new charge card before or during applying for a mortgage loan can hurt you

DESCRIPTION

ÂTRANSCRIPT

CREDIT SCO

RES TIPS AN

D TRICKS

The Federal Trade Commission’s February 2013 report shows that as many as 26% of people have an error on their credit report.

60% have not reviewed their credit score within past 12 months.

65% have not reviewed their credit report within past 12 months.

“4Ways American are Financially Illiterate” by Wall Street Journal published in June 2013 reported that 61% of American adults failed the basic finance test.

National independent studies show that the average American lacks the knowledge, skills and tools necessary to make the most effective decisions regarding financial matters.

Having good credit is more important in today’s economy than ever before. Just a few points on your score can be the difference between getting a home loan, auto loan, or even a credit card.

This book provides you information and tips & tricks on how to establish, re-establish good credit history and how to improve your credit score with no additional cost.

Do yourself a favor and save some money, too. Don’t pay fees to “repair” your credit history. Use this book and Do It Yourself. Texas Five Star Realty P.O. Box 261665 Plano, TX 75026 www.TexasFiveStarRealty.com

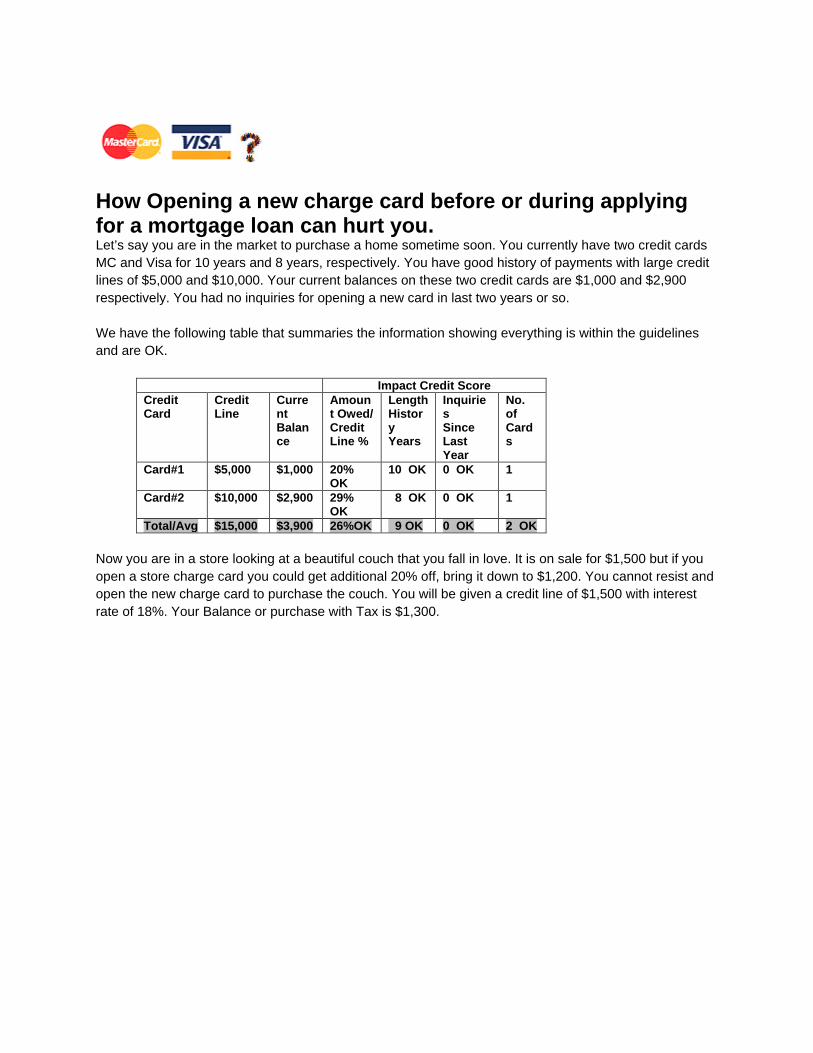

How Opening a new charge card before or during applying for a mortgage loan can hurt you. Let’s say you are in the market to purchase a home sometime soon. You currently have two credit cards MC and Visa for 10 years and 8 years, respectively. You have good history of payments with large credit lines of $5,000 and $10,000. Your current balances on these two credit cards are $1,000 and $2,900 respectively. You had no inquiries for opening a new card in last two years or so. We have the following table that summaries the information showing everything is within the guidelines and are OK.

Impact Credit Score Credit Card

Credit Line

Current Balance

Amount Owed/ Credit Line %

Length History Years

Inquiries Since Last Year

No. of Cards

Card#1 $5,000 $1,000 20% OK

10 OK 0 OK 1

Card#2 $10,000 $2,900 29% OK

8 OK 0 OK 1

Total/Avg $15,000 $3,900 26%OK 9 OK 0 OK 2 OK

Now you are in a store looking at a beautiful couch that you fall in love. It is on sale for $1,500 but if you open a store charge card you could get additional 20% off, bring it down to $1,200. You cannot resist and open the new charge card to purchase the couch. You will be given a credit line of $1,500 with interest rate of 18%. Your Balance or purchase with Tax is $1,300.

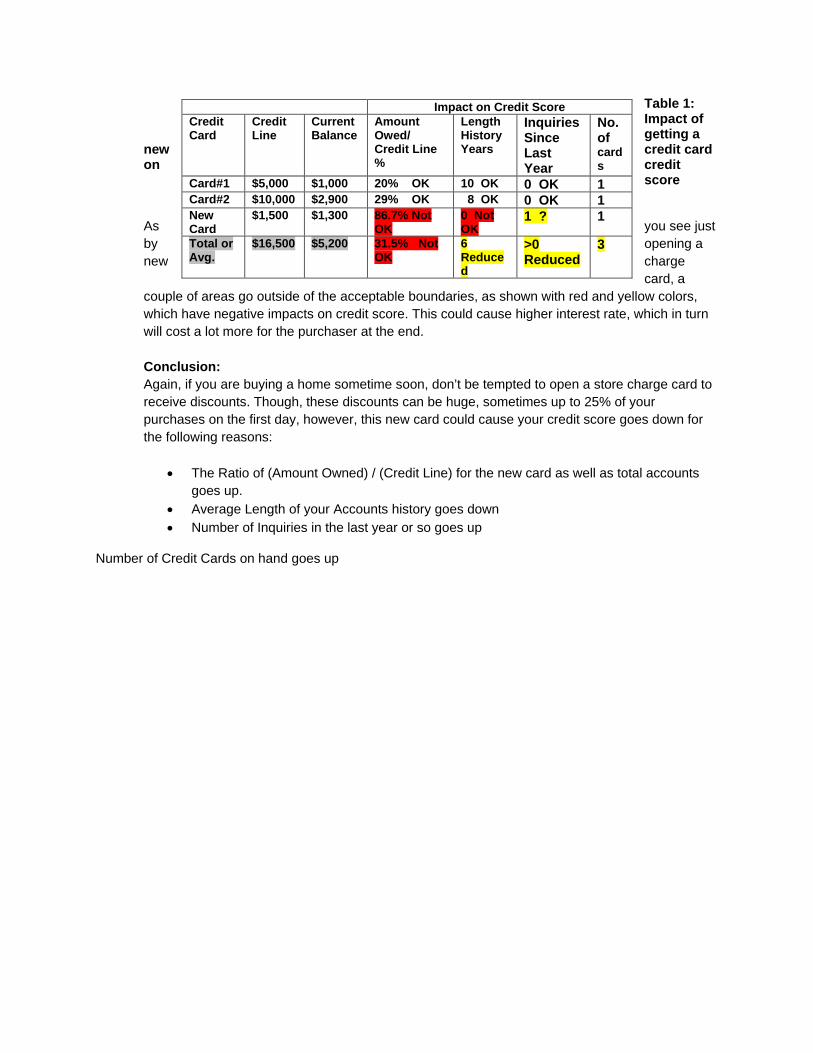

Table 1: Impact of getting a

new credit card on credit

score

As you see just by opening a new charge

card, a couple of areas go outside of the acceptable boundaries, as shown with red and yellow colors, which have negative impacts on credit score. This could cause higher interest rate, which in turn will cost a lot more for the purchaser at the end. Conclusion: Again, if you are buying a home sometime soon, don’t be tempted to open a store charge card to receive discounts. Though, these discounts can be huge, sometimes up to 25% of your purchases on the first day, however, this new card could cause your credit score goes down for the following reasons:

• The Ratio of (Amount Owned) / (Credit Line) for the new card as well as total accounts goes up.

• Average Length of your Accounts history goes down • Number of Inquiries in the last year or so goes up

Number of Credit Cards on hand goes up

Impact on Credit Score Credit Card

Credit Line

Current Balance

Amount Owed/ Credit Line %

Length History Years

Inquiries Since Last Year

No. of cards

Card#1 $5,000 $1,000 20% OK 10 OK 0 OK 1 Card#2 $10,000 $2,900 29% OK 8 OK 0 OK 1 New Card

$1,500 $1,300 86.7% Not OK

0 Not OK

1 ? 1

Total or Avg.

$16,500 $5,200 31.5% Not OK

6 Reduced

>0 Reduced

3