hmda business design review & feedback...

TRANSCRIPT

HMDA Business Design Review & Feedback Sessions

As part of the Compliance Initiative to enhance ARGO's Loan Origination

System, the Software Requirements Specifications (SRS) for 2018 HMDA is

complete and approved by ARGO. The Compliance Partnership with ARGO's

clients for this effort includes individual Web-Ex Sessions to review the design

and receive feedback (which is strongly encouraged).

Each session is 90 minutes in length and will consist of a brief overview of the

HMDA SRS with the bulk of the session to be used as an open forum to discuss

the regulation and the proposed design for ARGO's Loan Origination System.

Using the link below, please select a 90 minute time slot that works for the applicable group at your institution. Once a time slot is booked, your institution will receive a calendar invitation which will include Web Ex details.

www.SignUpGenius.com/go/409054BAAAD2CA1F49-hmda

1500 Greenville Ave., Suite 500 Richardson, Texas 75081 P: (972) 866-3300 F: (972) 866-3301

Copyright © 2016 ARGO Data Resource Corporation. All rights reserved. Information contained in this document is proprietary to ARGO Data Resource Corporation, and may be used or disclosed only with written permission from ARGO Data Resource Corporation. This document, or any part thereof, may not be reproduced without the prior written permission of ARGO Data Resource Corporation. This document refers to numerous products by their trade names. In most cases, these designations are claimed as Trademarks or Registered Trademarks by their respective companies. This document and the related software described in this document are supplied under license or nondisclosure agreement and may be used or copied only in accordance with the terms of the agreement. The information in this document is subject to change without notice and does not represent a commitment on the part of ARGO Data Resource Corporation. The names of companies and individuals used in any sample database and in examples in the manuals are fictitious and are intended to illustrate the use of the software. Any resemblance to actual companies or individuals, whether past or present, is purely coincidental. If you have comments or suggestions about this documentation, please send an e-mail to [email protected].

Collateral Management /

2018 HMDA Regulations Software Requirements Specifications

V1.0: 12/8/2016

V1.0, 12/8/2016: Software Requirements Specification 1

Contents

1 Document Management............................................................................................ 3

1.1 Approval History ......................................................................................... 3

1.2 Revision History .......................................................................................... 3

1.3 Related Documents ..................................................................................... 3

1.4 Contacts .................................................................................................... 3

2 Introduction ............................................................................................................ 3

2.1 Purpose ..................................................................................................... 3

2.2 Scope ........................................................................................................ 4

2.3 Out of Scope Items ..................................................................................... 4

2.4 Dependencies ............................................................................................. 4

2.5 Risks/Unknowns ......................................................................................... 4

2.6 Assumptions............................................................................................... 4

2.7 Additional Considerations & Responsibilities ................................................... 5

3 Requirements ......................................................................................................... 6

3.1 System will display the following based on the changes required by regulation

changes ............................................................................................................. 6

3.2 Provide the ability to capture additional ethnicity information ........................... 7

3.3 Provide the ability to capture additional race information ................................. 8

3.4 System will provide the following functionality within the HMDA view .............. 10

3.5 Provide the ability to capture HMDA information for Home Equity Lines of Credit..

.............................................................................................................. 13

3.6 System will NOT display HMDA questions for unsecured loans with the Purpose of Home Improvement, beginning 01/01/2018 .......................................................... 13

3.7 System will display HMDA questions in Loan Details when collateral type is Real Estate, Manufactured Housing, or Manufactured Housing with Land ......................... 13

3.8 System will display the ‘HMDA Questions’ section within Loan Details when the collateral is General Commercial Real Estate ......................................................... 14

3.9 Provide the ability to capture HMDA information when the Pre-Qualify indicator is selected ........................................................................................................... 14

3.10 Provide updates to Property Details .......................................................... 14

3.11 System will display HMDA questions after Terms within Loan Details ............ 14

3.12 Provide the ability to configure the effective date for the HMDA borrower

information ....................................................................................................... 15

3.13 Provide the ability to configure effective date for the HMDA HELOC information ........................................................................................................... 15

3.14 Integrations .......................................................................................... 15

4 Supplemental Detail ............................................................................................... 15

4.1 Process Flow ............................................................................................ 15

4.2 Field Information ...................................................................................... 16

4.3 ADE Tag Information ................................................................................. 17

4.4 Form Detail .............................................................................................. 18

5 Additional Items .................................................................................................... 18

5.1 Glossary .................................................................................................. 18

Collateral Management / 2018 HMDA Regulations

ii V1.0, 12/8/2016: Software Requirements Specification

Collateral Management / 2018 HMDA Regulations

V1.0, 12/8/2016: Software Requirements Specification 3

1 Document Management

1.1 Approval History

Version Date Name Company

1.0 12/08/2016 Jill Hart ARGO

1.0 12/08/2016 Danny Tatom ARGO

1.0 12/08/2016 Jeremy Tassin ARGO

1.2 Revision History

Version Date Author CR# Revision Notes

1.0 12/08/2016 Robert Crump N/A Initial document release

1.3 Related Documents

Type Title Author Version URL or Location

SRS HMDA Enhancements Stephen

Henry

1.3 N/A

Configuration HMDA Field Mappings Robert Crump

N/A N/A

1.4 Contacts

Name Role Organization Document Update

Notification

Jill Hart Product Manager ARGO Yes

Robert Crump Business Analyst ARGO Yes

Jeremy Tassin Business Systems Architect

ARGO Yes

Danny Tatom Technical Integrator ARGO Yes

Amber Gullatte Software Engineer ARGO Yes

2 Introduction

2.1 Purpose

The Home Mortgage Disclosure Act (HMDA), Regulation C, was first passed in 1976 and requires lending institutions to report public loan data. The data is used to:

Help determine whether or not financial institutions are serving the housing needs of their communities.

Help public officials to effectively distribute public-sector funds so that private-sector investments will be attracted to places they are needed.

Identify possible discriminatory loan practices.

The compiled data is available through the Consumer Financial Protection Bureau (CFPB) web

site. HMDA regulations are periodically updated to address changing needs. This document focuses on the new and modified data points that are required to be captured as a result of the recent amendments to the Act.

Collateral Management / 2018 HMDA Regulations

4 V1.0, 12/8/2016: Software Requirements Specification

2.2 Scope

Requirement ID Requirement Name

1 System will display the following based on the changes required by regulation changes

2 Provide the ability to capture additional ethnicity information

3 Provide the ability to capture additional race information

4 System will provide the following functionality within the HMDA view

5 Provide the ability to capture HMDA information for Home Equity Lines of Credit

6 System will NOT display HMDA questions for unsecured loans with the Purpose of Home Improvement, beginning 01/01/2018

7 System will display HMDA questions in Loan Details when collateral type is Real Estate, Manufactured Housing, or Manufactured Housing with Land

8 System will display the ‘HMDA Questions’ section within Loan Details when the

collateral is General Commercial Real Estate

9 Provide the ability to capture HMDA information when the Pre-Qualify indicator is selected

10 Provide updates to Property Details

11 System will display HMDA questions after Terms within Loan Details

12 Provide the ability to configure the effective date for the HMDA borrower information

2.3 Out of Scope Items

Requirement ID Requirement Name

N/A N/A

2.4 Dependencies

N/A

2.5 Risks/Unknowns

N/A

2.6 Assumptions

Requirements apply to systematically identified HMDA covered Business and Personal

Loan Applications.

Added or modified data points in this document are available for data extract for

HMDA reporting purposes.

Sales Management Full Access has the ability to modify HMDA information. Sales

Management Limited Access does not.

No modifications are required to the Copy Application Process or Adverse Action

Process to support the requirements documented within this document.

No modifications are required to the CBRM editors to support the requirements

documented within this document.

None of the requirements within this document are dependent on Organizational

Hierarchy (i.e. Institution, Office) within the application.

None of the requirements within this document are dependent on Operator Security

settings.

Collateral Management / 2018 HMDA Regulations

V1.0, 12/8/2016: Software Requirements Specification 5

Any properties defined for screen elements in a specific stage will be inherited by the

Sales Management view when accessed for that specific stage.

The requirements defined in this document do not require additional Error Handling

beyond the current base product template.

None of the requirements within this document introduce new Archive, Reporting,

Imaging, Calculations, Audit, Off-Line, Third Party Interfaces, Workflow Management or Queuing & Routing Rules.

No impacts to the Loan Summary View(s).

2.7 Additional Considerations & Responsibilities

The art provided is intended to be visual illustrations of the design details. They are

loose representations and allow for minor deviations where required. However, if

constraints exist that require a level of deviation resulting in a state unrepresentative of the illustration please consult ARGO for details.

Fields are optional unless specifically called out as required.

Fields are editable unless specifically called out as read-only.

Controls are enabled unless specifically called out as disabled.

Enterable fields in this document will be editable in the following stages/statuses,

unless stated otherwise:

– Origination: All statuses

– Underwriting: All statuses

– Processing: All statuses

– Closing: Underwriter Review

– Closing: Processor Review

Enterable fields described in this document will become read-only and/or disabled in

the following stages/statuses, unless stated otherwise:

– Closing: All statuses with the exception of Closing: Underwriter Review and

Closing: Processor Review

– Booking: All statuses

– Sales Management (Full Access)

– Sales Management (Limited Access)

HMDA borrower information is not available in the following stages/statuses:

– Underwriting: All Statuses

– Processing: All Statuses

– Closing: Underwriter Review

– Closing: Processor Review

All requirements apply to the following collateral types unless otherwise stated:

– Real Estate

Collateral Management / 2018 HMDA Regulations

6 V1.0, 12/8/2016: Software Requirements Specification

– Manufactured Housing with Land

3 Requirements

Functional Requirements

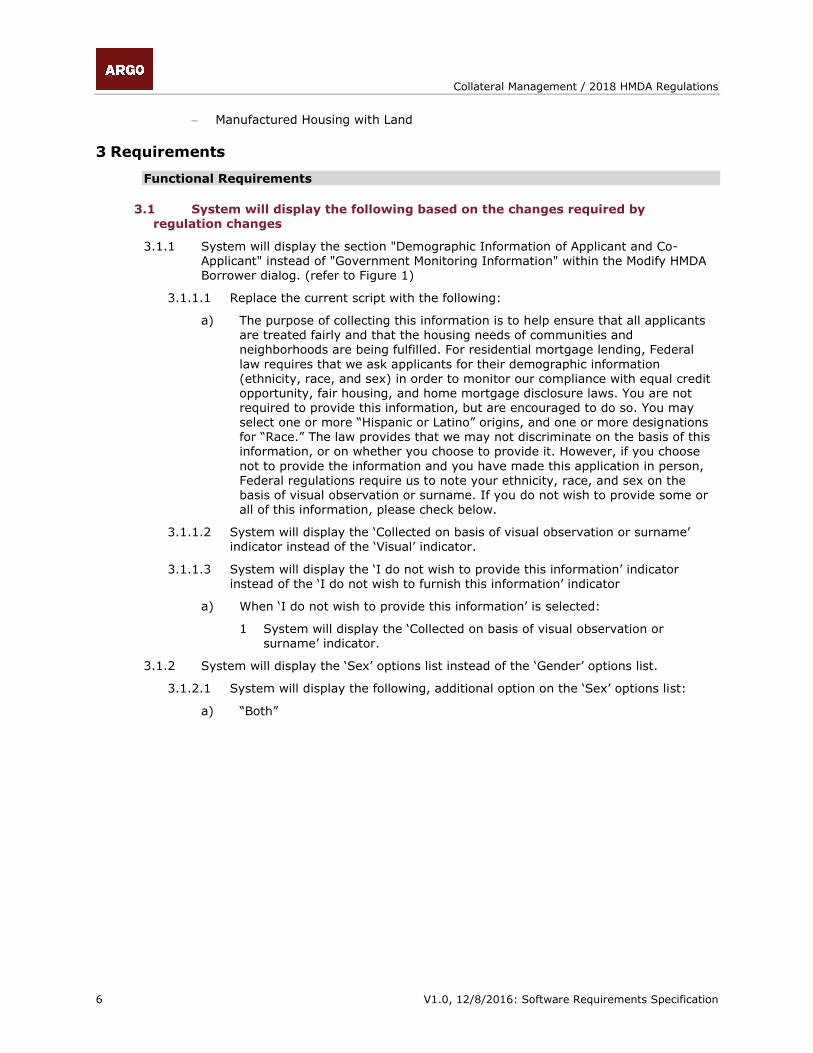

3.1 System will display the following based on the changes required by regulation changes

System will display the section "Demographic Information of Applicant and Co-3.1.1Applicant" instead of "Government Monitoring Information" within the Modify HMDA Borrower dialog. (refer to Figure 1)

Replace the current script with the following: 3.1.1.1

The purpose of collecting this information is to help ensure that all applicants a)are treated fairly and that the housing needs of communities and neighborhoods are being fulfilled. For residential mortgage lending, Federal

law requires that we ask applicants for their demographic information (ethnicity, race, and sex) in order to monitor our compliance with equal credit opportunity, fair housing, and home mortgage disclosure laws. You are not required to provide this information, but are encouraged to do so. You may select one or more “Hispanic or Latino” origins, and one or more designations for “Race.” The law provides that we may not discriminate on the basis of this information, or on whether you choose to provide it. However, if you choose

not to provide the information and you have made this application in person, Federal regulations require us to note your ethnicity, race, and sex on the basis of visual observation or surname. If you do not wish to provide some or all of this information, please check below.

System will display the ‘Collected on basis of visual observation or surname’ 3.1.1.2indicator instead of the ‘Visual’ indicator.

System will display the ‘I do not wish to provide this information’ indicator 3.1.1.3instead of the ‘I do not wish to furnish this information’ indicator

When ‘I do not wish to provide this information’ is selected: a)

System will display the ‘Collected on basis of visual observation or 1surname’ indicator.

System will display the ‘Sex’ options list instead of the ‘Gender’ options list. 3.1.2

System will display the following, additional option on the ‘Sex’ options list: 3.1.2.1

“Both” a)

Collateral Management / 2018 HMDA Regulations

V1.0, 12/8/2016: Software Requirements Specification 7

Figure 1: Modify HMDA Borrower dialog with ‘I do not wish to provide this information’ indicator selected.

3.2 Provide the ability to capture additional ethnicity information

System will display the ‘Ethnicity’ section on the Modify HMDA Borrower dialog. (refer 3.2.1to Figure 2)

When the ‘Hispanic or Latino’ indicator is selected, the system will: 3.2.1.1

Display the text “Check one or more” a)

Display the following indicators: b)

Mexican 1

Puerto Rican 2

Cuban 3

Other Hispanic or Latino 4

When ‘Other Hispanic or Latino’ is selected: c)

System will display the ‘Enter origin, for example Argentinean, Colombian, 1

Dominican, Nicaraguan, Salvadoran, Spaniard, etc.:’ field.

Collateral Management / 2018 HMDA Regulations

8 V1.0, 12/8/2016: Software Requirements Specification

Figure 2: Ethnicity and Race Selected

3.3 Provide the ability to capture additional race information

System will display the ’Race’ section on the Modify HMDA Borrower dialog. (refer to 3.3.1Figure 2)

Display the text “Check one or more” 3.3.1.1

Display the ‘American Indian or Alaska Native’ indicator. (refer to Figure 3) 3.3.1.2

When ‘American Indian or Alaska Native’ is selected, display the ‘Enter name a)of enrolled or principal tribe:’ field.

Display the ‘Asian’ indicator (refer to Figure 2) 3.3.1.3

When ‘Asian’ is selected, system will display the following indicators: 3.3.1.4

Asian Indian a)

Chinese b)

Filipino c)

Japanese d)

Korean e)

Collateral Management / 2018 HMDA Regulations

V1.0, 12/8/2016: Software Requirements Specification 9

Vietnamese f)

Other Asian g)

When ‘Other Asian’ is selected, system will display: 3.3.1.5

‘Enter race, for example, Hmong, Laotian, Thai, Pakistani, Cambodian, etc.’ a)

field.

Display the ‘Black or African American’ indicator (refer to Figure 3) 3.3.1.6

Display the ‘Native Hawaiian or Other Pacific Islander’ indicator (refer to Figure 3.3.1.74)

When ‘Native Hawaiian or Other Pacific Islander’ is selected, display the 3.3.1.8following indicators:

Native Hawaiian a)

Guamanian or Chamorro b)

Samoan c)

Other Pacific Islander d)

When ‘Other Pacific Islander’ is selected, system will display: 3.3.1.9

‘Enter race, for example, Fijian, Tongan, etc.:’ field. a)

Display the ‘White’ indicator. (refer to Figure 3) 3.3.1.10

Figure 3: HMDA American Indian/Alaska Native

Collateral Management / 2018 HMDA Regulations

10 V1.0, 12/8/2016: Software Requirements Specification

Figure 4: HMDA Native Hawaiian/Other Pacific Islander

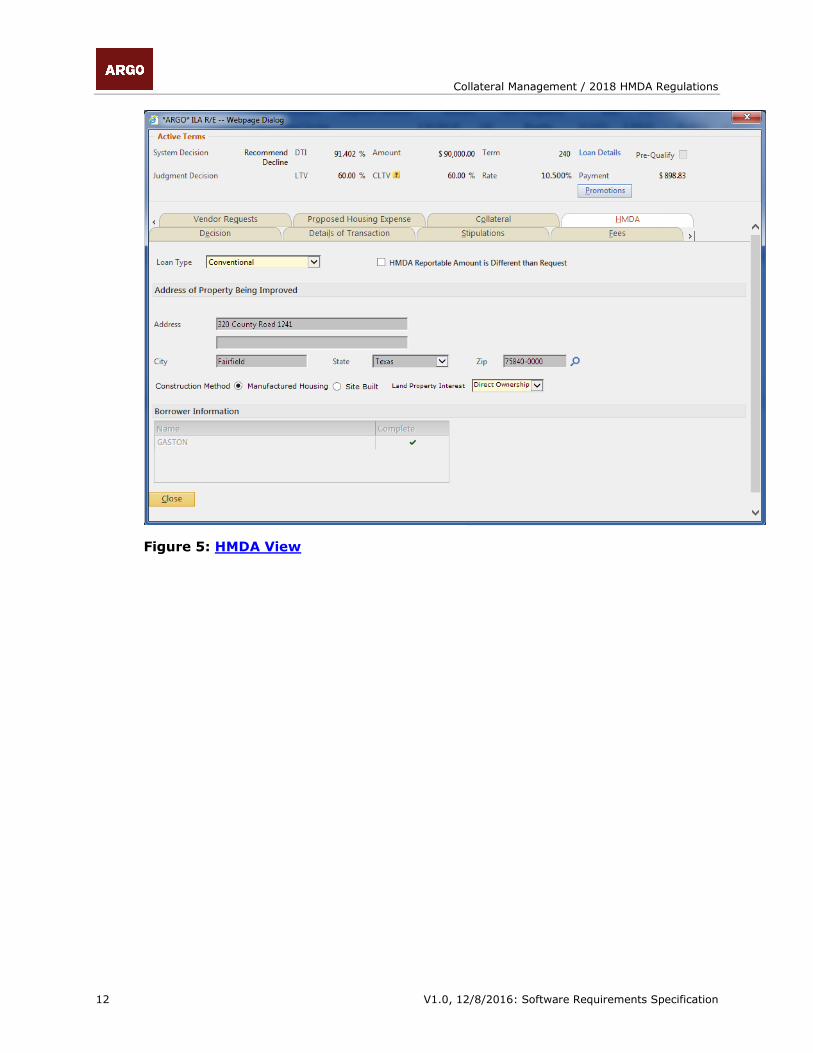

3.4 System will provide the following functionality within the HMDA view

System will hide the following fields in all stages and statuses: (refer to Figure 5) 3.4.1

State Code field 3.4.1.1

County Code field 3.4.1.2

MSA/MD field 3.4.1.3

Hide after 1/1/2018 a)

Occupancy Type options list 3.4.1.4

Property Type options list 3.4.1.5

Hide after 1/1/2018 a)

‘Prefill From’ options list 3.4.1.6

System will set the following fields read-only and populate from the subject property 3.4.2address:

Address Line 1 3.4.2.1

Address Line 2 3.4.2.2

City 3.4.2.3

State 3.4.2.4

Collateral Management / 2018 HMDA Regulations

V1.0, 12/8/2016: Software Requirements Specification 11

Zip 3.4.2.5

System will display ‘Construction Method’ with the following required options: (refer 3.4.3to Figure 5)

Site Built 3.4.3.1

HMDA value = 1 a)

Manufactured Home 3.4.3.2

HMDA value = 2 a)

Display the ‘Land Property Interest’ options list on the ‘HMDA’ view, with the 3.4.4following options:

Blank – Default 3.4.4.1

Direct Ownership 3.4.4.2

Indirect Ownership 3.4.4.3

Paid Leasehold 3.4.4.4

Unpaid Leasehold 3.4.4.5

Not Applicable 3.4.4.6

System will display the ‘Census Tract’ field within the ‘Property Details’ view. (refer 3.4.5to Figure 6)

Census Tract retains current functionality. 3.4.5.1

System will display the ‘Property Rights Appraised’ options list, within ‘Property 3.4.6Details’, with the following options:

Blank – Default 3.4.6.1

Fee Simple 3.4.6.2

Lease Hold 3.4.6.3

Indirect Ownership 3.4.6.4

Unpaid Leasehold 3.4.6.5

Other 3.4.6.6

System will display “Multifamily” instead of “Imp Residential 5 or more Family” in the 3.4.7‘Property Type’ options list, when the collateral type is General Commercial Real Estate (GCRE).

Collateral Management / 2018 HMDA Regulations

12 V1.0, 12/8/2016: Software Requirements Specification

Figure 5: HMDA View

Collateral Management / 2018 HMDA Regulations

V1.0, 12/8/2016: Software Requirements Specification 13

Figure 6: Property Details

3.5 Provide the ability to capture HMDA information for Home Equity Lines of

Credit

System will display the HMDA questions within Product Details for Products 3.5.1configured as Home Equity within Product Manager, beginning 10/01/2017.

3.6 System will NOT display HMDA questions for unsecured loans with the Purpose of Home Improvement, beginning 01/01/2018

3.7 System will display HMDA questions in Loan Details when collateral type is

Real Estate, Manufactured Housing, or Manufactured Housing with Land

System will display ‘Q1. Are any loan proceeds used to purchase a home or an 3.7.1ownership interest in a home, or pay off a construction loan that was used to build a home?’ with Yes/No options.

System will display ‘Q2. Are any loan proceeds being used to make home 3.7.2improvements/repairs, or pay off a construction loan that was used for home improvements/repairs?’ with Yes/No options.

System will display ‘Q3. Will any of the proceeds for this loan pay off a 1-4 family 3.7.3dwelling secured debt in the same borrower’s name (existing and the new loan are in the same names)?’ with Yes/No options?’ with Yes/No options.

Collateral Management / 2018 HMDA Regulations

14 V1.0, 12/8/2016: Software Requirements Specification

System will display ‘Q3.1. Does any portion of the proceeds include Cash-out?’ 3.7.3.1with Yes/No options, when ‘Q3. Will any of the proceeds for this loan pay off a 1-4 family dwelling secured debt in the same borrower’s name (existing and the new loan are in the same names)?’ is “Yes”.

System will display ‘Q4. Is this a dwelling secured loan with a purpose other than 3.7.4home purchase, home improvement, refinancing, or cash-out refinance?’ with Yes/No options.

3.8 System will display the ‘HMDA Questions’ section within Loan Details when the collateral is General Commercial Real Estate

System will display ‘Is this business loan secured by a dwelling?’ with Yes/No 3.8.1options.

System will display the HMDA questions when ‘Is this business loan secured by 3.8.1.1a dwelling?’ is “Yes”.

3.9 Provide the ability to capture HMDA information when the Pre-Qualify indicator is selected

System will display the HMDA questions within Product Details when the Pre-Qualify 3.9.1indicator is selected, AND the collateral is Real Estate.

System will NOT display the HMDA questions when one of the following is true: 3.9.1.1

‘Purpose’ is “Purchase” AND ‘Payment & Rate Option’ is “Open End” a)

‘Property Type’ within Property Details is “Multifamily” b)

3.10 Provide updates to Property Details

System will display the “Principal Residence” instead of “Primary Residence” within 3.10.1the ‘Occupancy Type’ options list. (refer to Figure 6)

System will display “Multifamily” as an option within the’ Property Type’ options list. 3.10.2

When ‘Property Type’ is “Multifamily”: 3.10.2.1

System will display the ‘Total Number of Units’ field as required. a)

Valid values are whole numbers greater than or equal to 5. 1

System will display ‘Is the Multifamily dwelling income restricted?’ with Yes/No b)options.

When ‘Is the Multifamily dwelling income restricted?’ is “Yes” c)

Display the ‘Number of units that are income restricted’ field as required. 1

Valid values are whole numbers greater than 0.

3.11 System will display HMDA questions after Terms within Loan Details

System will display the ‘HMDA Questions’ section directly below the ‘Terms’ section 3.11.1(refer to Figure 7)

Collateral Management / 2018 HMDA Regulations

V1.0, 12/8/2016: Software Requirements Specification 15

Figure 7: HMDA Section

Non-Functional Requirements

3.12 Provide the ability to configure the effective date for the HMDA borrower

information

Default effective date is 01/01/2018. 3.12.1

Based on application received date 3.12.1.1

3.13 Provide the ability to configure effective date for the HMDA HELOC

information

Default effective date is 10/01/2017. 3.13.1

Based on action date 3.13.1.1

Withdrawn a)

Decline b)

Funding c)

Customer not Accepted d)

Closed for Incompleteness e)

3.14 Integrations

N/A

4 Supplemental Detail

4.1 Process Flow

Collateral Management / 2018 HMDA Regulations

16 V1.0, 12/8/2016: Software Requirements Specification

N/A

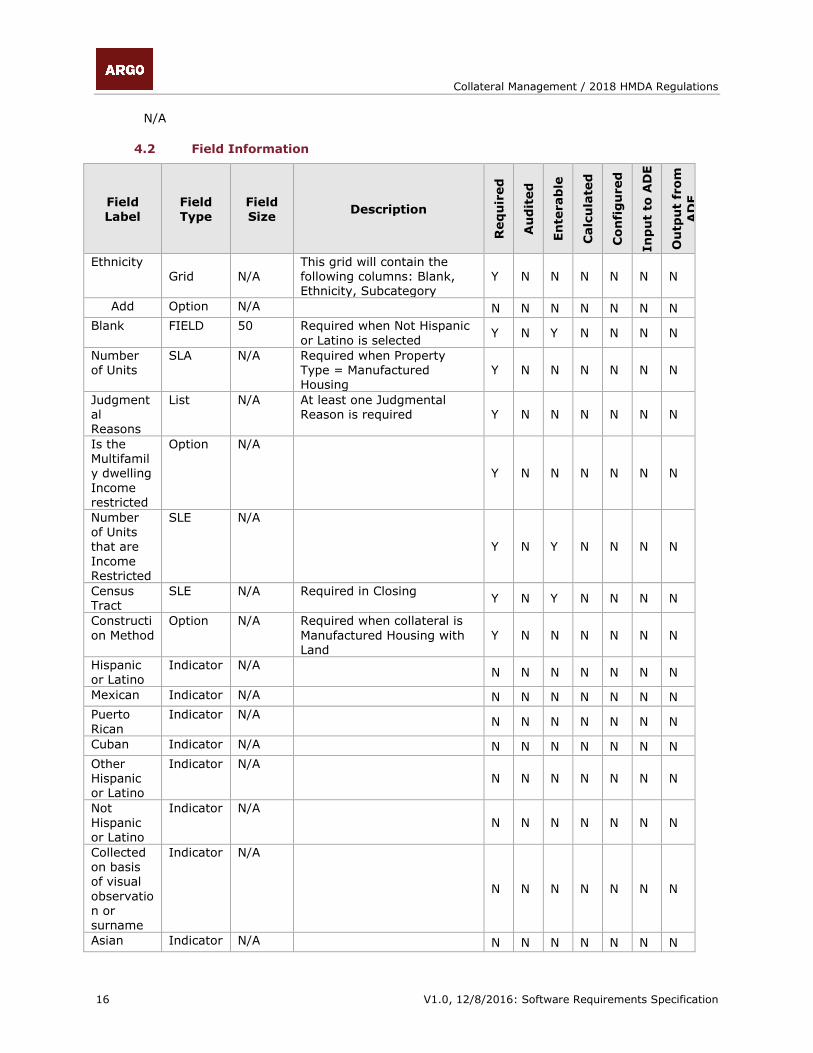

4.2 Field Information

Field

Label

Field

Type

Field

Size Description

Req

uir

ed

Au

dit

ed

En

terab

le

Calc

ula

ted

Co

nfi

gu

red

In

pu

t to

AD

E

Ou

tpu

t fr

om

AD

E

Ethnicity Grid N/A

This grid will contain the following columns: Blank, Ethnicity, Subcategory

Y N N N N N N

Add Option N/A N N N N N N N

Blank FIELD 50 Required when Not Hispanic

or Latino is selected Y N Y N N N N

Number of Units

SLA N/A Required when Property Type = Manufactured Housing

Y N N N N N N

Judgmental Reasons

List N/A At least one Judgmental Reason is required Y N N N N N N

Is the Multifamily dwelling

Income restricted

Option N/A

Y N N N N N N

Number of Units that are

Income

Restricted

SLE N/A

Y N Y N N N N

Census Tract

SLE N/A Required in Closing Y N Y N N N N

Constructi

on Method

Option N/A Required when collateral is

Manufactured Housing with Land

Y N N N N N N

Hispanic or Latino

Indicator N/A N N N N N N N

Mexican Indicator N/A N N N N N N N

Puerto

Rican

Indicator N/A N N N N N N N

Cuban Indicator N/A N N N N N N N

Other Hispanic or Latino

Indicator N/A N N N N N N N

Not

Hispanic or Latino

Indicator N/A

N N N N N N N

Collected on basis of visual

observation or surname

Indicator N/A

N N N N N N N

Asian Indicator N/A N N N N N N N

Collateral Management / 2018 HMDA Regulations

V1.0, 12/8/2016: Software Requirements Specification 17

Field Label

Field Type

Field Size

Description

Req

uir

ed

Au

dit

ed

En

terab

le

Calc

ula

ted

Co

nfi

gu

red

In

pu

t to

AD

E

Ou

tpu

t fr

om

AD

E

Indian

Chinese Indicator N/A N N N N N N N

Filipino Indicator N/A N N N N N N N

Japanese Indicator N/A N N N N N N N

Korean Indicator N/A N N N N N N N

Vietnamese

Indicator N/A N N N N N N N

Other Asian

Indicator N/A N N N N N N N

Native Hawaiian

Indicator N/A N N N N N N N

Guamanian or Chamorro

Indicator N/A N N N N N N N

Samoan Indicator N/A N N N N N N N

Other Pacific Islander

Indicator N/A N N N N N N N

I do not wish to provide this informatio

n

Indicator N/A

N N N N N N N

Sex DDLB N/A Y N N N N N N

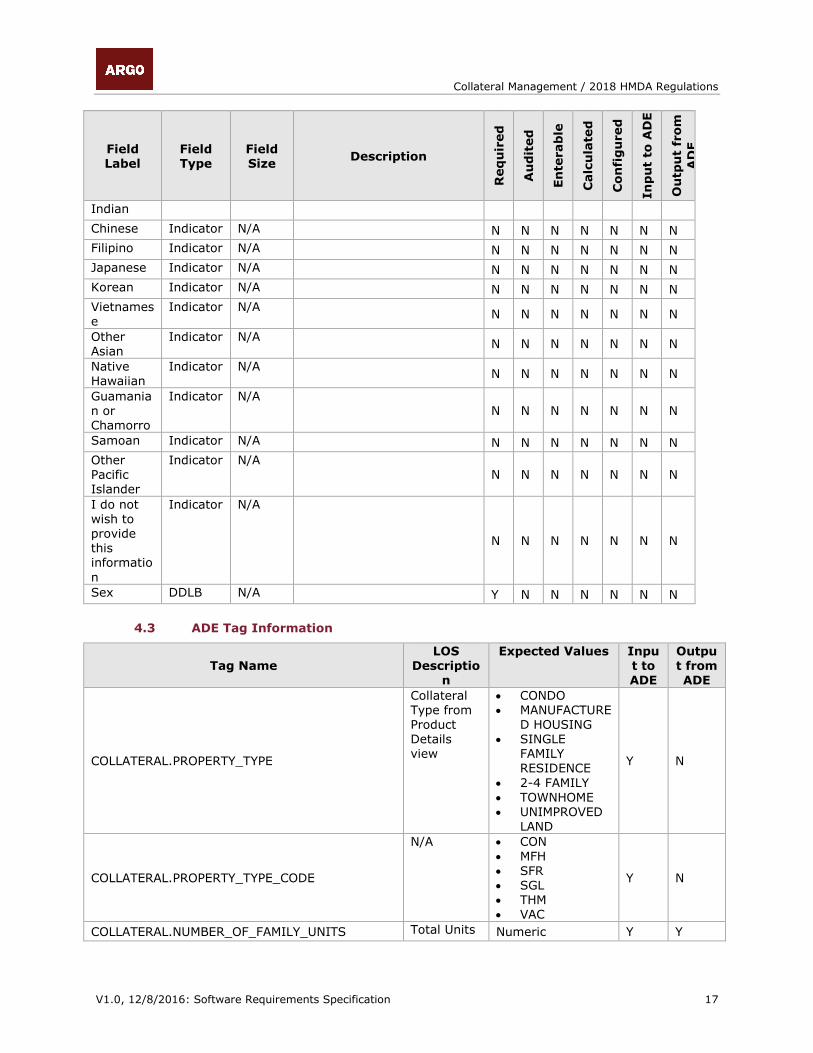

4.3 ADE Tag Information

Tag Name LOS

Description

Expected Values Input to ADE

Output from ADE

COLLATERAL.PROPERTY_TYPE

Collateral Type from Product Details view

CONDO MANUFACTURE

D HOUSING SINGLE

FAMILY RESIDENCE

2-4 FAMILY

TOWNHOME UNIMPROVED

LAND

Y N

COLLATERAL.PROPERTY_TYPE_CODE

N/A CON

MFH SFR SGL THM VAC

Y N

COLLATERAL.NUMBER_OF_FAMILY_UNITS Total Units Numeric Y Y

Collateral Management / 2018 HMDA Regulations

18 V1.0, 12/8/2016: Software Requirements Specification

PRODUCT.HIGHER_PRICED_MORTGAGE_APR_SPREAD

N/A Numeric N/A N/A

PRODUCT.HOEPA_YN N/A Y/N N/A N/A

4.4 Form Detail

Form Name Description Trigger Event

N/A N/A N/A

5 Additional Items

5.1 Glossary

Item Description

HMDA

Home Mortgage Disclosure Act. A federal act approved in 1975 that requires mortgage lenders to keep records of certain key pieces of information regarding

their lending practices. The primary purposes of the Home Mortgage Disclosure Act (HMDA) are to help authorities monitor discriminatory and predatory lending practices, as well as to ensure government resources are allocated properly

Census Tract

Small, relatively permanent statistical subdivisions of a county or equivalent entity that are updated by local participants prior to each decennial census as

part of the Census Bureau's Participant Statistical Areas Program. Census tracts generally have a population size between 1,200 and 8,000 people, with an optimum size of 4,000 people.

Tract Code Census tracts are identified by an up to four-digit integer number and may have an optional two-digit suffix; for example 1457.02 or 23.

CFPB Consumer Financial Protection Bureau