homeloan investment loan master class 2014

TRANSCRIPT

Important Legal Stuff [aka a disclaimer]

• This presentation has been prepared for general information purposes only and not as specific advice to any particular person. Any advice contained in this document is General Advice and does not take into account any person’s investment objectives, financial situation and particular needs.

• Before making any investment decision based on any of our presentations, you should consider, with or without the assistance of a professional adviser, whether it is appropriate to your particular investment needs, objectives and financial circumstances.

Agenda Rates Repayment Terms New credit laws Broker V Banker Tips + Tricks

Who are Foster Ramsay Finance ?

• Offer choice; through partnering with 40 of Australia’s top

Banks and Lenders. • To innovate through doing business with the best in the

industry; and • Take an honest, ethical, responsible and no-‐bullDsh

approach to business. • To invest in market leading soFware that will make

property investment efficient and effecDve

Experience CHRIS FOSTER-RAMSAY

Owner and Principal Finance Broker Mobile +61 (0)448 010 999

Office: +61 3 8844 5611 [email protected]

Full Member MFAA Approved MFAA Credit Adviser Qualification/s: Dip. FS | RG 146 | B.Arts | G.Cert Ent & Innv Authorised Credit Representative (402184) of Connective Credit Services who holds Australian Credit Licence 389328

Rates

Repayment Terms

New Credit Laws • What are the changes? • Does that mean if I’m a day late with my phone bill I wont be able to borrow any money?

• What informaDon will be reported back to my credit file?

• Are we heading towards an e-‐applicaDon process ?

Broker V Banker

Lending Panel

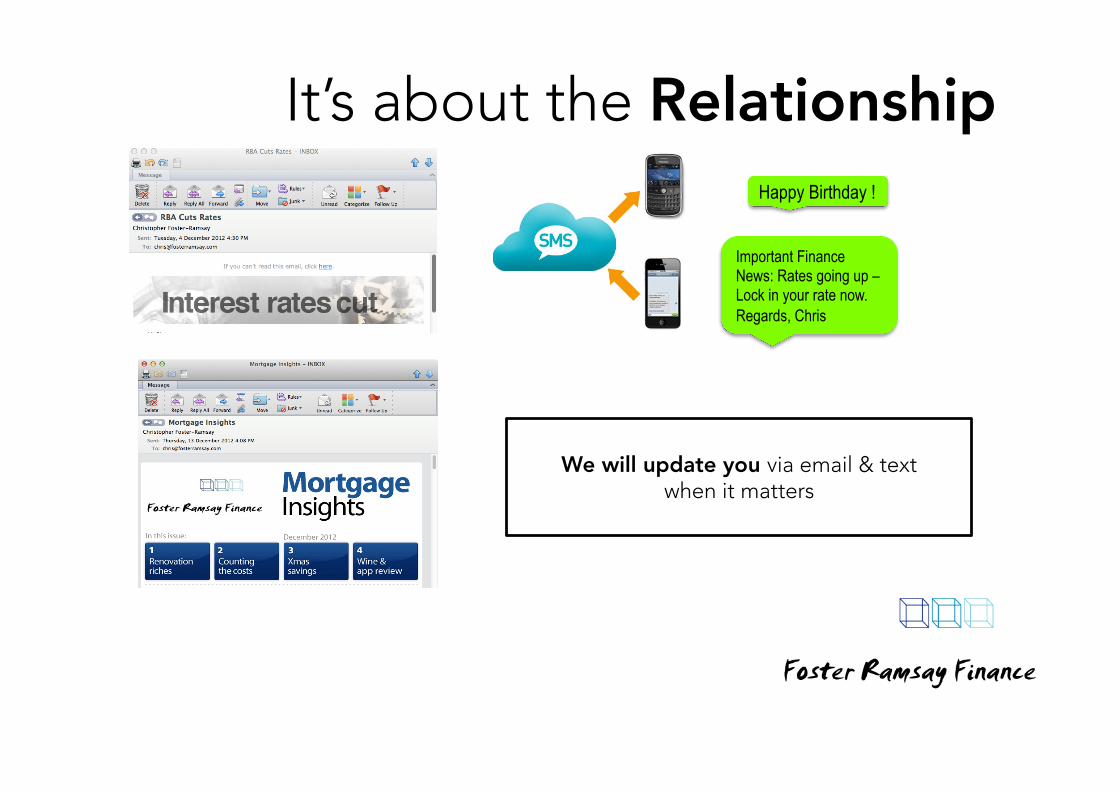

It’s about the Relationship Happy Birthday !

Important Finance News: Rates going up – Lock in your rate now. Regards, Chris

We will update you via email & text

when it matters

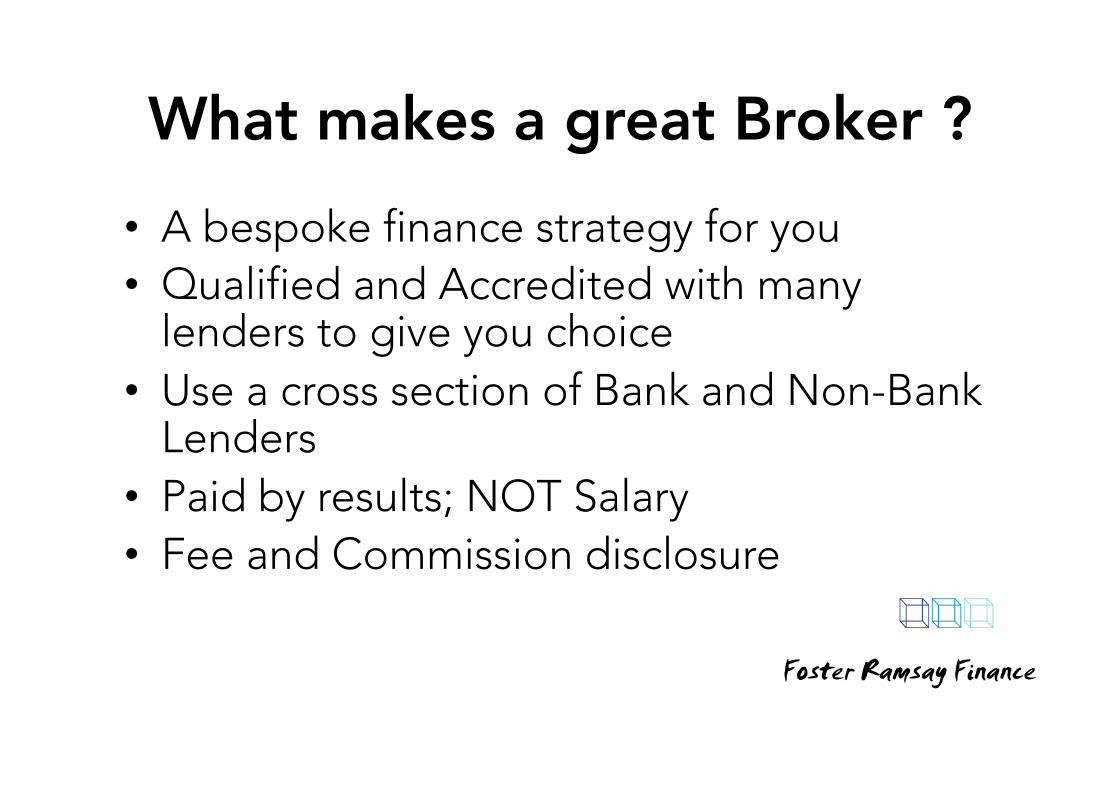

What makes a great Broker ? • A bespoke finance strategy for you • Qualified and Accredited with many

lenders to give you choice • Use a cross section of Bank and Non-Bank

Lenders • Paid by results; NOT Salary • Fee and Commission disclosure

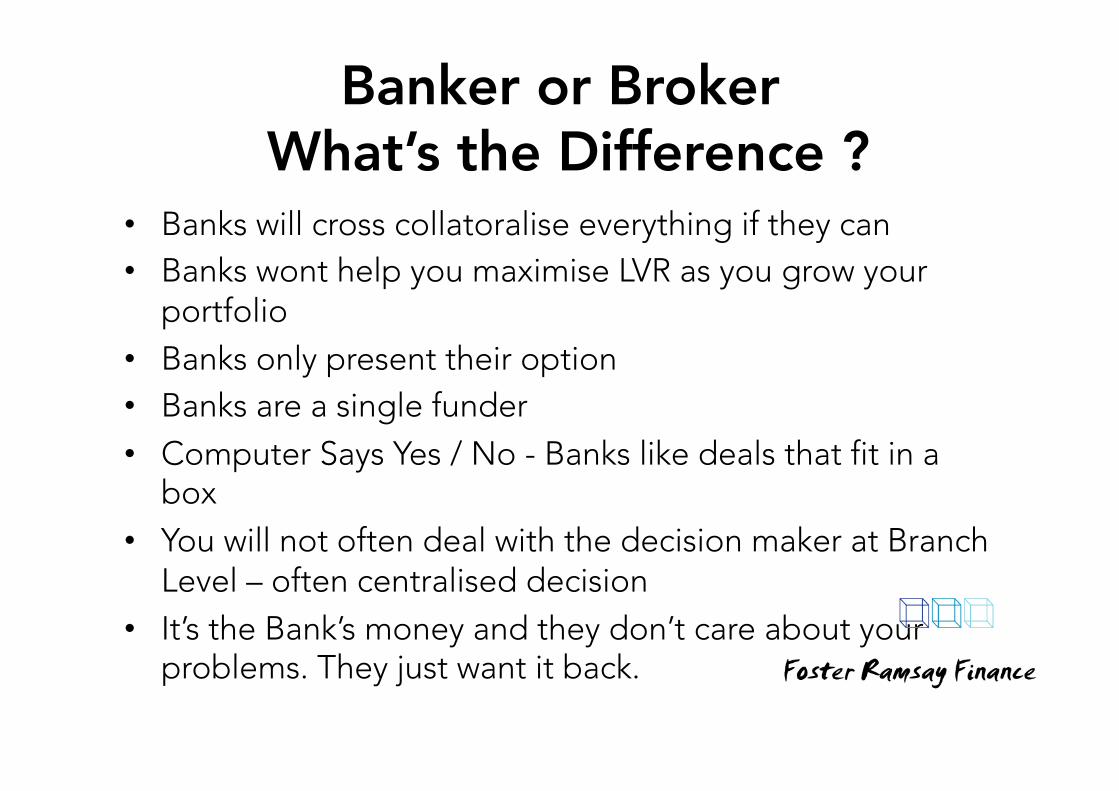

Banker or Broker What’s the Difference ?

• Banks will cross collatoralise everything if they can • Banks wont help you maximise LVR as you grow your

portfolio • Banks only present their option • Banks are a single funder • Computer Says Yes / No - Banks like deals that fit in a

box • You will not often deal with the decision maker at Branch

Level – often centralised decision • It’s the Bank’s money and they don’t care about your

problems. They just want it back.

Tips + Tricks

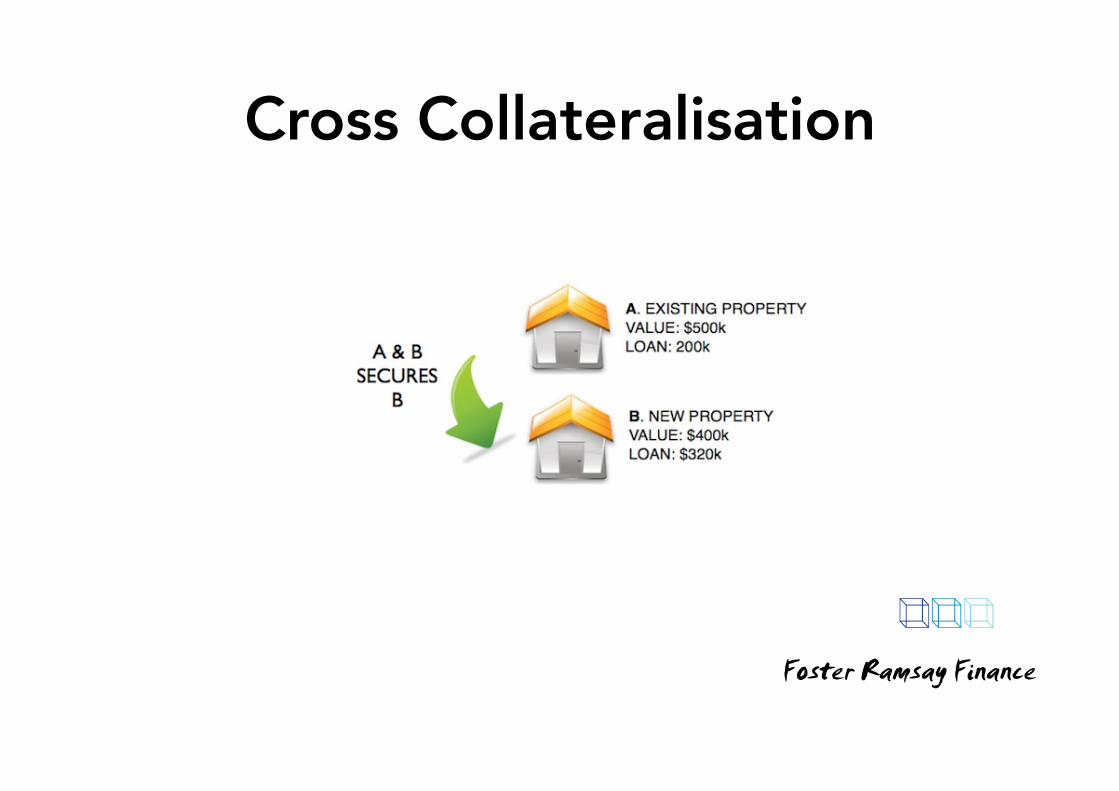

Cross Collateralisation

Cross Collateralisation • VERY RISKY • Bank contracts enable them to pool secured

assets across multiple debts by using an “all monies clause”

• If you have multiple loans with once bank they can take funds from one account to clear any arrears on any loan using an “account combination” clause

Individual Collateralisation

Individual Collateralisation • Allows you to regain control • Separate security for each loan – spreads the risk • Easier to top up multiple loans for small amount/s.

Easier to buy / sell / refinance • Avoids domino effect if you have difficulty in one

area • Financiers more negotiable if they can see assets

they can’t touch.

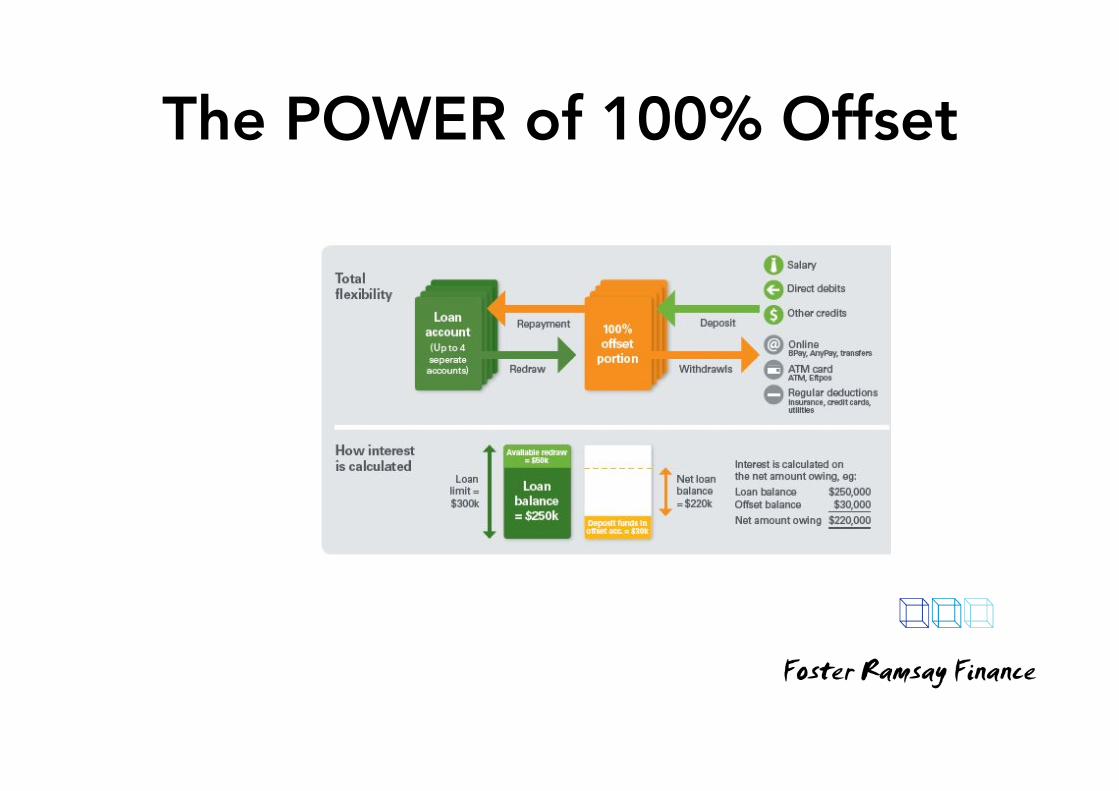

The POWER of 100% Offset

The POWER of 100% Offset • Keeps savings available and minimises

interest • Enable you to pay off debt many years

ahead of schedule • Keeps loan amount at its maximum whilst

minimising interest costs • Easier to access equity without refinancing

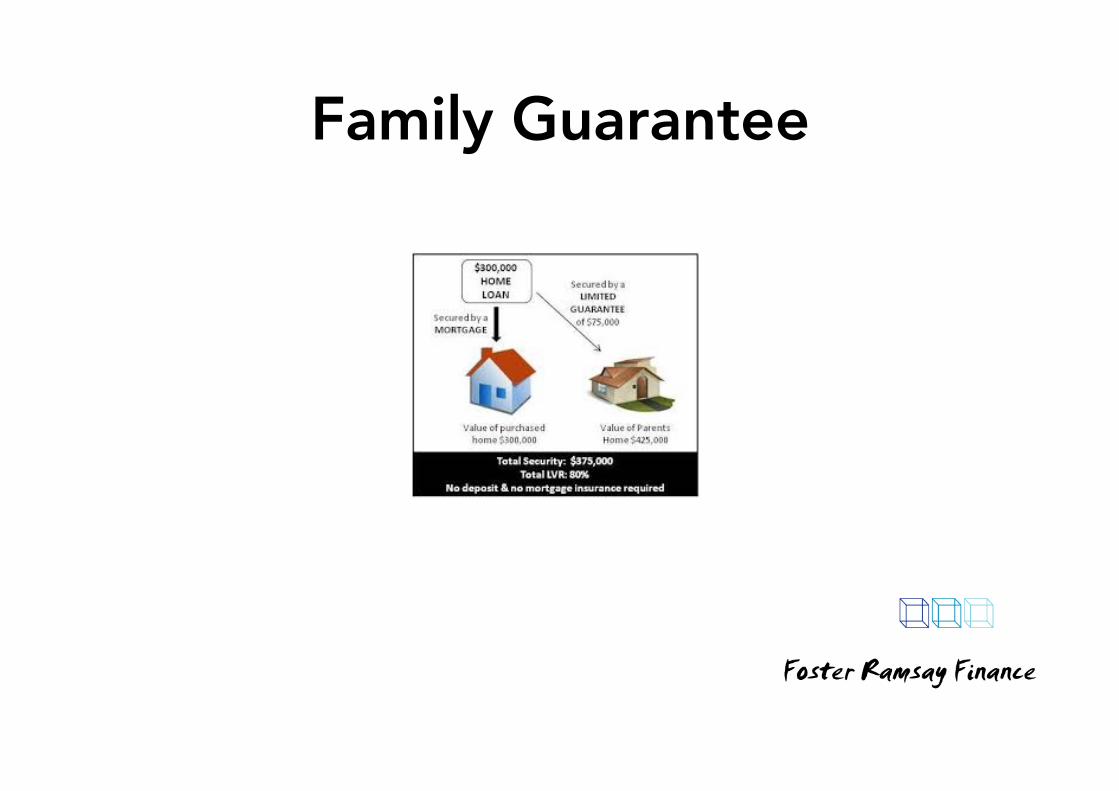

Family Guarantee

Questions

fosterramsay.com