hospitality industryoctober 24,...

TRANSCRIPT

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

Init

iatin

g C

overage

October 24, 2019

Hospitality Industry

Tourism – Turning into integral part of lifestyle

In the past few years, the Indian tourism sector has experienced a sea

change in its landscape, with travel being considered an integral part of

one’s annual calendar. With income levels expected to rise along with

various initiatives by the Government of India to enable the travel & tourism

ecosystem, this should augur well for the hospitality industry. Strategic

initiatives include relaxed FDI policies, revamping of the ‘Incredible India’

campaign, various schemes viz. UDAN, PRASAD, National Heritage City

Development, Augmentation Yojana (HRIDAY) and extension of e-visa to

166 countries. The recent move by the government with regard to lowering

the e-visa fees and reducing GST rates for hotel rooms will again make India

a more attractive destination. Going ahead, all these factors are expected to

keep demand growth healthy. With supply growth slowing down, we believe

the industry is at the cusp of an uptrend.

Tourism remains key focus area of government

The Indian travel & tourism industry plays a significant role in the nation’s

growth through employment, revenue generation as well as foreign

exchange earnings. Being among the top 10 contributors to global travel and

tourism GDP, it plays a significant role in economic and social aspects,

generating $247.3 billion in 2018, growing by 6.7% and contributed 9.2% to

the Indian economy. The government has announced various initiatives in

enabling the travel and tourism initiatives. The latest moves were GST rate

reduction for hotels and lowering of visa fees. The fees under the new e-visa

scheme have been brought down substantially from $80-100 to $30-45.

Further, the recent GST rate reduction (from 28% to 18% for tariff above

| 7500 and from 18% to 12% for tariff below | 7500 for hotels) has made the

cost of tour in India cheaper and more competitive.

Industry to witness uptrend with demand outpacing supply

Demand for India’s hospitality sector will continue to benefit from under-

penetration of hotels in India vs. developed economies, moderation in new

room supply, improved connectivity, rising income levels and growing

service sector that will aid increased business travels. Inbound tourism is

also on a growth trajectory aided by favourable policies and developments

such as e-visa, expansion of visa on arrival facility, the Incredible India 2.0

campaign and better regional connectivity. The supply growth projection of

5% in the next five years would help keep occupancy levels healthy. Average

occupancy levels are expected to increase to 73% by FY23E, which should

create room for ARR improvement for the companies, going forward.

Chalet Hotels and Lemon Tree Hotels set to reap benefits

The hospitality sector was in troubled waters since late 2008 due to

substantial supply growth coupled with a slowdown in demand. Occupancy

has revived since FY14 and more notably from FY15, as demand conditions

have improved and new supply has slowed. The upward trend in RevPAR

has mainly been occupancy led and is expected to gain further momentum.

With supply slowing down and demand expected to improve with

government initiatives to boost tourism (e-visa, GST rate cuts, revamping

“Incredible India”), improving connectivity (UDAN scheme, road projects,

etc) an uptrend looks to be on the cards for the hospitality industry. We like

Chalet Hotels and Lemon Tree Hotels in this space. We initiate coverage on

Chalet Hotels with a HOLD rating and on Lemon Tree Hotels with a BUY

rating.

Key Highlights

Hospitality players staring at industry

uptrend

Government’s push towards tourism in

form of GST rate cuts, reduction in visa

charges and thrust to improve

connectivity to boost travel & tourism

Foreign tourist arrivals growing at 8.8%

CAGR over last five years

Demand growth expected to outpace

supply growth

Pan-India occupancies to reach 73% by

FY23E

Initiate coverage on Chalet Hotels and

Lemon Tree

Rating Matrix – Initiating Coverage

Company Rating Target Upside

Chalet Hotels HOLD 350 2.9%

Lemon Tree Hotels BUY 73 25.0%

Research Analyst

Rashesh Shah

Romil Mehta

ICICI Securities | Retail Research 2

ICICI Direct Research

Initiating Coverage | Hospitality Industry

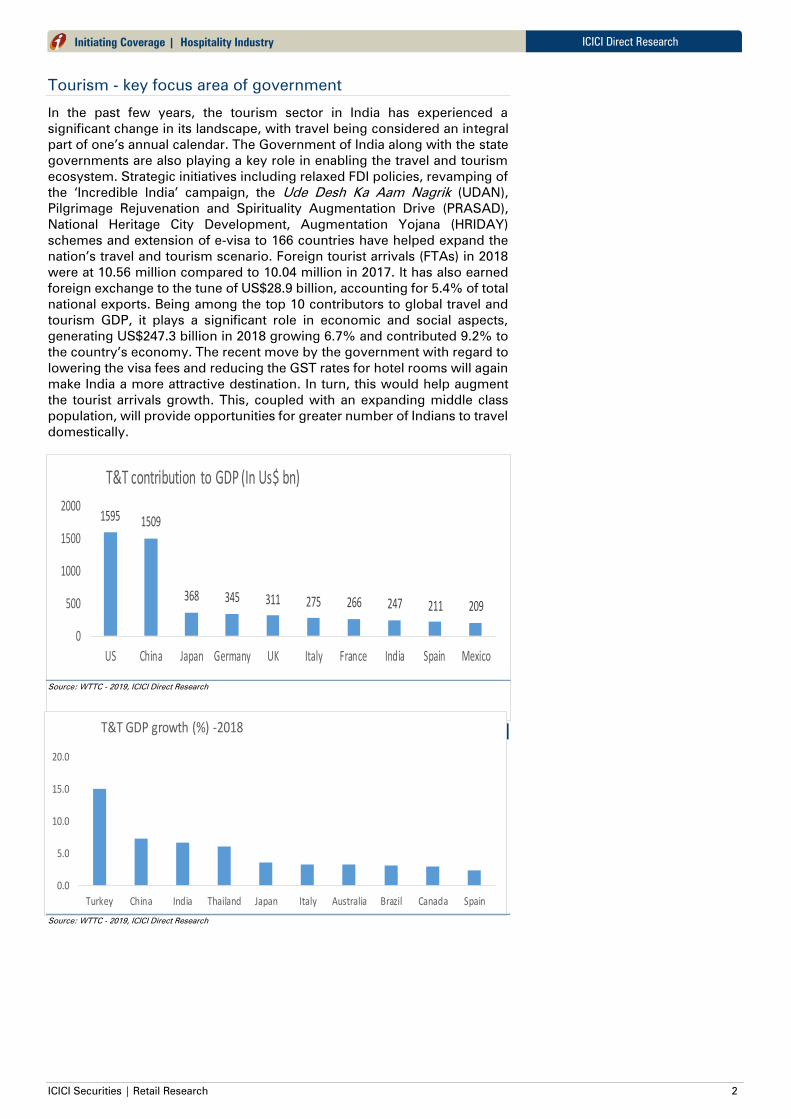

Tourism - key focus area of government

In the past few years, the tourism sector in India has experienced a

significant change in its landscape, with travel being considered an integral

part of one’s annual calendar. The Government of India along with the state

governments are also playing a key role in enabling the travel and tourism

ecosystem. Strategic initiatives including relaxed FDI policies, revamping of

the ‘Incredible India’ campaign, the Ude Desh Ka Aam Nagrik (UDAN),

Pilgrimage Rejuvenation and Spirituality Augmentation Drive (PRASAD),

National Heritage City Development, Augmentation Yojana (HRIDAY)

schemes and extension of e-visa to 166 countries have helped expand the

nation’s travel and tourism scenario. Foreign tourist arrivals (FTAs) in 2018

were at 10.56 million compared to 10.04 million in 2017. It has also earned

foreign exchange to the tune of US$28.9 billion, accounting for 5.4% of total

national exports. Being among the top 10 contributors to global travel and

tourism GDP, it plays a significant role in economic and social aspects,

generating US$247.3 billion in 2018 growing 6.7% and contributed 9.2% to

the country’s economy. The recent move by the government with regard to

lowering the visa fees and reducing the GST rates for hotel rooms will again

make India a more attractive destination. In turn, this would help augment

the tourist arrivals growth. This, coupled with an expanding middle class

population, will provide opportunities for greater number of Indians to travel

domestically.

Exhibit 1: T&T contribution to GDP (in US$ bn)

1595 1509

368 345 311 275 266 247 211 209

0

500

1000

1500

2000

US China Japan Germany UK Italy France India Spain Mexico

T&T contribution to GDP (In Us$ bn)

Source: WTTC - 2019, ICICI Direct Research

Exhibit 2: T&T GDP growth (%) - 2018

0.0

5.0

10.0

15.0

20.0

Turkey China India Thailand Japan Italy Australia Brazil Canada Spain

T&T GDP growth (%) -2018

Source: WTTC - 2019, ICICI Direct Research

ICICI Securities | Retail Research 3

ICICI Direct Research

Initiating Coverage | Hospitality Industry

Exhibit 3: Foreign tourist arrival growth

0.69 0.77 0.820.92

1.03 1.06

FY14 FY15 FY16 FY17 FY18 FY19

CAGR of 18.4% over FY14-19

FTAs (In cr)

Source: Ministry of Tourism, ICICI Direct Research

Exhibit 4: Foreign exchange earnings from tourism

20.2 21.1 22.927.7 28.6

19.3

2014 2015 2016 2017 2018 2019*

CAGR of 9% over 2014-2018

Foreign Exchange Earnings ($ billion)

Source: Ministry of tourism, ICICI Direct Research

Travel volumes, in terms of visits by domestic travellers, have grown at 9.5%

CAGR in the past five years. Although hotels and resorts in India get only a

small percentage of the overall domestic travel in the country, this segment

is an increasingly important demand generator for the hotel sector.

Exhibit 5: Domestic travellers increasing gradually

11425

12828

14320

16136 16525

18000

0

5000

10000

15000

20000

2013 2014 2015 2016 2017 2018

Dom

estic v

isitations (in Lakh)

Domestic tourist visits grew at CAGR of 9.5% during last 5 years

Source: Hotelivate - 2019, ICICI Direct Research

Demand growth potential is huge

Demand in India’s hospitality sector will continue to benefit from

Under-penetration of hotels in India compared to developing

economies, 2) moderation in new room supply

Improved road & rail connectivity

Rising income levels

Growing service sector that will aid increased business travels

Inbound tourism is also on a growth trajectory aided by favourable policies

and developments such as e-visa, expansion of visa on arrival facility, the

incredible India 2.0 campaign and better regional connectivity.

Significant room under-penetration

World USA China India

Total rooms (mn) 16.2 5.0 3.8 0.20

Population (mn) 7349 321 1379 1211

Penetration 2.20 15.58 2.76 0.17

ICICI Securities | Retail Research 4

ICICI Direct Research

Initiating Coverage | Hospitality Industry

Limited room supply growth to rev up occupancy

The hotel sector in India experienced a difficult period from late 2008, with

a double dip in occupancy. This was primarily due to the demand-supply

mismatch caused by substantial supply growth coupled with slowdown of

demand on the other hand. The occupancy rates across India remained

stagnant below 60% between FY09-15. During FY11 to FY15, 36,000 rooms

were added creating significant new capacity; simultaneously the economy

and demand patterns were weak. Occupancy has revived since the financial

year 2014 and more notably from the financial year 2016, as demand

conditions have improved and new supply has slowed. The upward trend in

RevPAR has mainly been occupancy led, and is expected to gain momentum

further due to limited capacity additions going forward. As a result, ARR

levels are expected to improve, slowly in some markets and more strongly

in some other markets which are already experiencing strong occupancy, as

demand and occupancy levels improve.

Exhibit 6: Room supply growth has been significantly high in past; cools down to single digits

7153

1

8431

3

9425

5

1071

77

10

76

95

1116

00

11

92

19

12

65

65

1333

59

1703

51

15.8% 17.9%

11.8% 13.7%

0.5%

3.6% 6.8% 6.2%5.4%

5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

0

50000

100000

150000

200000

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY24E

Rooms supply to grow at 5% CAGR during FY19-24E vs. 9% CAGR during FY10-19

Rooms (LHS) Growth (RHS)

[[

Source: Hotelivate 2019, ICICI Direct Research

The supply growth projection of 5% over the next five years would help keep

occupancy levels healthy. We expect average occupancy levels to increase

to 73% by FY23E. This should help companies to improve their ARR

significantly, going forward.

Exhibit 7: Occupancies to improve on the back of gradual demand growth outpacing room addition growth

70.8

59.5 59.560.6

59.3

57.858.4 58.8

63.3

64.8

66.767.5

73.0

50

55

60

65

70

75

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY23E

Occupancy levels to improve going forward (%)

Source: STR, Horwath HTL, ICICI Direct Research

Incremental Room supply– City wise

Location CAGR (FY19-23E)

Chennai 0.4

New Delhi 1.2

Hyderabad 1.7

Pune 2.4

Agra 3.0

Bengaluru 4.9

Mumbai 5.5

Goa 5.6

Gurugram 5.7

Jaipur 6.6

Noida 6.9

Kolkata 8.3

Ahmedabad 10.8

ICICI Securities | Retail Research 5

ICICI Direct Research

Initiating Coverage | Hospitality Industry

Mumbai, Delhi, Goa – Top three in terms of RevPAR

With improved demand and a balanced supply environment post FY15, all

major markets witnessed an improvement in occupancy and ARRs in the

past five years. In terms of city wise performance, Mumbai, Delhi and Goa

remain the top three, achieving highest occupancy and ARRs among top 13

cities in India. While ARR growth of Bengaluru, Ahmedabad and Pune

continued to remain healthy, Hyderabad has emerged as a leader in terms

of growth in both levers i.e. ARR & occupancy. The increase can be

attributed to Grade A commercial set-ups that are commencing operations

in the city leading to steady flow of demand

Exhibit 8: Mumbai, Delhi, Goa most dense markets

Occupancy (%) FY14 FY15 FY16 FY17 FY18 FY19 5 yr CAGR (bps)

Mumbai 67.0 71.8 73.7 74.4 75.5 77.1 285

New Delhi 60.9 61.7 66.7 69.4 70.5 72.5 355

Bengaluru 57.7 58.1 65.7 65.9 68.3 66.0 272

Chennai 55.4 58.9 62.7 64.8 63.0 65.0 325

Hyderabad 51.7 57.1 59.3 63.7 66.3 70.3 634

Kolkata 70.2 67.8 69.3 70.9 70.2 70.8 17

Gurugram 58.8 61.1 63.7 66.3 67.9 68.8 319

Noida 53.5 48.0 51.0 56.2 54.9 60.0 232

Pune 57.4 61.3 65.6 64.1 68.2 69.9 402

Ahmedabad 52.7 53.9 55.6 61.1 63.8 63.9 393

Goa 68.7 69.7 70.2 71.3 70.0 71.8 89

Jaipur 54.3 54.5 60.8 64.4 67.6 67.9 457

Agra 60.4 61.5 57.7 59.6 66.2 67.0 210

Business Destinations

Leisure Destinations

Source: Hotelivate – 2019, ICICI Direct Research

Exhibit 9: Mumbai, Delhi, Goa also have highest ARRs, thus highest RevPARs as well

ARR (|) FY14 FY15 FY16 FY17 FY18 FY19 5 yr CAGR (%)

Mumbai 7,158 7,230 7,353 7,612 7,760 8,096 2.5

New Delhi 6,941 6,568 6,211 6,292 6,649 7,026 0.2

Bengaluru 5,379 5,368 5,392 5,598 5,823 6,339 3.3

Chennai 5,050 4,825 4,767 4,761 4,863 5,045 0.0

Hyderabad 4,556 4,535 4,741 4,880 4,924 5,217 2.7

Kolkata 5,739 5,734 5,607 5,814 5,904 5,853 0.4

Gurugram 6,569 6,241 6,253 6,382 6,113 6,346 -0.7

Noida 5,964 5,429 5,281 5,652 5,323 6,100 0.5

Pune 3,908 3,846 3,922 4,195 4,484 4,807 4.2

Ahmedabad 3,734 3,753 3,884 3,897 4,158 4,578 4.2

Goa 6,692 6,819 7,020 7,538 7,920 7,912 3.4

Jaipur 4,743 4,743 4,721 4,787 5,051 5,296 2.2

Agra 6,338 6,488 6,083 5,508 5,316 5,726 -2.0

Business Destinations

Leisure Destinations

Source: Hotelivate – 2019, ICICI Direct Research

RevPAR growth – City wise

RevPAR (|) 5 year CAGR (%)

Mumbai 5.4

New Delhi 3.8

Bengaluru 6.2

Chennai 3.2

Hyderabad 9.3

Kolkata 0.6

Gurugram 2.5

Noida 2.8

Pune 8.4

Ahmedabad 8.3

Goa 4.3

Jaipur 6.9

Agra 0.0

Leisure Destinations

Business Destinations

ICICI Securities | Retail Research 6

ICICI Direct Research

Initiating Coverage | Hospitality Industry

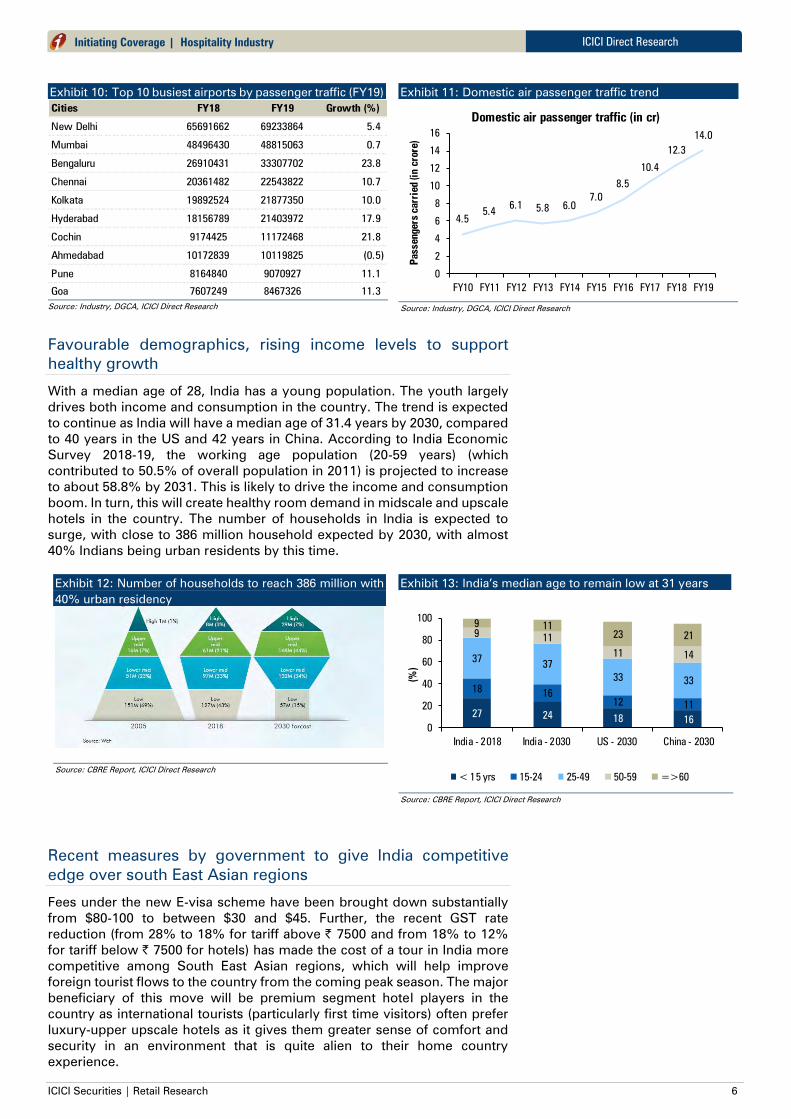

Exhibit 10: Top 10 busiest airports by passenger traffic (FY19)

Cities FY18 FY19 Growth (%)

New Delhi 65691662 69233864 5.4

Mumbai 48496430 48815063 0.7

Bengaluru 26910431 33307702 23.8

Chennai 20361482 22543822 10.7

Kolkata 19892524 21877350 10.0

Hyderabad 18156789 21403972 17.9

Cochin 9174425 11172468 21.8

Ahmedabad 10172839 10119825 (0.5)

Pune 8164840 9070927 11.1

Goa 7607249 8467326 11.3

Source: Industry, DGCA, ICICI Direct Research

Exhibit 11: Domestic air passenger traffic trend

4.5

5.46.1

5.8 6.0

7.0

8.5

10.4

12.3

14.0

0

2

4

6

8

10

12

14

16

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19

Passengers c

arried (in crore)

Domestic air passenger traffic (in cr)

Source: Industry, DGCA, ICICI Direct Research

Favourable demographics, rising income levels to support

healthy growth

With a median age of 28, India has a young population. The youth largely

drives both income and consumption in the country. The trend is expected

to continue as India will have a median age of 31.4 years by 2030, compared

to 40 years in the US and 42 years in China. According to India Economic

Survey 2018-19, the working age population (20-59 years) (which

contributed to 50.5% of overall population in 2011) is projected to increase

to about 58.8% by 2031. This is likely to drive the income and consumption

boom. In turn, this will create healthy room demand in midscale and upscale

hotels in the country. The number of households in India is expected to

surge, with close to 386 million household expected by 2030, with almost

40% Indians being urban residents by this time.

Exhibit 12: Number of households to reach 386 million with

40% urban residency

Source: CBRE Report, ICICI Direct Research

Exhibit 13: India’s median age to remain low at 31 years

27 2418 16

1816

12 11

3737

3333

911

11 14

9 11

23 21

0

20

40

60

80

100

India - 2018 India - 2030 US - 2030 China - 2030

(%

)

< 15 yrs 15-24 25-49 50-59 =>60

Source: CBRE Report, ICICI Direct Research

Recent measures by government to give India competitive

edge over south East Asian regions

Fees under the new E-visa scheme have been brought down substantially

from $80-100 to between $30 and $45. Further, the recent GST rate

reduction (from 28% to 18% for tariff above | 7500 and from 18% to 12%

for tariff below | 7500 for hotels) has made the cost of a tour in India more

competitive among South East Asian regions, which will help improve

foreign tourist flows to the country from the coming peak season. The major

beneficiary of this move will be premium segment hotel players in the

country as international tourists (particularly first time visitors) often prefer

luxury-upper upscale hotels as it gives them greater sense of comfort and

security in an environment that is quite alien to their home country

experience.

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

Init

iatin

g C

overage

October 24, 2019

CMP: | 340 Target: | 350 ( 3%) Target Period: 12 months

Chalet Hotels (CHAHOT)

HOLD

Play on high-end hospitality…

Chalet Hotels, a part of the K Raheja Corp group, is an owner, developer and

asset manager of luxury upper upscale and upscale hotels. The company

has a stabilized room portfolio of 2331 keys comprising five operating

hotels, three in the Mumbai Metropolitan Region (MMR) and one each in

Hyderabad and Bengaluru. The company also owns ~8.7 lakh sq. ft. of retail

and commercial assets in Mumbai and Bengaluru. With hotel assets

stabilized aided by favourable demand supply dynamics in its core markets

in the hospitality segment, we factor in ~5% CAGR growth in RevPARs on

the back of 3.6% growth in ARRs between FY19-21E. Further, with additional

revenues kicking in from the commencement of operations of commercial

& retail assets in Mumbai, we expect total revenues to grow at 8% CAGR in

FY19-21E and EBITDA at a CAGR of 15% during the same period. With

limited headroom for growth from current hospitality assets, we initiate

coverage on Chalet with a HOLD rating.

Retail, commercial assets to be major growth contributors

Chalet Hotels’ hospitality portfolio has stabilized and ended FY19 with an

occupancy of 76% with a major growth trigger expected to come from

FY22E. The company’s retail and commercial assets would be the major

revenue drivers in next two years with the operationalization of The Business

Centre – Sahar (3.7 lakh sq. ft.) for which an agreement has been signed with

WPP Marketing to lease the property and The Orb - Retail (1.2 lakh sq. ft.)

where agreements have been signed with retailers. From the current (FY19)

contribution of 3% of the total income (ex-real estate), this segment’s share

is expected to increase to 8% by FY21E to ~| 95 crore.

Highest EBITDA margins among peers; to remain margin leader

Chalet Hotels is an asset developer and owner of hotel properties. While, It

does not own any hospitality brand, it signs management contracts with

major hospitality brands (currently all brands owned by Marriott

International) to manage its properties and pays charges in the form of

royalty (% of revenues), incentive fees (% of gross operating profit) and

reimbursements to the brand owner. These payments form ~8%-9% of

revenues. Most of its peers, clock EBITDA margins in the 20-30% range

while Chalet, despite not having its own brand and no revenues from

management contract (which its peers generate), has been generating

EBITDA margins in excess of 30% since FY17.

Valuation & Outlook

Chalet Hotels raised ~| 950 crore via IPO and reduced its debt significantly,

slicing its debt/EBITDA from 11.1x in FY18 to 4.8x in FY19. While Chalet’s

profitability is expected to improve over the next two years, its current hotels

portfolio has limited space for growth (Blended occupancy for FY19 was

76%). Thus the next major growth trigger is expected between FY22-24E

with addition of new hotels and commercial assets. As the company is

currently under capex mode, we initiate coverage with a HOLD rating and a

target price of | 350 valuing the company at 21x FY21E EV/EBITDA.

Key Financial Summary

Key Financials FY17 FY18 FY19 FY20E FY21E CAGR (FY19-21E)

Net Sales 706 796 987 1052 1147 8%

EBITDA 212 245 319 374 424 15%

EBITDA (%) 30.1 30.8 32.3 35.5 37.0

PAT (Adj) 138 -15 -6 144 213 NA

EPS (|) 6.7 -0.7 -0.3 7.0 10.4

EV/EBITDA 45.1 39.5 26.4 22.8 20.8

RoNW (%) 25.7 -19.2 -0.8 9.7 13.0

RoCE (%) 12.5 7.0 8.9 10.0 10.9

Source: ICICI Direct Research, Company

Stock Data

Amount

Market Capitalization | 6971

Debt (FY19) | 1546

Cash & Invest (FY19) | 83

EV | 8434

52 week H/L | 387/250

Equity cap | 205

Face value | 10

Particulars

Price Chart

6,000

8,000

10,000

12,000

14,000

0

100

200

300

400

Oct-19

Jul-19

Apr-19

Jan-19

Oct-18

Jul-18

Apr-18

Jan-18

Oct-17

Aug-17

May-17

Feb-17

Nov-16

Price (R.H.S) Nifty (L.H.S)

Key Highlights

Three hotels and two commercial

assets under construction – All to begin

operations from CY21

The Orb and Business Centre in Powai

to begin operations from FY20E

Demand-supply dynamics getting in

favour of hospitality industry

Initiate coverage on Chalet Hotels with

HOLD rating and target price of |

350/share

Research Analyst

Rashesh Shah

Romil Mehta

ICICI Securities | Retail Research 8

ICICI Direct Research

Initiating Coverage | Chalet Hotels

Company Background

Owner of high-end properties at strategic locations

The company’s entire hotel portfolio is located in dense business districts of

MMR, Hyderabad and Bengaluru. Out of the total hotel portfolio of 2331 keys

across five hotels, 65% of the room portfolio is in Mumbai while the rest is

divided between Hyderabad and Bengaluru. All hotels are flagged under

global brands such as JW Marriott, Westin, Marriott, Renaissance and Four

Points by Sheraton, all of which are held by Marriott International and its

affiliates. Additionally, the company has ~8.7 lakh sq.ft. of retail and

commercial space, out of which ~5 lakh sq.ft. (Business Centre Sahar, The

Orb) would start generating revenues from FY20E.

Exhibit 14: Current room portfolio (65% in MMR)

Hotel NameLocation and size

of land parcel

No of roomsMonth of

opening

Nature of

Ownership

JW Marriott Sahar MumbaiSahar Mumbai

14.55 acres

588 Feb-15Freehold 100%

ownership

Bengaluru Marriott Hotel Whitefield

Whitefield,

Bengaluru

9.76 acres

391 Feb-13

Freehold 100%

ownership

The Westin Hyderabad Mindspace

Mindspace,

Hyderabad

3.1 acres

427 Dec-09

Freehold 100%

ownership

Renaissance Mumbai Convention

Centre Hotel and Lakeside Chalet

Powai Mumbai

15 acres

773 Jul-01Freehold 100%

ownership

Four Points By SheratonVashi, Navi

Mumbai

152 Jun-09 Leasehold

Total 2331

Source: Company, ICICI Direct Research

Exhibit 15: Commercial & Retail Portfolio

Project Name LocationLeasable Area (sq ft

in lakhs)

Operational Status Nature of ownership interest

Business Centre Sahar, Mumbai 3.74Leased to WPP Marketing

from September 2019

Freehold, 100% ownership

The Orb - Retail Sahar, Mumbai 1.23 To get operational in FY20E Freehold, 100% ownership

Bengaluru - Commerial Whitefield, Bengaluru 1.09 100% occupied by single tenant Freehold, 100% ownership

Inorbit Mall Bengaluru -

Retail

Whitefield, Bengaluru 2.60 Operational at full capacity Freehold, 100% ownership

Total 8.67

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 9

ICICI Direct Research

Initiating Coverage | Chalet Hotels

Exhibit 16: Current portfolio - A mix of Hospitality and Commercial & Retail assets

Source: Company, ICICI Direct Research

Exhibit 17: Micro-market dynamics and triggers

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 10

ICICI Direct Research

Initiating Coverage | Chalet Hotels

Historical performance of current hotel portfolio

Exhibit 18: Performance of Luxury upper upscale hotels

Particulars FY16 FY17 FY18

Number of keys 1771 2109 2176

ARR (|) 7723 7975 7979

Occupancy rate (%) 58.09% 65.99% 71.70%

RevPAR (|) 4486 5263 5721

Total Operating revenues (| crore) 515.2 631.5 788.4

Total Operating expenses (| crore) 342.7 402.7 471.7

EBITDA 172.5 228.8 316.7

EBITDA (%) 33% 36% 40%

Staff per Room 1.25 1.25 1.21

Source: Company, ICICI Direct Research

Exhibit 19: JW Marriott Mumbai Sahar

Particulars FY16 FY17 FY18

Number of keys (588 keys currenly) 585 585 585

ARR (|) 7735 8259 8499

Occupancy rate (%) 45.72% 65.13% 73.16%

RevPAR (|) 3536 5379 6218

Total Operating revenues (| crore) 149.4 204.8 242.3

Total Operating expenses (| crore) 111.7 135.1 144.6

EBITDA 37.8 69.7 97.7

EBITDA (%) 25% 34% 40%

No of meeting rooms 5 5 5

No of F&B outlets 3 3 3

Source: Company, ICICI Direct Research

Exhibit 20: Bengaluru Marriott Hotel Whitefield

Particulars FY17 FY18

Number of keys 324 391

Occupancy rate (%) 74.32% 76.79%

RevPAR (|) 6665 6619

Total Operating revenues (| crore) 125.4 147.7

Total Operating expenses (| crore) 78.9 80.5

EBITDA 46.4 67.2

EBITDA (%) 37% 46%

No of meeting rooms 2 2

Source: Company, ICICI Direct Research

Exhibit 21: The Westin Hyderabad Mindspace

Particulars FY16 FY17 FY18

Number of keys 427 427 427

ARR (|) 7654 7792 7973

Occupancy rate (%) 65.72% 68.64% 71.41%

RevPAR (|) 5030 5348 5694

Total Operating expenses (| crore) 83.5 86.8 88.9

EBITDA 54.1 58.2 63.7

EBITDA (%) 39% 40% 42%

No of meeting rooms 5 5 5

No of F&B outlets 4 4 4

Source: Company, ICICI Direct Research

Exhibit 22: Renaissance Hotel and Marriott Executive

Apartments

Particulars FY16 FY17 FY18

Number of keys 759 773 773

ARR (|) 7757 7340 7215

Occupancy rate (%) 63.33% 63.83% 69.18%

RevPAR (|) 4913 4685 4991

Total Operating revenues (| crore) 228.2 228.8 245.9

Total Operating expenses (| crore) 147.5 147.0 157.8

EBITDA 80.6 81.8 88.0

EBITDA (%) 35% 36% 36%

No of meeting rooms 9 9 9

No of F&B outlets 6 6 6

Source: Company, ICICI Direct Research

Exhibit 23: Four Points by Sheraton

Particulars FY16 FY17 FY18

Number of keys 150 150 152

ARR (|) 6494 6326 6435

Occupancy rate (%) 86.42% 86.14% 88.10%

RevPAR (|) 5612 5449 5669

Total Operating revenues (| crore) 49.2 49.2 51.1

Total Operating expenses (| crore) 30.6 30.4 29.2

EBITDA 18.6 18.8 22.0

EBITDA (%) 38% 38% 43%

No of meeting rooms 4 4 4

No of F&B outlets 3 3 3

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 11

ICICI Direct Research

Initiating Coverage | Chalet Hotels

Exhibit 24: Upcoming projects

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 12

ICICI Direct Research

Initiating Coverage | Chalet Hotels

Key Managerial Personnel & Directors

Ravi C Raheja – Promoter, Non-Executive Director

Ravi C Raheja is an alumnus of the London Business School with over 25

years’ experience across real estate, hospitality and retail. His multifarious

experience and inherent acumen for judging correctly, has led him to

spearhead business development for the real estate arm of the Group. Mr

Raheja is actively involved in charting the future growth of K Raheja Corp

Group and each of its businesses, while playing a key role in guiding the

hospitality and other divisions of the Group. Mr Raheja has held important

positions on several key forums, such as Mumbai Chairman of the Indian

Green Building Council and member of the World Economic Forum.

Neel C Raheja – Promoter, Non-Executive Director

Neel Raheja is a Graduate in Law from the Mumbai University, and an

alumnus of the Harvard Business School, Boston, Massachusetts. He has

been instrumental in setting up premium hotels in the country for the

company and been the cornerstone in establishing retail brands Shoppers

Stop, Inorbit Mall and Crossword. He is co-chair at CII National Committee

on Real Estate and Housing, Chairman, India Chapter of APREA, and was

President, NAREDCO West. He is also Vice Chairman of CORENET, and

Advisory Committee member of MCHI-CREDAI. Mr Raheja has been

appointed on the Government of India Committee to suggest changes in the

Special Economic Zone policy.

Sanjay Sethi – MD & CEO

Sanjay Sethi is a hotel management graduate from IHM Pusa. He is a

Certified Hotel Administrator (CHA) from American Hotel and Lodging

Educational Institute and has completed various management certifications

from IIM-Bangalore, XLRI and Cornel. He has over 30 years of experience

with leading Indian hotel chains, and across segments. Prior to joining

Chalet, Sanjay set up Berggruen Hotels in 2006 as promoter CEO and MD

along with Berggruen Holdings, New York. He worked with ITC Ltd as Chief

Operating Officer of their hotels division and The Indian Hotels Company as

a general manager to their hotel properties and area director for their

Hyderabad hotels.

Rajeev Newar – Executive Director and CFO

Rajeev Newar is a Chartered Accountant, Company Secretary and Bachelor

of Commerce (Honours) from Calcutta University. Over the past 27 years,

Mr Newar has held several leadership positions in finance. Prior to joining

Chalet Hotels, he was Vice President Finance with The Indian Hotels

Company and a Director on the Board of some of its subsidiaries. He has

been recognized on various forums and recently received recognition of

excellence at the CFO India Conference, 2019.

Hetal Gandhi - Chairman and Independent Director

Hetal Gandhi is a Chartered Accountant and has a bachelor’s degree in

commerce from the University of Mumbai. He is the co-founder and

managing director of Tano India Advisors Pvt Ltd (TIA). TIA is the India sub-

advisor for private equity funds set up and managed by Tano Capital, US for

investing in Indian companies. He was previously associated with a

diversified financial services company as its Head - Financial Services and

with Orix Auto and Business Solutions as its Chief Executive Officer. He has

over 31 years of experience in the financial services industry. Mr Gandhi has

been on the Board of Chalet since March 20, 2003 and was appointed an

Independent Director and Chairman of the company with effect from June

12, 2018.

ICICI Securities | Retail Research 13

ICICI Direct Research

Initiating Coverage | Chalet Hotels

Investment Rationale

Hospitality company but with DNA of real estate developer

Chalet Hotels is a part of the K Raheja Corp Group whose group companies

have extensive experience in developing large scale real estate and

commercial projects resulting in a strong understanding of the industry that

the company uses to identify suitable locations and opportunities. The

company also leverages this experience and relationships of these

companies with construction companies to develop hotels at optimal cost

and quality. With large FSI available on the lands along with effective design,

the company is able to construct hotels at costs and size per room that are

among the lowest in the industry.

Exhibit 25: Cost of setting-up a new hotel one of the lowest in industry

Hotel Location Number of keys Cost per room (| crore)

JW Marriott Sahar, Mumbai 577 1.4

ITC Royal Bengal Kolkata 456 3.1

ITC Narmada Ahmedabad 300 2

ITC Kohenur Hyderabad 271 2.9

Oberoi Rajgarh Dattia, MP 60 3.3

Source: Company, ICICI Direct Research

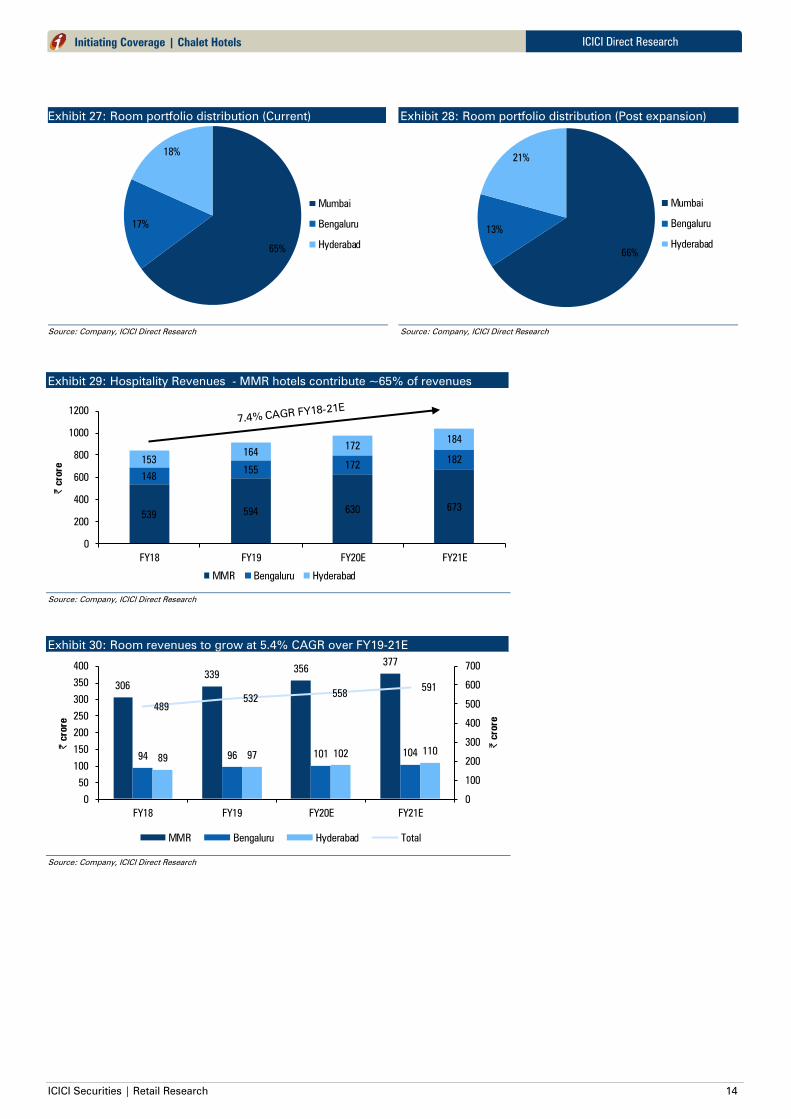

Capacity addition – MMR to remain dominant part of portfolio

Chalet plans to enhance its hospitality portfolio by 25% from the current

number of rooms. The company would be adding two hotels in MMR and

one in Hyderabad, all of which are expected to commence operations in

CY21. Further, to leverage additional FSI at some of its hotels, the company

has adopted the hotel-led mixed-use project development. Chalet is

currently developing commercial space in Powai, Mumbai along with an IT

Park in Whitefield, Bengaluru on unutilized land at the current hotels. In

CY21, the company would, thus, be adding 580 rooms across three hotels

and commercial projects with a leasable space of ~11 lakh sq.ft (Refer

exhibit 35). Thus, with additional assets getting into operations during CY21,

we expect the pace of revenue growth to increase to double digits in FY21E-

23E. Currently, out of 2331 keys, 1513 are in the MMR region (64.9% of the

room portfolio). Post expansion of the hotels portfolio, 1923 rooms would

be in the MMR region (66% of total room portfolio)

Exhibit 26: Upcoming pipeline of rooms

Location of Hotel No of rooms Expected Opening Ownership Interest Proposed brand

Hyderabad 170.0 Apr-2021 Leasehold rights Westin

Airoli, Navi Mumbai 260.0 Sep-2021 Leasehold rights Hyatt Regency

Powai, Mumbai 150.0 Sep-2021 100% ownership 'W'

Total 580.0

Total post expansion 2911.0

Hotels under development

Source: Company, ICICI Direct Research

JW Mariott Sahar, Mumbai was completed in FY15

at a cost of | 1.4 crore per room including land costs

According to the management estimates, funding all

the expansion (hotels and commercial spaces) will

entail a capital outlay of ~| 1250 crore and will be

spent over 3 years in the ratio of 25:35:45.

ICICI Securities | Retail Research 14

ICICI Direct Research

Initiating Coverage | Chalet Hotels

Exhibit 27: Room portfolio distribution (Current)

65%

17%

18%

Mumbai

Bengaluru

Hyderabad

Source: Company, ICICI Direct Research

Exhibit 28: Room portfolio distribution (Post expansion)

66%

13%

21%

Mumbai

Bengaluru

Hyderabad

Source: Company, ICICI Direct Research

Exhibit 29: Hospitality Revenues - MMR hotels contribute ~65% of revenues

539594 630 673

148155

172182153

164172

184

0

200

400

600

800

1000

1200

FY18 FY19 FY20E FY21E

| crore

MMR Bengaluru Hyderabad

Source: Company, ICICI Direct Research

Exhibit 30: Room revenues to grow at 5.4% CAGR over FY19-21E

306

339356

377

94 96 101 10489 97 102 110

489

532558

591

0

100

200

300

400

500

600

700

0

50

100

150

200

250

300

350

400

FY18 FY19 FY20E FY21E

| crore

| crore

MMR Bengaluru Hyderabad Total

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 15

ICICI Direct Research

Initiating Coverage | Chalet Hotels

Exhibit 31: F&B revenues to grow at 8% CAGR over FY19-21E

234

255272

294

53 5970 76

64 67 70 76

351

382

412

445

0

100

200

300

400

500

0

50

100

150

200

250

300

350

FY18 FY19 FY20E FY21E

| crore

| crore

MMR Bengaluru Hyderabad Total

Source: Company, ICICI Direct Research

Exhibit 32: ARRs to increase at 4% CAGR over FY19-21E

Average Room rate (|) FY18 FY19 FY20E FY21E

MMR 7634 8086 8369 8746

Bengaluru 8620 8756 9062 9380

Hyderabad 7973 8205 8533 8917

Combined 7862 8220 8515 8883

Source: Company, ICICI Direct Research

Exhibit 33: Occupancy rates to improve marginally over in

FY19-21E

Occupancy (%) FY18 FY19 FY20E FY21E

MMR 72.6% 76.0% 77.0% 78.2%

Bengaluru 76.8% 77.0% 78.0% 78.0%

Hyderabad 71.4% 76.0% 76.5% 78.8%

Combined 73.1% 76.2% 77.1% 78.3%

Source: Company, ICICI Direct Research

Exhibit 34: RevPAR to cross | 7500 by FY21E at 9.6% CAGR over FY19-21E

5,540

6,150

6,440

6,840

6,620

6,740

7,070

7,320

5,690

6,240

6,530

7,030

5,750

6,260 6,560

6,950

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY18 FY19 FY20E FY21E

||

MMR Bengaluru Hyderabad Combined

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 16

ICICI Direct Research

Initiating Coverage | Chalet Hotels

Commercial & retail segment revenue share to increase

Out of the existing capacity of ~8.7 lakh sq.ft. of commercial & retail assets,

~5 lakh sq.ft (The Orb and Business Centre, Sahar) to begin generating

revenues from FY20E (Refer Exhibit 15). Thus, the share in total revenues

(ex-real estate revenues) of the C&R segment is expected to improve from

2.8% of revenues in FY16 to a little over 8% by FY21E. We expect revenues

of this segment to grow at 58% CAGR in FY18-21E to | 95 crore with

occupancy levels near 90% by FY21E. Additionally, the company has a

pipeline of ~11 lakh sq.ft of commercial assets in Bengaluru and Mumbai.

Since these assets are expected to come on stream from FY22, we have not

built in revenues projections for the same in our model.

Exhibit 35: Upcoming Commercial & Retail assets

Project name Location

Total Built-up area

(sq. ft. in lakh)

Expected

Opening Nature of ownership interest

IT Building Phase II Bengaluru 4.0 Mar-2021 Freehold, 100% ownership

Powai Office Block Mumbai 7.0 Sep-2021 Freehold, 100% ownership

Total 11.0

Total post expansion 19.7

Commercial Projects under Development

Source: Company, ICICI Direct Research

Exhibit 36: The Orb and Business Centre to be leased from

FY20E

0.37

0.87 0.87 0.87

0.00

0.20

0.40

0.60

0.80

1.00

FY18 FY19 FY20E FY21E

million s

q. ft

Leasable area Leased area

Source: Company, ICICI Direct Research

Exhibit 37: Revenues from C&R segment to grow at 56%

CAGR over FY19-21E

23 24

39

67

95

90%92%

40%

65%

88%

0%

20%

40%

60%

80%

100%

0

20

40

60

80

100

FY17 FY18 FY19 FY20E FY21E

%

| crore

Revenues (| crore) Occupancy (%)

Source: Company, ICICI Direct Research

Exhibit 38: Share of C&R division to grow to 8.4% of revenues (ex real estate)

0%

20%

40%

60%

80%

100%

FY16 FY17 FY18 FY19 FY20E FY21E

Hospitality Commercial & Retail

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 17

ICICI Direct Research

Initiating Coverage | Chalet Hotels

Most profitable player in industry

None of the hotels owned by Chalet are managed by itself. It signs

management contract agreements with third parties to manage their hotels

and pays fees for the same that add up to ~8%-9% of total revenues.

Further, for a better performance, the company follows an active asset

management model where Chalet engages with the hotel management team

at each hotel to discuss budgeting, cost management initiatives and

operational & financial targets. The company also reviews the performance

of each hotel, conducts periodic meeting with the hotel management team,

holds discussion on pricing, renovation, etc. Chalet also optimises its

employee costs, which is among the biggest fixed costs of any hotel

company. The staff per room at the company’s hotels managed by third

parties at its luxury upper upscale and upscale properties as on March 31,

2017, were at 1.25 and 1.38, respectively, while the same for the industry

was at ~2 employees per room. Thus, owing to the above and despite not

having any management contract income, Chalet has been reporting highest

EBITDA margins among its listed peers.

Exhibit 39: Industry leader in terms of EBITDA margins

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

FY16 FY17 FY18 FY19 FY20E FY21E

(%

)

Chalet Hotels Indian Hotels EIH Limited TajGVK Hotels & Resorts

Source: Company, ICICI Direct Research

Exhibit 40: RoCE to improve over the coming years

12.5

7.0

8.9

10.010.9

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

FY17 FY18 FY19 FY20E FY21E

%

RoCE

RoCE

Includes significant non-recurring income

Source: Company, ICICI Direct Research

Exhibit 41: Industry best margins trend to continue

30.1

30.8

32.3

35.5

36.9

25.0

27.0

29.0

31.0

33.0

35.0

37.0

39.0

FY17 FY18 FY19 FY20E FY21E

%

EBITDA margins

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 18

ICICI Direct Research

Initiating Coverage | Chalet Hotels

Exhibit 42: Industry Tailwinds & Company Strength

Source: Company, ICICI Direct Research

Balance sheet to strengthen led by improving cash flows

From the IPO proceeds received in February, the company reduced its debt

significantly by cutting down on some of its long term as well as foreign

currency debt (thus reducing forex risk). The company repaid ~| 1370 crore

of debt during the year, and the foreign currency borrowing has reduced

significantly from $75.85 million as at the end of FY18 to $26.11 million by

the end of FY19. With these repayments, the Debt/EBITDA and D/E have

reduced to 4.8x and 1.1x, respectively, by the end of FY19. Going ahead,

Chalet would be spending ~| 1250 crore in the next two years to fund the

ongoing expansions of its hospitality and commercial assets. Higher cash

flows from the already operational properties and leasing out of Business

Centre Sahar & The Orb, are expected to result in an EBITDA CAGR of 15%

over FY19-21E. This is expected to lead to a reduction in debt/EBITDA further

to 4.5x by FY21E despite total debt rising from | 1546 crore in FY19 to ~|

1900 crore in FY21E.

Exhibit 43: D/E to remain stable over the next two years

5.6 5.5

1.1 1.0 1.1

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

FY17 FY18 FY19 FY20E FY21E

(x

)

Debt / Equity (x)

Source: Company, ICICI Direct Research

Exhibit 44: Debt/EBITDA set to improve led by ramp-up of

commercial & retail assets

12.4

11.1

4.84.2 4.5

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

FY17 FY18 FY19 FY20E FY21E

(x

)

Debt / EBITDA (x)

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 19

ICICI Direct Research

Initiating Coverage | Chalet Hotels

Ownership Summary

Exhibit 45: Top 10 Shareholders

Rank Name Last filing date % O/S Position (m) Change (m)

1 Casa Maria Properties L.L.P 30-Jun-19 8% 16.5 0.00

2 Raghukool Estate Development L.L.P. 30-Jun-19 8% 16.5 0.00

3 Capstan Trading L.L.P 30-Jun-19 8% 16.5 0.00

4 K Raheja Corporation 30-Jun-19 8% 16.2 0.00

5 Touchstone Properties and Hotels Pvt. Ltd. 30-Jun-19 7% 14.5 0.00

6 Cape Trading L.L.P 30-Jun-19 6% 13.1 0.00

7 Anbee Construction L.L.P. 30-Jun-19 6% 13.1 0.00

8 Ivory Properties & Hotels Pvt. Ltd. 30-Jun-19 6% 11.4 0.00

9 Reliance Nippon Life Asset Management Ltd 30-Jun-19 5% 11.2 0.47

10 Raheja (Neel Chandru) 30-Jun-19 5% 10.3 0.00

Source: Company, ICICI Direct Research, Thomson Reuters

Exhibit 46: Recent Activity

Investor NameValue

($mn)

Shares

(mn)

Investor NameValue

($mn)

Shares

(mn)

Reliance Nippon Life Asset Management Limited 2.15 0.47 Macquarie Funds Management Hong Kong Ltd. -0.73 -0.16

UTI Asset Management Co. Ltd. 1.00 0.22 SBI Funds Management Pvt. Ltd. -0.39 -0.08

Kuwait Investment Authority 0.92 0.20

FIL Investment Management (Australia) Limited 0.49 0.11

Fidelity International Asset Management Company (Korea) 0.30 0.06

Buys Sells

Source: Company, ICICI Direct Research, Thomson Reuters

Exhibit 47:

(in %) Feb-19 Mar-19 Jun-19 Sep-19

Promoter 71.41 71.41 71.41 71.41

FII 11.46 10.05 9.82 9.42

DII 10.99 15.87 16.08 17.69

Others 6.14 2.67 2.69 1.48

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 20

ICICI Direct Research

Initiating Coverage | Chalet Hotels

Risks & Concerns

Geographical concentration

A significant portion of the company’s revenues are derived from hotels

concentrated in a few geographical regions. Any adverse developments

impacting such hotels or regions could have an adverse effect on the

company’s business and operations.

Economic risks

The company operates in the luxury-upper upscale and upscale hotel

segments in India where the demand from business and MICE travelers is

highly dependent on the general economic performance in India. There has

been a history of rise and decline in demand for hotel rooms, in occupancy

levels and rates realized by owners and operators of hotels through

macroeconomic cycles. Variability of results through some of the cycles in

the past has been more severe due to changes in supply of hotel rooms.

Any future slowdown in economic growth could affect business and

personal discretionary spending levels, and lead to a decline in demand.

Relationship with hotel operators, leading hospitality brands

The company utilizes the brands of hotel operators and brand licensor to

operate and market the hotels. The company’s hotels are generally obliged

to pay periodic management fees, royalty fees, fees for technical services

and reimbursements for advertisement, marketing, promotion, sales &

software, among others. These payments to hotel operators and brand

licensors are based on a fixed percentage of gross revenue of the hotel as

well as a portion of gross operational profits, subject to certain exclusions

and adjustments. Any revision in the terms putting Chalet Hotels at a

disadvantage could severely impact the business. Also all the hotels

currently are managed by a single entity, Marriott International (along with

its affiliates). Deterioration in the relation with the entity or non-renewal of

contracts could have an impact on our estimates

Competition

Chalet operates in a highly competitive industry with success dependent on

its ability to compete on various factors such as attractiveness and quality

of its offerings, quality of accommodation, food & beverage, location, service

levels and amenities, together with the brand reputation of its brand

licensors. The company may also have to compete with any new hotel

properties that commence operations in the market in which it operates or

intend to commence operations.

Litigation of Bengaluru Residential Project

The company owns a property situated at Koramangala Industrial Layout,

Bengaluru where the company is developing a residential complex. While,

the project had received NOC from Hindustan Aeronautics Limited in 2011,

the same was cancelled in August 2013. Chalet Hotels filed a writ petition

before the Karnataka High Court challenging the same; the project continues

to remain under litigation. The company had already impaired the project by

~| 35 crore and also has made provisions for alterations (| 25 crore) and

refund/ compensation to the home buyers (~| 42 crore). To meet any costs,

expenses or liabilities towards the project, the promoters have subscribed

to 20000 non-cumulative non-convertible preference shares of ~| 1,00,000

each, aggregating to | 200 crore. Any fund requirement over this amount

would also be funded by the promoters in the future, if required. An adverse

order from the Karnataka High Court or penalties under RERA for non-

compliance could affect the company’s business and reputation.

ICICI Securities | Retail Research 21

ICICI Direct Research

Initiating Coverage | Chalet Hotels

Litigation of Vashi hotel land

The land where Chalet Hotels operates the Vashi, Navi Mumbai Hotel is a

leasehold land, allotted to K. Raheja Corp Private Limited (KRCPL) by CIDCO.

The allotment of land has been challenged by two public interest litigations

filed with the Bombay High Court, whereby the allotment was held illegal

and directed KRCPL to hand over the vacant possession of land to CIDCO.

KRCPL has filed a special leave petition with the Supreme Court and the

court has asked the parties to maintain status-quo and the SLP is currently

pending before the Supreme Court. The hotel has 152 rooms, ~7% of the

total rooms and has been operating at a healthy occupancy of above 85%

since 3 years and reporting a healthy performance. The carrying value of the

leasehold rights (already paid for) and hotel assets as on 31st March 2019

stood at ~| 50 crore. While we have assumed normalcy, adverse order by

the Supreme Court directing demolition of the hotel and handing over

possession of the premises to CIDCO could negatively impact our estimates.

ICICI Securities | Retail Research 22

ICICI Direct Research

Initiating Coverage | Chalet Hotels

Valuation & Outlook

Chalet Hotels has a strong presence in dense business districts with assets

strategically located in core business districts in the respective micro-

markets. Mumbai and Hyderabad are expected to see scarce growth in room

supply, which should augur well for occupancies and, hence, ARRs. Further,

association with leading hospitality player to manage its properties

combined with real estate expertise in selection of location and cost effective

construction will enable the company in achieving industry best returns and

profitability. Recent announcement of GST rate revision for hotels, is a shot

in the arm for the hospitality industry. Additionally, corporate tax cuts would

also help Chalet Hotels, as the company’s properties are located in major

business districts and corporate clients form a significant chunk of the total

revenue pie.

Debt, which was a concern, has been sliced significantly from internal

accruals and the proceeds from fresh issue of equity shares. The company

raised | 950 crore via IPO and utilized most proceeds to reduce its total debt,

thus slicing its debt/EBITDA from 11.1x in FY18 to 4.8x in FY19, which is

further expected to come down to 4.5x by FY21E despite capacity addition

plans. While improvement in profitability and debt coverage is expected, the

current hospitality portfolio has a limited room for growth. The current

pipeline of hotel and commercial assets should be the major growth triggers

going ahead, but are expected to start contributing to the company’s

performance from FY22E only. As the company is under the capex mode

we foresee limited upside and assign a HOLD rating to the company valuing

it at EV/EBITDA multiple of 21x on FY21E earnings. Thus we arrive at a target

price of | 350/share, implying an EV/room of ~| 4 crore.

ICICI Securities | Retail Research 23

ICICI Direct Research

Initiating Coverage | Chalet Hotels

Financial Summary

Exhibit 48: Profit & Loss Statement

(Year-end March) FY18 FY19 FY20E FY21E

Total operating Income 796 987 1052 1146

Growth (%) 12.7 24.1 6.6 8.9

Raw Material Expenses 76 137 144 154

Employee Expenses 128 145 156 169

Other Exp 347 386 378 400

Total Operating Expenditure 551 668 678 723

EBITDA 245 319 374 423

Growth (%) 15.3 30.4 17.2 13.1

Depreciation 112 115 136 136

Interest 212 266 139 119

Other Income 55.7 47.6 45.0 45.0

PBT -23.1 -14.3 143.5 212.9

Others -122 -4 0 0

Total Tax -52 -11 0 0

Reported PAT -93 -8 144 213

Adjusted PAT -15 -6 144 213

Growth (%) NA NA NA 48.3

EPS (|) -4.5 -0.4 7.0 10.4

Source: Company, ICICI Direct Research

Exhibit 49: Cash Flow Statement

(Year-end March) FY18 FY19 FY20E FY21E

Profit after Tax -92.9 -7.6 143.5 212.9

Add: Depreciation 111.6 115.4 136.4 136.1

(Inc)/dec in Current Assets 89.3 -76.4 -13.1 -6.1

Inc/(dec) in CL and Provisions -127.5 125.8 -15.1 10.6

CF from operating activities 76.5 331.9 345.9 427.6

(Inc)/dec in Investments 15.5 25.5 -216.2 -545.9

(Inc)/dec in Fixed Assets -62.1 -43.6 -55.3 -51.1

Others -78.1 233.7 3.8 -4.6

CF from investing activities -124.7 215.7 -267.7 -601.5

Issue/(Buy back) of Shares 117.2 937.5 -33.9 0.0

Inc/(dec) in loan funds 89.4 -1179.3 43.2 310.0

Dividend paid & dividend tax 0.0 0.0 0.0 0.0

Others -211.9 -265.7 -139.1 -119.2

CF from financing activities -5.2 -507.4 -129.8 190.8

Net Cash flow -1.5 51.0 -51.6 16.9

Opening Cash 33.2 31.7 82.6 31.0

Closing Cash 31.7 82.6 31.0 47.9

Source: Company, ICICI Direct Research

Exhibit 50: Balance Sheet

(Year-end March) FY18 FY19 FY20E FY21E

Liabilities

Equity Capital 171 205 171 171

Reserve and Surplus 324 1218 1361 1574

Total Shareholders funds 496 1425 1535 1748

Total Debt 2725 1546 1589 1899

Deferred Tax Liability 64 29 29 29

Minority Interest / Others 22 41 46 51

Total Liabilities 3306 3042 3199 3727

Assets

Gross Block 3558 3566 3725 4134

Less: Acc Depreciation 763 836 951 1067

Net Bloack 2795 2730 2773 3067

CWIP 22 34 151 342

Total Fixed Assets 2817 2764 2924 3409

Intangibles 24 23 22 21

Investments 9 10 10 10

Inventory 312 395 402 403

Debtors 55 48 55 60

Loans and Advances 235 2 2 2

Other Current Assets 72 72 68 73

Cash 32 83 31 48

Total Current Assets 706 599 557 585

Creditors 86 122 115 123

Provisions & Others 324 397 383 381

Total Current Liabilities 410 518 498 504

Net Current Assets 296 81 59 81

Others Assets 160 163 185 207

Application of Funds 3306 3042 3199 3727

Source: Company, ICICI Direct Research

Exhibit 51: Key Ratios

(Year-end March) FY18 FY19 FY20E FY21E

Per share data (|)

EPS -0.7 -0.3 7.0 10.4

Cash EPS 0.9 5.3 13.7 17.0

BV 24.2 69.4 74.7 85.1

DPS 0.0 0.0 0.0 0.0

Cash Per Share 1.5 4.0 1.5 2.4

Operating Ratios (%)

EBITDA Margin 30.8 32.3 35.5 37.0

EBIT Margin 23.7 25.5 26.9 29.0

PAT Margin -11.7 -0.8 13.6 18.6

Inventory days 169 131 138 128

Debtor days 19 19 18 18

Creditor days 39 38 41 38

Return Ratios (%)

RoE -19.2 -0.8 9.7 13.0

RoCE 7.0 8.9 10.0 10.9

RoIC 7.3 8.2 9.4 11.1

Valuation Ratios (x)

P/E NM NM 48.6 32.7

EV / EBITDA 39.5 26.4 22.8 20.8

EV / Net Sales 12.1 8.5 8.1 7.7

Market Cap / Sales 8.8 7.1 6.6 6.1

Price to Book Value 14.1 4.9 4.5 4.0

Solvency Ratios

Debt/EBITDA 11.1 4.8 4.2 4.5

Debt / Equity 5.5 1.1 1.0 1.1

Current Ratio 0.8 0.8 0.6 0.6

Quick Ratio 0.4 0.3 0.2 0.2

Source: Company, ICICI Direct Research

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

Init

iatin

g C

overage

October 24, 2019

CMP: | 58 Target: | 73 (25%) Target Period: 12 months

Lemon Tree Hotels (LEMTRE)

BUY

Leader in mid-market category upping its game

Lemon Tree Hotels is predominantly a midscale hotel player with a presence

in the economy and upper midscale as well. The company’s current

inventory of 5970 rooms (owned/leased and managed) is spread across 58

hotels in 35 cities. With ~11.8% share in the mid-market category, Lemon

Tree aims to consolidate a significant room inventory in the unbranded

category into the branded segment. The company plans to add rooms in the

upper-midscale (Lemon Tree Premier) and would also be entering the

upscale category in Mumbai and Udaipur with its new brand Aurika. While

the ongoing room addition plans (owned rooms) would require the

company to raise debt, it has also been leveraging its brand and adding

more rooms via management contracts (from 1841 rooms in FY19 to 4803

rooms by FY22E). With higher profitability, going ahead, led by management

contract and addition of upper-midscale and upscale hotels, debt/EBITDA is

expected to improve from 7.1x in FY19 to 5.1x by FY21E. We initiate

coverage on Lemon Tree with a BUY rating and target price of | 73.

Room inventory to cross 10000 mark by FY22E

Currently, Lemon Tree Hotels has a portfolio of 5970 rooms (owned/leased

and managed) across economy, midscale and upper-midscale. Over the

next three years, the company would be adding over 4680 rooms with a mix

of owned and management contract (Refer exhibit 57). With increasing share

of upper-midscale and upscale hotels, we expect ARRs to grow at 10.5%

CAGR in FY19-21E. Thus, we expect revenues to grow to | 940 crore by

FY21E, at a CAGR of 31% over FY19-21E.

Addition of high-end properties to further strengthen margins

Lemon Tree Hotels has a better cost structure than the industry with

operating costs being ~20% lower than the comparable peers in the

respective segment (Refer Exhibit 73). Additionally, out of the current

portfolio of owned & leased hotels, over ten hotels have been operational

for less than three years. Post stabilisation, these are expected to exhibit

strong improvement in RevPARs (Refer Exhibit 70, 72). With entry into the

dense markets of Mumbai with upper-midscale property and in the upscale

segment (Aurika MIAL, Aurika Udaipur), ARRs of the company are expected

to increase significantly from FY21E. Also, management contract income

will provide an additional fillip to profitability and returns. Hence, over FY19-

21E, we expect EBITDA to grow at 39% CAGR to | 326 crore.

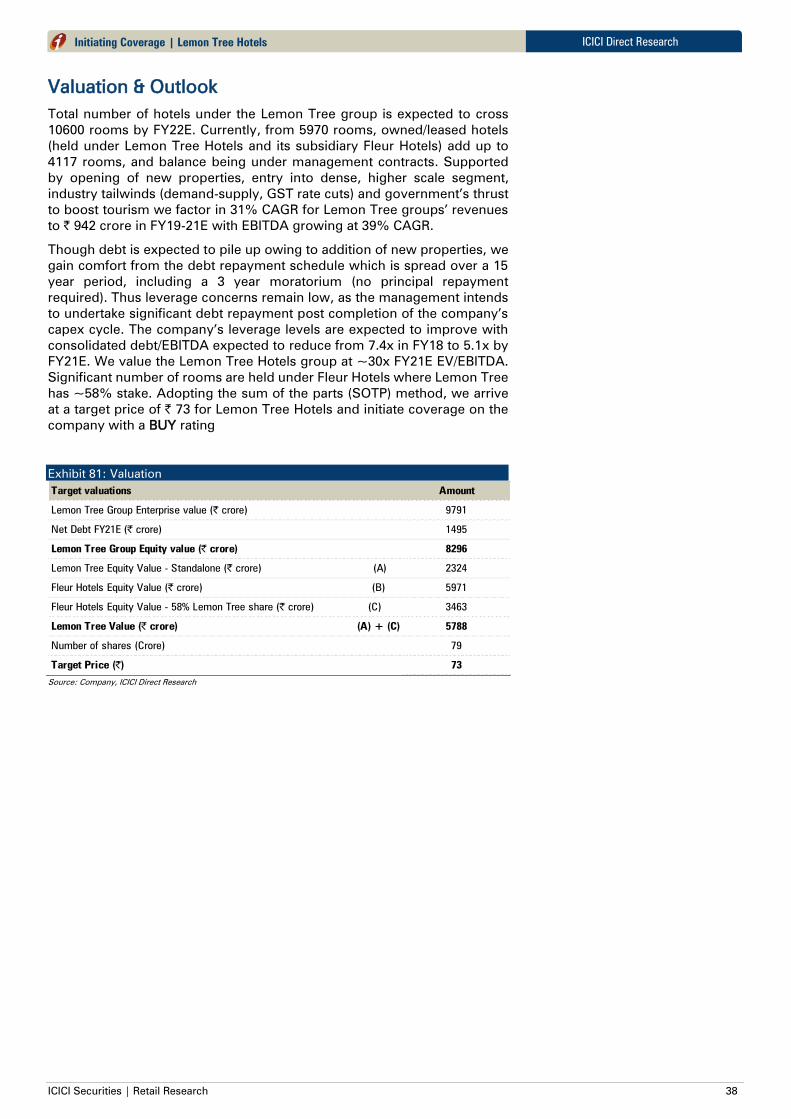

Valuations & Outlook

The hospitality industry to continue to witness uptrend on the back of

improving demand, limited capacity addition and the government’s thrust

to boost tourism. Lemon Tree with its widespread portfolio is well poised to

benefit from the improving industry scenario. Though debt is expected to

pile up owing to addition of new properties, leverage concerns remain low

as significant debt repayment is expected to commence post completion of

the company’s capex cycle. We initiate coverage on the company with a

BUY rating and a target price of | 73.

Key Financial Summary

Key Financials FY17 FY18 FY19 FY20E FY21E CAGR (FY19-21E)

Net Sales 412 484 550 786 940 30.8%

EBITDA 116 136 169 263 326 39.1%

EBITDA (%) 28.3 28.1 30.7 33.5 34.7

PAT (Adj) -5.1 14.6 56.4 73.4 100.2 33.3%

EPS (|) -0.1 0.2 0.7 0.9 1.3

EV/EBITDA 46.3 41.1 34.2 23.4 18.7

RoNW (%) -0.6 1.8 6.7 8.1 10.1

RoCE (%) 3.9 4.6 5.5 6.8 7.8

Source: ICICI Direct Research, Company

Stock Data

Particulars Amount

Market Capitalization (| crore) 4609

Debt (FY19) (| crore) 1196

Cash & Investment (FY19) (| crore) 60

EV (| crore) 5774

52 week H/L | 89/47

Equity Capital (FY19) (| crore) 789

Face Value | 10

Price Chart

0

5,000

10,000

15,000

0

20

40

60

80

100

Oct-19

Jul-19

Apr-19

Jan-19

Oct-18

Jul-18

Apr-18

Jan-18

Oct-17

Aug-17

May-17

Feb-17

Nov-16

Price (R.H.S) Nifty (L.H.S)c

Key Highlights

Lemon Tree to add in excess of 4820

rooms over next three years

Keys Hotels acquisition to be

completed in H2FY20E

Stepping into upscale category and

also into student housing and co-living

Debt coverage to improve led by

stabilisation of hotels

Initiate coverage with BUY rating and

target price of | 73 per share

Research Analyst

Rashesh Shah

Romil Mehta

ICICI Securities | Retail Research 25

ICICI Direct Research

Initiating Coverage | Lemon Tree Hotels

Company Background

Exhibit 52: Lemon Tree History

Source: Company, ICICI Direct Research

Exhibit 53: Group ownership structure

Source: Company, ICICI Direct Research

Exhibit 54: Hotel inventory by segment and Lemon Tree brand position

Source: Company, ICICI Direct Research

Company aims to target unbranded 2 million rooms

and bring them into the branded space

ICICI Securities | Retail Research 26

ICICI Direct Research

Initiating Coverage | Lemon Tree Hotels

Inventory growth and current portfolio

Exhibit 55: Lemon Tree current portfolio of hotels

Brand Rooms Hotels

Lemon Tree Premier 2142 15

Lemon Tree Hotels 2506 33

Red Fox Hotels 1322 11

Total 5970 59

Source: Company, ICICI Direct Research

Exhibit 56: Added rooms at 17.9% CAGR in FY15-19

2801

3249

3698

4870

5411

0

1000

2000

3000

4000

5000

6000

FY15 FY16 FY17 FY18 FY19

Total Rooms

Source: Company, ICICI Direct Research

Key Managerial Person and Senior Management

Patanjali Govind Keswani – Chairman and Managing Director

Mr Keswani has a bachelor’s degree in electrical engineering from the Indian

Institute of Technology, New Delhi and a post-graduate diploma degree in

management from the Indian Institute of Management, Calcutta. He was a

Tata Administrative Services Officer and associated with the Taj Group of

hotels for 17 years, including as the SVP (special projects). Mr Keswani was

also associated with AT Kearney Ltd, New Delhi as its associated consultant

and director. At present, he is also the chairman of the Skill Council for

Persons with Disability and a founding member of the Sector Skill Council

for the hospitality, travel and tourism industry.

Rattan Keswani – Deputy Managing Director

Mr Keswani has a Bachelor’s degree in electrical engineering from Indian

Institute of Technology, New Delhi. He also has a postgraduate diploma

degree in management from Indian Institute of Management, Calcutta. He

was a Tata Administrative Services officer & Associated with Taj Group of

Hotels for 17 years, including SVP (Special Projects). He has also worked

with AT Kearney, New Delhi as its associate consultant and director.

Vikramjit Singh – President

Mr Singh has a Bachelor’s degree in Commerce from the University of Delhi

and a postgraduate diploma degree in Hotel Management and

Administration from the Taj Group of Hotels. He was appointed the Chief

Sales Officer with effect from May 21, 2014. Prior to this, he was an

entrepreneur. He has 21 years of experience in the hospitality industry.

Kapil Sharma – CFO

Mr Sharma has a Bachelor’s degree in Commerce from the University of

Delhi and is a qualified Chartered Accountant. He was appointed as the DGM

(Finance) with effect from December 1, 2004 and was designated as the CFO

with effect from September 18, 2014. Prior to this, he was with Leroy Somer

& Controls India Pvt Ltd as the head of Finance and Accounts and managed

the finance and accounts division with commercial responsibilities. He has

previously also worked with AFL Ltd as its Assistant Manager (finance) and

with Onida Finance Ltd as its manager. He has more than 22 years of

experience in the field of finance.

ICICI Securities | Retail Research 27

ICICI Direct Research

Initiating Coverage | Lemon Tree Hotels

Davander Tomar - Executive Vice-President, Corporate Affairs

Mr Tomar, age 56 years, has a Bachelor’s degree in Commerce from the

University of Delhi, a Bachelor’s degree in Law from the University of Delhi

along with a master’s degree in arts from the University of Delhi. He was

appointed the vice president, security and administration with effect from

September 25, 2002. He has previously also worked with Taj Group of Hotels

as the security manager of Taj Palace Hotel, New Delhi for 18 years. He has

over 30 years of experience in the hospitality industry.

JK Chawla – Executive VP Projects & Engineering Services

Mr Chawla has a diploma degree in electrical engineering from Pusa

Polytechnic, New Delhi. He was appointed the VP– Projects and Engineering

with effect from November 2002. Prior to this, he was with the Taj Group of

Hotels for 20 years. He has previously also worked with NTPC, Bharti Electric

Steel Company Ltd and Mother Dairy while holding various positions. He

has more than 40 years of experience in the field of engineering,

constructions and operations.

ICICI Securities | Retail Research 28

ICICI Direct Research

Initiating Coverage | Lemon Tree Hotels

Investment Rationale

Acquisition fuels strong pipeline of rooms

Lemon Tree, which currently has a portfolio of 5970 rooms (as of October

2019), would be adding ~4680 rooms both owned/leased and management

contract over 49 hotels in the next three years taking total count to 10651

rooms and 107 hotels. Out of the 4680 rooms to be added, 2962 would be

added under management contract, taking total rooms under management

contracts to 45% of the entire room portfolio. Further, the company, via its

subsidiary would be acquiring 100% stake in Berggruen Hotels Pvt Ltd,

which owns and manages 1910 rooms under the Keys brand (Refer Exhibit

60) for an EV of | 605 crore (debt - | 134 crore). The company launched its

303 room Lemon Tree Premier Mumbai Hotel that started operations from

Q2FY20 and Lemon Tree Premier, Kolkata a 142 room hotel has been

opened for guests from mid-October 2019. The company is also entering

the upscale segment and would be setting up two hotels under its new brand

“Aurika”, one each in Mumbai and Udaipur, totalling to 716 rooms (the

company is in the process of converting some commercial spaces, which

would further add 92 rooms to the Aurika Mumbai inventory). Lemon Tree

Hotels is expected to end FY22 with an owned/leased room inventory of

5848 rooms (Refer exhibit 64)

Exhibit 57: Total room portfolio to cross 10000 rooms

28013249

3689

48705411

8637

982010651

-500

1000

2500

4000

5500

7000

8500

10000

11500

13000

FY15 FY16 FY17 FY18 FY19 FY20E FY21E FY22E

Owned Leased Managed

Source: Company, ICICI Direct Research

Exhibit 58: Owned/leased rooms inventory to increase at

17.9% CAGR over FY19-22E

25272788 2855

32773570

5192 5192

5848

0

1000

2000

3000

4000

5000

6000

7000

FY15 FY16 FY17 FY18 FY19 FY20E FY21E FY22E

Number of rooms

Source: Company, ICICI Direct Research

Exhibit 59: Managed rooms to grow to 4803 rooms at a CAGR

of 37.7% over FY19-22E

274461

843

15931841

3445

46284803

0

1000

2000

3000

4000

5000

6000

FY15 FY16 FY17 FY18 FY19 FY20E FY21E FY22E

Number of rooms

Source: Company, ICICI Direct Research

Aurika, Udaipur

Aurika, MIAL (Representative Image)

Aurika, MIAL (Under construction)

ICICI Securities | Retail Research 29

ICICI Direct Research

Initiating Coverage | Lemon Tree Hotels

Exhibit 60: Keys brand to be used to consolidate unbranded hotel market

Keys Hotels

1910 rooms

(EV - | 605 crore)

Management contract -

974 rooms (14 cities)

Owned/Leased - 936 rooms

(6 cities)

Source: Company, ICICI Direct Research

Exhibit 61: Snapshot of room portfolio post current addition plans

Source: Company, ICICI Direct Research

Lemon Tree Premier, Kolkata

Lemon Tree Mountain Resort, Shimla

(Representative Image)

Lemon Tree Mountain Resort, Shimla (Under-

construction)

LTP Kolkata started operations in mid-October,

thus the current portfolio of LTP increases to 2142

rooms over 14 hotels and the pipeline reduces by

142 rooms and 1 hotel

ICICI Securities | Retail Research 30

ICICI Direct Research

Initiating Coverage | Lemon Tree Hotels

Exhibit 62: Strong management contract pipeline (excluding Keys portfolio)

Source: Company, ICICI Direct Research

Exhibit 63: Lemon Tree to have presence in more than 68 cities

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 31

ICICI Direct Research

Initiating Coverage | Lemon Tree Hotels

Enters student housing, co-living; partners with Warburg Pincus

Lemon Tree has had a very strong relationship with Warburg Pincus, since

the initial fund raising from the latter in 2006. With the fund’s life coming to

an end, Warburg Pincus sold its entire stake in the company. In December

2018, Lemon Tree signed an agreement for a JV with Warburg Pincus, to

enter the business of students housing and co-living, with Warburg Pincus

owning 70% stake in the JV. Lemon Tree would be holding 29% stake while

the balance would be held by Patanjali Keswani. The management expects

this segment to open up huge opportunities for growth. The JV would entail

total investment of ~| 3000 crore in the next 10 years in two phases. In the

initial stages, properties would be added through long term lease while the

management expects to set up 10000 beds in FY20 itself. These properties

would be under the Lemon Tree brand for which the company would be

charging fees to the JV, which will help the company generate additional

revenues over and above the share of profits from the JV. Since the

developments are at a nascent stage, we do not factor in any revenues from

this segment in our estimates.

Revenues to clock 31% CAGR led by inventory addition

During FY20E, Lemon Tree’s portfolio of owned/leased rooms will increase

by 686 rooms over FY19 (In addition to Key Hotels portfolio), with most

hotels being in the upper-midscale and upscale segment, and one being in

the economy segment. Additionally, Keys Hotels’ portfolio is also expected

to be consolidated into the Lemon Tree group in H2FY20E. Keys Hotels

clocked revenues of | 87 crore in FY19. We expect Keys portfolio to cross

| 120 crore in crore by FY21E. Led by additional inventory, improved

RevPAR in existing hotels and higher ARRs in properties being added in

FY20E, Lemon Tree’s revenues are expected to grow at 31% CAGR over

FY19-21E to | 940 crore.

Exhibit 64: Owned/Leased hotel addition plans

Name/Location Rooms Expected opening Ownership (%)

End of FY19 3570

Addition during FY20:

LTP, Mumbai 303 Operational 58%

LTP, Kolkata 142 Operational 58%

RFH, Chandigarh 102 Operational Leased

Aurika, Udaipur 139 Oct-19/Nov-19 58%

Total addition (Ex-Keys) 686

Keys Hotels Inventory 936

End of FY20E 5192

Additions post FY20:

LT Mountain Resort, Shimla 69 Apr-21 100%

LT Vembanad Lake Resort, Alleppy, Kerala 10 Oct-21 100%

Aurika, MIAL 577 Nov-21 58%

Total Room addition 656

Total rooms by end of FY22 5848

Source: Company, ICICI Direct Research

Lemon Tree has applied to convert some commercial

spaces in Aurika, MIAL hotel to rooms. This will

increase the hotel’s inventory by 92 rooms to 669

and total inventory would reach 5940 rooms

Lemon Tree would consolidate Keys Hotels under its

own network. The target segment would be the mid

and economy segments. Expect improvement in

margins of Keys with improved RevPARs (owing to

improved presence through Lemon Tree’s existing

network) and lower corporate expenses

For 937 rooms (Kolkata, Shimla, Kerala, Aurika MIAL

and Aurika Udaipur) the company has estimated a

total capex of ~| 1250 crore, out of which it had

already spent | 635 crore as on 30th June 2019)

ICICI Securities | Retail Research 32

ICICI Direct Research

Initiating Coverage | Lemon Tree Hotels

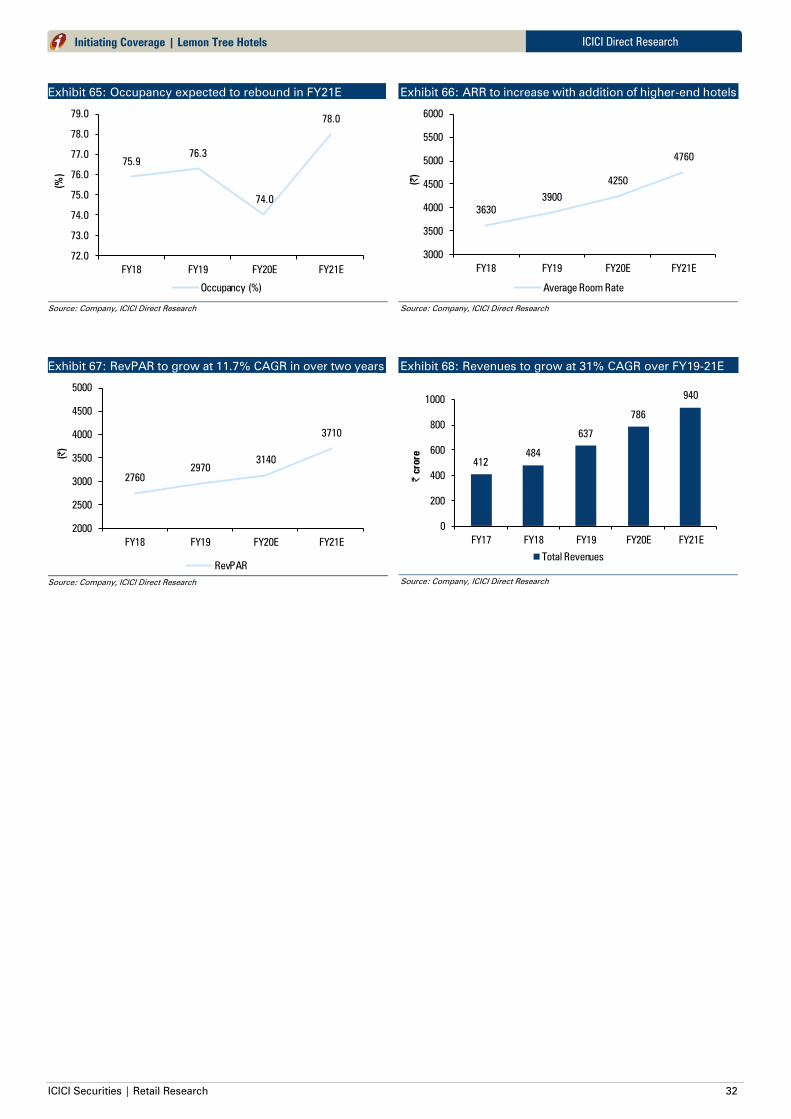

Exhibit 65: Occupancy expected to rebound in FY21E

75.9

76.3

74.0

78.0

72.0

73.0

74.0

75.0

76.0

77.0

78.0

79.0

FY18 FY19 FY20E FY21E

(%

)

Occupancy (%)

Source: Company, ICICI Direct Research

Exhibit 66: ARR to increase with addition of higher-end hotels

3630

3900

4250

4760

3000

3500

4000

4500

5000

5500

6000

FY18 FY19 FY20E FY21E

(|)

Average Room Rate

Source: Company, ICICI Direct Research

Exhibit 67: RevPAR to grow at 11.7% CAGR in over two years

2760

2970

3140

3710

2000

2500

3000

3500

4000

4500

5000

FY18 FY19 FY20E FY21E

(|)

RevPAR

Source: Company, ICICI Direct Research

Exhibit 68: Revenues to grow at 31% CAGR over FY19-21E

412

484

637

786

940

0

200

400

600

800

1000

FY17 FY18 FY19 FY20E FY21E

| crore

Total Revenues

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 33

ICICI Direct Research

Initiating Coverage | Lemon Tree Hotels

EBITDA margins to continue to remain strong

Typically, a hotel property takes one to one and a half years to break even

at the EBITDA level and additional one and a half to two years to achieve

profit before tax (PBT) breakeven. Thus, stabilisation of a hotel property

takes about three years to stabilise, post which the RevPARs also start

showing significant improvement. Currently ~35% of the owned/leased

room portfolio of Lemon Tree has been operational for less than three years.

Historically, Lemon Tree’s hotels have shown strong improvement in its