how is the offshore drilling competitive landscape …

TRANSCRIPT

HOW IS THE OFFSHORE DRILLING COMPETITIVE LANDSCAPE UNFOLDING?

JO FRIEDMANN, ENERGY SERVICE RESREACH, VP RIGS & VESSELS

NOVEMBER 2021

Agenda

Is shallow water oil and gas a competitive source of supply?

How is the competitive landscape in offshore drilling evolving?

Will the jackup market see a recovery?

1

2

3

Investment themes changes over time; Optionality and sustainability key in next phase

Upcycle (2007-2013) Downcycle (2014-2018) Future (2019 → )

Investment

themes

Materiality &

volume upside

Robustness &

cash-preservation

Optionality &

Sustainability

Price

regime

Communicated

focus

high oil price

low oil price

«Under pressure»

Volume

Cost

Carbon

3

Future (2019 →)Downcycle (2014-2019)Upcycle (2007-2013)

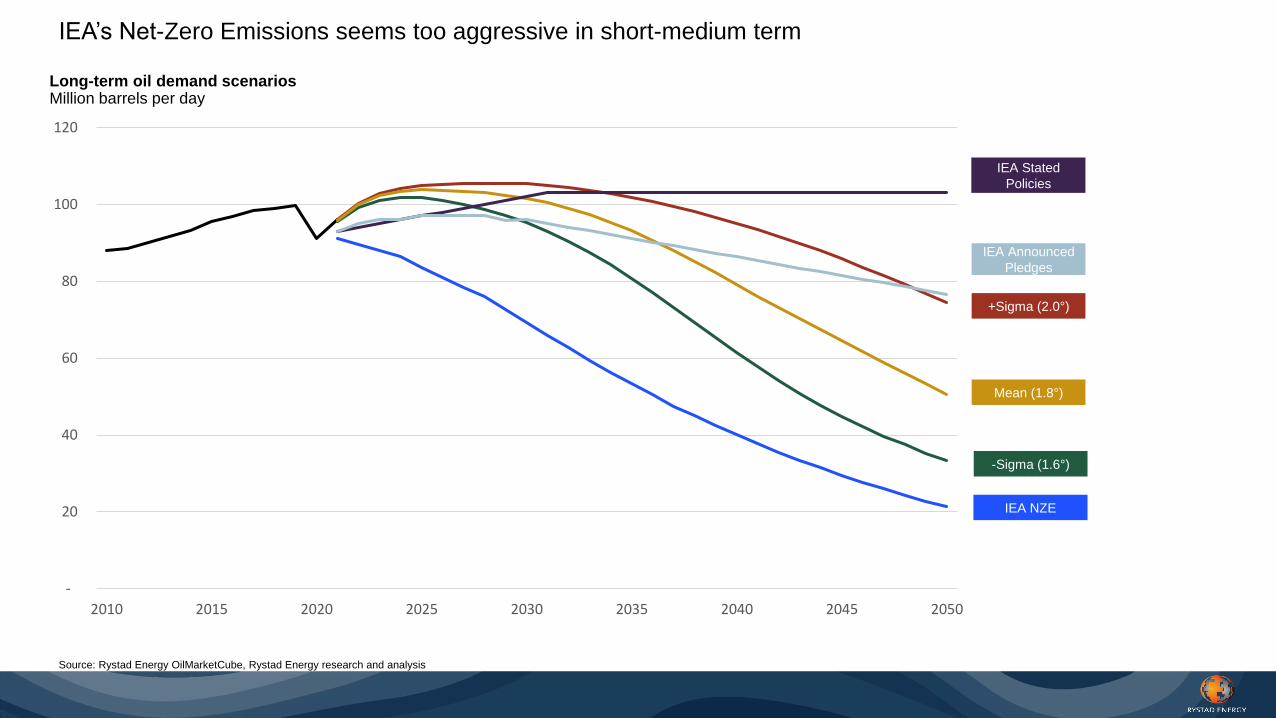

IEA’s Net-Zero Emissions seems too aggressive in short-medium term

Source: Rystad Energy OilMarketCube, Rystad Energy research and analysis

-

20

40

60

80

100

120

2010 2015 2020 2025 2030 2035 2040 2045 2050

Mean (1.8°)

IEA NZE

+Sigma (2.0°)

IEA Announced

Pledges

-Sigma (1.6°)

IEA Stated

Policies

Long-term oil demand scenariosMillion barrels per day

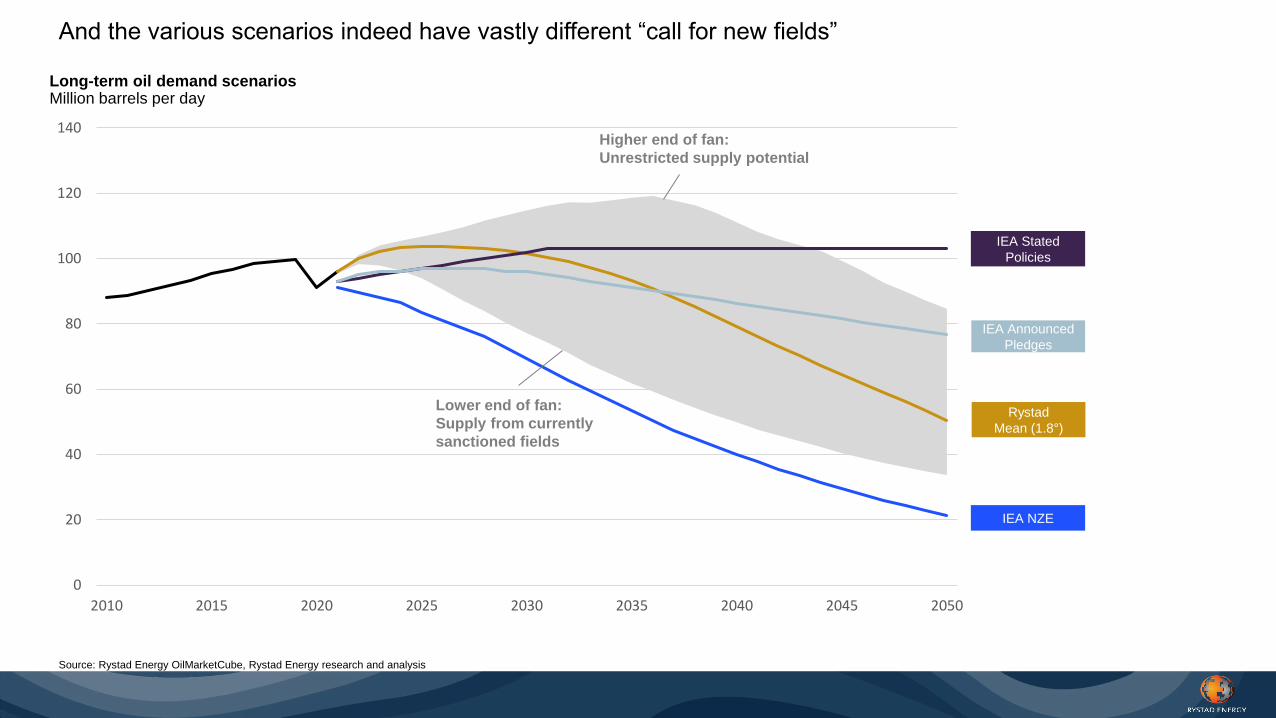

And the various scenarios indeed have vastly different “call for new fields”

Source: Rystad Energy OilMarketCube, Rystad Energy research and analysis

0

20

40

60

80

100

120

140

2010 2015 2020 2025 2030 2035 2040 2045 2050

Rystad

Mean (1.8°)

IEA NZE

IEA Announced

Pledges

IEA Stated

Policies

Long-term oil demand scenariosMillion barrels per day

Lower end of fan:

Supply from currently

sanctioned fields

Higher end of fan:

Unrestricted supply potential

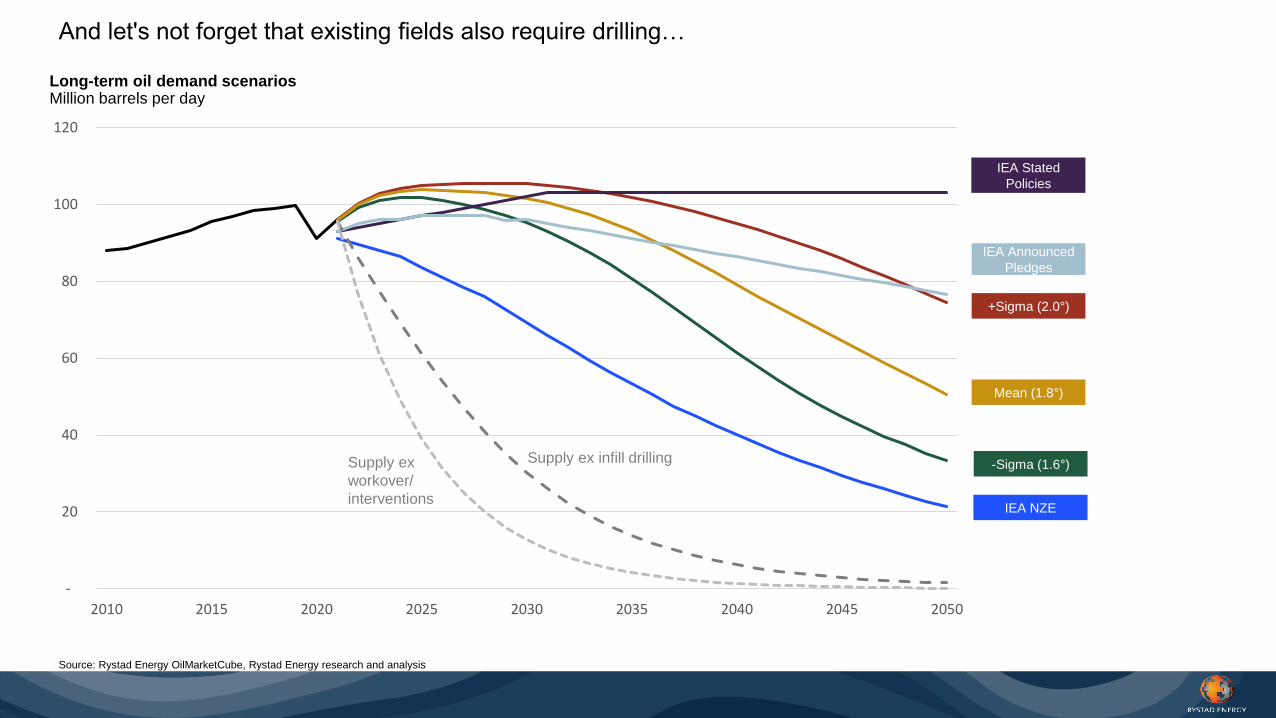

And let's not forget that existing fields also require drilling…

Source: Rystad Energy OilMarketCube, Rystad Energy research and analysis

-

20

40

60

80

100

120

2010 2015 2020 2025 2030 2035 2040 2045 2050

Mean (1.8°)

IEA NZE

+Sigma (2.0°)

IEA Announced

Pledges

-Sigma (1.6°)

IEA Stated

Policies

Long-term oil demand scenariosMillion barrels per day

Supply ex infill drillingSupply ex

workover/

interventions

7

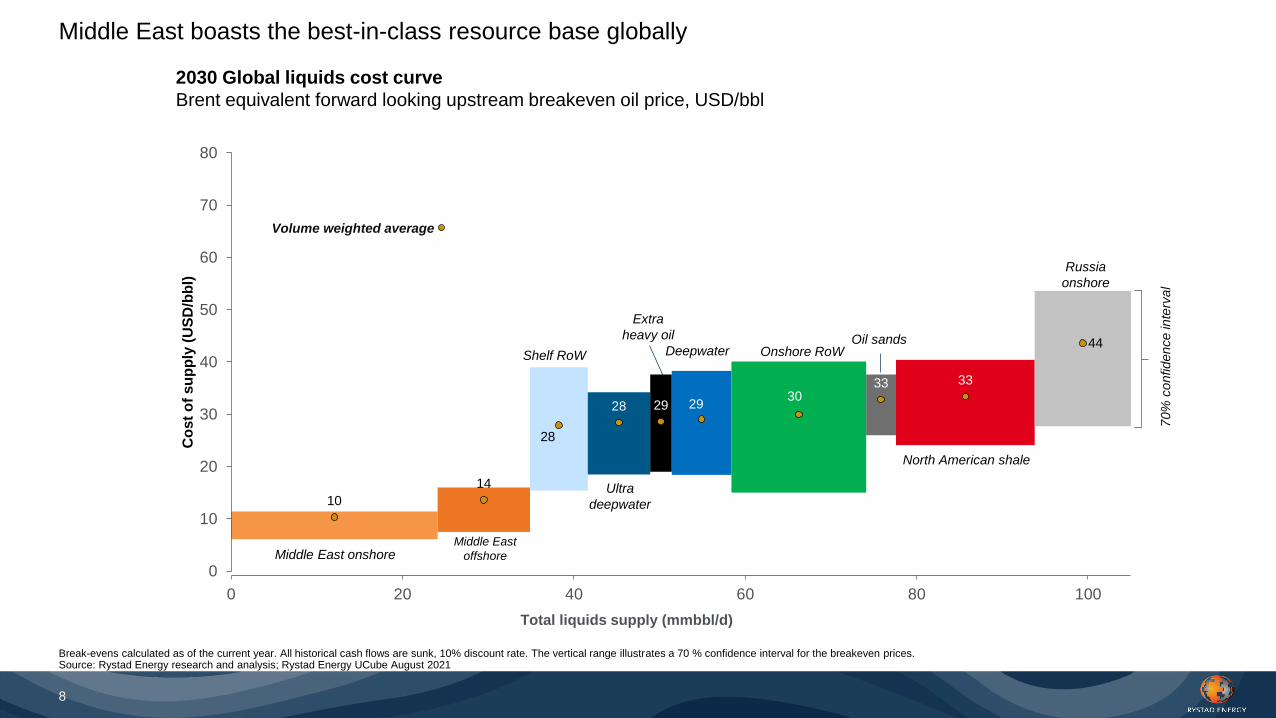

Middle East offsetting offshore shelf production decline in NS, SEA and GoM

Source: Rystad Energy research and analysis; Rystad Energy UCube

Shallow water production by region

Million boe/d

0

2

4

6

8

10

12

14

16

0

1

2

3

4

5

6

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Middle East (RHS)

Other

Southeast Asia

North Sea

US GoM

India

Mexico

China

West Africa

Million boe/d

10

14

28

28 29 2930

33 33

44

0 20 40 60 80 100

0

10

20

30

40

50

60

70

80

Total liquids supply (mmbbl/d)

Co

st

of

su

pp

ly (

US

D/b

bl)

Middle East boasts the best-in-class resource base globally

Break-evens calculated as of the current year. All historical cash flows are sunk, 10% discount rate. The vertical range illustrates a 70 % confidence interval for the breakeven prices. Source: Rystad Energy research and analysis; Rystad Energy UCube August 2021

8

Middle East onshore

Deepwater

Ultra

deepwater

Shelf RoW

Extra

heavy oil

Onshore RoW

North American shale

Russia

onshore

Middle East

offshore

Oil sands

70%

confidence in

terv

al

Volume weighted average

2030 Global liquids cost curve

Brent equivalent forward looking upstream breakeven oil price, USD/bbl

Source: Rystad Energy UCube and WellCube

0

10

20

30

40

50

60

70

80

90

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Offshore deepwater Offshore shelf

-50%

-40%

9

Development in average offshore well cost per well by segment

MUSD per well

Average shallow water well cost is down 40% since 2014

9.9

6.6

5.5

5.4

4.5

4.3

4.3

4.2

3.6

3.6

2.5

2.2

1.8

1.8

1.6

0 2 4 6 8 10 12

Thailand

United Kingdom

Angola

Nigeria

United States

Norway

Mexico

Malaysia

China

India

Trinidad and Tobago

Saudi Arabia

UAE

Brazil

Qatar

*Based on wells completed between 2010 and 2020 Source: Rystad Energy UCube

7.1

6.0

3.6

3.2

3.1

2.5

2.3

2.2

2.1

2.0

1.9

1.7

0.7

0.4

0.2

0 2 4 6 8

Thailand

United Kingdom

India

Indonesia

United States

China

Malaysia

Netherlands

Saudi Arabia

Malaysia/Thailand JDA

Norway

Trinidad and Tobago

Australia

Iran

Qatar

Oilfields Gas fields

10

Average well capex per boe for top 15 most active countries*

UDS/boe

Qatar, Brazil, UAE and Saudi Arabia with the most commercial oil wells drilled over the last decade

Agenda

Is shallow water oil and gas a competitive source of supply?

How is the competitive landscape in offshore drilling evolving?

Will the jackup market see a recovery?

1

2

3

12

Offshore drillers that filed for Chapter 11

Diamond Offshore Exited

Noble Drilling Exited

Valaris Exited

Pacific Drilling Exited & Acquired

Seadrill Partners (Aquadrill) Exited

Seadrill Limited On-going (4Q 2021)

Offshore Drilling Holding (part of Grupo R) On-going

Aban Offshore On-going

KS Energy (subsidiary company KS Drilling) On-going

Debt wipeout will enable further consolidation

13

Source: Rystad Energy research and analysis; Company 8Ks

Five drillers reduce debt burden by more than $14Bn in latest restructuring round

14

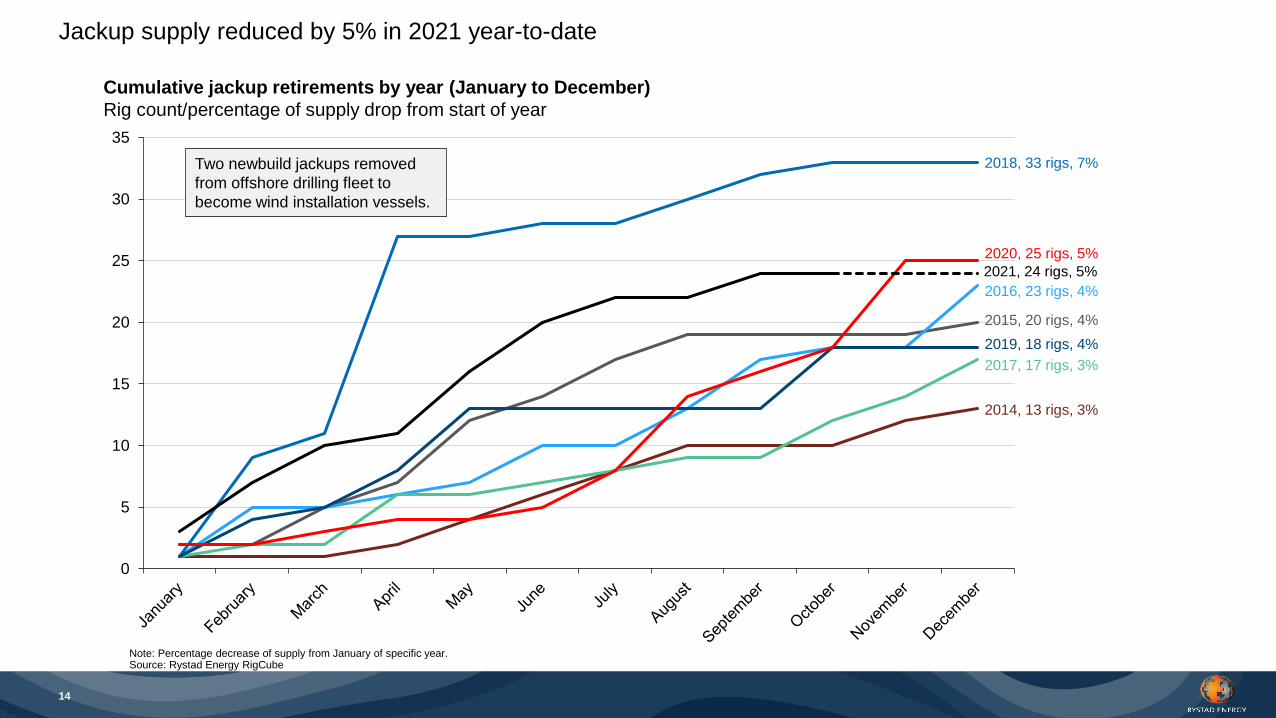

Note: Percentage decrease of supply from January of specific year. Source: Rystad Energy RigCube

Cumulative jackup retirements by year (January to December)

Rig count/percentage of supply drop from start of year

Jackup supply reduced by 5% in 2021 year-to-date

0

5

10

15

20

25

30

35

2018, 33 rigs, 7%

2014, 13 rigs, 3%

2020, 25 rigs, 5%

2017, 17 rigs, 3%

2016, 23 rigs, 4%

2015, 20 rigs, 4%

2019, 18 rigs, 4%

2021, 24 rigs, 5%

Two newbuild jackups removed

from offshore drilling fleet to

become wind installation vessels.

15

Stranded jackups are slowly but steadily leaving the yards and entering the market

Source: Rystad Energy research and analysis

Cumulative number of stranded jackups, 2015-2021 (YTD)

Number of rigs

Gulf Driller I stranded at CIMC

PaxOcean strands 2 jackups at PT Drydocks

Paragon strands Prospector 6, 7 & 8 at DISC

Speculative owner strands Gulf Driller VIII

TS Jade stranded at CSIC

TS Jasper stranded at KeppelFELS

Borr Drilling acquiires 9 rigs from PPL Shipyard

Borr Drilling acquires 5 rigs from KeppelFELS

Noble acquires 2 rigs from PaxOcean

Shelf Drilling buys 2 / BBCs 2 rigs from CMHI

CP Latina takes Gulf Driller 6 & 8 on BBC

COSL takes SinoOcean Auspicious on BBC

Shelf Drilling ends BBC deal for 2 rigs

COSL takes 3 x CHMI jackups on BBC

SinoOcean converts 2 jackups to wind vessels

ADNOC buys units previously under BBC to Shelf

0

10

20

30

40

50

60

70

16

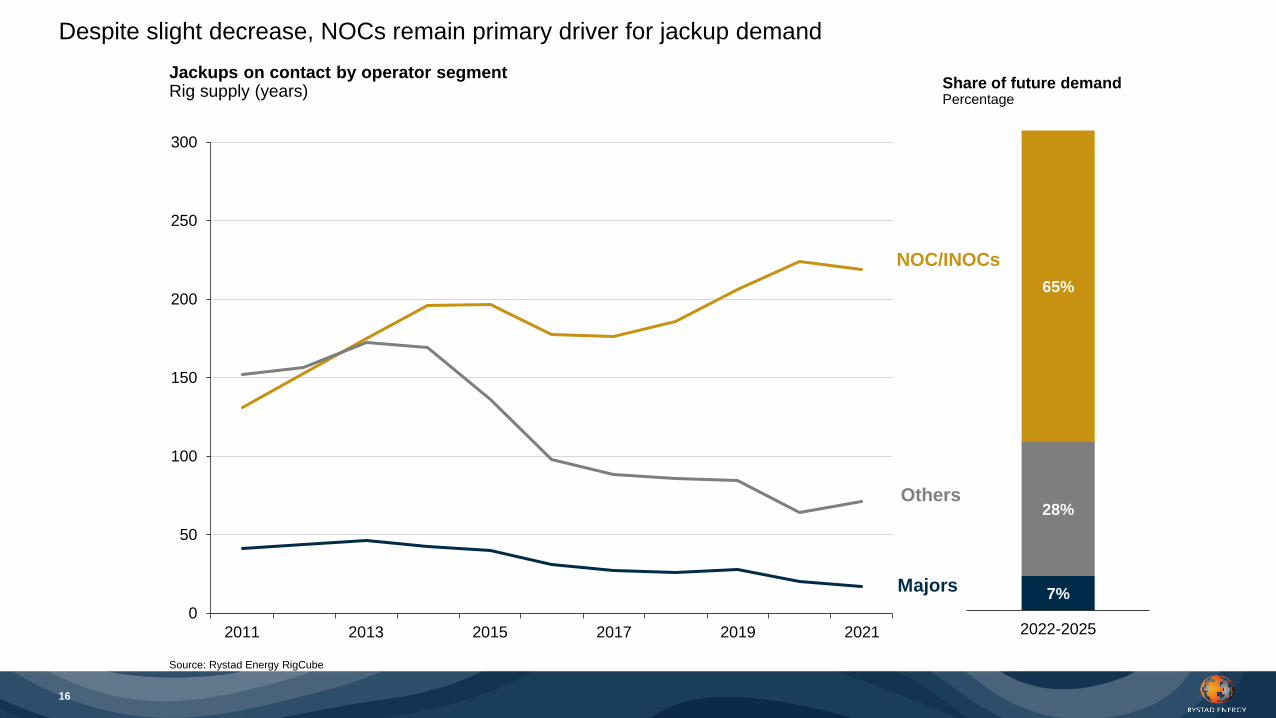

Despite slight decrease, NOCs remain primary driver for jackup demand

Source: Rystad Energy RigCube

0

50

100

150

200

250

300

2011 2013 2015 2017 2019 2021

7%

28%

65%

2022-2025

Share of future demandPercentage

Majors

NOC/INOCs

Others

Jackups on contact by operator segmentRig supply (years)

Source: Rystad Energy research and analysis

NOC Rig Demand National Rig Contractor / JV Regional Rig Contractor Standard International RigContractor

Premium International RigContractor

National / JVGuaranteed

contract wins

RegionalNOC relationship

and localization

Standard

International

Price competitionPremium

International

Technology

differentiation

17

NOC contracting preferences and contractor differentiation illustration

Agenda

Is shallow water oil and gas a competitive source of supply?

How is the competitive landscape in offshore drilling evolving?

Will the jackup market see a recovery?

1

2

3

19

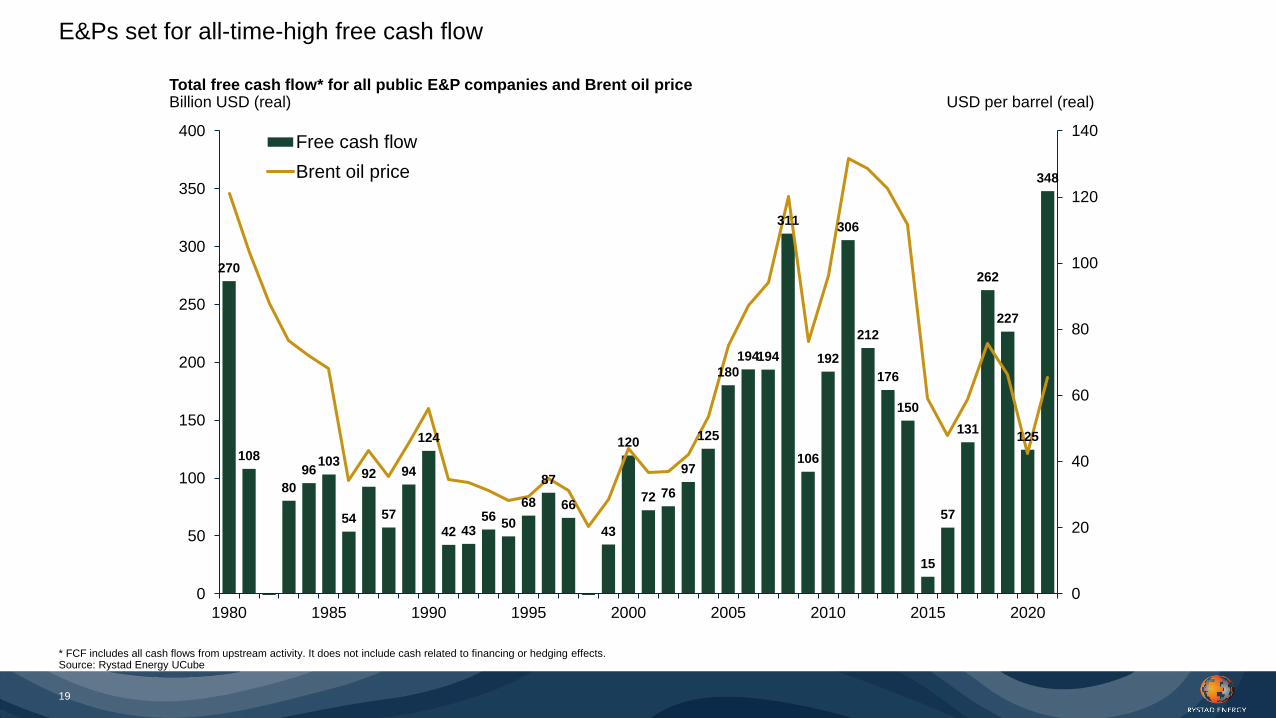

E&Ps set for all-time-high free cash flow

* FCF includes all cash flows from upstream activity. It does not include cash related to financing or hedging effects. Source: Rystad Energy UCube

Total free cash flow* for all public E&P companies and Brent oil priceBillion USD (real) USD per barrel (real)

270

108

80

96103

54

92

57

94

124

42 4356

50

68

87

66

43

120

72 76

97

125

180

194194

311

106

192

306

212

176

150

15

57

131

262

227

125

348

0

20

40

60

80

100

120

140

0

50

100

150

200

250

300

350

400

1980 1985 1990 1995 2000 2005 2010 2015 2020

Free cash flow

Brent oil price

Source: Rystad Energy RigCube

-20%

-10%

0%

10%

20%

30%

40% Drillships

Semisubmersibles

Jackups

Jackups, drillships and semisubmersibles on contract

Daily rig count indexed to October 27, 2020

Jackups with steady growth last 12 months after showing resilience during downturn

21

Note: Marketed utilization excludes cold-stacked units. Excluding newbuilds without contracts. Source: Rystad Energy RigCube

0%

20%

40%

60%

80%

100%

0

20

40

60

80

100

120O

ct-

18

Apr-

19

Oct-

19

Apr-

20

Oct-

20

Apr-

21

Oct-

21

Middle EastNumber of contracted rigs/utilization (%)

Southeast AsiaNumber of contracted rigs/utilization (%)

West AfricaNumber of contracted rigs/utilization (%)

North Sea (Norway)Number of contracted rigs/utilization (%)

North Sea (excl. Norway)Number of contracted rigs/utilization (%)

MexicoNumber of contracted rigs/utilization (%)

Marketed utilization (RHS)

Contracted rigs (LHS)

0%

20%

40%

60%

80%

100%

0

10

20

30

40

50

Oct-

18

Apr-

19

Oct-

19

Apr-

20

Oct-

20

Apr-

21

Oct-

21

0%

20%

40%

60%

80%

100%

0

5

10

15

Oct-

18

Apr-

19

Oct-

19

Apr-

20

Oct-

20

Apr-

21

Oct-

21

0%

20%

40%

60%

80%

100%

0

10

20

30

40

Oct-

18

Apr-

19

Oct-

19

Apr-

20

Oct-

20

Apr-

21

Oct-

21

Marketed utilization (RHS)

Contracted rigs (LHS)

0%

20%

40%

60%

80%

100%

0

10

20

30

40

Oct-

18

Apr-

19

Oct-

19

Apr-

20

Oct-

20

Apr-

21

Oct-

21

0%

20%

40%

60%

80%

100%

0

10

20

30

40

Oct-

18

Apr-

19

Oct-

19

Apr-

20

Oct-

20

Apr-

21

Oct-

21

Regional utilization and rig count trends

0

500

1000

1500

2000

2500

3000

3500

1Q 2019 2Q 2019 3Q 2019 4Q 2019 1Q 2020 2Q 2020 3Q 2020 4Q 2020 1Q 2021 2Q 2021

Transocean Valaris plc Noble Drilling Maersk Drilling

Diamond Offshore Odfjell Drilling Shelf Drilling Saipem

Borr Drilling Vantage Drilling Awilco Drilling PLC

*Transocean received a one-time cash settlement of $177 million recognized during 2Q 2020.Source: Rystad Energy ServiceSupplyCube

22

Revenues for selected listed rig owners

Quarterly revenue from offshore drilling by selected rig companiesQuarter-on-quarter percentage change in million USD

Source: Rystad Energy RigCube

Historical fixtures by asset class (new unique contracts)

Thousand USD/day

Rate improvement lagging for jackups

Premium jackup Standard jackupHarsh jackup

Source: Rystad Energy RigCube

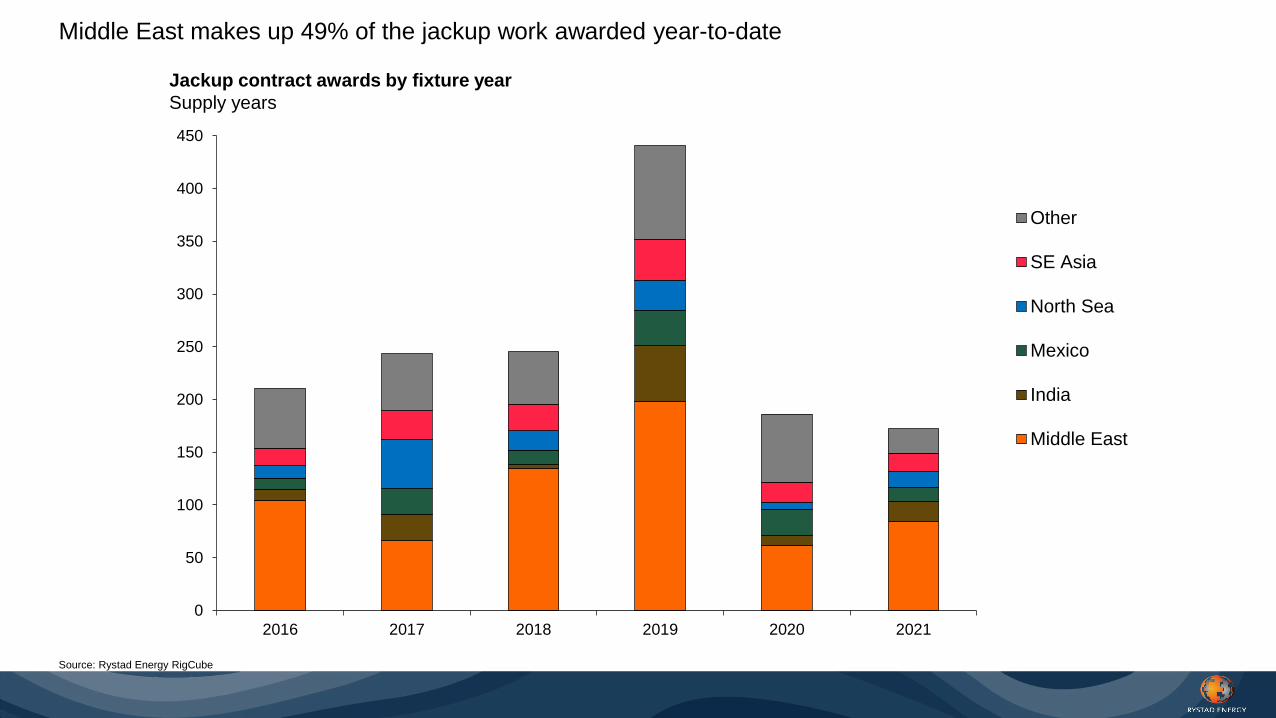

Jackup contract awards by fixture year

Supply years

Middle East makes up 49% of the jackup work awarded year-to-date

0

50

100

150

200

250

300

350

400

450

2016 2017 2018 2019 2020 2021

Other

SE Asia

North Sea

Mexico

India

Middle East

*Contract awards in 2021 YTD. Includes new unique contracts, exercised options and extensions.Source: Rystad Energy RigCube

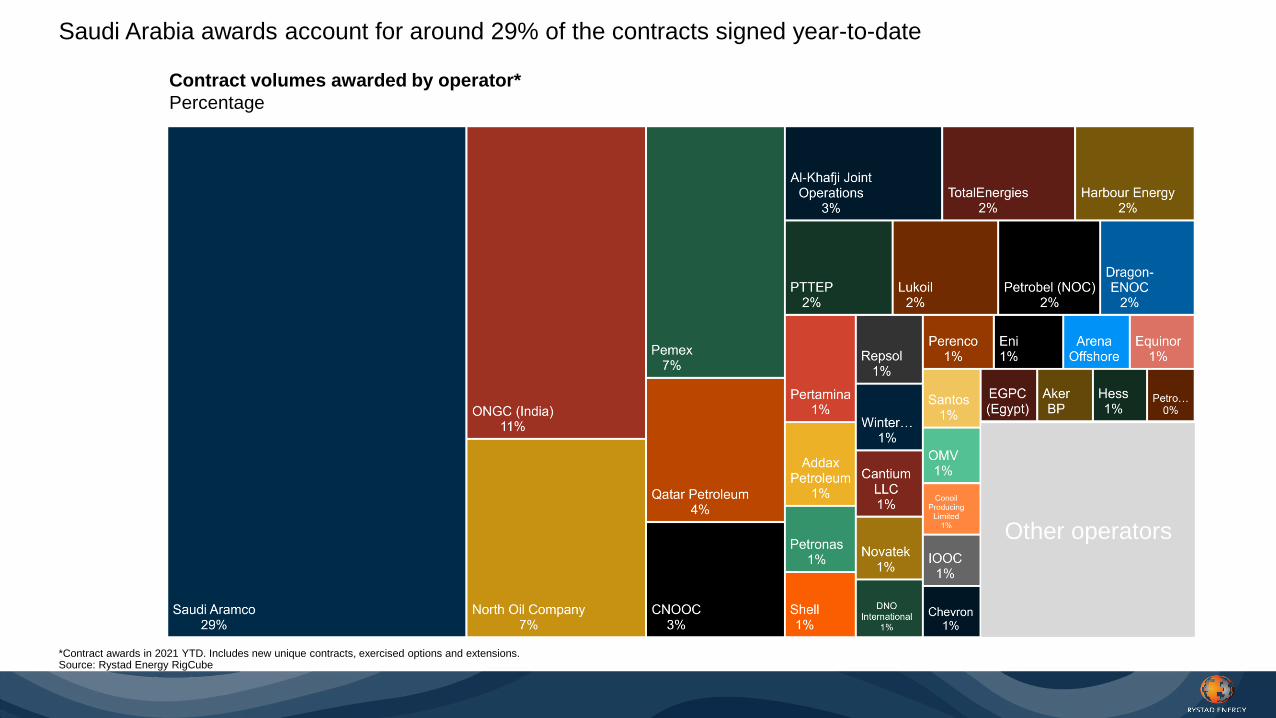

Contract volumes awarded by operator*

Percentage

Saudi Arabia awards account for around 29% of the contracts signed year-to-date

Other operators

26

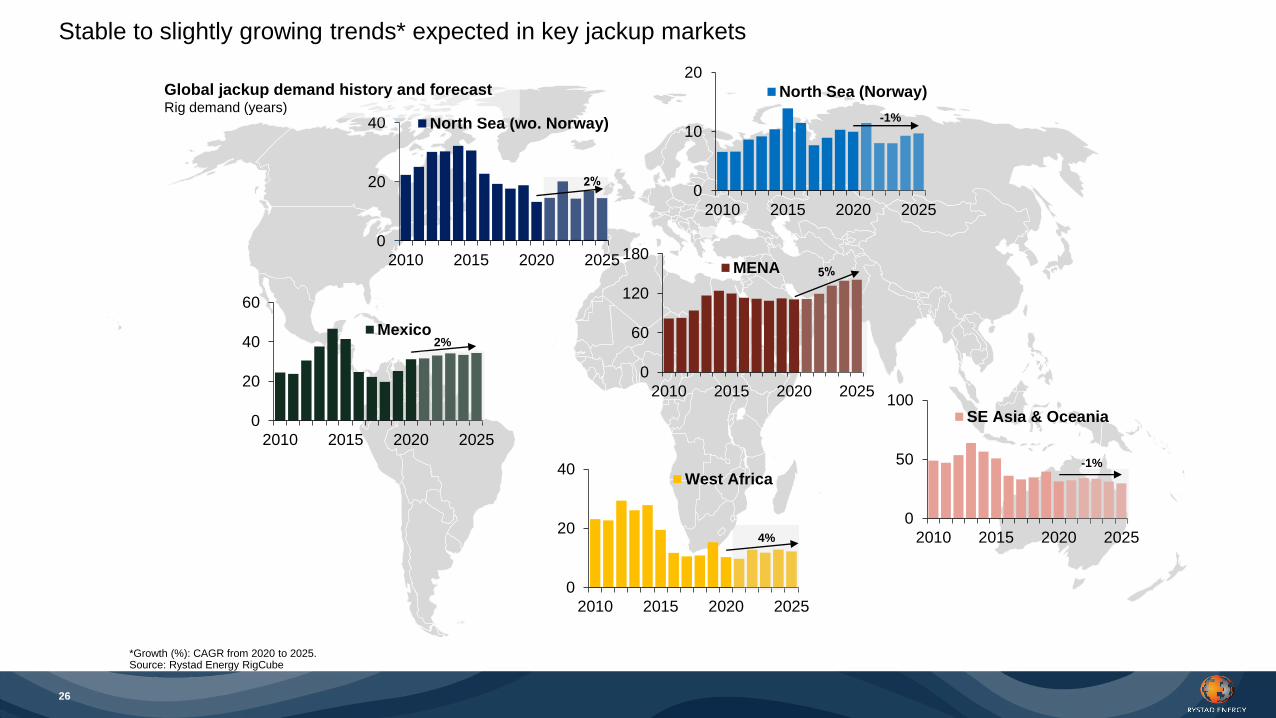

*Growth (%): CAGR from 2020 to 2025.Source: Rystad Energy RigCube

0

10

20

2010 2015 2020 2025

North Sea (Norway)

0

20

40

2010 2015 2020 2025

North Sea (wo. Norway)

0

20

40

60

2010 2015 2020 2025

Mexico2%

0

60

120

180

2010 2015 2020 2025

MENA

0

20

40

2010 2015 2020 2025

West Africa

0

50

100

2010 2015 2020 2025

SE Asia & Oceania

-1%

-1%

4%

Global jackup demand history and forecastRig demand (years)

Stable to slightly growing trends* expected in key jackup markets

Rystad Energy is an independent energy consulting services and business

intelligence data firm offering global databases, strategy advisory and

research products for energy companies and suppliers, investors,

investment banks, organizations, and governments. Rystad Energy’s

headquarters are located in Oslo, Norway.

Headquarters

Rystad Energy

Fjordalléen 16, 0250 Oslo, Norway

Americas +1 (281)-231-2600

EMEA +47 908 87 700

Asia Pacific +65 690 93 715

Email: [email protected]

© Copyright. All rights reserved.