homebuyer package

DESCRIPTION

Your guide to purchasing a home RE/MAX Niagara Realty Ltd., BrokerageTRANSCRIPT

Your Guide to Purchasing a Home

Homebuyers’

Package

Rebecca Burdon Sales Representative

Phone: 905-356-9600 Direct: 905-321-6717

NIAGARA REALTY LTD. Real Estate Brokerage

Each office independently owned & operated

Page 2 of 20

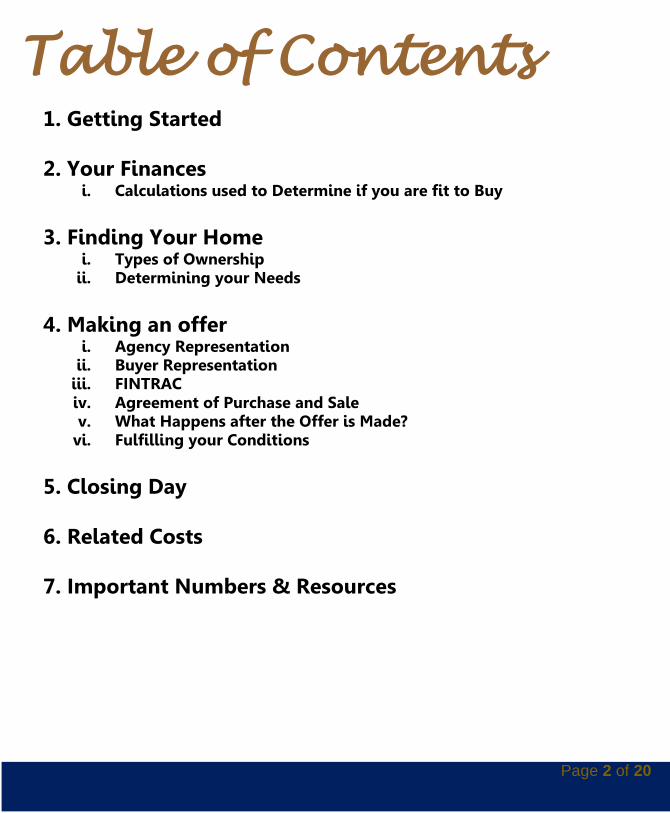

Table of Contents

1. Getting Started

2. Your Finances i. Calculations used to Determine if you are fit to Buy

3. Finding Your Home

i. Types of Ownership ii. Determining your Needs

4. Making an offer

i. Agency Representation ii. Buyer Representation

iii. FINTRAC iv. Agreement of Purchase and Sale v. What Happens after the Offer is Made?

vi. Fulfilling your Conditions

5. Closing Day

6. Related Costs

7. Important Numbers & Resources

Page 3 of 20

Getting Started

Congratulations on your decision of becoming a homeowner! Buying a home is one of the most exciting and important moments of your life. Your home is not just the roof over your head, where you live, eat, sleep, play, and raise a family; it’s also one of the most important investments you’ll ever make. I am Rebecca Burdon with RE/MAX Niagara Realty Ltd. and I am here to help. I want to do more than just help you buy a property; I want to teach you everything you need to know to buy your home. Even for people who have bought property or made other major purchases before, there’s a lot to know, learn, and manage as you make the transition to being a homeowner. And there are so many questions to answer:

Do you have enough money?

What can you afford?

Are you pre-approved for a mortgage?

Should you buy new or in an established neighbourhood?

How do I actually buy the home I want?

Page 4 of 20

Your Finances

This is, in my opinion, the single most important piece of the puzzle you need to know before start looking at properties. While online calculators are a great tool to help you get an idea of what you can afford, your first call should be to your financial institution to get pre-approved. I am happy to give you the contacts of mortgage specialists to

help you with this step

What to have ready for your visit to the lender?

Take stock of all your income and expenses to get an accurate picture of where you stand. You may have a good paying job and low expenses, but a lender will also want to know about your credit rating to make sure you’re going to make your mortgage payments.

Assess your present household budget and your annual

income to determine if you are eligible for a mortgage and how

much you can comfortable afford

Page 5 of 20

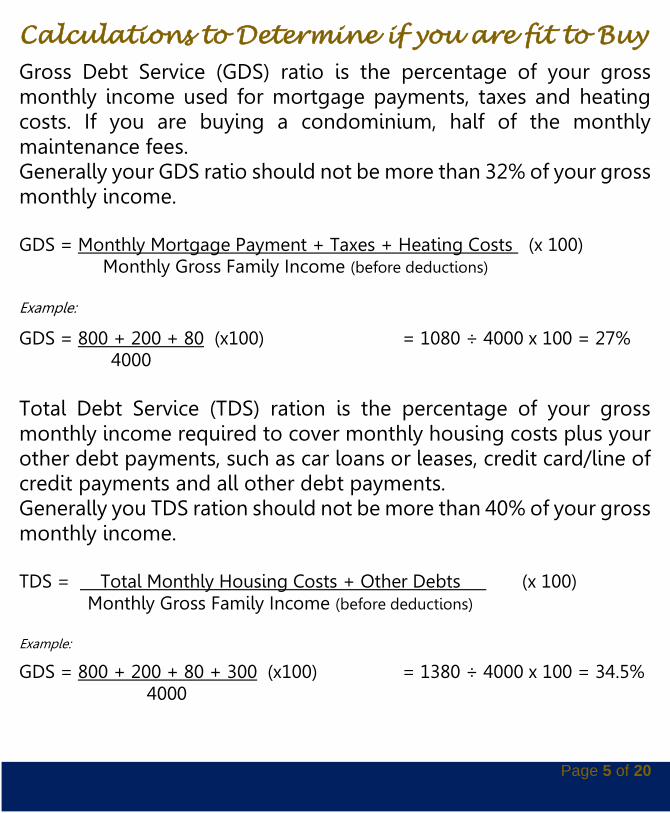

Calculations to Determine if you are fit to Buy

Gross Debt Service (GDS) ratio is the percentage of your gross monthly income used for mortgage payments, taxes and heating costs. If you are buying a condominium, half of the monthly maintenance fees. Generally your GDS ratio should not be more than 32% of your gross monthly income. GDS = Monthly Mortgage Payment + Taxes + Heating Costs (x 100) Monthly Gross Family Income (before deductions) Example:

GDS = 800 + 200 + 80 (x100) = 1080 ÷ 4000 x 100 = 27% 4000

Total Debt Service (TDS) ration is the percentage of your gross monthly income required to cover monthly housing costs plus your other debt payments, such as car loans or leases, credit card/line of credit payments and all other debt payments. Generally you TDS ration should not be more than 40% of your gross monthly income. TDS = Total Monthly Housing Costs + Other Debts (x 100) Monthly Gross Family Income (before deductions) Example:

GDS = 800 + 200 + 80 + 300 (x100) = 1380 ÷ 4000 x 100 = 34.5% 4000

Page 6 of 20

Finding Your Home

Finding your perfect home can be a long and overwhelming process, but as your realtor I am here to help identify the right type of home for you and continually watch for new listings that meet your needs.

Types of Ownership

There are two major types of property ownership you will come across in your search. The first is Freehold ownership and the other is Condominium ownership. Freehold Ownership: You own the land and the house, plus are responsible for everything inside and outside of the home Condominium Ownership (Condo): You own your unit and share ownership of the common spaces in the building. Common space includes areas such as hallways, the grounds around the building, and facilities such as a swimming pool and recreation rooms. Condominium owners together control the common areas through an owners’ association. The association makes decisions about using and maintaining the common space.

Page 7 of 20

Determining your Needs

When looking at homes, try to find homes that meets most of your needs for the next 5 to 10 years, or find a home that can grow and change with your needs. Here are some things to consider. Size How many bedrooms do you need? How many bathrooms do you need? Do you need space for a home office? What kind of parking do you need? For how many cars? Style Do you prefer a detached, semi-detached, townhouse or apartment? Would you like a single storey (bungalow), 2-storey, side-split or back-split? Location Is there an area you prefer in the city? Are there facilities you would like to be close to? Does school district matter? Any areas you would like to not be around? Special features Do you want air conditioning? Is a fireplace or a swimming pool high on your list? Do you want a fenced yard?

Page 8 of 20

Making an Offer

After looking at many different houses, you have found the one you would like to make an offer on! When you are ready for this step there are several forms that need to be filled out as this is a legal agreement you will be entering into. I am here to guide and answer all your questions through this process. The forms to be filled out are as follows:

Working with a REALTOR®

This form is sometimes completed before you start looking at homes. This form explains the different types of agency relationships you may enter into, which are Seller Representation, Buyer Representation, Multiple Representation & Customer Service. Below are brief descriptions of these agency types.

Buyer Representation

Working with a REALTOR®

FINTRAC

Agreement of Purchase and Sale

Confirmation of Cooperation

Page 9 of 20

Seller Representation: A real estate brokerage represents a seller and must do what is best for the seller of the property. This is a written contract entered into between the seller and the brokerage call a Listing Agreement. Buyer Representation: A real estate brokerage represents a buyer and must do what is best for the buyer of the property. This is a written contract entered into between the buyer and the brokerage. Multiple Representation: Sometime the same brokerage has signed contracts with both the seller and buyer in the same transaction. In this case both the seller and buyer must consent to this arrangement, which is explained and signed prior to an offer in the form Confirmation of Cooperation. Since the loyalty is divided between the two parties, the brokerage is to not disclose any information that could benefit either of the parties involved. Customer Service: The brokerage does not have a contract with buyer and must be honest and fair. There are customer representation forms that set out this agreement.

Buyer Representation

The buyer representation agreement is a contract between the buyer and the brokerage. This agreement is sometime entered into before looking at properties. It contains information pertaining to :

Whom is entering into the agreement (brokerage & buyer)

Time period the brokerage will be representing the buyer

Area & type of property you are looking for

Page 10 of 20

Who pays the brokerage (FREE to buyers)

Several pre-printed clauses, which will be explained by me before signing)

Places for signatures

FINTRAC (aka Individual Identification

Information Record)

This is completed for all parties that will have their name on title of the home being purchased. Valid ID (i.e. drivers licence, passport, etc.) must be presented to the agent to complete this form. This is required by the Proceeds of Crime (Money Laundering) and Terrorist Financing Act.

Confirmation of Cooperation

This form is completed before the offer is filled in. It again brings up what type of representation is being performed for both the buyer and seller. It also will disclose that the seller is paying for the commissions in the transaction.

Page 11 of 20

Now it is time for your offer…

Agreement of Purchase and Sale

It is important to understand that this is a legal and binding document once accepted. Offers to purchase are usually made conditional on factors such as financing, home inspection and insurance. Many other conditions could also be added as each transaction differs, which is what I will ensure is included for you. If any conditions are not met, you can changed or cancel the offer. Items are typically included in this document are: Names Your legal name, the name of the vendor and the legal civic address of the property. Price The price you are offering to pay. Amount of your deposit The closing day The closing day is the date you take possession of the home. It is usually 30 – 60 days after the date of agreement. But, it can be 90 days, or even longer. Things included (Chattels) Any items in or around the home that you think are included in the sale should be specifically stated in your offer. Some examples might be window coverings and appliances.

Page 12 of 20

Pre-printed clauses These I will review during signing. Other conditions This may include a satisfactory home inspection report, a property appraisal, and lender approval of mortgage financing. This means that the contract will become final only when the conditions are met.

What Happens after the Offer is Made?

Once the Agreement of Purchase and Sale is signed, your realtor (myself) will presents the offer to the vendor. The seller then has the option of four possible responses.

#1 The vendor accepts your offer. The deal is concluded and you move on to the next steps in the buying process.

#2 The vendor makes a counter-offer. The counter-offer might ask for a higher price, or different terms. You can sign the offer back to the vendor, offering a higher price than your original offer, but lower than the vendor’s counter-offer. If the vender accepts this counter-offer, the deal is concluded.

Page 13 of 20

Fulfilling your Conditions

Once the conditional offer is accepted it is now time to complete those conditions that were included (i.e. financing, home inspection, insurance, etc.). First you will contact your lender and let them know you have made an offer on a home. They will ask for details from you and then I will also get in touch with them to send over more information regarding the transaction. Your lender will then go over the offer and ensure it complies with what you can afford and start getting

#4 The vendor can decide to not sign back (perhaps offer was too low). You can then decide to walk away and continue looking or create a new Agreement of Purchase and Sale.

#3 The vendor makes a counter-offer, asking for a higher price or different terms. If a counter-offer is returned to you at a higher price, ensure that you know exactly how much you can afford before you start negotiating. You reject the counter-offer because the price is still too high, or you can’t agree to the conditions. The sale doesn’t go through, and your deposit is returned.

Page 14 of 20

the mortgage documents ready for you. This usually takes 3 business days to complete. At the same time you will contact the home inspector you would like (I am also able to supply you with a list of company’s) and schedule a time with them to inspect the property. Once you have a date and time be sure to relay this to me, as I will need to make this appointment with the sellers as well. At the home inspection you are welcome to come as most inspectors will show you where important utility access and shut-offs are in the home. I will also attend the inspection as your representative to ensure everything goes well. Once both your financing and home inspection are completed to your own satisfaction you will then make a call to your insurance provider to make sure they will ensure the home. Now that all the conditions are completed and you are happy with the results, we will fill-in a form to notify the sellers that we are removing the conditions. Once this is signed by all parties you are officially a homeowner!! Now you will contact your lawyer to let them know you have purchased a home. They will require some information, but most of the documents they require will be sent over by myself, your real estate agent. They will check title and get all the documents ready for your closing day.

Page 15 of 20

Closing Day

Hooray!! Your offer has been accepted and your move-in date is fast approaching!

This is the day you have been waiting for. You will finally take legal possession and get to call the house your home. The final signing usually happens at the lawyer office and you will be given the keys to your home. These are the things that happen on closing day:

Your lender will give the mortgage money to your lawyer.

You must give the down payment (minus the deposit) to your lawyer. You must also give the remaining closing costs.

Your lawyer

Pays the vendor

Registers the home in your name

Gives you the deed and the keys to your new home

Page 16 of 20

Related Costs

One of the most asked questions is, how much is it going to cost me? As each home and transaction is different it is hard to arrive at hard numbers. But what I can do is give you a guideline of what to expect during the buying process as it can surprise first time home buyers. CMHC and GE Capital recommend you to have at least 1.5% of the purchase price for closing costs, it is good practice to have 2%, just to be on the save side.

Here are some of the closing costs you may encounter, but please remember not all of them may apply to your specific situation, or there may be more that apply in your circumstance. This is a guideline. Talk to your lawyer, who can provide you with a better estimate, based on your specific situation. Deposit When your offer is accepted, a deposit is due to show good faith. It can range anywhere from $500-$20,000, depending of the purchase price. In most cases this is between $1,000-$5,000. Appraisal Fee The appraisal provides the lender with a professional opinion of market value of the property. This is normally the responsibility of the buyer and is only required if requested by your lender. It can range anywhere from $100-$300 approx., plus HST.

Page 17 of 20

CMHC and HST If your mortgage is insured by CMHC or GE Capital (this is when you are putting less than 25% down), the insurance premium will be added to the mortgage so it is not a cash requirement on closing, but the HST of 13% on the CMHC fee or GE Capital fee must be paid at closing. HST and the Resale Home The purchase of a used residential property (a property that has been occupied as a residence before you bought it) is “exempt” from HST. Most new build homes require this HST charge on the purchase price. Home Inspection A profession home inspection, top to bottom, is for the benefit of the buyer, therefore that who absorbs the cost. A typical home inspection can cost between $300-$500, but in most situations, is definitely worth the investment. Land Survey Fee A recent survey of the property is sometimes required of the lender, and if one is not available, it normally costs anywhere from $600-$900, for a new one. In lieu of the Survey, most lenders today will accept Title Insurance at a much lower price, approx. $225.

Page 18 of 20

Land Transfer Tax If you are a first-time homebuyer, you may be eligible for a refund of all or part of the tax. Otherwise it is payable to anyone who purchases property in Ontario. It is calculated on the property’s purchase price and varies from ½ to 2 percent. Legal Costs and Disbursements A lawyer will charge a fee for their professional services involved in drafting the title deed, preparing the mortgage, and conducting all the various searches. The disbursements, on the other hand, are out-of-pocket expenses incurred, such as registrations, searches, supplies, etc., plus HST. This typically cost between $1300-$2500. Home Insurance Protection for your home and contents. This approximately costs between $450-$800 annually. Other Costs An “adjustment” takes place when the seller has already paid for something in advance and wants to be credited for the unused portion on the date the home becomes yours adjustments usually include property taxes, utilities, or interest adjustments.

TIP: I always recommend to all home buyers to change out the locks, as you do not know who may have a key to the property.

Page 19 of 20

Important Resources

& Numbers

Property Search Engines: www.realtor.ca www.remaxniagara.ca Canadian Mortgage & Housing Corporation: www.cmhc-schl.gc.ca Post Office: (905) 374-6667 www.canadapost.ca City of Niagara Falls: (905) 356-7521 www.niagarafalls.ca Waste Management: (905) 356-4141 www.regional.niagara.on.ca District School Boards of Niagara: (905) 641-1550 www.dsbn.edu.on.ca

Niagara Catholic District School (905) 735-0240 www.niagaracatholic.ca Junk Removal: (905) 310- Haul (4285) (905) 646-5865 BELL Canada: (905) 310- BELL (2355) www.bell.ca COGECO: (905) 1-800- 267-9000 www.cogeco.com ENBRIDGE: 1-800-668-4732 www.enbridge.com Hydro: (905) 356-2681 www.niagarafallshydro.on.ca

Moving Company’s: Two Small Men with Big Hearts Moving: (905) 641-4485 Niagara Moving and Storage: (905) 354-3183 Atlas Van Lines: (905) 356-1666

Page 20 of 20

If any of your friends or family members are thinking of buying or selling a home,

please call me with their name and address, or have them call me and I would be happy to provide

them with the same level of service that I provide you.

One last Important Note…

NIAGARA REALTY LTD. Real Estate Brokerage

Each office independently owned & operated

Rebecca Burdon Sales Representative

Phone: 905-356-9600 Direct: 905-321-6717