hiscox plc preliminary results for the year ended 31 december 2005

DESCRIPTION

Hiscox plc Preliminary results for the year ended 31 December 2005. March 2006. Good results for a tough year. Profit before tax (£m). Combined Ratio (%). 89.5. 70.2. 92.6. 96.0. 2005. 2005. 2004. 2004. 2. Disciplined underwriting. Gross Written Premium (£m). - PowerPoint PPT PresentationTRANSCRIPT

www.hiscox.com

Aerospace Bloodstock Classic Cars Employers’ Liability Energy Financial Institutions Fine Art High Value Household Kidnap & Ransom Marine Media Personal Accident Political Risks Professional Indemnity Property Reinsurance Specie Technology Terrorism War

Hiscox plc

Preliminary results for the year ended 31 December 2005

March 2006

Good results for a tough year

2

Profit before tax (£m)

2004 2005

70.289.5

Combined Ratio (%)

2004 2005

96.092.6

3

0

100

200

300

400

500

600

700

800

900

2001 2002 2003 2004 2005

548.9

676.7

797.4 816.6

Gross Written Premium (£m) Net Premium Earned (£m)

0

100

200

300

400

500

600

700

800

900

2001 2002 2003 2004 2005

344.2385.1

547.5

714.9

Disciplined underwriting

861.2

693.3

31 Dec 2004 31 Dec 2005

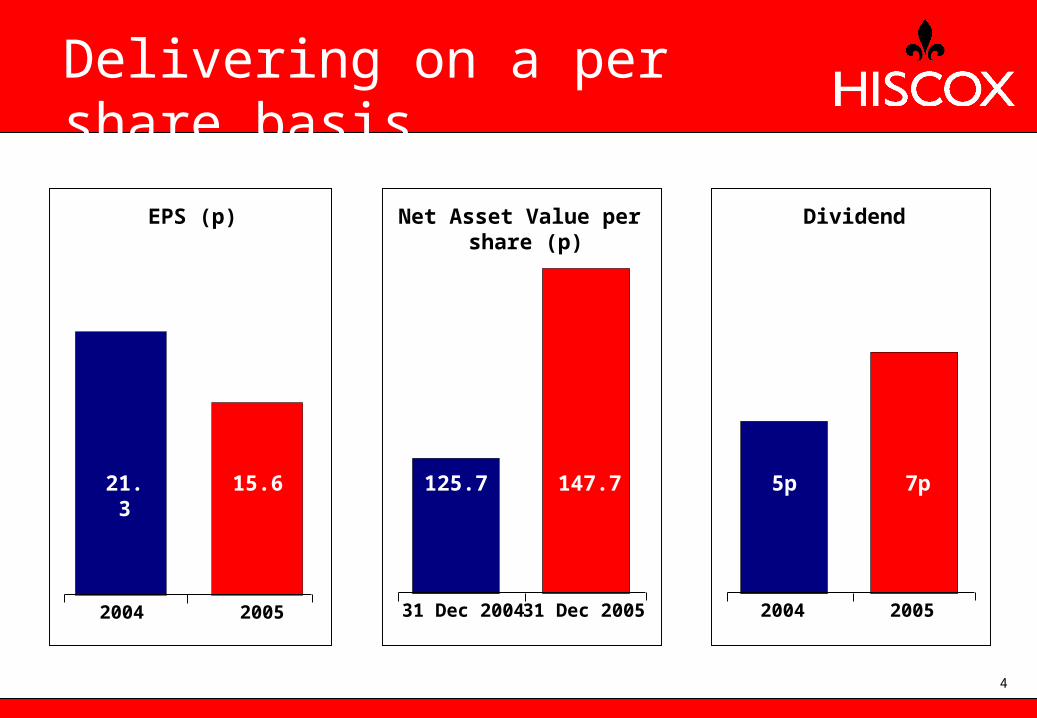

Delivering on a per share basis

Net Asset Value per share (p)

125.7 147.7

4

EPS (p)

2004 2005

15.621.3

2004 2005

Dividend

5p 7p

Strategy delivering balance

Hiscox UK

– Great results

Hiscox Global Markets

– Good underwriting results

Hiscox Europe

– Second year of profit

Regional expansion

– Creation of Hiscox Bermuda

– Creation of Hiscox USA

5

Financial performance

6

Hiscox plc results

Full Year 2005£000

Full Year 2004£000

Gross Premiums Written 861,174 816,609

Net Premiums Written 681,236 704,085

Net Premiums Earned 693,299 714,852

Profit before tax 70,221 89,522

Profit after tax 48,630 63,948

Basic Earnings per share (p) 15.6p 21.3p

Final Dividend (p) 4.75p 3.5p

Full Year Dividend (p) 7.0p 5.0p

Net Asset Value

• £m 578.0 368.8

• p per share 147.7 125.7

Return on equity after tax* 12.8% 20.6%

7

* Post tax, based on adjusted opening shareholders’ funds

Segmental analysis

For the year ended 31 December

8

2005Global Markets & Corporate

Centre£000

UK & Europe

£000International

£000

Total£000

Gross Premiums Written

Net Premiums Earned

Profit before tax

555,183

428,334

861,174

693,299

43,720

23,362

262,271

241,603

Combined Ratio 99.9% 96.0%91.3%86.9%

Global Markets & Corporate Centre: Hiscox plc’s share of the results of Syndicate 33, excluding Syndicate 33’s specie, fine art and non-US household business. It also includes the investment return and administrative costs associated with the parent company and other group management activities. UK & Europe: The results of Hiscox Insurance Company Limited, Hiscox plc’s share of Syndicate 33’s specie, fine art and non-US household business, together with the income and expenses arising from the group’s retail agency activities in the UK and in continental Europe.International: The results of Hiscox Insurance Company (Guernsey) Limited, Hiscox Insurance Company (Bermuda) Limited, and the US agency, Hiscox Inc.

70,2216,15520,716 43,350

Net Premiums Written 417,128 681,23628,832235,276

511,491

483,958

816,609

714,852

37,317

18,526

267,801

212,368

90.9% 92.6%92.0%98.0%

89,5222,85767,810 18,855

451,517 704,08519,465233,103

2004GlobalMarkets &Corporate

Centre£000

UK &Europe£000

International£000

Total£000

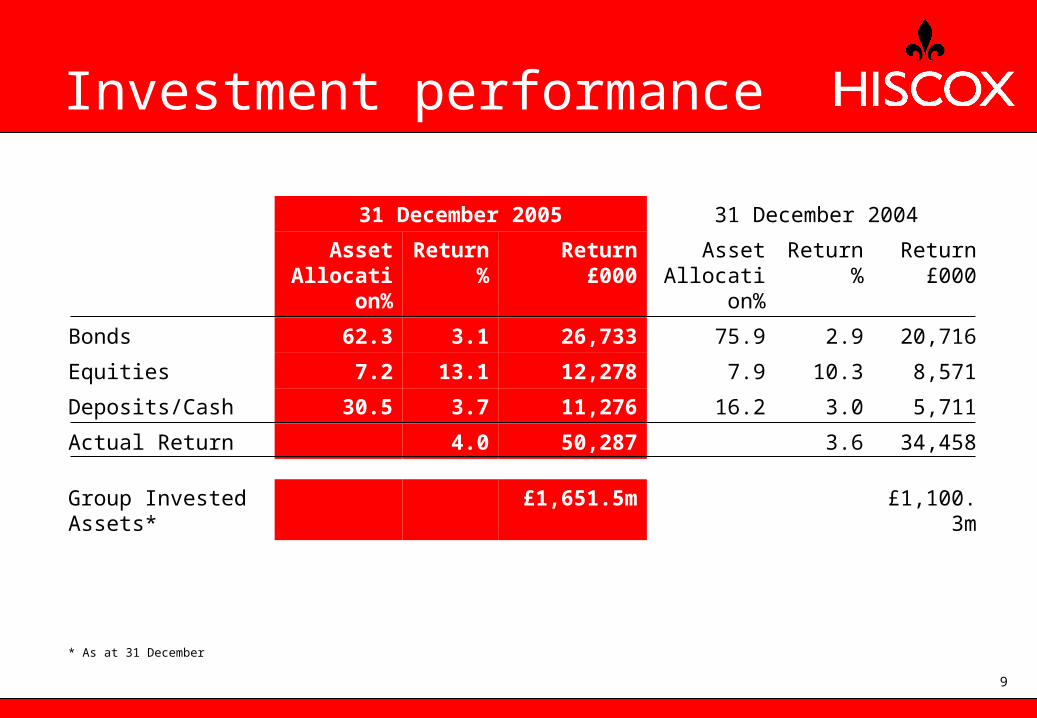

31 December 2005 31 December 2004

Asset Allocation

%

Return%

Return£000

Asset Allocation

%

Return%

Return£000

Bonds 62.3 3.1 26,733 75.9 2.9 20,716

Equities 7.2 13.1 12,278 7.9 10.3 8,571

Deposits/Cash 30.5 3.7 11,276 16.2 3.0 5,711

Actual Return 4.0 50,287 3.6 34,458

Investment performance

9

Group Invested Assets*

£1,651.5m £1,100.3m

* As at 31 December

Financial activity

£170m rights issue at 183p - Nov 2005

45% gearing at 31 December 2005

– £137.5m letter of credit

– $225m term and revolving loan facilities

– Further gearing from third party capital

Syndicate 33

– 73% ownership

– 41% capital ratio

Strong internal capital modelling10

Hiscox Global Markets

11

0

100

200

300

400

Jan

98

to D

ec9

8

Jul9

8 to

Ju

n9

9

Jan

99

to D

ec9

9

Jul9

9 to

Ju

n0

0

Jan

00

to D

ec0

0

Jul0

0 to

Ju

n0

1

Jan

01

to D

ec0

1

Jul0

1 to

Ju

n0

2

Jan

02

to D

ec0

2

Jul0

2 to

Ju

n0

3

Jan

03

to D

ec0

3

Jul0

3 to

Ju

n0

4

Jan

04

to D

ec0

4

Jul0

4 to

Ju

n0

5

Jan

05

to D

ec0

5

Rating

12

Syndicate 33 Rating Index

London MarketReinsuranceSpecialty

Ind

ex

le

ve

l%

Hurricane impact

Reserving process led by Jeremy Pinchin, new Head of Claims

Total estimated loss to plc:

Bottom line impact of £85m, an increase of £25m since rights issue

Limited reinsurance cover left for these events

Gross loss (US$m)

Net loss (US$m)

Katrina 485.0 156.9

Rita 166.1 81.2

Wilma 81.3 45.6

Total 732.4 283.7

13

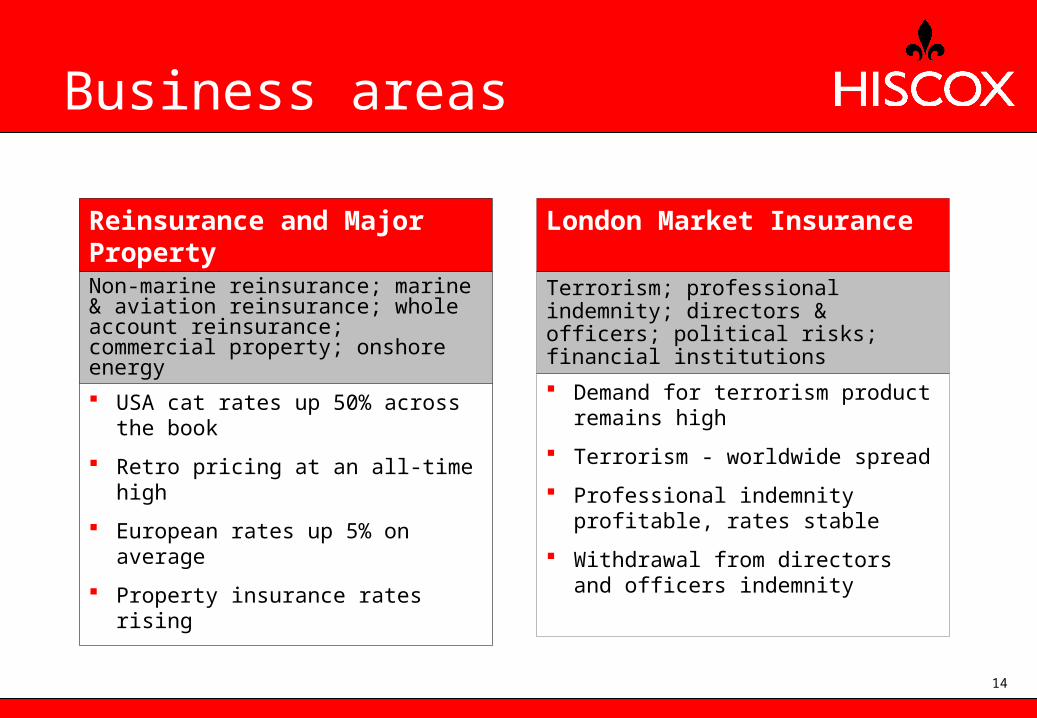

Business areas

Reinsurance and Major PropertyNon-marine reinsurance; marine & aviation reinsurance; whole account reinsurance; commercial property; onshore energy

USA cat rates up 50% across the book

Retro pricing at an all-time high

European rates up 5% on average

Property insurance rates rising

London Market Insurance

Terrorism; professional indemnity; directors & officers; political risks; financial institutions

Demand for terrorism product remains high

Terrorism - worldwide spread

Professional indemnity profitable, rates stable

Withdrawal from directors and officers indemnity

14

Business areas

Specialty

Kidnap & ransom; contingency; MGAs; homeowners; SMEs; bloodstock; personal accident

Profitable despite hurricane activity

Stable rating environment on non-catastrophe exposed business

Catastrophe exposed risks rates up – between 25% and 100%

Increased catastrophe deductible

Technology, Media, Telecoms

Technology, media, telecoms errors & omissions

Risk management and claims service remains highly valued

Continued expansion into Europe

San Francisco office now open

15

Marine and Energy

Marine hull; cargo; offshore energy; marine & energy liability;

Offshore energy rates up strongly, especially Gulf of Mexico

Offshore energy coverage reduced and more restrictive

Quota share for Gulf of Mexico

Liability and hull rates increasing

Expanding business reach

Representation in New York, San Francisco and Paris

E-commerce initiatives. Homeowners generated c.US$600K in January, increasing significantly month on month

Leading peer to peer trading

16

The opportunity

Hardening catastrophe market

Changes to reduce volatility

– Quota share reinsurance

– Reduction in property aggregate and line size

– Marine reinsurance book re-focused

Strong underlying specialty book

Established name, experienced team

17

Hiscox UK & Hiscox Europe

18

Hiscox Insurance Company

19

Gross Written Premium: £m Combined Ratio: %

0

20

40

60

80

100

120

1997 1998 1999 2000 2001 2002 2003 2004 2005

93.697.897.7

102.6107.9

118.0

0

50

100

150

200

250

1997 1998 1999 2000 2001 2002 2003 2004 2005

218.7

163.9

127.3

97.890.0

74.7

176.497.9

231.3

92.6

Core Non-Core

232.8

88.5

212.1

17.5

96.8%

170.0

55.7

1.4

103.2%

42.4

Performance

2005 (£m) 2004 (£m)

UK UK Europe

GWP 207.3

Profit before tax 40.4

Combined Ratio 84.1%

Net Premiums Earned 194.5

Europe

55.0

3.0

99.7%

47.1

20

Ro

llin

g 1

2 M

on

th I

nd

ex o

f R

ates

Rates

21

UK Personal Lines UK PI France Germany

80%

90%

100%

110%

120%

130%

140%

150%

160%Ju

l-00

to

Ju

n-0

1

Jan-

01

t0

De

c-01

Jul-0

1 t

o J

un

-02

Jan-

02

to

De

c-02

Jul-0

2 t

o J

un

-03

Jan-

03

to

De

c-03

Jul-0

3 t

o J

un

-04

Jan-

04

to

De

c-04

Jul-0

4 t

o J

un

-05

Jan-

05

to

De

c-05

Hiscox UK

Art and Private Client

High value household and contents; fine art; classic cars; specie; executive household

Successful launch of broker e-trading

Purchase of $8m of fine art renewal rights from AIG

UK Household products rated market leader by Defaqto

Strong growth in Direct

Professions & Specialty CommercialProfessional indemnity; directors & officers; commercial office; internet & email

Successful launch of broker e-trading

Strong underwriting growth/discipline

Cross-selling success

Launch of Direct Commercial

22

Europe

23

Art and Private Client

High value household and contents; fine art; classic cars; specie; executive household

Stable rating environment

Strong fine art growth following new product introduction in Nov 2004

Record combined ratio

Professions & Specialty Commercial

Professional indemnity; directors & officers; commercial office; internet & email

France: core professional indemnity launched

Germany: exited unprofitable partnerships

Holland: professional indemnity team in place

2006: Accelerated marketing

Build Hiscox as a consumer brand

Accelerate growth across direct and broker channelsObjective

A-B households

TV debut (May)

Invest behind proven growth drivers (digital, direct mail, press advertising)

Contemporary arts sponsorship

Target Market

Plans

24

UK HNW opportunity is enormous

2.8 million HNW households in UK

16% of UK total

39% of all sums insured

Highly fragmented

25Source: Hiscox, Datamonitor, ABI

UK Contents >£75K

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

£75K £1m+Contents Sums Insured

Po

lic

y V

olu

me

Hiscox International

26

37.3

2.9

92.0%

18.5

Performance

2005 (£m) 2004 (£m)

GWP

Profit before tax

Combined Ratio

Net Premiums Earned

27

43.7

6.2

91.3%

23.4

Guernsey

International: fine art; kidnap & ransom; personal accident

Stable rating environment

Record profitability for Guernsey operation in 2005

Staffing levels increased for 2006 to promote growth

Business areas

USA

Professional indemnity; fine art; terrorism

Ed Donnelly – experienced local as President

Recruited underwriting staff

13 March 2006 start

Est. US$15m first year

28

Bermuda

International: reinsurance; internal quota shares

Underwriting, pricing and modelling staff in place

Back office staff recruited

International reinsurance rates stable

USA rates continue to rise

2006 Bermuda business plan

Expected 2006 business mix100% = US$325m

27%

8%

Reinsurance

Kidnap & Ransom and Fine Art

UK

Syndicate 33 Q.S.

USA

52%8%

5%

External Internal

29

Already performing

Committed to a total of US$155m of business

– At 1 March 2006 48% of our budget

US$46m is new reinsurance business

– At 1 March 2006 26% of our budget

On target to meet business plan

30

Summary and outlook

31

Summary

Satisfying results

– Good profits

– Growth in net asset value per share

– Dividend growth

Disciplined underwriting

Distribution extended

– Hiscox Global Markets

– Hiscox Bermuda

– Hiscox USA32

Clear strategic focus

Build distribution to access new markets

Grow regional to balance London Market volatility

Retain specialist focus

33

100% = £1,105mTotal group controlled income for 2005

London Market Regional

Syndicate 33 & Hiscox Bermuda

Syndicate 33, Hiscox Insurance Company,

Hiscox Guernsey & Hiscox USA

TMT

Art & PrivateClient

London Market

Reinsurance & Major Property

Specialty

Professions & Specialty Commercial

29%

27%

15%9%

15%5%

Clear geographic and product focus

Hiscox plc

Hiscox Global Markets

Reinsurance & Major Property

London Market Marine & Energy Specialty Technology & Media

Hiscox Bermuda

Hiscox Guernsey

Hiscox USA

Reinsurance Group Capital

Support

Art & Private Client

Kidnap & Ransom

Art & Private Client

PI & Specialty Commercial

Regional Media & Technology

Hiscox International

Hiscox UK

Hiscox Europe

Art & Private Client

PI & Specialty Commercial

Regional Media & Technology

Art & Private Client

PI & Specialty Commercial

Regional Media & Technology

Direct

Hiscox UK & Europe

34

Outlook

Attractive rating environment

Strategy of balance will continue

– Regional business in UK, Europe, USA and Guernsey

– Global business in London and Bermuda

Seasoned leaders and staff in place

35

Appendices

36

Realistic disaster scenarios

Geographical & currency split

Loss ratios as a % of Syndicate premiums

Syndicate 33 capacity and Hiscox plc ownership

Reinsurance

Company background

Glossary of terms

Realistic disaster scenarios

37

Syndicate 33 - Losses shown as a percentage of 2006 capacity

0

5

10

15

20

25

30

35

CaliforniaEarthquake

FloridaWindstorm

SpecificEuropean

Windstorm

SpecificJapanese

Earthquake

Specific NewMadrid

Earthquake

Gulf ofMexico

Windstorm

Loss %Gross Loss

Net Loss

Industry Loss

Return Period

US$80Bn

1 in 200 yr

US$30Bn

1 in 500 yr

US$50Bn

1 in 500 yr

US$40Bn

1 in 500 yr

US$54Bn

1 in 250 yr

US$60Bn

1 in 250 yr

Geographical & currency split

38

CAD

USD

EURGBP

13.2%

55.9%

28.4%

2.5%

2006 Geographical split 2006 Currency split

North AmericaUK

1.2%Oceania

0.2%Northern Africa

0.4%South America

0.6%Middle East

1.1% East Asia

0.2%Central Asia

Western Europe (excl. UK)

0.2%South Asia

0.5%Central America

0.7%Central &

Southern Africa

0.5%Central &

Eastern Europe

0.9%Caribbean

23%

Worldwide

34.6%23%

9.4%26.5%

Loss ratios as a % of Syndicate premiums

39

GILR NILR

YOA 2002 2003 2004 2005 2002 2003 2004 2005

12 mths 13.4% 11.6% 30.0% 84.3% 20.0% 14.1% 30.8% 63.3%

24 mths 27.9% 30.0% 59.3% 36.6% 35.3% 59.0%

36 mths 37.2% 39.9% 45.3% 47.6%

48 mths 41.7% 44.9%

Syndicate 33 incurred losses as a percentage of signed premium

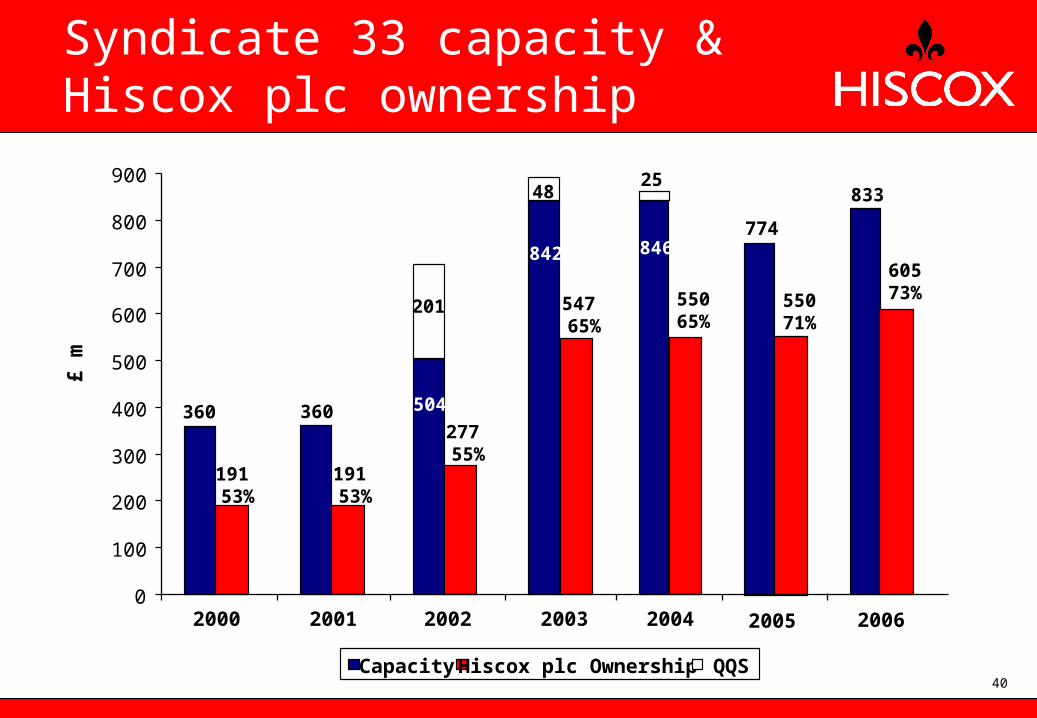

Syndicate 33 capacity & Hiscox plc ownership

40

0

100

200

300

400

500

600

700

800

900

2000 2001 2002 2003 2004

Capacity Hiscox plc Ownership QQS

£ m

2005

360

191 53%

360

191 53%

504

277 55%

201

842

547 65%

48

846

55065%

25

55071%

774

2006

60573%

833

Group reinsurance security

41

AAA6%

AA26%

A57%

Other 11%

2006 Programme

A

56%

AAA

AA40%

4%

Receivables at 31/12/05 of £467.8m

Reinsurance

42

0

5

10

15

20

25

30

35

40

2000 2001 2002 2003 2004 2005

35.3%

27.3% 26.0%

17.3%

13.7%

Reinsurance as a % of GWP (ex. QQS)

Reinsurance receivables as a % of total assets

0

5

10

15

20

25

30

2000 2001 2002 2003 2004 2005

18.2%

26.9%

15.4%

11.8% 10.8%

%%20.9% 17.0%

Regional Syndicate 33

Regional Hiscox Insurance Company

43

Building a balanced business

0

200

400

600

800

1000

1200

19

88

*

19

89

*

19

90

*

19

91

*

19

92

*

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

Gro

ss W

ritt

en P

rem

ium

* London Market/Regional split estimated for these years

London MarketSyndicate 33

Glossary of terms

44

Annual Venture The system used for running a Lloyd’s syndicate under which each “year of account” is treated separately. Members own capacity on a syndicate for a “year of account” and the results are declared when the year is closed by the RITC mechanism, usually after three years.

Claims ratio Net claims incurred, including IBNR, as a percentage of net earned premiums.

Combined ratio The total of the claims and expenses ratios.

Equalisation provision This a provision made to cover future catastrophe losses and is calculated in accordance with a set sector formula, which has the effect of smoothing the profit cycle.

Expenses ratio Expenses as a percentage of net written premiums.

Funds at Lloyd’s The amount of assets, which can be cash, investments or letters of credit, that a syndicate member has to deposit with Lloyd’s to support his share of the capacity on a syndicate. The minimum amount is 40% of the capacity owned by the member.

Gross written premium Premiums contracted for before any deductions.

Group controlled The total gross written premium controlled by the group including the 35% of the syndicate capacity not owned by Hiscox in 2004 (29% in 2005).

IBNR Incurred but not reported. An estimate made at the end of each accounting period to cover the expected cost of losses that have occurred but have not yet been reported to the insurer or reinsurer.

Incurred loss ratio Paid and outstanding losses as a percentage of premiums. Gross incurred loss ratio is before deducting any reinsurance and net is after deducting reinsurance.

gross written premium

Glossary of terms

45

Long-tail A term used to describe an insurance risk that has the potential for claims development or new claims to be reported a number of years after expiry of the term of the policy.

Member or Name The companies or individuals who own the capacity of a syndicate and who belong to the membership of the Society of Lloyd’s.

Net premiums earned Premiums received after the cost of reinsurance and adjustment for unearned premium. Unearned premium covers the future period of risk of an insurance policy.

Net premiums written Premiums contracted for after deduction of reinsurance.

Open year A Year of Account of a syndicate which has not been closed by Reinsurance To Close (RITC). RITC usually occurs at the end of the third year. A Year of Account can be left open beyond the third year if the extent of the future liability cannot be accurately quantified.

Qualifying quota share These are quota share reinsurance policies, which Lloyd’s allow in certain circumstances, that enable a syndicate to write gross premium in excess of its capacity.

Reinsurance to close – RITC The reinsurance to close comprises a premium payable by the closing year to the members on the next open year of account and a contract which transfers the liability for all claims in respect of the closing year to the next open year.

Run-off account At Lloyd’s, a year of account which is kept open after the date on which it would normally have been closed.

Subrogation The right of the underwriter to “stand in the shoes of the insured” and take over the Insured's rights, following payment of a claim, to recover the payment of an incurred loss from a third party responsible for the loss. It is limited to the amount of loss paid by the insurance policy.

Syndicate Capacity Also referred to as the ‘stamp’. The maximum amount of business that a syndicate in Lloyd’s can write per year, aggregated from all its members.

reinsurance