high-level meeting of regional associations of … · powers of cre. constitutional existence and...

TRANSCRIPT

Guillermo Zúñiga Martínez

Commissioner

Regulatory Commission of Energy

July 11th , 2017

Budapest, Hungary.

Opinions are sole responsibility of the speaker, only for informative matters, and by no means express an official position with respect to the subjects to be discussed within the scope of the Regulatory Energy Commission.

“The new framework for distributed generation in Mexico”

5th High-Level Meeting of Regional Associations

of Emerging Markets

The special report of the International Energy Agency, "Mexico Energy Outlook", compares the estimated benefits of the Energy

Reform to 2040, with a scenario without reform

Oil production would be about 1 mb/d lower than in the “With Reform” scenario;

Electricity rates for industrial consumers would be 14% higher by 2040;

The cost of generating and delivering electricity to the residential sector would be 16% higher; The additional cumulative subsidy would be USD 50 billion;

Economy of Mexico would be 4% lower.

Oil and gas production will increase and imports of petroleum products will decline;

Lower electricity rates for industrial consumers;

Subsidies will be phased out by 2035;

The economy of Mexico will double, be more efficient and its energy intensity will improve;

Mexico would not meet its clean energy objectives and its objectives for reducing GHG emissions;

Mexico will achieve its 35% clean energy generation objective by 2024 and reduce its GHG emissions;

Energy efficiency standards will significantly reduce Mexico's energy consumption.

With Reform Constitutional

× Without Reform Constitutional

Source: https://www.iea.org/publications/freepublications/publication/MexicoEnergyOutlook.pdf

CRE’s nature and

powers

The energy reform deeply modified the nature and powers of CRE.

Constitutional existence and powers;

7-years staggered appointments;

Independence from central government

Budgetary autonomy;

Subject to rigorous contact rules;

Acts subject to maximum transparency;

Board of directors: 7 Commissioners, appointed by the President and confirmed by

the Senate.

7 Commissioners Immovables through their

periods

CRE’s new features

Hyd

rocarb

on

s

Ele

ctr

icit

y

Exploration/

Extraction Refining/

Processing

Transportation Storage Distribution Commercialization

and retail Transportation

Generation ISO

Transmission Distribution

Supply and

commercialization

ISO

5

The reform allows to carry out new activities by the private sector, through different schemes…

1st auction: USD 2.6 billions

auction : USD 4 billions

Generation: USD 98.7 billions

Transmisión: USD 15.3 billions

Distribución: USD 17.7 billions*

Round 1:

1st bidding round: USD 2.7 billions

2nd bidding round: USD 3.1 billions

3rd bidding round : USD 1.1 billions

4th bidding round : USD 34.4 billions

Trión: 11.0 billions

Round 2:

1st bidding round: USD 8.2 billions

2nd bidding round: USD 5.0 billions

3rd bidding round: USD 1.0 billions

Sísmic: USD 2.5 billions

NG Pipelines: USD 16 billions

Fuels pipelines: USD 16 billions

• Transportation & Storage: USD 4.0 billions

• Distribución y Expendio: USD 12.0 billions

Exploration and Extraction:

Round 1&2 Natural Gas and Fuels

Electricity

* Estimated investment by Prodesen 2016- 2030. Source: Secretaría de Energía

A total of 88 companies –from 19 different countries- have been

awarded with contracts for the development of hydrocarbons and

electricity projects.

…resulting in important investments in every activity in the energy sector.

Inversión comprometida:

U70 mil millones de dólares

Estimated investment:

USD 239 billions Value of auctions/contracts entered into :

USD 78.2 billions

Renewables & Distributed

Generation

The trend of global investment is towards renewable energies

Global investment by energy source in 2016

68%

32%

Renewables Conventional Energy

Source: World Energy Outlook 2016

At a global level, renewables will become the most important fuels in the period 2015-2040.

MTOE: Million Tonnes of Oil Equivalent

Where is the investment growth taking place in LatAm?

Source: Latin America Energy Review

Wind & solar energy investments in Mexico will represent 40% and 57% of the total invested in the region

for the 2017-2020 period, respectively.

Source: Sener

Combined Cycle 50%

Conventional Thermal

[PORCENTAJE]

Coal-fired 11%

Turbo Gas 4%

Renewables 23%

Combined Cycle 36%

Coal-fired 2%

Renewables 62%

2015 2030

An important increase in the use of renewables for the period 2015-2030, will be held in Mexico.

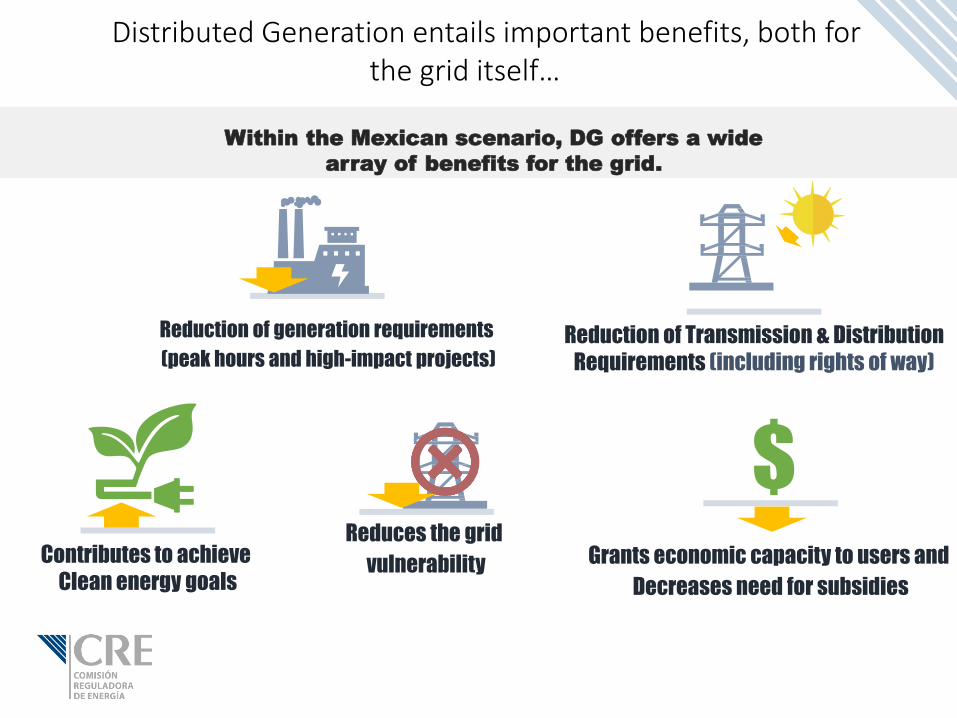

Distributed Generation entails important benefits, both for the grid itself…

Reduction of Transmission & Distribution

Requirements (including rights of way)

Grants economic capacity to users and

Decreases need for subsidies

Reduction of generation requirements

(peak hours and high-impact projects)

Contributes to achieve

Clean energy goals

Reduces the grid

vulnerability

Within the Mexican scenario, DG offers a wide

array of benefits for the grid.

…as well as for those subjects who are directly benefited from carrying out this activity.

Small

generators will

be able to

interconnect

their power

plants to the distribution grid

Regulatory

simplification

Simple and

straigthforward

contracts

Reduction of

response

terms

(Maximum

term of 18

days)

Technical and

administrative

guidelines in

favor to the

user

New

compensation

models (Net-

metering, Net

billing and Total Sale )

DG benefits for the users that invest in DG

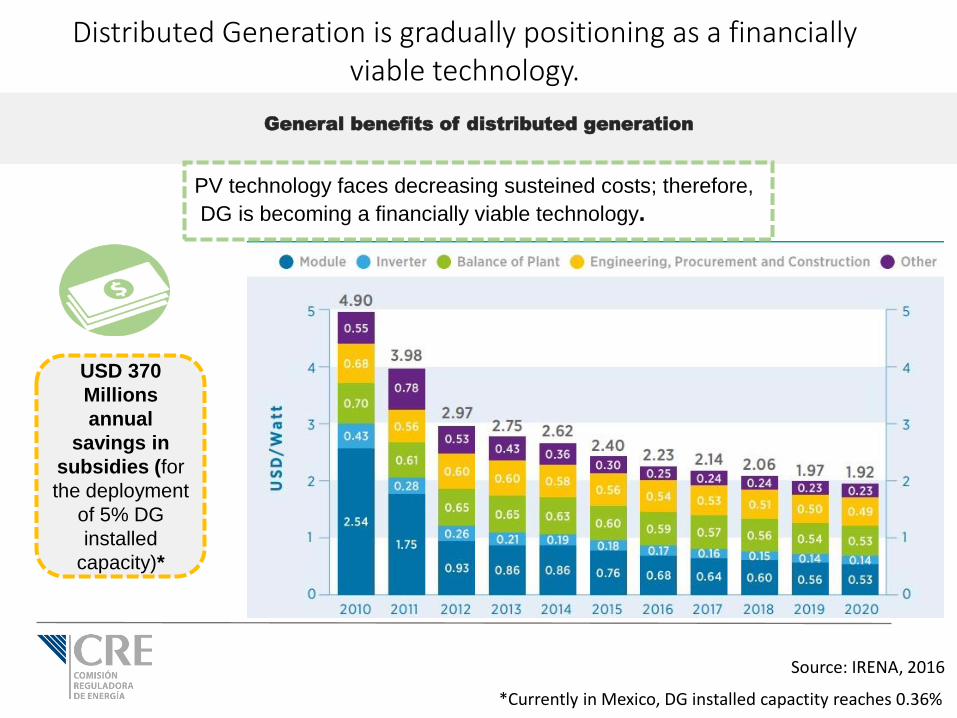

18

USD 370

Millions

annual

savings in

subsidies (for

the deployment

of 5% DG

installed

capacity)*

Distributed Generation is gradually positioning as a financially viable technology.

Source: IRENA, 2016

*Currently in Mexico, DG installed capactity reaches 0.36%

General benefits of distributed generation

PV technology faces decreasing susteined costs; therefore,

DG is becoming a financially viable technology.

The potential of distributed generation in Mexico is important, due to the geographic and climatological conditions of the country.

Average daily solar radiation in Mexico

5.5 kWh/m2

per day

Annual average

irradiation

GD Installed

capacity

GD Installed

capacity

247 MW 7,200 MW

Evolution of solar panel costs (1977-2013)

Fuen

te: C

lean

tech

nic

a

6 kWh/m2

per day

Annual average

irradiation

The development of small-scale photovoltaic installations is increasing...

Own elaboration with data provided by the CFE. * Cut-off date as of December 31, 2016

0.003 0.021 0.121 0.667 3.8 10.2 14.2

32.7

55.6

130

0.024 0.145 0.812 4.6 14.8

29.1 61.8

117.5

247.6

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Installed capacity (MW)

Capacidad instalada (Anual)

Capacidad Instalada (Acumulado)

70% 134%

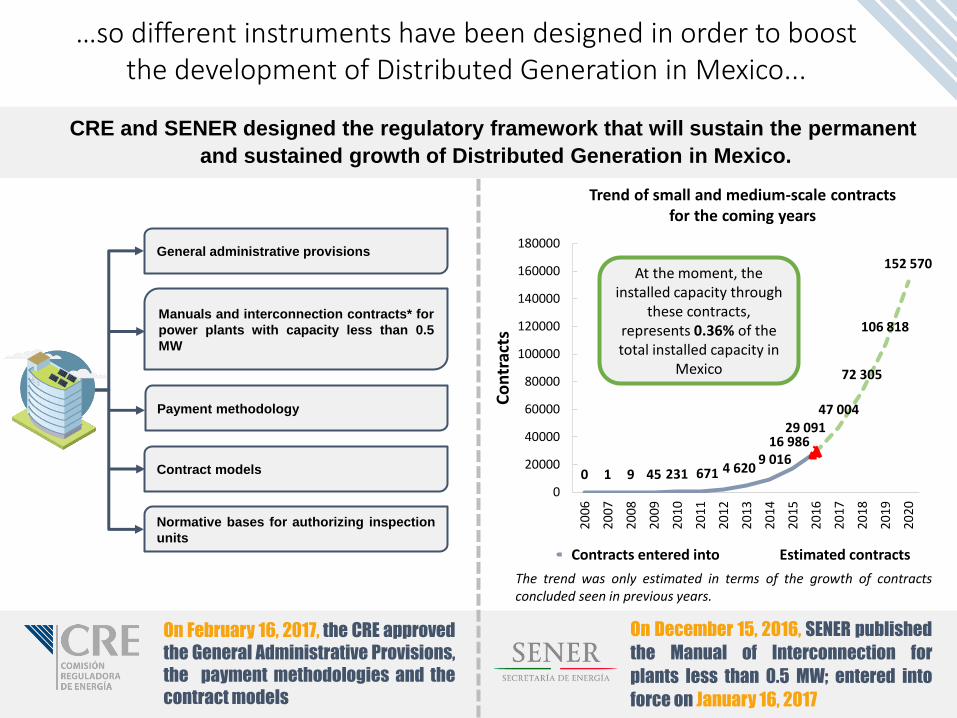

General administrative provisions

Normative bases for authorizing inspection

units

Manuals and interconnection contracts* for

power plants with capacity less than 0.5

MW

Payment methodology

Contract models 0 1 9 45 231 671 4 620 9 016

16 986 29 091

47 004

72 305

106 818

152 570

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

Co

ntr

acts

Celebrated contracts Estimated contracts

…so different instruments have been designed in order to boost the development of Distributed Generation in Mexico...

CRE and SENER designed the regulatory framework that will sustain the permanent

and sustained growth of Distributed Generation in Mexico.

Trend of small and medium-scale contracts for the coming years

On February 16, 2017, the CRE approved

the General Administrative Provisions,

the payment methodologies and the

contract models

On December 15, 2016, SENER published

the Manual of Interconnection for

plants less than 0.5 MW; entered into

force on January 16, 2017

The trend was only estimated in terms of the growth of contracts concluded seen in previous years.

Contracts entered into Estimated contracts

At the moment, the installed capacity through

these contracts, represents 0.36% of the total installed capacity in

Mexico

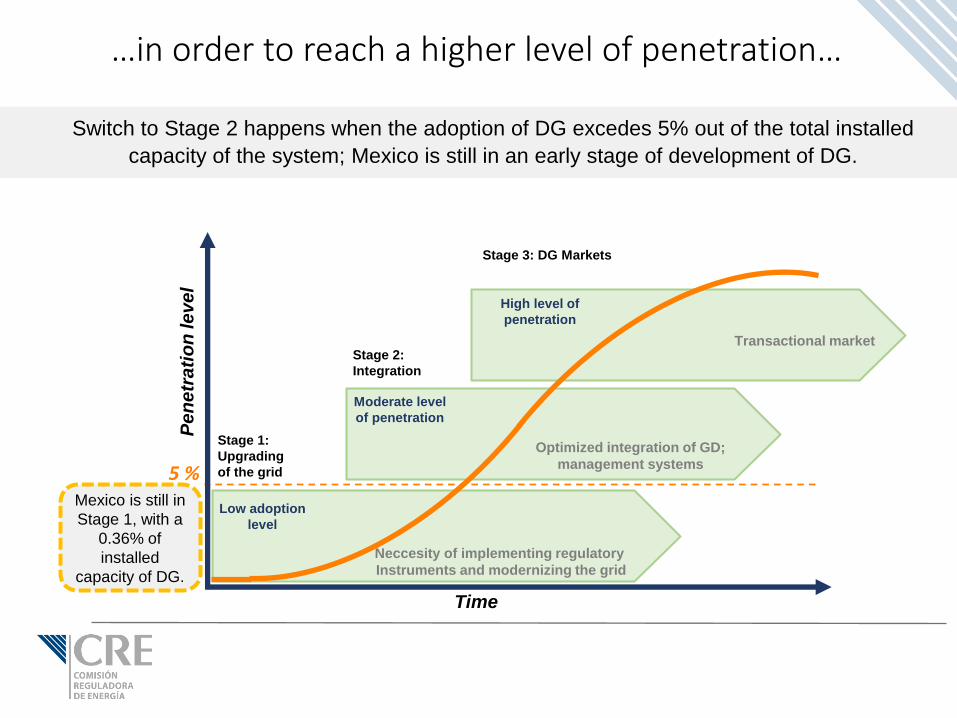

Stage 1:

Upgrading

of the grid

Stage 2:

Integration

Stage 3: DG Markets

Low adoption

level

Moderate level

of penetration

High level of

penetration

Neccesity of implementing regulatory

Instruments and modernizing the grid

Optimized integration of GD;

management systems

Transactional market

Time

Pe

ne

tra

tio

n le

ve

l

5 %

…in order to reach a higher level of penetration…

Mexico is still in

Stage 1, with a

0.36% of

installed

capacity of DG.

Switch to Stage 2 happens when the adoption of DG excedes 5% out of the total installed

capacity of the system; Mexico is still in an early stage of development of DG.

…by establishing more and better payment schemes, among other instruments.

Bi-directional meter

Excess energy

accumulates in favor of

the generator

Missing energy is

compensated with

accumulated energy

Exchange

In case of exhausting the

credit in favor is charged at

the applicable rate

Alternatively to Net Metering, the user can choose between the following schemes:

Net Metering

Energy delivered to the General Distribution Network

Energy delivered by the Basic Supplier

Net Billing

Energy delivered to the General Distribution Network

Total sale of electric energy

SSB

RGD

SSB

RGD

SSB

RGD

5.3 millions per year

(84.6% of the requested)

First Long term

aucion

$14.6 USD per CEL

Weighted price (aprox.) Second Long term

auction

9.3 millions per year

(87.3% of the requested)

$14.3 USD per CEL

Weighted price (aprox.)

Legacy Power Plants that generate electricity from Clean Energies

operating before August 11, 2014, as long as they have carried out a project

to increase their production of Clean Energy.

Clean Power Plants that have capacity that has been excluded from a

Legacy Interconnection contract in order to be included in an

Interconnection Contract in the terms of the Law.

Clean Power Plants operating after August 11th, 2014.

Who has the right to receive CEL?

...which generate incentives to all participants of the electric industry.

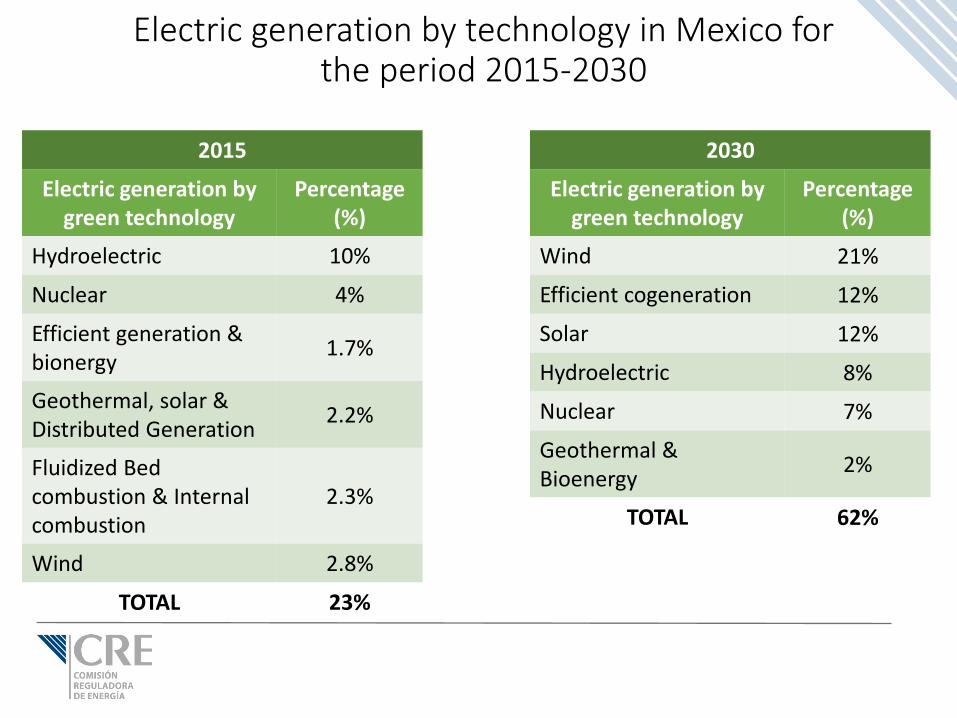

2015

Electric generation by green technology

Percentage (%)

Hydroelectric 10%

Nuclear 4%

Efficient generation & bionergy

1.7%

Geothermal, solar & Distributed Generation

2.2%

Fluidized Bed combustion & Internal combustion

2.3%

Wind 2.8%

TOTAL 23%

Electric generation by technology in Mexico for the period 2015-2030

2030

Electric generation by green technology

Percentage (%)

Wind 21%

Efficient cogeneration 12%

Solar 12%

Hydroelectric 8%

Nuclear 7%

Geothermal & Bioenergy

2%

TOTAL 62%

…which will generate better conditions to develop this activity, than those prevailing prior to the Reform.

Consideration

GD 2.0 GD 1.0

Small scale< 1 kV

Residential up to 10 kW

Commercial up to 30 kW

Medium scale< 69 kV

General in mid-voltage

< 500 kW

Small scale from 1 kV

Up to 50 kW

Medium scale from 34.5 kV

< 500 kW

Storage is allowed

Interconnection

Simplified contracts

Interconnection

Compensation

Net Metering

Excess energy is accumulated for the

following billing periods

Accumulation for 12 months

No possibility of selling excess energy

after 12 months.

Generation

capacity

Contracts

Interconnection

Net Metering Excess energy is accumulated for the following

billing periods; after 12 months, excess energy is

sold at the average LMP

Net Billing

Total sale

Typical model

Typical models which simplify interconnecion

and allow several commercial activities for

different users profiles

Obligation for the distribuitor to allow

interconnection.