how bad was lehman shock?:how bad was lehman …ifd/doc/mp-20110807-slide5.pdfhow bad was lehman...

TRANSCRIPT

How Bad was Lehman Shock?:How Bad was Lehman Shock?:Estimating a DSGE model with Firm and Bank Balance Sheets in a Data-Rich Environment*Balance Sheets in a Data-Rich Environment

(with H. Iiboshi, T. Matsumae, and R. Namba)

SWET ConferenceAugust 7 2011August 7, 2011

Shin-Ichi NishiyamaShin Ichi Nishiyama(Tohoku University)

1* The views expressed in this presentation are those of the presenter and does not necessarily reflect those of ESRI or Cabinet Office, Government of Japan.

Motivation of this paperMotivation of this paper

R t fi i l i i i U S hi h i it t d bRecent financial crisis in U.S. which was precipitated by so-called ‘Lehman Shock’ has exemplified that deterioration of balance sheet condition, especially that , p yof financial sector, can cause a deep and long-lasting recession.

As Alan Greenspan puts, “We are in the midst of a once-in-a century credit tsunami ” (Testimony made atonce-in-a century credit tsunami. (Testimony made at the House of Representatives, Oct. 23, 2008)

Since two years have past since Lehman Shock, time seems to be ripe in assessing the impact of the shock.

How Bad was Lehman Shock? 2

Objective of this paperObjective of this paper

I thi tif d th i t fIn this paper, we quantify and assess the impact of Lehman Shock.

We ask two questions:• How large was the magnitude of Lehman Shock?How large was the magnitude of Lehman Shock?

• How large was the effect of Lehman Shock to the geconomy?

Strategy: We identify Lehman Shock by banking sector net worth shock.

How Bad was Lehman Shock? 3

Contributions of this paperContributions of this paperWe combine two canonical financial friction models. • For corporate balance sheet, we adopt BGG (1999)• For bank balance sheet, we adopt Gertler and Kiyotaki

(2010) and Gertler and Karadi (2010)(2010) and Gertler and Karadi (2010)• We need to model two balance sheets to identify Lehman

Shock• Related work is Hirakata, Sudo, and Ueda (2010)

W d t D t Ri h th d d b B i i dWe adopt Data-Rich method proposed by Boivin and Giannoni (2006)• By utilizing multiple time series information for each y g p

observable, we can expect an improved efficiency in estimating parameters and structural shocks.

How Bad was Lehman Shock? 4

Model DescriptionModel Description

Th id i t b d t b l h t d b kThe idea is to embed corporate balance sheet and bank balance sheet to the stylized DSGE model.

Includes standard features: habit formation, sticky price, sticky wage, investment-adjustment cost, Taylor rule, y g j yetc.

Th 8 l h k TFP h k fThere are 8 structural shocks: TFP shock, preference shock, labor supply shock, investment-specific technology shock, govt. expenditure shock, monetarytechnology shock, govt. expenditure shock, monetary policy shock, entrepreneur net worth shock, and bank net worth shock

How Bad was Lehman Shock? 5

Goods and Factor Inputs Flow ChartGoods and Factor Inputs Flow ChartHousehold Government

τ

gc

Final Goods Mkt.

Y

Retailer

Labor Mkt.Y

i

y(j)y(j)

6Entrepreneur j Capital ProducerCapital Goods Mkt.

Financial Flow ChartFinancial Flow Chart

D it Bankers EntrepreneursDepositor Bankers Entrepreneurs

b b_Fb E

b_E

Q*K

b_E

n_F

n_EAgency Cost

(Moral Hazard/Costly Enforcement)

Agency Cost

(Costly state verification)

Model DescriptionModel Description

Model DescriptionModel Description

Representative Household’s Problem

⎤⎡

1)(

1)(E

0i

111

t∑∞

=

++

+

−−++

+⎥⎥⎦

⎤

⎢⎢⎣

⎡

+−

−−

LitL

itcititc

iti

Lc

lhccσ

χσ

χβσσ

0i ⎥⎦⎢⎣

R FEdi{ { { { { {

-bRb

bankersfromer net transf

Ft

urentreprenefromer net transf

Et

dividend

divt

incomelabor t1-t

t

1-t

depositt

nconsumptio

Ξ+Ξ+Ξ++=+ tt wc τπ

p

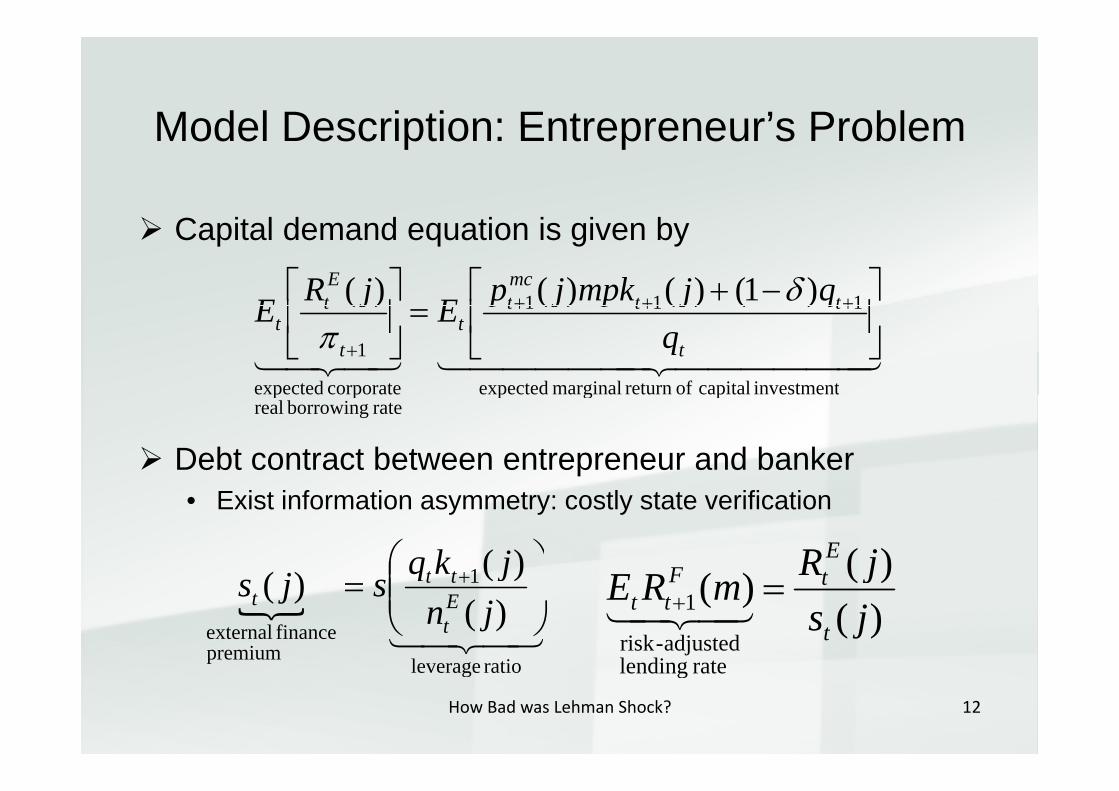

Model Description: Entrepreneur’s ProblemModel Description: Entrepreneur s Problem

EFaces stochastic survival rate, γEt+1

Each entering entrepreneur receives ‘start-up’ transfer from the household. Total ‘start-up’ transfer is ξE nE

t

For exiting 1- γEt+1 entrepreneurs, they transfer their

existing net worth back to household.e s g e o bac o ouse o d

So, the net transfer that household receive is (1- γE

t+1- ξE) nEt

Model Description: Entrepreneur’s ProblemModel Description: Entrepreneur s Problem

ααω −1)()()()( jljkAjjyProduction Function: {ω=

ShockTFP

Shockticidiosyncra

)()()()( jljkAjjy ttttt 321

Balance sheet equation is given by

)()()(1 jnjbjkq Et

Ettt +=+ )()()(

Net WorthLiabilityAsset

1 32132143421jnjbjkq tttt +

Income statement equation is given by

)( jRE

{ 44344214434421

43421capital of valueresale

tb i

11

costlabor revenue

)()1()()()()()( jkqjbjRlwjyjpjn ttEt

t

tttt

mct

Et δ

π−+−−= −

−

How Bad was Lehman Shock? 11

costborrowing

Model Description: Entrepreneur’s ProblemModel Description: Entrepreneur s Problem

Capital demand equation is given by

111 )1()()()(⎥⎤

⎢⎡ −+

⎥⎤

⎢⎡ +++ tt

mct

Et qjmpkjpEjRE δ

444444 3444444 2143421investmentcapitalofreturn marginalexpected

111

corporate expected

1

)()()()(⎥⎦

⎢⎣

=⎥⎦

⎢⎣

+++

+ t

tttt

t

tt q

qjpjpEjEπ

Debt contract between entrepreneur and banker

pgprate borrowing real

pp

• Exist information asymmetry: costly state verification

1 )()( ⎟⎞

⎜⎛ + jkqj tt )()( jRRE

EtF

{43421ratioleverage

1

premiumfinance external

)()()( ⎟⎟⎠

⎜⎜⎝

= +

jnjqsjs E

t

ttt )(

)()(

ratelendingadjusted-risk

1 jsjmRE

t

tFtt =+ 43421

How Bad was Lehman Shock? 12

ratioleverage ratelending

Model Description: Entrepreneur’s ProblemModel Description: Entrepreneur s Problem

A tiAggregation• Thanks to constant-return-to-scale production technology and

risk-neutrality of entrepreneur, marginal cost, MPL, MPK, and y p gleverage ratio are the same across entrepreneurs.

A t t th t itiAggregate net worth transition

1111 ][ Et

EEt

Et

ttk

tEt

Et nbRkqrn ξγ +−= ++++ 321

32143421

household from transferup-start

repaymentdebt

1capital from

return gross realized

1111 ][ ttt

ttttt q ξπ

γ+

++++

Notice that stochastic survival rate act like an aggregate net worth shock in corporate sector

13

Model Description: Banker’s ProblemModel Description: Banker s Problem

FFaces stochastic survival rate, γFt+1

Each entering banker receives ‘start-up’ transfer from the household. Total ‘start-up’ transfer is ξF nF

t

For exiting 1- γFt+1 bankers, they transfer their existing

net worth back to the household.e o bac o e ouse o d

So, the net transfer that household receive is (1- γF

t+1- ξF) nFt

Model Description: Banker’s ProblemModel Description: Banker s Problem

Balance sheet equation is given by

)()()( mnmbmb Ft

Ft

Et +=

321321321

net worthsbanker'

liabilitysbanker'

assetsbanker'

)()()( ttt

• Notice that banker’s asset becomes entrepreneur’s liability

Income statement equation is given byIncome statement equation is given by

)( RmR FEF

F

4342144 344 21 11

11 )()()()( mbRmbmRmn F

tt

tEt

t

tFt

++

++ −=

ππ

15

22repaymentdebt lending fromreturn gross

Model Description: Banker’s ProblemModel Description: Banker s Problem

Banker’s objective function is given by

)1()( FFFiF nEmV∞

∑= γγβ44444 344444 21

businessbankingofluepresent vanet

10

1 ,11)1()( iti

ittttt nEmV ++=

++++∑ −= γγβ

Moral hazard / costly enforcement problem

businessbanking of luepresent vanet

• Banker has a technology to divert fraction λ of his asset• Incentive constraint for a banker to remain in business becomes

EF

43421n valuereservatio

)()( mbmV Et

Ft λ≥

16bankerby retained

n valuereservatio

Model Description: Banker’s ProblemModel Description: Banker s Problem

Imposing this constraint, Gertler and Kiyotaki (2010) shows the NPV of banking business to be

Al th h b k l ti t b t i d b

)()()( mnmbmV Ftt

Ett

Ft ην +=

Also, they show bank leverage ratio to be constrained by

tEt mb ηφ≤)(

t

ttF

t

t

mn νληφ−

≡≤321

ratioleveragebank

)()(

Notice the similarity with Basel Regulation

ratioleveragebank

How Bad was Lehman Shock? 17

Model Description: Banker’s ProblemModel Description: Banker s Problem

AggregationAggregation• Gertler and Kiyotaki (2010) shows that νt, ηt, and φt to be equal

across bankers which makes the aggregation very simple.• Also given that E RF (m) is equal across m we can obtain the• Also given that EtRF

t(m) is equal across m, we can obtain the following aggregate transition of banking sector net worth.

Aggregate net worth transition of banking sector1

11 ][ Ft

FFt

tEt

FtF

tFt nbRbRn ξγ +−= +

321321321

household from transferup-start

repaymentdebtgross aggregate

1

lendingfromreturngross aggregate

111 ][ tt

tt

ttt nbbn ξ

ππγ +

++++

Notice that stochastic survival rate act like an aggregate net worth shock in banking sector.

repaymentdebt lendingfromreturn

net worth shock in banking sector.How Bad was Lehman Shock? 18

Model Description: Recap of Interest RatesModel Description: Recap of Interest Rates

There are two types of interest rate spreads in this model• External finance premium• Profit margin of bank lending rate

FE RRR { { ttEt RRR

tl dib kofmargin profit

ifinance external

>>ratelendingbank premium

Stemming from agency problem between entrepreneur and banker:

Stemming from agency problem between banker and depositor:

M l h d / tl f t

How Bad was Lehman Shock?19

Costly state verification Moral hazard / costly enforcement

Data Rich EstimationData-Rich Estimation

f G ( )The idea of Boivin and Giannoni’s (2006) Data-Rich method is to extract a common factor from multiple time series data and to match that with each observable variable in the model.match that with each observable variable in the model.• One-to-one matching (standard Bayesian estimation)• One-to-many matching (Data-Rich estimation)

A merit of this approach is that we can expect improved efficiency in estimating parameters and structural shocksefficiency in estimating parameters and structural shocks.

Why Data-Rich estimation in this paper?Why Data Rich estimation in this paper?• Since our focus is to obtain a reliable estimate of the impact of

Lehman Shock, Data-Rich estimation is vital.

How Bad was Lehman Shock? 20

Data Rich EstimationData-Rich Estimation

DSGE model in state-space form…

{ { { { {eq.)n transitiostate (optimal

)()(− Γ+Φ=

JNNNt1tt uss

{ { {

{ { { {equation)nt (measureme

)1()()1()()1( ×××××

+=JJNNNNN

ttt esΛx

The idea is to increase the dimension of X (i e larger

{ { { {)1()1()()1( ×××× MNNMM

The idea is to increase the dimension of Xt (i.e., larger M) by supplying multiple time series, while keeping the dimension of Φ, Γ, st, and ut constant. ⇒ Can expect efficiency gain in estimating structural parameters, smoothing states and structural shocks.

How Bad was Lehman Shock? 21

Data Rich Estimation: Measurement EqData-Rich Estimation: Measurement Eq.Case A set-up: (Standard Bayesian estimation)

tt es +⋅⎥⎥⎥

⎦

⎤

⎢⎢⎢

⎣

⎡=

⎥⎥⎥

⎦

⎤

⎢⎢⎢

⎣

⎡

OMM

L

L

M

1001

#1 datainflation #1 dataoutput

Case B set-up: (Data-Rich estimation)

⎥⎦⎢⎣⎥⎦⎢⎣ OMMM

⎤⎡⎤⎡

⎥⎥⎥⎤

⎢⎢⎢⎡

⎥⎥⎥⎤

⎢⎢⎢⎡

MMMM

L

L

M

00001

#2 dataoutput #1dataoutput

2yλ

tt es +⋅⎥⎥⎥⎥⎥

⎢⎢⎢⎢⎢

=⎥⎥⎥⎥⎥

⎢⎢⎢⎢⎢

L

L

MMMMM

01000

#1 datainflation n# dataoutput y ynλ

⎥⎥⎥⎥⎥

⎢⎢⎢⎢⎢

⎥⎥⎥⎥⎥

⎢⎢⎢⎢⎢

MMMM

L

M

00#2 datainflation 2πλ

22⎥⎥

⎦⎢⎢

⎣⎥⎥

⎦⎢⎢

⎣ MMMM

L

M

00n#datainflation nππ λ

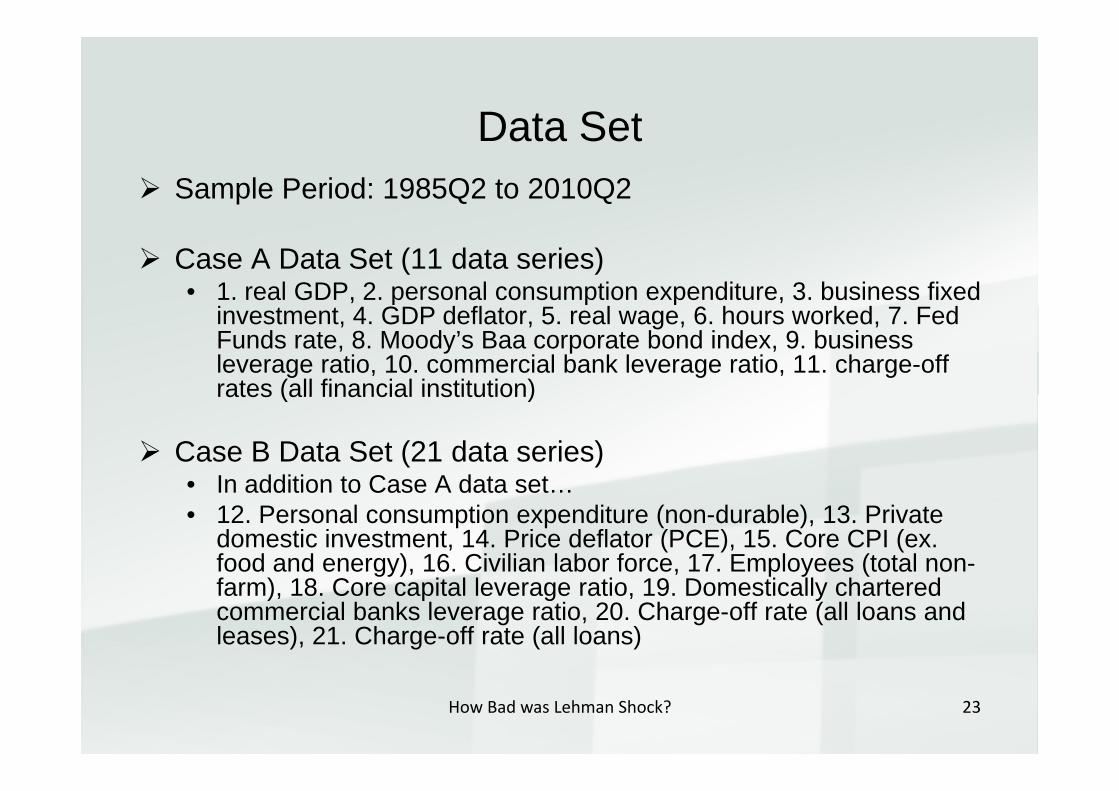

Data SetData SetSample Period: 1985Q2 to 2010Q2

Case A Data Set (11 data series)• 1. real GDP, 2. personal consumption expenditure, 3. business fixed

G finvestment, 4. GDP deflator, 5. real wage, 6. hours worked, 7. Fed Funds rate, 8. Moody’s Baa corporate bond index, 9. business leverage ratio, 10. commercial bank leverage ratio, 11. charge-off rates (all financial institution)rates (all financial institution)

Case B Data Set (21 data series)• In addition to Case A data set• In addition to Case A data set…• 12. Personal consumption expenditure (non-durable), 13. Private

domestic investment, 14. Price deflator (PCE), 15. Core CPI (ex. food and energy), 16. Civilian labor force, 17. Employees (total non-gy) p y (farm), 18. Core capital leverage ratio, 19. Domestically chartered commercial banks leverage ratio, 20. Charge-off rate (all loans and leases), 21. Charge-off rate (all loans)

How Bad was Lehman Shock? 23

Estimation Results: Estimated IRF

bank net worth shockcorporate net worth shock

24

Estimation Results: Smoothed Observables

Actual DataSmoothed (Case A)

How Bad was Lehman Shock? 25

Estimation Results: Smoothed Observables

Actual DataSmoothed (Case A)

How Bad was Lehman Shock? 26

Smoothed (Case B)

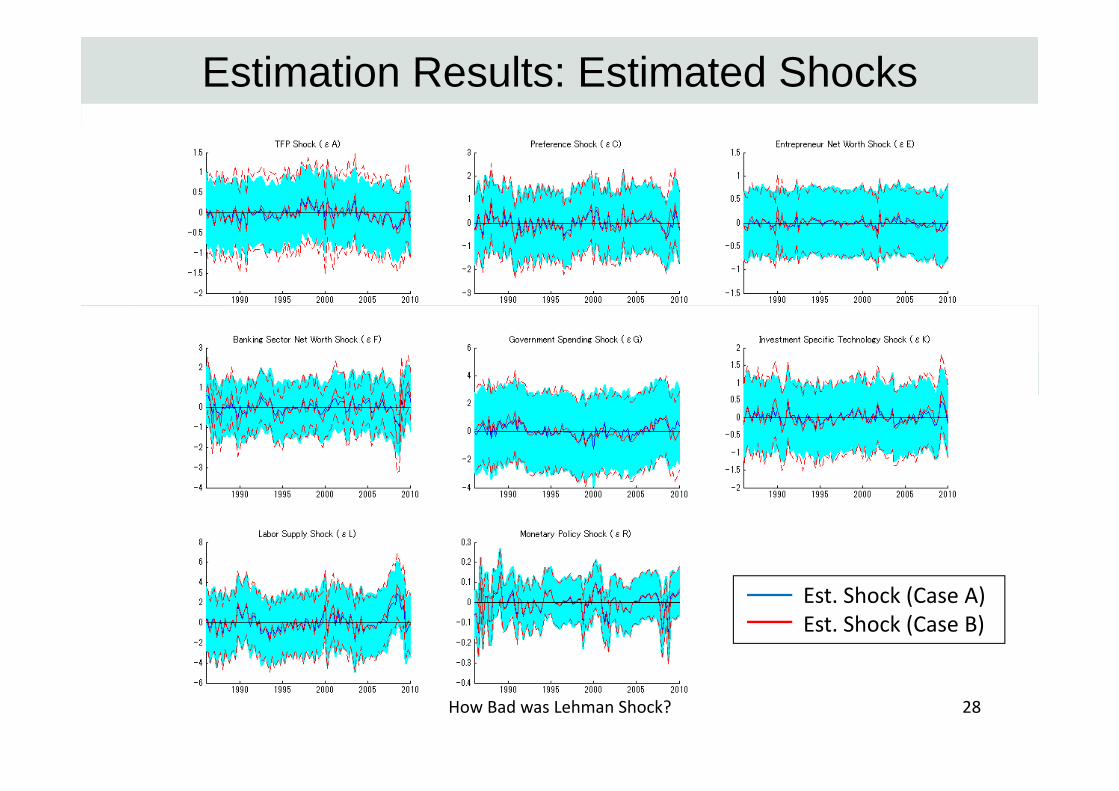

Estimation Results: Estimated Shocks

Est. Shock (Case A)

How Bad was Lehman Shock? 27

Estimation Results: Estimated Shocks

Est. Shock (Case A)Est. Shock (Case B)

How Bad was Lehman Shock? 28

Estimation Results: Bank Net Worth Shock

Est. Shock (Case A)

How Bad was Lehman Shock? 29

Estimation Results: Bank Net Worth Shock

Est. Shock (Case A)Est. Shock (Case B)

How Bad was Lehman Shock? 30

Historical Decomposition: Output (Case A)p p ( )

4

6

‐2

0

2

‐6

‐4

‐12

‐10

‐8

5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

TFP Shock Preference Shock

Entrepreneur Net Worth Shock Banking Sector Net Worth Shock

Government Spending Shock Investment Specific Technology ShockGovernment Spending Shock Investment Specific Technology Shock

Labor Supply Shock Monetary Policy Shock

Output Smoothed (Output)

How Bad was Lehman Shock? 31

Historical Decomposition: Output (Case B)p p ( )

4

6

‐2

0

2

‐6

‐4

‐12

‐10

‐8

5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

TFP Shock Preference Shock

Entrepreneur Net Worth Shock Banking Sector Net Worth Shock

Government Spending Shock Investment Specific Technology ShockGovernment Spending Shock Investment Specific Technology Shock

Labor Supply Shock Monetary Policy Shock

Output Smoothed (Output)

How Bad was Lehman Shock? 32

Historical Decomposition: Investment (Case A)p ( )

20

30

‐10

0

10

‐30

‐20

‐60

‐50

‐40

5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

TFP Shock Preference Shock

Entrepreneur Net Worth Shock Banking Sector Net Worth Shock

Government Spending Shock Investment Specific Technology ShockGovernment Spending Shock Investment Specific Technology Shock

Labor Supply Shock Monetary Policy Shock

Investment Smoothed (Investment)

How Bad was Lehman Shock? 33

Historical Decomposition: Investment (Case B)p ( )

20

30

‐10

0

10

‐30

‐20

‐60

‐50

‐40

5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

TFP Shock Preference Shock

Entrepreneur Net Worth Shock Banking Sector Net Worth Shock

Government Spending Shock Investment Specific Technology ShockGovernment Spending Shock Investment Specific Technology Shock

Labor Supply Shock Monetary Policy Shock

Investment Smoothed (Investment)

How Bad was Lehman Shock? 34

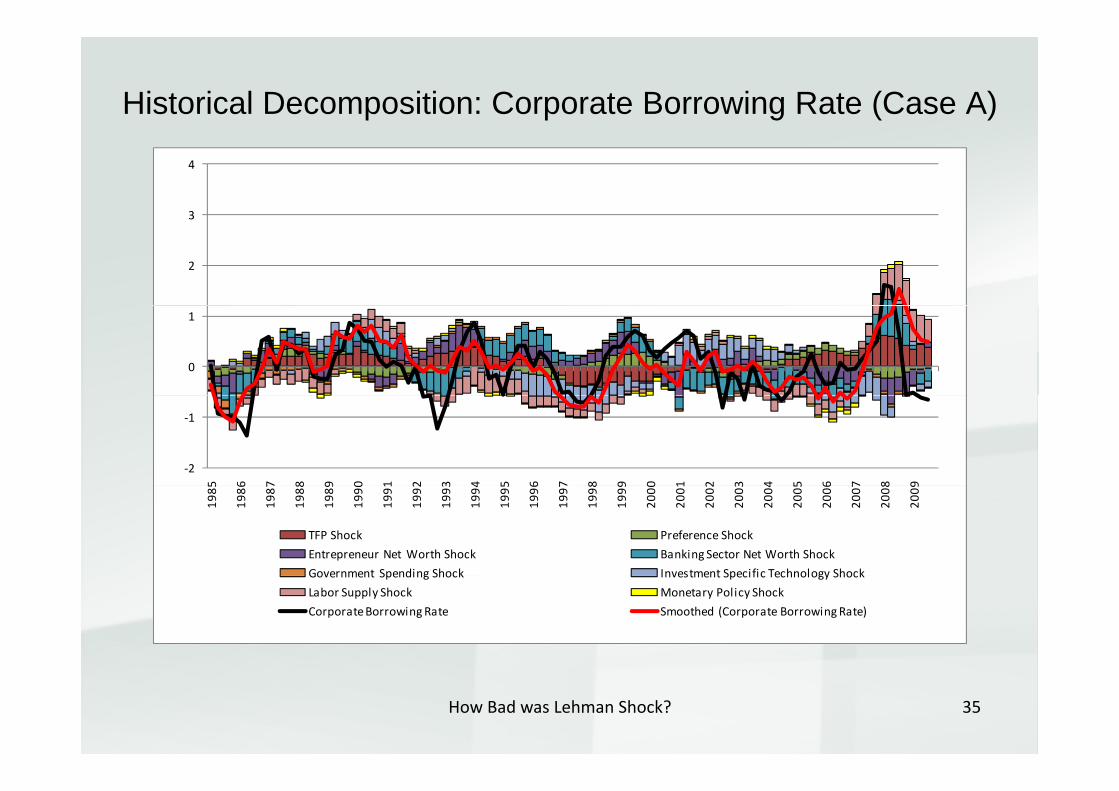

Historical Decomposition: Corporate Borrowing Rate (Case A)

3

4

2

3

0

1

‐2

‐1

5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

TFP Shock Preference Shock

Entrepreneur Net Worth Shock Banking Sector Net Worth Shock

Government Spending Shock Investment Specific Technology ShockGovernment Spending Shock Investment Specific Technology Shock

Labor Supply Shock Monetary Policy Shock

Corporate Borrowing Rate Smoothed (Corporate Borrowing Rate)

How Bad was Lehman Shock? 35

Historical Decomposition: Corporate Borrowing Rate (Case B)

3

4

2

3

0

1

‐2

‐1

5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

TFP Shock Preference Shock

Entrepreneur Net Worth Shock Banking Sector Net Worth Shock

Government Spending Shock Investment Specific Technology ShockGovernment Spending Shock Investment Specific Technology Shock

Labor Supply Shock Monetary Policy Shock

Corporate Borrowing Rate Smoothed (Corporate Borrowing Rate)

How Bad was Lehman Shock? 36

Historical Decomposition: Bank Leverage (Case A)p g ( )15

5

10

0

‐10

‐5

5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

TFP Shock Preference Shock

Entrepreneur Net Worth Shock Banking Sector Net Worth Shock

Government Spending Shock Investment Specific Technology ShockGovernment Spending Shock Investment Specific Technology Shock

Labor Supply Shock Monetary Policy Shock

Bank Leverage Smoothed (Bank Leverage)

How Bad was Lehman Shock? 37

Historical Decomposition: Bank Leverage (Case B)p g ( )15

5

10

0

‐10

‐5

5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

TFP Shock Preference Shock

Entrepreneur Net Worth Shock Banking Sector Net Worth Shock

Government Spending Shock Investment Specific Technology ShockGovernment Spending Shock Investment Specific Technology Shock

Labor Supply Shock Monetary Policy Shock

Bank Leverage Smoothed (Bank Leverage)

How Bad was Lehman Shock? 38

Historical Contribution of Bank Net Worth Shock

output

investinvest.

corp. borr. rate

profit margin

bank lev.

39

hist. cont. bank nw shock (Case A)

Historical Contribution of Bank Net Worth Shock

output

investinvest.

corp. borr. rate

profit margin

bank lev.

How Bad was Lehman Shock? 40

hist. cont. bank nw shock (Case A) hist. cont. bank nw shock (Case B)

Conclusion: Contributions of this paperConclusion: Contributions of this paper

Theoretical Contribution:• Combined two canonical financial friction

models and embedded to the stylized DSGE model.

E i i l C t ib tiEmpirical Contribution:• Adopted Data-Rich estimation method in

estimating bank net worth shock.

How Bad was Lehman Shock? 41

Conclusion: So How Bad was Lehman Shock?Conclusion: So How Bad was Lehman Shock?How large was the magnitude of Lehman Shock?• Largest bank net worth shock at least in past 25 years.

Much larger than those during S&L crisis.

How large was its impact to the economy?• Quite large. Lehman Shock may have suppressed

investment by nearly 10%.

Is it over?Is it over?• The shock seems to have been successfully countered by

TARP and aggressive credit easing that the recessionary effect directly caused by Lehman Shock seems to be over.

How Bad was Lehman Shock? 42