hotels & hospitality - jll · hotels & hospitality hotel intelligence paris 2013 ......

TRANSCRIPT

Hotels & Hospitality

Hotel Intelligence Paris 2013

With record performance results in 2011 and 2012, Paris has confirmed the strength and dynamism of its hotel market. 2013 is expected to witness a continued growth in Revenue Per Available Room, albeit at a slower rate due to the continued weakness in the global economy.

2 Hotel Intelligence: Paris

Authors

Market Snapshot Record foreign tourist arrivals in 2012 Paris is as a leading trade fair and congress destination Record number of passengers at Paris airports in 2012 A well balanced hotel mix from budget to luxury Limited new supply due to high barriers to entry Three consecutive years of record trading performance Positive trading expectations for 2013

Josef Filser Associate, EMEA [email protected]

Table of Contents

3

4

5

6

6

7

9

10

Jones Lang LaSalle’s Hotels & Hospitality Group serves as the hospitality industry’s global leader in real estate services for luxury, upscale, select service and budget hotels; timeshare and fractional ownership properties; convention centers; mixed-use developments and other hospitality properties. The firm’s more than 265 dedicated hotel and hospitality experts partner with investors and owner/operators around the globe to support and shape investment strategies that deliver maximum value throughout the entire lifecycle of an asset. In the last five years, the team completed more transactions than any other hotels and hospitality real estate advisor in the world totaling nearly US$25 billion, while also completing approximately 4,000 advisory and valuation assignments. The group’s hotels and hospitality specialists pro-vide independent and expert advice to clients, backed by industry-leading research. For more news, videos and research from Jones Lang LaSalle’s Hotels & Hospitality Group, please visit: www.jll.com/hospitality

Marcus Linden Research Assistant, EMEA [email protected]

Gwenola Donet Director, France [email protected]

Bastien Buffat Analyst, France [email protected]

Hotel Intelligence: Paris 3

Market Snapshot

Tourism: Paris is the economic, cultural and administrative

capital of France, and one of the world’s most visited cities. The

French capital benefits from a diversified demand, well-balanced

between leisure and business, and between domestic and

foreign clientele. Over the last decade, Paris has witnessed

stable levels of tourism demand with visitation and overnight

stays showing an annual average growth rate (CAAG) of 1.1%

and 0.6% respectively.

Supply: As at January 2013, the graded hotel supply in Paris

comprised 1,475 hotels, offering a total of 78,382 rooms. The

market is well balanced in terms of room supply with 34% in the

upscale segment, 38% in the midscale segment and 28% in

budget/economy segment. Room supply in Paris in the past 10

years has grown by only +0.3% annually due to the scarcity of

land plots available for hotel development. Hotel supply is only

expected to increase marginally in the coming years with 3,900

bedrooms currently in the development pipeline. New hotels are

primarily positioned in the upscale segment.

Trading: Revenue per available room (RevPAR) in Paris

rebounded quickly after the downturn in 2009. Since then, hotels

have recorded positive growth in performance year-on-year with

occupancy levels at about 78%. RevPAR grew by 14% in 2011

and by another 8% in 2012 to €202, representing a 10-year

high. Overall, RevPAR has grown at about twice the level of

inflation over the past 8 years.

4 Hotel Intelligence: Paris

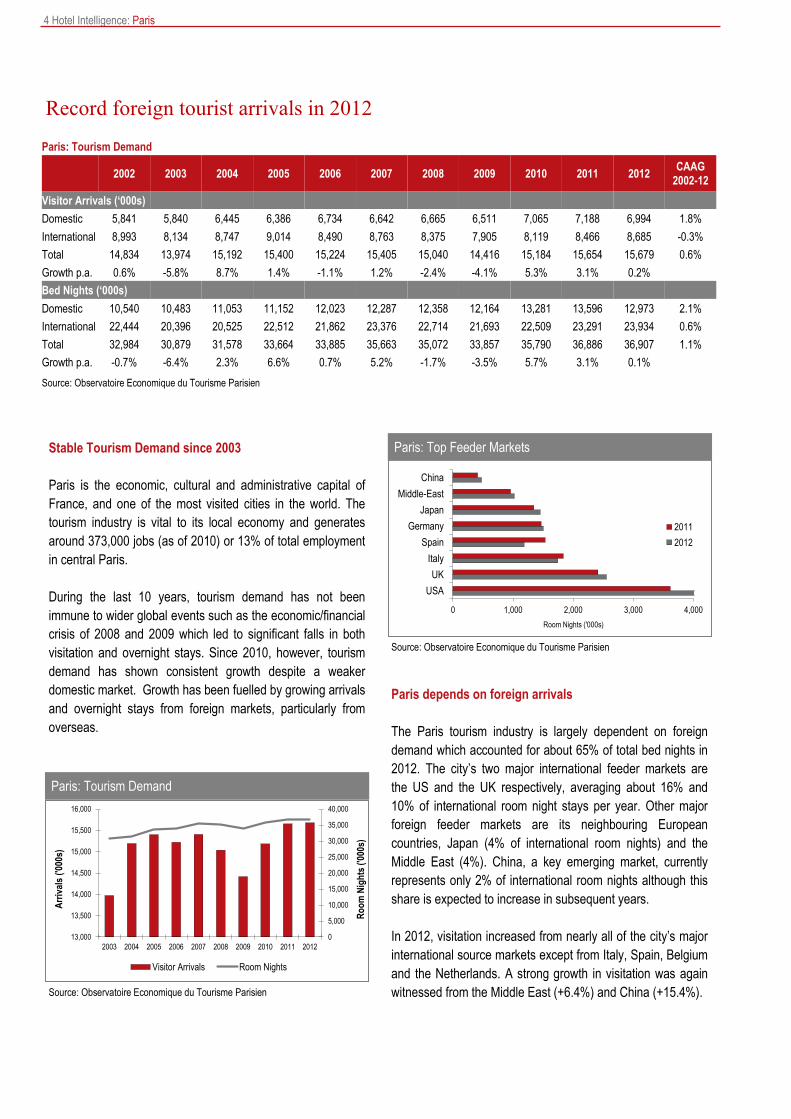

Record foreign tourist arrivals in 2012

Stable Tourism Demand since 2003

Paris is the economic, cultural and administrative capital of

France, and one of the most visited cities in the world. The

tourism industry is vital to its local economy and generates

around 373,000 jobs (as of 2010) or 13% of total employment

in central Paris.

During the last 10 years, tourism demand has not been

immune to wider global events such as the economic/financial

crisis of 2008 and 2009 which led to significant falls in both

visitation and overnight stays. Since 2010, however, tourism

demand has shown consistent growth despite a weaker

domestic market. Growth has been fuelled by growing arrivals

and overnight stays from foreign markets, particularly from

overseas.

Paris depends on foreign arrivals

The Paris tourism industry is largely dependent on foreign

demand which accounted for about 65% of total bed nights in

2012. The city’s two major international feeder markets are

the US and the UK respectively, averaging about 16% and

10% of international room night stays per year. Other major

foreign feeder markets are its neighbouring European

countries, Japan (4% of international room nights) and the

Middle East (4%). China, a key emerging market, currently

represents only 2% of international room nights although this

share is expected to increase in subsequent years.

In 2012, visitation increased from nearly all of the city’s major

international source markets except from Italy, Spain, Belgium

and the Netherlands. A strong growth in visitation was again

witnessed from the Middle East (+6.4%) and China (+15.4%).

Paris: Tourism Demand

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

13,000

13,500

14,000

14,500

15,000

15,500

16,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Ro

om

Nig

hts

('0

00s)

Arr

ival

s ('

000s

)

Visitor Arrivals Room Nights

Source: Observatoire Economique du Tourisme Parisien

Source: Observatoire Economique du Tourisme Parisien

Paris: Top Feeder Markets

0 1,000 2,000 3,000 4,000

USA

UK

Italy

Spain

Germany

Japan

Middle-East

China

Room Nights ('000s)

2011

2012

Paris: Tourism Demand

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 CAAG

2002-12

Visitor Arrivals (‘000s)

Domestic 5,841 5,840 6,445 6,386 6,734 6,642 6,665 6,511 7,065 7,188 6,994 1.8%

International 8,993 8,134 8,747 9,014 8,490 8,763 8,375 7,905 8,119 8,466 8,685 -0.3%

Total 14,834 13,974 15,192 15,400 15,224 15,405 15,040 14,416 15,184 15,654 15,679 0.6%

Growth p.a. 0.6% -5.8% 8.7% 1.4% -1.1% 1.2% -2.4% -4.1% 5.3% 3.1% 0.2%

Bed Nights (‘000s)

Domestic 10,540 10,483 11,053 11,152 12,023 12,287 12,358 12,164 13,281 13,596 12,973 2.1%

International 22,444 20,396 20,525 22,512 21,862 23,376 22,714 21,693 22,509 23,291 23,934 0.6%

Total 32,984 30,879 31,578 33,664 33,885 35,663 35,072 33,857 35,790 36,886 36,907 1.1%

Growth p.a. -0.7% -6.4% 2.3% 6.6% 0.7% 5.2% -1.7% -3.5% 5.7% 3.1% 0.1%

Source: Observatoire Economique du Tourisme Parisien

Hotel Intelligence: Paris 5

Paris is as a leading trade fair and

congress destination

In terms of foreign arrivals, Paris is to some extent affected by

exchange rate fluctuations. A weak Euro in 2012 certainly had

a positive impact on foreign visitation, particularly on tourist

arrivals from the US and the UK. We could anticipate a similar

trend in 2013/14.

The capital benefits from a well balanced mix between

leisure and corporate business

Paris benefits from a diversified client mix, attracting leisure,

corporate and trade fair/congress business. In 2011, business

demand, including the corporate and meetings, incentives,

conferences and exhibitions (MICE) sectors, represented

about 45% of total hotel room nights in Paris. This high ratio is

partially explained by the fact that the capital is home to the

largest office market in Europe with around 52 million sq. m. It

is the second largest in the world after New York.

The majority of tourists are leisure guests and attracted by the

capital’s cultural offerings such as its world famous museums

and monuments. This includes the Louvre Museum with

almost 9 million visitors per annum and the Eiffel tower with 7

million visitors per annum. In more recent years Euro Disney

has also been attracting more than 15 million visitors per

annum.

Similar positive results were reported by the Office du

Tourisme et des Congrès de Paris which recorded a total of

995 events in 2011, compared to 959 in 2010 and 931 in

2009.

Paris has the largest total provision of covered exhibition

space in Europe, with more than 680,000 sq. m. The city’s key

venues are:

Paris Expo in Porte de Versailles (226,000 sq. m.)

Palais des Congrès de Paris (32,000 sq. m.)

CNIT in La Défense (21,000 sq. m.)

Espace Champerret (9,100 sq. m.)

Espace Grande Arche (9,500 sq. m.)

Carrousel du Louvre (7,100 sq. m. downtown)

Le Bourget (80,000 sq. m.)

The Parc des Expositions in Villepinte (206,000 sq. m.) is currently under renovation.

The three leading trade fairs taking place regularly in Paris are

the International Air Show at Le Bourget (odd years), the Auto

Show at Porte de Versailles (even years) and Batimat, a

construction fair in Villepinte (annual).

Trade fair and congress demand in Paris has witnessed a

steady growth since the dip in 2009. According to the

International Congress and Convention Association (ICCA)

the number of events in Paris increased from 147 in 2010 to

174 in 2011. In its global ranking, the ICCA ranked Paris 2nd

place, after Vienna.

Source: ICCA

Paris: International Conference & Exhibition Demand

30

60

90

120

150

180

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Nu

mb

er o

f E

ven

ts

6 Hotel Intelligence: Paris

A well balanced hotel mix from

budget to luxury

Record number of passengers at

Paris airports in 2012

The French capital benefits from excellent accessibility, both

nationally and internationally. Paris is at the heart of the

railway network, including the national high-speed trains

(TGV), as well as the international Thalys to Belgium/

Germany/Netherlands and the Eurostar to the UK. The city

also hosts the leading international airport in France.

Paris is served by two main airports, Roissy Charles de Gaulle

(CDG) and Orly. In terms of passenger numbers, Roissy CDG

was the second largest airport in Europe in 2011 with close to

61 million passengers, while Orly ranked eleventh with over

27 million passengers. Both airports benefit from their

proximity to Paris, being less than 25 kilometres from the city;

however, they suffer from poor public transport connections to

Paris. An additional express train from Gare de l’Est in Paris

to Roissy CDG is planned in order to improve the connection,

but it is still in the planning stage and no year of opening has

yet been announced.

While Roissy CDG has room for growth, traffic is limited at

Orly due to flight volume restrictions. Orly is also more

focused on domestic and European flights and short- to

medium-haul flights than Roissy CDG, which is the hub for

international long-haul flights.

Passenger volumes at both airports remained almost static in

2012, with a +0.9% increase compared to 2011. This was

mostly driven by international visitors (+1.6%) while domestic

arrivals decreased by −1.9%. This slight growth followed a

notable +5.7% increase in 2011, leading to a volume slightly

above the 2008 peak.

As at January 2013, the graded hotel supply in Paris

comprised 1,475 hotels with a total of 78,382 rooms. The

market is well balanced in terms of room supply with 33% in

the upscale segment, 38% in the midscale segment, and 28%

in the budget/economy category. The most luxurious hotels

are located in the 1st, 8th, 9th and 16th districts of Paris, with

the Right Bank home to the majority of these hotels. The Left

Bank is mainly composed of boutique hotels and/or small

independent properties.

Sources: ADP; Jones Lang LaSalle

Paris Airports: Passenger Arrivals

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Pas

sen

ger

s ('0

00s)

Domestic International

The 5-star category was created in early 2009 as part of a

new star classification system. The creation of this new

category has not brought major changes to the hotel sector,

but has clarified classification for international travellers. A

‘Palace’ label was introduced in 2010 and today encompasses

five hotels in Paris out of a total of twelve in France.

The most significant openings in 2011 and 2012 were the

Mandarin Oriental and the W Opera, following the Shangri-La

and Royal Monceau, both in 2010.

Paris: Graded Hotel Supply (as at January 2013)

Grade Establishments Rooms % Share

4 & 5 Star 259 26,149 33.4%

3 star 627 30,113 38.4%

Other 589 22,120 28.2%

Total 1,475 78,382

Source: Insee, Jones Lang Lasalle

Hotel Intelligence: Paris 7

Limited new supply due to high barriers to entry

Paris remains a highly attractive city for hotel operators seeking

flagship properties in continental Europe. However, developing

a new hotel is not the easiest way to enter the Parisian market

due to the lack of available sites, high development costs and

the fact that there are relatively few hotels for sale on the

market. Consequently, graded hotel room supply in the French

capital grew at a very slow rate, showing a cumulated annual

average growth (CAAG) rate of only 0.3% between 2002 and

2012. The market therefore faces little oversupply risk which

has boosted prices for hotel acquisitions to peak levels.

New supply that has recently entered the Parisian hotel market

has generally been positioned in the luxury segment, often

considered as Palace hotels (average daily rate above €700).

Hotel development in Paris is expected to remain moderate

with 869 rooms planned for 2013 and about 1,500 rooms in

the pipeline for 2014, reflecting yearly growth rates of 1.1%

and 2.4% respectively. Nonetheless, the Palace segment is

expected to become more competitive in the medium term

with the opening and re-opening of another five properties by

2016. The budget segment is also set to increase and will

continue to grow at the ‘Portes de Paris’ (on the ring-road) and

in the inner suburbs.

Key development highlights will include the Mélia La Défense

that is expected to open in 2014. This hotel will be located in

the business district of La Défense and will offer 369 rooms.

Another notable opening will be the Peninsula in 2014, the

second largest Palace hotel in the city after the Four Seasons

George V. In 2016, LVMH is also planning to open the 100

room The Cheval Blanc. This new hotel will complete the

LVMH collection, following new hotels in Courchevel and the

Maldives in 2013 and Oman and Egypt in 2015.

Furthermore, the iconic Ritz and Hotel de Crillon Palace hotels

are closing for approximately 2 years to undergo a multi-

million-euro transformation. The Plaza Athénée and the

Shangri-La are also planned to be extended.

New brands entering the Parisian hotel market include: AC

Hotel by Marriott at Porte des Ternes (close to the Palais des

Congrès) in 2014, and Motel One at Porte Dorée (East) in

2015. At Charles de Gaulle airport, CitizenM and Garden Inn/

Hampton Inn will also be launched on to the French market.

f = forecast Source: Jones Lang LaSalle

65,000

70,000

75,000

80,000

85,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013f 2014f

To

tal R

oo

ms

Developments Existing

Paris: Graded Hotel Supply

8 Hotel Intelligence: Paris

Paris: Hotel developments (as at March 2013)

Hotel Location Rooms Grade Due Date Operator

RECENTLY OPENED 2011 & 2012

Courtyard Paris Arcueil Arcueil 170 3 Feb-11 Marriott

Mandarin Oriental 1st arrondissement 150 5 June-11 Mandarin Oriental

Holiday Inn Grand Boulevard 9th arrondissement 118 3 June-11 InterContinental Hotel Group

Suite Novotel Issy les Moulineaux 128 4 Dec-11 Accor

Hôtel Crayon 1st arrondissement 27 4 2011 Independant

W Opéra 9th arrondissement 80 4 Feb-12 Starwood Hotels & Resorts

Courtyard Marriott Boulogne Boulogne Billancourt 115 3 March-12 Marriott

Total Rooms 2011 & 2012 673

NEW DEVELOPMENTS 2013

PROPOSED

Shangri-La, extension 16th arrondissement 20 5 2013 Shangri-La

Buddha Bar Hôtel 8th arrondissement 65 5 2013 Buddha Bar

123 Sébastopol 10th arrondissement 65 4 2013 Astotel

Porte de Vanves 14th arrondissement 96 4 2013 Boissée Finance

MGallery Piscine Molitor 16th arrondissement 124 4 2013 Accor

Courtyard Porte de la Villette 19th arrondissement 297 3 2013 Marriott

B&B Porte de la Villette 19th arrondissement 202 2 2013 B&B

Total Rooms Proposed 869

NEW DEVELOPMENTS 2014 <

PROPOSED

Hôtel Zadig & Voltaire 7th arrondissement 40 5 2014 Thierry Gillier

Plaza Athénée, extension 8th arrondissement 25 5 2014 Dorchester Collection

The Peninsula Paris 16th arrondissement 200 5 2014 Peninsula

AC by Marriott Porte Maillot 17th arrondissement 166 4 2014 Marriott

Renaissance Malmaison Rueil Malmaison 80 4 2014 Marriott

Renaissance Paris Saint-Cloud Saint-Cloud 113 4 2014 Marriott

Marriott Courtyard Le Bourget Le Bourget 120 4 2014 Marriott

Mélia La Défense La Défense 343 4 2014 Mélia

Projet Boulevard d'Indochine 19th arrondissement 149 3 2014 Kyriad Design by Enzo

Hilton Garden Inn Roissy-Charles de Gaulle n/a 3 2014 Hitlon Worldwide

B&B Porte des Lilas 20th arrondissement 265 2 2014 B&B

Hampton by Hilton Roissy-Charles de Gaulle n/a 2 2014 Hilton Worldwide

Porte Dorée 12th arrondissement n/a n/a 2014 Mairie de Paris

Porte de Vincennes 12th arrondissement n/a n/a 2014 Mairie de Paris

Porte de Choisy Project 13th arrondissement n/a n/a 2014 Mairie de Paris

Mélia Roissy Roissy-Charles de Gaulle 369 5 2015 Mélia

Projet Austerlitz Sud 13th arrondissement n/a 4 2015 n/a

Projet Duo (B3A) 13th arrondissement 237 4 2015 n/a

Pullman Porte de Ternes 17th arrondissement 150 4 2015 Accor

Suite Novotel Porte de Vanves 14th arrondissement 96 3 2015 Accor

Motel One Porte Dorée 12th arrondissement 300 2 2015 Motel One

Paris Rive Gauche Rehabilitation 13th arrondissement 170 n/a 2015 Mairie de Paris

Le Cheval Blanc (La Samaritaine) 1st arrondissement 100 5 2016 LVMH

Poste du Louvre 1st arrondissement 80 4 2016 n/a

Projet Gare Austerlitz 13th arrondissement n/a 2/3 2016 n/a

Tour Hermitage La Défense n/a 5 2017 n/a

Zenit Hôtel 2nd arrondissement n/a 4 TBC Zenit Hôteles

Hôtel Rivié 2nd arrondissement 100 4 TBC n/a

Total Rooms Proposed 3,103

Source: Jones Lang LaSalle

Hotel Intelligence: Paris 9

Paris has historically been one of the most successful hotel

markets in Europe. Although relatively resilient to domestic

shocks, the destination is still affected by worldwide

geopolitical, economic and financial crises, leading to

temporary decreases in RevPAR. Nevertheless, over the past

6 years, Paris has proven its capability to rebound quickly

from these temporary declines and posted impressive

RevPAR growth rates in comparison to other European

gateway markets.

The resilience of the Paris hotel market could also be seen in

2012 when hoteliers posted another record year in terms of

trading performance. RevPAR improved by 8.1% year on year

to a new peak of €202 at the end of 2012. Due to stable

demand, hoteliers were able to increase their average room

rates by 8% with occupancy remaining close to 80%.

One of the reasons for Paris solid market fundamentals are its

tight supply conditions with a limited number of land plots

available for development. This has encouraged hoteliers to

increase room rates which have increased by a CAAG rate of

4.1% between 2005 and 2012.

Despite the on-going uncertainty in Europe and the economic

challenges in France, trading performance results in Paris

remained positive in the first three months of 2013. RevPAR

at YTD March 2013 improved by 4.5% due to a 0.8% increase

in occupancy and a 3.8% appreciation in average room rates.

Three consecutive years of record trading performance

Paris: Hotel Trading Performance

0%

20%

40%

60%

80%

100%

100

150

200

250

300

2005 2006 2007 2008 2009 2010 2011 2012

Occ

up

ancy

€(2

012

valu

es)

ADR 2012 values (€) RevPAR 2012 values (€) Occupancy

Source: STR Global, December 2012

Paris: YTD March 2013

2012 2013 Change

Occupancy 69.9% 70.4% 0.8%

ADR(€) 226.38 234.87 3.8%

RevPAR (€) 158.14 165.31 4.5%

Source: STR Global

2004 2005 2006 2007 2008 2009 2010 2011 2012

Occupancy 67.6% 70.5% 74.6% 78.9% 78.7% 74.9% 77.7% 79.0% 78.9%

ARR (€) 148.85 193.24 205.80 204.15 214.36 197.42 210.65 237.04 256.58

RevPAR (€) 100.59 136.16 153.57 161.17 168.73 147.78 163.68 187.26 202.44

RevPAR Growth (%) 4.9% 35.4% 12.8% 5.0% 4.7% -12.4% 10.8% 14.4% 8.1%

Inflation 2.1% 1.7% 1.7% 1.5% 2.8% 0.1% 1.50% 2.1% 1.3%

ADR 2012 values (€) 160.83 215 226 221 225 207 218 240 257

RevPAR 2012 values (€) 108.69 152 168 174 177 155 169 190 202

Source: STR Global, Global Insight

10 Hotel Intelligence: Paris

Over the past 4–8 years, average occupancy has remained

high at around 77–78%. Stable growth in ADR was also

witnessed in both periods fluctuating between 2.5–3.3%.

RevPAR grew at about twice the rate of inflation over the past 4

-8 years.

Due to the city’s well-balanced business mix, hotels in Paris

register moderate seasonality, which results in high year-round

trading performance. Peak seasons correspond to spring and

autumn months, driven by the combination of corporate

clientele, trade fair and congress activity, and tourist demand.

The impact of the leading trade fairs and congresses is

significant (see the following graph), with performance peaking

in June during the Air Show, and October during the Auto Show.

This high level of seasonality tends to cap any major increase in

occupancy.

RevPAR is expected to improve slightly in 2013, although at a

slower pace than in 2011 and 2012 due to weak economic

prospects. Occupancy is likely to plateau, whereas ADR

growth is expected to remain above inflation. This will be

supported by a limited supply growth.

The outlook for hotel performance in the medium to long term

is likely to remain promising, with hotels expected to benefit

from an improvement in economic conditions and a further

strengthening in foreign travel, particularly from Brazil, Russia

and China. The recent and future opening of several luxury

Asian brands should increase the volume of Asian clientele.

The gradual moving of Ramadan to earlier in the year will also

mean that the traditional peak demand from Middle Eastern

guests will be more easily accommodated.

With a continuing growth in RevPAR, and limited future

supply, investor interest is expected to remain very strong.

This will be reinforced by the reputation of Paris as a safe

haven for investors and by the long-term strength of hotels

operating in the city.

Positive trading expectations for

2013

Paris Trading Growth Rates

2005-2012 2008-2012

Average Occupancy 76.7% 77.8%

ARR CAAG 2.5% 3.3%

RevPAR CAAG 4.2% 3.4%

Source: STR Global

Source: STR Global

Paris: RevPAR Seasonality

50

100

150

200

250

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

€

2010 2011 2012

Hotel Intelligence: Paris

This report is confidential to the recipient of the report. No reference to the report or any part of it may be published in any document, state-ment or circular or in any communication with third parties without the prior written consent of Jones Lang LaSalle, including specifically in relation to the form and context in which it will appear. We stress that forecasting is a problematical exercise which at best should be regarded as an indicative assessment of possibilities rather than absolute certainties. The process of making forward projections involves assumptions in respect of a considerable number of varia-bles which are acutely sensitive to changing conditions, variations in any one of which may significantly affect the outcome and we draw your attention to this factor. Jones Lang LaSalle makes no representation, warranty, assurance or guarantee with respect to any material with which this report may be issued and this report should not be taken as an endorsement of or recommendation on any participation by any intending investor or any other party in any transaction whatsoever. This report has been produced solely as a general guide and does not constitute advice. Users should not rely on this report and must make their own enquiries to verify and satisfy themselves of all aspects of information set out in the report. We have used and relied upon information from sources generally regarded as authoritative and reputable, but the information obtained from these sources may not have been independently verified by Jones Lang LaSalle. Whilst the material contained in the report has been prepared in good faith and with due care, no representation or warranty is made in relation to the accuracy, currency, completeness, suitability or otherwise of the whole or any part of the report. Jones Lang LaSalle Hotels, its officers, employees, subcontractors and agents shall not be liable (to the extent permitted by law) to any person for any loss, liability, damage or expense (‘liability’) arising directly or indirectly from or connected in any way with any use of or reliance on this report. If any liability is established, notwithstanding this exclusion, it shall not exceed $1,000.

12 Hotel Intelligence: Paris

AMERICAS

Atlanta

Buenos Aires

Chicago

Dallas

Denver

Los Angeles

Mexico City

Miami

New York

San Francisco

Sao Paulo

Washington DC

EMEA

Barcelona

Dubai

Dusseldorf

Exeter

Frankfurt

Glasgow

Istanbul

Leeds

London

Madrid

Manchester

Milan

Moscow

Munich

Rome

ASIA

Bangkok

Chengdu

Jakarta

New Delhi

Peking

Shanghai

Singapore

Tokyo

ANZ

Auckland

Brisbane

Melbourne

Perth

Sydney

FRANCE

Lyon

Marseille

Paris

Our domestic & global reach

Hotels & Hospitality

Yves Marchal MD Southern Europe + 33 1 40 55 17 18 [email protected]

Gwenola Donet Director France +33 1 40 55 15 56 [email protected]

Thomas Lamson EVP Mid-Market Transactions +33 1 40 55 15 83 [email protected]

Katell Bourgeois SVP Corporate Transactions +33 1 40 55 15 87 [email protected]

Winoc’h Billette Consultant +33 1 40 55 49 94 [email protected]

Our dedicated local team & expertise:

Paris 40 rue la Boétie 75008 Paris

Lyon 55 avenue Foch 69006 Lyon

Marseille 2 place Sadi-Carnot 13001 Marseille

www.jll.com/hospitality | www.jllhotels.fr

COPYRIGHT © JONES LANG LASALLE IP, INC. 2013