home cover prestige

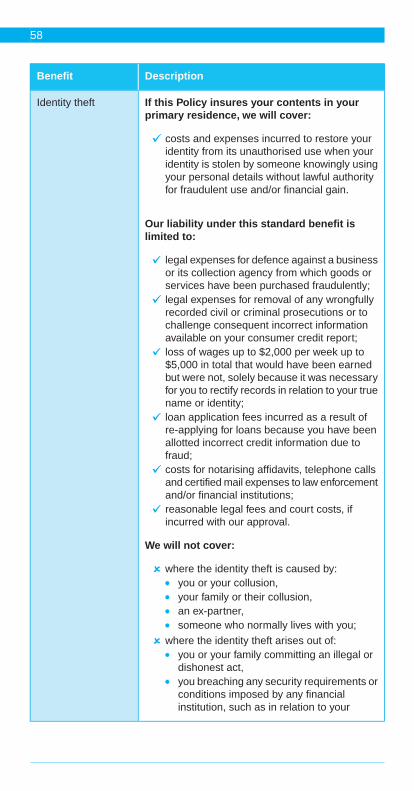

TRANSCRIPT

QBE Insurance (Australia) Limited

Home cover prestigeInsurance Product Disclosure Statement and Policy Wording

CONTENTS

3Introduction & welcome

3About this booklet

3Updating our PDS

4About QBE

5IMPORTANT INFORMATION

5Choose your type of cover

6Duty of Disclosure

7Changes to the information you have given us

8If you move and do not tell us

8Keep receipts

8Privacy Promise

10Your premium

1121 day cooling off period

11Dispute resolution

12The General Insurance Code of Practice

12Financial Claims Scheme

13POLICY WORDING

13Insurer

13Our agreement with you

13Your Policy

13Paying your premium

14Preventing our rights of recovery

14Other party's interests

14Changing your Policy

15Policy comes to an end on total loss

15Definitions (The meaning of some words)

20Insuring your building and/or contents

27Where your contents are covered

28How much you are covered for

30Your sum insured

31When your home is unoccupied

32Your proof of ownership

33What you are covered for

41Your standard benefits

61Optional benefits

Date of preparation: 7th December 2013Date effective: 7th December 2013QM4969-1213

1

64Legal liability

68When you are not insured

68Sanction clause

69How to make a claim

71How we settle your claim

75Repairer information

76How GST affects any payments we make

77Your excess

79After we have paid a claim

80How your Policy may be cancelled

2

Introduction & welcomeWe understand how important it is to be comfortable with your cover so weare glad you chose QBE to take care of your insurance. As the largestAustralian owned general insurer and reinsurer, we have been taking careof the insurance needs of Australians since 1886. Safe, strong and secure,you can be confident you’ve made a great choice.

Inside, you will find the information you need to know about your Policy. Weexplain what your Policy covers, information about discounts and excessesand importantly, how to make a claim. Remember, whether you call us for aquote, or to report a claim, or to change your details, you can rely on ourfriendly team to help you.

Please take the time to read through this booklet and if you have any questionsor need more information, call us on 1300 734 729 or the phone number atthe top of your Policy Schedule.

Thank you for making QBE your first choice.

About this bookletThis booklet is a Product Disclosure Statement (PDS) and is also the PolicyWording. Other documents may comprise the PDS and we will tell you if thisis the case in the relevant document.

This booklet has two (2) parts: Important Information to help you understandthe insurance, and the Policy Wording, which sets out terms and conditionof the cover provided. It is up to you to choose the cover you need. Any advicein this booklet is general in nature only and has not considered your objectives,financial situation or needs.You should carefully consider the informationprovided having regard to your personal circumstances to decide if it is rightfor you.

Updating our PDSWe may update the information contained in this PDS when necessary. Apaper copy of any updated information is available to you at no cost by callingus. We will issue you with a new PDS or a supplementary PDS, where theupdate is to rectify a misleading or deceptive statement or omission, whichis materially adverse from the point of view of a reasonable person decidingwhether to obtain or renew this insurance.

3

About QBEQBE Insurance (Australia) Limited is a member of the QBE Insurance Group(ASX: QBE). QBE Insurance Group is Australia’s largest international generalinsurance and reinsurance group, and one of the top 25 insurers andreinsurers worldwide. The company has been operating in Australia since1886 and continues to provide insurance solutions that are focused on theneeds of policyholders.

QBE is a respected name in Australian insurance, backed by sizeable assets,and well known as a strong and financially secure organisation.

4

IMPORTANT INFORMATIONThe information provided in this section includes high level information aboutthe options in cover you can choose from, as well as factors that affect thecost, our dispute resolution process, your duty of disclosure, cooling off rights,how to make a claim and other relevant information.

The Policy Wording section sets out the detailed terms, conditions andexclusions relating to the insurance.

If we issue you with a Policy, you will be given a Policy Schedule. The PolicySchedule sets out the specific terms applicable to your cover and should beread together with the Policy Wording.

The Policy Wording and Policy Schedule form your legal contract with us soplease keep them is a safe place for future reference.You should check thePolicy or Renewal Schedule when you receive it to ensure it accurately stateswhat you have insured.

If you require further assistance or information about this product, pleasecontact the company you are buying this Policy through, contact QBE on1300 734 728.

Choose your type of coverYour QBE Policy insures you for loss or damage caused by certain insuredevents, including accidental damage.

You can choose to insure your:

Building - the dwelling used entirely or primarily as a place of residence;Contents - items you own or have legal responsibility for in your placeof residence; andValuables - portable valuable items, including jewellery and electronicequipment temporarily removed from your place of residence (onlyavailable for specific items and limits) and cover is only available whereyou have insured your contents.

5

Duty of Disclosure

New business

What you must tell us

When answering our questions, you must be honest and you have a dutyunder the law to tell us anything known to you, and which a reasonable personin the circumstances would include in answer to the questions. We will usethe answers in deciding whether to insure you and anyone else to be insuredunder this insurance and on what terms.

Who needs to tell us

It is important that you understand you are answering our questions in thisway for yourself and anyone else who is an insured under this insurance.

If you do not tell us

If you do not answer our questions in this way, we may reduce or refuse topay a claim, or cancel your insurance. If you answer our questionsfraudulently, we may refuse to pay a claim and treat the insurance as neverhaving worked.

Renewals, variations, extensions and reinstatements

Once your insurance is entered into and is no longer new business then yourduty to us changes.You are required before you renew, vary, extend orreinstate your insurance, to tell us everything you know and that a reasonableperson in the circumstances could be expected to know, is a matter that isrelevant to our decision whether to insure you, and anyone else to be insuredunder this insurance, and if so, on what terms.

You do not have to tell us about any matter:

that diminishes the risk to be undertaken by us;that is of common knowledge;that we know or should know or, in the ordinary course of our business,we ought to know;as to which compliance with your duty is waived by us.

Non-disclosure

If you fail to comply with your duty of disclosure, we may be entitled to reduceour liability under the insurance in respect of a claim or may cancel theinsurance.

If your non-disclosure is fraudulent, we may also have the option of avoidingthe insurance from its beginning.

6

You must disclose to us all previous claims

You are asked at the time you take out this insurance to give us full andcorrect details concerning any:

renewal or insurance policy declined, cancelled or refused, or where anyexcess was imposed;claim refused by an insurer;claim made;criminal conviction or finding of guilt for an offence,

in relation to you and your family because any of these may affect the premiumand extent of insurance.

For example, we may be entitled to:

charge you an additional premium;impose (back-dated) restrictions including declining your insurance backto when this information should have been provided;decline to insure your building, contents or valuables;refuse a claim.

When renewing your Policy with us you must also advise us of any changesto your:

claims;insurance; orcriminal history.

We will notify you in writing of the effect a change may have on your renewal.

Changes to the information you have givenusIt is important to advise us of any changes to information you have given us,otherwise your insurance may be affected. Changes would include:

should you move address;changes in the occupancy of your home;additions or renovations to your building (you will need to revise yourbuilding sum insured to ensure you are adequately insured);purchasing new items which increase the value of your contents (youwill need to revise your contents sum insured to ensure you areadequately insured);purchasing a high risk item worth more than the stated limit as set outin 'How much you are covered for - High risk items with limits’.

We may require you to pay an additional premium as a result of thesechanges.You must pay the additional premium before these charges comeinto effect.

7

If you move and do not tell usYou must notify us when you change your place of residence.

This insurance and premium payable is based on the address you haveprovided, which is shown on the Policy Schedule.You may have to pay anadditional premium as a result of changing your address. If you changeaddress and you do not inform us you will have no insurance at the newaddress except under 'Your standard benefits - Cover when you move sites’,if this Policy insures your contents.

Keep receiptsYou should keep receipts, invoices or other evidence of ownership and valueof all property that you insure because if you make a claim you will be askedto prove ownership and value in order for us to pay the claim.

Privacy PromiseAll companies in the QBE Group are committed to safeguarding your privacyand the confidentiality of your personal information. QBE collects only thatpersonal information from or about you for the purpose of assessing yourapplication for insurance and administering your insurance policy, includingany claim made by you. QBE will only use and disclose your personalinformation for a purpose you would reasonably expect. We will request yourconsent for any other purpose.

Without this personal information we may not be able to issue insurancecover, administer your insurance or process your claim. Our aim is to alwayshave accurate and up-to-date information. When you receive a PolicySchedule, Certificate of Insurance, Renewal or other document from us, youshould contact us if the information is not correct.

QBE uses the services of a related company located in the Philippines toprovide Call Centre sales and claims handling, accounting and administrationservices to QBE in Australia.

QBE or our authorised agent may collect or disclose your personal informationfrom or to:

any person authorised by you;a mail house, records management company or technology servicesprovider (for printing and/or delivery of mail and email, including securestorage and management of our records). These companies may belocated or the records stored using 'Cloud' technology overseas, includingin India, Ireland, USA or the Netherlands;a financier whose name appears on your Policy Schedule (for the purposeof confirming the currency of your Policy or when you have a claim andthe insured property is a total loss, to confirm if the financier has a currentinterest);

8

an organisation that provides you with banking facilities (for the purposeof arranging direct debit or other payment transactions or confirmingpayments made by you to us);a financial services provider or our agent who is arranging your insurance(for the purpose of confirming your personal and insurance details);another person named as a co-insured on your Policy (for the purposeof confirming if full disclosure has been made to us);another insurer (to obtain confirmation of your no claim bonus or to assessinsurance risks or to assist with an investigation);our reinsurer that may be located overseas (for the purpose of seekingrecovery from them);a dispute resolution organisation such as the Financial OmbudsmanService (for the purpose of resolving disputes between QBE and you orbetween QBE and a third party);a company to conduct surveys on our behalf for the purpose of improvedcustomer services; andan insurance reference bureau (to record any claims you may make uponus).

In addition to the above, in the event of a claim, QBE or our authorised agentmay disclose your personal information:

to a repairer or supplier (for the purpose of repairing or replacing yourinsured items);to an investigator, assessor (for the purpose of investigating or assessingyour claim);to a lawyer or recovery agent (for the purpose of defending an action bya third party against you or recovering our costs including your excessor seeking a legal opinion regarding the acceptance of a claim);to a witness to a claim (for the purpose of obtaining a witness statement);to another party to a claim (for the purpose of obtaining a statement fromthem or seeking recovery from them or to defend an action by a thirdparty).

Personal information (about you) may also be obtained from the above peopleor organisations.

In addition we will:

give you the opportunity to find out what personal information we holdabout you and when necessary, correct any errors in this information.Generally we will do this without restriction or charge; andprovide our dispute resolution procedures to you, should you wish tocomplain about how we handle your personal information.

To obtain further information about our Privacy Policy or to request accessto or correct your personal information, please email:[email protected] make a complaint email: [email protected].

9

Your premiumPremium means any amount we require you to pay under the Policy andincludes government charges.

You pay the premium – We insure you

Provided we receive the premium, we will insure you as set out in this Policyand the Policy Schedule in respect of an incident occurring during the periodof insurance. When you apply for this insurance, you will be advised of thepremium. If you choose to effect cover, the amount will be set out in the PolicySchedule.

How your premium is calculated

We take various factors into consideration when calculating your premiumincluding:

the sum(s) insured;the address of your building and/or contents covered;any no claim bonus discount to which you may be entitled to on yourbuilding and/or your contents;your insurance history;the security features of your home;the construction and age of your home;the level of excess you choose to pay;the cost of any optional benefits you have selected.

The premium also includes compulsory government charges including StampDuty, GST and any Emergency Services Levy (where applicable).

Ways to reduce your premium

You may be eligible for the following discounts we offer:

No claim bonus discountNo claim bonus is a premium discount awarded for not making a claim.A no claim bonus discount increases each year that you remain claimfree until you reach our maximum discount. Based on the claims lodgedduring the period of insurance, your Policy’s no claim bonus will beadjusted when you renew your Policy and this can either:

increase (up to our maximum no claim bonus);decrease; orremain the same.

Multi policy discountIf this Policy insures both your building and/or your contents and/or yourvaluables at the same site, we may provide you with a multi policydiscount.You may also be entitled to the same discounts on otherinsurance products. For more information, contact your financialinstitution.Over 50’sIf any of the named Policy holders of this Policy are over 50 and no longerworking full time, we will give you an over 50’s discount.You will need

10

to contact us and advise us once you become eligible for this discount.We will then apply the discount to any future premiums.Retirees discountIf any of the named Policy holders of this Policy are retired and no longerworking full time, we will give you a retirees discount.You will need tocontact us and advise us once you become eligible for this discount. Wewill then apply the discount to any future premiums.

Other ways you can help reduce your premium:

Increase your securityWe provide discounts when you have installed advanced operationalsecurity measures such as deadlocks on all external doors and keyedwindow locks, local and monitored alarms or a fixed home safe.Choose a higher excessYou can choose a higher excess for a reduced premium.Your PolicySchedule will indicate the excess applicable in the event of a claim.Please refer to 'Your excess' for more information on excess options.

21 day cooling off periodIf you want to return your insurance after your decision to buy it, you maycancel it and receive a full refund. To do this we must receive your requesteither in writing or via email: [email protected] within twenty one (21) daysof its commencement.

This cooling off right does not apply if you have made or are entitled to makea claim. Even after the cooling off period ends, you still have cancellationrights. However, we may deduct certain amounts from any refund (see 'Howyour Policy may be cancelled – Refund of premium').

Dispute resolutionWe will do everything possible to provide a quality service to you. However,we recognise that occasionally there may be some aspect of our service ora decision we have made that you wish to query or draw to our attention. Wehave a complaints and dispute resolution procedure which undertakes toprovide an answer to your complaint within fifteen (15) working days.

If you would like to make a complaint or access our internal dispute resolutionservice please contact your nearest QBE office and ask to speak to a disputeresolution specialist. If you are not happy with our answer, or we have takenmore than fifteen (15) working days to respond, you may take your complaintto the Financial Ombudsman Service (FOS), an ASIC approved externaldispute resolution body.

FOS resolves certain insurance disputes between consumers and insurersand will provide an independent review at no cost to you. QBE is bound bythe determination of FOS but the determination is not binding on you.

11

The General Insurance Code of PracticeQBE Insurance (Australia) Limited is a signatory to the General InsuranceCode of Practice. The Code aims to:

promote more informed relations between insurers and their customersimprove consumer confidence in the general insurance industryprovide better mechanisms for the resolution of complaints and disputesbetween insurers and their customers, andcommit insurers and the professionals they rely upon to higher standardsof customer service.

Financial Claims SchemeThis Policy is a protected policy under the Financial Claims Scheme (FCS),which protects certain insureds and claimants in the event of an insurerbecoming insolvent. In the unlikely event of QBE becoming insolvent youmay be entitled to access the FCS, provided you meet the eligibility criteria.

More information may be obtained from APRA - www.apra.gov.au or1300 55 88 49.

12

POLICY WORDING

InsurerThis Policy is underwritten by QBE Insurance (Australia) LimitedABN 78 003 191 035, AFS Licence No. 239545 of 82 Pitt Street, SydneyNSW 2000.

Our agreement with youThis Policy is a legal contract between you and us.You pay us the premiumand we provide you with the cover you have chosen as set out in the Policy,occurring during the period of insurance shown on your Policy Schedule orany renewal period.

The limits of cover applying to the cover selected by you and the amount ofany excess that applies to your Policy, is shown on your Policy Schedule.

Your PolicyYour Policy consists of the Policy Wording in this booklet and the PolicySchedule we give you. Please keep them in a safe place for future reference.

Please check the Policy Schedule details to ensure it accurately states whatyou have insured. Be sure to check that the sum insured for the various areasof cover are adequate.

If you need any further information about any part of your Policy, please askus or your financial services provider.

Paying your premiumAnnual premium

Paying your premium on time is important because it affects your insurance.If you are paying your premium annually in one payment, and you have notpaid by the due date or your payment is dishonoured, this Policy will notoperate and there will be no cover.

Instalment payments

If you are paying your premium by instalments, we will specify on your PolicySchedule when we will deduct the first instalment. Thereafter, instalmentpayments will be debited on the date or frequency you have nominated. Ifyou are paying your premium in instalments by direct debit from your creditcard or financial institution account, you must tell us if these details changeno later than seven (7) days before your next instalment is due. We will notpay a claim under this Policy if, at the time the claim occurred, any premiuminstalment has remained unpaid for one (1) month or more.

13

If any instalment of premium has remained unpaid for one (1) month, we maycancel this Policy. However, we will send you a notice confirming the actionwe intend to take and when any cancellation will become effective.

At renewal

If you have been paying your premium by instalment, we will continue todeduct instalments for your Renewal Policy on the same day of the monthat the new premium level unless you tell us otherwise.

If any instalment of premium has remained unpaid for one (1) month, we willcancel this Policy. We will send you a reminder setting out our intention totake two (2) instalments on the next payment date. If payment is not receivedafter this reminder, we will send you a notice telling you of the date the Policywill cease unless payment is received.We send a notice to confirm the Policyhas been cancelled.

Adjustment of premium on renewal

If a claim occurs in the previous period of insurance and you do not notify usuntil after the premium for the current period of insurance was calculated,then you must pay any additional premium that would have been calculatedhad you told us about the claim on the day that the claim occurred. Thiscondition does not affect any other rights that we have, including the rightsthat we have under 'Your duty of disclosure'.

If your payment details change

If the direct debit arrangements you use to pay by instalment changes, suchas you are issued a new credit card or change your bank arrangements, youmust tell us. You should do this at least seven (7) days in advance of yournext payment date.

Preventing our rights of recoveryIf you have agreed not to seek compensation from another person who isliable to compensate you for any loss, damage or liability which is coveredby this Policy, we will not cover you under this Policy for that loss, damageor liability.

Other party's interestsYou must tell us of the interest of all parties (e.g. financiers) who will becovered by this insurance. We will protect their interests only if you have toldus about them and we have noted them on your Policy Schedule.

Changing your PolicyIf you want to make a change to this Policy, the change becomes effectivewhen:

we agree to it; andwe give you a new Policy Schedule detailing the change.

14

Policy comes to an end on total lossIf you have a claim that results in QBE declaring you have a total loss, thePolicy terms have been met by QBE and the Policy comes to an end.

If you paid an annual premium no refund is due to you.

If you were paying by instalments, we will deduct the premium outstandingfor the period of insurance from our settlement payment to you.

Where you have both your building and contents insured under the Policy,and only either the building or contents are a total loss, the part of the Policythat is not a total loss remains in place.

Definitions (The meaning of some words)Some words and expressions in this Policy have a specific meaning whichis given below.

DefinitionWord or term

a written notice issued by us about any alteration tothe insurance made by you under this Policy.

Alteration Notice

For example, if you change your address.

building and outbuildings and fixtures as describedunder the heading 'What we will cover as your building'on page 24.

Building

an object of real or intrinsic value collected as aninvestment, hobby or general interest purpose and theitem is not used as a household good or personaleffect.

Collection

an accident directly caused by the sudden impact ofa moving body or object.

Collision

a desktop or portable personal computer includingperipherals such as printers, modems, data projectorsand speakers and standard purchased computersoftware but no data of any kind or custom writtensoftware.

Computerequipment

items described under the heading 'What we will coveras your contents' on page 25 which you or your familyown or have legal responsibility for located in yourbuilding or at the site.

Contents

a small article valued as a collectors’ item.Curio

15

DefinitionWord or term

when an item insured by this Policy is physicallyharmed but does not include wear and tear.

Damage ordamaged

the reduction in the value of the item or property dueto wear and tear.

Depreciation

heave, landslide, land-slippage, mudslide, settling,shrinkage or subsidence.

Earth movement

a written alteration to the terms, conditions andlimitations of this Policy which is shown in the PolicySchedule.

Endorsement

one or more sound or visual entertainment systemsin your home including each individual item such as atelevision, radio, video player or projector, CD player,entertainment disc playing devices, amplifier orspeakers and all accessories.

Entertainmentequipment

being worn or washed away by water, ice or wind.Erosion

the amount you must pay towards a claim.You willfind the amount of any excess shown on the PolicySchedule. See page 77 ‘Your excess’ for moreinformation.

Excess

any of the following people who normally live with you:Familyspouse or partner;children, step children;parents, grandparents;grandchildren;brothers, sisters;domestic staff;a person who normally resides with you, but doesnot include a person with whom you may share ahouse for any financial consideration.

a fire producing flames, but not charring, melting orscorching without flames.

Fire

an item that is permanently attached to or fixed to yourbuilding or the site, but does not include carpets,internal blinds, curtains, swimming pool or spa coversor pool or spa accessories.

Fixtures

Please see page 24 under ‘What we will cover as yourbuilding’ for a list of examples of fixtures.

16

DefinitionWord or term

the covering of normally dry land by water that hasescaped or been released from the normal confinesof any of the following:

Flood

(a) a lake (whether or not it has been altered ormodified);

(b) a river (whether or not it has been altered ormodified);

(c) a creek (whether or not it has been altered ormodified);

(d) another natural watercourse (whether or not ithas been altered or modified);

(e) a reservoir;(f) a canal;(g) a dam.

the process of fusing or melting together the windingsof an electric motor following damage to the insulatingmaterial as a result of overheating caused by anelectric current.

Fusion

those items listed under the heading ‘High risk itemswith limits’ on page 28.

High risk item

an event neither expected nor intended from thestandpoint of you or your family which results in a claimon this Policy.

Incident

those events listed under the heading ‘What you arecovered for’ which start on page 33.

Insured event

the replacement cost of a similar item to the one stolenor damaged taking into account the age of the item.

Market value

Non lockable structures and non lockable parts ofstructures.

Open air

a vessel designed to be operated by a personstanding, sitting astride or kneeling upon it. It useswater jet propulsion and has an engine in a watertightcompartment.

Personalwatercraft

Photographicequipment

camera body; andall lenses which attach to the camera body; andall camera accessories including but not limitedto carry case, filters, cleaning equipment, tripod,battery and memory cards;

however not photographic data.

17

DefinitionWord or term

one of the following:Policy Schedulethe Policy Schedule;the renewal notice you have paid;the alteration notice sent to you.

evidence of ownership and value of an item. Theevidence can be a combination of:

Proof ofownership

receipts, valuations, instruction manuals;guarantee certificates, catalogues;make, model and serial number;photographs or video film of item.

your building is structurally sound, secure and in agood state of repair and its roof guttering regularlycleaned.

Properlymaintained

water that has fallen from the sky onto your buildingand site. This also includes where there are heavy,intense bursts of rainfall, usually during thunderstorms

Rain

where so much water falls in a very short time that itcannot get away quickly enough and collects and flowsinto your building, but does not include flood.

locked so as to prevent entry other than by usingviolent force.

Secured

the land at the address shown on the Policy Scheduleon which the building is built, including the yard orgarden used only for domestic purposes.

Site

your items that are listed in the ‘Schedule of SpecifiedContents’ section of your Policy Schedule.

Specifiedcontents

your items that are listed in the ‘Schedule of SpecifiedValuables’ section of your Policy Schedule.

Specifiedvaluables

equipment, clothing, helmets, footwear, protective gearused when participating in recreational or competitivesport, but does not include a bicycle, firearm, a powerdriven vehicle or a power driven item of any kind.

Sportingequipment

violent weather and high winds, sometimesaccompanied by rain, hail or snow including a cycloneor tornado.

Storm

the amount you have insured either your building, yourcontents (including specified contents) or yourvaluables as shown on the Policy Schedule. We will

Sum insured

18

DefinitionWord or term

pay no more than these amounts plus certain standardbenefits (see page 41) or optional benefits (see page61).

any act of any person acting on their own or inconnection with an organisation or foreign government,which can involve the use of or threat of force or

Terrorism

violence, where the purpose, by its nature or context,is to put the public or a section of the public in fear, toresist or influence a government or, to further anideological, religious, ethnic or similar aim.

those items you use to carry on a business or earn anincome, but does not include those items you woulduse in a home office.

Tools of trade

a high tide or tidal wave caused by an earthquake,earth tremor or seismological disturbance under thesea.

Tsunami

the building at the site does not have enough furnitureor furnishings for normal living needs.

Unfurnished

that either:Unoccupiedno-one is living in the building; orsomeone is living in the building at the site withoutyour consent.

QBE Insurance (Australia) Limited, ABN 78 003 191035.

We, our and us

damage or a reduction in value through age, ordinaryuse or lack of maintenance.

Wear and tear

a piece of fine art such as a painting or picture, Persiancarpet, rug or wall hanging, tapestry, vase, ornament,sculpture or other creation.

Works of art

the person(s) named in the Policy Schedule as theinsured including a family member.

You and your

19

Insuring your building and/or contents

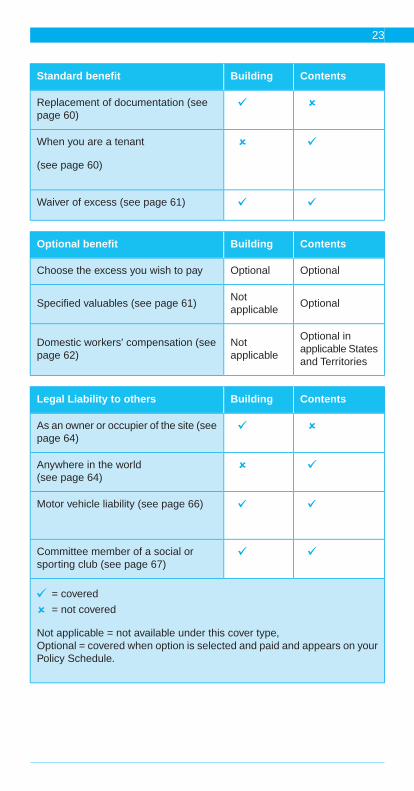

Policy coverage summary

You can choose to insure your building, your contents or both under the QBEHome Cover Prestige Policy. If this Policy insures your contents, you willreceive automatic cover away from the home however, some items havelimits. If you would like to extend these limits, for an additional premium youcan choose to specify these items under the Specified valuables optionalbenefit.

Your building and/or contents will be covered for loss or damage caused byone (1) of the fourteen (14) insured events. In addition, there are also standardbenefits you may be entitled to at no extra cost.

You can extend your cover by paying extra premium for options we offer.

A summary of cover available under this QBE Home Cover Prestige Policyis listed in the table below.

ContentsBuildingInsured event

Accidental loss or damage (see page33)

Fire (see page 33)

Explosion or implosion (see page 34)

Lightning or thunderbolt(see page 34)

Earthquake or tsunami(see page 35)

Theft (see page 35)

Vandalism and malicious damage (seepage 35)

Water or other liquid(see page 36)

Collision (see page 37)

Falling tree, branch or aerial (see page38)

Damage by animals(see page 38)

20

ContentsBuildingInsured event

Riot (see page 38)

Storm, rain or flood(see page 38)

Glass breakage(see page 40)

Power surge (see page 40)

ContentsBuildingStandard benefit

Building sum insured safeguard (seepage 41)

Environmental upgrades to yourbuilding ( see page 42)

Environmental upgrades to yourcontents (see page 43)

Accommodation costs(see page 43)

Contracting purchaser (see page 44)

Inflation adjustment(see page 45)

Mortgage discharge(see page 45)

Extra costs of reinstatement (see page45)

Fusion of electric motors(see page 47)

Forced evacuation by governmentauthority(see page 48)

External door locks (see page 49)

Essential temporary repairs(see page 50)

21

ContentsBuildingStandard benefit

Modifications to the building due toparaplegia or quadriplegia(see page 50)

Building materials awaiting installation(see page 51)

Building costs (see page 52)

Cover when you move sites(see page 52)

Contents being conveyed to your newresidence (see page 53)

Food spoilage (see page 53)

Accessories, appliances or spare parts(see page 54)

Guest’s property(see page 54)

Your contents temporarily removedfrom your home (see page 55)

Loss or theft of credit or transactioncard (see page 56)

Veterinary expenses (see page 57)

Strata title home owners(see page 60)

Legal defence costs (see page 45)

Taxation audit (see page 46)

Trees, shrubs and plants (see page 49)

Compensation for death (see page 51)

Identity theft (see page 58)

Monitored alarm attendance after theft(see page 59)

22

ContentsBuildingStandard benefit

Replacement of documentation (seepage 60)

When you are a tenant

(see page 60)

Waiver of excess (see page 61)

ContentsBuildingOptional benefit

OptionalOptionalChoose the excess you wish to pay

OptionalNotapplicable

Specified valuables (see page 61)

Optional inapplicable Statesand Territories

Notapplicable

Domestic workers' compensation (seepage 62)

ContentsBuildingLegal Liability to others

As an owner or occupier of the site (seepage 64)

Anywhere in the world(see page 64)

Motor vehicle liability (see page 66)

Committee member of a social orsporting club (see page 67)

= covered

= not covered

Not applicable = not available under this cover type,Optional = covered when option is selected and paid and appears on yourPolicy Schedule.

23

Who we will cover

We cover:

you, and

your family.

What we will cover as your building

Your building does not meanYour building means

a caravan, trailer or theiraccessories;

the main residential building;

outbuildings; anda shipping container;

fixtures such as:a building of flats;a fixed spa, sauna, barbecue,

clothes line, room heater, strata title, company orcommunity title units withstove, air conditioner, ceiling

fan, lighting fixtures respect to insuring thepermanently secured to thebuilding, hot water system;

building, however we willinsure contents contained inthese units under a contentspolicy;

kitchen cupboards, built infurniture;

trees, shrubs, plants, hedges,lawns (real or artificial), earth;

meter box;exterior blinds and awnings;

paths or driveways made ofearth or gravel;

carport, pergola, garden shed,gazebo;

landscaping of any kind;path, driveway, terrace, well,bore; a pool cover;in-ground swimming pool,water tank;

a swimming pool that is ableto be moved from the site;

garage doors; a sea wall or pontoon;reticulation system;

a building or structure usedsolely for business;

television aerial, radio mast oraerial and fittings;

a building or structure that isin the course of construction,

fixed floor coverings andfloating floor coverings exceptcarpets;

alteration or substantialrepair;

solar panels (but not plasticsolar heating systems forpools or spas);

fixtures such as:carpets and rugs,internal blinds,private jetties including fixed

floating jetties; and curtains,swimming pool or spacovers,

water in a tank;at the site.

pool or spa accessories;

jetties used for businesspurposes;

24

Your building does not meanYour building means

water in a swimming pool;

water in pipes.

= covered

= not covered

What we will cover as your contents

We insure items which you or a family member own or have legal responsibilityfor located in your building or at the site.

Your contents does not meanYour contents means

specified valuables insuredunder the valuables section ofthis Policy;

furniture, furnishings, carpets(whether fixed or unfixed), floorrugs, internal blinds, curtains;household goods; fish, birds or other animals;

lawns, hedges, trees, shrubs,plants (real or artificial);

light fixtures not permanentlysecured to the building andwhich are relocatable; earth;white goods; a power driven vehicle other

than:clothing and other personaleffects; a wheel chair,high risk items as listed withlimits on page 28;

an unregistered batterypowered single personvehicle,swimming pool or spa that is

not in-ground; an unregistered gardenappliance,swimming pool or spa covers

and accessories; an unregistered golf buggy,items used in connection withyour business or occupation

a battery powered children’stoy,

used in an office or surgery in an unregistered motorcycleup to 125cc engine capacity;your home, but not if a high risk

item listed on page 28. a personal watercraft;

a powercraft, watercraftexceeding four (4) metres inlength, including accessoriesand spare parts whether fittedto the powercraft or watercraftor not other than a:

surf ski,surfboard,

25

Your contents does not meanYour contents means

one to four person canoe,a powercraft with an engineof no more than ten (10)horsepower;

an aircraft or aerial device,other than a:

kite,model aircraft or modelglider;

a caravan or trailer, includingaccessories and spare partswhether fitted to the caravan ortrailer or not;a hovercraft;

water.

= covered

= not covered

Specified contents

We consider certain items to be of high risk and have limits onwhat we will pay.The types of items and limits we pay are listedon page 28 under the heading ‘High risk items with limits’.

You can increase your cover beyond these limits by specificallylisting high risk items as specified contents.

When you specify these items, they will be listed in the‘Schedule of Specified Contents’ section of your Policy Scheduleand you will be covered for loss or damage up to the limit youhave specified. Specified contents are only insured whilst atthe site.

Specified valuables

items that are listed in the ‘Schedule of SpecifiedValuables’ section of your Policy Schedule if you haveselected and paid for this optional benefit.

26

Wh

ere

you

r co

nte

nts

are

cov

ered

If th

is P

olic

y in

sure

s yo

ur c

onte

nts,

they

will

be

cove

red

whi

lst i

n yo

ur b

uild

ing

for

acci

dent

al lo

ss o

r da

mag

e an

d in

sure

d ev

ents

up

to th

e su

min

sure

d or

hig

h ris

k ite

ms

limits

.You

r co

nten

ts a

re a

lso

insu

red

anyw

here

in A

ustr

alia

or

New

Zea

land

and

any

whe

re in

the

wor

ld fo

r up

to 9

0 da

ys.

The

re a

re li

mits

on

the

max

imum

am

ount

we

will

pay

for

cert

ain

item

s. P

leas

e se

e un

der

the

head

ing

'You

r co

nten

ts te

mpo

raril

y re

mov

ed fr

omyo

ur h

ome'

for

mor

e in

form

atio

n.

Co

nte

nts

insu

ran

ceL

oca

tio

n o

f co

nte

nts

Sp

ecif

ied

val

uab

les

Sp

ecif

ied

co

nte

nts

Co

nte

nts

At

the

site

Insi

de y

our

build

ing.

Aw

ay f

rom

th

e si

te

Tem

pora

rily

in tr

ansi

t to

your

new

hom

e (s

ee C

onte

nts

bein

g co

nvey

edto

you

r ne

w r

esid

ence

).

Any

whe

re in

Aus

tral

ia a

nd N

ew Z

eala

nd (s

ee Y

our c

onte

nts

tem

pora

rily

rem

oved

from

you

r ho

me)

.

Up

to 9

0 da

ysU

p to

90

days

Up

to 9

0 da

ysW

orld

wid

e (s

ee Y

our

cont

ents

tem

pora

rily

rem

oved

from

you

r ho

me)

.

= c

over

ed

= n

ot c

over

ed

27

How much you are covered for

Building

Sum insured (shown on your Policy Schedule).

Important note: We ask you to nominate your requiredsum insured.Your building sum insured should beadequate to replace your building and its fixtures andfittings using new materials as well as other necessarycosts in the event of a claim.

Refer to page 30 for tips on setting your sum insured.

Contents

Sum insured (shown on your Policy Schedule).

Important note: We ask you to nominate your requiredsum insured.Your contents sum insured should beadequate to replace all your contents with new items.

Refer to page 30 for tips on setting your sum insured.

High risk items with limits

Because we consider the items listed below to be highrisk, there are limits on what we will pay. If a claim ismade for a high risk item we will pay no more than theprescribed limit unless the item is specifically shownon the Policy Schedule as specified contents.The tablebelow also shows if you have the option to increasethe limit for that item by listing the item as specifiedcontents on your Policy Schedule. If you wish toincrease any of the allowed limits, please contact yourfinancial institution.

Please note that the most we will pay in total on a claimfor unspecified high risk items is the amount shown inthe table below.

28

Option toincrease limit

The most we willpay is:

High risk items withlimits

$1,000.Cash, bullion or negotiablesecurities

$10,000 per collection andin total 25% of the suminsured for unspecifiedcontents.

Collections of any kind

$3,000 per item and intotal 25% of the suminsured for unspecifiedcontents.

Each item of jewellery, goldor silver articles, furs andwatches

$2,000 per bicycle.A bicycle

$25,000 per item and intotal 25% of the suminsured for unspecifiedcontents.

Works of art, pictures,tapestries, rugs, antiques

$15,000 in total.Office or surgicalequipment used by you oryour family in your or theirown business in the home.

$5,000 in total.Tools of trade

= can be increased = cannot be increased

Specified valuables

As shown on your Policy Schedule.Sum insured

Legal liability

$30,000,000 ($30 million).Limit of legal liability

29

Your sum insured

Making the wrong assumptions about your sum insured, or the costs to rebuildyour home at today’s prices, can lead to under insurance and could cost youdearly.

Your home is unique so when considering how much to insure your homefor, it is important to remember that even homes identical in size will not haveidentical rebuilding costs. Costs such as removal of debris, replacement ofnew for old materials or items and the preparation of the land and foundationswill all vary from home to home.

To help make calculating your sum insured easy we have available for youon-line sum insured calculators that can assist you in determining your suminsured. The sum insured calculators take into account all those extra coststhat may not be obvious. For instance, removal of debris alone can add 10%to 15% to your sum insured.You will find these sum insured calculators byvisiting our website on:

http://www.intermediary.qbe.com.au/Insurance-Products/Home-And-Contents/Sum-Insured-Calculators/insurance.html

Alternatively, you can contact your financial institution and we can arrangeto send you QBE’s Home list guide. This will also help you to determine yoursum insured.

Remember that the cost of replacing your home and contents varies overtime, so it’s important to re-evaluate your cover each year, taking intoconsideration home renovations and new purchases. Although we make anaverage adjustment to your sum insured for inflation each year, we suggestyou review this increase to ensure it’s enough for you.

30

When your home is unoccupied

If your home is left unoccupied, cover may be reduced. Please see the tablebelow for details:

Unoccupied formore than 90days

Unoccupied formore than 30days

Unoccupied forup to 30 days

If yourbuilding is

no cover for:no change toyour coverage.

no change toyour coverage.

Furnishedfire;

explosion;

theft;

vandalismandmaliciousdamage;water orother liquid;orglassbreakage.

no cover for:no cover fortheft orvandalism andmaliciousdamage.

no change toyour coverage.

Unfurnishedfire;

explosion;

theft;

vandalismandAll other Policy

coverage, termsand conditionsremainunaltered.

maliciousdamage;water orother liquid;orglassbreakage.

The above will apply unless you have advised us and we agree to providefull Policy cover in writing.

Our agreement will take the form of an endorsement. We will send you aPolicy Schedule to confirm your Policy has been extended to insure you fora greater period of time.

31

Your proof of ownershipAt the time of making a claim if this Policy insures your contents, you willneed to provide evidence of value. We will also require evidence of value forhigh risk items or valuables whether specified on the Policy or not. Thisevidence can be a combination of:

receipts;a recent valuation provided by an Australian qualified valuer;instruction manuals;guarantee or warranty certificate;catalogues;make, model and serial number;photographs or video film of the item.

Proof of valuation – Jewellery, gold or silver articles

Jewellery, gold or silver articles, regardless of whether they are specifiedcontents or specified valuables, must have the valuation as listed in the tablebelow. If the evidence required by us is not provided, your claim will not beprocessed.

Required proof of ownershipItem value

No valuation required, only proof ofownership at the time of a claim.

Less than $1,499

A valuation dated prior to the date of lossrequired to be provided at the time oflodging a claim on the item.

$1,500 up to $14,999

A valuation dated prior to the Policyinception, or one more current replacing aprior valuation, to be provided at the timeof making a claim.

$15,000 up to $24,999

Important note: You will be required toacknowledge that a valuation of the itemexists at the time of specifying it on yourPolicy Schedule.

A valuation must be sighted by QBE priorto the item being specified on your PolicySchedule.

More than $25,000

32

What you are covered forYour QBE Policy insures you up to the amount of the sum insured for lossor damage to your building and/or contents caused by an insured event listedbelow.

Your Policy Schedule will indicate if you have insured your building, yourcontents or both.

Insured event

We will cover:Accidental loss ordamage

unintended and unexpected accidental loss ordamage to your building and/or contents.

We will not cover:

an event that is excluded by another sectionof this Policy;loss or damage to sporting equipment whilstin use or play;any items misplaced or disappeared if youcannot establish the cause;loss or damage to bicycles whilst they arebeing ridden;loss or damage to electronic data;

loss or damaged to mechanical, electronic orelectronic breakdown;loss or damage due to any process of cleaninginvolving the use of chemicals;loss or damage caused by deliberateapplication of heat.

For example, this would include where an elementunder or forming part of a ceramic cooktop causesdamage to the cooktop.

We will cover:Fire

damage to your building and/or contentscaused by a fire.

We will not cover:

damage to a heat resistant item and anyfittings or attachments on or in these items ifthe fire only caused damage to that item.

33

Insured event

Examples of heat resistant items are a cookingappliance, iron, toaster, microwave oven, heater,clothes dryer, electric kettle, chimney, fireplace,oven, potbelly stove.

We will cover:Explosion orimplosion

damage to your building and/or your contentscaused by an explosion or implosion.

We will not cover:

the item that exploded or imploded.

For example, we will not pay for an explodedheating boiler or a hot water system.

We will cover:Lightning orthunderbolt

damage to your building and/or contentscaused by a direct lightning strike orthunderbolt.

We will not cover:

damage if there is no visible evidence ofdamage to your building or your contents;damage if the Australian Government Bureauof Meteorology has no record of lighting orthunder in your area at the time the damageoccurred;damage caused by a power surge caused byanything other than lightning.

For example, when there has been a lightning strikethere will be visible damage to a power line or polenearby your home. Visible damage will also beevident to the appliance which is not working andwill include scorch or burn marks to the electricalcircuitry consistent with a lightning strike nearbyyour home.

34

Insured event

We will cover:Earthquake ortsunami

damage to your building and/or contentscaused by an earthquake or tsunami. Alldamage that occurs within a period of 48 hourswill be regarded as one incident.

We will not cover:

damage caused by a wave that arises fromany event other than a tsunami;

damage by erosion or earth movementoccurring more than seventy two (72) hoursfollowing the event.

Refer to the section ‘Your excess’ on page 77 fordetails on the excess payable on all earthquakeand tsunami claims.

We will cover:Theft

loss or damage to your building and/orcontents caused by theft or attempted theft.

We will not cover:

loss or damage if the theft was by you, yourfamily or tenants;loss or damage if the theft was caused by aperson who was in your building or at the site:

with your consent,with the consent of a person who lives inyour building,a person who with your consent is intemporary possession of your building.

We will cover:Vandalism andmalicious damage

damage to your building and/or your contentscaused by vandalism or malicious damage.

35

Insured event

We will not cover:

damage if the vandalism or malicious damagewas by you, your family or tenants;damage if the vandalism or malicious damagewas by a person who was in your building orat the site:

with your consent,with the consent of a person who lives inyour building, ora person who with your consent is intemporary possession of your building.

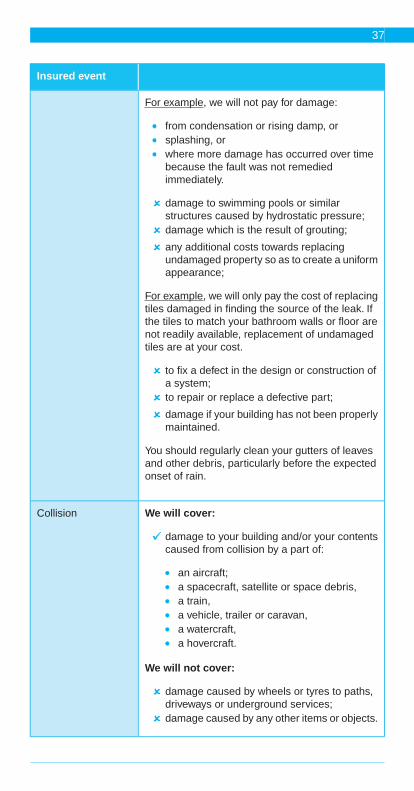

We will cover damage by:Water or other liquid

water or other liquids discharged, overflowingor leaking from any apparatus, appliance orpipe.

If this Policy insures your building and we acceptyour claim, we will also pay the reasonable cost:

to find the source of the leak; and

to repair only that section of your buildingwhich needs to be removed to repair the leak.

We will not cover:

water seeping through a wall or floor;

damage if the cause of the water or other liquidescaping was a deliberate act by you, or yourfamily or another person with your express orimplied consent to cause damage;costs to fix the leak;

costs of lost water;

the costs to repair or replace any defective partor item that caused the damage or the loss ofwater as a result of a leak;

For example, we will not pay for a new dishwasherhose that broke.

damage by erosion or earth movementoccurring more than seventy two (72) hoursfollowing the event;damage which is the result of gradualprocesses;

36

Insured event

For example, we will not pay for damage:

from condensation or rising damp, orsplashing, orwhere more damage has occurred over timebecause the fault was not remediedimmediately.

damage to swimming pools or similarstructures caused by hydrostatic pressure;damage which is the result of grouting;

any additional costs towards replacingundamaged property so as to create a uniformappearance;

For example, we will only pay the cost of replacingtiles damaged in finding the source of the leak. Ifthe tiles to match your bathroom walls or floor arenot readily available, replacement of undamagedtiles are at your cost.

to fix a defect in the design or construction ofa system;to repair or replace a defective part;

damage if your building has not been properlymaintained.

You should regularly clean your gutters of leavesand other debris, particularly before the expectedonset of rain.

We will cover:Collision

damage to your building and/or your contentscaused from collision by a part of:

an aircraft;a spacecraft, satellite or space debris,a train,a vehicle, trailer or caravan,a watercraft,a hovercraft.

We will not cover:

damage caused by wheels or tyres to paths,driveways or underground services;damage caused by any other items or objects.

37

Insured event

We will cover:Falling tree, branchor aerial

damage to your building and/or your contentscaused by a falling tree, branch, television orradio aerial or satellite aerial;the costs to remove the fallen tree or branchfrom the inside of your building to the nearestpermissible dumping ground so that thedamage can be dealt with. We will only paythese costs where the falling object has causeddamage to your building or contents;the reasonable cost of felling, pruning or stumpremoval when your building has beendamaged.

We will not cover:

damage to your building and/or your contentscaused by tree lopping or felling by you ordone with your consent;the costs for repairing:

a television, radio or satellite aerial, orthe fittings or masts, that caused thedamage.

We will cover:Damage by animals

damage to your building and/or your contentscaused from collision by an animal or bird thatis not kept in your building or at the site.

We will not cover:

damage caused by eating, chewing, clawing,pecking, scratching, soiling or fouling or anyother way of polluting your home.

We will cover:Riotdamage to your building and/or your contentscaused by riot, civil commotion, industrial orpolitical demonstration.

We will cover:Storm, rain or flood

damage to your building and/or your contentscaused by storm, rain or flood.

38

Insured event

We will not cover:

water damage to your building caused bystorm or rain seeping or otherwise enteringyour building unless the water entered throughan opening in the wall or roof that had beenmade directly by the storm or rain or as a directresult of it;damage caused by water penetrating orentering your building or as a result of a designfault, structural defect or because of defectiveworkmanship;damage caused by water entering yourbuilding through an opening in the wall or roofmade for the purpose of alterations, additions,renovation or repair;

For example, if, as part of renovations made toyour home an opening is made to your building wewill not continue to insure you against any storm,rain or flood damage unless the builder covers thisopening with a tarpaulin in a workmanlike way atevery possible opportunity.

damage caused by storm, rain or flood to:gates and fences which have been fitted tothe site and constructed of corrugatedfibrous materials and do not have asupporting frame except where installed tomanufacturers specifications,timber gates and fences more than fifteen(15) years old,privacy screens or retaining walls,shade-cloth, shade-sails, PVC blinds orumbrellas,spa or swimming pool covers, solar coversor plastic liners (including vinyl);

damage caused by water to external paintwork,treated surfaces or finishes, if that is the onlydamage done to that part of your building;damage caused by any residue deposited bythe rain on your building;damage to your swimming pool or spa if thedamage is as a result of hydrostatic pressure;damage caused to electrical or mechanicalequipment left in the open air, unless theequipment is designed to be weather proof;damage caused by the seas or high tide;

39

Insured event

damage caused by erosion or earth movementoccurring more than seventy two (72) hoursafter the event;damage caused by lightning or thunderbolt.

Cover for lightning or thunderbolt is provided underinsured event ‘Lightning or thunderbolt’.

We will cover:Power surgeloss or damage to your building and/orcontents caused by a power surge.

We will cover:Glass breakage

glass that is accidentally broken which formspart of your building if this Policy insures yourbuilding;glass that is accidentally broken which formspart of your contents if this Policy insures yourcontents;glass that forms part of the building when youare a tenant, but only if you are responsiblefor that glass under your lease if this Policyinsures your contents.

We will not cover:

glass that is part of a glass house orconservatory.

Limit:

Maximum $500 towards replacement of an ovendoor, stove door or cooking surfaces.

= covered = not covered

40

Your standard benefitsThis Policy also insures you for standard benefits set out in this section.

We pay these standard benefits as part of the sums insured for building orcontents depending on the type of cover you have chosen unless otherwisestated.

DescriptionBenefit

If this Policy insures your building, we willcover:

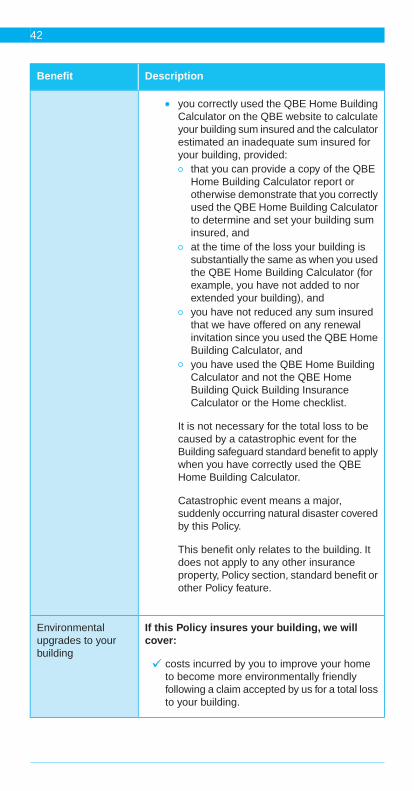

Building sum insuredsafeguard

up to 30% more than your building sum insuredto repair or replace your building if we agreethat the cost to repair or replace your buildingis greater than your building sum insured dueto:

the increased cost of repairing damage toyour building was caused directly by acatastrophic event, oryou correctly used the QBE Home BuildingCalculator on the QBE website to calculateyour building sum insured and the calculatorestimated an inadequate sum insured foryour building.

This benefit applies only if:

this Policy insures your building; and

your building is so damaged by an event thatis insured by this Policy that it is consideredby us to be a total loss; andthe cost to repair or replace your building isgreater than your building sum insuredbecause either:

the increased cost of repairing damage toyour building was caused directly by acatastrophic event. This applies where theresultant catastrophic event damage in thevicinity of your property is so extensive andwidespread that there is a surge in demandfor materials and labour, leading to anincrease in repair costs.Your building must be replaced in the areaaffected by the catastrophic event whilstbuilding costs remain elevated for thisbenefit to apply,or

41

DescriptionBenefit

you correctly used the QBE Home BuildingCalculator on the QBE website to calculateyour building sum insured and the calculatorestimated an inadequate sum insured foryour building, provided:

that you can provide a copy of the QBEHome Building Calculator report orotherwise demonstrate that you correctlyused the QBE Home Building Calculatorto determine and set your building suminsured, andat the time of the loss your building issubstantially the same as when you usedthe QBE Home Building Calculator (forexample, you have not added to norextended your building), andyou have not reduced any sum insuredthat we have offered on any renewalinvitation since you used the QBE HomeBuilding Calculator, andyou have used the QBE Home BuildingCalculator and not the QBE HomeBuilding Quick Building InsuranceCalculator or the Home checklist.

It is not necessary for the total loss to becaused by a catastrophic event for theBuilding safeguard standard benefit to applywhen you have correctly used the QBEHome Building Calculator.

Catastrophic event means a major,suddenly occurring natural disaster coveredby this Policy.

This benefit only relates to the building. Itdoes not apply to any other insuranceproperty, Policy section, standard benefit orother Policy feature.

If this Policy insures your building, we willcover:

Environmentalupgrades to yourbuilding

costs incurred by you to improve your hometo become more environmentally friendlyfollowing a claim accepted by us for a total lossto your building.

42

DescriptionBenefit

For example, installation of a rain water tank,skylight or insulation.

We will not cover:

costs in addition to your building sum insuredfor replacement of items or equipment alreadyinstalled in or on your building;costs incurred if your building is not a total loss.

Limit:

$2,500 per period of insurance.

If this Policy insurers your contents, we willcover:

Environmentalupgrades to yourcontents

additional costs that you have incurred toimprove the environmental rating of yourappliances following a claim for loss or damageto the item which we have paid.

For example, replacing a two (2) star energy ratedwashing machine with a three star energy ratedwashing machine.

We will not cover:

any costs where there has not been a claimaccepted and paid by for loss or damage tothe item.

Limit:

$500 per item up to a maximum of $2,500 perperiod of insurance.

If this Policy insures your building, we willcover:

Accommodation cost

the reasonable costs you incur for similaraccommodation while your building is beingrebuilt, repaired or replaced if you live in yourbuilding; orthe actual rent you lose or would have lost upto the time your building is built repaired orreplaced if you leased out your building or canshow that you would have leased it out;

43

DescriptionBenefit

if we have accepted a claim following damage toyour building and we agree that your building is notfit to live in.

If this Policy insures your contents, we willcover:

the reasonable costs that you incur for similaraccommodation or lost rent while your homeis being rebuilt, repaired or replaced if:

your home is a strata title unit that you ownand live in at the time of damage, oryou are a tenant and you are required tocontinue to pay rent under your lease,

if we have accepted a claim following damage toyour contents and we agree that your home is notfit to live in.

Limit:

The maximum we will pay for temporaryaccommodation or lost rent is the highest of:

the time it would take to repair or replace yourbuilding (or home) provided work commencesas soon as practicable after the incident, or10% of the sum insured, orif this Policy insures your building and you electnot to replace your building, the time it wouldhave taken to repair or replace your buildinghad you elected to do so.

This benefit is in addition to the sum insured.

If this Policy insures your building, and youhave entered a contract to sell the home, wewill cover the purchaser from:

Contractingpurchaser

when they become liable for any damage tothe home until the contract is settled orterminated, oruntil the purchaser insures the home,

whichever happens first.

44

DescriptionBenefit

If this Policy insures either your building oryour contents, we will:

Inflation adjustment

increase your building and/or contents suminsured as shown on your Policy Schedule by0.4% per month until the next renewal date.

If this Policy insures your building, we willcover:

Mortgage discharge

the legal costs to discharge any mortgage onyour building and the site if your building hasbeen completely destroyed.

Limit:

These legal costs will be paid by us in addition tothe sum insured for your building and paid as partof your claim for your building.

If this Policy insures your building, we willcover:

Extra costs ofreinstatement

the extra costs necessary to meet therequirements of any statutory authority inconnection with rebuilding or repairing yourbuilding at the site if your building is damagedas a result of an insured event under thisPolicy.

We will not cover:

any extra costs for requirements of anystatutory authority in connection to undamagedparts of your building;any extra costs which resulted from any noticewhich a statutory authority served on youbefore your building suffered loss or damage.

If this Policy insures either your building asyour primary residence or contents in yourprimary residence, we will cover:

Legal defence costs

your legal fees, costs and expenses which youreasonable incur in legal proceedings initiatedagainst you by a third party (and defended byyou) but only where the proceedings arecommenced in Australia during the period ofinsurance.

45

DescriptionBenefit

We will not cover any costs for proceedings orclaims:

relating to fines, penalties, punitive damages;

by family members including spouse,ex-spouse, partner or ex-partner;for or relating to divorce, separation, childvisiting, maintenance, property disputes;for or relating to defamation or slander;

for or relating to dishonesty, intentionalviolence, misconduct;relating to facts or occurrences, occurring priorto the commencement of the Policy which youknew or ought to have known at the time ofcommencement of this Policy, would, or might,give rise to a claim;initiated, threatened or commenced prior tothe commencement of this Policy;under or relating to any workers compensationlegislations, industrial award or agreement, orstatutory accident compensation scheme orcompulsory third party insurance;which could have been made under the section‘Legal liability’ if you had chosen to insure yourbuilding (if you own it) or contents.

Limit:

The maximum we will pay is $5,000 for any oneclaim or series of claims arising from the samecause or event.

If this Policy insures either your building asyour primary residence or contents in yourprimary residence, we will cover:

Taxation audit

costs for accountants fees which youreasonably incur as a result of your personaltaxation affairs being audited by the AustralianTaxation Office.

We will not cover any costs for:

any fines, penalties or shortfall in the amountof tax payable;any audit conducted in relation to criminalactivity;

46

DescriptionBenefit

any audit not commenced during the period ofinsurance;any fees incurred outside any statutory timelimit;any fees incurred as a result of any fraudulentact or fraudulent admission or any statementmade by you or on your behalf to a taxationofficer which:

is false or misleading in a material particular,andcan be attributed to deliberate evasion ofrecklessness as stipulated in income taxruling IT2517;

any audit conducted in relation to any facts orcircumstances of which you were aware, priorto the commencement of this Policy whichwere likely to lead you to your making a claimunder this Policy; orany fees incurred in relation to any enquiriesfrom the Australian Taxation Office which arenot related to an identified intention to conductan audit.

Limit:Up to a maximum of $5,000 for any one (1) audit.

We will cover:Fusion of electricmotors

the cost to repair a household electric motorif:

the motor has been burnt out by fusion, andthe motor is part of a machine or appliancewhich is part of your building and/orcontents insured by this Policy.

If it is not economical to repair your motor we will:

pay to replace the motor, or

pay you the amount it would cost us to replacethe motor.

Depreciation:

Where the motor is older than ten (10) years,depreciation will be applied to the cost of repairsat a rate of 20% per year for each additional year.In no case will your contribution exceed 90% afterapplying the excess.

47

DescriptionBenefit

We will not pay:

for motors more than fifteen (15) years old fromthe date of purchase when new or more thanfifteen (15) years old from the date ofrewinding;the cost of retrieving, removing or replacingthe pump section of pool or pressure pumpsor the cost of retrieving submersible pumps ortheir driving motors;the cost of hiring a replacement machine orappliance;for the cost of repair or replacement ofadditional parts or service items, includingworn or broken bearings or switches;for leakage of refrigerant driers;

electronic controllers or other electronics;

for lighting elements;

For example, light bulbs or fluorescent tubes,heating elements, solenoids, fuses or protectivedevices.

to repair or replace electrical contacts at whichsparking or arcing occurs in ordinary working;to repair or replace motors undermanufacturers' guarantee or warranty.

If this Policy insures either your building asyour primary residence or contents in yourprimary residence, we will cover:

Forced evacuationby governmentauthority

any increase in your living expenses up to sixty(60) days that is necessary and reasonable tomaintain your household’s normal standard ofliving following a forced evacuation by agovernment authority who prohibits you fromusing the site.

48

DescriptionBenefit

We will not cover:

if the evacuation and prohibition of the site wasnot a direct result of damage to neighbouringpremises that would be classed as insureddamage under this Policy.

Limit:Sixty (60) days.

If this Policy insures your building as yourprimary residence, we will cover:

Trees, shrubs andplants

loss or damage to a tree, shrub or plant causeddirectly by an insured event other than storm,or other events connected to weather or anyevent that is not sudden and unforeseen thatresults in the tree, shrub or plant being sodamaged that they die, are permanentlydisfigured or not recovered after being stolen.

We will not cover:

any loss or damage to grass or lawn.

Limit:We will pay up to $500 per tree, shrub or plant andup to $3,000 in total in any one (1) period ofinsurance.

If this Policy insures either your building orcontents, we will cover:

External door locks

costs to re-key or replace the locks in yourhome when the keys to these locks have beenstolen following an incident of theft.

Limit:$2,500 any one (1) claim.

49

DescriptionBenefit

We will cover:Essential temporaryrepairs

any essential temporary repairs to yourbuilding and/or contents which are necessaryfollowing damage by an insured event.Youare able to proceed with essential temporaryrepairs up to the limits stated below withoutobtaining our agreement beforehand.

For example, placing a tarpaulin over your roof ifit was damaged in a storm exposing the house tofurther damage would be considered essential.

Limit:

$500 any one (1) claim.

If this Policy insures either your building asyour primary residence or your contents in yourprimary residence, we will cover:

Modifications to thebuilding due toparaplegia orquadriplegia

costs incurred to modify your building orrelocate to a suitable building if you or amember of your family normally living with youpermanently become a paraplegic orquadriplegic as a direct result of an insuredevent occurring at the site for which we agreeto pay a claim.

Limit:$10,000 any one (1) period of insurance.

Conditions:

By the terms ‘paraplegic’ and ‘quadriplegic’ wemean where the paraplegic or quadriplegiccondition has existed for twelve (12) months andthe prognosis made by a registered medicalpractitioner confirms the condition is expected tolast indefinitely.

50

DescriptionBenefit

If this Policy insures your contents in yourprimary residence, we will pay:

Compensation fordeath

$10,000 to the legal representative of thedeceased person in the event of death of youor a member of your family normally living withyou, which occurs as a direct result of:

physical injury caused by an insured eventat the site, andif the insured event that caused the deathalso caused damage to which we agree topay a claim.

Limit:

$10,000 any one (1) period of insurance.

If this Policy insures your building as yourprimary residence, we will cover:

Building materialsawaiting installation

unfixed building materials intended to be usedfor repair, alteration or additions to yourbuilding that are lost or damaged at the sitedue to an insured event covered by this Policy.

We will not cover:

loss or damage caused to:soil,sand,gravel,bark, ormulch or similar materials;

loss or damage to any gas or electricalappliances unless they are in a locked andfully enclosed building at the site where thoseitems are not visible from the outside of thebuilding;where the building is not residentially occupiedat the time of the loss.

Limit:

$2,000 any one (1) period of insurance.

51

DescriptionBenefit

If this Policy insures your building, we willcover:

Building costs

costs to temporarily protect your building;

costs to remove debris from the site;

reasonable architecture or surveyor fees;

demolition costs;

costs to comply with statutory notice thatrelates to that part of your building which isdamaged and is served after the damageoccurred;

as part of your sum insured following damage toyour building.

Conditions:

We will only pay if these costs are necessary toreplace, repair, rebuild or preserve your building.

We will not cover any:

portion of these costs that relate to theundamaged parts of your building except inrespect to the temporary protection of yourbuilding.

If this Policy insures your contents in yourprimary residence, we will cover:

Cover when youmove sites

your contents at both your current site and atyour new address when you are moving intoa new building within Australia for up to thirty(30) days.

Limit:

The portion of the sum insured that the value ofthe contents at that site bears to the total value ofthe contents at both sites up to a maximum of thirty(30) days.

Conditions:

Your new address must be where you are movingto live instead of your current site.

52

DescriptionBenefit

You will need to advise us of your new address tocontinue cover beyond thirty (30) days.

You may need to pay us additional premium if weask for this and comply with any conditions weimpose.

If this Policy insures your contents in yourprimary residence, we will cover:

Contents beingconveyed to yournew residence

your contents for damage while they are in avehicle being used to convey your contents ifthe damage was as a direct result of:

theft from the conveying vehicle involvingthe use of a violent force,fire on the conveying vehicle, orcollision and/or overturning of the conveyingvehicle,

while your contents are in transit by road to:

your new primary place of residence withinAustralia, ora storage facility within Australia at whichyour contents or some of your contents willbe temporarily located pending conveyanceto your new primary place of residence.

We will not cover:

for removal to any residence other than oneintended to be occupied by you as yourprimary residence;for damage to china, glass, earthenware orany other item of a brittle nature;for damage caused by scratching, denting,bruising or chipping;outside Australia.

Limit: