hierarchy of plans and linkages participatory budgeting

TRANSCRIPT

Hierarchy of Plans and Linkages

Participatory Budgeting

Policy-Based Budgeting

Performance Informed Budgeting (PIB)

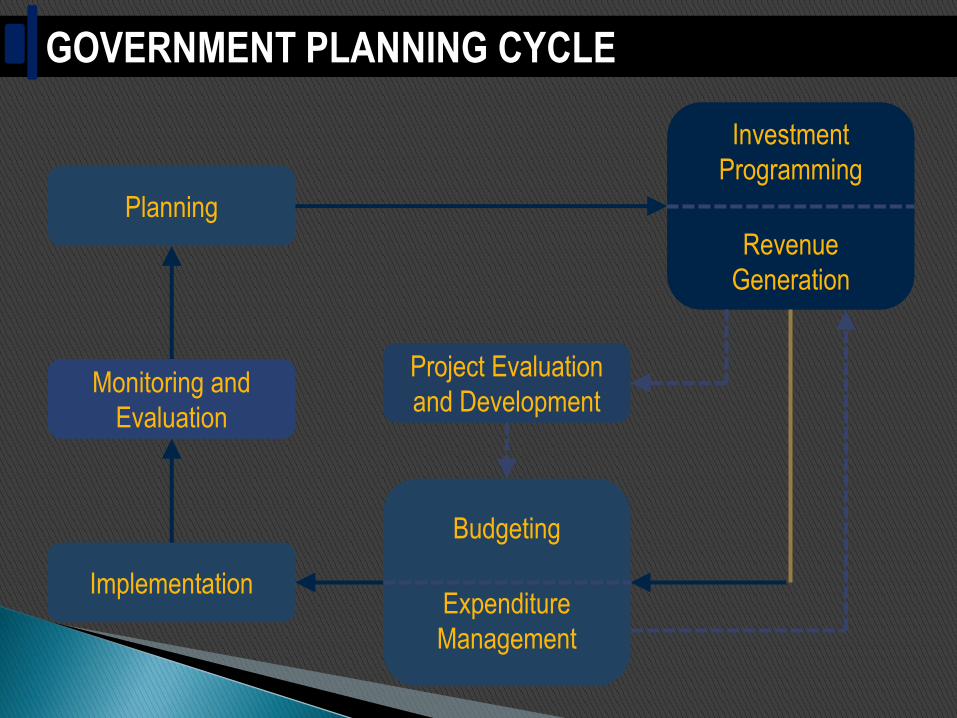

GOVERNMENT PLANNING CYCLE

Planning

Monitoring and

Evaluation

Implementation

Project Evaluation

and Development

Budgeting

Expenditure

Management

Investment

Programming

Revenue

Generation

VERTICAL & HORIZONTAL LINKAGES:HIERARCHY OF PLANS

Level/Political Unit

(Coordinating Entity)

Physical and Land

Use PlanDevelopment Plan Investment Program

NATIONAL(NEDA Board

NEDA Central Office)

REGIONAL(RDC/NEDA Regional Office)

PROVINCIAL(PDC/PPDO)

MUNICIPAL/CITY(M/CDCM/CPDO)

National

Physical Framework

Plan (NPFP)

Philippine Investment

Program (PIP)

Regional Development

Plan (RDP)

BARANGAY(BDC/Barangay Officials)

Regional Physical

Framework Plan

(RPFP)

Annual Investment

Program (AIP)

Regional Development

Investment Program

(RDIP)

Ex. Sketch Map of the

Barangay

Comprehensive Land

Use Plan (CLUP)

Provincial Development and

Physical Framework Plan (PDPFP)

Comprehensive

Development Plan

Municipal/City

Development Investment

Program (M/CDIP)

Provincial Development

Investment Program

(PDIP)

Regional Development

Investment Program

(RDIP)

Philippine

Development Plan

(PDP)

Regional Development

Plan (RDP)

Barangay Development

Plan

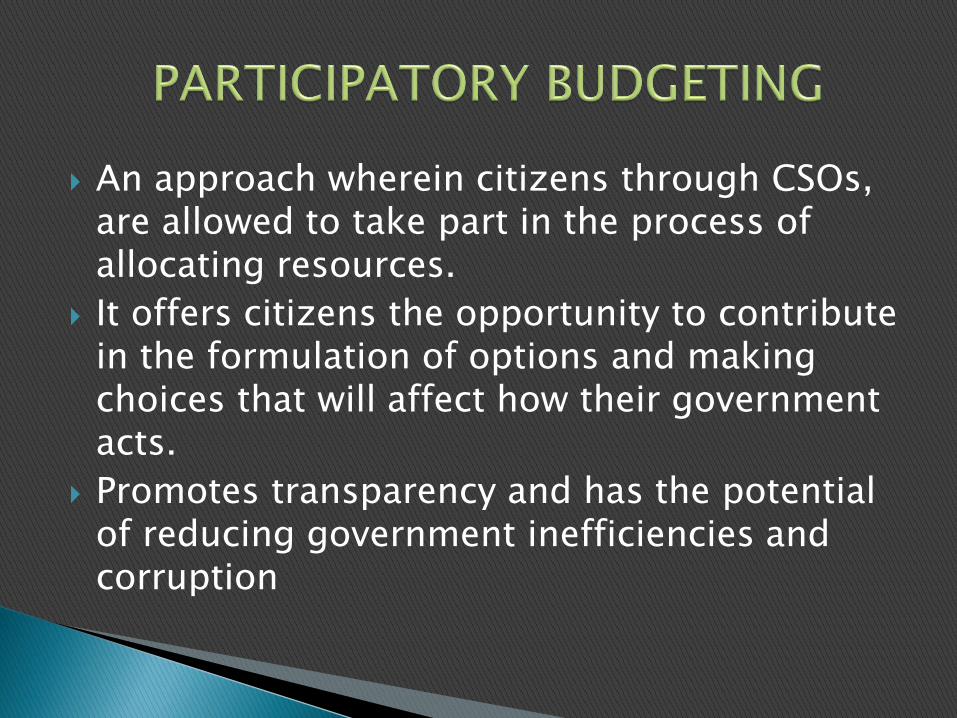

An approach wherein citizens through CSOs, are allowed to take part in the process of allocating resources.

It offers citizens the opportunity to contribute in the formulation of options and making choices that will affect how their government acts.

Promotes transparency and has the potential of reducing government inefficiencies and corruption

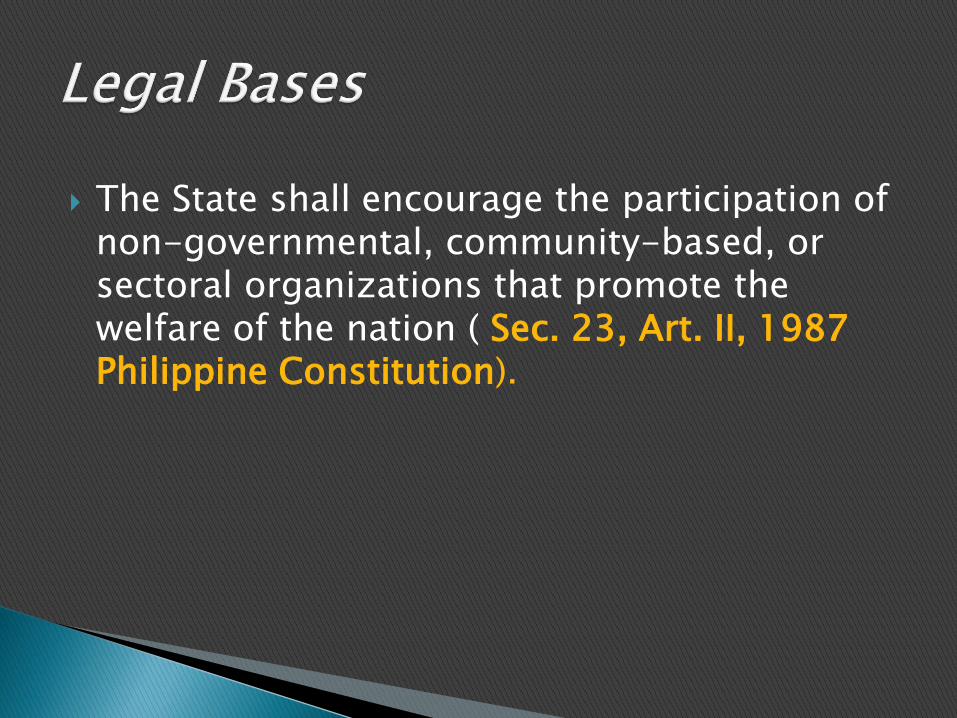

The State shall encourage the participation of non-governmental, community-based, or sectoral organizations that promote the welfare of the nation ( Sec. 23, Art. II, 1987 Philippine Constitution).

The participation of the private sector in local governance, particularly in the delivery of basic services, shall be encouraged to ensure the viability of local autonomy as an alternative strategy for sustainable development (Sec. 3[l], R.A. 7160).

Role of People’s and Non-governmental Organizations ◦ LGUs shall promote the establishment and

operation of people’s and non-governmental organizations to become active partners in the pursuit of local autonomy (Sec. 34, RA 7160).

LGUs shall allow participation of people in planning and budgeting processes.

LGUs shall encourage participation and involvement of CSOs as part of the Local Development Councils (LDCs) and as observers in the Local Finance Committees (LFC).

LGUs shall apply democratic principles in group decision-making techniques to arrive at choices and preferences that are genuinely responsive to people’s needs.

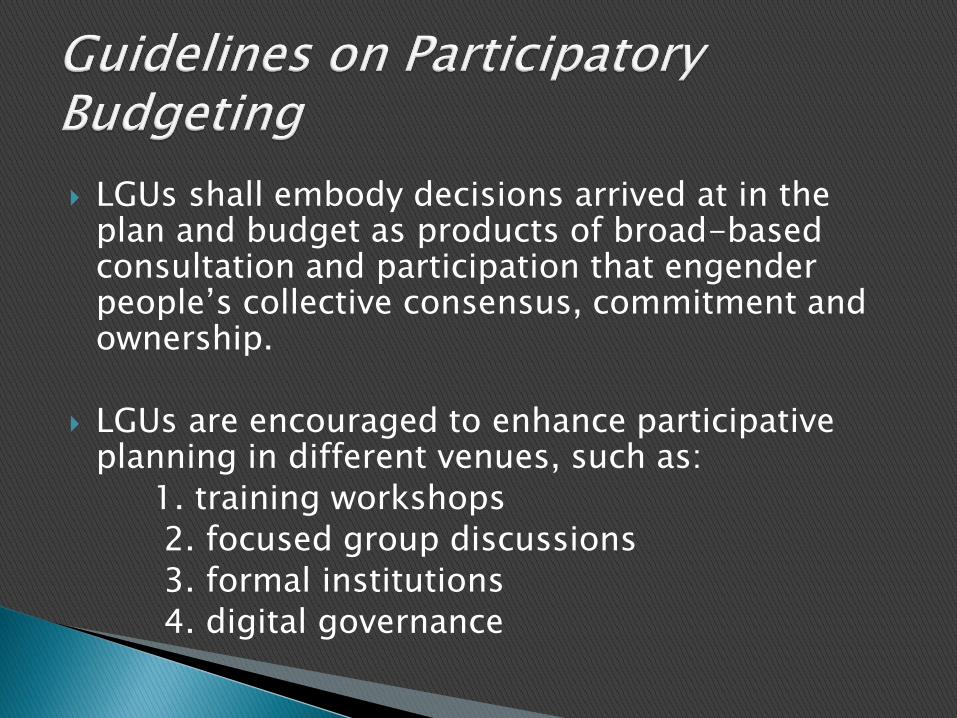

LGUs shall embody decisions arrived at in the plan and budget as products of broad-based consultation and participation that engender people’s collective consensus, commitment and ownership.

LGUs are encouraged to enhance participative planning in different venues, such as:

1. training workshops

2. focused group discussions

3. formal institutions

4. digital governance

LGUs shall establish priorities and allocate resources during investment programming of Programs, Projects and Activities (PPAs) as major links to budgeting.

The ranked PPAs and corresponding resource requirements become the bases for preparing the annual budget proposal.

Transparency

Accountability

Integrity

Partnership

Consultation and mutual empowerment

Respect for internal processes

Sustainability

Helps the LGU maximize the use of resources

Reduces delay in the implementation of urgent projects

Develops trust in Government

Ensures continuity and sustainability of plans and budgets

The CSOs may be engaged in all phases of the budget process, as provided in the Handbook on the Participation of Civil Society Organizations in the Local Budget Process.

It means that the budget is prepared with due regard to local government policy, which in turn, should be harmonized with the development plans and reflected in the investment programs that the LGUs are required to prepare pursuant to RA No. 7160.

An LGU is able to fund in its general fund budget(s) the PPAs that were prioritized in the investment programs, which, in turn, were based on the approved long-term development plan.

Orderliness in the planning and budget processes, demonstrated by compliance with the Synchronized Planning and Budgeting Calendar for LGUs.

Each LGU shall have a comprehensive multi-sectoral development plan to be initiated by its development council and approved by its sanggunian. For this purpose, the development council at the provincial, city, municipal or barangay level, shall assist the corresponding sanggunian in setting the direction of economic and social development, and coordinating development efforts within its territorial jurisdiction (Sec. 106, RA No. 7160).

Provincial, city and municipal development councils shall, among others: ◦ (1) formulate long-term, medium-term and annual

socio-economic development plans and policies; and

◦ (2) formulate the medium term and annual public investment programs

◦ (Sec.109, RA No. 7160).

Local budgets shall operationalize the approved local development plans (Sec. 305 [i], RA No. 7160).

NGAs and GOCCs shall provide LGUs all necessary information on projects already funded in their respective budgets.

Such information shall include specifically, among other things: name of project, location, sources, and levels of funding for said projects. The same information must be made available to the local finance committee concerned within the first quarter of the year to avoid duplication in funding project proposals (Art. 410, Implementing Rules and Regulations [IRR], RA No. 7160).

RA No. 7160 explicitly requires all LGUs to have a multi-sectoral development plan, which shall be translated into programs, projects and activities (PPAs) through investment programs.

The DILG and NEDA planning manuals require the LGUs to prepare the following:

PROVINCES:1. Provincial Development and Physical Framework

Plan (PDPFP)

The PDPFP is a document that identifies strategies and corresponding PPAs that serve as primary inputs to the provincial investment programming process. The PDPFP also serves as a key vertical influence in linking provincial development objectives with local, regional and national policies and priorities.

PROVINCES:

2. Provincial Development Investment

Program (PDIP)

The PDIP is a basic document linking the local development plan to the budget for provinces. It contains a prioritized list of PPAs which are derived from the Provincial Development Physical Framework Plan (PDPFP) matched with financing resources, and to be implemented within a three to six-year period.

COMPONENT CITIES AND MUNICIPALITIES

1. Comprehensive Development Plan (CDP)

The CDP is the multi-sectoral plan formulated at the city or municipal level, which embodies the vision, sectoral goals, objectives, development strategies and policies within the terms of LGU officials and the medium-term. The CDP contains: (1) Ecological Profile; (2) Social Development Plan; and (3) Implementing Instruments.

COMPONENT CITIES AND MUNICIPALITIES

2. Local Development Investment Program

(LDIP)

The LDIP is a basic document linking the local development plan to the budget for cities and municipalities. It contains a prioritized list of PPAs which are derived from the CDP matched with financing resources and to be implemented within a three to six-year period.

PROVINCES, CITIES AND MUNICIPALITIES

1. Annual Investment Program (AIP)

The AIP refers to the annual slice of the Provincial/Local Development Investment Program, which constitutes the total resource requirements for all PPAs, i.e., the annual capital expenditure and regular operating requirements of the LGU.

The processes for formulating the foregoing development plans and investment programs are detailed under the CDP Guide and Concise Illustrative Guide for the Preparation, Review, Monitoring and Updating of the CDP and LDIP issued by the DILG, and in the Manual for Provincial/Local Planning and Expenditure Management issued by the NEDA.

Under Art. 410 of the IRR, RA No. 7160, the following are provided:

1. That the AIP should be prepared and approved before the start of the local budget preparation phase; and

2. That the local budgets shall fund PPAs included in the AIP.

Thus, to ensure plan-budget linkage and ensure that the local budgets truly operationalize the approved local development plans, it is imperative that:

1. The investment programs contain priority PPAs that will directly contribute to the achievement of the goals and objectives of the LGU, as embodied in the development plans; and

2. The local budgets fund the PPAs included in the investment programs, particularly in the AIP.

All procurement should be within the approved budget of the Procuring Entity and should be meticulously and judiciously planned by the Procuring Entity concerned (Sec. 7, RA No. 9184).

No government procurement shall be undertaken unless it is in accordance with the approved Annual Procurement Plan of the Procuring Entity.

(Sec. 7.3.1, RA 9184) Upon issuance of the budget call…and LGUs, the Procuring Entity shall prepare its indicative APP for the succeeding year to support its proposed budget taking into consideration the budget framework for that year in order to reflect its priorities and objectives.

At the local level, as soon as the AIP has been approved by the respective Local Sanggunian, departments/offices or end-users may start preparing their Project Procurement Management Plan (PPMPs) to support the requirements and/or cost estimates of the different PPAs, as embodied in the approved AIP.

Factors to consider in preparing/consolidating the APP:

1. Inclusion of all procurement activities planned for the year

2. Include provisions to cover emergencies or contingencies usually indicated by historical records

3. Scheduling of procurement activities in the APP should be done in such a manner that the BAC and other 0ffices/units involved in the procurement process in the LGU are able to efficiently manage the conduct of procurement transactions.

PIB is the new budgeting approach that uses performance information in appropriation document to link funding to results and to provide a framework for more informed resource allocation and management.

Enables the more meaningful presentation of the budget, whereby each government peso is aligned with performance indicators and tangible targets of the LGU.

Budgets of LGUs shall include a brief description of the functions, projects and activities for the ensuing fiscal year, expected results for each function, project and activity, and the nature of work to be performed, including the objects of expenditure for each function, project and activity (Sec. 317 [b] [3], RA No. 7160).

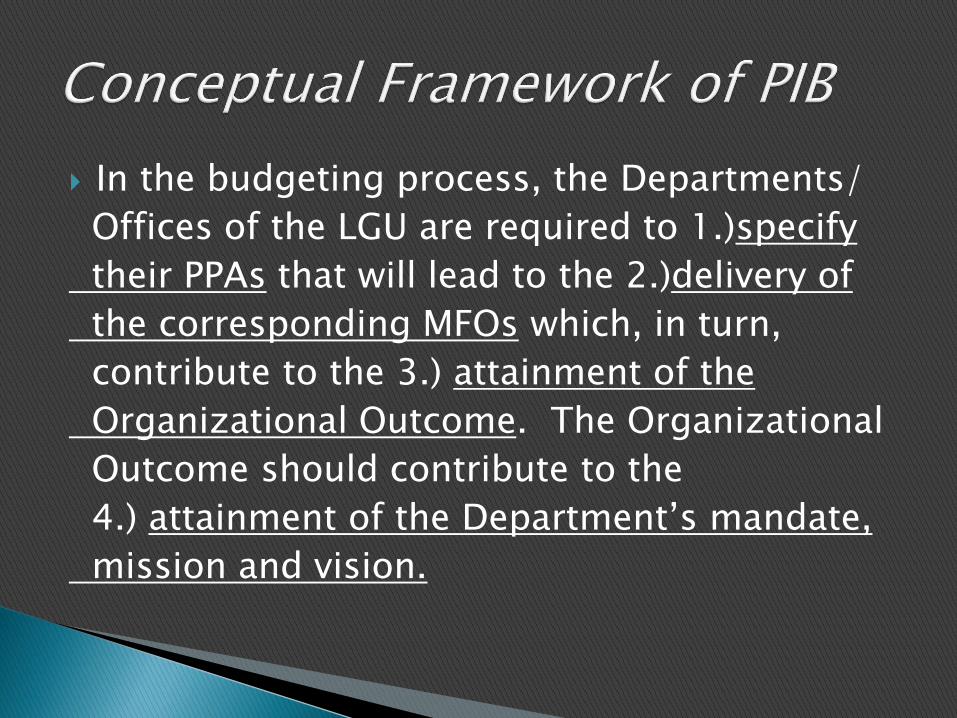

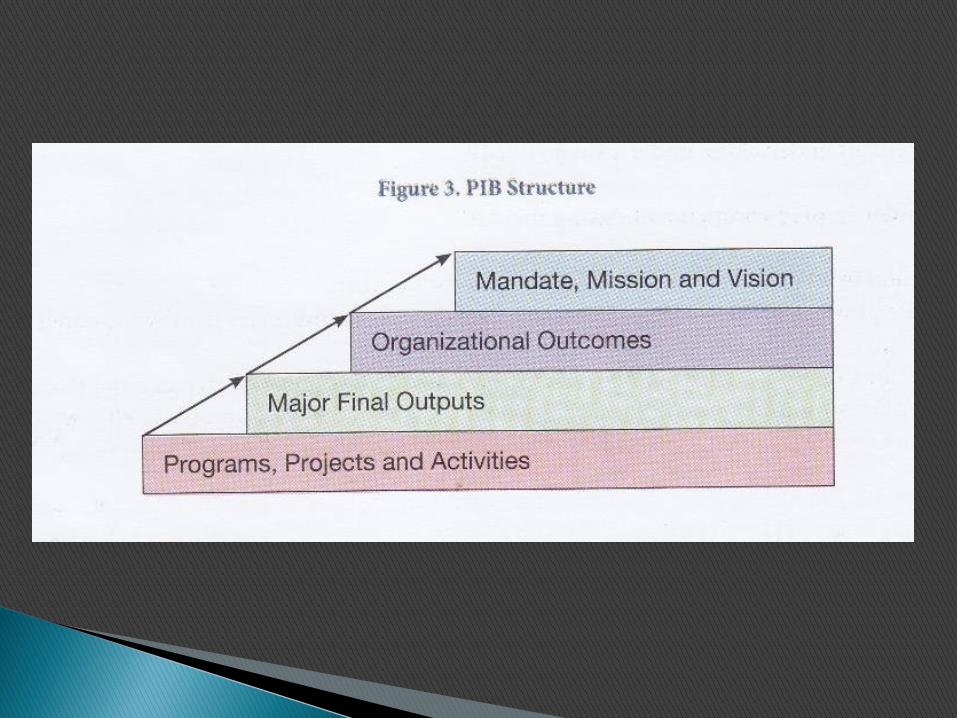

In the budgeting process, the Departments/

Offices of the LGU are required to 1.)specify

their PPAs that will lead to the 2.)delivery of

the corresponding MFOs which, in turn,

contribute to the 3.) attainment of the

Organizational Outcome. The Organizational

Outcome should contribute to the

4.) attainment of the Department’s mandate,

mission and vision.

The PIB as a core PFM reform program is seen as a critical tool in steering the government towards inclusive growth and delivers the following key benefits:

1. Reinforce the meaning of accountability as a commitment to perform

2. Empower citizens to participate in the utilization and allocation of resources with more transparent, accountable and responsive budget documents

3. Enable individual agencies/LGUs to see opportunities on how activities fit in the broader development plan and how they could collaborate with other agencies/LGUs in achieving a common goal

4. Allow the Executive Branch to ensure that each peso spent is tightly linked to its priority outcome to reduce overlaps and to avoid duplicative or inefficient spending

5. Enable legislators to better evaluate the budget proposals and to better exercise their oversight function to check it the agencies/LGU deliver the results they committed to deliver;

6. Ensure that projects and programs are properly aligned with national development goals and objectives.

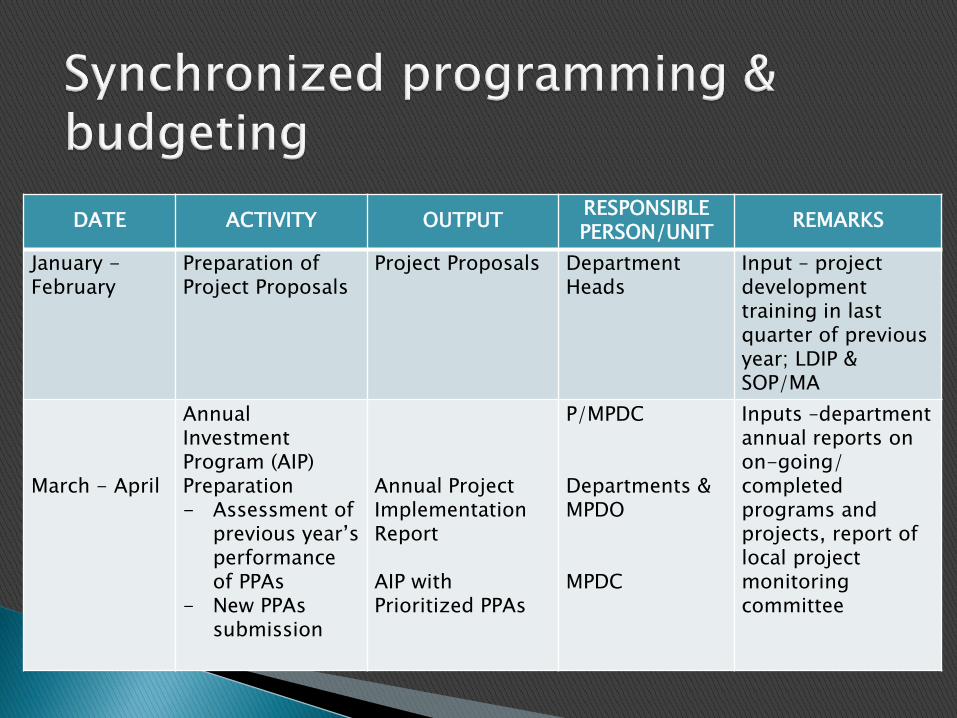

DATE ACTIVITY OUTPUTRESPONSIBLE PERSON/UNIT

REMARKS

January -February

Preparation of Project Proposals

Project Proposals Department Heads

Input – project development training in last quarter of previous year; LDIP & SOP/MA

March - April

Annual Investment Program (AIP) Preparation- Assessment of

previous year’s performance of PPAs

- New PPAs submission

Annual Project Implementation Report

AIP with Prioritized PPAs

P/MPDC

Departments & MPDO

MPDC

Inputs –department annual reports on on-going/ completed programs and projects, report of local project monitoring committee

DATE ACTIVITY OUTPUTRESPONSIBLE PERSON/UNIT

REMARKS

April - June Estimation of Revenue

Actual (previous 3 years) and Projected (planning year) Revenue

Treasurer and Expanded Local FinanceCommittee

Inputs – New DBM issuances, COA report/AOMs

July Budget Call Memorandum from the LCE to all Department Heads

LCE

July - August Estimation of Expenditures

Actual (previous 3 years) and Projected (planning year) Expenditures

Budget Officer and Expanded Local Finance Committee

Inputs – New DBM issuances, COA report/AOMs

August -September

BudgetPreparation

Proposed Local Budget

Finance Committee and LCE

DATE ACTIVITY OUTPUTRESPONSIBLE PERSON/UNIT

REMARKS

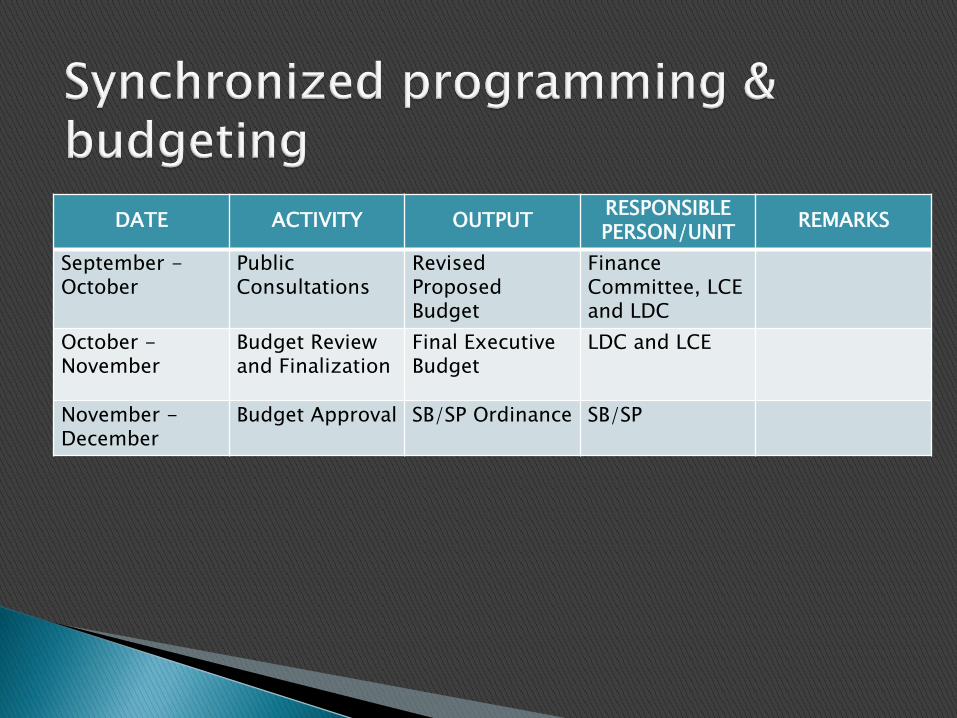

September -October

Public Consultations

Revised Proposed Budget

Finance Committee, LCE and LDC

October -November

Budget Review and Finalization

Final Executive Budget

LDC and LCE

November -December

Budget Approval SB/SP Ordinance SB/SP