how omni-channel retail will reshape swiss retail floor space · 2015-05-24 · retail will...

TRANSCRIPT

Masterthese zur Erlangung des

Master of Advanced Studies in Real Estate

How Omni-Channel Retail will Reshape Swiss Retail Floor Space

Verfasserin: R. Taraborrelli

Email: [email protected] Eingereicht bei: Prof. Dr. Erik Hofmann

Universität St. Gallen, Lehrstuhl für Logistikmanagement Dufourstrasse 40a, 9000 St. Gallen, Email: [email protected]

II

Table of Contents

Abbreviations .................................................................................................................. IV

Index of Figures ............................................................................................................... V

Index of Tables ............................................................................................................. VII

Executive Summary ..................................................................................................... VIII

1 Introduction ................................................................................................................. 1

1.1 Starting position and problem .............................................................................. 1

1.2 Objective .............................................................................................................. 1

1.3 Working Hypothesis and Relevance of Topic ...................................................... 2

1.4 Scope and Non-Scope .......................................................................................... 2

1.5 Methodology ........................................................................................................ 3

1.6 Structure of Thesis, Procedure ............................................................................. 4

2 Literature and theory, principles of retail, logistics and retail properties ................... 5

2.1 Retail supply chain ............................................................................................... 5

2.2 The Value of Retail in the supply chain ............................................................. 10

2.3 Retail Properties ................................................................................................. 11

2.3.1 How is the value of retail linked to retail property? .................................... 12

2.4 Marketing and Branding ..................................................................................... 13

2.5 Porter’s five competitive forces ......................................................................... 14

3 Figures and trends in retail ........................................................................................ 16

3.1 A look outside of Switzerland ............................................................................ 16

3.2 Switzerland ......................................................................................................... 18

3.2.1 General trends in the Swiss market ............................................................. 18

3.2.2 Online retail trends in the Swiss market ...................................................... 21

3.2.3 Trends in Swiss retail space ......................................................................... 23

4 The evolution of traditional commerce ..................................................................... 24

4.1 Swiss traditional retail and previous structural changes .................................... 24

4.1.1 The arrival of specialist retailers ................................................................. 24

4.1.2 The arrival of the department store .............................................................. 25

4.1.3 Arrival of the vertical retailer ...................................................................... 26

4.1.4 The sale decouples from store ..................................................................... 27

5 Analysis of Online Retail .......................................................................................... 27

5.1 A brief history of online services ....................................................................... 27

III

5.2 Why are consumers shopping online? ................................................................ 29

5.3 The competitive advantages of online retail ...................................................... 30

5.4 Winners and losers in the supply chain .............................................................. 33

5.5 Internet capital investments are a new financial phenomenon ........................... 34

5.6 Online ecosystem of demand generation ........................................................... 35

5.7 Impact of online retail on retail real estate ......................................................... 37

6 Analysis of Omni-Channel Retail ............................................................................. 37

6.1 Evolution to omni-channel ................................................................................. 37

6.2 Why Retailers are adopting Omni-Channel ....................................................... 38

6.3 New roles of physical store in the context of omni-channel retail ..................... 38

6.4 Competitive Analysis of Omni-Channel Retail ................................................. 40

6.5 Winners and losers in the supply chain with Omni-Channel ............................. 42

6.6 Impact on retail floor space ................................................................................ 43

6.6.1 Better understanding of location .................................................................. 43

6.7 More flexible access to retail spaces .................................................................. 45

6.8 Impact of omni-channel retail on retail floor space ........................................... 45

6.9 Overview ............................................................................................................ 47

7 Conclusion ................................................................................................................ 48

7.1 Summary ............................................................................................................ 48

7.2 Discussion .......................................................................................................... 50

7.3 Outlook ............................................................................................................... 51

List of References ........................................................................................................... 52

Internet Sources .............................................................................................................. 54

Glossary .......................................................................................................................... 58

Appendix Expert Interview ............................................................................................. 60

IV

Abbreviations API Application Programming Interface

BFS Schweizer Bundesamt für Statistik

Bfs Bundesamt für Statistik, Swiss Federal Statistical Office

ETH Swiss Federal Institute of Technology Zurich

GfK GfK Switzerland AG, Detailhandel Schweiz

HSG University of St. Gallen

IG DHS Interessengemeinschaft Detailhandel Schweiz

KOF Konjunkturforschungsstelle, Swiss Economic Institute of ETH

POS Point of Sales

RFID Radio Frequency Identification

V

Index of Figures

Figure 1: Example of a Supply chain, Network of Materials, Products, Information and

Capital Flows, Wallenburg /Wieland (2011) .................................................................... 5

Figure 2: Flow of goods and information in the supply chain, (2014) ............................. 6

Figure 3: Logistic Management Task for Retailers, Fernie/ Sparks (2014) ..................... 7

Figure 4: The Evolution of the Conception of the Supply Chain, Bechtel/ Mulumundi

(1996 ................................................................................................................................. 8

Figure 5: Marketing Strategy and the Supply Chain, Mass Media vs. Fragmented Media

(2014) .............................................................................................................................. 13

Figure 6: Porter’s Five Forces Model of Competition Applied to Retail Space, (2014) 14

Figure 7: Global Growth of Online Retail Sales, 2007-2012, A.T.Kearney (2013) ....... 16

Figure 8: Growth of Online Retail in the USA. 2002-2013, Comscore (2014) .............. 16

Figure 9: Growth of Online Retail Sales as Per cent of Total in the UK, 2000-2013,

Verdict (2013) ................................................................................................................. 17

Figure 10: Growth of Online Retail Sales in the EU 2009-2014, Forrester (2014) ........ 18

Figure 11: Breakdown of Percentage of Positive (= improved) and Negative (=

worsened) Retail Profits,: KOF ETH, Credit Suisse, (2014) .......................................... 19

Figure 12: Breakdown of Retail Revenue by Class of Goods, 2001-2013, BfS (2014) 20

Figure 13: Retail Sales and Retail Prices, Change in Quarterly Sales Figures; Growth

Drivers (nominal); 2014: Outlook, BfS, Credit Suisse (2014) ....................................... 21

Figure 14: Switzerland, Growth of Online Retail Sales, 2008-2013, GfK, Credit Suisse

(2014) .............................................................................................................................. 22

Figure 15: Growth of Selected Online Shopping Searches in Switzerland: Amazon,

Zalando, Digitec, Galaxus. 2004-2014, Google Trends (Aug 2014) .............................. 23

Figure 16: Replacement Process of Swiss Food Retailers, Number of Points of Sale,

(excluding specialized dealers), Gfk Switzerland (2012) ............................................... 26

Figure 17: Retail Space growth of Migros and Coop, Years 1990-2011 in 1000 m2 GfK

Switzerland (2012) .......................................................................................................... 26

Figure 18: Timeline of Significant Events in the History of Online Services (2014) .... 29

Figure 19: Reasons Internet Users Buy Products Digitally Rather Than In-Store, across

European countries, pwc (2013c) ................................................................................... 30

Figure 20: Growth of petrol stations and convenience shops in Switzerland, GFK ....... 39

Figure 21: Example of recording neighbourhoods in New York, USA and Montreal,

Canada, livehoods.com, livehoods (2014) ...................................................................... 43

VI

Figure 22: Example of Heat map Showing Smartphone Activity near Central Park, New

York, Monday, March 29th 2010 at 6pm, Mims, C. (2012) ........................................... 44

VII

Index of Tables

Table 1: Summary of values of retail across traditional, online and omni-channel

retailers. ........................................................................................................................... 48

VIII

Executive Summary

Retail business has always been highly dynamic. The retail supply chain from supplier

to consumer is complex and continuously generates entrepreneurial opportunities for

applying new technologies to gain greater efficiency. So it is unsurprising that online

retail appeared very early on in the evolution of the online world. Online tools enable

those with expertise in the retail supply chain to quickly scale that expertise.

Now after 20 years and a sustained annual growth rate of over 10%, online retail has

become a significant part of the modern retail environment. The Swiss market is no

exception.

The significant difference of the online retail trend for retail properties is that a physical

presence in the targeted markets is no longer required. The success of the Internet as a

direct selling channel has shifted the power in the supply chain away from the

traditional gatekeepers of supply and demand, the distributors and retailers, towards

consumer and the supplier.

However even the most optimistic projections for online retail suggest that over 70% of

retail will continue to occur on the high street. Omni-channel retailing is recognition of

both this fact and the shift of power to the consumer. Consumers demand quality of

service and convenience in addition to competitive pricing. Additionally the fight for

the new commodity “awareness” will require many retailers to maintain or develop a

high street presence.

Though a 30% of sales taken away from retail floor space will inevitably have a

significant impact on property strategies. Combined with power in the supply chain

shifting toward the consumer and the supplier this will leave retail properties in a much

more competitive environment.

The winners and losers amongst retail space owners will not be evenly spread. Whilst

prime real estate is benefiting greatly from the value proposition of retail real estate

shifting towards global lead generation and brand building, for non-prime positions

deep understanding of the demands of a new generation of omni-channel retailers and

the new metrics by which they will be evaluated and differentiated is required.

1

1 Introduction

1.1 Starting position and problem

Retail properties in Switzerland are about to face big challenges. The emergence of the

Internet and e-commerce has changed the way people in the world get informed,

communicate and shop. The Internet provides an “infinite” product catalogue making

the whole world of retail accessible or at least visible. This increased transparency is

causing a strong downward price pressure on commoditised products as well as a

change of power between producer and consumer: The direct line between producer and

consumers, who can now communicate with each other directly and fast, is making

shops “superfluous”.

In the past there has always been a physical framework built on essential pillars: The

dealer who created or assembled a range of products and wanted -in one way or

another- to show it to its potential customers, the buyers who knew the point of sale or

at least how to find it, the space where traders met and the environment in where the

whole action was embedded.

The evolution of Internet retail has being going on for a few years now and it’s

beginning to leave its marks on retail properties. Weak high street retailers with poor

service offerings are going out of business. What is happening dramatically outside of

Switzerland is slowly happening within Switzerland too. Retail is unbundling.

Conventional store-based retailers must position themselves in a new order. And if true

for them, it will be also true for properties harbouring retail.

1.2 Objective

This work sets out to explain the main differences between the two worlds of traditional

and online retail and the supply chain behind them and then show how their are taking

over each others commons and merging into omni-channel retail. It makes an attempt to

understand the underlying changes and consequences that the Internet is bringing into

high street retail. The overview given by this study should contribute to recognize the

main driving its mechanism and trends.

2

1.3 Working Hypothesis and Relevance of Topic

Based on the initial position a working hypothesis is formulated here which will be

verified in the course of this research1:

Online retail is the latest incarnation of the supply chain being reconfigured towards

greater efficiency. Like with each previous waves of innovation Switzerland will not be

immune to the change. Change will bring winners and losers amongst the established

players.

The value of retail property will be adjusted to the value their clients, the new omni-

channel retail tenants, ascribe to retail space. The overall volume of trade moving to

online will inevitably drive down the sum and reconfigure the value of retail space.

Retail property may be more vulnerable to this latest supply chain reconfiguration as

the threat does not come from new physical spaces being created and can not be

controlled through building decisions.

The relevance of this investigation has to be seen in the context of a growing oversupply

of retail space in Switzerland and a further and sometimes inadequate supply of new

spaces. In numbers it means that a 10% of retail revenue moving to online from the

physical stores will lead to harder competition.

Switzerland has high quality urban centres; the population and retail spaces are

homogeneously spread across the country. However the Swiss market is not immune: as

it will be shown in this study; it has adopted previous structural changes, and customer

surveys show that there is a growing interest for Internet shopping as offerings becomes

available.

1.4 Scope and Non-Scope

The scope of this study is to analyse the changes happening to retail to understand the

role of high street shops in the context of multi- and omni-channel retail. The aim of this

is study is to outline where the value of high street shops comes from in order to deliver

a strategic overview when repositioning or planning retail space.

1 cp. Reichelt, P. (2014)

3

It is important to keep in mind that retail space has always been greatly adaptive and

that a marketing concept can turn unexpected locations into uppermost retail spaces.

In addition throughout this study, retail is looked at in a very generalized way. (I.e. food

retail or non food retail are treated equally) omitting the singularity that should be

considered for each category. This approach might result in an overgeneralization as

each category of goods, (e.g. food, non-food, fresh food, preserved food) requires a

specific supply chain, marketing and sales strategy. For different goods, the dynamics of

demand, stocking and transportation conditions, regulation, capital flow etc. vary and

function may differ radically and make some generalization may result in being only

partially or not true at all. The study will not cover the psychology and physiology of

retail, nor will it cover marketing aspects. Though all of them are crucial aspects of

retailing.

1.5 Methodology

Since a significant amount of relevant data already exists on markets and companies

operating within this business, the basis of this work is a secondary desk research,

which uses data, which has already been published by someone else at some other

time.2

Secondary data allows the study to cover a wider range of aspects (e.g. different

geographical areas, different industries) and compare them, not only with each other to

deduct new insights or plausibility, but also over different time periods, to help

understand when, where, and maybe why, changes happen. Another important

advantage of secondary data is the indirect access to information in aggregated form

that might be otherwise confidential.

Data was collected from literature, studies, reports, and statistical data from trade press,

professional institutes, regulatory and government bodies, interest groups, financial

institutions, national and international organisations, specialist organisations, business

consultants and online aggregators.

Interviews with various stakeholders were conducted in order to provide exploratory,

descriptive or explanatory case-study-like insights. The interviews are either

exploratory, aiming to help define the questions and hypothesis of the study, descriptive

2 cp. Crouch, S. (2003), p. 19, 41

4

to represent a phenomenon within its context or exploratory to presents cause-effect

relationship.3

There are limits to secondary research as a method. Being a secondary user of the data,

data may not be precisely designed for the purpose of this study or not be completely up

to date or complete. Studies may not be scientifically independent or neutral, many

being studies and surveys carried out by consultants on behalf of industry interest

groups. The author of this thesis did not carry out the correctness of the data; the

correctness of data was taken for granted. Lack of industry understanding and limited

expert knowledge of the author might also lead to misinterpreting data or misjudging

the importance of certain aspect.

1.6 Structure of Thesis, Procedure

The first chapter of this work gives an introduction to the problem, explains why the

issues tackled are current and relevant, and defines the goals and the methodology

applied to achieve them. It also defines the focus and the limits of this diploma thesis.

Chapter two conducts a literature review on the fundamentals and applied tools to

exhaustively understand the topics of the study.

Chapter three covers the principle numbers and trends, to size the on-going process.

In the ensuing two chapters, 4 and 5, the two worlds of online and traditional retail

along with their functioning mechanism will be analysed. In chapter 6 the convergence

into omni-channel retail and the resulting consequences for retail properties will be

illustrated.

Finally chapter 7 will lead to the conclusion and discussion of the study and reviewing

of the working hypothesis.

The appendix contains the interview transcripts. A read through them reveal that the

issues dealt with in these thesis are well known, current and relevant to all interviewed

stakeholders.

3 cp. Yin, R., K. (2011), p. 5

5

2 Literature and theory, principles of retail, logistics and retail properties

2.1 Retail supply chain

Retailing is about making suitable products available in the shops at the right time.

Behind this simple statement lies a complex network of product, information and capital

flows within the retail business itself, as well as in a wider integrated system aiming

toward fulfilling this goal. Figure 1 shows an example of a supply chain transforming

the raw material to the end consumer product, behind the sale of a laptop.

Figure 1: Example of a Supply chain, Network of Materials, Products, Information and Capital Flows, Wallenburg /Wieland (2011)

Retailers are intermediaries positioned towards the one end of the supply system.

Generally they purchase goods in large quantities from manufacturers or a wholesaler,

and resell them in tailored quantities in their shops. Selling goods or services to

customers they make a profit.

The sales might happen in intended physical locations like shops and markets, via

catalogue and door-to-door sales or - in more recent times in “virtual locations” - using

Internet websites, electronic payment, and delivery services.

6

Figure 2: Flow of goods and information in the supply chain, (2014)

In order to make products available to consumers retailers have to be concerned with the

flow of goods and manage their logistics in terms of product movement and demand

management. They need to know what is selling through their store and both anticipate

and react quickly to demand changes. The flow of goods and information in the supply

chain in Figure 2, displays the position of retailers at the one end of the chain as

intermediaries, delivering goods to customers and gathering information about products

towards the consumer and about the consumer’s demand towards the manufacturer.

As Figure 3, Logistic Management Task for Retailers, shows, the logistics management

task for retailers is hence - after Fernie and Sparks4 - initially concerned with managing

the five identifiably tasks, defined below: storage facilities, inventory or stock,

transportation, unitization and packaging and communication:

a. Storage facilities: These might be warehouses, distribution centres or simply the

stock rooms of stores. Retailers manage the stock in order to anticipate or react to

demand.

b. Inventory: To some extent all retailers hold a certain inventory or stock. The crucial

question for retailers is to know how much stock of each product they should hold and

where.

c. Transportation: Products need to be transported from the site of production to the

place of consumption. This transport operation might involve different forms of

transports, sizes of containers and vehicles and the scheduling of drivers and vehicles.

d. Unitization and packaging: This task is about packaging the products in an appealing

form and unit for the consumer and yet keeping the packaging cheap and easy to handle.

e. Communication: To get the products to the consumers it’s necessary to gather

information about stock, quantities, prices and movements therefore it is important to

4 cp. Fernie, J., Sparks, L., (2014), P. 3-10

7

capture information at appropriate points in the system to optimize the whole logistic

process.

Figure 3: Logistic Management Task for Retailers, Fernie/ Sparks (2014)

In the “beginning of logistics” these different task were handled as separate functional

areas or silos and while potentially optimized within each function, the process as a

whole was suboptimal in logistics terms. In the last decades logistics have been going

through a continuous evolution. In Figure 4 the supply chain schools of thought and

their conceptual development over time are displayed5: newest concepts of logistics in

fact aim to integrate these processes and lower the barriers between the functional units.

5 cp. Essig, M. et al. (2013), p. 28

8

Figure 4: The Evolution of the Conception of the Supply Chain, Bechtel/ Mulumundi (1996

Alan McKinnon synthesized this evolution in the following six trends in 1996:6

1. Increased control over secondary distribution: e.g. the movement of goods from

warehouse to shop by channelling an increasing proportion of their supplies through

distribution centres. In some sectors like food this process is almost completed.

2. Restructured logistical systems: reducing inventory and improving efficiency.

3. Adoption of “ quick response ”: aiming at cutting inventory and improve the speed of

product flow, leads to rate of stock- turn and amount of product “cross docked”7

4. Rationalization of primary distribution: retailers have extended their control

upstream (e.g. factory to warehouse) by integrating them in their network system.

5. Increased return flow of packaged material and handling equipment.

6. Introduction of supply chain management (SCM) and Efficient Consumer response

(ECR).

The overall focus of logistics moved from the functional aspects of moving products to

the attempt of developing an end-to-end supply chain. This evolution implies that the

6 cp. Fernie, J., Sparks, L., (2014), p. 6

7 When a product is sold or scanned in the shop, the information is used to inform replenishment and

reordering systems. This data are sometimes shared in real time.

9

whole supply chain can be optimized and managed towards a single entity. Managing

the logistics mix in an integrated retail supply chain, whilst balancing costs and level of

services, are the essential elements and challenges of logistics management.8

Having made their logistics more efficient, retailers have begun to collaborate with

suppliers to maximize the efficiency of the supply chain as whole. Once the functions

begun to be integrated, following key aspects emerged9:

− The supply chain took a shift from push to pull becoming a demand driven

supply chain

− Customers gained more power in the marketing channel

− Information systems become highly important to take better control of the

supply chain

− Unnecessary inventory could be eliminated

− Stakeholders of the chain started to focus on their capabilities and outsourcing

non-core activities to specialists

The information flow gained importance making significant progress with the

introduction of UPC, RFID, and POS10 etc., which allowed collection of data enterprise

wide. In this process retailers have gone from being the passive recipients of products

allocated to stores by manufacturers in anticipation of demand to being active - by

collecting and delivering all information - controller and designer of supply. They

extended their channels and moved towards collaborative strategies.

The evolution steps of supply chain management described up to this point were

certainly advanced but they were incremental rather than revolutionary. They were in

the end systems for harmonizing accounting and supply chain management and each

enterprise acquired and implemented similar systems11. The real revolution happened

when processing power of computers, fast network wired or wireless and growing data

storing capacity became available for everyone towards the end of 90’s causing a real

transformation that embraced all stakeholders involved in retailing.

The so-called “big data” meet - so Fernie and Sparks - following characteristics:

− Scale: Data comprehend massive data-sets (multi-petabytes) 8 cp. Fernie, J., Sparks, L., (2014), p. 5

9 cp. Fernie, J., Sparks, L., (2014), p. 8 10 cp. Glossary 11 cp. Niemeier, S. et al (2014), p. 68-73

10

− Distribution: Data source are dispersed outside and inside the organisation

− Diversity: Data can be semi structured, structured or combined

− Timeliness: rapid and real time

− Analytics: adaptive, learning and enabling to extract pattern through innovative,

collaborative and iterative querying

Now technology and capacity are now out there to access and process all data, to make

instant analysis of trends and shifts in sales and customers and react in real time. Data

also allow precise segmentation and targeting of customers and a sophisticated demand

generation. Retailers are only beginning to understand the opportunities connected with

it.

2.2 The Value of Retail in the supply chain

Retailers add value to the supply chain as intermediaries between supplier and

customer. Zocchi, Niemeier and Catena12 name four categories of values, retailers add

to the supply chain: pre selecting goods for sale, aggregating demand, offering sales

advice and physically moving the stock to the point of sale as defined here:

Preselection: retailer present customers with a variety of goods, often introducing

customers to new products. To the supplier they offer the service of marketing their

product in an appropriate way, implying that the product will be relevant to customers

who come to the shop. The assortment in the store might be slow or fast moving, it may

cover a multiple categories for goods or be specialized fewer. Retailer knowledge of

their customer creates value for both customers and suppliers. Their insights into

customer preferences derive from their observation and from their possession of

transaction data.

Demand aggregation: the ability to gather enough end users to a single or to several

point of sale is called demand aggregation. To the supplier this means access to more

consumers, more markets and maybe at lower costs in addition they get important

information on how much to produce at what time. For consumers the retailer’s

bargaining power with suppliers allows lower prices than individual consumers would

be able to negotiate. Even if products are distributed on large scales and worldwide, the

ability to curate a consistent and relevant offer is mainly a store- level competence and

12 cp. Niemeier, S. et al (2014), p. 30-33

11

each single location must be able to attract sufficient demand for its collection of items

on sale. Each shop must offer enough to prospective customers to justify their visit.

Sales advice: traditionally the point of sale was the place where to get the information

about product to buy and to choose, eventually in context of an attractive and inspiring

ambiance. The supplier as a matter of course has far more knowledge about his products

than retailers but also less experience in selling to customer and not enough impartiality

towards competitors. The context of the product in the shop itself is also source to

useful information for the customer: knowing what is available and how better and

worse examples look like in reality is valuable.

Physical movement of stock: the fast and efficient delivery of stock through from the

manufacturers to the supplier, to the customer through a complex network of

warehouses, distribution, delivery and return points can drive end-user prices

significantly. In the past, the responsibility for moving stock was shared by

manufacturers, logistics supplier and retailers by taking charge of one set of movements

each. But lately the value creation is drifting toward larger retailers who have the ability

of steering stock flow by either following the movements through electronic data or by

taking charge of the products right from the factory.13

2.3 Retail Properties

What services do retail spaces provide to retailers?

Looking again through the added values defined by Niemeier, Zocchi and Catena:

Preselection: Through a knowingly selection of shops around the shop, the curated

range of products offered in the retails space can even be amplified by so making it even

more relevant for potential customer to visit the specific area when in search of items.

Demand aggregation: The key contribution of properties to retail is providing footfall

and proximity through location of the property. The parameters named by Wuest +

Partner14 to rank locations as reachability, quality of infrastructure, demographic

dynamic, development of employment, attractivity of town or village, tax rate, building

industry dynamic, attractivity of the property, market liquidity, development of prices,

attractivity for institutional investors, all refer to potential rate and quality (in terms of

spending power) of footfall in the area.

13 cp. Niemeier, S. et al (2014), p. 30-33 14 Wüest & Partner (2014)a

12

Sales advice: There isn’t any service provided by the property to the value of sales

advice, this is again a key competence of the retailer and depends on his sales strategy.

Nevertheless the built environment might contribute to the adequacy of the spaces for

the purpose.

Physical movement of stock: The space of the store is where; goods are stored,

displayed and handed over to the buyer after purchasing. Therefore the service of

harbouring the goods provided by retail space to retailing is somehow fundamental.

2.3.1 How is the value of retail linked to retail property?

Profit margins determine the proportion of turnover a retailer is prepared to pay for

retail space, since the rent is a residual of turnover less cost and profit. The rent

affordable by the retailer reflects the value and its reverse, the risk, provided by the

property to a specific retail business in a determined space.15

To determine the price of retail floor space located in shopping centres, a shared risk

model is generally adopted: The rent is constituted by a base rent which is fixed and an

optional rent which is coupled to the total sales revenue of the shop in the centre.16 If

the total sales revenue exceeds the base rent by the agreed factor, then the percentage of

the total sales revenue is due to the landlord as lease. The value of the property is

therefore given by the potential total return generated on the retail space. E.g.:

Fix Base Rent for 200 m2= 1’000 CHF/ m2 x 200 m2 = 200’000 CHF

Plus 6% of sales over 200’000 CHF

The idea behind this risk-shared model there is that the centre management provides for

lead (frequency) generation. The centre management creates a destination and provides

footfall through maintenance, marketing, branding and other measures like an

appropriate and functioning infrastructure or a convenient selection of shops. In this

model, the landlord and the retailer both contribute adding value and therefore the

revenue is shared. If the centre is well managed the sales increase and both the

management and the retailers get rewarded for their performance.

For common, single retail spaces or traditional shops located in other type of buildings

than shopping centre or special locations, the price of the square meter in the market is

generally almost entirely based on the value attributed by the retailer to the location as

15 cp. Wildenauer, F. (2011) 16 Ritz, K., Hermes, A. (2014)

13

defined above. The rent is usually a fixed amount17. These yearly rents revenue and

costs flow into dynamic DCF models that deliver the present value of retail properties.

Briefly footfall and purchasing power are almost entirely given by the specific location

of the shop. It is assumed that if these two factors are high, sales return in the shop will

also be high.

2.4 Marketing and Branding

Marketing management concepts aiming to align consistently all activities of a retailing

enterprise to the demands of the sale markets18 begun to steer the supply chain by

demand, meaning not only for fulfilling a an order but also for the adaptation of new or

next generation product to customers feedback. Demand creation became demand

fulfilment.

In Figure 5 Marketing Strategy and the Supply Chain, Mass Media vs. Fragmented

Media illustrates that the improvement of the responsiveness and flexibility of the

supply chain with the associated infrastructure and information databases about the

customer led to a new buyer-seller relationship and to a shift from mass marketing to

micro marketing to mass customization.

Figure 5: Marketing Strategy and the Supply Chain, Mass Media vs. Fragmented Media (2014)

17 Interview Appendix IVX 18 cf. Essig, M. et al. (2013), P. 50-68

14

2.5 Porter’s five competitive forces

As this study is looking at how the business of retail is being reconfigured, and how the

competitive forces of this reconfiguration will affect property owners, it is valuable to

have a conceptual framework, or lens, through which to evaluate these changes.

In 1980 Michael E. Porter proposed a framework of five forces to evaluate the

competitiveness of an industry and therefore it’s attractiveness to an investor. The

original paper and his subsequent books are widely cited in the field of business

strategy. Each of the stakeholders in the supply chain, including the suppliers of retail

space, is exposed to competitive forces. This study will refer back to Porter’s

framework as a tool to evaluate the impact of changes being observed.19

Figure 6: Porter’s Five Forces Model of Competition Applied to Retail Space, (2014)

19 Porter, M., E (1980)

15

Figure 6 illustrates Porter’s five forces. In the context of retail floor space supplier the

forces can be explained in more detail:

Supplier power (retail floor space supplier)

o Footfall and proximity including concentration, quality or qualification of

footfall past the space.

o The attractiveness of environment in which it is situated including

availability and proximity of core services value such as infrastructure

(parking, public transport, delivery space) or socio-cultural values

(architecture, address, connotation, etc.).

o Cost of a retailer moving to an alternative location (e.g. customers not

knowing where the new store is).

o Local knowledge of consumer behaviour and relative opaqueness to the

retailer of alternative locations.

Buyer power (retail floor space renter)

o The brand value the retailer brings to the space: Does the retailer’s brand

generate qualified footfall?

o Knowledge of local consumers behaviour and awareness of alternative

locations.

Threat of new entrants

o Availability of new spaces for retail development e.g. de-industrialization

of cities.

o Cost of capital and the willingness to invest in developing new retail

spaces.

o Threat of substitution

o The ease with which retailers can reach and sell to their customers

without the need for retail space at all.

Rivalry between firms

o How many alternative suppliers of space are there in an area?

o How aggressively do these suppliers compete with each other?

o Supply and demand. Are there more potential renters of spaces than

space available? What is the vacancy rate?

The following chapters will refer back to these five forces and analyse how pure online

retail and omni-channel retail have, or will, change these competitive forces.

16

3 Figures and trends in retail

3.1 A look outside of Switzerland

It this chapter a quantitative overview of the phenomena will be given by looking first

globally and at countries where this trends started and that can be seen as trendsetter for

Switzerland.

Figure 7 shows the global growth of Internet sales, in 2012 the annual sales surpassed ½

trillion dollars globally. This is more than double the revenue from 5 years earlier in

2007.

Figure 7: Global Growth of Online Retail Sales, 2007-2012, A.T.Kearney (2013)

In the USA, the country that could be considered the birthplace and trendsetter for

online retail, the annual growth over the last 10 years, as shown in Figure 8 has dropped

from the 30% seen in the early 00’s to a sustained annual growth rate of a more

moderate but still substantial 10%.

Figure 8: Growth of Online Retail in the USA. 2002-2013, Comscore (2014)

17

Figure 9 shows the growth of Internet retail in the UK, the country where Internet retail

has taken the greatest share of retail overall. The value of Internet sales as a proportion

of total retail sales rose from less than 2% in 2000 to a shade under 12% in 2013. The

share has grown consistently every year including through the financial crisis of 2008

and the subsequent recession the country is only now emerging from in 2014. In

January 2013 the average value of weekly retail sales on the Internet had peaked at £

844 Millions in December 2012.

The increase in online sales is in part due to a move towards Internet only stores and

products. In 2008, online and mail-order businesses accounted for 3.4% of the total

number of enterprises in the retail industry (except of motor vehicles and motorcycles).

This had increased to 6.8% in 2011. In the music and film sector, more than half the

sales of physical products (not including downloads) are already online.

Figure 9: Growth of Online Retail Sales as Per cent of Total in the UK, 2000-2013, Verdict (2013)

The rapid growth in UK led in 2011 to the UK BIS commissioned research

“Understanding High Street Performance”20 to noting that the Internet is one of the key

threats to retail on the high streets causing a high number of shops to close. Although

Internet sales currently account for less than 10% of all retail sales some estimates

20 Genecon (2011)

18

suggest that e-commerce accounted for nearly half of all retail sales growth in the UK

between 2003 and 2010, as Internet access has become more widespread.

Across the EU-17 the trend is similar though not as dramatic as in the USA and UK.

Growth rates over the past 5 years have been dropping slightly, though they are still

around 10%, with overall revenue topping 115 Billions EUR.

Figure 10: Growth of Online Retail Sales in the EU 2009-2014, Forrester (2014)

It’s worth observing not just the growth rate and the percentage of spend being taken in

the USA, UK, and EU and globally but also the absolute value of revenue.

The top line revenue numbers are significant and the many billions flowing to online

retailers result in re-investment in the industry as a whole. New software and tools can

be funded, driving efficiency and lower cost for new entrants and making the industry

even more competitive.

3.2 Switzerland

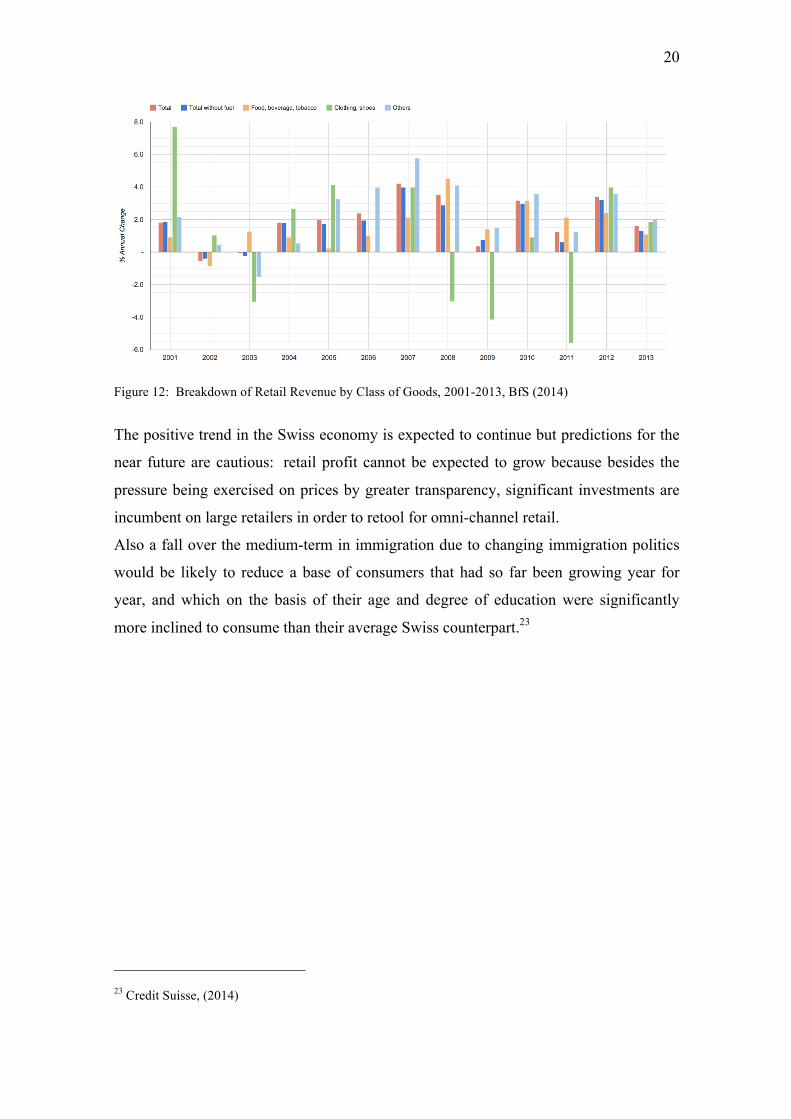

3.2.1 General trends in the Swiss market

With 96 billion out of 316 billion francs retail today represents a 30% share of Swiss

private consumption.21

According to the Research Institute for Conjunctural Studies of ETH (KOF), Credit

Suisse and the Swiss Federal Statistical Office (BfS) the Swiss retail market is slowing

down. Figure 11 and 12 show the breakdown of percentage of positive (= improved)

and negative (= worsened) retail profits and by firm size respectively kind of good and

21 GfK (2012)

19

reveal that even most of the major retailers, which were still among the winners in the

last decade, are also reporting a slowing down of profits.

Even though the Swiss domestic economy is been residing in a super cycle, where

strong private consumption is being held up by low interest rates and population growth

through high immigration the retail sector showed a tough year in 2013. After discounts

of 2.5% in the two previous years, retailers reduced prices by at least a further 1.0% in

2013 as seen in Figure 13.22

Figure 11: Breakdown of Percentage of Positive (= improved) and Negative (= worsened) Retail Profits,: KOF ETH, Credit Suisse, (2014)

22 Credit Suisse (2014)

20

Figure 12: Breakdown of Retail Revenue by Class of Goods, 2001-2013, BfS (2014)

The positive trend in the Swiss economy is expected to continue but predictions for the

near future are cautious: retail profit cannot be expected to grow because besides the

pressure being exercised on prices by greater transparency, significant investments are

incumbent on large retailers in order to retool for omni-channel retail.

Also a fall over the medium-term in immigration due to changing immigration politics

would be likely to reduce a base of consumers that had so far been growing year for

year, and which on the basis of their age and degree of education were significantly

more inclined to consume than their average Swiss counterpart.23

23 Credit Suisse, (2014)

21

Figure 13: Retail Sales and Retail Prices, Change in Quarterly Sales Figures; Growth Drivers (nominal); 2014: Outlook, BfS, Credit Suisse (2014)

3.2.2 Online retail trends in the Swiss market

Only two years ago in 2012 only 5% (not counting online auction and bidding

platforms) of total retail sales were made using an online channel according to figures

of the market research company GfK and the Swiss Mail Order Federation.24

In the past years Internet sales have been growing more strongly than the retail market

as a whole (Figure 14). The sales have multiplied seven-fold since 2010 due to the

introduction apps for mobile and tablets.25

24 Credit Suisse (2014) 25 Credit Suisse (2014)

22

*2013 estimate Figure 14: Switzerland, Growth of Online Retail Sales, 2008-2013, GfK, Credit Suisse (2014)

Figure 14 shows also that whilst online retail sales in Switzerland make up only 5% of

total retail sales, the growth rate since 2009 has been at least as strong as in the USA

and in the EU17 at above 10% annually, though starting from a lower baseline. Since

there is no indication that Switzerland is any different from the countries it is

surrounded by it is to be assumed that the growth will level off around 10% of total

retail sales.

Almost 25% of the population are now hourly online, particularly the frequency of

mobile computing has recently increased rapidly: in 2011 almost three-quarters 44.1%

of the population where using mobile computing devices around, nearby or on the road

to find stores and products or to compare prices and get reviews from other customers.26

The Swiss customer is very advanced and open to convenient innovation. Figure 15

shows -using the example of Google searches for Amazon, Zalando, Digitec - online

only retailers recently launched in Switzerland - that searches went up immediately after

the service had became available, this fact can be interpreted as an indicator for the

interest in the new services.

26 Langer, M.A, (2014)

23

Figure 15: Growth of Selected Online Shopping Searches in Switzerland: Amazon, Zalando, Digitec, Galaxus. 2004-2014, Google Trends (Aug 2014) These facts illustrate that while the high street retail trade still makes quite most of the

sales today, the growth is clearly happening online. And there is no end to this trend is

sight. On the contrary, younger generations make their purchases increasingly online. In

Switzerland, the 25-to-34-year-olds are among the most industrious online shoppers. 90

per cent of them have shopped online. In Germany even 98 per cent of the age group

between 20 and 39 year olds have online buyer experience. And even older generations

are discovering the online shopping.27

The most recent figures on local online trading published by the Society for Consumer

Research (GfK) show how dynamically the market in Switzerland is changing: whilst

the entire retail sector in 2013 - as in previous years - rose by only 0.3%, the sales via

Internet orders increased by 14% to 5.35 billion francs, the authors of the study believe

that the online and mail order trade is likely to continue to grow by 8% annually.

Collaterally pick up points near the border - addresses to which items ordered from

foreign websites that don’t ship to Switzerland can be posted to - are becoming more

popular among consumers. Such cross-border purchases counted for CHF 200 million

in 2013 and grew in comparison to the overall online market over proportionately.28

3.2.3 Trends in Swiss retail space

Even if the transfer of sales from high street retail to the Internet will not be fully

reflected in the demand for retail space, a substantial medium to long-term effect can be

27 Rudolph et al. (2009) 28 Langer, M.A (2014)

24

expected. According to the GfK report mentioned by Credit Suisse in the next decade

the portion of online Retail will reach one third.29

According to the most recent Wüest and Partner’s property market report on

Switzerland in 2012 there were 33’378’800 square meters retail space and a growing

vacancy rate in non-prime sites in most Swiss centres. Their prognosis for the sector is

optimistic regarding the earning potential of the retail economy but cautious on the

supply and demand estimation: due to the development of big projects in highly

attractive, frequented places and on green fields, a local oversupply of retail floor space

might result. The impact on prices is still unclear. Apparently the implementation of

new sales concepts (not specified)30 have led in the last year to an increase of rent

prices, the rise of price is considerable for prime locations like the centre of Zurich or

Geneva (+ 2.5 % and + 2%)31.

What can be expected for the retail floor space branch? The Credit Suisse Retail Report

expects a conversion of exceeding space into logistics spaces for (for being logistics

integrated into retail), there is also a tendency to concentration of locations32 and to

getting smaller on one hand and to use up more floor space by big international player

to stage products effect fully on the other.33

4 The evolution of traditional commerce

4.1 Swiss traditional retail and previous structural changes

4.1.1 The arrival of specialist retailers

In the past 100 years there have already been more radical revolutions in the retail

business than in the precedent 5000 years. And all of them have been associated with

the adoption of new technologies and innovation. The rise of both production and

demand that had started back in the industrial revolution let a consumer society emerge

29 Credit Suisse (2014a) 30 Wüest & Partner (2014b) 31 Wüest & Partner (2014a) 32 Interviews Appendix I.E and I.N 33 Credit Suisse (2014a)

25

and brought the advent of more specialist retailers which focused on the sale of a larger

variety of limited kind of products. 34 Following this innovation developers and city

authorities recognized the economical potential of dedicated shopping areas in town.

Investments in paving and lighting give birth to attractive retail areas in the cities.

4.1.2 The arrival of the department store

In the mid 19th century the first department store (Bon Marché) opened in Paris

pioneering a new kind of store with unprecedented spacious display areas, where buyers

could explore, discover, touch and feel a spectacularly exposed and rich assortment of

goods. It were this department stores that first adopted all sort of technical innovations,

like glass walls, lifts, electrical illumination and also fix prices and data-processing

equipment to analyse sales. They were the pioneers of inventory control, promotional

techniques, and credit policies as well as efficient use of capital invested in stocks and

construction.35

More significant to the industrialized masses was the arrival of the supermarket: flow at

cash points was speeded up and purchasing, packaging, stocking and refilling were

rationalized lowering the prices of goods massively. This concept would revolutionise

food distribution globally. Since the first shops of this kind in 1879 were tested in New

York, retail has undergone a continuous process of refinement and differentiation. (one

price, internationalized or locally refurbished, integrating large non food departments,

central, or out of town by important traffic junctions, (hypermarkets). Before the advent

of supermarkets people went to single shop to buy grocery, got served by the shop

personnel that portioned and packaged the single requests of the customers. This was

highly inefficient.

These new trends were adopted in Switzerland too and a dramatic decease of

independent shops resulted. All the traditional shops with a classic sales counter

disappeared while the new and established competitive and efficient shops grew steadily

and became bigger retailer chains.

As shown in

34 Kühne, M. (2013) 35 Niemeier, S. et al. (2013)

26

Figure 16 and Figure 17, large national players replaced most of high street retail and

soon all the streets in the country looked very similar.

Figure 16: Replacement Process of Swiss Food Retailers, Number of Points of Sale, (excluding specialized dealers), Gfk Switzerland (2012)

Figure 17: Retail Space growth of Migros and Coop, Years 1990-2011 in 1000 m2 GfK Switzerland (2012)

4.1.3 Arrival of the vertical retailer

In various sectors but mainly in the fashion industry many retailers pushed into an

exclusive sourcing and production of goods or into integrating distribution and retailing

in the own business (Benetton, Inditex). This activity extension allowed them to gain

another mark in efficiency and to “selling in production” meaning that products that

27

were successfully sold in the shops could be resent in production and reordered. This

became possible thanks to a precise and real time communication of shops with the

integrated production lines.36

4.1.4 The sale decouples from store

In the present era - last 15 years - a new revolution is taking place. Traditional retail

consolidated over centuries are being thrown over, as derived in chapter 2, by a new

order founded on three technological pillars: computing, power networking and data

storage capacity. Traditional retailers no longer hold the monopoly on marrying

information about supply and demand with the appropriate flow of goods. They are not

any longer the only aggregators of demand. A range of online retailers now harnesses

the power of computing and the Internet both to aggregate online demand and to fulfil

it.37

The following chapters will analysis this era in more detail.

5 Analysis of Online Retail

5.1 A brief history of online services

Whilst the Internet itself had existed since the 1970s, back in 1990, there was little

evidence that the familiar online world of today could exist.

The history of the online world can be seen as coined by four major events: the

invention of the WWW in 1991, the release of the first web browser in 1994, the

dotcom crash of 2000 and the release of the iPhone in 2007.

With the invention of the WWW 1991 (World Wide Web) the first commercial web

browser was released along with the SSL protocol (enabling secure communication).

Amazon launched in 1995, 20 years ago.38

The period between 1995 and 2000 was the period of the dotcom boom. Many online

companies were launched including Google, Expedia (the first online travel agency).

This period represented the typical phase of overestimation of new technologies. The

36 cp. Niemeier, S. et al. (2013) 37 cp. Niemeier, S. et al. (2013) 38 cp. Amazon (2014)

28

consumers were simply not there in the volumes needed to support the business models

being proposed. It all came to a halt in 1999/2000 with the dotcom burst.

Between 2000 and 2007 the online business made more steady progress. The driving

force was the growing penetration of broadband Internet: In 2000 virtually no

households in the OECD countries had broadband, by 2004 a tipping point was reached

where more than half of the households were connected with broadband, whilst by 2010

broadband was the default accounting for 90% of connections. Improved connectivity

also enabled a trend towards cloud computing infrastructure, Amazon AWS (Amazon

Web Services) and other SaaS that has enabled online businesses to be created without

the capital investment still required in the 90s.39

The iPhone in 2007 introduced ubiquitous connected computing. It released the online

world from being tied to a desktop computer. Quickly mimicked in cheaper forms

competitors, it set the expectation of unlimited access to the full power of the Internet

(at home, work, in transit or in a store).

Additionally 2008 was the year of the global financial crisis. The event put most

western economies into a recession and set more pressure on the retail industry and their

prices. It hit the financial services based UK economy particularly hard, resulting in

consumers becoming much more price sensitive. The online retail industry in the UK

now accounts for greater than 12% of overall retailing, more than any other OECD

country.

39 cp. Chmielewski, J. (2014)

29

Figure 18: Timeline of Significant Events in the History of Online Services (2014)

5.2 Why are consumers shopping online?

In chapter three the growth of online retail is shown through different figures. The

PWC’s global report on digital commerce shows that across the major markets

surrounding Switzerland (Germany, Italy & France) and the e-Commerce trendsetting

markets of the UK and USA, price and convenience is the principal reasons consumers

report for why they shop online. The overall trends for the reasons seem to be similar in

all countries.

Figure 19 displays reasons why Internet users buy products digitally rather than in-store

across European countries; Looking at Switzerland specifically, price and convenience

remain the dominant factors, though Swiss shoppers do appear less price sensitive.

However there are indications that Switzerland may be an outlier compared to other

markets when it comes to product availability and choice. More shoppers in

Switzerland, compared to the surrounding countries, UK and USA, report shopping

online because of reasons of being able to compare products, find their favourite brands

30

and have a wider variety of choice. This trend could be interpreted as reflection of the

chasm existing in terms of choices between the worlds of retail.40

A survey from University of St. Gallen focusing only on Swiss Internet shoppers

appears to confirm the PWC data. Whilst the survey asked the question across only 3

factors, price and convenience remained the primary drivers for online shopping.

Quality and innovation, the 3rd factor, was rated lower, but not by a great deal, 69.2%

of respondents in 2013 reported it as a strong factor compared to 76.7% and 76.2% for

price and convenience respectively.41

* Swiss data several factors were aggregated into “convenience” (e.g. 24x7, fast checkout etc.) shown here as „able to shop from home“

Figure 19: Reasons Internet Users Buy Products Digitally Rather Than In-Store, across European countries, pwc (2013c)

5.3 The competitive advantages of online retail

The widely reported threats of online retail can be summarised in themes such as; price

transparency, show rooming, margins being squeezed and the death of the high street.42

In chapter 2 two frameworks for analysis were introduced, Porter’s five forces and the

four values added by retailers to the supply chain as defined by Zocchi, Niemeier and

Catena. 40 cp. pwc (2013a) 41 cp. Rudolph., T. et al. (2013) 42 cp. pwc (2013b)

31

Looking first at Niemeier, Zocchi and Catena’s four values: preselection, demand

aggregation, sales advice and fulfilment (physical movement of stock). How are these

functions of retail converted (mapped and being adapted) in the online world? How do

online retailers provide higher value to the consumer and how has the online channel

altered the relationship between consumers and the various players in the supply chain?

A: Preselection Pre-selection value can be seen through both the lens of the consumer

and the supplier. From the consumer side preselection can be seen as curating, the

retailer has edited down the universe of possibilities to those relevant to the customers

of the retailer.

From the supplier side this also adds value, as the retailer (in theory) knows the

consumer better than the supplier, and by selective ordering provides feedback to the

supplier on what product lines to develop. In the online world these value-adding

functions have become harder to assign to just retailers. The customer journey between

an online media article and fulfilment through a retailer or the manufacturers site is little

more than a click. Media sites can generate revenue through the affiliate programs

retailers offer or by carrying highly contextually targeted Ads. This means that online

media, without being a retailer, can directly generate revenue from writing, reviewing,

collecting products together in new and innovative ways. An example being “pinterest”,

a fashion pin boards site, and the many thousands of specialist blogs writing about

products. From the manufacturers perspective, customer feedback no longer has to

come exclusively from the retailers or distributors. Online has enabled manufacturers to

sell directly to consumers. By using crowd-sourced funding for developing new

products manufacturers can even get feedback on products before they are produced.

B: Demand Aggregation: In the physical world the limits of demand aggregation

(creating footfall) for a retailer was given: A store had a location and the population

over which demand could be aggregated was limited by the physical distance and time

customers were prepared to travel to the store and by the number of potential

customers43 in this population.44

43 Given by the demographic structure of the population sample in question 44 Refer to value of property chapter fundamentals

32

In the online world the population over which demand can be aggregated is not only

theoretically unlimited (for retailers which ship globally the theoretical population is

everyone) but it can also be segmented into narrower groups.

However there are real limits, and the limits come from the ability of the retailer to

communicate effectively with the customer and the frictions of fulfilment (inefficiency

of the systems). On the communication side language is an obvious barrier, but also

social norms of how retail is conducted add additional barriers. On the fulfilment side

the ability to take payments is a major hurdle, the cost of shipping, and cross border

customs are also major sources of friction. (Different stages of economical and service

development of countries as well)

The lack of physical space constraints online means there is a larger disparity between

the population an online retailer could theoretically aggregate demand across, and the

population they can in practice reach. Firstly, whilst a given retailer can ship anywhere

so can all of his competitors. Secondly, web sites and online retailers are invisible by

default (unlike a store it’s impossible to stumble across a website by accident, without it

being linked to from somewhere), so they have to work hard either building a brand and

becoming a “go-to” destination or being linked to from the “go-to” destinations of

online consumers.

The largest retail demand aggregator online may not be a retailer. Google is the first

point of call in many consumers’ online (or traditional) retail journeys. Given Google

search results contain only 10 sites plus a few Ads the constraints on demand

aggregation may be the frequency within which a retailer can appear on the first page of

the search results. Besides Google there myriads of aggregators have been generated

around online media. (Blogs, Magazines, Experts, Compare Sites etc.)

So online stores has to work hard to become the “go to” destination for a category (or

range of categories) of products as a traditional retailer has to pay for a prime location.

This aggregation works extremely efficiently for product categories with large

catalogues where local stores could rarely hold the whole catalogue locally so the

frictions of fulfilment are less of an impediment.

Switzerland is a small market and not part of the EU market, different laws, border

controls and customs might cause friction to fulfilment of cross borders commerce.

C: Sales Advice: Throughout the supply chain there is disparity of information between

parties, but not more so than between the consumer and the retailer.

33

For many product categories the consumer makes a specific product purchase

infrequently and so is in need of help and advice in making a selection. However

specific retailer’s pre-selections of products may not have been fully aligned with the

customer’s best interests, and the sales expertise available within a store can vary

wildly.

For this reason consumers have always turned to others for independent advice, whether

friends or experts. Online retailers themselves have now incorporated feedback tools

into their sites.

However online media has maybe had the biggest impact in this area. The ease with

which anyone can publish online means has resulted in a large number of sources

consumers can refer to, to find opinions comparing products or first hand experiences of

owning products. Surveys have found 9X% of consumers who are online start their

purchase journeys with online research, even if the final purchase is made in a high

street shop.

Product manufacturers have also established online presences to explain their product.

The two-way nature of online means they are able to enter into a conversation with the

end consumer and garner valuable feedback and give advice.

D: Fulfilment: Fulfilment is maybe where online retailers have the most mixed impact

on the value chain. Whilst a high street customer can walk out of the store with a

product, online retail always takes time to ship. However traditional retailers not always

have product in stock, the customer then has to order, wait, and often return to the store

to pick-up the product. Online retailers in contrast will always deliver, however many

efforts are being done to solve the “last mile”45 problem. The customers’ circumstances

dictate different trade-offs. Payments can also be harder online, whilst traditional

payments can be made in cash, online a credit card is the preferred method. Though

payment security technology is developing parallel for both and becoming the same.

5.4 Winners and losers in the supply chain

The manufacturer now has unprecedented direct access to the end consumer of his

products. He has tools to put himself in-front of the consumer when they are ready to

buy, he can also both sell to and get feedback from the customer directly.

45 cp. Glossary

34

Looking through the lens of Porter’s 5 forces, the success of the online direct channel

changes the dynamics of several key relationships in the supply chain.

Firstly the relationship between the manufacturer and the distributor or retailer is

changed, with the power shifter towards the manufacturer (the buyer of the distribution

service). The manufacturer has an effective substitute service (direct selling), therefore

less need of the value add services retailers and distributors have traditionally provided

(access to markets and feedback on products) and have himself greater insights into the

market value of his product. All of which give him a far stronger position.

Secondly the relationship between the consumer and the retailer has changed with the

power shifting from the retailer to the consumer. The consumer (the buyer) has access

to a wider variety of retailers online; he can easily compare prices and service levels

across them all. The cost of entry into the market for a new retailer (or manufacturer

wishing to sell directly) is low. An e-commerce software infrastructure, which would

have cost several millions to build 10 years ago, can be had for <$50,00046. Lastly the

consumer has access to far more information about the products and services he is

buying, putting him in a position to demand much high level of quality from all parties.

5.5 Internet capital investments are a new financial phenomenon

The Internet economy as a whole, across the G-20 countries was estimated by BCG to

contribute 4.1% of total GDP or approximately $ 2.3 trillion47. Online commerce in the

UK and US alone contributed $354B of that number. ROPO (research online, purchase

in shop) contributed an additional $539B of sales in the UK and US during 201048.

As Wölfke and Leimstoll point out in their e-Commerce Report Schweiz 201449, new to

the industry is the concept of establishing an “innovation” in an existing market by

bringing services that are not actually profit-making with the intend to establish market

leadership and become cost effective some when later. Amazon was founded 20 Years

ago and is since then being operating with the goal of gaining users, reinvesting

continuously, in its own growth but without generating profit. The same can be said for

Zalando, which grew in two years from nothing to a business of 200 Mio. in

Switzerland. The growth of this company, (where each sale causes actually losses) 46 cp. Laudon, K.C., Traver, C.G. (2013) 47 cp. Dean, D., et al (2012) 48 cp. Dean, D., et al (2012) 49 cp. Wölfke, R., Leimstoll, U. (2014)

35

through new investment gives these companies a value growth that allows new rising of

capital.50

As we explained above online demand aggregation (or generation) is a key component

of the online retail ecosystem. Online companies, which can build up large and

frequently active audiences, can become extremely valuable even in the absence of

immediate revenue streams. Large amounts of capital are expended building and

acquiring such online start-ups. Valuations per user can range from $20 to >$500.51

This leads to the new fact, that competition is not actually given by the business itself

but by the way the companies are financed. Primary markets lose market share because

these start ups give customers expectations that existing players cannot satisfy.52

5.6 Online ecosystem of demand generation

Setting up an online retail store alone can be compared to setting up a store in a derelict

part of town, very few people will find it by accident.

Put this way, it seems implausible that this type of store could compete successfully

with traditional retailers who have a presence in every prime high street location.

However when an online store is placed in the context of the ecosystem of online

demand generation it becomes plausible that these stores can become a competitive

threat.

The online retail environment is ruthlessly competitive and experiments with any edge,

which can be employed to increase revenue and margins. There are 100s of Ad tech

companies innovating in this space.53

The principle online demand generation systems are:

• Search and search advertising

• Display advertising

• Email/direct Marketing

• Social media (paid and unpaid)

• Public relations (references in prominent blogs or media outlets

50 cp. Lager, M. A. (2014) 51 cp. Sterling, G. (2014) 52 cp. Wölfle, R., Leimstoll, U., (2014) 53 cp. Ad Choices (2014)

36

A successful online retailer or product brand will likely employ a mix of all of these

tools.

Online digital advertising (paid search, display, and social) has some key differences to

traditional advertising:

1. Scalability. Each advert displayed is generated on the fly; this means each “slot”

can be dynamically allocated to a different ad or advertiser. This opens up the

possibility of an advertiser being able to scale a campaign from single dollar to

many $1000s per day. Small businesses can manage risk; alternatively a large

advertiser can run an infinite variety of creatives.

2. Measurement. The outcome of every ad impression is measured. If a user clicks

this is reported (Click Through Rate - CTR). If a user after clicking goes on to

make a purchase this is also measured as a “conversion”. Online retailers know

the value of every conversion; combined with the cost of the impression and

CTR this gives a “Cost per Conversion”.

3. Experimentation. With the ability to dynamically scale campaigns, change

creatives at will, and measure the outcome of these, businesses have the ability

to rapidly iterate through ideas for demand generation, zeroing in on the most

effective strategies.

4. Targeting. Most Ad networks assign a unique ID to a browser or phone (in the

case of the phone the phone itself has a unique Ad ID). Ad networks build a

profile of this ID which allows advertisers to target specific segments or

consumers who have visited their website (retargeting).

5. Payment by Auction. Ad networks have generally settled on a model of

auctioning Ad slots. This means that the cost of Ad impressions migrates

towards the market value of the impression.54

With such a direct and measurable relationship between spending on demand generation

and revenue generated, combined with the ability to scale campaigns dynamically, a a

tool which can effectively match demand to supply and smoothly scale a growing

business is generated.

54 cp. Varian, H.R. (2009)

37

5.7 Impact of online retail on retail real estate

As seen in Chapter 3 a growing amount of retail turnover is being generated online.

Goods get sold without going passing the shop.

6 Analysis of Omni-Channel Retail

6.1 Evolution to omni-channel

Most retailers - traditional or online retailer - are now combining the two approaches in

what is called “Multi-Channel” retailing. Bill Davis55 a retailing expert describes omni

channel retailing as the natural evolution of multi channel retailing. Omni channel

retailing aims to a seamless consumer experience across all available shopping channels

including, but not limited to, physical brick and mortar stores, e-Commerce, contact