hennepin health foundation...3 hennepin health foundation a component unit of hennepin healthcare...

TRANSCRIPT

Hennepin Health Foundation A Component Unit of Hennepin Healthcare System, Inc. Financial Report December 31, 2017

Contents Independent auditor’s report 1-2 Financial statements

Statements of net position 3

Statements of revenues, expenses and changes in net position 4

Statements of cash flows 5

Notes to financial statements 6-15

1

Independent Auditor’s Report To the Board of Directors Hennepin Health Foundation Report on the Financial Statements We have audited the accompanying financial statements of Hennepin Health Foundation (HHF) a component unit of Hennepin Healthcare System, Inc. d/b/a Hennepin County Medical Center, as of and for the year ended December 31, 2017, and the related notes to the financial statements, which collectively comprise HHF’s basic financial statements as listed in the table of contents. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion the financial statements referred to above present fairly, in all material respects, the financial position of HHF as of December 31, 2017, and the changes in financial position and cash flows for the years then ended, in conformity with accounting principles generally accepted in the United States of America.

2

Emphasis of Matter As discussed in Note 1 to the financial statements, management evaluated and determined presentation of the financial statements in accordance with Governmental Accounting Standards Board standards for business-type activities using the economic resources measurement focus and the full accrual basis of accounting is appropriate. The December 31, 2016 financial statements were presented in accordance with Governmental Accounting Standards Board standards for governmental type activities and governmental funds using the current financial resources measurement focus and the modified accrual basis of accounting. Our opinion is not modified with respect to this matter. Other Matters The financial statements of HHF, as of and for the year ended December 31, 2016, were audited by other auditors, whose report, dated February 24, 2017, expressed an unmodified opinion on those statements. Management has omitted a management’s discussion and analysis that accounting principles generally accepted in the United States of America require to be presented to supplement the basic financial statements. Such missing information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic or historical context. Our opinion on the basic financial statements is not affected by this missing information.

Duluth, Minnesota March 5, 2018

3

Hennepin Health Foundation

A Component Unit of Hennepin Healthcare System, Inc.

Statements of Net Position

December 31, 2017 and 2016

2017 2016Assets

Cash and cash equivalents 7,845,435 $ 5,318,322 $ Other accounts receivable 410,469 67,679 Contributions and grants receivable, net 2,209,441 5,564,335 Receivable from related parties 80,221 5,933 Prepaids 700 1,393 Investments 12,189,154 10,786,661

Capital assets:Non-depreciable, art collection 673,258 394,893 Depreciable, furniture and equipment 19,257 19,257

Total capital assets 692,515 414,150 Less accumulated depreciation 19,257 19,257

Total capital assets, net 673,258 394,893

Total assets 23,408,678 $ 22,139,216 $

Liabilities and Net Position

Liabilities:Grants payable 512,288 $ 216,611 $ Accounts payable 85,168 10,037 Payable to related parties 33,243 140,881 Unearned revenue 58,333 - Due to fiscal agent 22,941 44,497

Total liabilities 711,973 412,026

Net position:Unrestricted 368,143 442,661 Net investment in capital assets 673,258 394,893 Restricted:

Expendable 19,373,389 18,767,524 Nonexpendable 2,281,915 2,122,112

Total net position 22,696,705 21,727,190

Total liabilities and net position 23,408,678 $ 22,139,216 $

See notes to financial statements.

4

Hennepin Health Foundation

A Component Unit of Hennepin Healthcare System, Inc.

Statements of Revenue, Expenses and Changes in Net Position

Years Ended December 31, 2017 and 2016

2017 2016Operating revenues:

Contributions 2,420,638 $ 1,809,618 $ Grants and contracts 859,678 2,065,217 Noncash contributions 2,342,970 2,263,241 Special events 577,928 575,976 Commissions 171,814 153,825 Other income 98,808 163,201

Total operating revenue 6,471,836 7,031,078

Operating expenses:Grants and disbursements 3,521,807 3,507,985 Personnel expense 1,861,980 1,696,642 Supplies and services 920,679 1,116,371 Facility 100,432 100,432 Other 584,029 590,443

Total operating expenses 6,988,927 7,011,873

(Loss) income from operations (517,091) 19,205

Nonoperating gains (losses):Investment income, net 1,540,530 715,938 Other (263,750) -

Total nonoperating revenues 1,276,780 715,938

Income before capital items 759,689 735,143

Contributions to permanent endowment 209,826 926,675

Change in net position 969,515 1,661,818

Net position:Beginning of year 21,727,190 20,065,372

Ending of year 22,696,705 $ 21,727,190 $

See notes to financial statements.

5

Hennepin Health Foundation

A Component Unit of Hennepin Healthcare System, Inc.

Statements of Cash Flows

Years Ended December 31, 2017 and 2016

2017 2016Cash flows from operating activities:

Contributions 5,379,625 $ 3,403,305 $ Grants 859,678 1,440,717 Special events 675,699 575,472 Other revenues - 158,814 Other payments (494,807) (359,929) Commissions 171,814 153,825 Paid for grants (3,226,130) (3,325,949) Paid to suppliers (684,513) (777,644)

Net cash provided by operating activities 2,681,366 1,268,611

Cash flows provided by noncapital financing activities,contributions to permanent endowments 209,826 926,675

Cash flows used in capital financing activities, purchases of capital assets (278,365) (4,114)

Cash flows from investing activities:Purchase of investments (794,260) (10,451,797) Sale of investments 302,864 6,314,790 Investment earnings received 405,682 799,186

Net cash used in investing activities (85,714) (3,337,821)

Net increase (decrease) in cash and cash equivalents 2,527,113 (1,146,649)

Cash and cash equivalents:Beginning of year 5,318,322 6,464,971

End of year 7,845,435 $ 5,318,322 $

Reconciliation of operating income to net cash provided by operating activities:Operating (loss) income (517,091) $ 19,205 $

(Increase) decrease in assets:Other accounts receivable (417,078) 13,448 Grants and contributions receivable 3,354,894 969,187 Prepaids 693 (1,393)

Increase (decrease) in liabilities:Accounts payable (54,063) 104,468 Grants payable 295,677 182,036 Unearned revenue 18,334 (18,340)

Net cash provided by operating activities 2,681,366 $ 1,268,611 $

Noncash investing, capital and financing activities:Noncash contributions 2,342,970 $ 2,263,241 $

Donated artwork -$ 4,114 $

See notes to financial statements.

Hennepin Health Foundation A Component Unit of Hennepin Healthcare System, Inc. Notes to Financial Statements

6

Note 1. Nature of Organization and Summary of Significant Accounting Policies

Nature of organization: Hennepin Health Foundation (HHF) is a Minnesota nonprofit corporation and has been recognized by the Internal Revenue Service as exempt from federal income taxes under the Internal Revenue Code Section 501(c)(3). Hennepin Healthcare System, Inc. (HHS) d/b/a Hennepin County Medical Center is the sole member of HHF. HHS is a public corporation and a component unit of Hennepin County (the County), Minnesota. HHF supports the mission of HHS, Minnesota's largest public safety net and academic medical center where no one is turned away due to lack of insurance or inability to pay. HHS is home to the largest and busiest trauma center in the state, and trains the majority of the physicians, nurses and other clinicians who care for the citizens of Minnesota. HHS's hospital and clinics deliver more than 111,000 emergency and urgent care visits and more than 628,000 clinic visits each year. Hennepin Health Foundation raises and administers philanthropic support for HHS and its research arm, Minneapolis Medical Research Foundation (MMRF) in the following functional areas: Innovations in patient care: Programs funded in this area help to improve the patient and family experience, reduce barriers to health care access, assist with social determinants of health, and launch innovation in care delivery. Examples of funded activities include: Volunteer Services, Inspire Arts Program, Children’s Literacy, Mother Baby Program, renovations to patient and family waiting areas, and a variety of specific department funds for patient urgent needs. HHF provides support for MVNA home health and in home hospice services which provided more than 23,000 home health visits in 2017. Trauma and critical care: This area provides funding to patient care services related to HCMC’s Level 1 Trauma designation. Funded programs include patient comfort in traumatic brain injury, the burn unit, stroke, heart health, poison control and toxicology care, care during and after transplant, and care in dealing with the effects of domestic violence, sexual assault, and child abuse and neglect. Operating the largest, multi chamber Hyperbaric Oxygen (HBO) Chamber in the state, the HBO provided over 5,422 treatments in 2017. The Regional Poison Information Center for Minnesota, North and South Dakota, managed at HHS, handled over 63,000 calls in 2017. Educating the workforce of tomorrow: HHS is the state’s primary training center for physicians, nurses, ancillary care, pre-hospital emergency personnel and other health professions. Funded programs include: the development of a health sciences education center to improve the quality of instruction and learning for trainees in the medicine, nursing and allied health professions, a scholarship program to assist employees in non-patient care areas in entering health careers, various ongoing training funds for hospital departments and clinics, a fund to support emergency medicine residency education and the Hennepin Medical History Center which collects, preserves and interprets the history of HHS, Metropolitan Medical Center and its organizational predecessors. In 2017, HHF helped raise $400,000 to support the Stillman Endowment for Education held at Minneapolis Medical Research Foundation. Research: Searching for new ways to improve care is a commitment voiced in the mission of HHS, where medical research directed by the Minnesota Medical Research Foundation (MMRF) leads to breakthroughs in medical treatment and disease prevention. MMRF is the third largest nonprofit medical research organization in Minnesota and it ranks in the top 7 percent of all institutions receiving research funding from the National Institutes of Health. As its philanthropic partner, HHF raises funds to support its research endeavors ranging from addiction and kidney disease to traumatic brain injury.

Hennepin Health Foundation A Component Unit of Hennepin Healthcare System, Inc. Notes to Financial Statements

7

Note 1. Nature of Organization and Summary of Significant Accounting Policies (Continued)

Reporting entity: In accordance with Governmental Accounting Standards Board (GASB) Statement No. 80, Blending Requirements for Certain Component Units—an amendment of GASB Statement No. 14, HHS has included HHF as a blended component within their statements. HHS is the sole corporate member of HHF. Accounting principles generally accepted in the United States of America require that the financial reporting entity include 1) the primary government, 2) organizations for which the nature and significance of their relationship with the primary government are such that exclusion would cause the reporting entity’s financial statements to be misleading or incomplete. Based on these criteria, there are no other organizations or agencies whose financial statements should be combined and presented with these basic financial statements. Accounting basis and standards: The financial statements of HHF have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP) as applied to governmental units. The Governmental Accounting Standards Board (GASB) is the accepted standard setting body for establishing governmental accounting and financial reporting principles. The GASB pronouncements are recognized as GAAP for state and local governments. The December 31, 2016 financial statements were presented in accordance with GASB standards for governmental type activities and governmental funds using the current financial resources measurement focus and the modified accrual basis of accounting. During 2017 management evaluated and determined presentation in accordance with GASB standards for business-type activities using the economic resources measurement focus and the full accrual basis of accounting was more appropriate based on the nature of HHF activities. Therefore, these financial statements are presented as such. HHF recognizes revenues and expenses on the accrual basis of accounting using the economic resources measurement focus. Revenue is recognized when earned and expenses are recognized when a liability has been incurred. Under this basis of accounting, all assets and liabilities associated with HHF are included in the statements of net position. Cash and cash equivalents: Cash and cash equivalents include highly liquid investments with a maturity of three months or less and HHF’s share of the cash management pool of Hennepin County. The pool is a cash equivalent (see Note 2). Investments: Investments in equity securities with readily determinable fair values and all investments in debt securities are measured at fair value in the statements of revenue, expenses and changes in net position. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Other accounts receivable: Accounts receivable are recorded at net realizable value. HHF provides an allowance for uncollectible accounts using the reserve method, which is based on management judgment considering historical information. Accounts more than 90 days past due are individually analyzed for collectability. In addition, an allowance is provided for other accounts when a significant pattern of un-collectability has occurred. When all collection efforts have been exhausted, the accounts are written off against the related allowance. At December 31, 2017 and 2016, management determined that an allowance was not warranted.

Hennepin Health Foundation A Component Unit of Hennepin Healthcare System, Inc. Notes to Financial Statements

8

Note 1. Nature of Organization and Summary of Significant Accounting Policies (Continued)

Contributions and grants receivable: Contributions receivable are unconditional promises to give. Contributions and grants receivable are recorded, net of an allowance for uncollectable accounts, at the time of the gift. Conditional promises to give are not recorded as revenue until such time as the conditions are substantially met. Contributions and grants receivable that are expected to be collected in greater than one year are recorded at the present value of the amounts expected to be collected using a discount rate reflective of the market and conditions at the time of the gift. Amortization of the discount is included in contribution revenue. Art collection: HHF has pieces of art located throughout Hennepin Healthcare System. The art is valued at cost or acquisition value at the date of the purchase or donation. HHF typically only records pieces that are originals and signed prints. HHF set its capitalization threshold for pieces at $300. With the opening of the new Clinical and Specialty Center building planned for spring of 2018, HHF added a major art piece to the collection in 2017, bringing the value of the collection to $673,258 from $394,893 as of December 31, 2017 and 2016, respectively. Furniture and equipment: All expenditures for equipment exceeding $1,000 are capitalized at cost. Contributed items are recorded at acquisition value at date of donation. Depreciation is computed through the use of the straight-line method over the assets’ estimated useful lives. As of December 31, 2017, HHF had fully depreciated assets of $19,257. Grants payable: Unconditional grants are recorded as expense when approved by HHF's board of directors. Grants and contributions: Revenues from grants and contributions are recognized when all eligibility requirements, including time requirements, are met. Grants and contributions may be restricted for either specific operating purposes or for capital purposes. Amounts restricted to capital acquisitions are reported after nonoperating revenue and expenses. There were not restricted to capital acquisitions as of December 31, 2017 and 2016. Functional expenses: The cost of services provided and expense are allocated to program, fundraising and management and general services based on identification of both direct and indirect expenses:

2017 Percent 2016 PercentProgram services:

Hennepin Healthcare System, Inc. 4,197,038 $ 4,698,166 $ Minneapolis Medical Research Foundation 434,989 13,175 Special events 447,567 438,664

Total program services 5,079,594 72% 5,150,005 73% Fundraising 1,018,884 15 1,037,548 15 Management and general 890,449 13 824,320 12

6,988,927 $ 100% 7,011,873 $ 100%

Hennepin Health Foundation A Component Unit of Hennepin Healthcare System, Inc. Notes to Financial Statements

9

Note 1. Nature of Organization and Summary of Significant Accounting Policies (Continued)

Noncash contributions: Goods and services donated to HHF are recorded at the fair acquisition as determined by management at the time of receipt. Net position: The net investment in capital assets consists of capital assets, net of accumulated depreciation and any outstanding borrowings used to finance the purchase or construction of these assets. Restricted expendable net position are amounts that must be used for a particular purpose, as specified by creditors, grantors, donors, or contributors external to HHF. Restricted nonexpendable net position are amounts that represent donors’ fund principal that must be maintained in perpetuity. Unrestricted net position are amounts that do not meet the definition of the other components of net position described above. Restricted expendable net position is available for the following donor-imposed purposes as of December 31:

2017 2016

Innovations in patient care 17,555,720 $ 17,021,362 $ Educating the workforce of tomorrow 1,201,784 931,615 Critical care mission 429,852 433,779 Research 28,754 11,186 Special events 157,279 369,582

19,373,389 $ 18,767,524 $

Reclassifications: Certain prior year amounts on the financial statements have been reclassified to conform to the December 31, 2017 presentation. These reclassifications had no effect on the change in the net position or total net position as previously reported. Estimates: Management uses estimates and assumptions in preparing financial statements in accordance with U.S. generally accepted accounting principles. Those estimates and assumptions affect the reported amounts of assets (including artwork) and liabilities, the disclosure of contingent assets and liabilities, and the reported revenue and expenses. Actual results could vary from the estimates that were used. Income taxes: HHF has a tax-exempt status under Section 501(c)(3) of the Internal Revenue Code (IRC) and Minnesota Statute and corresponding tax codes and, therefore, the financial statements do not include a provision for income taxes. It has been classified as an organization that is not a private foundation under the IRC and charitable contributions by donors are tax deductible. HHF's 2014-2017 tax years are open for examination by federal and state taxing authorities. HHF files as a tax exempt organization, should that status be challenged in the future, all years since inception would be subject to review by the IRS.

Hennepin Health Foundation A Component Unit of Hennepin Healthcare System, Inc. Notes to Financial Statements

10

Note 2. Interest in Hennepin County Investment Pool

The County’s Office of Budget and Finance is responsible for the treasury function of all the County’s deposits and investments held by its funds. Cash from all funds is pooled for deposit and investment purposes. At December 31, 2017, HHF comprised $7,845,435 or .74 percent of the County’s total cash and investments. As of December 31, 2017, a majority of the pool’s investments were invested in U.S. government and agency issues, with the remainder invested in repurchase agreements and money market funds. Detailed information about the County’s deposits with financial institutions, repurchase agreements, interest rate risk, credit risk, concentration of credit risk, and custodial credit risk can be obtained directly from the County’s 2017 financial statements. Investment earnings and losses are allocated based on average monthly cash balances.

Note 3. Concentrations

Financial Instruments that potentially subject HHF to concentrations of credit risk consist principally of pledges and grants receivable. HHF had approximately 43 percent of its contributions and grants receivable balance from two grantors/donors at December 31, 2017.

Note 4. Investments

HHF categorizes its assets and liabilities measured at fair value into a three-level hierarchy based on the priority of the inputs to the valuation technique used to determine fair value. The fair value hierarchy gives the highest priority to quoted prices in active markets for identical assets or liabilities (Level 1) and the lowest priority to unobservable inputs (Level 3). If the inputs used in the determination of the fair value measurement fall within different levels of the hierarchy, the categorization is based on the lowest level input that is significant to the fair value measurement. Assets and liabilities valued at fair value are categorized based on the inputs to the valuation techniques as follows: Level 1: Inputs that utilize quoted prices (unadjusted) in active markets for identical assets or liabilities

that an entity has the ability to access. Level 2: Inputs that include quoted prices for similar assets and liabilities in active markets and inputs

that are observable for the asset or liability, either directly or indirectly, for substantially the full term of the financial instrument. Fair values for these instruments are estimated using pricing models, quoted prices of securities with similar characteristics, or discounted cash flows.

Level 3: Inputs that are unobservable inputs for the asset or liability, which are typically based on an

entity’s own assumptions, as there is little, if any, related market activity. HHF uses fair value measurements to record fair value adjustments to certain assets and liabilities and to determine fair value disclosures. Custodial credit risk: For an investment, custodial credit risk is the risk that, in the event of failure of the counterparty, the fund will not be able to recover the value or collateral securities that are in the possession of an outside party. Investment securities are exposed to custodial risk if the securities are uninsured, are not registered in HHF’s name and are held by either (a) the counterparty or (b) the counterparty’s trust department or agent but not in HHF’s name. HHF’s investment policy does not limit the value of investments that may be held by an outside party. At December 31, 2017 and 2016, HHF’s investments had no custodial credit risk exposure.

Hennepin Health Foundation A Component Unit of Hennepin Healthcare System, Inc. Notes to Financial Statements

11

Note 4. Investments (Continued)

The following table presents the fair value hierarchy for the balances of assets and liabilities measured at fair value on a recurring basis as of December 31:

Level 1 Level 2 Level 3 Total

Mutual funds—bonds

Short term 1,188,261 $ -$ -$ 1,188,261 $ Intermediate term 3,608,154 - - 3,608,154

Mutual funds—equities

Mid Cap 1,227,070 - - 1,227,070 Large Cap 4,331,965 - - 4,331,965 International 1,822,238 - - 1,822,238

Total investments at fair value 12,177,688 $ -$ -$ 12,177,688

Cash and cash equivalents 11,466 Total investments 12,189,154 $

Level 1 Level 2 Level 3 Total

Mutual funds—bonds

Short term 997,987 $ -$ -$ 997,987 $ Intermediate term 3,093,555 - - 3,093,555

Mutual funds—equities

Mid Cap 1,055,955 - - 1,055,955 Large Cap 3,790,852 - - 3,790,852 International 1,547,675 - - 1,547,675

Domestic equities 32,149 - - 32,149 Other - - 263,751 263,751

Total investments at fair value 10,518,173 $ -$ 263,751 $ 10,781,924

Cash and cash equivalents 4,737 Total investments 10,786,661 $

2017

2016

Interest rate risk: Interest rate risk is the risk that changes in interest rates will adversely affect the fair value of an investment. As a means of limiting HHF's exposure to interest rate risk, HHF's investment policy states there will be a long-term investment pool and near term investment pool. Near term pool is invested with Hennepin County Treasury Department in fixed income securities with an average weighted maturity of 3.3 years. The long-term investment pool is invested in mutual funds.

Hennepin Health Foundation A Component Unit of Hennepin Healthcare System, Inc. Notes to Financial Statements

12

Note 4. Investments (Continued)

As of December 31, 2017, HHF had the following investments and maturities:

Carrying Less than 1 to 5 5 to 10Amount 1 Year Years Years Over 10

Mutual funds—bonds 4,796,415 $ 4,796,415 $ -$ -$ -$

Mutual funds—equities 7,381,273 Cash and cash equivalents 11,466

12,189,154 $

As of December 31, 2016, HHF had the following investments and maturities:

Carrying Less than 1 to 5 5 to 10Amount 1 Year Years Years Over 10

Mutual funds—bonds 4,091,542 $ 4,091,542 $ -$ -$ -$

Mutual funds—equities 6,394,482 Other 263,751 Domestic equities 32,149 Cash and cash equivalents 4,737

10,786,661 $

Credit risk: Generally, credit risk is the risk that an issuer of an investment will not fulfill its obligation to the holder of the investment. This risk is measured by the assignment of a rating by a nationally recognized statistical rating organization. HHF does not have a policy specific to investment credit risk. As of December 31, 2017 and 2016, the investments as rated by Moody’s had the following ratings:

2017 2016Carrying Carrying

Type of Investment Amount Quality Rating Amount Quality Rating

Mutual funds—bonds 4,796,415 $ Baa3 4,091,542 $ Baa3Not rated:

Mutual funds—equities 7,381,273 6,394,482 Other - 263,751 Domestic equities - 32,149 Cash and cash equivalents 11,466 4,737

Total investment 12,189,154 $ 10,786,661 $ Concentration of risk: Concentration of credit risk is the risk of loss attributed to the magnitude of an entity’s investment in a single issuer. HHF's investment policy does not limit the type of investment but does establish asset allocation targets. As of December 31, 2017 and 2016, not more than 5 percent of HHF’s total investments were invested in securities of any one issuer, excluding securities issued or guaranteed by the U.S. government, mutual funds, and external investment pools or other pooled investments.

Hennepin Health Foundation A Component Unit of Hennepin Healthcare System, Inc. Notes to Financial Statements

13

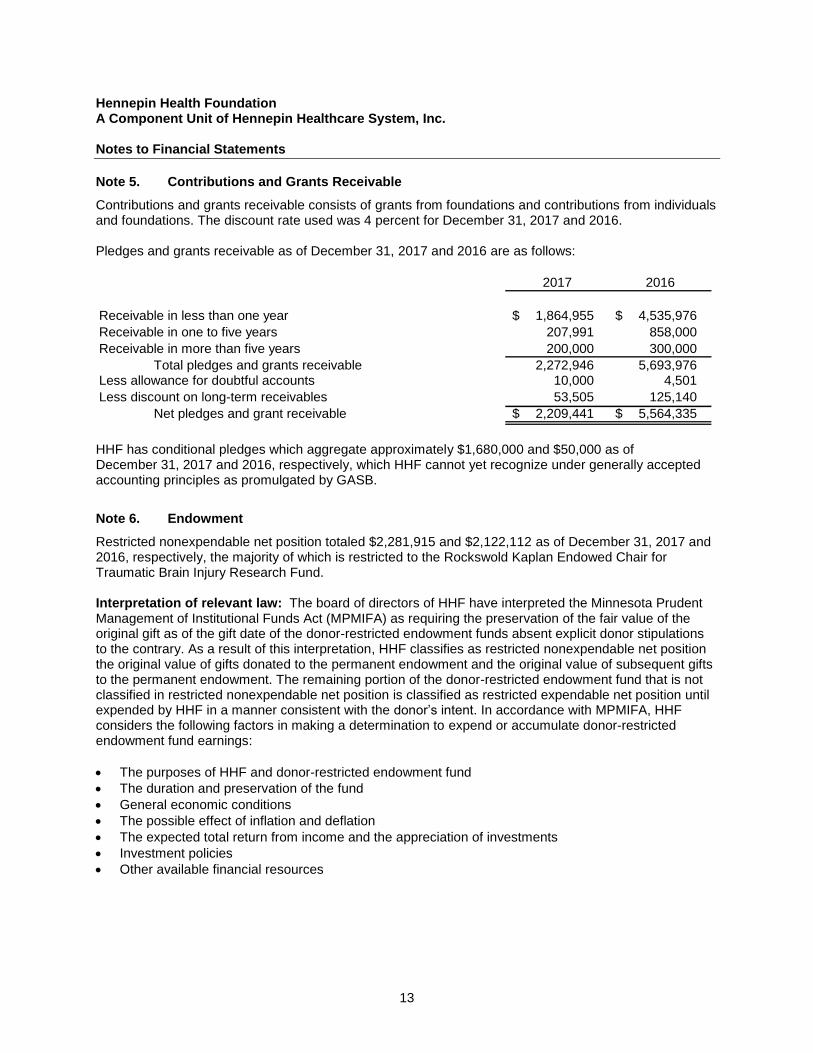

Note 5. Contributions and Grants Receivable

Contributions and grants receivable consists of grants from foundations and contributions from individuals and foundations. The discount rate used was 4 percent for December 31, 2017 and 2016. Pledges and grants receivable as of December 31, 2017 and 2016 are as follows:

2017 2016

Receivable in less than one year 1,864,955 $ 4,535,976 $ Receivable in one to five years 207,991 858,000 Receivable in more than five years 200,000 300,000

Total pledges and grants receivable 2,272,946 5,693,976 Less allowance for doubtful accounts 10,000 4,501 Less discount on long-term receivables 53,505 125,140

Net pledges and grant receivable 2,209,441 $ 5,564,335 $

HHF has conditional pledges which aggregate approximately $1,680,000 and $50,000 as of December 31, 2017 and 2016, respectively, which HHF cannot yet recognize under generally accepted accounting principles as promulgated by GASB.

Note 6. Endowment

Restricted nonexpendable net position totaled $2,281,915 and $2,122,112 as of December 31, 2017 and 2016, respectively, the majority of which is restricted to the Rockswold Kaplan Endowed Chair for Traumatic Brain Injury Research Fund. Interpretation of relevant law: The board of directors of HHF have interpreted the Minnesota Prudent Management of Institutional Funds Act (MPMIFA) as requiring the preservation of the fair value of the original gift as of the gift date of the donor-restricted endowment funds absent explicit donor stipulations to the contrary. As a result of this interpretation, HHF classifies as restricted nonexpendable net position the original value of gifts donated to the permanent endowment and the original value of subsequent gifts to the permanent endowment. The remaining portion of the donor-restricted endowment fund that is not classified in restricted nonexpendable net position is classified as restricted expendable net position until expended by HHF in a manner consistent with the donor’s intent. In accordance with MPMIFA, HHF considers the following factors in making a determination to expend or accumulate donor-restricted endowment fund earnings: The purposes of HHF and donor-restricted endowment fund The duration and preservation of the fund General economic conditions The possible effect of inflation and deflation The expected total return from income and the appreciation of investments Investment policies Other available financial resources

Hennepin Health Foundation A Component Unit of Hennepin Healthcare System, Inc. Notes to Financial Statements

14

Note 6. Endowment (Continued)

Spending policy, objectives and strategies: HHF has adopted investment and spending policies for permanently restricted cash contributions that attempt to provide a predictable stream of funding to programs, while maintaining purchasing power. The annual investment withdrawal is calculated at 4 percent of the 3-year quarterly average of the investment market values at September 30th. All earnings from these funds are reflected as restricted expendable net position until appropriated for program expenditures. Endowment net position composition by type as of December 31, 2017 and 2016 is as follows:

2017Restricted Restricted

Expendable Nonexpendable Total

Donor-restricted endowment funds 30 $ 2,281,915 $ 2,281,945 $

2016Restricted Restricted

Expendable Nonexpendable Total

Donor-restricted endowment funds 315 $ 1,858,361 $ 1,858,676 $

The changes in endowment net position for the years ended December 31, 2017 and 2016 are as follows:

2017Restricted Restricted

Expendable Nonexpendable Total

Endowment investments, beginning 315 $ 1,858,361 $ 1,858,676 $ Investment gain - 213,728 213,728 Contributions 480 209,826 210,306 Appropriations of endowment assets for

expenditures (765) - (765) Endowment investments, ending 30 $ 2,281,915 $ 2,281,945 $

2016Restricted Restricted

Expendable Nonexpendable Total

Endowment investments, beginning 163 $ 898,944 $ 899,107 $ Investment gain 460 32,742 33,202 Contributions 20 926,675 926,695 Appropriations of endowment assets for

expenditures (328) - (328) Endowment investments, ending 315 $ 1,858,361 $ 1,858,676 $

Hennepin Health Foundation A Component Unit of Hennepin Healthcare System, Inc. Notes to Financial Statements

15

Note 7. Related Party Transactions

In-kind contributions: HHS employs all HHF personnel and, therefore, provides all salaries, employee benefits and administrative costs for those personnel. For the years ended December 31, 2017 and 2016, salaries and benefits paid by HHS totaled $1,861,980 and $1,696,642, respectively. HHS provides computer usage, office supplies, and professional services utilized by HHF, which totaled $280,480 and $348,091 for the years ended December 31, 2017 and 2016, respectively. HHS supports HHF by providing space for the general office, and space for collections of the Hennepin Historical Center and the Inspire Arts Program. The total estimated support of space was $100,431 for each of the years ended December 31, 2017 and 2016. Contributions: HHF supports HHS with monies given to maintain programs, provide urgent needs, assist in patient care and provide seed money for new initiatives. For the years ended December 31, 2017 and 2016, HHF disbursed $3,086,817 and $3,489,811, respectively, to HHS. HHF serves as the fundraising portal of the HHS campus, including its research partner, Minneapolis Medical Research Foundation (MMRF). HHF dedicates a portion of its fundraising efforts to assist MMRF in providing startup and bridge funding for medical research. HHF distributed $434,989 and $13,175 to MMRF at December 31, 2017 and 2016, respectively. HHF received artwork valued at $13,480 and $9,000 for the years ended December 31, 2017 and 2016, respectively. The artwork is added to HHF’s collection and is used and displayed by HHS. Due to/due from related party: HHS owed HHF $70,411 as of December 31, 2017 and HHF owed HHS $114,726 as of December 31, 2016. The County owed HHF $9,810 and $5,933 as of December 31, 2017 and 2016, respectively. HHF owed MMRF $33,243 and $26,155 as of December 31, 2017 and 2016, respectively.