hosted by - files.irishfunds.ie · • delegation by fund management companies does not reduce a...

TRANSCRIPT

22 irishfunds.ie

HOSTED BY

33 irishfunds.ie

Six Financial

Robert Jeanbart

Welcome Address

44 irishfunds.ie

Minister of State for Financial Services and Insurance

Michael D’Arcy

Irish Government Address

55 irishfunds.ie

Irish Funds

Kieran Fox

Overview of Irish Funds Industry

66 irishfunds.ie

Total Assets Under Administration – Split between Irish

& Non Irish Funds

434 584 728 807 646 748964 1,055 759 1,344

1,6641,899 2,085 2,231

636838

965

1,394 1,398 1,443

1,883 1,886

2,199

2,722

3,375

3,806

4,0954,251

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 June-17

EU

R

Billi

on

Total Assets Under Administration

Net Assets Domiciled Net Assets Non Domiciled

77 irishfunds.ie

Irish Domiciled Assets

• UCITS represent 75% of Irish

Domiciled Assets

• 86 UCITS Man Cos

• 156 AIFMs Registered or Authorised

• 597 AIFMs operating in Ireland on

cross border basis

• 364 ICAVs established (since 18 March

2015)

88 irishfunds.ie

Ireland’s Relationship with European Investment Fund Landscape

• €13 trillion in assets

• €8 trillion UCITS

• €5 trillion Alternative Investment Funds (AIFs)

• €1 trillion of net inflows into UCITS over last 3 years

• €463 billion net inflows into European funds 2016 (>30% of which went to

Irish domiciled funds)

99 irishfunds.ie

Growth of Largest European Fund Domiciles

2012 2013 2014 2015 2016

Europe 113 123 142 158 178

Luxembourg 114 125 148 167 177

Ireland 116 127 157 180 198

France 109 110 114 121 129

Germany 113 124 140 153 166

UK 117 135 159 179 177

-

50

100

150

200

250

% G

row

th116 127

157180

198

Source: EFAMA Statistics

1010 irishfunds.ie

Irish Funds: Passport to Europe & Beyond

UCITS funds & AIFMs benefit from an EU wide

passport and can be sold in any other EEA

member state without need for additional

authorisation

Top 10 countries where Irish Funds

registered for sale

1. UK 6. Austria

2. Germany 7. Luxembourg

3. France 8. Sweden

4. Switzerland 9. Italy

5. Netherlands 10. Spain

Global Distribution of Irish Funds: 70 countries

1111 irishfunds.ie

Irish Funds – Maximising Distribution

1212 irishfunds.ie

Irish Domiciled Funds – Net Sales

-30.0

20.0

70.0

120.0

170.0

Dec-13 Dec-14 Dec-15 Dec-16 YTD July 2017

Net Sales into Irish funds by type € Bn

Equity Funds

Bond Funds

Balanced Funds

Money MarketFunds

AIF

Net sales for

YTD July 2017

have already

surpassed the

total for 2016 (by

>€45bn) – which

itself was a

record year

98,463 85,465

135,668114,706

139,416

185,100

0

50,000

100,000

150,000

200,000

2012 2013 2014 2015 2016 YTD - July2017

EU

R M

n

Net Sales - Total Domiciled Funds

Net Sales - Total Domiciled Funds

1313 irishfunds.ie

ETFs - An Irish Success

Ireland as a

Domicile for

European

ETFs

Total Assets

of European

ETFs - € Bn

Source: Irish Funds,

June 2017

Ireland310

Rest of Europe

248€ bn

56%

44%

€ bn

41

3

Net Sales into All European ETFs 2016 €Bn

Ireland

Rest ofEurope

Bn93%

7%

Bn

1414 irishfunds.ie

Looking Ahead - Technology

1515 irishfunds.ie

Looking Ahead – Brexit

Three interdependent themes

Distribution

Management

Models

(‘Delegation’)

Growth

OVER 2,000 IRISH

FUNDS SOLD TO UK

INVESTORS1

€613 bn2 IN IRISH FUND

ASSETS MANAGED BY

170+ UK FIRMS IN

IRELAND2

Continuity in UK investor

access to EU/Irish funds

Continuity in

UK firm

management

of Irish funds

Increase Ireland’s growth

trajectory as an

international asset

management centre

SOURCE: 1-Lipper IM Dec 2015

2-Monterrey Ireland Fund Report 2016

Current context Target outcome

1616 irishfunds.ie

International asset management centre

Growth

‘The Basics’

•Predictability / efficiency of regulatory process

•12.5% corporate tax rate

•Common law system

•Only English-speaking country in the Eurozone

•Less expensive than Zurich, Paris & Luxembourg1

Asset Manager Activity

Infra-structure

Re-affirm Ireland’s attractiveness as an

international asset management centreOpportunity

Benefits

SolutionProvide UK managers with options to support the

establishment of a physical presence in Ireland

NOTES:

1. Source PwC

2. http://www.iaim.ie/why-ireland (STEM = Science, Technology, Engineering &

Mathematics) & http://www.hea.ie/sites/default/files/awards_-

_all_undergraduate_by_level_and_field.xlsx

3. IFS 2020 Action Plan 2017 (http://finance.gov.ie) & IDA Ireland

4. MiFID firms, UCITS ManCos, Irish AIFMs & Non-Irish AIFMs

• Space for 100K new employees by 2020, 100K new houses3

• Leading global tech centre & fintech location

• London-Dublin: Most flight options in Europe

• 35K+ employed in international financial services in Ireland, 14K in funds industry

• 130K degree-level graduates across business, law and STEM w/ 20K new grads p.a.2

• 800+ investment firms active in Ireland4

• Increased presence of front office activities

• 18 of the top 20 global AMs have Irish funds

• €4trn total AuA, €300bn managed from Ireland2

• AM counterparties already in transit from UK

1717 irishfunds.ie

CP86 Update - Mark Browne, Dechert.

MMF & MMFR developments - Sarah Murphy, PwC.

Ireland as a leading ETF location & CBI ETF Discussion Paper / PE in

Ireland & the new Investment Limited Partnership - Iain Ferguson,

McCann Fitzgerald.

Irish Funds Update talks

1818 irishfunds.ie

Dechert

Mark Browne

CP86

1919 irishfunds.ie

CP 86 Overview

• Review of Fund Governance by Central Bank of Ireland

• Primarily focuses on:

– Delegate oversight

– Organisational Effectiveness

– Directors’ Time Commitments

– Managerial Functions

– Operational Matters

2020 irishfunds.ie

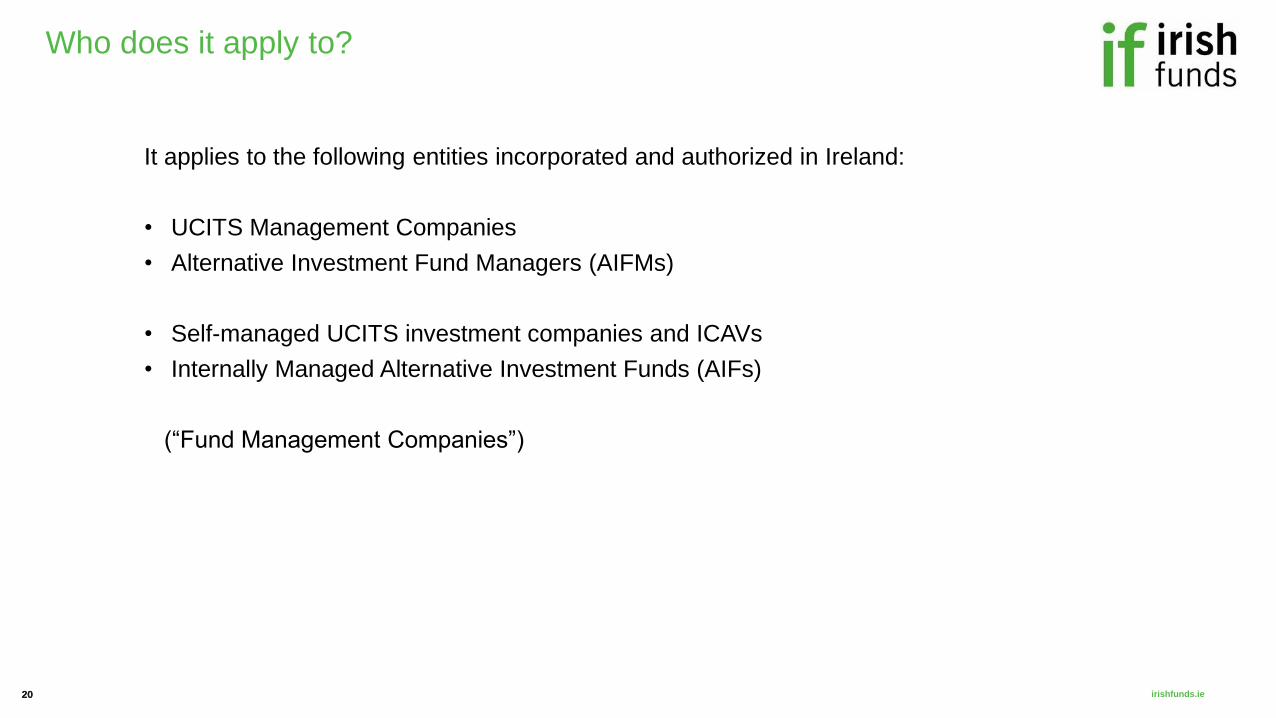

Who does it apply to?

It applies to the following entities incorporated and authorized in Ireland:

• UCITS Management Companies

• Alternative Investment Fund Managers (AIFMs)

• Self-managed UCITS investment companies and ICAVs

• Internally Managed Alternative Investment Funds (AIFs)

(“Fund Management Companies”)

2121 irishfunds.ie

Letterbox Entities and Delegation

• extensive provisions on anti-letterbox tests.

• outsourcing / delegating tasks or functions but NOT responsibilities.

• Delegation by Fund Management Companies does not reduce a board’s ultimate

responsibility.

• Directors must at all times retain and exercise overall control of the relevant company’s

management and supervision of its delegates.

2222 irishfunds.ie

ESMA Principles on Supervisory Approach to Relocations from UK

• Opinion setting out general principles aimed at fostering consistency in:

– authorisation;

– supervision; and

– enforcement

related to the relocation of entities, activities and functions from the United Kingdom.

• Addressed to national competent authorities (NCAs), in particular of the 27 Member

States that will remain in the EU (EU27).

2323 irishfunds.ie

ESMA Principles on Supervisory Approach to Relocations from UK

• “The EU27 have a shared interest in building a common approach to dealing with

relocating firms that wish to continue to benefit from access to EU financial

markets. Firms need to be subject to the same standards of authorisation and

ongoing supervision across the EU27 in order to avoid competition on regulatory

and supervisory practices between Member States. Effective and efficient

supervision are essential to support the Capital Markets Union.” – Steven Maijoor

• View of Central Bank of Ireland

2424 irishfunds.ie

PwC

Sarah Murphy

European Money Market Fund Reform

2525 irishfunds.ie

Agenda

• MMF – size of the market

• Background - where it all started…

• Timeline

• Key points

• Accounting & tax matters

• Current status

2626 irishfunds.ie

MMF – Size of the market

2727 irishfunds.ie

Background – where it all started..

• Financial crisis – noise in the system

• 2011 G20/FSB “strengthen the oversight and regulation of shadow banking system”

• FSB/IOSCO recommendations

• FSOC/SEC/EC

• 2013 – European Commission Proposal

• What did this look like?

2828 irishfunds.ie

Timeline

• Commission proposal 04 September 2013

• Council compromise proposal (1) 10 November 2014

• Council compromise proposal (2) 27 November 2014

• Council compromise proposal (3) 17 December 2014

• Council Italian Presidency progress report 17 December 2014

• Council compromise proposal (4) 12 April 2016

• Council compromise proposal (5) 10 May 2016

• Council compromise proposal (6) 10 June 2016

• Council General Approach 15 June 2016

• European Parliament draft report 04 March 2015

• European Parliament text adopted in plenary vote 29 April 2015

• Political Agreement 14 November 2016

• European Parliament adoption 05 April 2017

• Council endorsement 16 May 2017

• Publication in OJ 30 June 2017

• Entry into force 20 July 2017

2929 irishfunds.ie

Key Points

• The MMF Regulation permits four types of Money Market Funds (“MMF”):

Public debt constant NAV MMFs (“Public Debt CNAV MMFs”)

Low volatility NAV MMFs (“LVNAV MMFs”)

Short-term variable NAV MMFs

Standard variable NAV MMFs

• Some of the main differences between the existing Irish CNAV MMFs and the

two new types of CNAV MMF (LVNAV and Public Debt CNAV):

Eligible Investments

Fund valuation

Liquidity requirement

Fees and gates

3030 irishfunds.ie

Accounting & tax matters

• Cash & cash equivalents – no change to accounting standards. Industry and accounting

standards setters have not considered yet.

• IFRS 9 – potential impact on classification as AFS.

• Tax - There should be no change for investors in Public Debt CNAV/LVNAV MMFs (NAV of

the fund should remain constant)

• Impact on investors in VNAV funds will need to be considered -

Investors that are taxed on a realisation basis - any uplift in NAV likely a taxable event on redemption.

Investors that are taxed on a fair value basis - any uplift in NAV may be subject to tax on an unrealised basis.

3131 irishfunds.ie

Current Status

• The EU Money Market Fund Regulation was published on 30 June 2017 in the EU Official

Journal and became effective on 21 July 2018.

• New funds have 12 months (to July 2018) and existing funds have 18 months (to January

2019) to achieve compliance with the Regulation.

• ESMA consultation on Delegated Acts.

• The Regulation will be reviewed by the Commission five years after entry into force.

3232 irishfunds.ie

McCann Fitzgerald

Iain Ferguson

Ireland as a leading ETF location & CBI ETF Discussion Paper /

PE in Ireland & the new Investment Limited Partnership

3333 irishfunds.ie

• Irish funds industry centre for excellence: ETF issuers have access to services providers with specialist legal, tax and accounting expertise applied through highly automated and scalable global models.

• Home to some of the top ETF issuers in Europe, Ireland is at the forefront of innovative product, operational and infrastructure development, including the ICSD model to centralise settlement of ETF shares.

• Ideally located as a hub for cross-border fund distribution and one of the main domiciles for UCITS funds.

• Internationally recognised jurisdiction with membership of the EU, Eurozone, OECD, FATF and IOSCO and one of the most open economies in the world.

Ireland as an ETF location & CBI ETF Discussion Paper

3434 irishfunds.ie

Ireland as an ETF location & CBI ETF Discussion Paper

• Straightforward, fast and cost efficient primary listings offered on the Irish Stock Exchange (ISE), that allow ETF issuers access to the London Stock Exchange’s (LSE) market.

• Well-established but sufficiently flexible UCITS framework that allows promoters to structure a wide variety of index-tracking and actively managed ETFS and bring innovative and complex products to market quickly.

• ETFs benefit from Ireland’s neutral tax regime. Among other benefits, income and gains derived from investments are exempt from Irish tax. In addition to a transparent domestic tax regime Ireland has a continuously expanding, favourable tax treaty network spanning over 70 countries.

• Continued regulatory flexibility and sensitivity to market developments including the growth of non-traditional indexing strategies, or Smart Beta, and the introduction of Active ETFs.

3535 irishfunds.ie

• ETFs discussion paper from the Central Bank of Ireland – why?

• Themes

– Investor expectation

– Liquidity

– Increasing popularity of ETFs

• Discussion items

– ETF dealing

– ETF risks

– Types and features of ETFs

– ETFs and market liquidity

Ireland as an ETF location & CBI ETF Discussion Paper

3636 irishfunds.ie

PE in Ireland & the new (and improved!) ILP

• Private equity funds – global appetite

• Private equity through Irish funds and a fully engaged Central Bank of Ireland

• Significant benefits to a fully regulated Irish private equity structure

3737 irishfunds.ie

PE in Ireland & the new (and improved!) ILP

• ILP - completing the “toolkit” for fund providers in Ireland

• Heads of legislation agreed by Irish government and due for publication (in days!)

• Technical, but necessary, adjustments to Irish Limited Partnership structure to ensure

consistency with similar offerings globally

• Significant utilisation expected based on investor/fund promoter feedback for all the usual

reasons for selection of Ireland as fund domicile

3838 irishfunds.ie

John Aherne, A&L Goodbody

Patrick Schleiffer, Lenz & Staehelin

MiFID II – Distribution of Irish Funds in EU and Switzerland

3939 irishfunds.ie

Overview

• Scope

– MiFID investment firms, credit institutions providing MiFID services (but not just EEA based

clients!)

– UCITS Mancos/AIFMs only where providing Article 6(3)/6(4) services (e.g. IPM)

• MiFID II package comprises

– Level 1: Recast MiFID directive and MiFIR

– Level 2: Delegated acts and Regulatory technical standards

– Level 3: ESMA guidance, ESMA Q & As

• Transpose by July 2017 and effective from 3 January 2018

• Implemented in Ireland: MiFID Regulations SI 60/2017 (generally a copy out approach)

MAIN-37501412-1

4040 irishfunds.ie

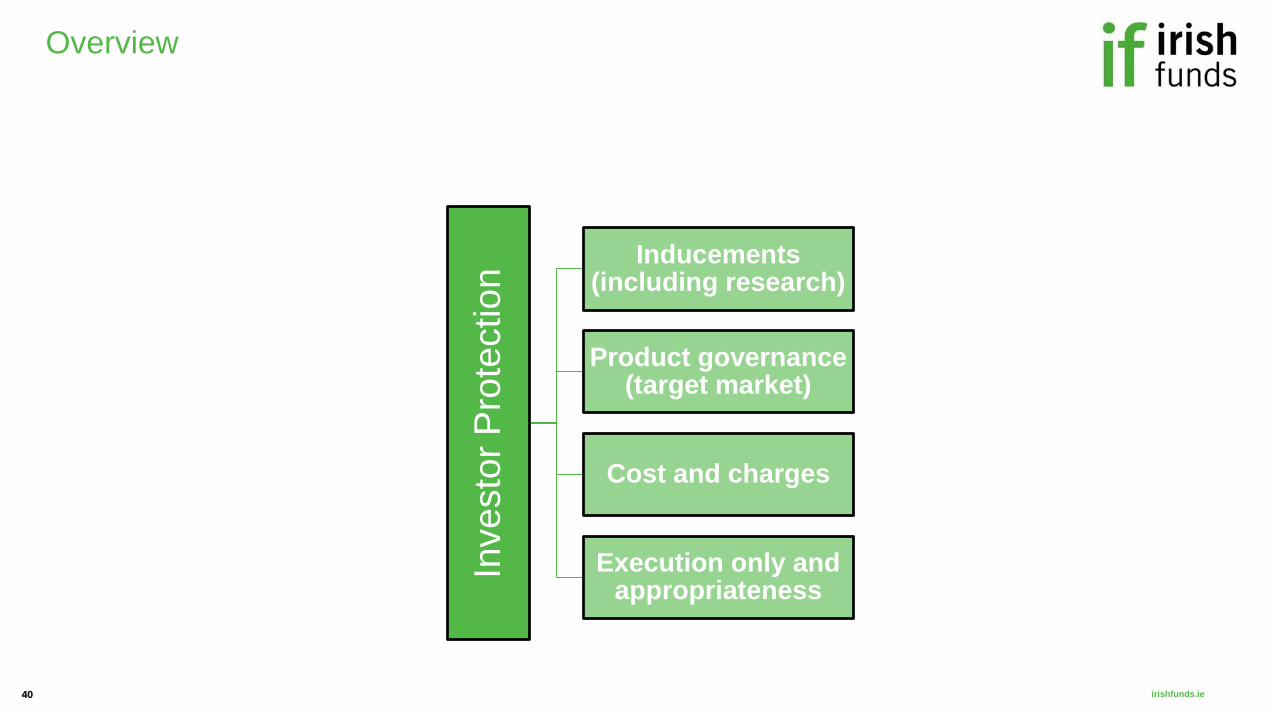

Overview

Investo

r P

rote

ctio

n

Inducements (including research)

Product governance (target market)

Cost and charges

Execution only and appropriateness

4141 irishfunds.ie

Inducements

• “Independent” investment advice/portfolio management:

• Ban on receiving and retaining payments/commissions/non-minor benefits from product provider (other than

minor non-monetary benefits)

• Off-setting against a firm’s own fees is same as retaining

• Quality Enhancement Test

– Criteria

• justified by the provision of an additional, or higher, level of service;

• it must not directly benefit the firm without tangible benefit to the client; and

• for ongoing inducements, there must be ongoing benefits to the client.

– Record-keeping and disclosure

• Inducements received or paid

• How these enhanced client service

• Client disclosure (ex-ante and ex post at least annually)

MAIN-37501412-1

4242 irishfunds.ie

Inducements

MAIN-37501412-1

Independent Advice and

Discretionary management

All other investment

services

Inducements received

(and retained) from a

third party

Not allowed

(except for minor non-monetary benefits

(MNB) if disclosed and enhance quality of

the service and there is exhaustive list of

MNB)

Allowed subject to disclosure

and QET

Inducements paid to a

third party

Allowed subject to disclosure and QET Allowed subject to disclosure

and QET

4343 irishfunds.ie

Investment research

• Prohibited for MiFID investment managers but may be received if:

Paid by the investment firm from its own P & L (recovery through AMC increase?)

Paid by the client through a research payment account (RPA)

• RPA model subject to detailed requirements including:

Research budget and client agreement to the research budget

Agree means/frequency of deducting research costs over the year (upfront versus alongside

execution commissions)

Control and oversight environment/robust quality criteria on research purchased

Written research policy available to clients

Client reporting

• No gold plating in Ireland to Mancos/AIFMs.

MAIN-37501412-1

4444 irishfunds.ie

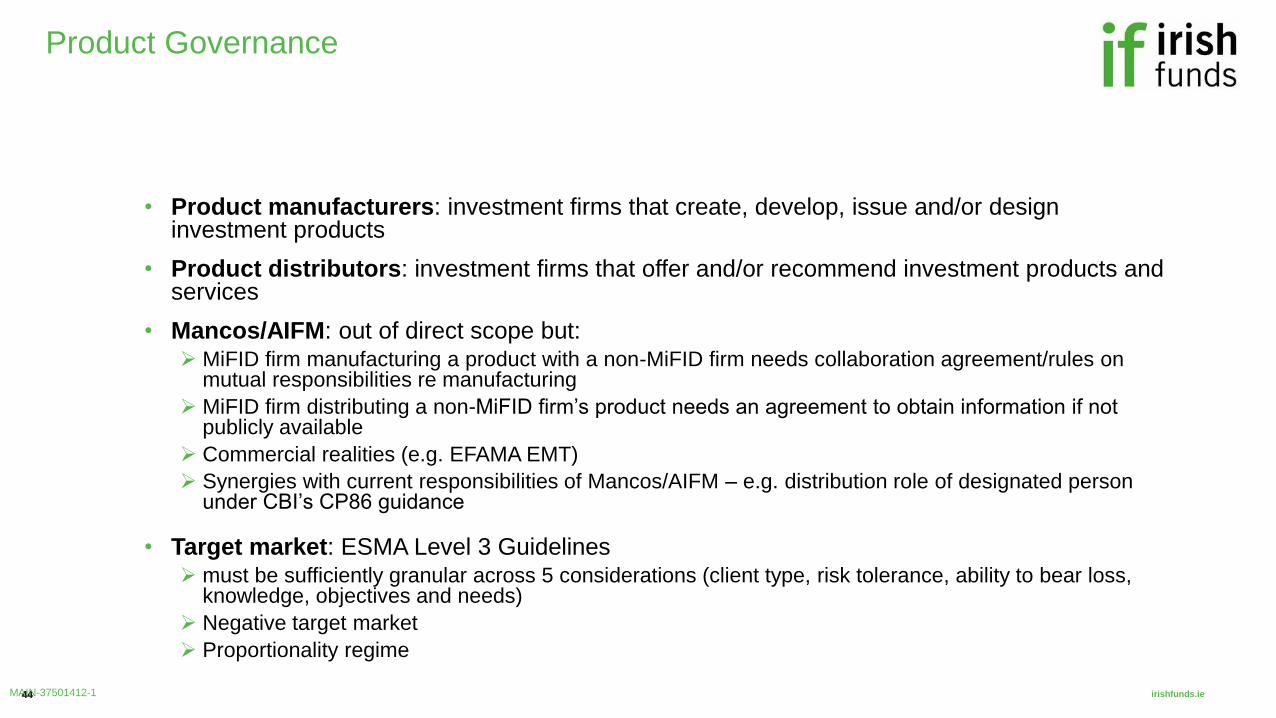

Product Governance

• Product manufacturers: investment firms that create, develop, issue and/or design investment products

• Product distributors: investment firms that offer and/or recommend investment products and services

• Mancos/AIFM: out of direct scope but: MiFID firm manufacturing a product with a non-MiFID firm needs collaboration agreement/rules on

mutual responsibilities re manufacturing

MiFID firm distributing a non-MiFID firm’s product needs an agreement to obtain information if not publicly available

Commercial realities (e.g. EFAMA EMT)

Synergies with current responsibilities of Mancos/AIFM – e.g. distribution role of designated person under CBI’s CP86 guidance

• Target market: ESMA Level 3 Guidelines must be sufficiently granular across 5 considerations (client type, risk tolerance, ability to bear loss,

knowledge, objectives and needs)

Negative target market

Proportionality regime

MAIN-37501412-1

4545 irishfunds.ie

Product Governance

Manufacturer Distributors

• Product approval process (new

products and significant adaptions)

Identify target market

Assessment of relevant risks

Distribution strategy

• Regular product reviews

• Scenario analysis/stress testing for

risks and taking appropriate steps

• Governance and oversight (with

compliance input)

• Make necessary info available to

distributors

• Steps to ensure products are sold to TM

and function as intended

• Determine target market of the financial

instrument for its clients

• Processes to ensure products offered in

line with the identified target market

• Regular product reviews

• Ensure sales staff understand the

product’s characteristics and risks

• Governance and oversight (with

compliance input)

• Provision of sales info to PM

• Arrangements to obtain sufficient info

from PM (including target market and

distribution strategy)

4646 irishfunds.ie

Cost transparency

• Enhanced cost transparency drivers:

MiFID II, PRIIPs, UK DC workplace pensions…..

• MIFID II requires:

Ex ante: Clients of all costs on an aggregated basis PRIOR to investment (can be

estimated but related to actual costs)

Ex post: Inform clients about all costs at least annually DURING investment

Aggregate distributor's own costs (including rebates to be disclosed separately)

and product costs (provide itemised breakdown on request)

Costs shown as cumulative effect on return

• Obligation to liaise with the UCITS Manco /AIFM for information not publicly available ( e.g.

transaction costs)

• UCITS OCF – is it redundant?

MAIN-37501412-1

4747 irishfunds.ie

Execution only/Appropriateness

• Investment firms required to conduct appropriateness test for sale of complex products

(request information on client’s knowledge and experience to assess appropriateness)

• List of non-complex products includes UCITS (except structured)

• Automatically complex products:

structured UCITS

AIFs (but EFAMA pushback on ESMA Q & A)

Test in Article 57 of Delegated Regulation for “other non-complex financial instruments”

MAIN-37501412-1

4848 irishfunds.ie

New Swiss Financial Services Act

• New Swiss Financial Services Act (FinSA)

– New rules on client segmentation (similar to MIFID 2)

– New rules at point of product: uniform prospectus rule generally applying to any securities offered

in/into Switzerland (similar to EU PD/PR)

– New rules at point of sale: market conduct rules

• Currently under debate in Swiss parliament

• FinSA expected to enter into effect on 1 January 2019 (together with new Swiss Financial

Institutions Act inter alia providing for harmonized regulation for asset manager providers)

4949 irishfunds.ie

New Rules at Point of Product (Cross-Border)

Offering of Irish Funds per Client Category

Offering of Irish Funds

into Switzerland

Registration

of Fund

in Switzerland

Registration

of Prospectus

in Switzerland

KID Appointment

Swiss Representative/

Swiss Paying Agent

Comments

Institutional Clients

(similar to eligible counterparty

category under MiFID II)

No No No No Lower regulation

Professional Clients

(similar to professional client category

under MiFID II)

No No No No Lower regulation

HNWIs with Opting-out

(to be treated as professional client)

No No No Yes Lower regulation

Private Clients with

discretionary portfolio agreement

advisory agreement

No Yes No/

yes

No Stricter regulation

Private Clients (retail) Yes Yes Yes Yes Stricter regulation

5050 irishfunds.ie

New Rules at Point of Sale (Cross-Border)

Swiss Client Adviser Register

Main Registration Requirements Comments

Client adviser (C/A) to register with Swiss Client Adviser Register

• C/A: natural person providing financial services, i.e. person having contact to clients (such as

sales force, investment advisers, RMs)

• Delegation to Swiss Government to exempt C/A of non-Swiss financial service providers

subject to prudential supervision, provided services to be rendered exclusively to institutional

clients/professional clients (w/o HNWIs)

Stricter regulation

Key will be that C/A of financial

service providers subject to

prudential supervision are

exempted

C/A to comply with education/training requirement of FinSA Stricter regulation

Duties of conduct

• Duty to comply with duties of conduct under FinSA

• To institutional clients: duties of conduct of FinSA do no apply

• To professional clients (w/o HNWIs): may waive certain duties of conduct

Stricter regulation

C/A to obtain professional liability insurance Stricter regulation

C/A to join an ombudsman’s institution under FinSA Stricter regulation

5151 irishfunds.ie

New Rules at Point of Sale (Cross-Border)

Requirements per Client Category

Offering of Irish Fund

Into Switzerland by

Non-Swiss FSP

License

Requirements

Registration with

Swiss Adviser

Register

Swiss Duties of Conduct

applicable

Comments

Institutional Clients

(similar to eligible counterparty

category under MiFID II)

No No (expected) No Key will be that

registration

requirement does not

apply

Professional Clients

(similar to professional client

category under MiFID II)

No No (expected) May be partially waived by

professional client

Key will be that

registration

requirement does not

apply

HNWIs with Opting-out

(to be treated as professional

client, with exceptions)

No Yes May be partially waived by

professional client

Stricter regulation

Private Clients with

discretionary

portfolio/advisory agreement

No Yes Yes Stricter regulation

Private Clients (retail) No Yes Yes Stricter regulation

5252 irishfunds.ie

FinSA: Key Differences to EU Regulations

• No requirement to establish branch/obtaining regulatory license if distributing funds (and

other financial instruments) on a cross-border basis into Switzerland

• No license requirement for mere investment advisers (but duty to register in Swiss adviser

register)

• Execution only orders of retail clients available for any financial instruments

• Inducements not prohibited in the context of discretionary mandates

• No distinction between dependent and independent financial services

• No product governance rules

5353 irishfunds.ie

Credit Suisse

David Dubach

CS Investor Services – Setting up in Ireland

Irish Funds, Zurich Seminar

CS Investor Services - Setting up in Ireland

External

Credit Suisse Investor Services

21 September 2017

People

Credit Suisse Investor Services (CSIS)Our growth is based on our people’s skills and partnership with our clients

Client segments: Pension funds, insurance companies, banks, asset

managers, family offices, UHNWIs, external asset managers, fund

management companies

Fund domiciles: CH, LU, KY, BVI and IRL

Fund types: UCITS & AIFs

Asset types: Liquid & illiquid (including real estate funds)

661Funds

200+Fund specialists

Switzerland

Luxembourg

Ireland

Poland

Growth

Credit Suisse Investor Services

Clients

311

140

today2009

AuA growth from

Q4 2009 until

today (as of 31

July 2017, in bn

CHF):

+120%AuA

5521 September 2017

Fund

Administratio

n&

Transfer

Agent

Depository

Bank

Fund

Management

Company &

Distribution

Support

CS

Core

Services

Ireland market entry completes our pan-

European coverage model of

regulated fund domiciles

Extending the integrated model to Ireland

enhances our UCITS and AIF offering

CS has decided that Ireland will be the

future centre for servicing all offshore

structures

Ireland market entry enhances

diversification while leveraging our

capabilities across Europe

Integrated model – a one-stop-shop for our clients Strategic goals for CS’ Ireland coverage

56

Integrated service offeringWe are a one-stop-shop for UCITS, AIFs and non regulated fund structures

Credit Suisse Investor Services 21 September 2017

Rationale for expansionFive key drivers to expand our integrated fund services value chain to Ireland

Ireland as the second largest European fund services market, represents a major

growth opportunity for CS as a fund service provider.

Growth strategy

A subset of clients have indicated a desire to use Ireland as their principal fund

servicing centre

Client needs

The opportunity to passport our established EU-based, third party management company

and create a branch of our Luxembourg bank

EU regulation

We consider the our integrated model of Fund Administration, Depository Bank,

Management Company & Distribution Support to be a unique offering in the Irish market

Integrated model

Ireland market entry enables CSIS to leverage existing investments in people,

processes and technology

Leverage investment

57Credit Suisse Investor Services 21 September 2017

Expansion to IrelandTailor-made fund solutions and services in Switzerland and Europe

Credit Suisse (Luxembourg) S.A.

Depositary Bank

Credit Suisse Fund Services (Luxembourg) S.A.

Fund Administration

Credit Suisse (Poland) Sp Z.o.o. –

Info Management

Operational leverage for existing

CSIS fund domiciles

MultiConcept Fund Management S.A.

Fund Management company for third-party-clients

Credit Suisse Funds AG

Fund Management Company and Fund

Administration

Credit Suisse (Switzerland) Ltd

Depositary Bank

Credit Suisse (Luxembourg) S.A., Ireland Branch

Depositary Bank

Credit Suisse Fund Services (Ireland) Ltd

Fund Administration

MultiConcept Fund Management S.A.

Fund Management Company passported from Lux

58Credit Suisse Investor Services 21 September 2017

Credit Suisse experience when expanding to IrelandA highly developed and mature fund services market

59

Authorisation

Processes

Support

Ireland is a

highly mature

regulatory

environment,

consistent with

Switzerland

and

Luxembourg

Transparent,

open and

communicative

Leverages best

practice set

down in UCITS

and AIFMD

9 months for full

authorisation of

all three legal

entities

Highly experienced

and qualified staff

on site

Professional

services provided by

- legal firms

- advisory firms

Regulatory

Environment

Ecosystem

The industry in Ireland

is mature and

supported through

representative bodies

and forums

Irish Funds in

particular were

supportive, providing

guidance and industry

connections

Credit Suisse Investor Services 21 September 2017

Distribution supportCSIS supports clients’ growth ambition along distribution value chain

21 September 2017 60

Distribution strategy

Fund documents including publication

Distribution agreements

Registration all countries

Trailer fee management

Sales

Supporting your distribution activities worldwide Distribution support services by CS

Credit Suisse Investor Services

Distribution of Irish funds Switzerland as one of the key markets for the distribution of Irish funds in Europe

Source: Irish Funds, 2017

61Credit Suisse Investor Services

2013

1’130

20162015

1’568

2014

1’371

1’689

#5

#IRL funds distributed in

CH

Top markets

21 September 2017

Disclaimer

The information provided herein constitutes marketing material. It is not investment advice or otherwise based on a consideration of the

personal circumstances of the addressee nor is it the result of objective or independent research. The information provided herein is not

legally binding and it does not constitute an offer or invitation to enter into any type of financial transaction.

The information provided herein was produced by Credit Suisse Group AG and/or its affiliates (hereafter "CS") with the greatest of care and

to the best of its knowledge and belief.

The information and views expressed herein are those of CS at the time of writing and are subject to change at any time without notice.

They are derived from sources believed to be reliable.

CS provides no guarantee with regard to the content and completeness of the information and does not accept any liability for losses that

might arise from making use of the information. If nothing is indicated to the contrary, all figures are unaudited. The information provided

herein is for the exclusive use of the recipient.

Neither this information nor any copy thereof may be sent, taken into or distributed in the United States or to any U. S. person (within the

meaning of Regulation S under the US Securities Act of 1933, as amended).

It may not be reproduced, neither in part nor in full, without the written permission of CS.

Copyright © 2017 Credit Suisse Group AG and/or its affiliates. All rights reserved.

62Credit Suisse Investor Services 21 September 2017

6363 irishfunds.ie

Irish Funds

Kieran Fox

Closing Remarks

6464 irishfunds.ie

Networking Lunch

Kindly hosted by Six Financial