hotel le meridien, new delhi, india august 1st 2014 · hotel le meridien, new delhi, india august...

TRANSCRIPT

Hotel Le Meridien, New Delhi, India August 1st 2014

2nd India International DRI Summit 2014

2

The Role of the Metallics

Industry in Steelmaking

Stuart G Horner Secretary General

International Iron Metallics Association

http://metallics.org.uk

Disclaimer

This presentation is intended for information purposes only and is not intended as commercial material in any respect. The material is not intended as an offer or solicitation for the purposes of sale of any financial instrument, is not intended to provide an investment recommendation and should not be relied upon for such. The material is derived from published sources, together with personal research. No responsibility or liability is accepted for any such information of opinions or for any errors, omissions, misstatements, negligence or otherwise for any further communication, written or otherwise.

4

• International Iron Metallics Association?

• What are Ore Based Metallics?

• Ore Based Metallics Market

• Benefits to steelmakers in using DRI /HBI or Pig

Iron

Topics

IIMA ORIGIN

HBIA (Hot Briquetted Iron Association) IPIA (International Pig Iron Association)

5

PRINCIPAL OBJECTIVES

Provide value for members Sustain & grow membership

PURPOSES

PROMOTE The use of ore-based metallics in steel production and iron casting

REPRESENT The collective interest of members

COLLECT & PRESENT Trade statistics and Industry data

PROVIDE A forum for technical co-operation and exchange of views

7

8 Meeting with AIIS Management - Nov 7,

2011

SPANNING THE SUPPLY CHAIN

Diverse Membership ... Unified Presence

– Producers of DRI, HBI, Iron Nuggets, and Merchant Pig Iron

– Traders/Distributors of metallics

– Suppliers of iron ore, energy/reductants, process technology, proprietary equipment, transportation and logistics services, know-how, etc.

– Individuals whose careers have contributed to furthering the industry

8

9

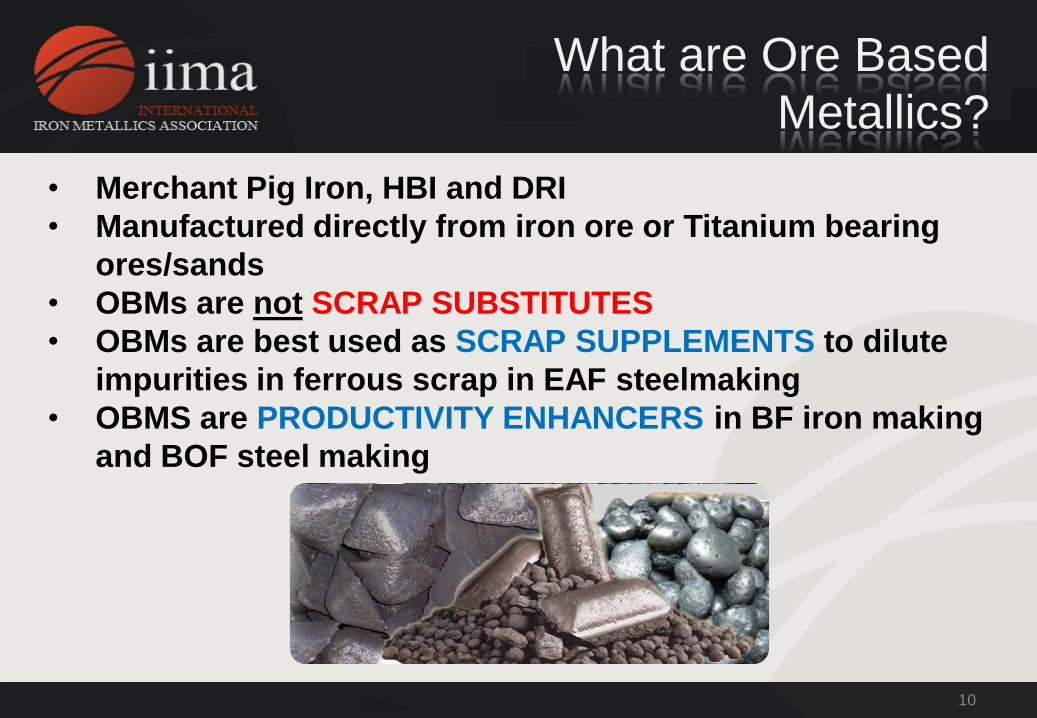

What are Ore Based Metallics?

10

• Merchant Pig Iron, HBI and DRI

• Manufactured directly from iron ore or Titanium bearing

ores/sands

• OBMs are not SCRAP SUBSTITUTES

• OBMs are best used as SCRAP SUPPLEMENTS to dilute

impurities in ferrous scrap in EAF steelmaking

• OBMS are PRODUCTIVITY ENHANCERS in BF iron making

and BOF steel making

What are Ore Based

Metallics?

11

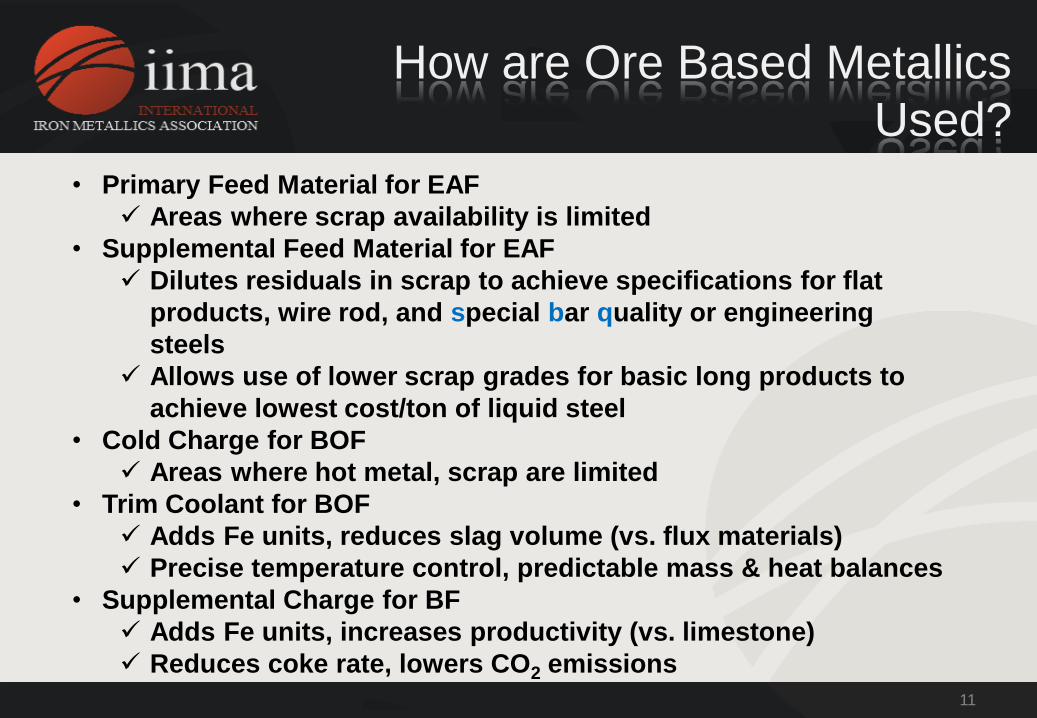

• Primary Feed Material for EAF

Areas where scrap availability is limited

• Supplemental Feed Material for EAF

Dilutes residuals in scrap to achieve specifications for flat

products, wire rod, and special bar quality or engineering

steels

Allows use of lower scrap grades for basic long products to

achieve lowest cost/ton of liquid steel

• Cold Charge for BOF

Areas where hot metal, scrap are limited

• Trim Coolant for BOF

Adds Fe units, reduces slag volume (vs. flux materials)

Precise temperature control, predictable mass & heat balances

• Supplemental Charge for BF

Adds Fe units, increases productivity (vs. limestone)

Reduces coke rate, lowers CO2 emissions

How are Ore Based Metallics

Used?

12

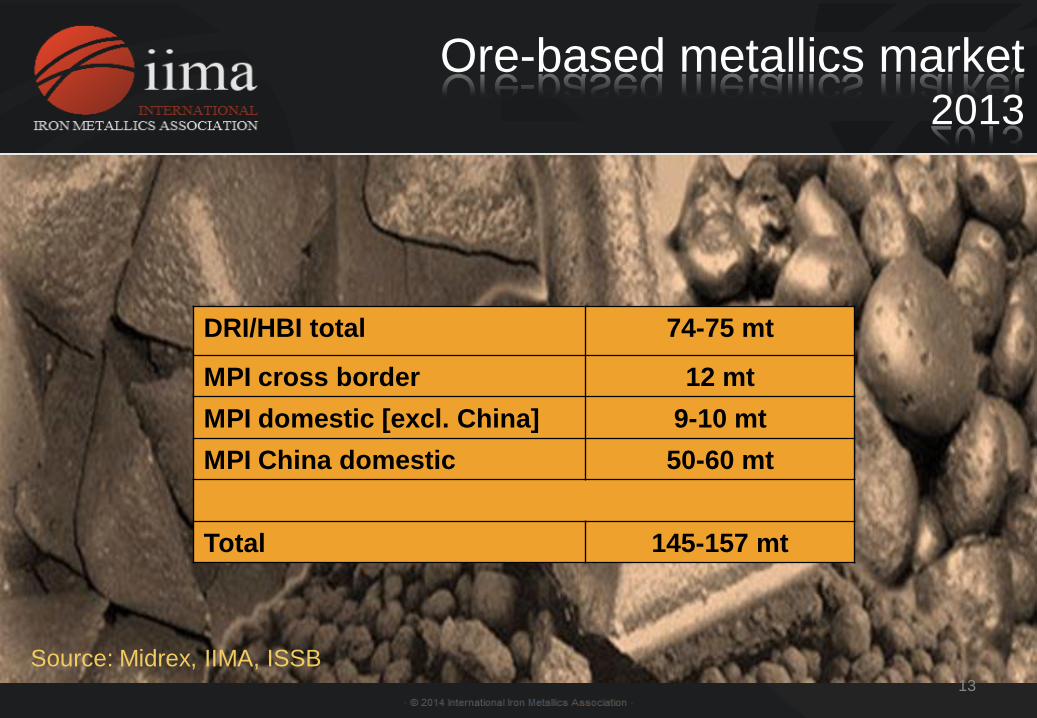

Ore Based Metallics Market

Ore-based metallics market 2013

13

DRI/HBI total 74-75 mt

MPI cross border 12 mt

MPI domestic [excl. China] 9-10 mt

MPI China domestic 50-60 mt

Total 145-157 mt

Source: Midrex, IIMA, ISSB

14

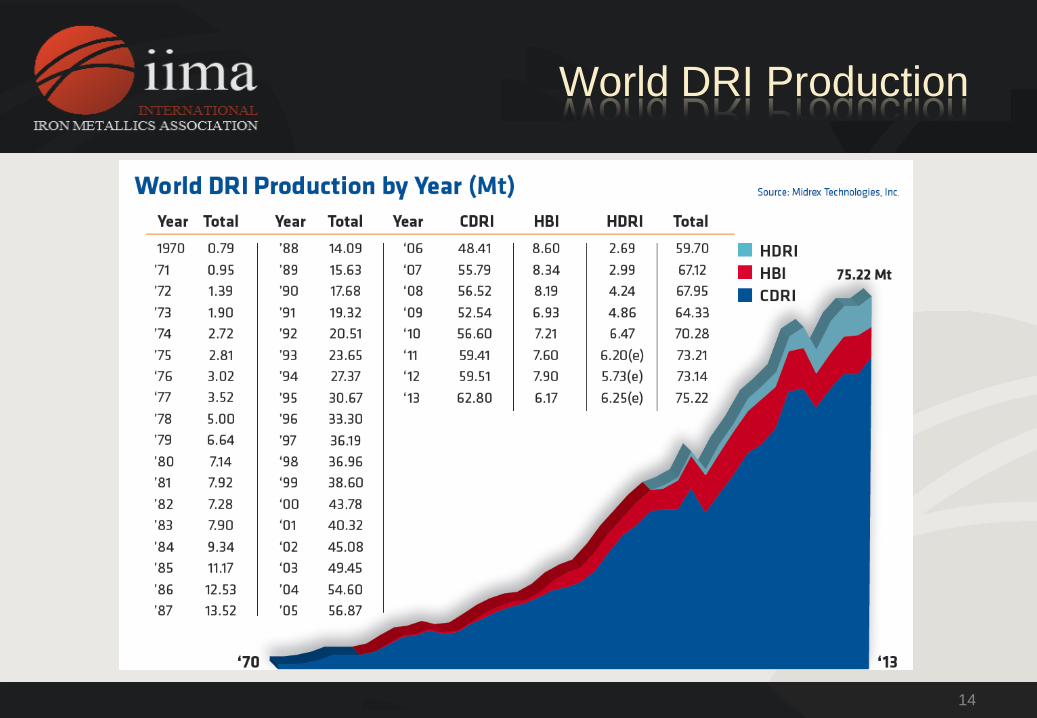

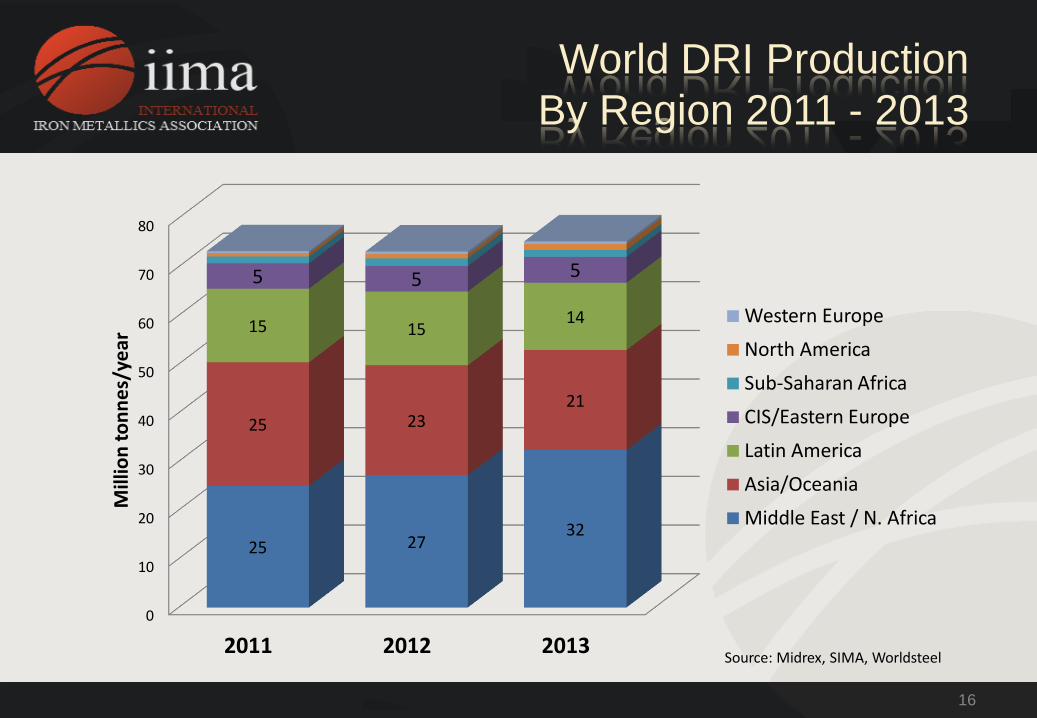

World DRI Production

15

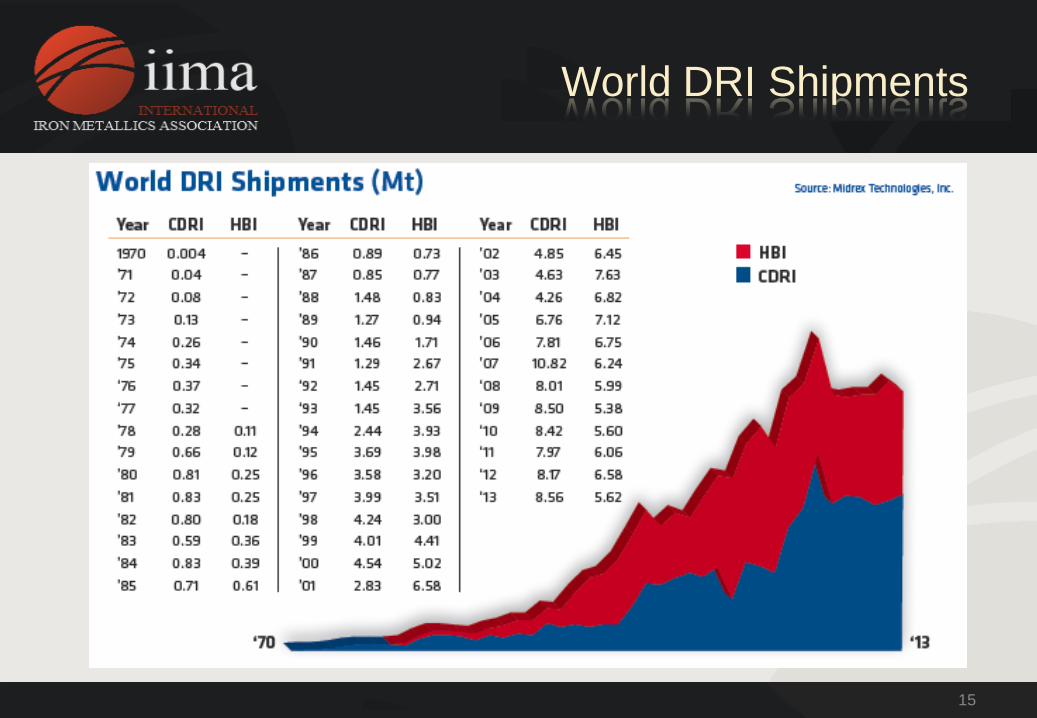

World DRI Shipments

16

0

10

20

30

40

50

60

70

80

2011 2012 2013

25 27 32

25 23 21

15 15 14

5 5 5

Mill

ion

to

nn

es/

year

Western Europe

North America

Sub-Saharan Africa

CIS/Eastern Europe

Latin America

Asia/Oceania

Middle East / N. Africa

Source: Midrex, SIMA, Worldsteel

World DRI Production

By Region 2011 - 2013

17

Libya

1.75 mill t

Russia

2.3 mill t

Qatar

1.5 mill t

Trinidad & Tobago

3.6 mill t

Venezuela

6.9 mill t

India

1.5 mill t

Malaysia

2.44 mill t

Libya

1.75 mill t

Russia

2.3 mill t

Qatar

1.5 mill t

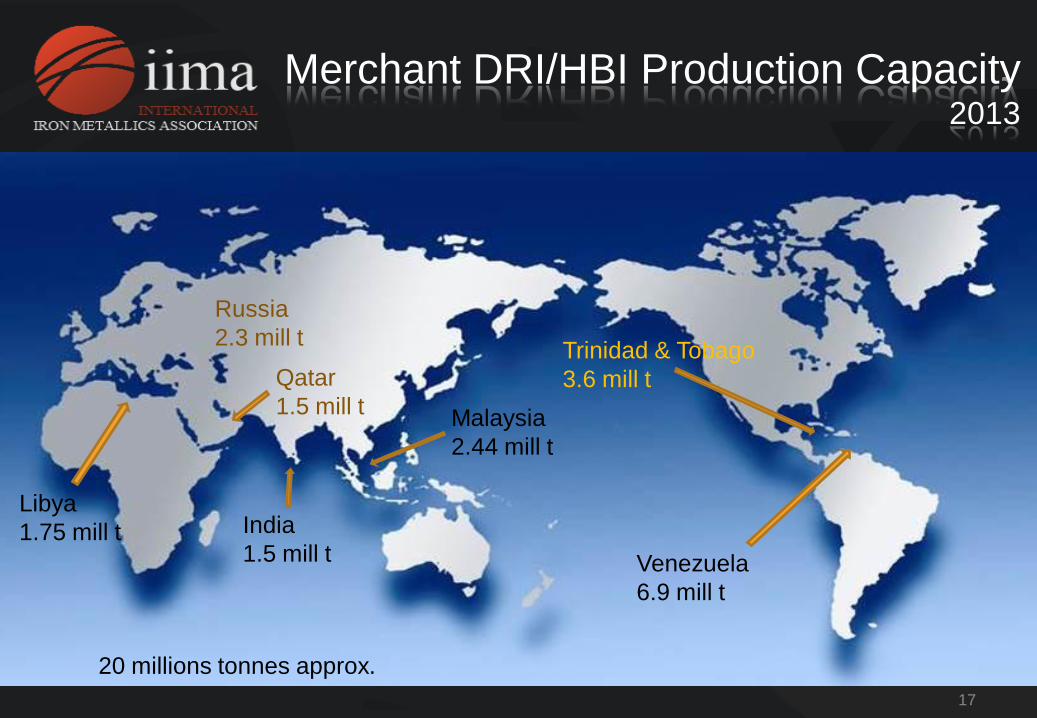

Merchant DRI/HBI Production Capacity 2013

20 millions tonnes approx.

18

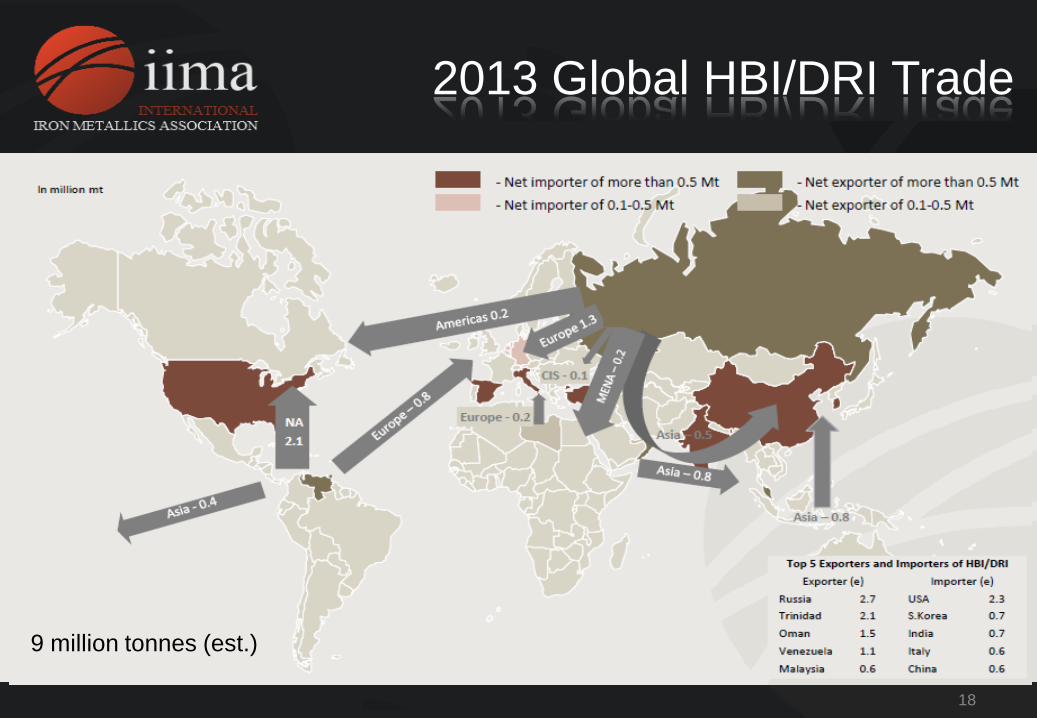

2013 Global HBI/DRI Trade

9 million tonnes est. 9 million tonnes (est.)

19

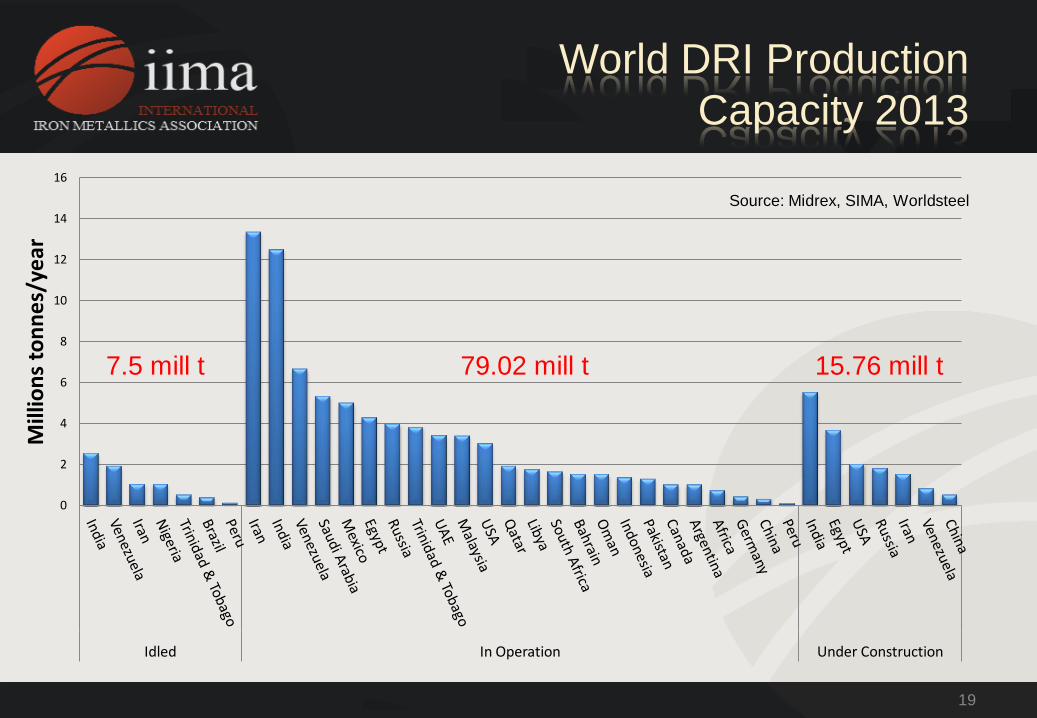

0

2

4

6

8

10

12

14

16

Idled In Operation Under Construction

Mill

ion

s to

nn

es/

year

79.02 mill t 15.76 mill t

World DRI Production

Capacity 2013

7.5 mill t

Source: Midrex, SIMA, Worldsteel

20

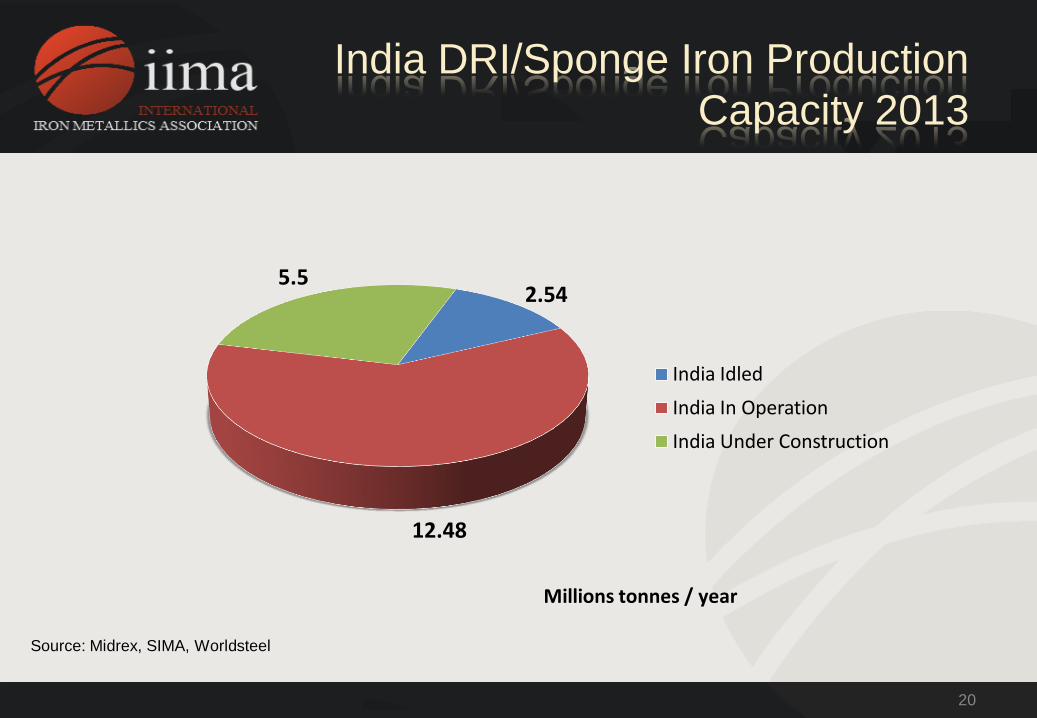

2.54

12.48

5.5

India Idled

India In Operation

India Under Construction

Millions tonnes / year

India DRI/Sponge Iron Production

Capacity 2013

Source: Midrex, SIMA, Worldsteel

21

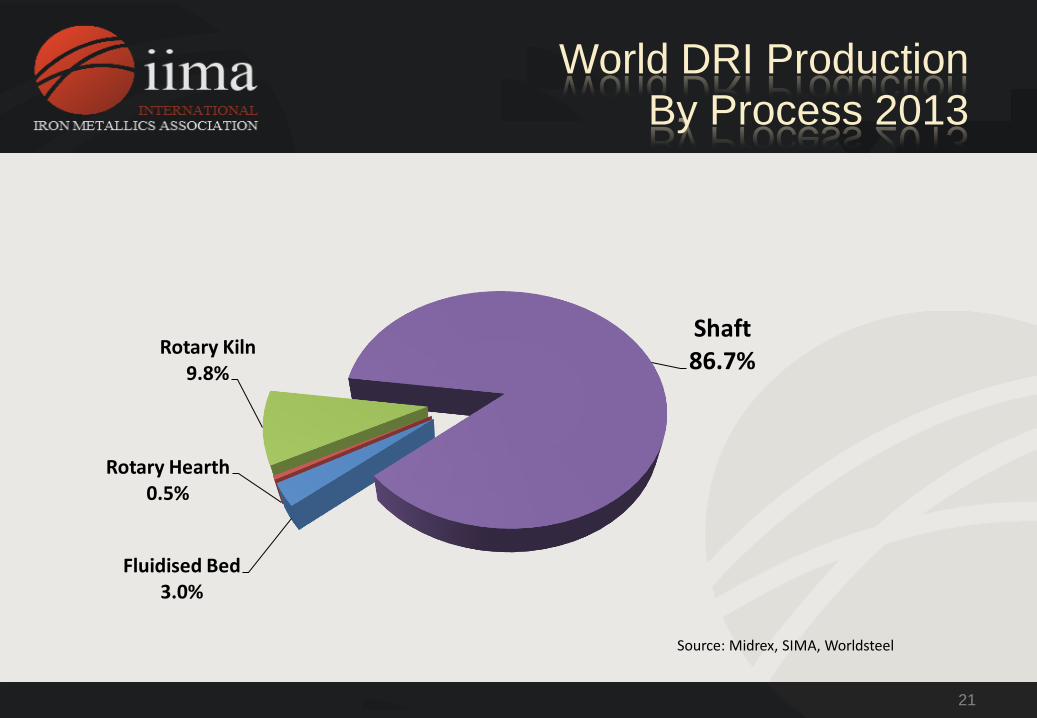

Fluidised Bed 3.0%

Rotary Hearth 0.5%

Rotary Kiln 9.8%

Shaft 86.7%

Source: Midrex, SIMA, Worldsteel

World DRI Production

By Process 2013

22

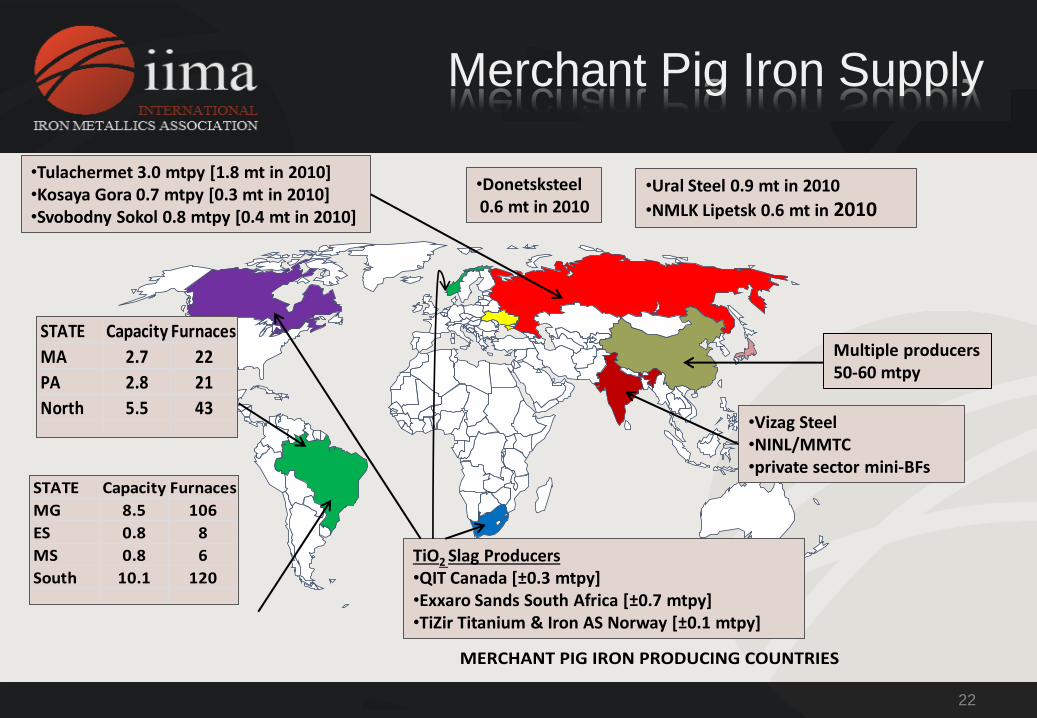

•Donetsksteel 0.6 mt in 2010

STATE Capacity Furnaces

MG 8.5 106

ES 0.8 8

MS 0.8 6

South 10.1 120

STATE Capacity Furnaces

MA 2.7 22

PA 2.8 21

North 5.5 43

•Ural Steel 0.9 mt in 2010

•NMLK Lipetsk 0.6 mt in 2010

•Tulachermet 3.0 mtpy [1.8 mt in 2010] •Kosaya Gora 0.7 mtpy [0.3 mt in 2010] •Svobodny Sokol 0.8 mtpy [0.4 mt in 2010]

TiO2 Slag Producers •QIT Canada [±0.3 mtpy] •Exxaro Sands South Africa [±0.7 mtpy] •TiZir Titanium & Iron AS Norway [±0.1 mtpy]

•Vizag Steel •NINL/MMTC •private sector mini-BFs

Multiple producers 50-60 mtpy

Merchant Pig Iron Supply

23

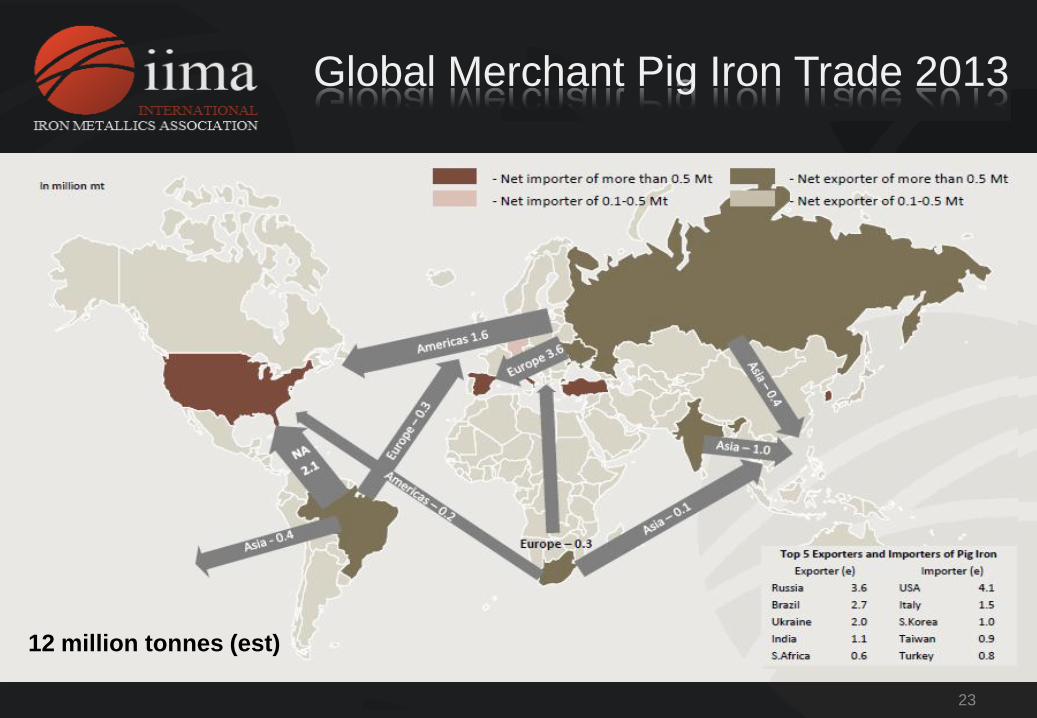

Global Merchant Pig Iron Trade 2013

12 million tonnes (est)

24

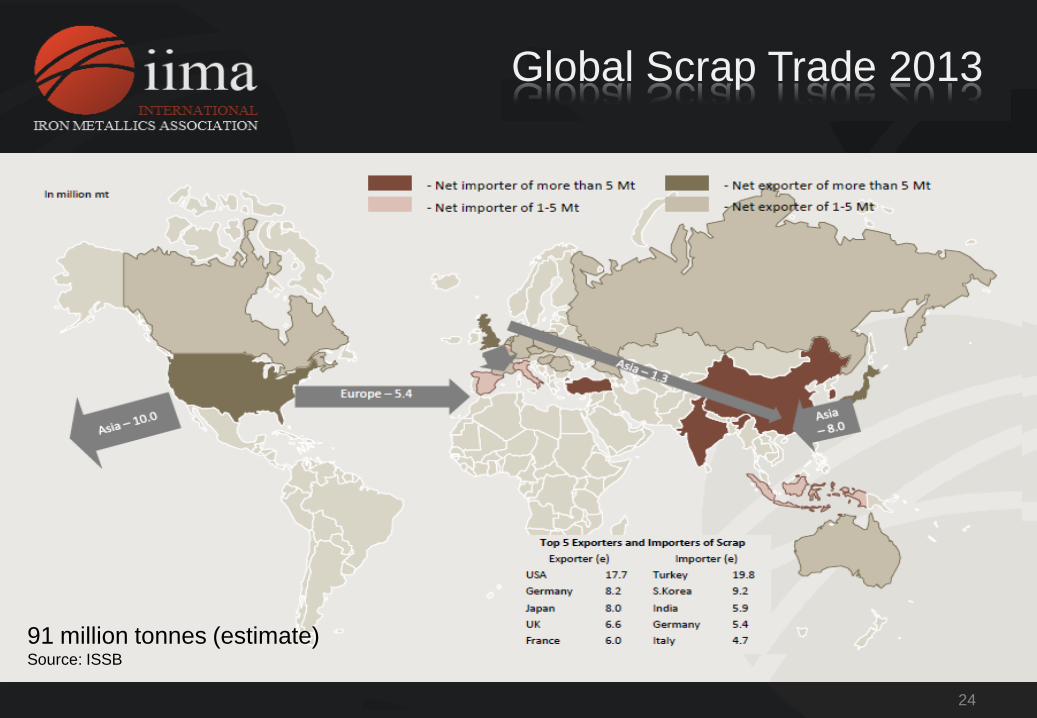

Global Scrap Trade 2013

91 million tonnes (estimate) Source: ISSB

25

Benefits to Steelmakers in

Using DRI /HBI or Pig Iron

26

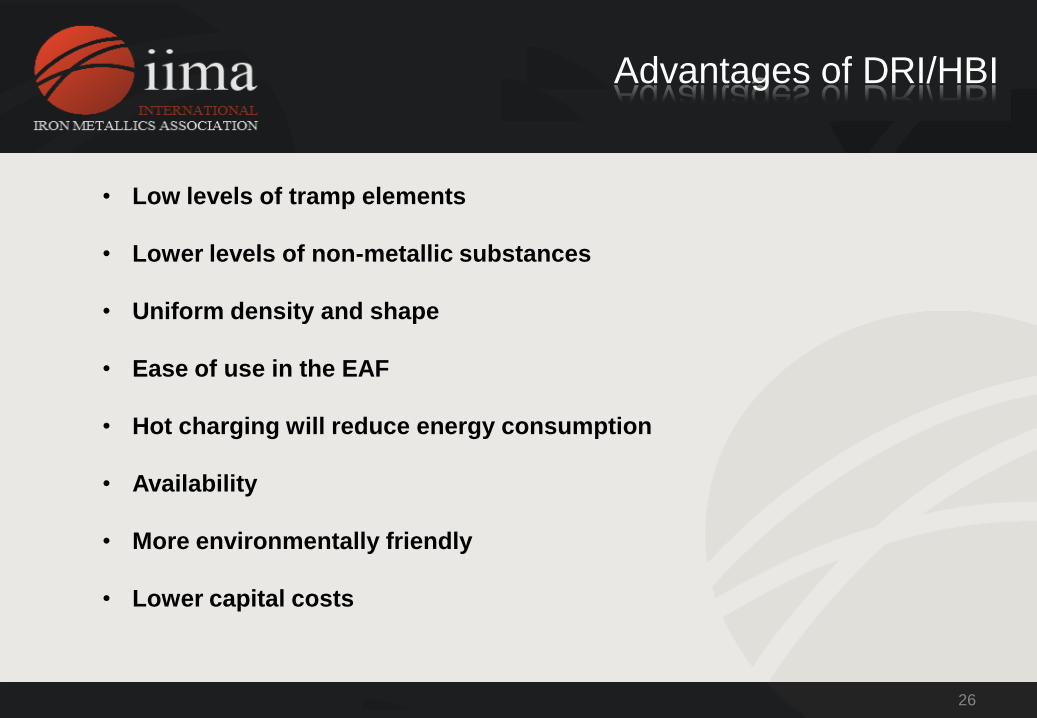

Advantages of DRI/HBI

• Low levels of tramp elements

• Lower levels of non-metallic substances

• Uniform density and shape

• Ease of use in the EAF

• Hot charging will reduce energy consumption

• Availability

• More environmentally friendly

• Lower capital costs

27

Value in Use

28

• Steelmakers use OBM’s, as part of the

metallics charge to electric arc furnaces

(EAF)

• OBM’s contain little or no residual

elements i.e. Cu, Cr, Ti, V, Mo, Sn etc.

• Many steelmakers have calculated a

yielded cost of Fe units as a means to

determine the value-in-use

• OBM suppliers have long held the position

that OBM’s have an intrinsic value but have

struggled to quantify it.

Historical Perspective

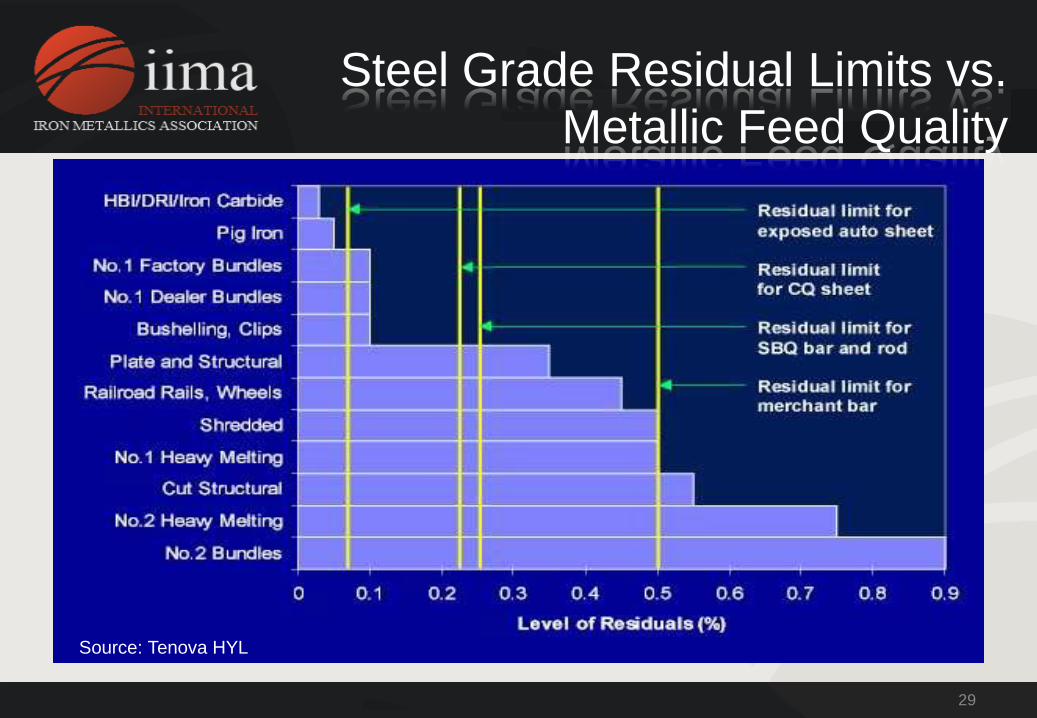

29

Steel Grade Residual Limits vs.

Metallic Feed Quality

Source: Tenova HYL

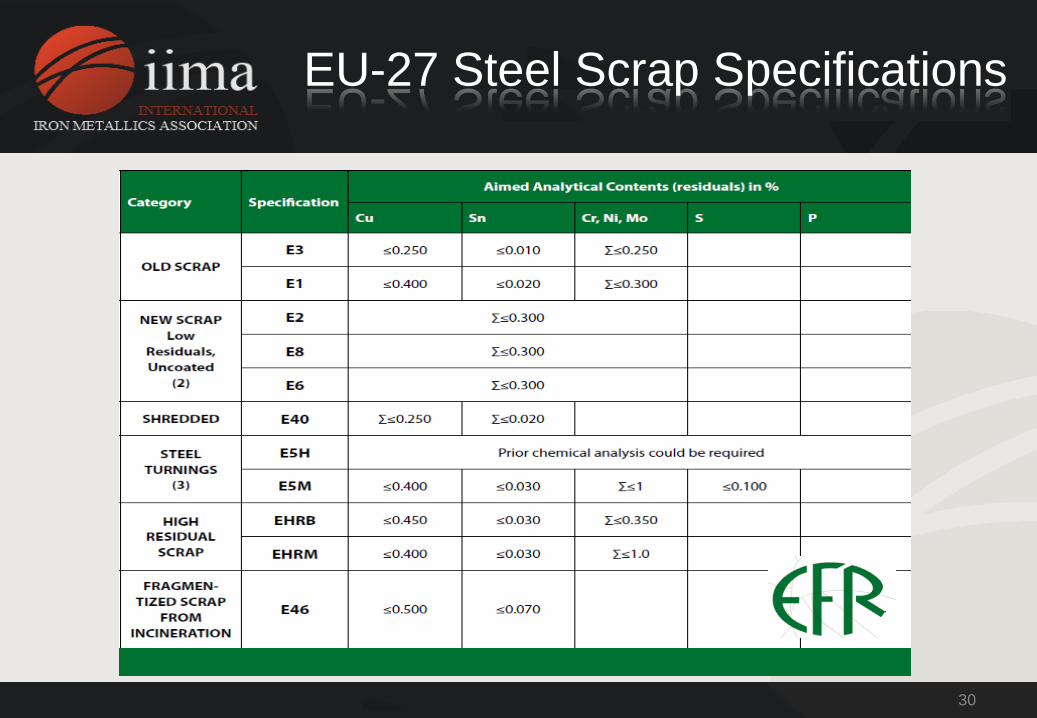

30

EU-27 Steel Scrap Specifications

31

• HBI often sells for less than

prime scrap

• Pig iron usually manages to stay

close to the price of prime scrap

32

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

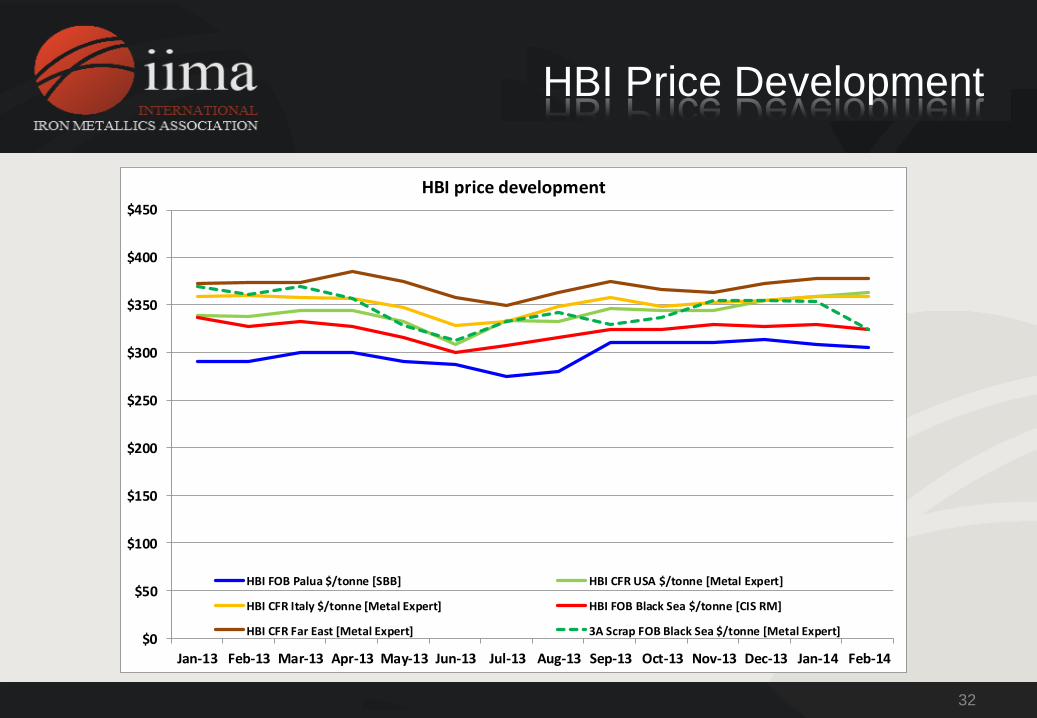

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Jan-14 Feb-14

HBI price development

HBI FOB Palua $/tonne [SBB] HBI CFR USA $/tonne [Metal Expert]

HBI CFR Italy $/tonne [Metal Expert] HBI FOB Black Sea $/tonne [CIS RM]

HBI CFR Far East [Metal Expert] 3A Scrap FOB Black Sea $/tonne [Metal Expert]

HBI Price Development

33

$-

$50

$100

$150

$200

$250

$300

$350

$400

$450

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Jan-14 Feb-14

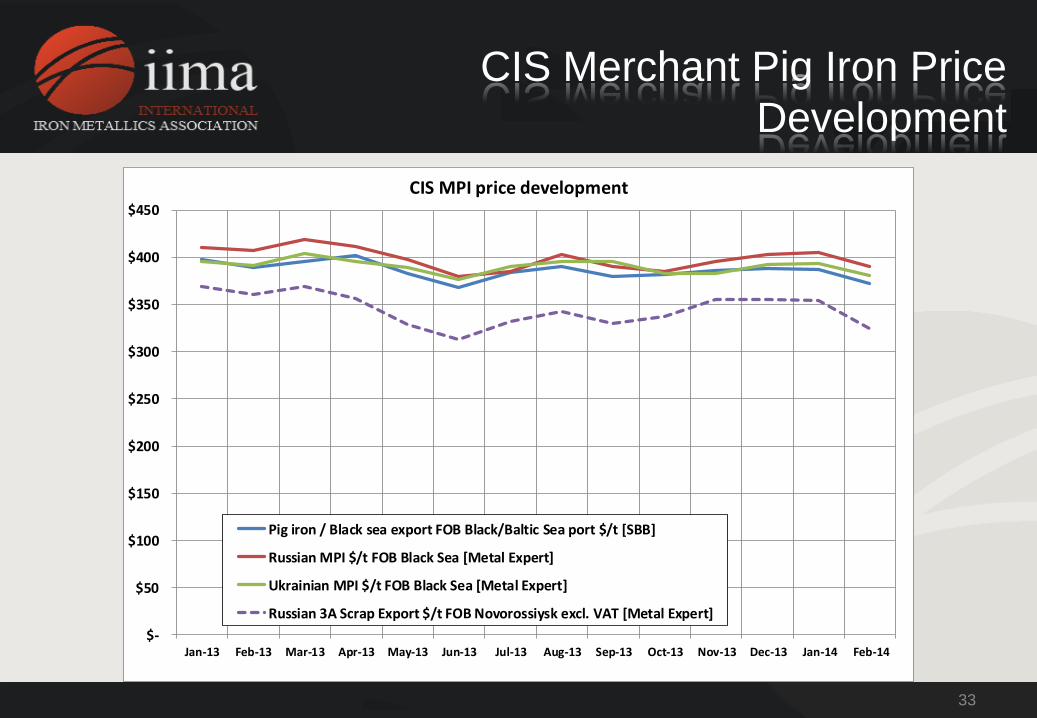

CIS MPI price development

Pig iron / Black sea export FOB Black/Baltic Sea port $/t [SBB]

Russian MPI $/t FOB Black Sea [Metal Expert]

Ukrainian MPI $/t FOB Black Sea [Metal Expert]

Russian 3A Scrap Export $/t FOB Novorossiysk excl. VAT [Metal Expert]

CIS Merchant Pig Iron Price

Development

34

• The study showed when comparing similar scrap types that differ in

characteristics only with respect to residual content, the inherent cost

of a point (0.01 weight %) of copper in the scrap has been determined

to be approximately $2.00.

• Considerable savings can be accrued by replacing low Cu high grade

scrap with a blend of higher Cu content low grade scrap and OBM’s.

• The range of savings for the HBI case was ($43) to $331/tonne

over the 10 year period evaluated.

• The range of savings for the pig iron case was ($29) to

$439/tonne over the 10 year period.

Value in Use Study

35

The Future

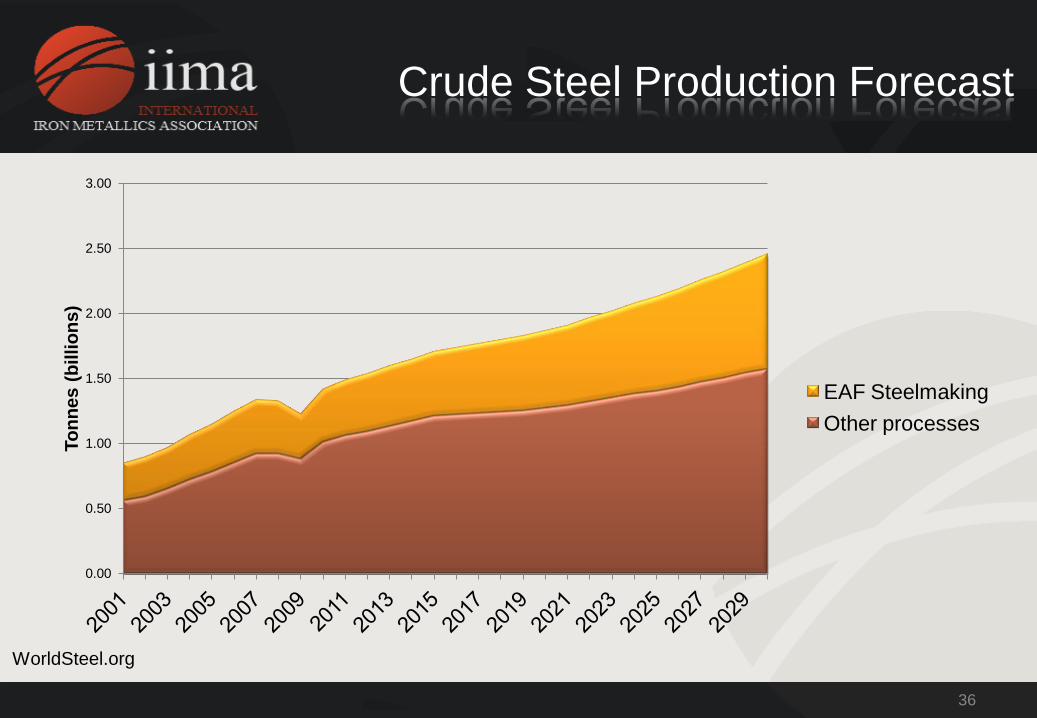

36

Crude Steel Production Forecast

0.00

0.50

1.00

1.50

2.00

2.50

3.00

To

nn

es (

billio

ns)

EAF Steelmaking

Other processes

WorldSteel.org

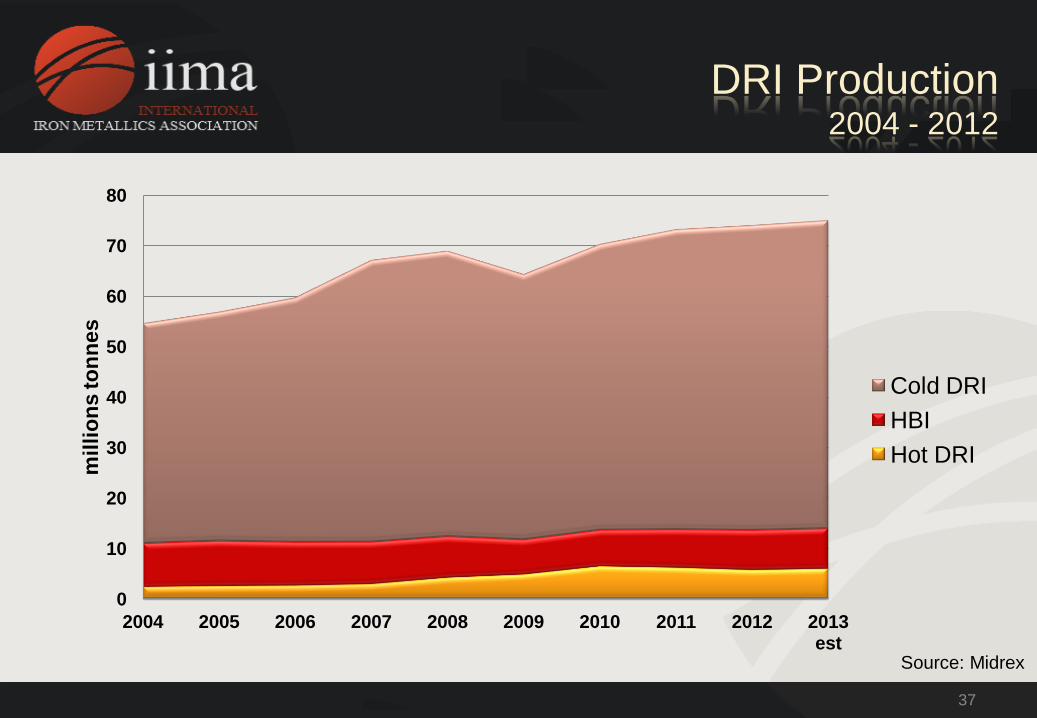

37

DRI Production

2004 - 2012

Source: Midrex

0

10

20

30

40

50

60

70

80

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 est

mil

lio

ns

to

nn

es

Cold DRI

HBI

Hot DRI

38

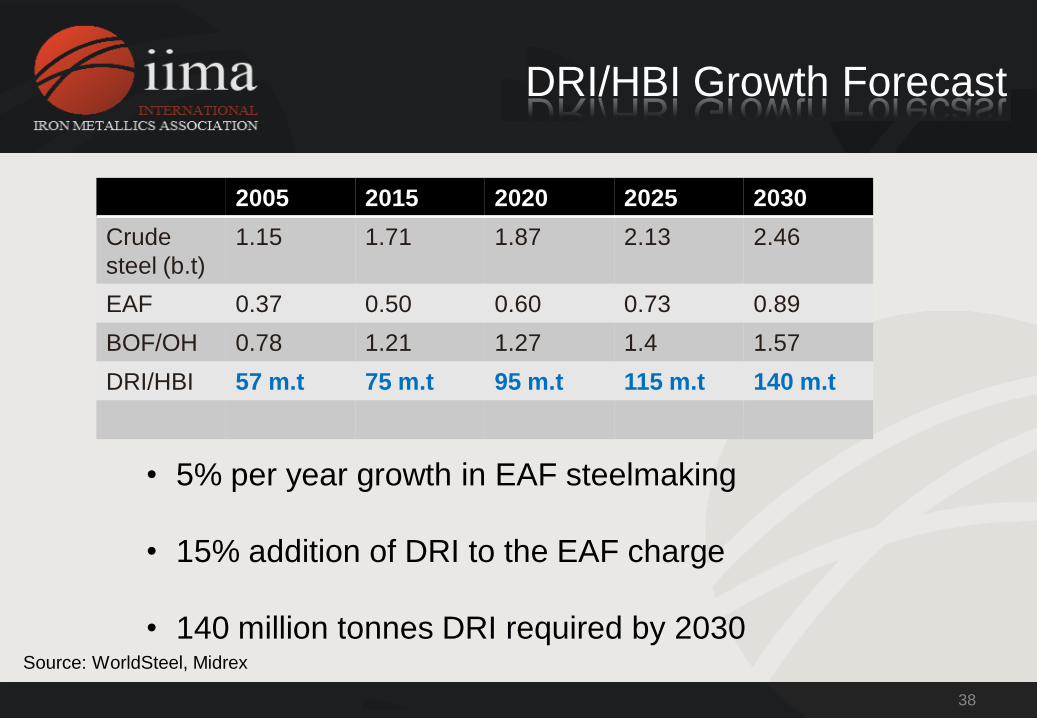

2005 2015 2020 2025 2030

Crude

steel (b.t)

1.15 1.71 1.87 2.13 2.46

EAF 0.37 0.50 0.60 0.73 0.89

BOF/OH 0.78 1.21 1.27 1.4 1.57

DRI/HBI 57 m.t 75 m.t 95 m.t 115 m.t 140 m.t

• 5% per year growth in EAF steelmaking

• 15% addition of DRI to the EAF charge

• 140 million tonnes DRI required by 2030

DRI/HBI Growth Forecast

Source: WorldSteel, Midrex

39

• OBM’s give steelmakers: • Flexibility

• Enhanced productivity

• Consistency

• Value for money

• Quality

Summary

40

THANK YOU

Ask us for Membership Details

or visit our website:

http://metallics.org.uk