highlighting a few key ideas and issues. m&m: equity = debt value of firm projects matters a...

TRANSCRIPT

Highlighting a Few Key Ideas and Issues

M&M: Equity = Debt

Value of firm projects matters a lot more than small differences in costs of funds

Breaks down at high debt/income ratios

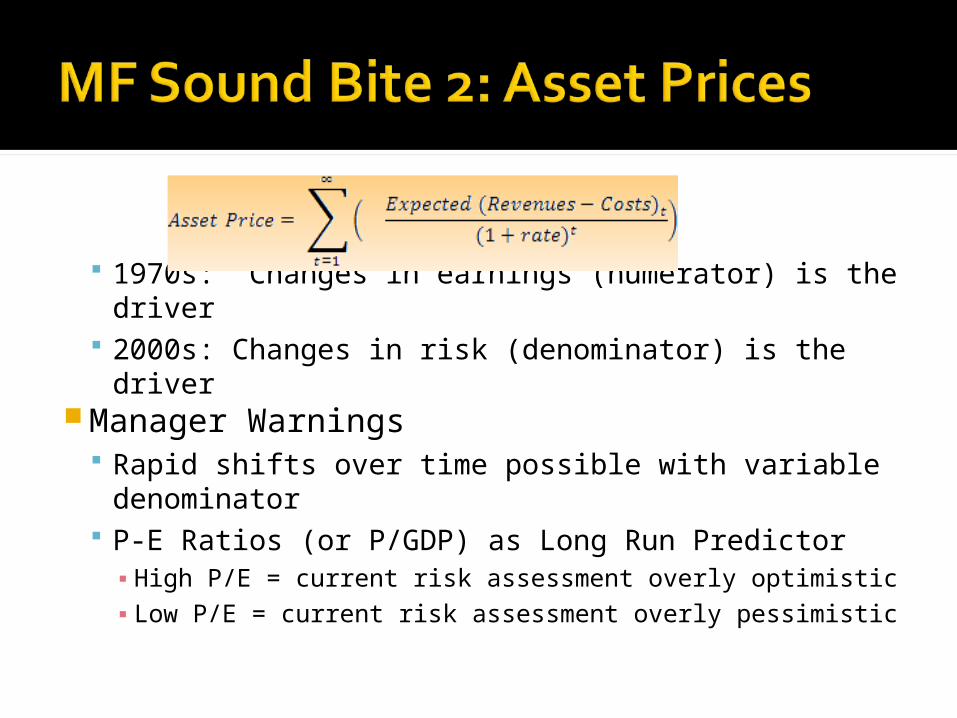

1970s: Changes in earnings (numerator) is the driver

2000s: Changes in risk (denominator) is the driver

Manager Warnings Rapid shifts over time possible with variable

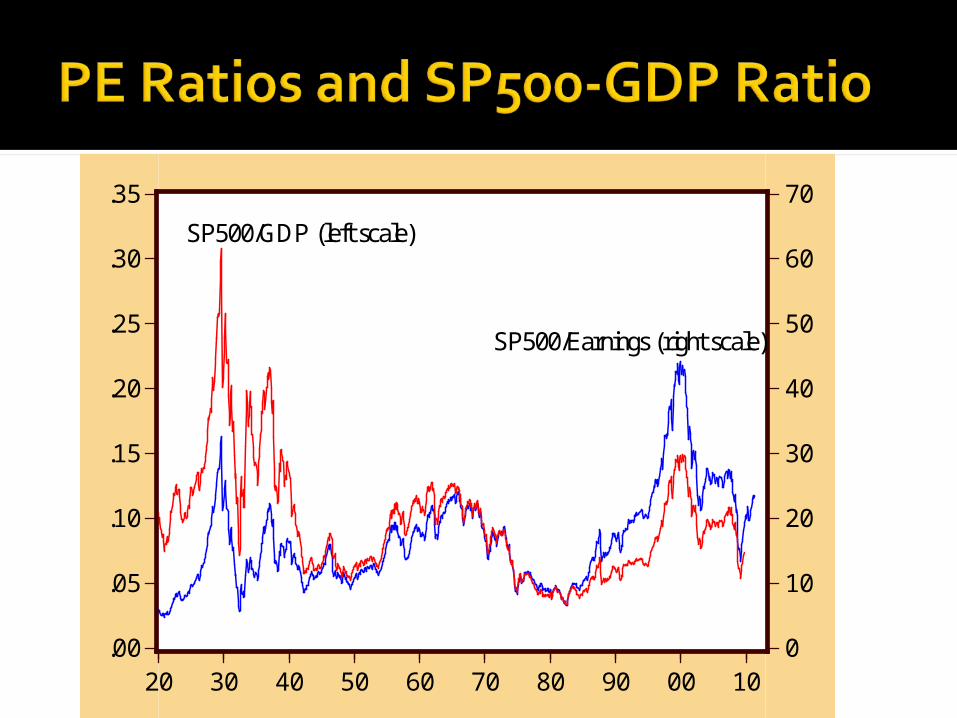

denominator P-E Ratios (or P/GDP) as Long Run Predictor

▪ High P/E = current risk assessment overly optimistic▪ Low P/E = current risk assessment overly pessimistic

.00

.05

.10

.15

.20

.25

.30

.35

0

10

20

30

40

50

60

70

20 30 40 50 60 70 80 90 00 10

SP500/GDP (left scale)

SP500/Earnings (right scale)

Fed & Rates: Taylor RuleTarget Rate = 2 + 0.5*(Actual Inflation – Target Inflation)

+ 0.5*(Actual GDP – Potential GDP)

Markets & Rates: Fisher EquationObserved Rates = Real Rates + Expected Inflation

▪ Real Rates influenced by economic growth (higher when growth higher)▪ Estimate of Real Rate: TIPS (See Bloomberg Rates)

▪ Expected inflation influenced by Fed actions and velocity of money

Policy Limits: No interest rate “knob” for Fed; influences with money creation “Insurance” for system-wide panics

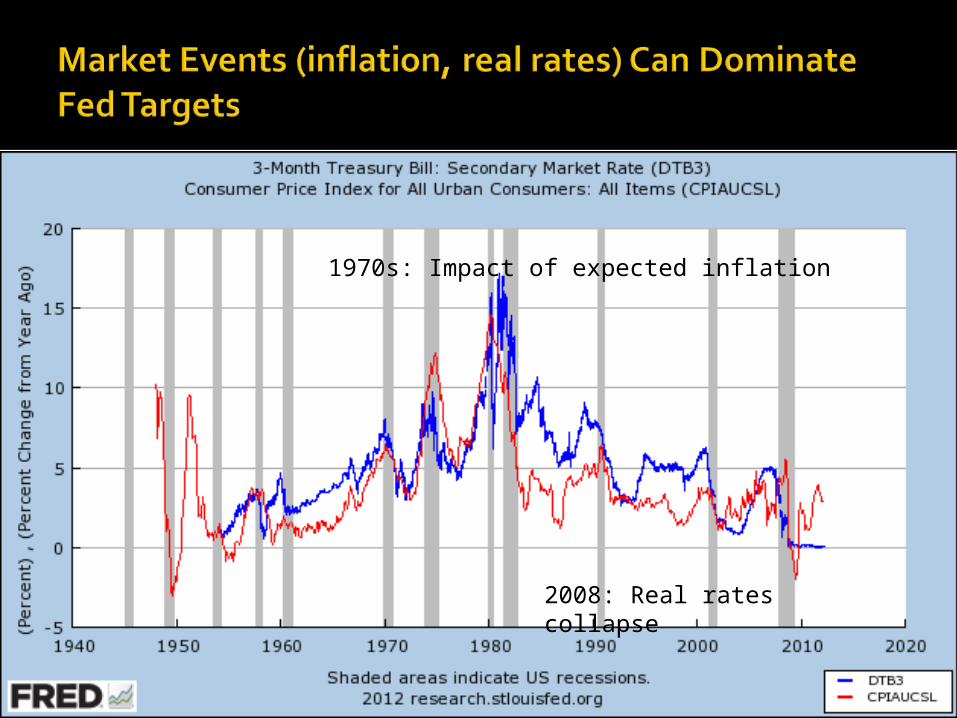

1970s: Impact of expected inflation

2008: Real rates collapse

Responses: Limit new projects; Put off new hires; Pull back credit …

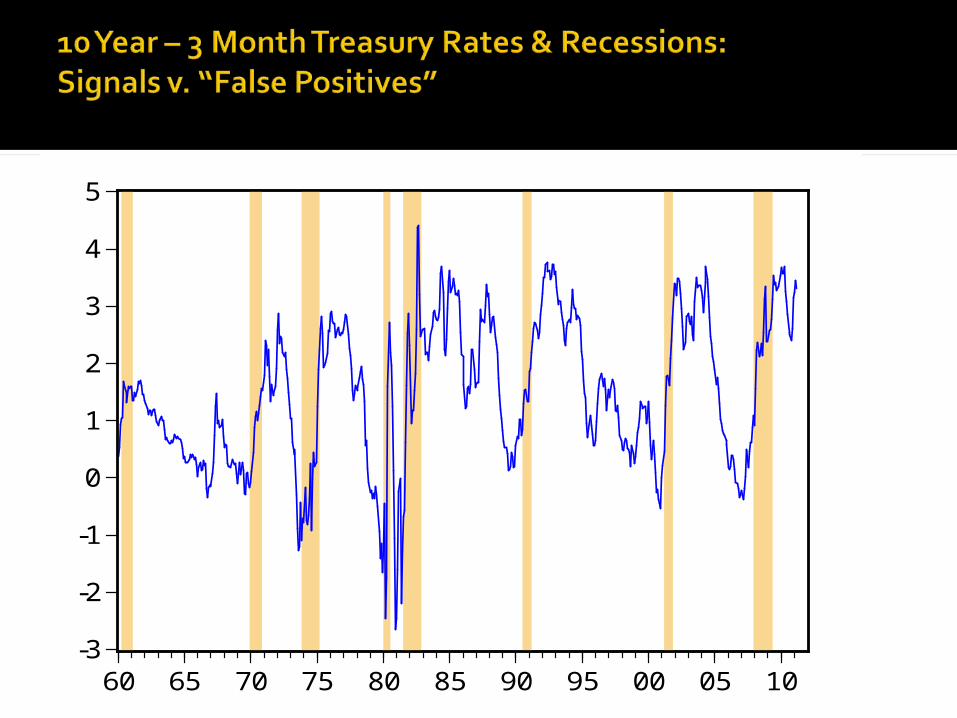

The Treasury Yield Curve: Steep: High growth or inflation expected Flat/Inverted: Low growth or inflation

expected

US Treasury Site

"Living Yield Curve"

-3

-2

-1

0

1

2

3

4

5

60 65 70 75 80 85 90 95 00 05 10

Response: Limit risk; increase liquidity; cash in fixed price assets; no new projects; secure longer term deals; …

-1

0

1

2

3

4

5

6

2006 2007 2008 2009

KC-FSILIBOR-Tbill

Fannie-Freddie

BearStearns

Lehman-AIG

-1

0

1

2

3

4

90 92 94 96 98 00 02 04 06 08 10

Kuwati Invasion

Asian Debt

07-08

Nominal 10-

Inflation Indexed Rate

Nominal Rate

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

60

70

80

90

100

110

120

130

90 92 94 96 98 00 02 04 06 08 10

$ per AU$FX per US$

Cheap Credit Public Sector Backing (Fannie, Freddie,

Homeownership) High Leverage (Assets/Equity) for Investment

Banks (Bear, Lehman, Merrill …) + AIG Banks Lending on 25 years of

growth/repayment Foreign Investment in US

NOTARIETY BUT TOO SMALL ▪ Securitization (Collateralized Debt: CDOs)▪ Derivatives (Credit Default Swaps)▪ Market-to-Market Accounting

Mortgage-related securities marked-to-market daily Immediately begin to reflect deteriorating

conditions in 2007 Commercial loans on bank books valued by banks

at their PV of expected cash flow Widespread writing down of these loans doesn’t

begin until 2009, giving appearance that mortgage market problems causing these problems

Problems already developing coincidental with mortgage problems in 2007-08