housing & economic development in the commonwealth

DESCRIPTION

Housing & Economic Development in the Commonwealth. Kirk Sykes President, Urban Strategies for America Fund Barry Bluestone Dean, School of Social Science, Urban Affairs, and Public Policy, Northeastern University Ted Carman - PowerPoint PPT PresentationTRANSCRIPT

Housing & Economic Development in the Commonwealth

Kirk Sykes President, Urban Strategies for America Fund

Barry Bluestone Dean, School of Social Science, Urban Affairs, and Public Policy, Northeastern University

Ted Carman President, Concord Square Development Corporation

Progressive Business Leaders NetworkOctober 26, 2007

The Economic State of the Commonwealth

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Jan-9

3

Jan-9

4

Jan-9

5

Jan-9

6

Jan-9

7

Jan-9

8

Jan-9

9

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

US MA

Economic Activity Index: Massachusetts vs. U.S. (1993-2007)

January 1993 – October 2001Leading the Nation

October 2001 – June 2007Lagging the Nation

2,800

2,900

3,000

3,100

3,200

3,300

3,400

3,500

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Nu

mb

er

Em

plo

yed

, in

Th

ou

san

ds

Feb 2001 - Dec 2003: -205,100

Dec 2003 - Dec 2006: +79,100

Jan 2007 - Aug 2007: +25,800

Feb 2001: 3,384.0

Dec 2003: 3,178.9

Aug 2007: 3,286.8

Jan 1996: 2,997.9 Jan 1996 - Feb 2001: + 386,100

Total Massachusetts Non-Farm Employment

Employment in Massachusetts

-2.8%

0.5%

1.3%

1.7%

2.9%

3.8%

4.2%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

MA CT ME VT NH RI U.S.

-95,900 jobs

+5,566,000 jobs

Source: U.S. Bureau of Labor

Change in Total Non-Farm Employment (Seasonally Adjusted) (January 2001 - August 2007)

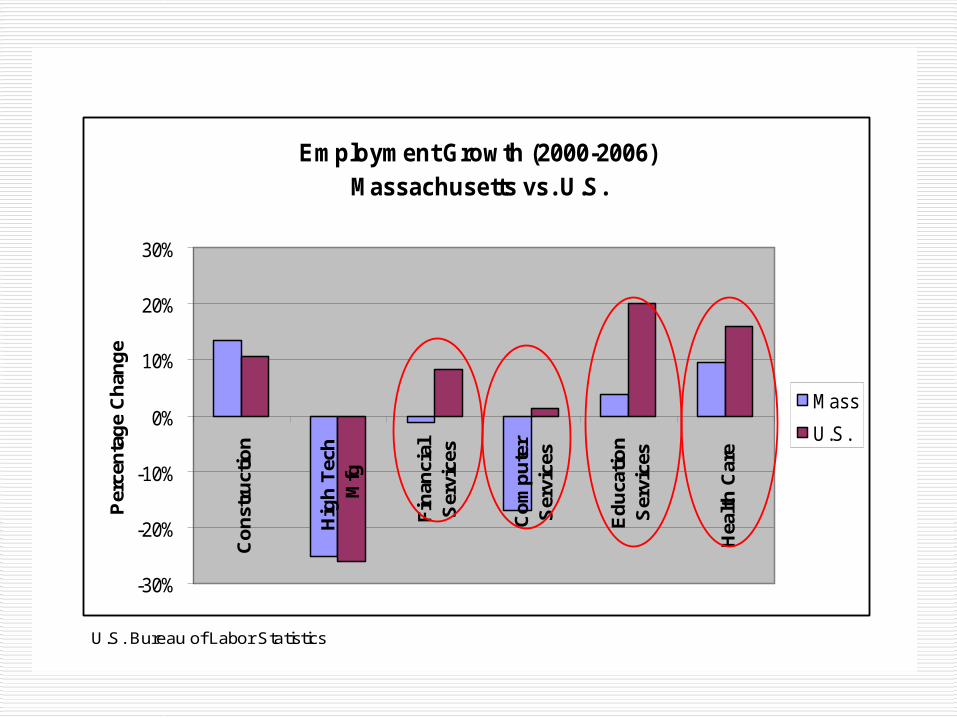

Employment Growth (2000-2006) Massachusetts vs. U.S.

-30%

-20%

-10%

0%

10%

20%

30%C

on

stru

ctio

n

Hig

h T

ech

Mfg

Fin

anci

alS

ervi

ces

Co

mp

ute

rS

ervi

ces

Ed

uca

tio

nS

ervi

ces

Hea

lth

Car

e

Per

cen

tag

e C

han

ge

Mass

U.S.

U.S. Bureau of Labor Statistics

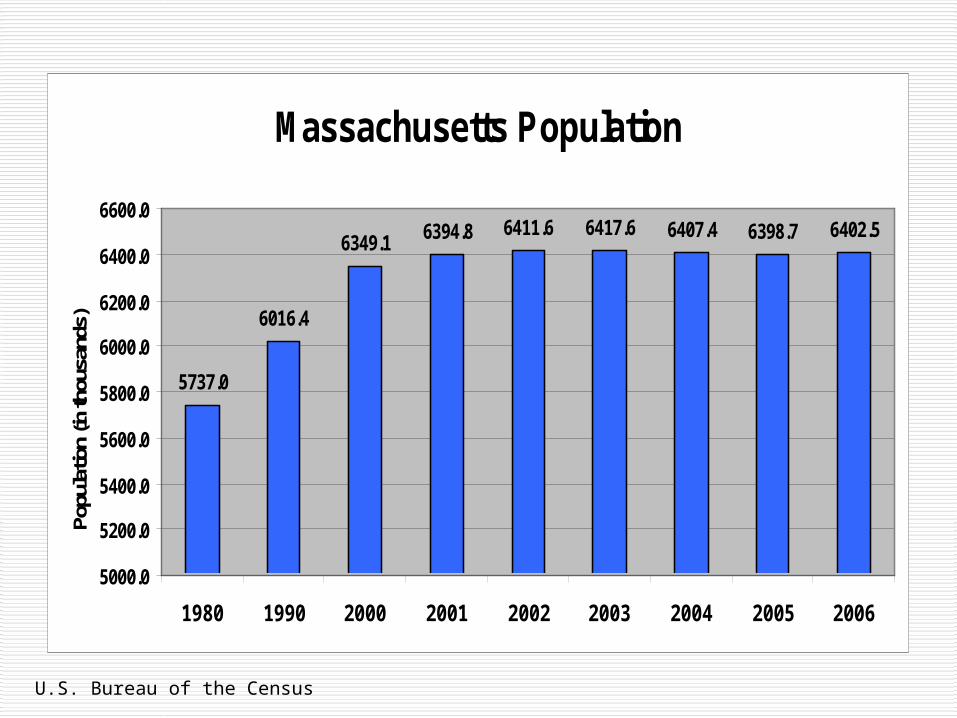

• Between 2000 and 2006, the population of Massachusetts increased by only 74,000 (1.2%) – the slowest increase in New England.

• Since 2000, Massachusetts has suffered a net domestic out-migration of over 280,000 residents.

• This outflow of people has been softened only somewhat by the arrival of about 186,000 foreign immigrants.

Population Trends

Massachusetts Population

5737.0

6016.4

6349.1 6394.8 6411.6 6417.6 6407.4 6398.7 6402.5

5000.0

5200.0

5400.0

5600.0

5800.0

6000.0

6200.0

6400.0

6600.0

1980 1990 2000 2001 2002 2003 2004 2005 2006

Popu

latio

n (in

thou

sand

s)

U.S. Bureau of the Census

Population Trends in New England

Population Growth, 2000-2006

1.17%1.60%

2.28%2.70%

3.45%

5.98% 6.09%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

MA RI VT CT ME NH US

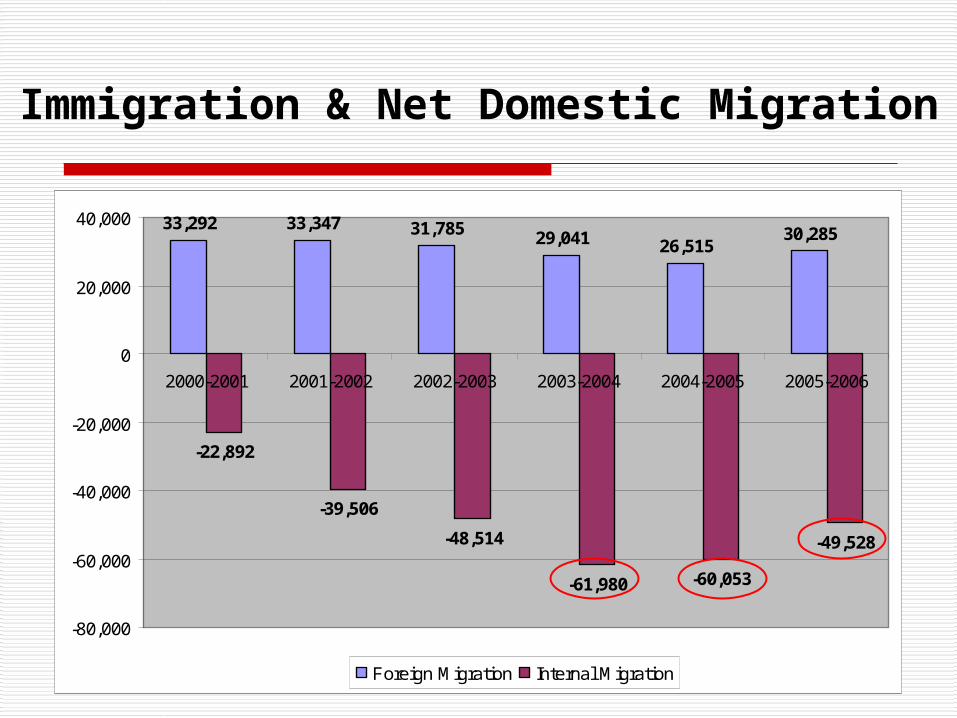

33,292 33,347 31,785 29,041 26,51530,285

-22,892

-39,506

-48,514

-61,980 -60,053

-49,528

-80,000

-60,000

-40,000

-20,000

0

20,000

40,000

2000-2001 2001-2002 2002-2003 2003-2004 2004-2005 2005-2006

Foreign Migration Internal Migration

Immigration & Net Domestic Migration

-8.91%-8.69%

-15

-10

-5

0

5

10

15

20

25

30

Under 5 5-19 20-24 25-34 35-54 55-64 65+

Massachusetts US

Who’s Leaving Massachusetts?

Where did they go?

TX

CA

MT

AZ

ID

NV

NM

CO

IL

OR

UT

KS

WY

IA

SD

NE

MN

ND

FL

OK

WI

MO

AL

WA

GA

AR

LA

MI

IN

NY

PA

NC

MS

TN

KYVA

OH

SC

ME

WV

MI VTNH

MD

NJ

MA

CT

DE

RI

Net Migration* Betweeen Massachusetts and Competitor States1990-2002

*Thicker line represents more migration

State Net Migration from State

Florida -99,082 New Hampshire -78,201 California -23,978 Arizona -11,033 North Carolina -8,983 Washington -4,516

Stagnant Incomes/Rising Poverty in Greater Boston

Year 2000 2002 2004 2005 % Change 2000-2005

Real Median Household Income

$62,481 $65,569 $64,060 $62,462 -0.03%

Real Median Homeowner Income

$80,995 $82,925 $80,936 $81,886 1.10%

Real Median Renter Income

$38,780 $39,602 $39,762 $35,748 -7.82%

Families Below the Poverty Line

59,913 58,882 68,687 68,038 +13.56%

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

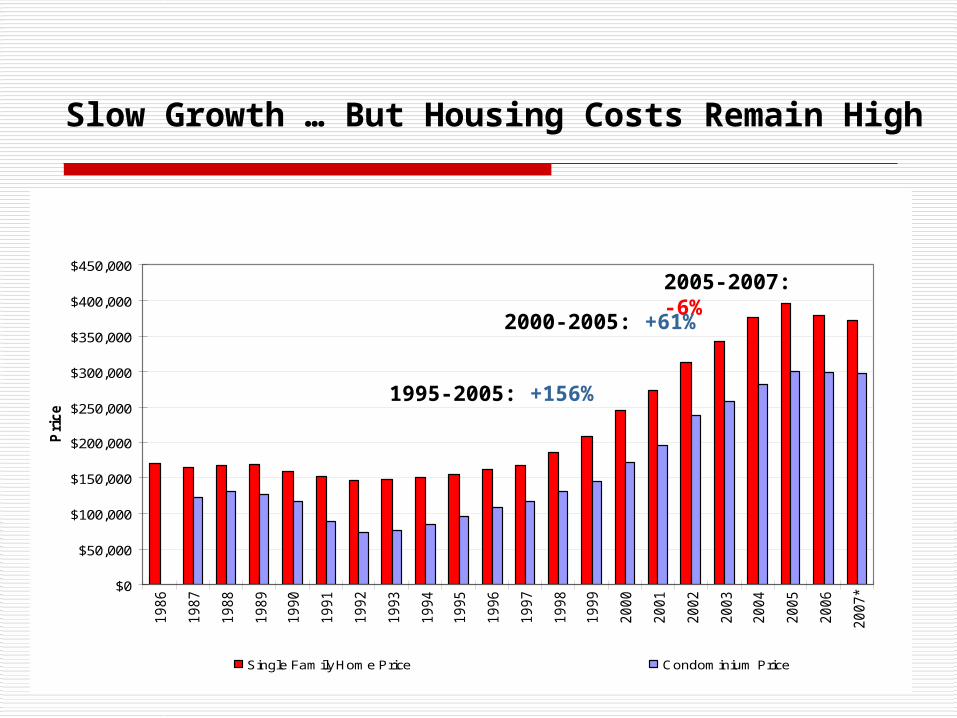

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007*

Pri

ce

Single Family Home Price Condominium Price

1995-2005: +156%

2005-2007: -6%

Slow Growth … But Housing Costs Remain High

Median Price of Single Family Homes and Condominiums

2000-2005: +61%

Effective Rents – Rising Again

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

1995 - 2005: +58%

2000 - 2005: +1%2005 - 1Q 2007: +6%

(Un)Affordable Communities in Greater Boston

• In 2007, only 6 communities out of 161 in Greater Boston – Bellingham, Blackstone, Bolton, Southborough, Stow, and Townsend – are affordable for a typical first-time homebuyer in 2007

• Back in 1998, affordable housing was available in 116 Greater Boston communities

Year

Communities Affordable to Median Income Homebuyer Purchasing Median Priced

House (20% down payment)

Percent Affordable

Communities

Communities Affordable to First Time Homebuyer Earning 80% of Median Purchasing House Priced

at 80% of Median (10% down payment)

First Time Homebuyer

Percent Affordable

Communities

1998 148 92% 116 72%

2000 101 63% 87 54%

2001 86 53% 42 26%

2002 77 48% 17 11%

2003 59 37% 5 3%

2004 27 17% 1 <1%

2005 19 12% 0 0%

2006 30 19% 1 <1%

2007* 46 29% 6 4%

Summary of Affordability Gap Analysis

Number of Affordable Communities

Housing Affordability in Greater Boston

2000 2005Renter Households paying >30% of Income

39.2% 50.1%

Renter Households paying >50% of Income

18.4% 25.0%

Owner-Occupied Households paying >30% of Income

26.7% 39.3%

Owner-Occupied Households paying >50% of Income

9.0% 13.9%

Year Total Units

% Change from Prior

Year

Units in Single Family

Structures

% Change from Prior

Year

SingleFamily as

%of Total

Units in 2-4 Unit

Structures

Units in 5+ Unit

Structures

% Change

from Prior Year

1998 10,846 8,639 79.7% 574 1,633

1999 10,662 -1.7% 7,775 -10.0% 72.9% 746 2,141 31.1%

2000 10,342 -3.0% 7,102 -8.7% 68.7% 701 2,539 18.6%

2001 9,701 -6.2% 6,313 -11.1% 65.1% 686 2,702 6.4%

2002 9,520 -1.9% 6,408 1.5% 67.3% 764 2,348 -13.1%

2003 12,121 27.3% 6,020 -6.1% 49.7% 1,093 5,003 113.1%

2004 13,556 11.8% 7,000 16.3% 51.6% 994 5,562 11.2%

2005 15,561 14.8% 7,270 3.9% 46.7% 1,015 7,276 30.8%

2006 13,759 -11.6% 5,429 -25.3% 39.5% 1,224 7,107 -2.3%

2007 est. 9,950 -27.7% 4,094 -24.6% 41.1% 713 5,228 -26.4%

Single Family v. Multifamily Building Permits in Greater Boston

Housing Production in Greater Boston

Needed Production: 18,000 Units/Year

Housing Costs and Economic Development

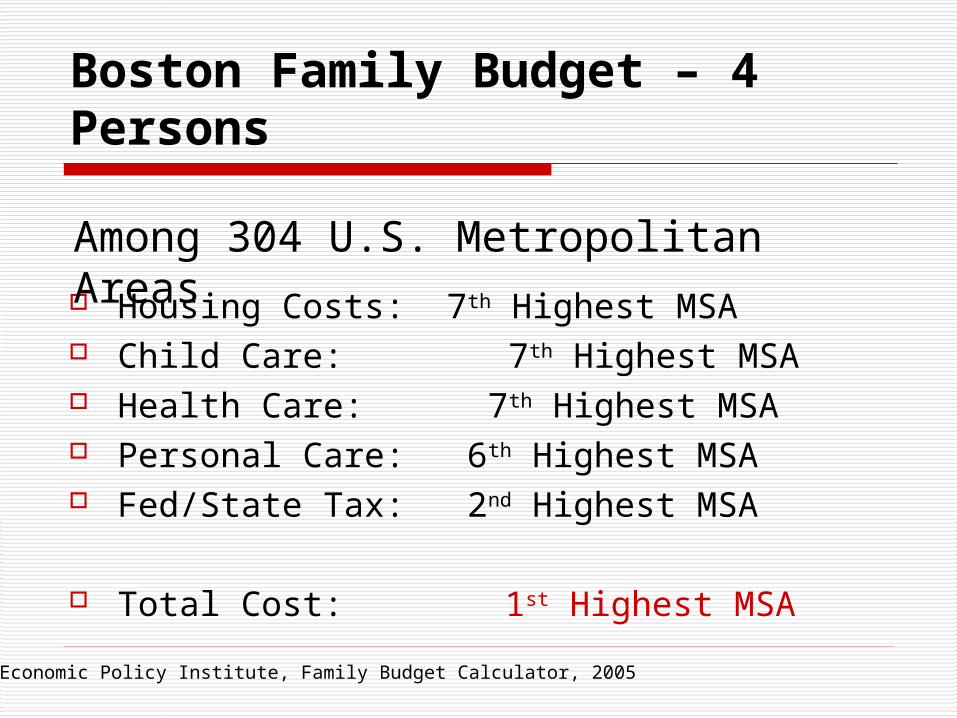

Boston Family Budget – 4 Persons

Housing Costs: 7th Highest MSA Child Care: 7th Highest MSA Health Care: 7th Highest MSA Personal Care: 6th Highest MSA Fed/State Tax: 2nd Highest MSA

Total Cost: 1st Highest MSA

Economic Policy Institute, Family Budget Calculator, 2005

Among 304 U.S. Metropolitan Areas

Top Decile: Metro Area Cost of Living

Boston $ 64,656Washington (D.C. portion) $ 61,440Nassau-Suffolk, NY $ 60,780 Stamford-Norwalk, CN $ 60,720 Lawrence (Mass. portion) $ 59,280 New York, NY $ 58,656 Barnstable-Yarmouth, MA $ 58,236 San Francisco, CA $ 57,624 Worcester (Mass. portion) $ 55,704Springfield, MA $ 55,320Minneapolis-St. Paul, MN $ 54,948 Nashua, NH $ 54,852 Santa Cruz-Watsonville, CA $ 53,808Oakland, CA $ 53,412 San Jose, CA $ 52,800 Pittsfield, MA $ 52,632 Rochester, MN $ 51,288

Monmouth-Ocean, NJ $ 50,736San Diego, CA $ 50,088Newark, NJ $ 49,992New Haven-Meriden, CN $ 49,848Honolulu, HI $ 49,824Philadelphia (Pa. portion) $

49,716Boulder-Longmont, CO $ 49,596Bridgeport, CN $ 49,272Manchester, NH $

49,152Santa Rosa, CA $ 48,924Albany-Schenectady-Troy, NY $ 48,900Hartford, CN $ 48,684Trenton, NJ $ 48,576Rochester, NY $ 48,540

Economic Policy Institute: Family Budget Calculator

Universe: 304 U.S. Metro Areas

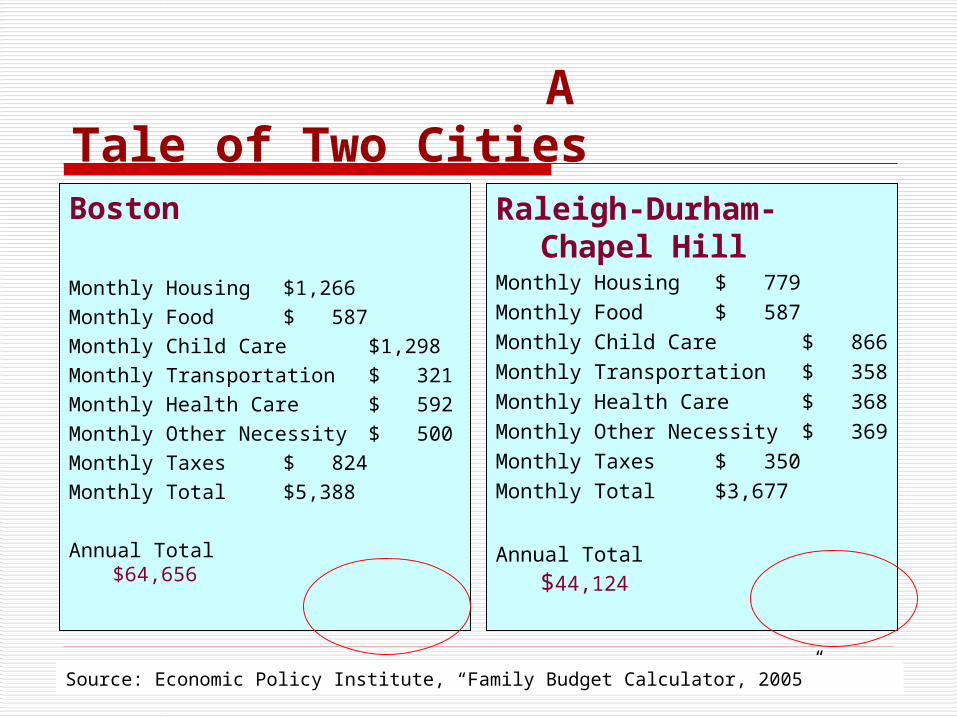

A Tale of Two CitiesBasic Budget2 Parents, 2 Children

Boston

Monthly Housing $1,266

Monthly Food $ 587

Monthly Child Care $1,298

Monthly Transportation $ 321

Monthly Health Care $ 592

Monthly Other Necessity $ 500

Monthly Taxes $ 824

Monthly Total $5,388

Annual Total $64,656

Raleigh-Durham-Chapel Hill

Monthly Housing $ 779

Monthly Food $ 587

Monthly Child Care $ 866

Monthly Transportation $ 358

Monthly Health Care $ 368

Monthly Other Necessity $ 369

Monthly Taxes $ 350

Monthly Total $3,677

Annual Total $44,124

A Tale of Two Cities

Source: Economic Policy Institute, “Family Budget Calculator, 2005”

Employment Growth (%) (2000-2004)

-1.00%

-0.50%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

1 2 3 4 5 6 7 8 9 10

Housing Price Decile

Per

cent

Cha

nge

Low Price High Price

Economic Policy Institute, “Family Budget Calculator, 2005”; U.S. Bureau of Labor Statistics

Universe: 245 U.S. Metro Areas

0.95%

2.91%

2.29%

0.86%

1.53%

0.68%

-0.68%

0.12%

-0.62%

1.49%

Employment Growth (%) (2000-2004)

-1%

0%

1%

2%

3%

1 2 3 4 5 6 7 8 9 10

Cost of Living Decile

Per

cent

Cha

nge

Low Cost High Cost

Economic Policy Institute, “Family Budget Calculator, 2005”; U.S. Bureau of Labor Statistics

-0.21%

0.93%

-0.02%

0.84%1.06%

0.50%

1.09%

1.98%

0.62%

2.53%

Universe: 245 U.S. Metro Areas

Internal Net Migration (%) (2000-2004)

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

1 2 3 4 5 6 7 8 9 10

Housing Cost Decile

Decil

e P

erc

en

t

Boston MSA (-5.2%)

Economic Policy Institute, “Family Budget Calculator, 2005”; U.S. Bureau of the Census

Universe: 304 U.S. Metro Areas

Internal Net Migration (2000-2004)

-2.50%

-2.00%

-1.50%

-1.00%

-0.50%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

1 2 3 4 5 6 7 8 9 10

Cost of Living Decile

Dec

ile

Per

cen

t

-2.12%

0.16%

1.54%1.40%

2.19%

1.04%

0.60%0.41%

0.19%

0.39%

Economic Policy Institute, “Family Budget Calculator, 2005”; U.S. Bureau of the Census

Universe: 304 U.S. Metro Areas Boston

Key Point

Housing Costs – and more generally the cost of living – is a key economic challenge in the Commonwealth … and perhaps the #1 barrier to a full economic recovery

Progress on the Housing Front: Chapter 40R/40S

ADD SLIDES FROM TED CARMAN

Chapter 40R/40S

• As of July 2007, 16 communities in Massachusetts towns have approved Chapter 40R “Smart Growth” districts. More than 30 others are considering such districts.

• Existing 40R Districts can provide over 5,800 new units of housing

• Over 3,000 more units in the pipeline

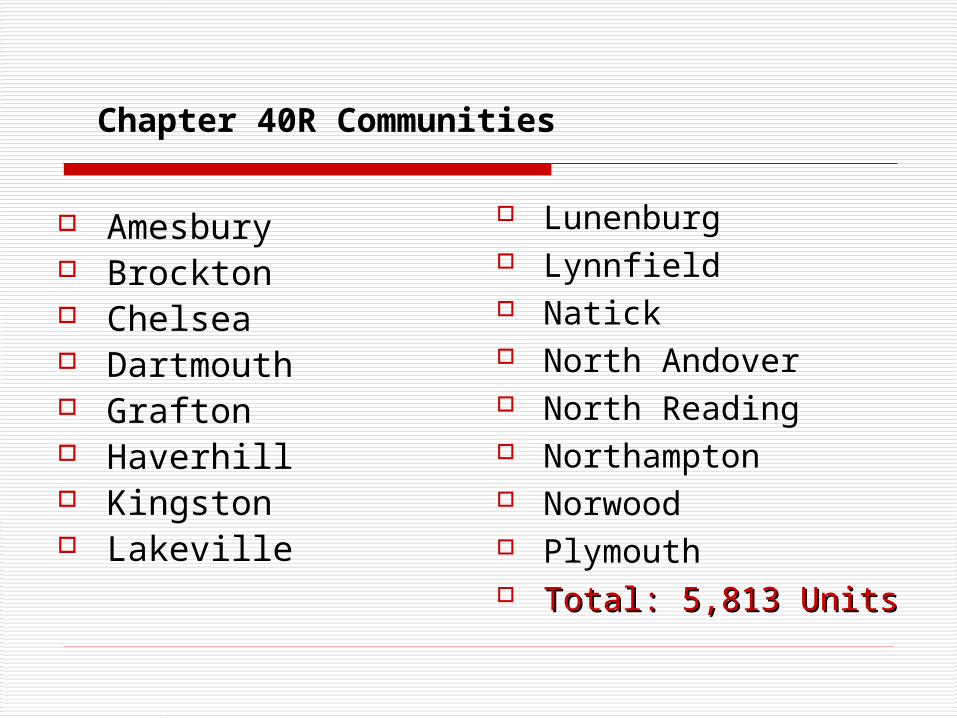

Chapter 40R Communities

Amesbury Brockton Chelsea Dartmouth Grafton Haverhill Kingston Lakeville

Lunenburg Lynnfield Natick North Andover North Reading Northampton Norwood Plymouth Total: 5,813 UnitsTotal: 5,813 Units

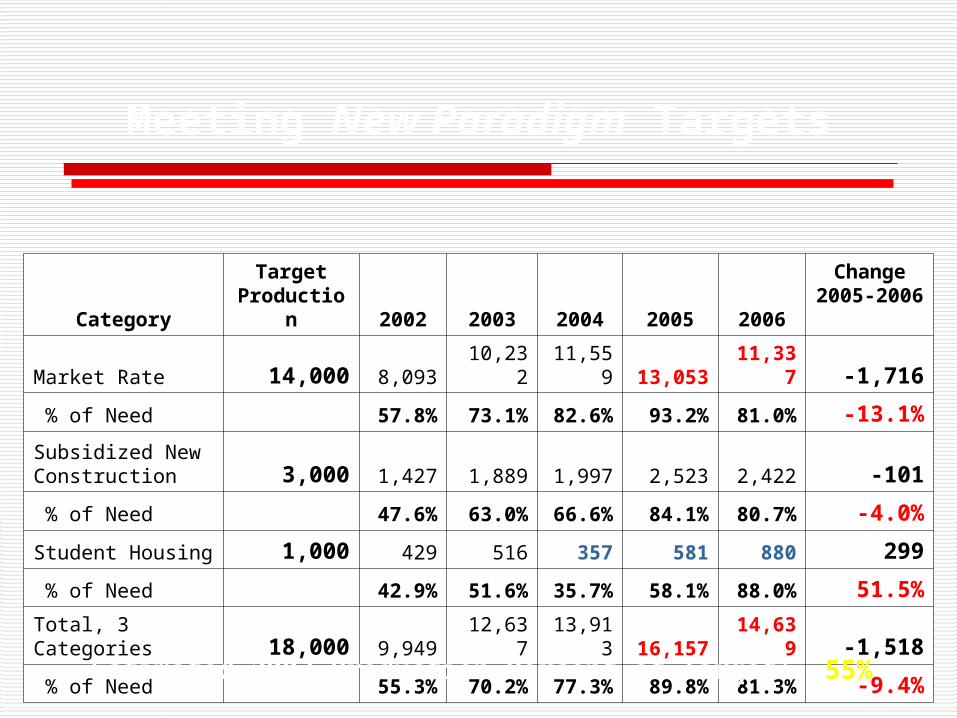

CategoryTarget

Production 2002 2003 2004 2005 2006Change

2005-2006

Market Rate 14,000 8,093 10,232 11,559 13,053 11,337 -1,716

% of Need 57.8% 73.1% 82.6% 93.2% 81.0% -13.1%

Subsidized New Construction 3,000 1,427 1,889 1,997 2,523 2,422 -101

% of Need 47.6% 63.0% 66.6% 84.1% 80.7% -4.0%

Student Housing 1,000 429 516 357 581 880 299

% of Need 42.9% 51.6% 35.7% 58.1% 88.0% 51.5%

Total, 3 Categories 18,000 9,949 12,637 13,913 16,157 14,639 -1,518

% of Need 55.3% 70.2% 77.3% 89.8% 81.3% -9.4%

Meeting New Paradigm Targets

Estimated 2007 Production Percent of Target: 55%

Conclusions

The “Perfect Storm” – Anxious homeowners, declining production … but no improvement in affordability

The weak economy is linked to the continuing housing crisis

We still have a lot to do to get us back on track toward economic prosperity equitably shared

Finding Solutions

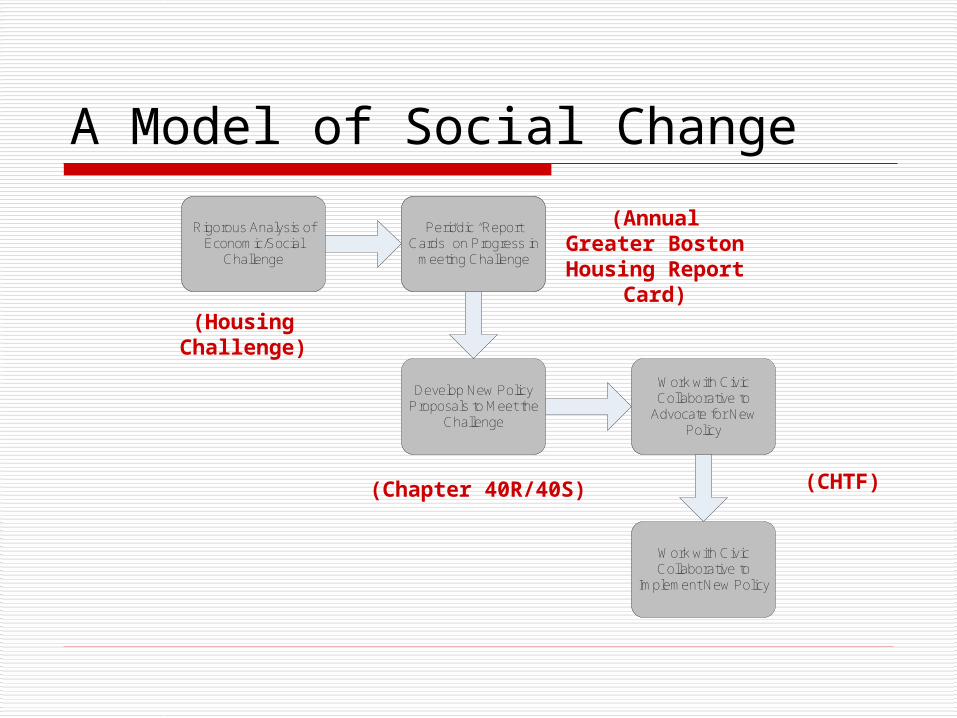

A Model of Social Change

Rigorous Analysis of Economic/Social

Challenge

Periodic “Report Cards” on Meeting the

Challenge

Develop New Policy Proposals to Meet the

Challenge

Work with Civic Collaborative to

Advocate for New Policy

Work with Civic Collaborative to

Implement New Policy

Periodic “Report Cards” on Progress in

meeting Challenge

(Housing Challenge)

(Annual Greater Boston Housing Report Card)

(Chapter 40R/40S) (CHTF)

The Nature of the Problem

With housing – Two Americas

1. The Midwest, the South, the Southwest.

2. The East Coast and the West Coast

Therefore – the problems are not inevitable

The Culprits

Zoning

Multiple Academic Studies Govt. Regulations

Shortage of Land for building

Increases land costs Extensive permitting delays

Local and State Finance

Perverse Interaction

Prop. 2 ½ Property Taxes Chapter 70

Single Family Home

Sale price - $400,000 Property taxes at .15 = $6,000 Half for school costs = $3,000 On average – 1 school child

Actual cost of education: $10,000

A New House

Local Costs: Loss of Open Space Increase in traffic More public services Education

State Benefits Sales Tax Income Tax Corporate Tax

It’s no Surprise

Local communities do all they can to discourage the production of housing.

They are remarkably successful

The economy shows the results

Smart Growth Zoning

Chapters 40R and 40S

Goal: a surplus of zoned land

Incentives if: Smart Growth Locations 20% of units affordable Minimum Densities

Incentives

Initial Payment - $1,000 per unit

Construction Payment - $3,000 / Unit

School Cost Hold Harmless

Design Standards

How has it worked?

Zoned land for 6,000 units 3,000 more in the pipeline Diverse developments and communities

17 of 17 communities have approved A cooperative dynamic

But, all multifamily.

Starter Homes still not being built

Starter Homes

Credible long term funding for school costs.

Additional incentives.

Proposal in the works.

Public Policy Ingredients

A good idea

Institutional Support

Significant Funding

Intense effort

Broad and deep process

How Did it Happen?

18 months from concept paper to legislation

The Commonwealth Housing Task Force The Center for Urban and Regional Policy The Boston Foundation The Legislature and Administration

Conclusion

Much Success, but, more to be done.

The Process can be replicated.