home décor - phillipcapitalbackoffice.phillipcapital.in/backoffice/researchfiles/pc_-_home... ·...

TRANSCRIPT

Home Décor Making Homes, Decorating Returns

• Higher disposable income and urbanization to be the key demand drivers • Increasing preference for branded goods, driven by aggressive advertizing • FMCG like business model with high cash flow and ROEs • Distribution network a key entry barrier, in an attractive industry • Decreasing dependence on real estate growth Kapil Bagaria & Vibhor Singhal

– 2 of 94 –

Home Décor Making Homes, Decorating Returns

4 December 2012PhillipCapital (India) Pvt. Ltd.

Known companies, a different lens In this report, we analyze five leading companies of a sector, which has been there right in front of our eyes, but hasn’t been brought under the magnifying glass as a complete basket – the Home Décor sector. This sector has historically been dominated by small local players, but over the last decade, it has seen emergence of few large players (listed and private) which have registered robust earnings growth, and look set to continue the same over the next five years. Macro tailwinds to provide boost to the earnings growth With increasing urbanization, growth in disposable income and growing aspirations of the Indian middle class, we believe the market pie for home décor products is set to expand significantly over the next five years. At the same time, increasing preference for branded goods would help the organized segment to garner a much larger share of this increasing pie. We expect the organized companies to report 15‐20% topline growth over the next three years. FMCG like business model ensures high cash flow generation and ROEs Most of the home décor companies (except plywood) have negative to low working capital cycle and high asset turnover. This helps in converting large part of the operating profit into free cash flow for the companies. The high cash flow in‐turn keeps the leverage in check, and hence the ROE are typically in the range of 20‐40%. Attractive industry, but not without entry barriers The home décor sector has two key entry barriers – Dealer network and Brands. Companies in this sector operate through a vast network of exclusive dealers, who ‘seemed’ happy with the current business environment (in our dealer visits), and have been the prime reason behind the exponential growth of their respective companies. At the same time, the companies have been investing large part of their revenue on advertizing, building a strong brand for their products. Decreasing dependence on real estate growth The product replacement cycle of all the home décor products has shrunk substantially over the last decade. This decouples the growth of these companies from real estate growth in the country, though a large part of their sales still caters to the ‘new’ home sales category. An excellent investment opportunity for the investors We believe the home décor sector represents an excellent investment opportunity, to ride the consumer wave of the Indian economy. In this report, we have identified five sub‐segments in the home décor sector, and analyzed the leading company in that sub‐segment. We expect all of these five companies to register robust earnings growth over the next three years, and outperform their peers. While most of them look attractive on valuations too, each of them has a unique reason and investment story behind it. We recommend BUY on Kajaria Ceramics, HSIL, Havells Ltd, Greenply Industries and Berger Paints.

Companies Covered Kajaria Ceramics CMP Rs259Reco BUYTarget Price Rs325 HSIL Ltd CMP Rs137Reco BUYTarget Price Rs193 Havells Ltd CMP Rs585Reco BUYTarget Price Rs695 Greenply Industries CMP Rs305Reco BUYTarget Price Rs405 Berger Paints CMP Rs153Reco BUYTarget Price Rs182 Upside Potential

19% 19%25%

32%41%

Havells

Berger

Kajaria

Green

ply

HSIL

Relative positioning

HSIL

Berger

0

10

20

30

0 10 20 30 40

P/E

ROE (%)

Greenply

Havells

Kajaria

Kapil Bagaria (+ 9122 6667 9965) [email protected] Vibhor Singhal (+ 9122 6667 9949) [email protected]

3 of 94

4 December 2012 / INDIA EQUITY RESEARCH / HOME DÉCOR

Table of Contents

Investment Thesis ........................................................................... 4

Why This Sector? ............................................................................. 5

Business Model ................................................................................ 9

Valuations ........................................................................................ 12

Dealer feedback .............................................................................. 13

Companies Covered

Kajaria Ceramics .............................................................................. 15

HSIL .................................................................................................. 33

Havells Ltd ....................................................................................... 53

Greenply Industries ......................................................................... 71

Berger Paints ................................................................................... 83

4 of 94

4 December 2012 / INDIA EQUITY RESEARCH / HOME DÉCOR

Investment Thesis The Home Décor segment has grown considerably in the past few years – both in terms of market size and the variety of products available. Gone are the days when all you could get for your home decoration were bland single‐color tiles and standard bathroom fittings. The market today is flush with multi‐design, multi‐colored tiles, along with bathroom fittings of the most innovative designs. The furniture no longer has that old‐boring look; and the plain vanilla bulbs and tube‐lights have long been replaced by fancy elegant fixtures carrying advanced CFL tubes. The Home Décor segment doesn’t have a strict definition, but we have identified five major sub‐segments, where most of the companies under the umbrella reside: • Ceramics: This segment comprises of companies manufacturing and distributing tiles

– glazed and vitrified, used for covering walls (interior and exterior) and ceiling. Its market size in India currently stands at Rs170bn, having grown at over 15% CAGR over the last five years.

• Sanitaryware: This segment mainly comprises of companies that make sanitaryware and bathroom fittings. Its market size in India currently stands at Rs20bn, having grown at over 15% CAGR over the last five years.

• Electricals: This segment consists of various sub‐segments, but we have grouped the companies under the umbrella of companies that solve the electrical needs of a residential/commercial place – switches, circuit breakers, wires, lightings and electrical durables. The current market size of all these put together, is a whopping Rs625bn, and has grown at CAGR of 19% over the last five years.

• Furniture: In the furniture segment, we look at the companies that manufacture various forms of plywood and laminates, in the absence of a furniture maker of significant size. The current market size for this industry is Rs200bn, and has grown at CAGR of 7% over the last five years.

• Paints: And lastly, the paints segment comprises of the companies making various forms of paints. The market size of this segment is currently estimated to be ~Rs250bn, and has grown over 12% CAGR over last five years.

Home décor market at a glance Segment Market size

(FY12) Rs bn

CAGR (FY07‐12)

%

Organized share (FY12)

%

Major listed players Major private players

Ceramics 170 15% 50% Kajaria, Somany HR Johnson

Sanitary ware 20 15% 60% HSIL, Cera Jaguar

Electricals 626 19% 50% Havells, Bajaj, Crompton Philips, Anhor, Polycab

Furniture 200 7% 44% Century ply, Greenply Uniply, Marino

Paints 250 12% 70% Asian Paints, Berger ‐

Source: PhillipCapital India Research

While the home décor sector has grown in size, so has the valuation of the companies listed in the space. The market cap of the leading ten companies in the sector has more than trebled in the last five years. However, we expect the momentum to continue over the next five years. We believe riding this growth wave can lead to significant value creation for investors, and the sector presents an extremely interesting investment opportunity, at current levels.

5 of 94

4 December 2012 / INDIA EQUITY RESEARCH / HOME DÉCOR

Why This Sector? Increasing Market Pie The House Décor sector has demonstrated robust growth over the last five years. On an average, all the sub‐segments have grown at 14% CAGR over the period FY07‐12. We expect the sector and the companies to continue reporting strong growth over the next three years, driven by the following factors: Increasing urbanization

Increasing Urbanization

‐

200

400

600

800

1,000

1,200

1,400

1,600

1991 2001 2008 2030

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%Total Population, mn (lhs)

Urbanization rate (rhs)

Source: Mckinsey Research

Increasing affluence level and disposable income

Source: Mckinsey Research

6 of 94

4 December 2012 / INDIA EQUITY RESEARCH / HOME DÉCOR

More people will join the great Indian middle class, over the next two decades

6450

2615

31

34

40

32

12

25

29

6

17

7

0%

20%

40%

60%

80%

100%

2000 2008 2020 2030

Deprived Aspirers Seekers Strivers Globals

Source: Mckinsey Research

Decreasing Dependence on Real Estate Growth One of the popular perceptions about the home décor sector is that its growth is heavily dependent on the growth in real estate sector, and the former will witness a downturn (if not already) due to slowdown in the latter. While the real estate growth definitely drives the growth for home décor sector and the two have a high correlation, we note that the dependence has been “increasingly decreasing”. And the main reason for the decreasing dependence has been the shortening product replacement cycle – people now tend to replace their old furniture, tiles and electrical goods much more frequently, than twenty years ago. Sales growth does not seem to have a high correlation with real estate sales

‐20%

0%

20%

40%

60%

80%

100%

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

YoY Sales grow

th (%

)

‐5%

0%

5%

10%

15%

20%

25%

Net absorption rate (%

)

Havells Greenply KajariaHSIL Berger Residential

Source: PhillipCapital India Research, Jones Lang Lasalle

Category Annual Income (Rs thousand) Deprived < 90 Aspirers 90 ‐ 200 Seekers 200 ‐ 500 Strivers 500 ‐ 1000 Globals > 1000

Net absorption rate (ratio of sales over inventory of residential units) for top seven cities of India – Mumbai, NCR‐Delhi, Bangalore, Chennai, Pune, Hyderabad and Kolkata

7 of 94

4 December 2012 / INDIA EQUITY RESEARCH / HOME DÉCOR

Increasing Share Of Pie (Organized Market) While the market size of the home décor sector has been growing, so has the share of the organized market. Over the last ten years, organized players have garnered, on an average, 2‐3% market share every year, from the unorganized players. This has been driven by increasing brand awareness amongst the consumers, which has in‐turn been driven by the increasing focus of these companies on advertizing and brand building. Increasing share of advertisement expenses

0%

1%

2%

3%

4%

5%

6%

FY07 FY08 FY09 FY10 FY11 FY12

Advertizing expe

nses as % of sales

Havells Ltd Greenply Kajaria CermaicsHSIL Ltd Berger Paints

Source: Companies, PhillipCapital India Research

8 of 94

4 December 2012 / INDIA EQUITY RESEARCH / HOME DÉCOR

Branding by Aggressive Advertizing

Kajaria Ceramics

HSIL Ltd

Havells

Greenply

Berger Paints

Source: PhillipCapital India Research

9 of 94

4 December 2012 / INDIA EQUITY RESEARCH / HOME DÉCOR

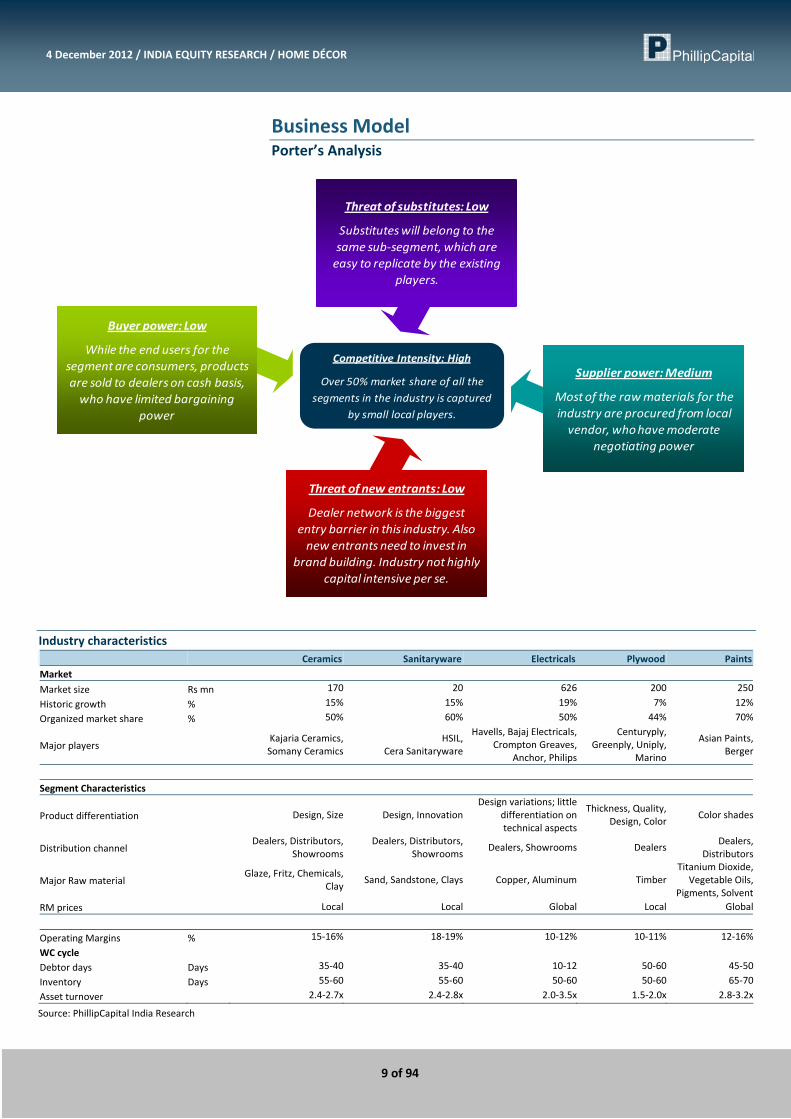

Business Model Porter’s Analysis

Supplier power: Medium

Most of the raw materials for the industry are procured from local vendor, who have moderate

negotiating power

Threat of new entrants: Low

Dealer network is the biggest entry barrier in this industry. Also new entrants need to invest in

brand building. Industry not highly capital intensive per se.

Buyer power: Low

While the end users for the segment are consumers, products are sold to dealers on cash basis, who have limited bargaining

power

Threat of substitutes: Low

Substitutes will belong to the same sub‐segment, which are easy to replicate by the existing

players.

Competitive Intensity: High

Over 50% market share of all the segments in the industry is captured

by small local players.

Industry characteristics Ceramics Sanitaryware Electricals Plywood Paints

Market

Market size Rs mn 170 20 626 200 250

Historic growth % 15% 15% 19% 7% 12%

Organized market share % 50% 60% 50% 44% 70%

Major players Kajaria Ceramics, Somany Ceramics

HSIL, Cera Sanitaryware

Havells, Bajaj Electricals,Crompton Greaves,

Anchor, Philips

Centuryply, Greenply, Uniply,

Marino

Asian Paints,Berger

Segment Characteristics

Product differentiation Design, Size Design, Innovation Design variations; little

differentiation ontechnical aspects

Thickness, Quality, Design, Color

Color shades

Distribution channel Dealers, Distributors,

ShowroomsDealers, Distributors,

ShowroomsDealers, Showrooms Dealers

Dealers,Distributors

Major Raw material Glaze, Fritz, Chemicals,

ClaySand, Sandstone, Clays Copper, Aluminum Timber

Titanium Dioxide,Vegetable Oils,

Pigments, SolventRM prices Local Local Global Local Global

Operating Margins % 15‐16% 18‐19% 10‐12% 10‐11% 12‐16%

WC cycle Debtor days Days 35‐40 35‐40 10‐12 50‐60 45‐50

Inventory Days 55‐60 55‐60 50‐60 50‐60 65‐70

Asset turnover 2.4‐2.7x 2.4‐2.8x 2.0‐3.5x 1.5‐2.0x 2.8‐3.2x

Source: PhillipCapital India Research

10 of 94

4 December 2012 / INDIA EQUITY RESEARCH / HOME DÉCOR

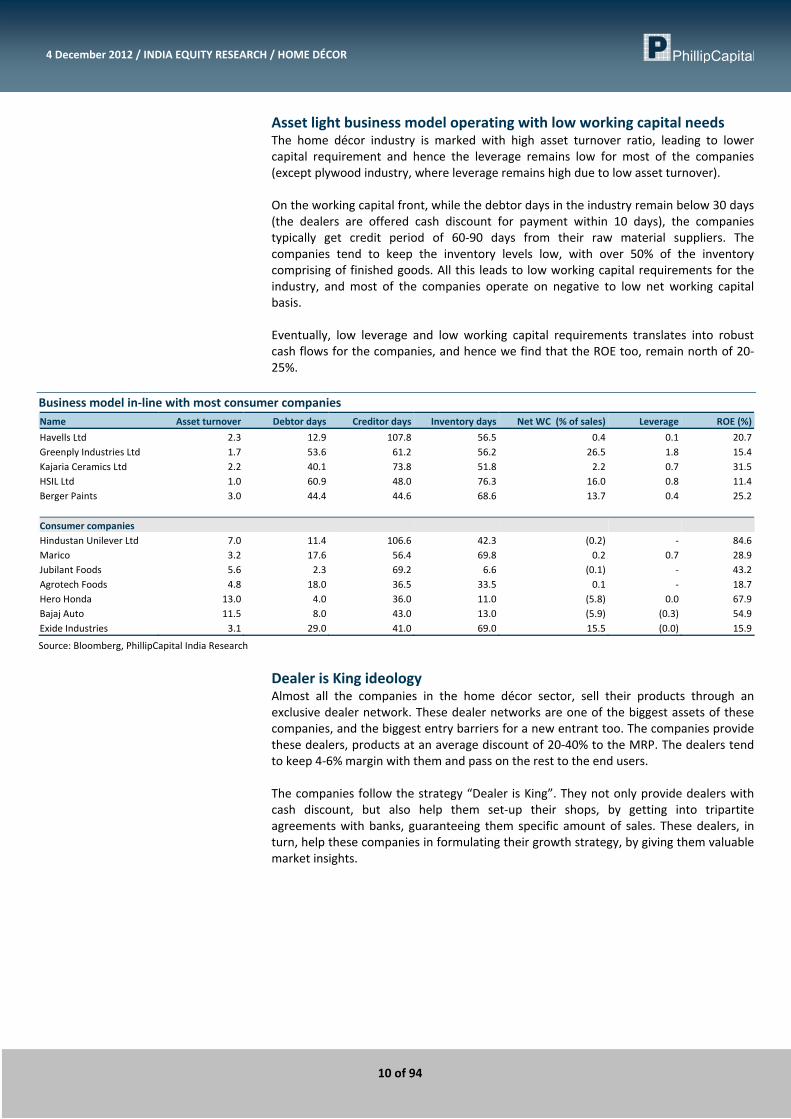

Asset light business model operating with low working capital needs The home décor industry is marked with high asset turnover ratio, leading to lower capital requirement and hence the leverage remains low for most of the companies (except plywood industry, where leverage remains high due to low asset turnover). On the working capital front, while the debtor days in the industry remain below 30 days (the dealers are offered cash discount for payment within 10 days), the companies typically get credit period of 60‐90 days from their raw material suppliers. The companies tend to keep the inventory levels low, with over 50% of the inventory comprising of finished goods. All this leads to low working capital requirements for the industry, and most of the companies operate on negative to low net working capital basis. Eventually, low leverage and low working capital requirements translates into robust cash flows for the companies, and hence we find that the ROE too, remain north of 20‐25%.

Business model in‐line with most consumer companies Name Asset turnover Debtor days Creditor days Inventory days Net WC (% of sales) Leverage ROE (%)

Havells Ltd 2.3 12.9 107.8 56.5 0.4 0.1 20.7 Greenply Industries Ltd 1.7 53.6 61.2 56.2 26.5 1.8 15.4 Kajaria Ceramics Ltd 2.2 40.1 73.8 51.8 2.2 0.7 31.5 HSIL Ltd 1.0 60.9 48.0 76.3 16.0 0.8 11.4 Berger Paints 3.0 44.4 44.6 68.6 13.7 0.4 25.2

Consumer companies Hindustan Unilever Ltd 7.0 11.4 106.6 42.3 (0.2) ‐ 84.6 Marico 3.2 17.6 56.4 69.8 0.2 0.7 28.9 Jubilant Foods 5.6 2.3 69.2 6.6 (0.1) ‐ 43.2 Agrotech Foods 4.8 18.0 36.5 33.5 0.1 ‐ 18.7 Hero Honda 13.0 4.0 36.0 11.0 (5.8) 0.0 67.9 Bajaj Auto 11.5 8.0 43.0 13.0 (5.9) (0.3) 54.9 Exide Industries 3.1 29.0 41.0 69.0 15.5 (0.0) 15.9

Source: Bloomberg, PhillipCapital India Research

Dealer is King ideology Almost all the companies in the home décor sector, sell their products through an exclusive dealer network. These dealer networks are one of the biggest assets of these companies, and the biggest entry barriers for a new entrant too. The companies provide these dealers, products at an average discount of 20‐40% to the MRP. The dealers tend to keep 4‐6% margin with them and pass on the rest to the end users. The companies follow the strategy “Dealer is King”. They not only provide dealers with cash discount, but also help them set‐up their shops, by getting into tripartite agreements with banks, guaranteeing them specific amount of sales. These dealers, in turn, help these companies in formulating their growth strategy, by giving them valuable market insights.

11 of 94

4 December 2012 / INDIA EQUITY RESEARCH / HOME DÉCOR

Dealer network expansion

‐

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

FY07 FY08 FY09 FY10 FY11 FY12

No of dealers

Havells Ltd Greenply Kajaria Cermaics

HSIL Ltd Berger Paints

Source: Company, PhillipCapital India Research

This Was History, How Does The Future Look? While this was how the past decade has fared for the industry, the future looks even brighter in our opinion. Most of these companies have already put in enough capacity to see them through the next three‐five years (except Greenply) and hence the utilization levels remain significantly below 100%. With the demand for branded home décor products on the rise, on the back of increasing disposable income, brand awareness and share of organized market, we expect the industry to clock an average 15% CAGR in revenue and earnings over the period FY12‐14E. At the same time, the operating cash flows too should register healthy growth, leading to an average ROE of 20% over the same period.

Past and Future _________________FY07‐12_________________ _________________FY12‐14E_________________

Name Market Cap

(Rs mn) Rev

CAGREarnings

CAGRAnnual OCF

(Rs mn) Avg ROERev

CAGR Earnings

CAGR Annual OCF

(Rs mn) Avg ROE

Havells Ltd 71,624 19% 24% 2,458 26% 19% 18% 4,344 21%Greenply Industries 7,362 33% 19% 168 23% 16% 42% 1,050 19%Kajaria Ceramics Ltd 18,908 26% 60% 643 17% 20% 28% 1,415 31%HSIL Ltd 8,771 25% 26% 684 15% 19% 17% 1,473 11%Berger Paints 44,642 19% 15% 1,273 26% 15% 18% 1,260 25%

Source: Bloomberg, PhillipCapital India Research

12 of 94

4 December 2012 / INDIA EQUITY RESEARCH / HOME DÉCOR

Valuations

Peer comparison – Domestic & Global

Name MCap Revenue

CAGR Earnings

CAGR _______P/E_______ _______ROE_______ _______P/B_______ ____EV/EBITDA____ USD mn FY12‐14E FY12‐14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E

Havells* 1,294 11% 11% 21.5 15.8 30.9 33.0 6.0 4.6 11.5 9.0Crompton Greaves 1,336 11% 23% 22.4 12.9 9.3 14.3 1.9 1.7 11.2 7.7Finolex Cables 148 12% 44% 6.0 4.0 13.0 17.0 0.9 0.7 4.1 2.6Bajaj Electricals 372 14% 23% 16.5 11.5 16.6 20.2 2.6 2.2 9.2 6.8 Kajaria Ceramics* 341 20% 28% 18.7 14.2 30.7 31.7 5.2 4.0 8.6 6.9 Somany Ceramics 58 17% 24% 10.1 8.2 22.3 22.5 2.0 1.7 4.8 4.1 HSIL Ltd * 153 19% 17% 9.4 6.6 9.0 11.8 0.8 0.8 6.0 4.7 Cera Sanitaryware 93 27% 22% 12.6 10.7 25.4 23.9 2.9 2.3 7.9 6.7 Greenply Indst* 129 16% 42% 8.1 6.6 21.3 21.4 1.6 1.3 5.8 5.0 Century Plyboards 234 25% 31% 8.5 6.1 14.7 17.9 1.2 1.0 8.2 5.6 Berger Paints * 903 15% 16% 23.5 19.7 24.4 24.4 5.5 4.6 14.9 12.7 Asian Paints 7,323 17% 19% 34.8 28.8 37.6 36.9 11.8 9.7 22.0 18.2

Global comparables Geberit AG 8,126 9% 6% 19.1 17.8 27.4 27.6 5.4 4.9 13.4 12.6Cie de St‐Gobain 20,621 2% 7% 12.8 10.8 7.0 8.2 0.9 0.8 5.9 5.6Wienerberger AG 939 17% ‐ (22.9) (106.4) (1.6) (0.6) 0.4 0.4 8.0 6.7

Source: Bloomberg, PhillipCapital India Research (*PhillipCapital estimates)

Do these companies deserve valuation in‐line with other consumer companies ?

Comparison with consumer companies

Name MCap Revenue

CAGR Earnings

CAGR _______P/E_______ _______ROE_______ _______P/B_______ ____EV/EBITDA____ USD mn FY12‐14E FY12‐14E FY13E FY14E FY13E FY14E FY13E FY14E FY13E FY14E

FMCG Hindustan Unilever 20,364 15.8 21.2 33.4 29.1 96.5 92.5 32.6 22.9 23.6 20.0Marico 2,464 19.0 22.4 33.6 28.4 25.0 21.1 6.6 5.5 21.7 18.2Jubilant Foods 1,517 41.5 41.4 57.7 39.4 38.9 38.5 18.8 12.7 28.3 19.2Agrotech Foods 194 10.9 13.6 26.2 22.8 18.0 17.7 4.4 3.8 17.4 14.7

Automobiles Bajaj Auto 6,781 6% 2% 16.0 15.0 47.6 41.1 6.8 5.6 10.0 9.4Hero Honda 10,198 11% 12% 17.5 14.8 46.3 42.7 7.2 5.6 14.2 11.9Exide Industries 2,202 19% 27% 19.8 16.5 20.7 20.8 4.0 3.4 12.1 10.0

Home décor Havells Ltd 1,294 11% 11% 21.5 15.8 30.9 33.0 6.0 4.6 11.5 9.0Kajaria Ceramics 341 20% 28% 18.7 14.2 30.7 31.7 5.2 4.0 8.6 6.9HSIL Ltd 153 19% 17% 9.4 6.6 9.0 11.8 0.8 0.8 6.0 4.7Greenply Industries 129 16% 42% 8.1 6.6 21.3 21.4 1.6 1.3 5.8 5.0Berger Paints 903 15% 16% 23.5 19.7 24.4 24.4 5.5 4.6 14.9 12.7

Source: PhillipCapital India Research

13 of 94

4 December 2012 / INDIA EQUITY RESEARCH / HOME DÉCOR

Dealer feedback Dealer of Havells ‐ Fans &

appliances Havells ‐ Domestic MCBs

Kajaria tiles Kajaria tiles HSIL HSIL Greenply Greenply

How long have you been in business? Do you keep only one or multiple brands?

Havells, Orient, Bajaj, Khaitan

Since 1960 – Havells & Finolex

26 years old shop ‐ Kajaria dealers since 1 year after Kajaria started

Shop since 50 years; HSIL dealer since 5‐7 years. Only HSIL

Major HSIL dealer ‐since 10 years.

Exclusive dealer – Mumbai – manly laminates

25 years relationship ‐ exclusively Greenply dealer ‐ plywood only

Have you seen a shift in consumer pref. towards organized or branded products?

Brand conscious customers in fans atleast; Havells ‐ fastest growing brand

Customer pref. was always there ‐ has been aided off late by more variety, marketing etc

Ceramic tiles sold more than vitrified ‐ 4 walls as compared to 1 ceiling.

Customers ask more for imported. HSIL is sold as Italian collection.

Branded:Unbranded‐50:50

People do ask for brand. Anchor, KIT, Samrat.

How is the current competitive scenario in the tiles industry?

Attrition at the branch level high for Havells, so a concern. Higher sale for OSRAM

Competition from RAK (UAE based, Hyd in India, 3rd largest worldwide); NITCO; Morbi etc

Imported, Parryware, Cera (not much of a competition)

Price competition‐Gujarat players

Gujarat‐Lam. Yamunanagar (Haryana) ‐ Ply

Century, Kenwood, Anchor, Uniply ‐ Sharda not in Mumbai

How has the business been in the last 6 months? Outlook for the next 12 months?

Footfalls are less as compared to previous years.

Overall slow since Dec, esp. last 4 months

8‐9 months‐ bad business; Overall demand less

50% down during last 6 months

Demand increasing. Growth in Metro is slower than Tier II/III cities

No slowdown, last 3 years ‐ 20% YoY growth

How do the products of the company (in question) fare? How are they priced?

Fans priced higher as compared to leaders. Premium product (not bothered)‐premium pricing

Havells has priced wires in‐line with Finolex ‐ should have kept it at discount. Overall expensive ‐ only one discount across the board

Kajaria has much more variety than others; Price difference between Kajaria and Gujarat based players is only Rs4 per sq ft

Hindware‐good growth, overall‐worse than last year

Price diff‐20% (from local). Ply‐90% of sales is Greenply. Vast difference in branded and non branded‐Quality

What is the working capital situation?

Mostly Cash & Carry ‐ has bounced PDCs from builders, architects

No problem in collection period also

Payment cycle up from 45 days to 60days

Consistent delays by RE players: 45‐60 days; Retailers faster payment

How much is the share of institutions and retail?

Retail, company (inst)‐25:75 (mktg)

70% institutional; keeps stock of over Rs 2cr

Customers are architects mainly. Total retail < 25% institutional

< 10% institutional

More wholesale‐all retailers 75:25‐inst. No Furniture Retailers. Not to direct real estate.

50:50 Inst:Retail

Terms and conditions given to the distributors by the manufacturing companies?

Havells fixtures doing well‐not in CFL. 10 days to 45 days

Cash discount ‐ 7 days; Without cash discount ‐ 25 days (of which 7 days go in transport)

10 days‐ cash discount sale

Debtor days ‐15‐120 days. Not to any builders. Cash discount till 30 days

cash discount on upfront payment only

45% on MRP. 35%‐40% passed to the customers

3 modes of payment: APD, PPD, CD Margins: 7‐8%. competitive market so one HAS to operate on APD**

Who drives the purchase decision?

Mainly Architects

Mainly Architects Mainly Architects Mainly Architects

50:50‐architect/ Personal

Architects mainly. > 40%

50:50 (carpenter: people)

Mainly Architects

Is there a cyclical pattern to sales? Festival, marriage season?

No No No off season per se; Rainy season a bit low

No No Same sale all the time; seasonality has reduced over the years

Same all around. Just 5‐10%‐ Current peaking

Slack period in May ‐ contractors & laborers go to native place

Source: PhillipCapital India Research (*APD – Advance Payment; PPD – Prompt payment; CD – Cash discount)

14 of 94

4 December 2012 / INDIA EQUITY RESEARCH / HOME DÉCOR

Compa

nies Section

– 15 of 94 –

Kajaria Ceramics Ltd Leadership through acquisitions and premiumisation

MIDCAP: HOME DÉCOR |Initiating Coverage 4 December 2012

PhillipCapital (India) Pvt. Ltd.

Kajaria Ceramics (KJC IN) is the largest in terms of tiles manufacturing capacity and the second largest in terms of revenues in the country. With its diversified product offering, extensive distribution reach and established brand, KJC has carved out robust business model which would lead to profitable growth for over the coming few years, in our opinion. Investment Rationale • KJC has increased its capacity from 1 MSM to 41 MSM in last 23 years and

offers more than 800 options in ceramic wall & floor tiles, vitrified tiles, designer tiles and much more.

• The Company embarked on a strategy of brownfield capacity expansion projects and inorganic growth over the last 5 years to increase capacity and also product offering, thereby manufacturing the value added products in‐house. The increased in‐house production of the value‐added products like Glazed Vitrified Tiles has led to sharp increase in the realizations and profitability for the company in the last 5 years.

• The high‐margin value‐added Vitrified Tiles segment is expected to grow faster than the Ceramic Tiles segment, leading to better realizations and margins. We estimate share of Ceramic Tiles to decrease from 48% to ~44% in FY12‐14E.

• KJC enjoys ~16.6% market share in the National Brands segment which has grown consistently from ~11.9% in FY10. It has consistently pursued the strategy to focus on retail distribution and increase its retail presence.

• Over the period of FY12‐14E we expect the company to generate operating cash flows to the tune of Rs 2.8bn and free cash flow to the tune of Rs 765mn. We expect the ROCE to improve from 24.5% in FY12 to 26.5% in FY13E and then further to 28.1% in FY14E.

Outlook and Valuation Given the superior cash flow generating ability of the business, established brand, consistent growth in revenues and profitability, efficient capital deployment and robust return ratios, we believe the company would continue to command rich valuations. We estimate the EPS to grow at 27.5% CAGR in FY12‐14E period. At the CMP of Rs 259, KJC trades at 19.2x and 14.5x FY13E and FY14E PER, respectively. We are optimistic on the growth prospects of the company and initiate coverage with a BUY rating and a target price of Rs 325.

BUY KJC IN | CMP RS 259

TARGET RS 325 (+25%) Company Data

O/S SHARES (MN) : 74MARKET CAP (RSBN) : 19MARKET CAP (USDBN) : 0.352 ‐ WK HI/LO (RS) : 209 / 91LIQUIDITY 3M (USDMN) : 0.5FACE VALUE (RS) : 2

Share Holding Pattern, %

PROMOTERS : 53.5FII / NRI : 7.8FI / MF : 6.8NON PROMOTER CORP. HOLDINGS : 11.3PUBLIC & OTHERS : 17.7

Price Performance, % 1mth 3mth 1yr

ABS 18.8 49.2 153.5REL TO BSE 15.9 38.1 138.9

Price Vs. Sensex (Rebased values)

0

100

200

300

400

500

Apr‐10 Nov‐10 Jun‐11 Jan‐12 Aug‐12Kajaria Ceramics BSE Sensex

Source: Bloomberg, Phillip Capital Research

Other Key Ratios

Rs mn FY12 FY13E FY14E

Net Sales 13,130 15,889 18,869EBIDTA 2,062 2,396 2,944Net Profit 809 993 1,315EPS, Rs 11.0 13.5 17.9PER, X 23.6 19.2 14.5EV/EBIDTA, % 10.2 8.9 7.1EV/Net Sales, x 1.6 1.3 1.1ROE, % 31.5 30.4 31.5Source: PhillipCapital India Research Kapil Bagaria (+ 9122 6667 9965) [email protected] Vibhor Singhal (+ 9122 6667 9949) [email protected]

– 16 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

Investment Overview At the CMP of Rs 216, KJC trades at 19.2x FY13E and 14.5x FY14E PER, respectively. In terms of EV/EBIDTA, the stock trades at 8.9x and 7.1x, on FY13E and FY14E financials respectively. Given the superior cash flow generating ability of the business, established brand, consistent growth in revenues and profitability, efficient capital deployment and robust return ratios, we believe the company would continue to command higher valuations. We are optimistic on the growth prospects of the company and initiate coverage with a BUY rating and a target price of Rs 325. Challenges • The demand for tiles is discretionary in nature and is viewed as lifestyle enhancing.

Consumer sentiment plays a vital role in determining the demand for Tiles. Upbeat consumer confidence will lead to good demand for these products whereas vice‐versa is also very much applicable. Concerns over rise in prices of essential commodities and worries about employment prospects have dragged down the confidence of urban consumers in India during September 2012, says a study by financial services provider BluFin. BluFin's Consumer Confidence Index (CCI) slipped by 2.9 points from August to 36.7 in September. This was the biggest month‐on‐month decline to date for the index. This short term decline in the consumer confidence may lead to lower growth in the short term.

• Chinese products were posing stiff competition to the profitability of Indian tile manufacturers prior to 2008‐09. To safeguard the interest of the Indian manufacturers, anti‐dumping duty was levied on ceramic tiles in 2009. Currently, anti‐dumping duty of Rs 137 per SQM is imposed on ceramics tiles of over 16 cms in size and Rs 215 per SQM on all vitrified tiles imported from China. The date for review of this Anti‐dumping duty is being set as December 2014. If this duty is not retained it could pose a threat of cheaper imports after December 2014.

• Unorganised sector accounts for 50% of the total tiles industry. These unorganized players have lower fixed overheads enabling them to keep the pricing competitive and garner market share. Stiff competition from players in the unorganised segment can exert pressure on margins. We believe that KJC’s strategy to increase the brand awareness through advertisements and brand building initiatives will help it to compete with organised as well as unorganised players.

• During FY12, net imports of the company stood at ~18.5% of the net revenues (although lower as compared to 29.5% in FY11) but still the currency depreciation does impact the profitability of the company quite significantly. Thus sharp depreciation of rupee impacts the margins of the company adversely. We believe that the reducing trend in imports as a percentage of sales (due to enhanced in‐house manufacturing capabilities) will lower the volatility of profits on this account.

– 17 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

Assumptions and value drivers Key data and assumptions FY10 FY11 FY12 FY13E FY14E

Costs (Rs per MSM)

‐ Raw Material cost 49.5 56.4 49.6 50.1 49.9

‐ Staff Cost 60.1 103.2 67.3 67.9 67.7

‐ Power & Fuel cost 1.7 1.7 1.7 1.7 1.7

‐ Other Exp 5.9 4.5 3.7 4.3 4.3

‐ Advertising Expenses 14.3 9.8 16.0 16.0 16.0

‐ Total A&SP 8.3 8.0 8.2 8.2 7.9

‐ Interest Cost 26.5 20.0 26.6 26.7 26.5

‐ Depreciation 5.1 3.2 3.7 3.0 2.5

Margins

‐ Gross margin per MSM 146.8 139.6 168.2 182.2 191.2

‐ EBIDTA Margin per MSM 48.5 41.3 47.3 50.3 51.7

‐ PAT Margin per MSM 15.6 15.5 15.7 15.1 15.6

‐ Gross Margin % 12.1 12.5 12.8 12.3 13.1

‐ EBIDTA Margins % 7.0 9.4 9.1 9.4 10.6

‐ EBIT Margins % 4.9 6.4 6.2 6.4 7.2

‐ PBT Margins % 45.4 49.8 52.4 55.1 59.6

‐ PAT Margins % 14.2 20.4 20.5 22.8 26.6

Sales

‐ Volumes 25.3 29.7 39.4 43.5 49.4

YoY growth, % 11.9 17.5 32.5 10.5 13.5

‐ Realisation (Rs per MSM) 302.8 337.7 355.3 362.4 369.7

YoY growth, % (0.8) 11.5 5.2 2.0 2.0

‐ Realisation (Rs per SQFT) 28.1 31.4 33.0 33.7 34.3

Share of Total Sales

‐ Mfg Sales as % of Total Sales 62.5 54.7 62.8 63.2 64.4

‐ Outsourced Sales as % of Total Sales 37.5 45.3 37.2 36.8 35.6

‐ Ceramic Tiles as % of Total Sales 63 51 48 46 44

‐ Polishes Vitirified Tiles as % of Total Sales 23 33 36 37 39

‐ Glazed Vitirified Tiles as % of Total Sales 8 12 10 10 10

‐ Kajaria World as % of Total Sales 5 3 5 6 6

‐ Bathware / Wooden as % of total Sales ‐ 0.8 1.1 1.1 1.1

Source: Company, PhillipCapital India Research Estimates

Working Capital

Days FY10 FY11 FY12 FY13E FY14E

Inventory Turnover 70 59 52 53 54

Debtor Turnover 38 36 40 40 39

Creditor Turnover 60 91 74 70 65

Source: Company, PhillipCapital India Research Estimates

– 18 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

Company Overview • Kajaria Ceramics is the largest manufacturers of ceramic and vitrified tiles in India

with an annual aggregate capacity of 41 MSM. Founded more than two decades ago by Mr. Ashok Kajaria, it is today the second largest in terms of revenues in the country only to H&R Johnson. The manufacturing capacities are distributed across six plants – Sikandrabad in Uttar Pradesh, Gailpur in Rajasthan, three plants in Morbi in Gujarat and one at Vijayawada in Andhra Pradesh. Its Gailpur plant is India’s largest tile manufacturing capacity in a single location with installed capacity of 20.1 MSM. KJC is a member of the Indian Green Building Council, reassuring that its products are eco‐friendly. It is the world’s only ceramic tile company to receive the ISO:50001 certificate (for energy conservation).

• KJC has increased its capacity from 1 MSM to 41 MSM in last 23 years and offers more than 800 options in ceramic wall & floor tiles, vitrified tiles, designer tiles and much more. These tiles come in a wide range of colours and textures to complement bathrooms, living rooms, corridors, study rooms & kitchen. It has pioneered the digitally polished glazed vitrified tiles in India (60x60cm).

• The company’s products are marketed across India through an extensive distribution network of dealers (825), sub‐dealers, company‐owned showrooms and also through the project sales to major real estate developers. It derives 70% of its revenue from retail customers, while institutional sales account for 30%.

• Over the years, the company has developed three pillars of growth – namely State of the art huge installed capacities, pan‐India distribution network to reach out to the consumers and the Kajaria brand.

• KJC forayed into the high‐end sanitaryware business which positions the company as a complete bathroom solution provider by way of tie up with VitrA (Eczacibasi Group from Turkey) and also established a foothold in wooden flooring solutions, by way of import from China.

• The sales volume for the company has increased at 17.3% CAGR during FY08‐12 period as they jumped from 20.8 MSM in FY08 to 39.4 MSM in FY12. Consequently the net revenues for the company rose by 27.1% from Rs 5bn in FY08 to Rs 13bn in FY12. EBIDTA during the said period has also increased at a CAGR of 26% from Rs 819mn in FY08 to Rs 2,062mn in FY12. PAT for the period from FY08‐12 has registered a CAGR of 52.3% as it increased from Rs 150mn in FY08 to Rs 809mn in FY12.

Manufacturing facilities The company has manufacturing capacities distributed across six plants‐Sikandrabad in Uttar Pradesh, Gailpur in Rajasthan, three plants in Morbi in Gujarat and one at Vijayawada in Andhra Pradesh. The current manufacturing capacity of the company stands at 41 MSM across all the plants. Its Gailpur plant is India’s largest tile manufacturing capacity in a single location with installed capacity of 20.1 MSM. KJC is a member of the Indian Green Building Council, reassuring that its products are eco‐friendly.

– 19 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

Production Capacities

21.0 19.6 21.9 24.2

2.4 8.011.1

13.83.0

3.0

3.0

‐

10.0

20.0

30.0

40.0

FY10 FY11 FY12 FY13E

Ceramic Glazed Tiles Polished Vitrified Tiles Glazed Vitrified Tiles

Source: Company, PhillipCapital India Research Estimates

Plant wise and segment wise capacities Plant (MSM) Ceramic Tiles Polished Vitrified Glazed Vitrified Total

Sikandarabad, UP 3.2 5.0 ‐ 8.2Gailpur, Rajasthan 14.1 3.0 3.0 20.1Jaxx, Morbi, Gujarat ‐ 3.1 ‐ 3.1Soriso, Morbi, Gujarat 4.6 ‐ ‐ 4.6Vennar, Vijaywada, AP 2.3 ‐ ‐ 2.3Cosa, Morbi, Gujarat ‐ 2.7 ‐ 2.7Total 24.2 14.8 3.0 41.0

Source: Company, PhillipCapital India Research Estimates

Diversified product range and Robust Distribution Network • KJC offers more than 800 options in ceramic wall & floor tiles, vitrified tiles, designer

tiles and much more. These tiles come in a wide range of colours and textures to complement bathrooms, living rooms, corridors, study rooms & kitchen. It has pioneered the digitally polished glazed vitrified tile in India (60x60cm).

Product Range Ceramic Wall & Floor Tiles Polished Vitirified Tiles Glazed Vitrified Tiles Sizes 11 3 2 Designs 750 60 more than 100 Price Range (Rs per MSM) 200 to 900 400‐1200 600‐1200 Sourcing Own Manufacturing, JVs and Outsourcing Own Manufacturing, JVs and Imports Own Manufacturing and Imports Distribution Dealers and Sub‐dealers, Kajaria Prima and

Kajaria Galaxy Dealers, Kajaria Studio and Kajaria Galaxy

Dealers, Kajaria Eternity Studio, Kajaria Galaxy and Kajaria World

Contribution to Net Sales 47% 36% 10% Manufactured at Gailpur, Sikandarabad, Soriso, Vennar Gailpur, Sikandarabad, Jaxx, Cosa Gailpur Source: Company, PhillipCapital India Research Estimates

• KJC’s products reach across the country through an extensive distribution network of dealers, sub‐dealers and own showrooms. The imported tiles are marketed through the Kajaria World retail chain.

• The company’s products are marketed across India through an extensive distribution network of dealers (825), sub‐dealers, company‐owned showrooms and also through the project sales to major real estate developers. It derives 70% of its revenue from retail customers, while institutional sales account for 30%.

• The company has very unique strategy of extending the distribution network deeper into under‐penetrated pockets – primarily the Tier‐II and III towns pan‐India – creating a ‘demand pull’ for its products. In doing so, the company ensures that the sales mix to retail remains dominant.

Production Capacity expansion through Greenfield projects, Brownfield projects and Acquisitions

– 20 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

Investment Thesis

Shift in the product mix leads to improved margins The Company embarked on a strategy of brownfield capacity expansion projects and inorganic growth over the last 5 years to increase capacity and also product offering, thereby manufacturing the value added products in‐house. The increased in‐house production of the value‐added products like Glazed Vitrified Tiles has led to sharp increase in the realizations and profitability for the company in the last 5 years. KCL acquired a 51% stake in Soriso Ceramics in February 2011 and doubled its capacity to 4.6 MSM, which got operational in March 2012. Similarly, the company acquired a 51% stake in Jaxx Vitrified having a capacity of 3.1 MSM in February 2012 and also Vennar Ceramics with a capacity of 2.3 MSM in April 2012. KCL spent Rs 256mn on three acquisitions and made Rs 30mn equity contribution to expand Soriso’s capacity in FY12 (capex incurred by Soriso was Rs 135mn), which got operational in March 2012 and will contribute to revenues in FY13. The company has recently acquired 51% stake in Cosa Ceramics Private Ltd., based in Morbi, Gujarat with capacity of 2.7mn sqm of polished vitrified tiles for consideration of Rs 116mn. This is the company’s 4th acquisition which takes its total capacity to 41 MSM while capacity under JVs increased to 12.7 MSM contributing 30% of total capacity. Increasing Realisation with increase in value added tiles

21.0 19.6 21.9 24.2 24.2

2.4 8.0

11.113.8 13.8

3.0

3.0

3.0 3.0

‐

10.0

20.0

30.0

40.0

FY10 FY11 FY12 FY13E FY14E

280

320

360

400

Ceramic Glazed Tiles Polished Vitrified Tiles

Glazed Vitrified Tiles - Realisation (Rs per MSM)

Source: Company, PhillipCapital India Research Estimates

The Company’s sales mix altered in favour of high‐end tiles consequent to the launch of unique products which met customer aspirations and were well accepted in the markets. The newly launched digital printing (on ceramic and vitrified tiles) enhanced realizations significantly. The share of outsourced sales as a percentage of total revenues of the company are also expected to see declining trend as the company has made 4 JVs (with 51% stake in each) over the last 2 years leading to more production coming out of owned JV units. This will help the company to maintain or improve margins as the production is under control. Outsourced sales as % of total sales

Realisation per MSM improving on the back of premiumisation as the share of Polishes and Glazed Vitrified Tiles increases in the total volumes of the company

– 21 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

37.5

45.3

37.2 36.835.6

30.0

35.0

40.0

45.0

50.0

FY10 FY11 FY12 FY13E FY14E

Source: Company, PhillipCapital India Research Estimates

One more factor which has a significant impact on the profitability of the company is the foreign currency movement as most of the outsourced products of the company are imported. Increase in EBIDTA per MSM with increase in share of value added tiles

6351 48 46 44

2333 36 37

8 12 10 10 105 3 5 6

39

6

‐

20

40

60

80

100

FY10 FY11 FY12 FY13E FY14E

40

50

60

70

- Ceramic Tiles as % of Total Sales - Polishes Vitirified Tiles as % of Total Sales - Glazed Vitirified Tiles as % of Total Sales - Kajaria World as % of Total Sales - EBIDTA Margin per MSM

Source: Company, PhillipCapital India Research Estimates

Market share increase with focus on brand building Presently as per the company presentation the total tiles industry is estimated to be Rs 170bn. Out of which 50% of the market is covered by National players and another 50% by smaller unorganized players. The industry has seen revenue CAGR of 15‐16% in last 4‐5 years. In terms of installed tiles manufacturing capacity KJC is the largest player today in the country and second‐largest in terms of revenue after H&R Johnson Gain in market share

EBIDTA per MSM increased from Rs 45 in FY10 to Rs 52 in FY12, it is expected to further increase to Rs 55 in FY13E and Rs 60 in FY14E as the product mix shift turns favourable

– 22 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

18.519.9 20.3

11.913.6

16.6

‐

5

10

15

20

25

FY10 FY11 FY12

‐

10

20

30

40

50

Mkt Share for HRJ, % Mkt Share for KJC, %

HRJ YoY Sales growth, % KJC YoY Sales growth, %

Source: Company, PhillipCapital India Research Estimates

As per FY12 data, KJC enjoys ~16.6% market share in the National Brands segment. Over the years, the company has narrowed the gap between itself and the largest player H&R Johnson. The market share for KJC has increased from 11.9% in FY10 to 13.6% in FY11 and then to 16.6% in FY12. KJC reported revenue growth of 40.2% during FY12 as against 17.4% revenue growth reported by H&R Johnson. KJC has consistently pursued the strategy to focus on retail distribution and increase its retail presence, whereas HRJ is more focused on government projects and thus KJC has benefitted from the brand building initiatives as the consumers become more brand conscious.

Revenue growth of 19.9% during FY12‐14E We expect revenue to grow at a CAGR of 19.9% for FY12‐FY14E for the company on the back of volume growth of 12%. We estimate volumes to climb to 43.5 MSM in FY13E (YoY increase of ~10.5%) and then to 49.4 MSM in FY14E (YoY growth of 13.5%), registering a CAGR of 12% in FY12‐FY14E. The high‐margin value‐added Vitrified Tiles segment is expected to grow faster than the Ceramic Tiles segment. We estimate the share of Ceramic Tiles to decrease from 48% in FY12 to ~44% in FY14E. This share has already seen a decline from 63% in FY10 to 48% in FY12. The share of Vitrified Tiles (Glazed as well as Polished) as a percentage of total sales is expected to increase from 46% in FY12 to ~49% in FY14E. Thus, we expect the high‐margin business to increase its share to the total revenues at the expense of the low‐margin businesses, leading to better realisation and better profitability.

Growing faster than the industry leader and gaining market share

– 23 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

Net Sales Growth

7,3559,523

13,130

18,869

15,889

0

5,000

10,000

15,000

20,000

FY10 FY11 FY12 FY13E FY14E

0

10

20

30

40

50Net Sales (Rs Mn) % YoY Change

Source: Company, PhillipCapital India Research Estimates

We estimate net sales to increase from Rs 13130mn in FY12 to Rs 15889mn in FY13E, YoY growth of 21% on the back of volume growth of 10.5% YoY to 43.5 MSM. In FY14E, we estimate volume growth to the tune of 13.5% YoY to 49.4 MSM and the net sales are expected to grow at 18.7% YoY to Rs 18869mn. Growth in Sales Volumes

25.3

29.7

39.443.5

49.4

0

10

20

30

40

50

FY10 FY11 FY12 FY13E FY14E

0

10

20

30

40Sales Qty (MSM) YoY Change, %

Source: Company, PhillipCapital India Research Estimates

EBIDTA estimated to register a CAGR of 19.5% in FY12‐14E We estimate the EBIDTA to increase from Rs 2062mn in FY12 to Rs 2396mn (YoY growth of 16.2%) in FY13E and then to Rs 2944mn (YoY growth of 22.9%) in FY14E. We expect the margins to improve gradually from Rs 52.4 per MSM in FY12 to Rs 59.6 per MSM in FY14E. The improvement in margins is on account of the following factors: • Increasing share of Vitrified Tiles in the total net revenues of the company. • The aforementioned factor would lead to the increase in the realisation per MSM by

2% in the said period. The increasing volumes are expected to bring operational leverage as volumes expand over the next two years. The sales classification, in terms of product segments and raw material prices, will be the major determinants of margins, going forward.

Revenue growth to be aided by ~12% CAGR in volumes during FY12‐14E

– 24 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

EBIDTA Growth and Margins

1,1481,479

2,0622,396

2,944

0

1,000

2,000

3,000

FY10 FY11 FY12 FY13E FY14E

40

45

50

55

60EBIDTA (Rs Mn) EBIDTA per MSM (Rs)

Source: Company, PhillipCapital India Research Estimates

No major capex expected in the short term The company has invested considerable amount in increasing its installed capacities and product categories by way of green field expansions, brown field expansions and acquisitions. The installed tiles manufacturing capacity for the company has increased from 23.4 MSM in FY10 to 41 MSM currently, an increase of ~75% in last 3 years. During this period it has invested over Rs 2.5bn in enhancing its manufacturing capabilities. The increase in the gross block has led to increase in the depreciation for the company. But depreciation as a percentage of sales has declined considerably from 3.6% in FY10 to 3% in FY12 as the company has been able to sweat its assets better. The depreciation as a percentage of sales is expected to decline from 3% in FY12 to 2.8% in FY13E and to 2.6% in FY14E as well. The company does not plan to add further capacity in the coming two years and hence in‐house manufacturing capex would be lower at ~Rs 300mn each year. For the future inorganic growth route also, KCL plans to acquire a 51% stake in a entity from the promoters rather than acquiring the entire stake, in line with its past three acquisitions, which would reduce acquisition cost

EBIDTA margins to improve with better product mix and higher operating leverage

– 25 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

Depreciation as a percentage of sales to decline

267 297393

451497

0

150

300

450

600

FY10 FY11 FY12 FY13E FY14E

2.0

2.5

3.0

3.5

4.0Depreciation (Rs Mn) % of Sales

Source: Company, PhillipCapital India Research Estimates

Most of the funding of these capacity enhancement initiatives has been done through internal accruals. The cashflow for the company has improved significantly over the last 3‐4 years on account of robust sales growth and working capital efficiencies. The increased cashflow helped the company to reduce the debt over the last 3 years. Total debt has come down from Rs 3.3bn in FY09 to Rs 2.1bn in FY12. This decline in the total debt has led to reduce the interest outgo for the company. The interest levels have come down significantly from the levels of FY10, when the interest as a percentage of EBIDTA touched a high of 32.7% but there on it has been on a gradual downward trend. The interest to EBIDTA declined to 23.5% in FY12. This is estimated to decline in the next two years to 19.6% in FY13E and 16.1% in FY14E as there are no incremental fund requirements, except for the working capital. Interest as a percentage of sales has also declined from 5.1% in FY10 to 3.7% in FY12 and is further estimated to decline to 3% and 2.5% respectively in FY13E and FY14E. Interest as a percentage of ebidta

0

1,000

2,000

3,000

FY10 FY11 FY12 FY13E FY14E

0

10

20

30

40

EBIDTA (Rs Mn) Interest Cost (Rs Mn) Interest as % of EBIDTA

Source: Company, PhillipCapital India Research Estimates

Interest and Depreciation as a percentage of sales to decline in the coming years

– 26 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

Improved Working Capital situation leading to controlled increase in Capital Employed Despite the robust increase in the sales of ~34% during FY10‐12 period the company has been able to manage the working capital very efficiently. The inventory turnover days have come down from 70 days in FY10 to 52 days in FY12. We expect it to stablise at these levels in the coming years as well. The debtor turnover has been consistent at between 37‐40 days over the last 4‐5 years. The efficient management of working capital and judicious initiatives on capacity expansions has led to controlled increase in the overall Capital Employed for the company. Capital Employed has increased from Rs 5.1bn in FY10 to Rs 5.6bn in FY12 and we further expect it to go up to Rs 6.6bn in FY13E and then to Rs 7.5bn in FY14E Capital employed, inventory and debtor days

5,0705,726 5,597

6,636

7,537

‐

2,000

4,000

6,000

8,000

FY10 FY11 FY12 FY13E FY14E

20

40

60

80

Capital Employed (Rs Mn) Inventory Days Debtor Days

Source: Company, PhillipCapital India Research Estimates

Above factors lead to consistent free cash flow As discussed above KJC has managed its working capital and balance sheet very efficiently even as compared to the competitors. Over the last 5 years the company has generated cumulatively operating cash flow to the tune of ~Rs 3.3bn. During the same period the company generated free cash flow to the tune of ~Rs 1.6bn as the company carried out capacity expansions and acquisitions during this period. Now as the in‐house manufacturing facilities have come to a reasonable size and the company has established its brand, we expect the company to reap sweet fruits in the coming years. Over the period of FY12‐14E we expect the company to generate operating cash flows to the tune of Rs 2.8bn and free cash flow to the tune of Rs 765mn

Sustained efforts to keep the working capital cycle in check

– 27 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

Operating cash flow and free cash flow

927

1,725 1,733

1,389 1,434

(14)

1,056

574

463

191

‐500

0

500

1,000

1,500

2,000

FY10 FY11 FY12 FY13E FY14E

Operating Cash Flow (Rs Mn) Free Cash Flow (Rs Mn)

Source: Company, PhillipCapital India Research Estimates

PAT to grow at 27.5% in FY12‐14E On the back of a robust increase in the estimated EBIDTA (CAGR of 19.5% in FY12‐FY14E) and lower interest and depreciation, we expect the company to post PAT CAGR of 27.5% in the said period. The growth in EBIDTA will be aided by the lower depreciation, as a percentage of sales, over the next two years (as discussed earlier) and lower interest cost as a percentage of EBIDTA. The tax rate for the company is estimated to remain in the range of 32% of PBT over the next two years. We expect the company to register PAT of Rs 993mn (YoY growth of 22.8%) in FY13E and then expect it to grow to Rs 1315mn in FY14E (YoY growth of 32.4%). Similarly, the EPS of the company is expected to grow from Rs 11 in FY12E to Rs 13.5 in FY13E and then to Rs 17.9 in FY14E PAT growth and margins

359

606809

993

1,315

4.9

6.46.2 6.3

7.0

0

350

700

1,050

1,400

FY10 FY11 FY12 FY13E FY14E

4.0

5.0

6.0

7.0

8.0PAT (Rs Mn) % Margin

Source: Company, PhillipCapital India Research Estimates

Lower working capital requirement and capex needs to lead to better cash flows in the coming years

– 28 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

Return ratios to improve over the next two years Given the increase in the share of value added products in the total sales mix for the company over the next two years, we expect PAT margins to increase from 6.2% in FY12 to 7% in FY14E gradually. Also, the company has almost concluded a major capacity expansion programme and the capacities are expected to stablise in the next two years, leading to better asset turnover. We estimate the asset turnover ratio for the company to improve from 2.2x in FY12 to 2.7x by FY14E.

Improving asset turnover and net margins

1.0

1.5

2.0

2.5

3.0

FY10 FY11 FY12 FY13E FY14E

Asset Turnover, x

4.5

5.5

6.5

7.5

FY10 FY11 FY12 FY13E FY14E

% Margin

Source: Company, PhillipCapital India Research Estimates

We believe that the above‐mentioned factors will lead to an improved Return on Capital Equity for the company over the next two years. We expect the ROCE to improve from 24.5% in FY12 to 26.5% in FY13E and then further to 28.5% in FY14E. Also, the Return on Equity is expected to remain consistently over the 30% mark during the next 2 years. ROE & ROCE to improve, going forward

10.0

15.0

20.0

25.0

30.0

35.0

FY10 FY11 FY12 FY13E FY14E

ROE, % ROCE, %

Source: Company, PhillipCapital India Research Estimates

ROCE to improve over the next 2 years and ROE to remain over 30% in the same period

– 29 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

Sector Outlook

Global Tile Industry The global tile industry has shown a ~6% CAGR over CY06‐10 to 9350 MSM in terms of volumes. Following rising manufacturing costs, there has been a shift in manufacturing capacity from developed countries. This is visible from the fact that Spain, the second‐largest producer of tiles in CY03, witnessing a 7.4% CAGR decline over CY03‐10. Similarly, Italy, the fourth‐largest producer of tiles in CY03, witnessed a 6.1% CAGR decline over the same period. At the cost of producers in developed countries, China and India have benefited the most, witnessing 10.4% and 12.6% production CAGR, respectively, over the same period. Currently, China, Brazil and India are top three producers as well as consumers of tiles globally. China accounted for 44%/37.4%, Brazil accounted for 7.9%/7.5% while India accounted for 5.8%/6.0% of the world’s production/consumption of tiles, respectively, in CY10. World tile consumption

(MSM) CY06 CY07 CY08 CY09 CY10

China 2450 2700 2830 3030 3500

Brazil 484 535 605 645 700

India 350 397 403 494 557

Iran 182 236 265 295 335

Vietnam 145 210 220 240 330

Indonesia 148 178 262 297 277

Egypt 103 105 140 180 200

Usa 308 249 211 173 186

Saudi Arabia 95 110 136 166 182

Mexico 167 173 176 163 168

Total 7420 8060 8350 8460 9350

Source: Company, PhillipCapital India Research Estimates

Indian Tile Industry The per capita tile consumption in India is amongst the lowest in the world at 0.46 SQM.

2.61

3.67

0.46

4.42

3.84

1.17

2.47

0

1

2

3

4

5

China Brazil India Iran Vietnam Indonesia Egypt

Source: Company, PhillipCapital India Research Estimates

Lowest per capita consumption of Tiles globally

– 30 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

Indian tile industry was around 557 MSM as of March 2011 and estimated to be 625 MSM as of March 2012. The size of the industry is estimated to be ~Rs 170bn as of March 2012 and 50% of the market is expected to be controlled by the National Brands and rest by the regional local brands. The industry has been growing at a healthy rate of 15‐16% CAGR over the last 4‐5 years. Rs mn FY12 Turnover

H&R Johnson 17290

Kajaria Ceramics 14070

Nitco Tiles 9590

Somany Ceramics 9270

Asian Granito 6220

RAK Ceramics 6000

Orient Bell Ceramics 5840

Varmora 3560

Murudeshwar Ceramics 1900

Regency Ceramics 1660

Euro Ceramics 1600

Bell Granito 1400

Others (Marbomax, Restile, Decolight, Marbito, Spartek etc) 6600

Total 85000

Source: Company, PhillipCapital India Research Estimates

H&R Johnson (20% market share) today is the largest tile company in terms of revenues whereas Kajaria is currently the second largest player with ~16.5% market share.

Segmentation in the Indian Tiles industry

Glazed Vitrified Tiles (20 MSM/ Rs 10bn)

Polished Vitrified Tiles(205 MSM / Rs 70bn)

Ceramic Glazed Tiles(400 MSM / Rs 90bn)

The company has manufacturing capacity of 8 MSM at Gailpur (Rajasthan) and Sikandrabad (UP) put up between Feb’11 & March’11 substituting the imports from China significantly. Also acquired 51% stake in Jaxx Vitrified in Feb’12 further reducing the import portion to 40% of the PVT sale and now with Cosa acquisition it has further enhanced its manufacturing capacity to 13.80 MSM

KJC has manufacturing capacity of 17.30 MSM at Gailpur (Rajasthan) and Sikandrabad (UP). Also acquired 51% Soriso (morbi) in February 2011 & Vennar Ceramics (AP) in April 2012. Total aggregate capacity currently stands at

24.20 MSM.

KJC has manufacturing capacity of 3 MSM at Gailpur (Rajasthan),

put up in March 2011 substituting the imports from Europe and China significantly.

10 MSM Imported

4 MSM Imported

15 MSM Imported

Glazed Vitrified Tiles (20 MSM/ Rs 10bn)

Polished Vitrified Tiles(205 MSM / Rs 70bn)

Ceramic Glazed Tiles(400 MSM / Rs 90bn)

The company has manufacturing capacity of 8 MSM at Gailpur (Rajasthan) and Sikandrabad (UP) put up between Feb’11 & March’11 substituting the imports from China significantly. Also acquired 51% stake in Jaxx Vitrified in Feb’12 further reducing the import portion to 40% of the PVT sale and now with Cosa acquisition it has further enhanced its manufacturing capacity to 13.80 MSM

KJC has manufacturing capacity of 17.30 MSM at Gailpur (Rajasthan) and Sikandrabad (UP). Also acquired 51% Soriso (morbi) in February 2011 & Vennar Ceramics (AP) in April 2012. Total aggregate capacity currently stands at

24.20 MSM.

KJC has manufacturing capacity of 3 MSM at Gailpur (Rajasthan),

put up in March 2011 substituting the imports from Europe and China significantly.

10 MSM Imported

4 MSM Imported

15 MSM Imported

Source: Company, PhillipCapital India Research Estimates

– 31 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

Absolute Rolling Valuation Band Charts

PE band

3x

6x

9x

12x

0

50

100

150

200

250

Apr‐06 Apr‐07 Apr‐08 Apr‐09 Apr‐10 Apr‐11 Apr‐12

Rs

PBV band

1x

2x

3x

4x

0

50

100

150

200

250

300

Apr‐06 Apr‐07 Apr‐08 Apr‐09 Apr‐10 Apr‐11 Apr‐12

Rs

MCap/Sales band

0.2x

0.4x

0.6x

0.8x

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

Apr‐06

Apr‐07

Apr‐08

Apr‐09

Apr‐10

Apr‐11

Apr‐12

Rs mn

EV/EBIDTA band

3x

6x

9x

12x

0

5000

10000

15000

20000

25000

30000

35000

40000

Apr‐06

Apr‐07

Apr‐08

Apr‐09

Apr‐10

Apr‐11

Apr‐12

Rs mn

EV/Sales band

0.4x

0.6x

0.8x

1x

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

Apr‐06

Apr‐07

Apr‐08

Apr‐09

Apr‐10

Apr‐11

Apr‐12

Rs mn

Source: Company, PhillipCapital India Research

– 32 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / KAJARIA CERAMIC

Financials (Consolidated)

Income Statement Y/E Mar, Rs mn FY11 FY12 FY13E FY14E

Net sales 9,523 13,130 15,889 18,869

Growth, % 29.5 37.9 21.0 18.7

Other income 11 15 15 19

Total income 9,534 13,145 15,904 18,888

Operating expenses ‐8,044 ‐11,068 ‐13,493 ‐15,924

EBITDA 1,479 2,062 2,396 2,944

Growth, % 28.8 39.4 16.2 22.9

Margin, % 15.5 15.7 15.1 15.6

Depreciation ‐297 ‐393 ‐451 ‐497

EBIT 1,182 1,669 1,944 2,447

Growth, % 34.1 41.2 16.5 25.9

Margin, % 12.4 12.7 12.2 13.0

Interest paid ‐301 ‐485 ‐469 ‐473

Pre‐tax profit 892 1,199 1,490 1,993

Tax provided ‐285 ‐381 ‐477 ‐638

Profit after tax 607 818 1,013 1,355

Net Profit 606 809 993 1,315

Growth, % 69.1 33.4 22.8 32.4

Unadj. shares (m) 74 74 74 74

Wtd avg shares (m) 74 74 74 74

Balance Sheet Y/E Mar, Rs mn FY11 FY12 FY13E FY14E

Cash & bank 38 72 48 165

Debtors 942 1,442 1,756 2,036

Inventory 1,546 1,865 2,304 2,774

Loans & advances 811 549 659 758

Total current assets 3,338 3,928 4,767 5,733

Investments 34 1 401 601

Gross fixed assets 7,178 7,865 8,666 9,296

Less: Depreciation ‐2,263 ‐2,656 ‐3,107 ‐3,604

Add: Capital WIP 1 24 20 50

Net fixed assets 4,916 5,233 5,579 5,742

Non‐current assets 0 1 0 0

Total assets 8,287 9,162 10,747 12,076

Current liabilities 3,238 4,352 5,086 5,460

Provisions 389 357 421 480

Total current liabilities 3,627 4,709 5,507 5,941

Non‐current liabilities 2,435 1,633 1,682 1,562

Total liabilities 6,062 6,341 7,190 7,503

Paid‐up capital 147 147 147 147

Reserves & surplus 2,078 2,673 3,410 4,426

Shareholders’ equity 2,225 2,821 3,557 4,573

Total equity & liabilities 8,287 9,162 10,747 12,076

Source: Company, PhillipCapital India Research Estimates

Cash Flow Y/E Mar, Rs mn FY11 FY12 FY13E FY14E

Pre‐tax profit 892 1,199 1,490 1,993

Depreciation 297 393 451 497

Chg in working capital 679 664 ‐111 ‐462

Total tax paid ‐142 ‐523 ‐442 ‐594

Cash flow from operating activities 1,725 1,733 1,389 1,434

Capital expenditure ‐1,739 ‐710 ‐798 ‐660

Chg in investments 0 33 ‐400 ‐200

Cash flow from investing activities ‐1,739 ‐677 ‐1,198 ‐860

Free cash flow ‐14 1,056 191 574

Equity raised/(repaid) ‐46 0 0 0

Debt raised/(repaid) 178 ‐896 0 ‐200

Dividend (incl. tax) ‐86 ‐171 ‐214 ‐257

Cash flow from financing activities 46 ‐1,067 ‐214 ‐457

Net chg in cash 32 ‐11 ‐23 117

Valuation Ratios & Per Share Data FY11 FY12 FY13E FY14E

EPS, Rs 8.2 11.0 13.5 17.9

BVPS, Rs 30.5 39.3 49.6 63.9

DPS, Rs 2.0 2.5 3.0 3.5

Return on assets (%) 10.8 12.9 13.2 14.5

Return on equity (%) 29.3 31.5 30.4 31.5

Return on Invested capital (%) 14.3 19.1 21.2 24.0

RoIC/Cost of capital (x) 1.1 1.4 1.5 1.7

RoIC ‐ Cost of capital (%) 1.2 5.3 7.3 10.2

Return on capital employed (%) 18.3 24.5 26.5 28.5

Cost of capital (%) 13.1 13.8 13.9 13.8

RoCE ‐ Cost of capital (%) 5.2 10.7 12.6 14.7

Asset turnover (x) 1.7 2.2 2.5 2.7

Sales/Total assets (x) 1.3 1.5 1.6 1.7

Sales/Net FA (x) 2.3 2.6 2.9 3.3

Receivable days 36.1 40.1 40.3 39.4

Inventory days 59.3 51.8 52.9 53.7

Payable days 90.7 73.8 69.6 64.9

Current ratio (x) 0.9 0.9 0.9 1.0

Quick ratio (x) 0.5 0.4 0.5 0.5

Interest cover (x) 3.9 3.4 4.1 5.2

Dividend cover (x) 4.1 4.4 4.5 5.1

PER (x) 31.4 23.6 19.2 14.5

Price/Book (x) 8.5 6.6 5.2 4.1

EV/EBIT (x) 18.5 12.6 11.0 8.6

EV/NOPLAT (x) 27.2 18.5 16.1 12.6

EV/CE 4.7 4.6 4.0 3.4

EV/IC (x) 3.9 3.5 3.4 3.0

– 33 of 94 –

HSIL Ltd. Leader in Sanitary ware business

MIDCAP: HOME DÉCOR |Initiating Coverage 4 December 2012

PhillipCapital (India) Pvt. Ltd.

HSIL is the leader in the domestic Sanitaryware market and the second largest player in the container glass segment. HSIL has established an extensive distribution channel and brand over a period of years. We initiate coverage on HSIL with a BUY rating. Investment Rationale • HSIL is the leading player in the sanitaryware market with a ~40% share by

revenue in the organised space. Its brand Hindware has a very significant recall as compared to the competitor brands. The company sells its products through a wide distribution network of ~2,000 dealers and ~15,000 retailers making it the most penetrated player in the sanitaryware segment.

• HSIL is the second largest player in the domestic container glass industry with ~18% market share in terms of revenues and 20% market share in terms of capacity. It is one of the leading players in the South India market with ~60% of the total container glass capacity.

• For FY09‐12 period, HSIL has shown healthy CAGR growth of 33.4% and 29.3% in Revenue and PAT, respectively. The company has been in a capacity expansion phase for the last 4 years in both its business segments to drive this growth. The gross fixed assets of the company have increased from Rs 6.5bn in FY09 to Rs 15.5bn in FY12 and are further expected to increase to Rs 20.4bn by FY14E. Despite this big capital expenditure the balance sheet of the company remains strong with the debt to equity at 0.8x in FY12.

• We expect consolidated revenues to register a CAGR of 19.3% for FY12‐14E to reach Rs 20.8bn in FY14E from Rs 14.6bn in FY12. We expect the EBIDTA margins to consolidate at around 17% in the next two years and thus estimate the EBIDTA to grow at a CAGR of 18.5% in FY12‐14E period. PAT for the period is expected to grow at a CAGR of 16.5% to Rs 1272mn in FY14.

Outlook and Valuations Given the market leadership in business segments, superior brand recall, extensive distribution reach, cash flow generating ability of the sanitary ware business, consistent growth in revenues and profitability, we believe the company would see re‐rating in the coming years. As the capacity utilization of the new assets moves up, the profitability of the company will see major boost. We estimate the EPS to grow at 16.5% CAGR in FY12‐14E period. At the CMP of Rs 137, HSIL trades at 10.1x and 7.1x FY13E and FY14E PER, respectively, which we believe, are attractive valuations. We are positive on the growth prospects of the company and initiate coverage with a BUY rating and a target price of Rs 193.

BUY HSI IN | CMP RS 137

TARGET RS 193 (+41%) Company Data

O/S SHARES (MN) : 66MARKET CAP (RSBN) : 8MARKET CAP (USDBN) : 0.252 ‐ WK HI/LO (RS) : 181 / 104LIQUIDITY 3M (USDMN) : 0.3FACE VALUE (RS) : 2

Share Holding Pattern, %

PROMOTERS : 51.6FII / NRI : 29.7FI / MF : 2.7NON PROMOTER CORP. HOLDINGS : 2.2PUBLIC & OTHERS : 13.9

Price Performance, % 1mth 3mth 1yr

ABS 18.3 30.3 ‐9.0REL TO BSE 15.4 19.3 ‐23.6

Price Vs. Sensex (Rebased values)

0

50

100

150

200

250

300

350

Apr‐10 Jan‐11 Oct‐11 Jul‐12

HSIL BSE Sensex

Source: Bloomberg, Phillip Capital Research

Other Key Ratios

Rs mn FY12 FY13E FY14E

Net Sales 14,628 17,704 20,811EBIDTA 2,498 2,794 3,507Net Profit 937 898 1,272EPS, Rs 14.2 13.6 19.3PER, X 9.7 10.1 7.1EV/EBIDTA, x 6.5 6.1 4.8EV/Net Sales, x 1.1 1.0 0.8ROE, % 11.4 9.0 11.8Source: Phillip Capital India Research Kapil Bagaria (+ 9122 6667 9965) [email protected] Vibhor Singhal (+ 9122 6667 9949) [email protected]

– 34 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / HSIL LTD.

Investment Overview At the CMP of Rs 137, HSIL trades at 10.1x FY13E and 7.1x FY14E PER, respectively. In terms of EV/EBIDTA, the stock trades at 6.1x and 4.8x, respectively, on FY13E and FY14E financials. Given the market leadership in business segments, superior brand recall, extensive distribution reach, cash flow generating ability of the sanitary ware business, consistent growth in revenues and profitability, we believe the company would see re‐rating in the coming years. As the capacity utilization of the new assets moves up the profitability of the company will see major boost. We are positive on the growth prospects of the company and initiate coverage with a BUY rating and a target price of Rs 193. Challenges • Soda ash is one of the important raw materials for container glass segment of HSIL

and is mostly imported. It constitutes around ~14% of glass manufacturing cost and ~34% of HSIL’s overall material cost. A sharp volatility in prices could impact margins in the segment.

• Unorganised sector plays an important role in the market dynamics of the sanitary ware business in the country with around 35% market share. These unorganized players have lower fixed overheads enabling them to keep the pricing competitive and garner market share. Stiff competition from players in the unorganised segment can exert pressure on margins. We believe that HSIL has over the years built a brand which will help it to compete with organised as well as unorganised players.

• During FY12, imported raw material stood at ~11% of the net revenues and ~33% (37% in FY11) of the total raw material consumption for the company. Thus sharp depreciation of rupee impacts the margins of the company adversely. We believe that the reducing trend in imports as a percentage of sales (due to enhanced in‐house manufacturing capabilities) will lower the volatility of profits on this account.

• The container glass business of the company is a B2B business and is heavily dependent on the demand of the user segments like beer, beverages, pharma, etc. Any deviation in the demand for these products may lead to adverse revenue trends for HSIL. Also the capacities in this segment have also increased significantly over the last 3 years and this has reduced the bargaining power for the glass container manufacturers.

• The replacement of PET bottles and aluminium cans for packaging in F&B and beer industries is picking up pace may pose a threat to the overall demand for the container glass. However, the acquisition of Garden Polymer is expected to mitigate the risk to some extent.

– 35 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / HSIL LTD.

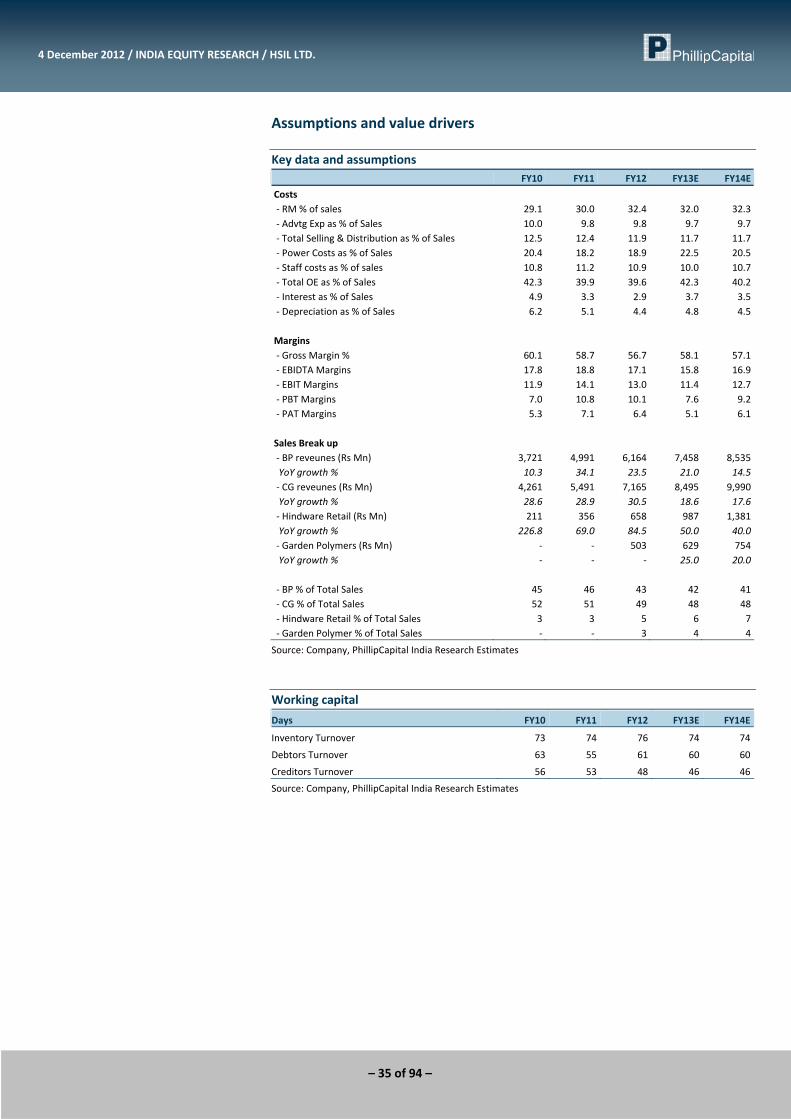

Assumptions and value drivers Key data and assumptions FY10 FY11 FY12 FY13E FY14E

Costs ‐ RM % of sales 29.1 30.0 32.4 32.0 32.3 ‐ Advtg Exp as % of Sales 10.0 9.8 9.8 9.7 9.7 ‐ Total Selling & Distribution as % of Sales 12.5 12.4 11.9 11.7 11.7 ‐ Power Costs as % of Sales 20.4 18.2 18.9 22.5 20.5 ‐ Staff costs as % of sales 10.8 11.2 10.9 10.0 10.7 ‐ Total OE as % of Sales 42.3 39.9 39.6 42.3 40.2 ‐ Interest as % of Sales 4.9 3.3 2.9 3.7 3.5 ‐ Depreciation as % of Sales 6.2 5.1 4.4 4.8 4.5 Margins ‐ Gross Margin % 60.1 58.7 56.7 58.1 57.1 ‐ EBIDTA Margins 17.8 18.8 17.1 15.8 16.9 ‐ EBIT Margins 11.9 14.1 13.0 11.4 12.7 ‐ PBT Margins 7.0 10.8 10.1 7.6 9.2 ‐ PAT Margins 5.3 7.1 6.4 5.1 6.1 Sales Break up ‐ BP reveunes (Rs Mn) 3,721 4,991 6,164 7,458 8,535 YoY growth % 10.3 34.1 23.5 21.0 14.5 ‐ CG reveunes (Rs Mn) 4,261 5,491 7,165 8,495 9,990 YoY growth % 28.6 28.9 30.5 18.6 17.6 ‐ Hindware Retail (Rs Mn) 211 356 658 987 1,381 YoY growth % 226.8 69.0 84.5 50.0 40.0 ‐ Garden Polymers (Rs Mn) ‐ ‐ 503 629 754 YoY growth % ‐ ‐ ‐ 25.0 20.0 ‐ BP % of Total Sales 45 46 43 42 41 ‐ CG % of Total Sales 52 51 49 48 48 ‐ Hindware Retail % of Total Sales 3 3 5 6 7 ‐ Garden Polymer % of Total Sales ‐ ‐ 3 4 4

Source: Company, PhillipCapital India Research Estimates

Working capital

Days FY10 FY11 FY12 FY13E FY14E

Inventory Turnover 73 74 76 74 74

Debtors Turnover 63 55 61 60 60

Creditors Turnover 56 53 48 46 46

Source: Company, PhillipCapital India Research Estimates

– 36 of 94 –

4 December 2012 / INDIA EQUITY RESEARCH / HSIL LTD.

Company Overview • HSIL is the market leader in the building products market, and a dominant player in

the container glass segment in the country. The Building Products commands ~40% of the organized market in the sanitaryware industry, while the Container Glass is the second largest player in India.

• The product range of the company has a wide spectrum from Sanitaryware to Wellness, to Faucets and Kitchen Appliances, thus meeting all the needs of bathroom and kitchen products.

• HSIL sells its products through an extensive distribution channel made up of more than 2000 distributors and ~15,000 retailers in addition to its own outlets and dealer shops in malls.

• The institutional client list includes some of large business houses of the country – DLF, The Taj Hotels, GMR, Unitech, ITC Hotels, Mahindra, Infosys, Coca Cola, Pepsi, Dr. Reddy’s Laboratories, Hindustan Unilever, Pernod Ricard, Pfizer, Sab Miller, Dabur, Nestle, to name a few.

• HSIL is the second largest player in the domestic container glass industry with ~18% market share in terms of revenues and 20% market share in terms of capacity. The company has a strategic presence in southern India with its capacity representing ~60% of total capacity as the region represents the highest net capita consumption.

• HSIL is recognized among the top 300 companies in India, while rated amongst the best 100 small and medium sized companies in the world by the Forbes Magazine.

• In 2008, the company forayed into the retail of Home Interiors to extend its reach to the end‐customer through its wholly owned subsidiary Hindware Home Retail Private Limited (HHRPL). It has introduced EVOK brand which specializes in providing a comfortable and convenient one‐stop shopping experience. Currently the EVOK has 18 stores across all metro and category‐A cities and it plans to consolidate its presence across all states.

• “Hindware" brand has been recognized as a Super brand for the last four consecutive years.

• The sales for the company have increased at 33.4% CAGR during FY09‐12 period. The net revenues rose from Rs 6158mn in FY09 to Rs 14628mn in FY12. EBIDTA during the said period has also increased at a CAGR of 37.2% from Rs 967mn in FY09 to Rs 2498mn in FY12. PAT for the period from FY09‐12 has registered a CAGR of 29.3% as it increased from Rs 433mn in FY09 to Rs 937mn in FY12.

Manufacturing Facilities • HSIL has vertically integrated manufacturing facilities, where vital raw materials and

consumables are produced and upgraded in captive units, thereby ensuring superior quality and on time availability.

The Sanitary ware manufacturing facilities – a snapshot Unit Installed Capacity (mn pieces annually) Products

Bahadurgarh, Haryana 1.5 SanitarywareSomanypuram, Bibingar, Andhra Pradesh 2.0 SanitarywareBhiwadi, Rajasthan 0.5 Faucet

Source: Company, PhillipCapital India Research

The Container Glass manufacturing facilities – a snapshot Unit TPD