helsinki university of technology mba programs · found applicable for valuation of biotechnology...

TRANSCRIPT

1

Helsinki University of Technology

MBA Programs

Margita Engström

REAL OPTION MODEL FOR VALUATION OF BIOTECHNOLOGY COMPANIES

Thesis submitted in partial fulfillment of the requirements of the MBA Program

Espoo, September 14, 2001

SUPERVISOR

Tomi Laamanen

Professor of Strategy and International Business

INSTRUCTORS

Saila Miettinen-Lähde Investment Banking, D. Carnegie Ab

Janne Aura Investment Banking, D. Carnegie

Mika Naumanen

Helsinki University of Technology

2

Helsinki University of Technology

MBA Programs

Abstract of the MBA Thesis

REAL OPTION MODEL FOR VALUATION OF BIOTECHNOLOGY COMPANIES

Margita Engström, Master of Science in Engineering Espoo, September 11, 2001

Number of pages

124

Supervisor Tomi Laamanen, Professor of Strategy and International Business

Instructors

Saila-Miettinen-Lähde, D. Carnegie Ab, Investment banking Janne Aura, D. Carnegie Ab, Investment banking

Mika Naumanen, Helsinki University of Technology

The purpose of this study was to apply a real option framework to valuation of biotechnology companies. The

study identified the weakness of traditional valuation methods as applied to immature industries to be the over-emphasis on risk and the inflexibility to act rationally as new information is acquired. Real option was

found applicable for valuation of biotechnology companies, as the analogy to financial options of the right but not the obligation to exercise was identified in development projects. Real options have been applied in

valuation of biotechnology companies and they are likely to add significant value due to high volatility and

long times to maturity.

The real option model produce was based on the binomial lattice methodology. The typical development project of a biotechnology company is analogous to an American financial call option. The portfolio of assets

could be modeled as an American or European call option in order to incorporate the realized effects (i.e. the volatility) on the market of similar (i.e. replicating) companies hence not only focusing on asset volatility. In

order to identify the effect of continuously compoundness a Black-Scholes valuation is applied. All real option

valuation methods described above were applied to case valuation of a typical biotechnology company.

The volatility parameter estimated in the study was calculated to be 82% based on the replicating portfolio method, which is used for ROV of the portfolio of assets. The volatility of individual asset, i.e. the revenue

distribution of asset was estimated out of the Decision Tree analysis and varied from 18…23% depending on

asset. The risk free interest rate was of today 5,06% and the time to maturity varied from 4…6 years depending on the drug development project.

The value of the company as of DCF were found to be 276,7 mEUR. The study identified an additional option

value of 73,6 mEUR based on individual valuations of each asset in comparison to the traditional discounted cash flow valuation. The Black-Scholes method results in an additional ROV of 1,31, which is the result of

underestimation of volatility effect. The valuation based on the portfolio of asset resulted in very similar

valuations as the corresponding base case valuations (0…3%), which is illustrating the effect on volatility on company value. The high volatility results in low asset values that are resulting from several subsequent

downward changes in asset value.

ROV add value to the valuation process. The main advantages of real option valuations are the quantification

of strategic value and a deep understanding of critical financial decisions that the company face.

3

ACKNOWLEDGEMENTS

I wish my to express my greatest gratitude to Saila Miettinen-Lähde at D. Carnegie Ab for giving me this challenging opportunity to such an interesting title for the thesis. I also am very grateful for her most

valuable input to the thesis and for her trust in me. I also wish to thank Janne Aura for his insights on the problems of valuation and for him sharing his experience on valuation.

Finally, I want to thank the supervising professor Tomi Laamanen and researcher Mika Naumanen for their valuable input and courage they have given me in order to complete the challenge of real option modeling.

1. INTRODUCTION 7

1.1 BACKGROUND INFORMATION 7

1.2 RESEARCH PROBLEM 7

1.3 OBJECTIVES OF THE STUDY 7

1.4 SCOPE OF THE STUDY 7

1.5 RESEARCH APPROACHES AND METHODS 8

2. BIOTECHNOLOGY INDUSTRY 9

2.1 THE BIOTECHNOLOGY INDUSTRY OVERLOOK 9 2.1.1 Innovation and intensive R&D 11 2.1.2 Technological pace 11 2.1.3 Uncertainty, risk and volatility 11 2.1.4 The regulatory approval process 12 2.1.5 Intellectual property rights 13

2.2 RECENT CHANGES IN THE BIOTECHNOLOGY INDUSTRY STRUCTURE 13 2.2.1 Financing 13 2.2.2 Separating from technology 15 2.2.3 The public and private financial markets for biotechnology companies 15 2.2.4 Strategic alliances 16 2.2.5 Biotechnological manufacturing capacity 17 2.2.6 The impact of size and structure as success factors of the biotechnology industry 17

2.3 BIOTECHNOLOGY INDUSTRY PROSPECTS 18 2.3.1 Technological jumps 18 2.3.2 Demographics change 20 2.3.3 Global financial markets 20 2.3.4 Technology trends affecting individuals 20 2.3.5 Trends in the biotechnology industry sector 20 2.3.6 The pharmaceutical market 21 2.3.7 Technological development affecting the industry 21

3. THEORY ON VALUATION METHODS 23

3.1 ASSETS BASED VALUATIONS OF COMPANIES 24 3.1.1 Yield capitalization method 24 3.1.2 Conclusions on valuation by accounting methods 25

3.2 MULTIPLES METHODS 25 3.2.1 P/E and P/D multiples 25 3.2.2 EBIT multiple 26 3.2.3 Free cash flow multiple 26 3.2.4 Historic and prospective multiples 26 3.2.5 Other quick methods for valuation 27 3.2.6 Conclusions on valuation by quick methods 27

3.3 DISCOUNTED CASH FLOW MODELS 28 3.3.1 Calculating the FCF’s over the explicit time horizon 28 3.3.2 Estimating the cost of capital 29 3.3.3 Calculating the continuing value (CV) 30 3.3.4 Discounting to present 31 3.3.5 Modified discounted cash flow methods (APV) 32 3.3.6 Conclusions on valuation by cash flow methods 32

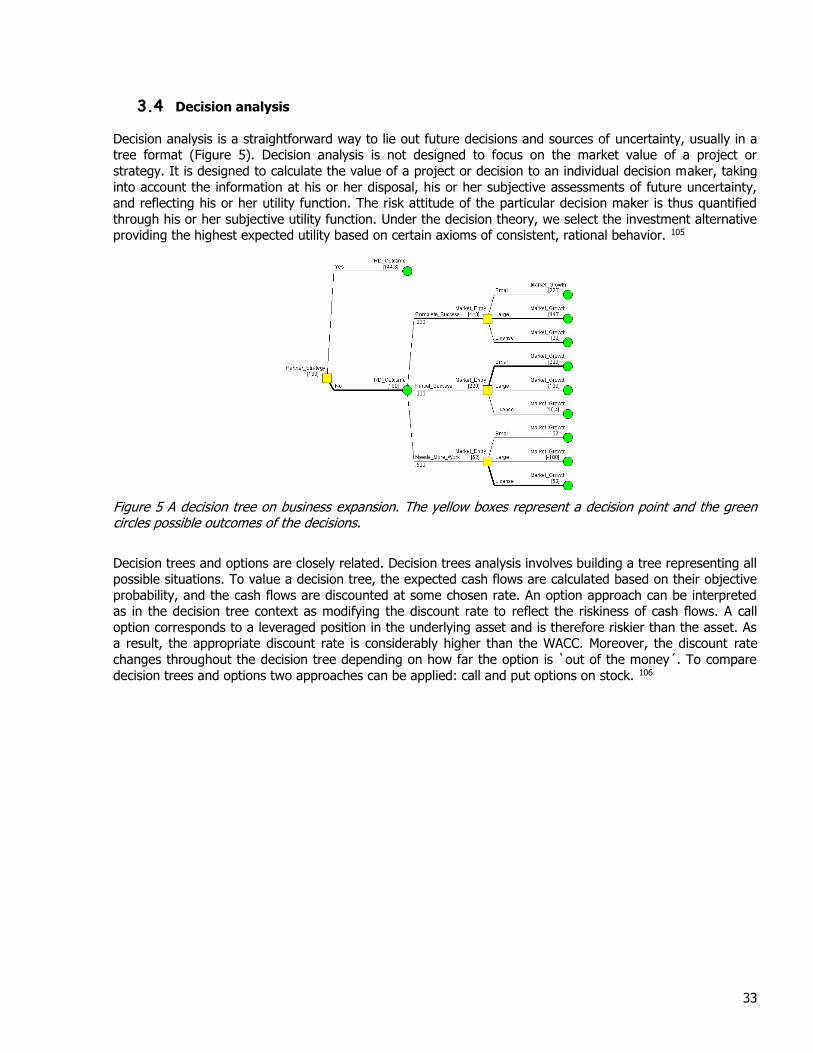

3.4 DECISION ANALYSIS 33

5

4. REAL OPTIONS 34

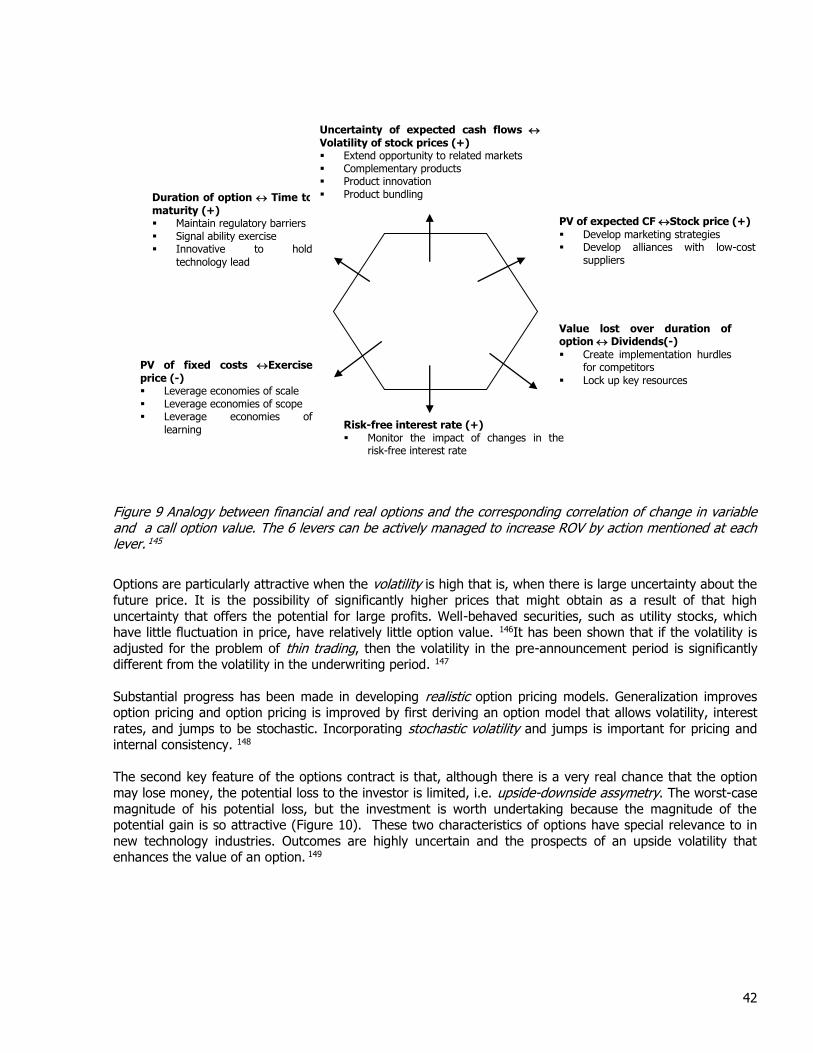

4.1 CLASSIFICATION OF REAL OPTIONS 36 4.1.1 Real options reflect value creation due to flexibility 38 4.1.2 Advantages and disadvantages of real options 40 4.1.3 Characteristics of real options 41

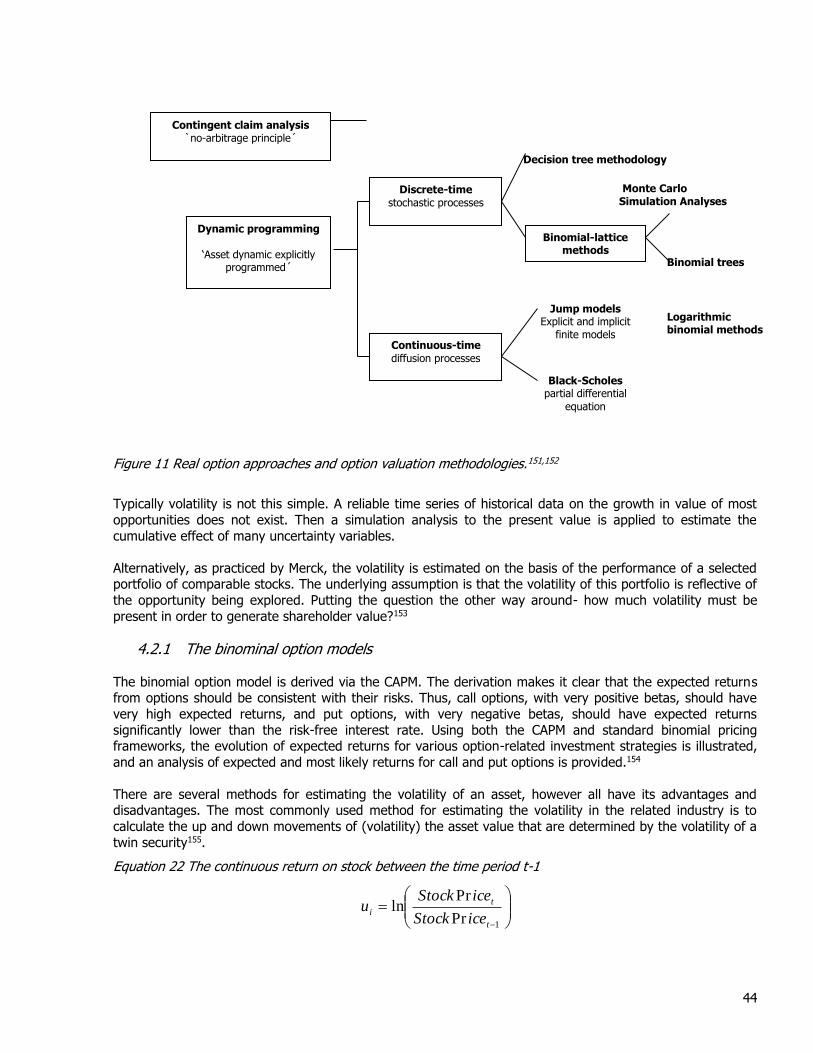

4.2 REAL OPTION VALUATION FRAMEWORKS 43 4.2.1 The binominal option models 44 4.2.2 The Black-Scholes option valuation model 46 4.2.3 The Jump model 47 4.2.4 The Monte Carlo approach 47 4.2.5 Complex real option models 48 4.2.6 Real option applications 49 4.2.7 Conclusions on real option valuation 52

5. VALUATION OF BIOTECHNOLOGY COMPANIES 53

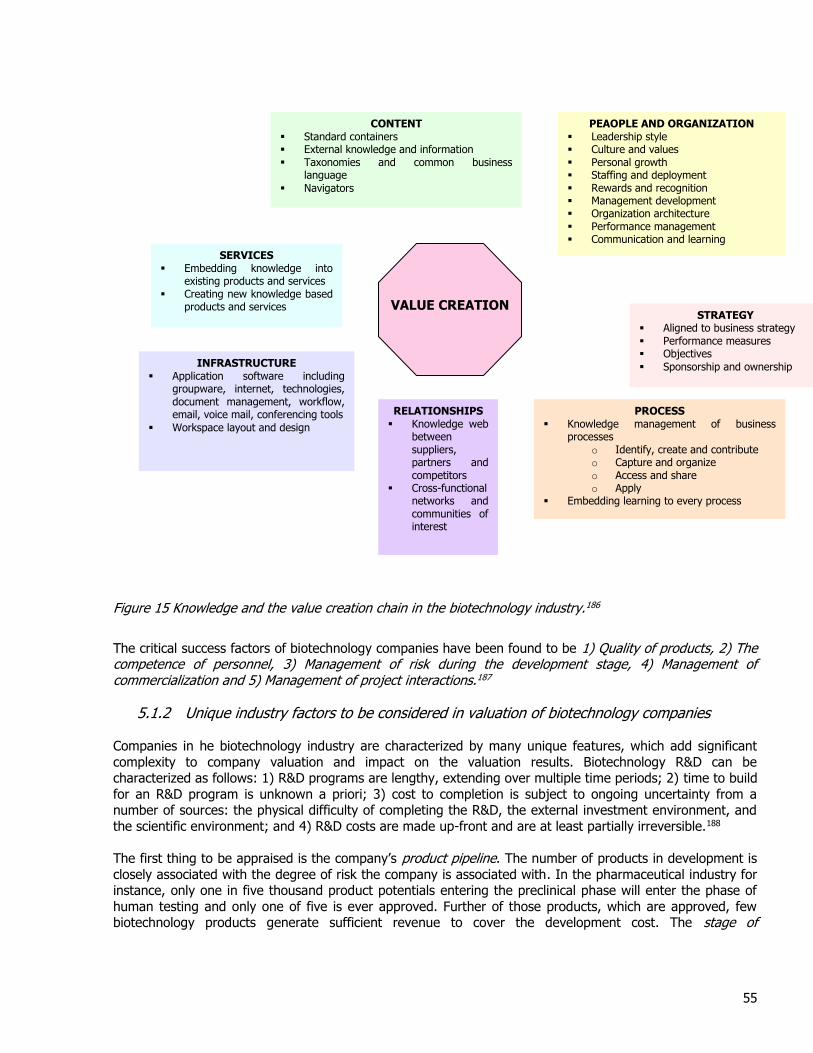

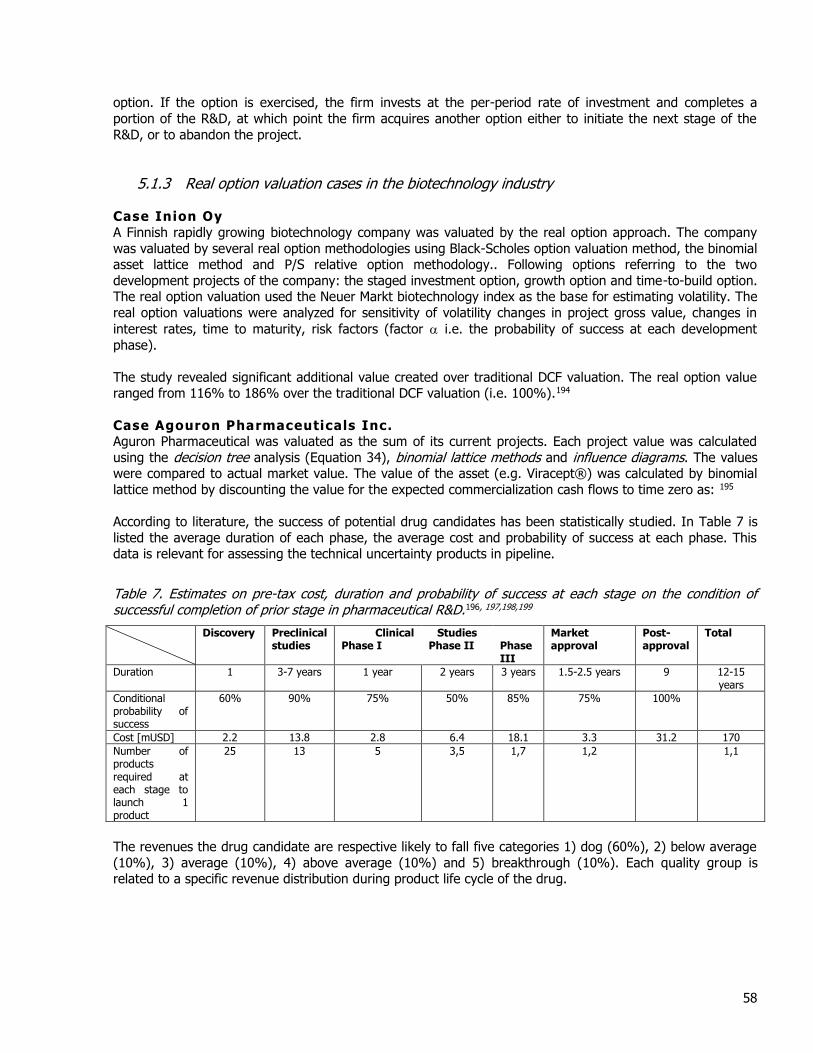

5.1 VALUATION ASPECTS IN THE BIOTECHNOLOGY INDUSTRY 54 5.1.1 Biotechnology value creation and critical success factors 54 5.1.2 Unique industry factors to be considered in valuation of biotechnology companies 55 5.1.3 Real option valuation cases in the biotechnology industry 58 5.1.4 Conclusions on factors affecting biotechnology valuation 60

5.2 ANALYSIS OF THE CASE COMPANY BIOTIE THERAPIES OYJ 62 5.2.1 The technology strategy of the case company 62 5.2.2 The market for selected target areas 63

5.3 DEVELOPING A REAL OPTION MODEL FOR VALUING A BIOTECHNOLOGY COMPANY BASED ON OPTION THEORY 64 5.3.1 Applicability of real option methodology in valuation of biotechnology companies 64 5.3.2 Assumptions for the valuation model on forecasted cash flows 66 5.3.3 Assumptions underlying the real option valuation model 67 5.3.4 The real option method applied 68

5.4 STARTING POINT FOR THE BASE CASE VALUATION 70

5.5 VALUATION OF THE CASE BIOTECHNOLOGY COMPANY WITH REAL OPTIONS 70 5.5.1 The parameters estimated for real option valuation 70 5.5.2 Variables of the replicating portfolio for estimation of company volatility 71 5.5.3 The asset volatility of a drug under development 71

6. RESULTS OF THE CASE STUDY 72

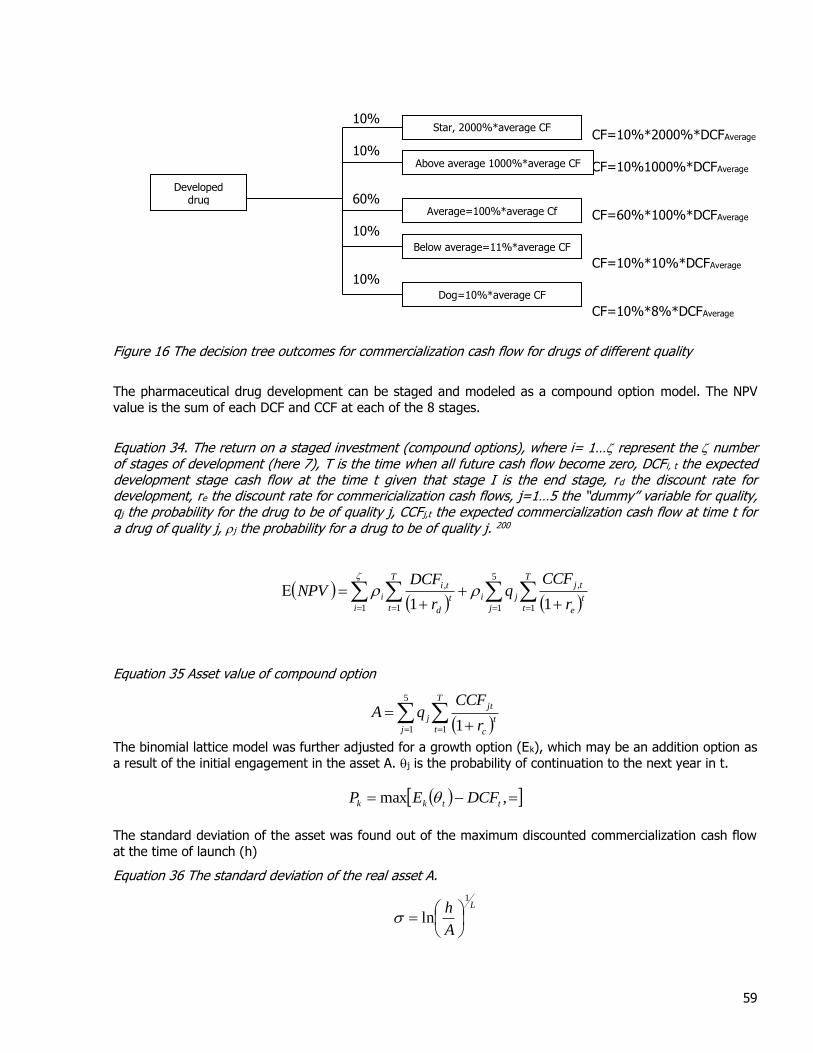

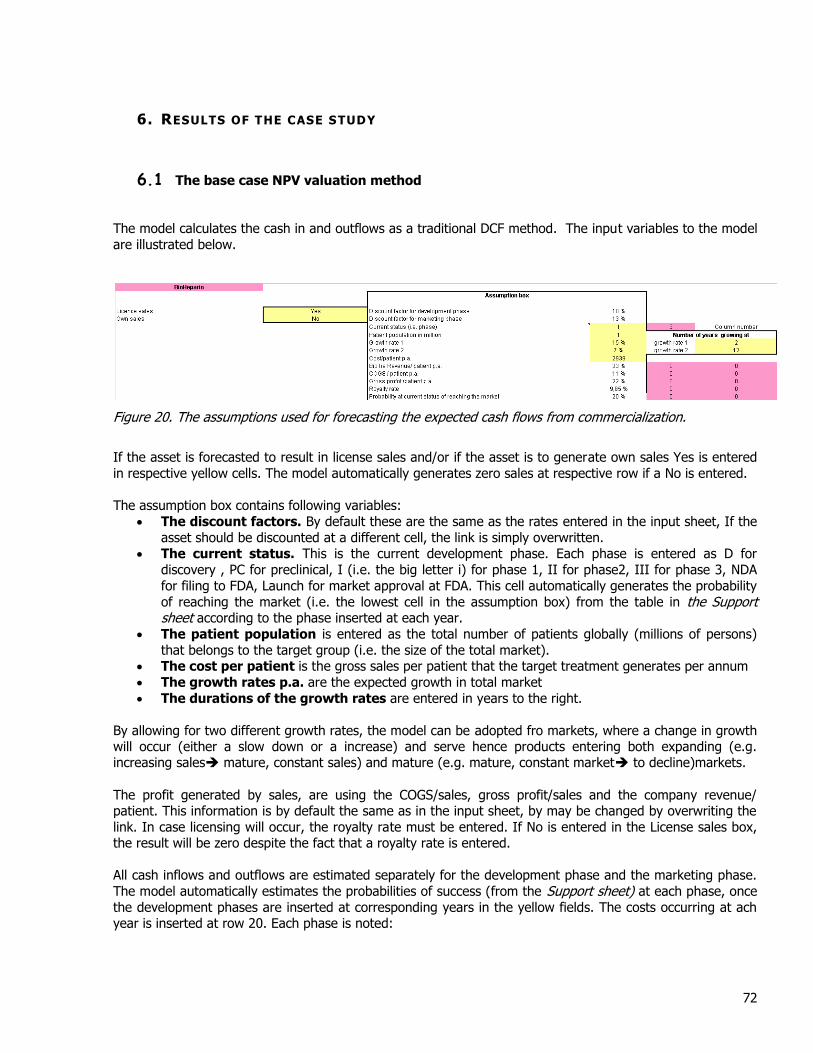

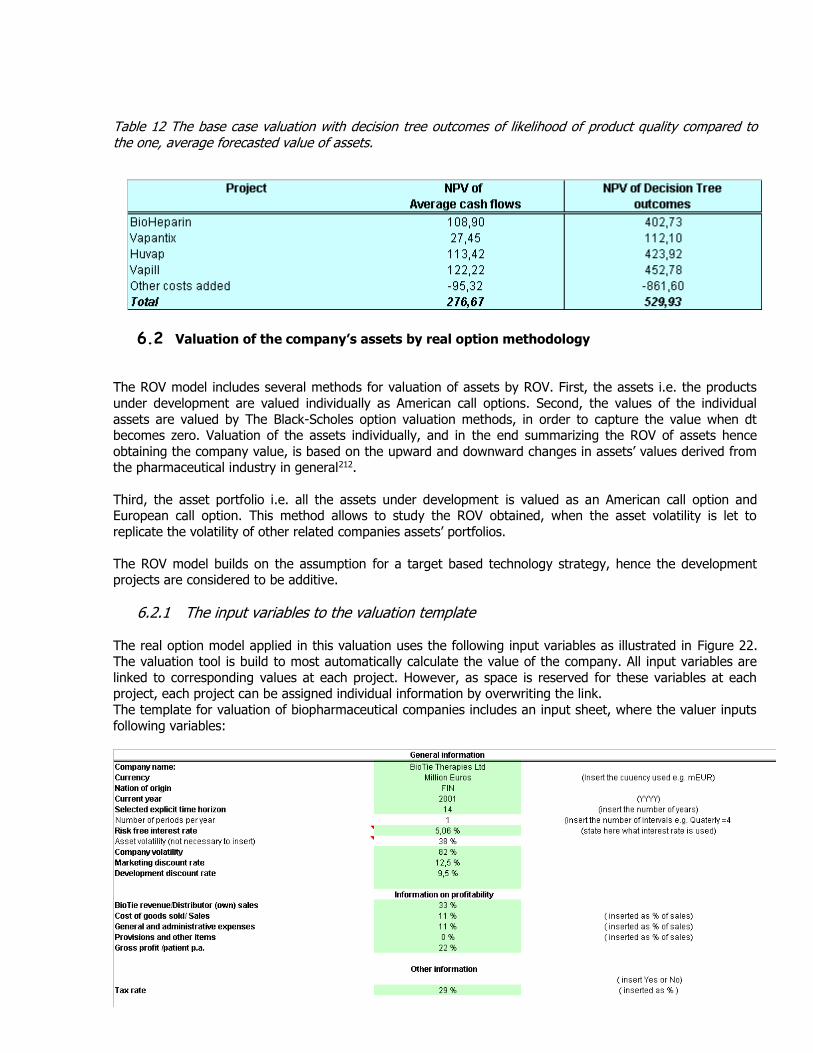

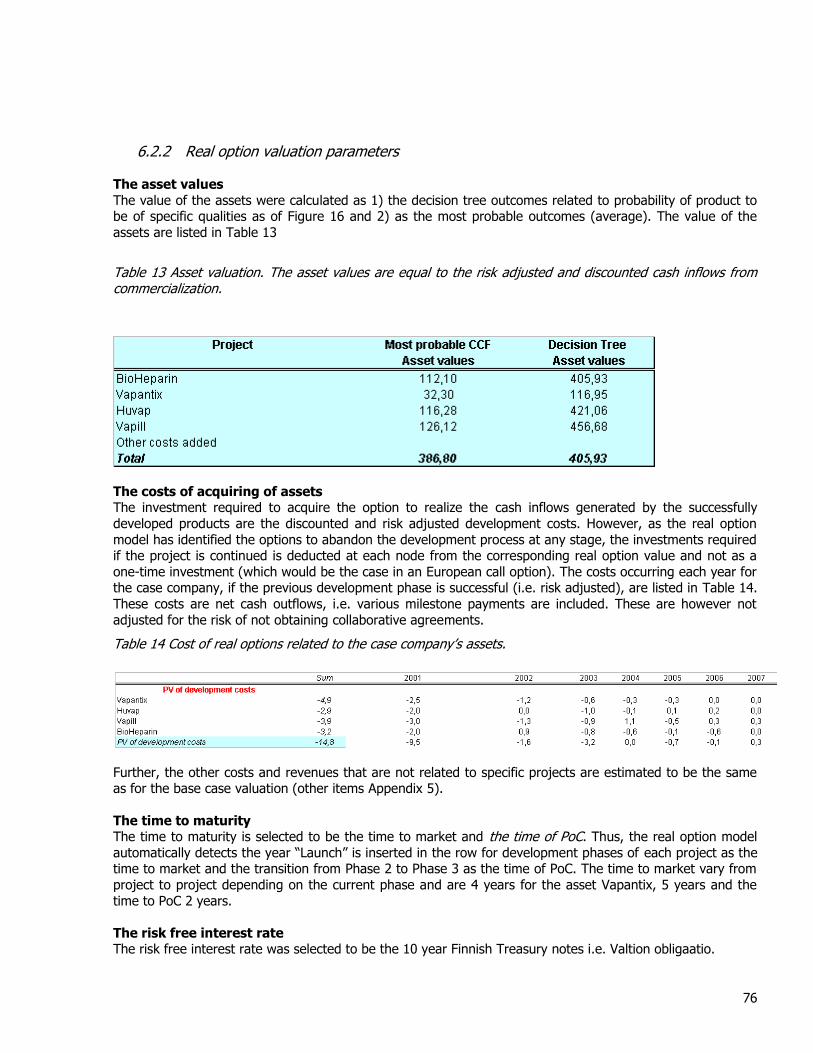

6.1 THE BASE CASE NPV VALUATION METHOD 72 6.1.1 The result of the base case valuation (NPV) 73 6.1.2 The base case valuation with Decision Tree outcomes of commercialization cash flows. 73

6.2 VALUATION OF THE COMPANY’S ASSETS BY REAL OPTION METHODOLOGY 74 6.2.1 The input variables to the valuation template 74 6.2.2 Real option valuation parameters 76 6.2.3 Derived real option parameters 77 6.2.4 The ROV of all asset individually by the binomial method as American call options 78 6.2.5 ROV of all assets individually by the Black-Scholes method 78 6.2.6 ROV of the entire portfolio of assets 79

6.3 RESULTS OF THE REAL OPTION VALUATION 80 6.3.1 Valuation of the company as the sum of the individual assets by the binomial method 80 6.3.2 Valuation of the company as the sum of the individual assets by the Black-Scholes option valuation method 80 6.3.3 Valuation of the company based on a portfolio of most probable assets values 81 6.3.4 Valuation of the company based on a portfolio of decision tree outcomes of asset values 81

6

6.3.5 Comparison of the results 82 6.4 SENSITIVITY ANALYSIS 84

6.4.1 Sensitivity with respect to the volatility parameter 84 6.4.2 Sensitivity with respect to the risk free interest rate parameter 85 6.4.3 Sensitivity with respect to the time to maturity parameter 85

6.5 RELIABILITY ANALYSIS 86

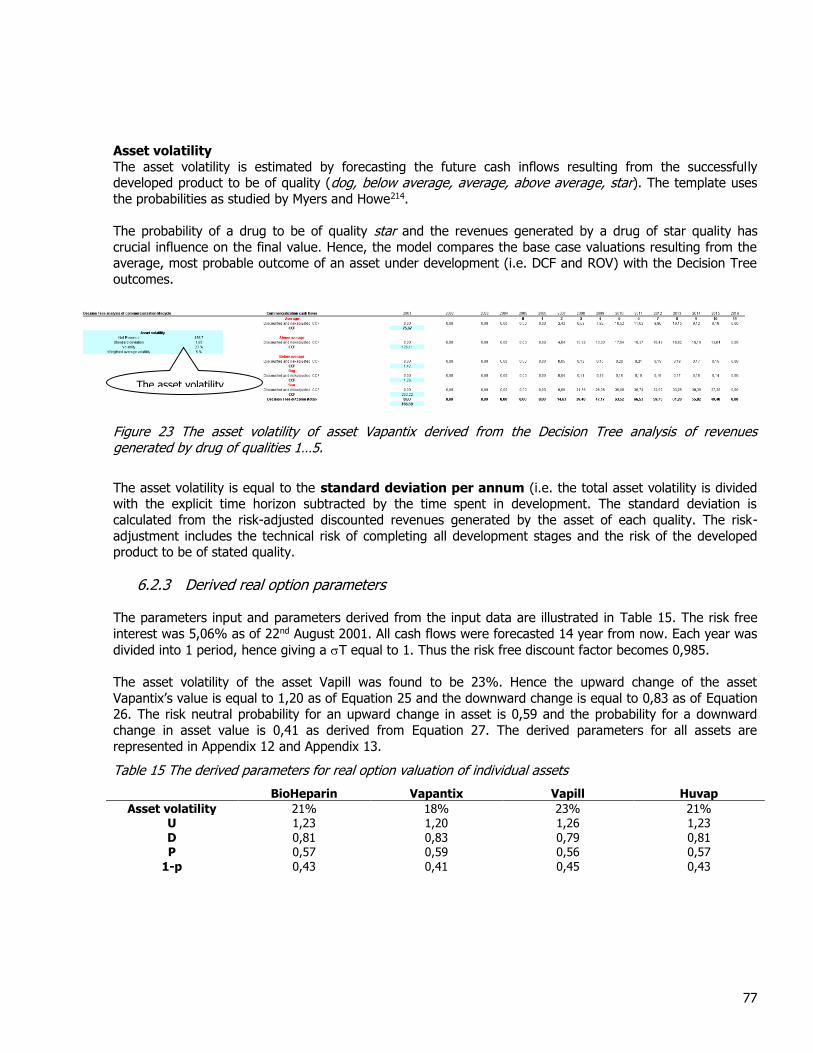

6.6 CONCLUSIONS ON REAL OPTION VALUATION 86

7. SUMMARY 88

Appendices

References

7

1. INTRODUCTION

Biotechnology is a rapidly growing industry in early stage. Valuation of biotechnology companies is difficult

because most companies still have their products in the development phase hence having no or negative revenues. The business and technology environments are highly dynamic and risky thus neither the products

nor the markets for the products exist.

1.1 Background information

Biotechnology firms include many different types of companies. In general, biotechnology firms are defined as any firm using biotechnology in R&D, manufacturing of products such as genetic products, proteins,

biopharmaceuticals, medical devices, services and bioinformatics. The biotechnology industry is characterized

as immature and highly uncertain and the main assets lie in intangibles such as knowledge and expertise. Biotechnology companies typically make huge upfront investments, opening a wide array of opportunities to

exploit the great many inventions.

Traditional valuation methods tend to overemphasize risk, as the huge array of opportunities cannot be

properly incorporated in the valuation method as the value of opportunities that are rights not obligations to take action nor do the traditional methods valuate flexibility to take action as events unfold. Real option

models properly express the uncertainty, risk, and the option to pursue from a great array of opportunities.

1.2 Research problem

Traditional valuation methods tend to focus on mature businesses and the tools used for valuation of mature

having positive revenues. The most frequently used valuation method is the discounted cash flow method, where a discount factor is used to reveal risk to return. However, this approach is not considered appropriate

for valuation of businesses that highly dynamic and immature since the same discount factor is not to be

used for products under development facing development risks and revenues from product sales associated with returns to market risk, since these risks are different. Discounted cash flow method fail also to reflect

the ability to respond to changes in technology and market, it simply assumes that the project is forecasted concerning its duration, cost and possible revenue generation once and it gives no room for management’s

flexibility. Further, high discount rates reflecting high uncertainty and risk reduces the valuation too much in

order to conduct businesses efficiently. If low valuations are obtained for biotechnology companies, the risk for them not obtaining sufficient funding to maintain a product pipeline will occur and promising development

projects might not get spotted.

1.3 Objectives of the study

The main objective of the study is to build a real option model for valuation of biotechnology companies. The study will explore and compare traditional valuation methods used for valuation of biotechnology firms such

as multiples methods, discounted cash flow methods and other net present valuations. In order to build an option model for valuation biotechnology companies, the industry and company characteristics and structure

must be analyzed properly in order to identify factors affecting valuation. These factors will be applied in a

real case valuation in order to demonstrate the applicability.

1.4 Scope of the study

The study will briefly explore different valuation methods in valuation biotechnology companies. The emphasis is on comparing the strengths and weaknesses of diverse valuation techniques in relation to real

8

option valuation. The study will focus on identifying industry specific factors affecting valuation and methods

for incorporating these into the real option valuation context.

1.5 Research approaches and methods

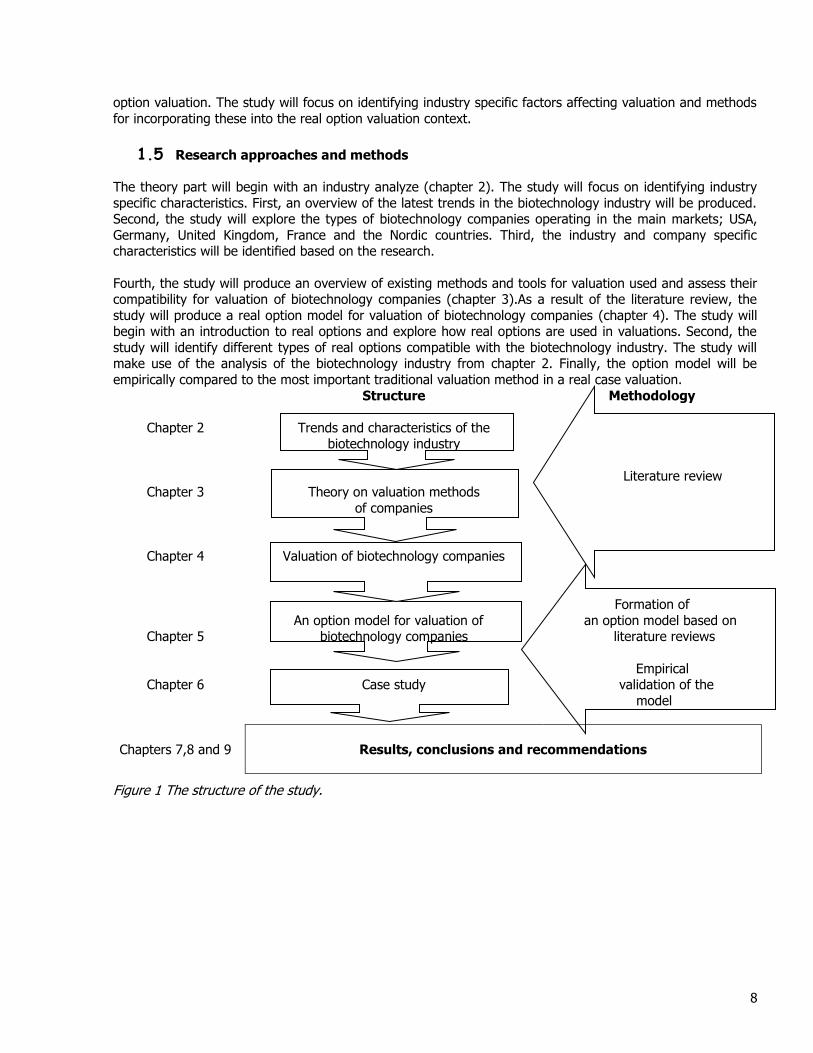

The theory part will begin with an industry analyze (chapter 2). The study will focus on identifying industry

specific characteristics. First, an overview of the latest trends in the biotechnology industry will be produced. Second, the study will explore the types of biotechnology companies operating in the main markets; USA,

Germany, United Kingdom, France and the Nordic countries. Third, the industry and company specific characteristics will be identified based on the research.

Fourth, the study will produce an overview of existing methods and tools for valuation used and assess their compatibility for valuation of biotechnology companies (chapter 3).As a result of the literature review, the

study will produce a real option model for valuation of biotechnology companies (chapter 4). The study will begin with an introduction to real options and explore how real options are used in valuations. Second, the

study will identify different types of real options compatible with the biotechnology industry. The study will make use of the analysis of the biotechnology industry from chapter 2. Finally, the option model will be

empirically compared to the most important traditional valuation method in a real case valuation.

Structure Methodology

Chapter 2

Trends and characteristics of the biotechnology industry

Chapter 3

Theory on valuation methods

of companies

Literature review

Chapter 4

Valuation of biotechnology companies

Chapter 5

An option model for valuation of biotechnology companies

Formation of

an option model based on literature reviews

Chapter 6

Case study

Empirical validation of the

model

Chapters 7,8 and 9

Results, conclusions and recommendations

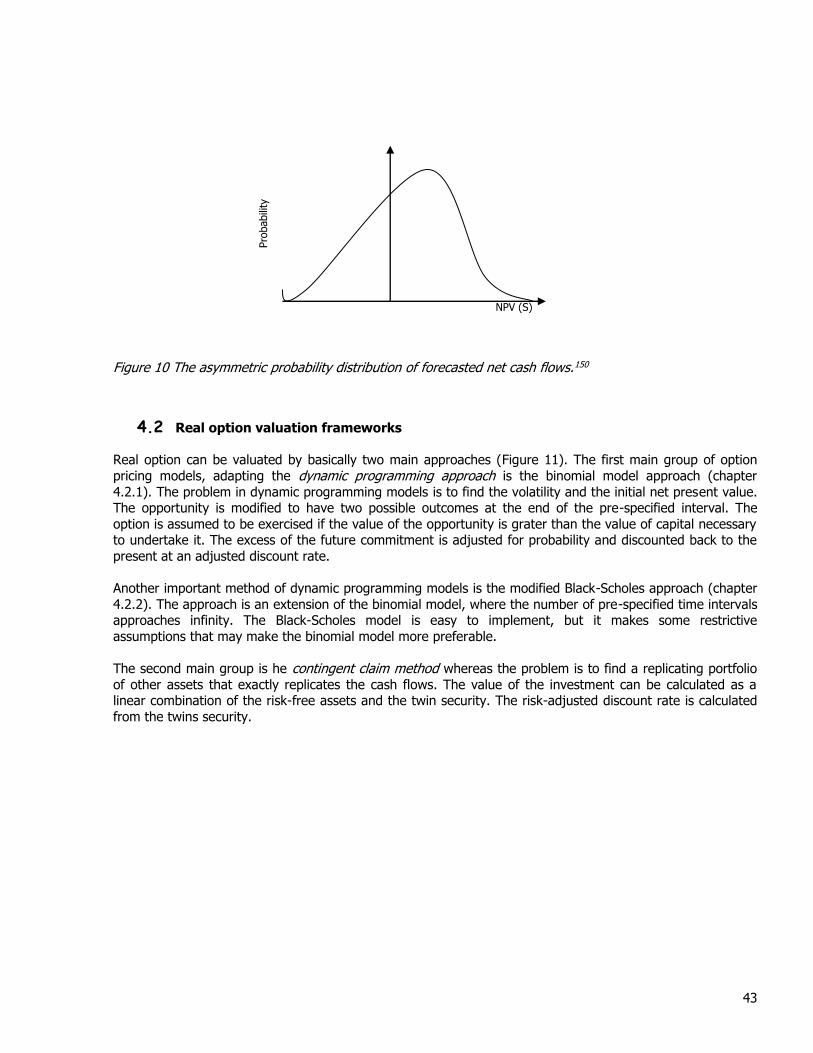

Figure 1 The structure of the study.

9

2. BIOTECHNOLOGY INDUSTRY

Companies offering enabling technologies were a driver behind this increased financing. The most significant

trend in the biotechnology sector last year was "the effusion of stocks with enabling technologies," explains Eric Schmidt, analyst with SG Cowen. These technologies include functional genomics, proteomics,

bioinformatics, pharmacogenomics and directed evolution.

The general perspective of the health of the industry also affects financing to the biotechnology sector. SG

Cowen analyst Mr. Schmidt says that previously demonstrated success of biotech firms has aided in reducing the investment perception that the biotechnology industry is merely speculative. 1

2.1 The biotechnology industry overlook

So far in 2001, the healthcare services sector has replaced biotech as the darling of Wall Street's healthcare

bankers. That hardly means that the days of biotech are numbered-after all, gene research is still in its infancy, in many ways-but it does mean that capital is flowing into what has rapidly morphed into a sizzling

sector that includes hospitals, nursing homes and managed care companies, among others. The shift to

healthcare services from biotech may result in some scrambling among firms trying to assemble teams in this sector, which has largely been ignored by the Street for the past three years. Merrill Lynch & Co., Banc of

America Securities, Lehman Brothers and CIBC World Markets all report having healthcare services deals in the pipeline. Deals include standard equity and debt offerings and, increasingly, convertibles. Peter Crowley,

who runs healthcare banking at CIBC, added that specialized medical facilities for treating heart disease and orthopedic ailments, for example, are also experiencing a growth spurt, and probably will seek funding

sometime this year. The threat of economic recession and the precipitous decline in high-growth technology

stocks have increased investors' appetite for non- cyclical safe-haven stocks like healthcare services.2

The advances that are the result of genetic engineering, diagnostic techniques, and cell/tissue techniques will surely change our world and our lives. We have already observed the importance and results of biological

techniques in developing products and services that serve the needs of human health care or animal health,

agricultural productivity, food processing, renewable resources and environmental affairs.3

Biotechnology consist of a variety of applications. The medical related biotechnology sector consists of following segments:

1. Biopharmaceuticals . Companies in this segment discover and develop proteins, antibodies, and small molecules for potential drug treatments. Biotech companies have over 300 compounds in

human clinical trials, and as these products are approved in the next few years, more and more are

going to become profitable. In addition, the time required to create and test a drug will go from the current 10 to 15 years to under two years; the failure rate will drop to less than 20 percent.

2. Pharmaceutical companies starting to access biotechnology. Traditional pharmaceutical companies will do well in the next decade. Most large drug companies have formed joint ventures or

affiliations with biotech firms, to tap their capabilities. Demographics will also play a role. Aging baby

boomers will increase the demand for medicines and treatments." 3. Genomics: the study of genes and their functions. The genes involved in disease are likely to be

few in numbers. Hence the competition to discover these genes and to gain intellectual property is intense. The research on the genetic basis for diseases is intense. Many illnesses are caused is of

genetc origion or caused by genetic damage. Diseases may be treated by gene therapy (premises for

treatment of cancer) or other short genetic treatment. 4. Proteonomics: proteins decoded by the genes are usually the real targets of the therapeutics.

Consequently, the characterization of the proteins, rather than the gene, protein expression and protein function is a starting point for drug development. Many proteins (e.g. albumin, clotting

factors, insulin, enzyme replacements) are needed for medical treatment. These proteins is be produced today more cost-efficiently and of better quality by genetic engineering.

10

5. Antibodies are developed as therapeutics, diagnostics and as a tool for identification of the targets

yieled by genomics and proteomics. Antibodies is one of the most important area in biotechnology

due to their flexibility, specificity and they are not rejected by the immunity system. Monoclonal humanized antibodies are being developed (Mab) and produced by various techniques (e.g. the use

of transgenetic manufacturing cells, phage display 6. Services. Insurers, hospitals, managed care companies, and ancillary services will be profitable in

the coming year. The hospital stocks are tought to l outperform every other health care sector in

2001." 7. Medical supplies. This category includes devices that are implanted in patients, used to monitor

and diagnose conditions, or used to discover and test new drugs and gene products. 4

8. Bioinformatics. Computer science will play a key role in biotechnology development.

By matching the chemical structure to the biological activity and protein interaction and

hence producing chemical libraries the probability of drug discovery is increased.

Bioinfomatics enable faster screening technologies for genomics and proteonomics.5, 6, 7 The size of each segment can be approximated for the venture capital funding in 1999 (Figure 2).

Figure 2 Breakdown of 1999 venture financing8

At the beginning of a new century, European countries have made progress in breaking down economic and

political boundaries to enable an integrated approach to common problems. Efforts to create pan-European systems include the introduction of a single currency, the Euro, to integrate the economies as well as the

formation of regulatory boards to minimize duplication. Yet, an important question lingers: Will Europeans have access to the best health care possible, including the latest technology and prescription drugs? This

paper presents a brief overview that policymakers can use to reflect on this critical task.9

Indeed, it also means that many more biotechs will be in-licensing technologies from their smaller brethren,

which is a new role for a lot of European companies, bringing with it the prospect of a withdrawal from dependency on big pharma. However, that does not mean the pressure is off entirely. One of the biggest

developments in the European biotech industry last year was that it partially uncoupled itself from the general technology malaise that dragged the equity markets down in the latter part of 2000. 10

Health care services

and sysems

2 %

Software

17 %

Biopharmaceuticals

3 %

Communications&Net

working

21 %

Medical devices

4 %Other IT and IS

18 %

Retail and other

35 %

11

While nations demonstrate interest and motivation in systems designed to meet the needs of their citizens,

disparities in care and inefficiencies exist among European nations. This is particularly true in areas that offer the greatest potential for innovation.

Nor will there be enough capacity anytime in the near future. Fermentation and purification facilities are very

expensive, ranging from $50 million to $400 million each, and they take several years to bring on line. Its not

a cheap method of production. It's not only the equipment which must be precision-engineered to high standards, but the plant must be located in a housing which is biologically sterile and has been validated by

regulatory authorities such as FDA. Chemical synthesis plants for the production of pharmaceutical active ingredients must also be validated by regulatory authorities, but the design conditions are not as stringent as

for a biological plant. Fermentation and cell culture have proven their commercial viability; transgenics, a very different vehicle, has yet to bring a product to market. That day may not be far off, however. Based on

the types of inquiries we are getting, there is increased activity there. Companies such as PPL Therapeutics,

Pharming, and Genzyme Transgenics Corporation (GTC) all have products obtained from transgenic animals in development.11

It is clear that we have entered what is being called "the Biotechnology Century”. While biotechnology has

been around for some time—there are those who date it from the earliest production of wine and bread

10,000 years ago—the medical, agricultural, and environmental benefits of biotechnology in the years to come will be nothing like those that preceded them.

As biotechnology evolves, data management, intellectual property, and privacy issues will have to be

addressed so that the result of the product development can be realized by the public. Biotechnology is advancing rapidly, making it difficult for regulations and policies to keep up, and advances raise ethical,

political, and public concern - not unlike those faced by the nuclear industry. To be successful, public

education about biotechnology is essential.12

2.1.1 Innovation and intensive R&D

U.S-based companies have more than doubled their research and development expenditures since 1990, when collectively they spent $8.42 billion. The major pharmaceutical companies are expected to invest more

than $28 billion in research and development (R&D) in 2001.13 These sustain a rate of progress in sciences,

at the interface of biotechnology and materials research, promises plenty of exciting opportunities14. But investing wrong can be costly but it can also lead to a profitable business as one of the world's largest

biophamaceutical contractors (as an example due, in part, to a major regulatory development).15

2.1.2 Technological pace

Speed throughout the whole innovation chain is a prerequisite to success. There is no shortage of good ideas

wherever well-trained chemists and biologists are working on biocatalysis. However, the ability to convert ideas into products quickly is crucial.16

2.1.3 Uncertainty, risk and volatility

The biotechnology sector experienced significant volatility in 2000. The Nasdaq Biotechnology Index

composite dropped 18 percent in 2000. In contrast, the S&P 500 index dropped 9 percent during the same

time. The biotechnology sector did not match the volatility of Nasdaq, which dropped an unprecedented 64 percent in 2000. The Nasdaq Biotechnology Index reached its height in the first quarter of 2000 with a

trading composite of 1596.53 points. This represented a 48 percent differential between the high and low.

When investing in biotech, first recognize that the risk is heavy. Genomic businesses have no or minuscule

profits and astronomical stock valuations17. Although scientific advances offer great promise in the

12

development of new medical therapies and new ways to test and produce these products, regulators and

manufacturers acknowledge that scientific data cannot resolve all controversies. Despite increased

understanding of the function and therapeutic capacity of proteins and monoclonal antibodies it has been acknowledged that it may be difficult to anticipate the effects of product and process changes on subsequent

clinical performance.18

2.1.4 The regulatory approval process

In the EU countries the European Medicines Evaluation Agency (EMEA) evaluates the New Drug Applications.

In each country there is a National Agency of Medicine which has to be notified of the investigational new drugs and which audits the quality of manufacturing facilities and procedures. In the United States the

corresponding authority is the Food and Drug Agency (FDA).

The Food and Drug Administration has begun to expeditiously review new pharmaceutical products at a

highly efficient level. FDA approval times were 20% faster in 1998 than 1997, and the median time has decreased from 8.9 to 6.9 months. In 1998 the agency approved 39 therapeutic drugs. The FDA is expected

to receive another $600 million to increase efficiency through streamlining the regulatory process.

There is now no established regulatory pathway for approving generic, or multi-source, biotech drug products. A part of the reason is that the biotechnology industry followed the establishment of procedures for

generic drug introduction. The biotech industry was still in its infancy when the generics industry as it is

known today was established through the 1984 Hatch-Waxman Act (Drug Price Competition and Patent arm Restoration Act of 1984). Branded manufacturers achieved patent extension terms in exchange for

implementation of a regulatory pathway for approval of generic drugs based on chemical entities. However, biotech drugs were not part of these reforms. Hence the only way for multi-source biotech to be approved is

by a virtual repeat of the pre-clinical and clinical testing, even if the comparator drug is physically and

chemically identical to the innovator. The current differences in review and approval processes for new drugs versus biologics will most likely extend to their generic counterparts. The multi-source biotech manufacturers

may spend considerably more time in process development, characterization, and validation than for a chemically derived drug product. The Food and Drug Administration's (FDA) regulatory philosophy shifted

and allowed greater flexibility for scale-up and post-marketing changes, based on demonstrating comparability.19

Historically, there has always been a well defined separation of drug (Table 1) versus biologics law and regulatory guidance. Thus, it is understandable that biologics- approved under the Public Health Service

(PHS) Act-were not included in the formal abbreviated new drug application (ANDA) process that was used for approval of chemical-entity based drugs under Section 505 of the Food, Drug and Cosmetic (FD&C) Act.

However, that classic distinction has been blurred with the evolution of recombinant DNA products reviewed

and approved under FDAs Center for Drug Evaluation and Research (CDER). FDA is divided into two centers-CDER and the Center for Biologics Evaluation and Research (CBER)-that handle drug evaluation and approval

of new entities. Within CDER is the Office of Generic Drugs (OGD), the only group with review and approval capacity for generic drugs. CBER has responsibility for approval of new biopharmaceuticals but has no

process for approval of generic biopharmaceuticals. It is not clear whether multi-source biologics would be handled by a CBER equivalent of CDER or if CDER would expand to include biologics. Approval of a generic

biologic requires the existence of an approved innovator product under the FD&C Act or the PHS Act. The

notion of multi-source biotech stretches it further in terms of administrative review and consistent approaches. 20

Table 1 Drug development in most western jurisdictions follows essentially identical procedures and is subject to similar regulatory systems.

1. Basic research. In this phase most development of pharmaceuticals begin with studies of the biological origins of an illness, which leads to a method of treatment by a new pharmaceutical

13

2. Preclinical stage. In the preclinical phase the substance are tested in terms of their effect and their

toxicity in animal studies. Comparisons with existing treatments are made to gain an indication of the

development potential. Successful preclinical work leads to an application to begin clinical trials. The Investigational New Drug (IND) application is made to National Agency for Medicines, whereas upon

acceptance clinical trials can be initiated. 3. Clinical phase.

a. Phase I. The purpose is to identify the highest dose of the substance being tested which

can be administered to patients in phase II, without serious side effects. The trials also study how the substance is distributed and how it is metabolized. The phase I studies take

approximately 1 year. b. Phase II. The purpose of the phase II studies is to identify the relationship between a

certain dose and the negative effects to the patients. The phase II testing takes approximately 1 to 3 years.

c. Phase III. Before the phase III testing is initiated, the drug candidate has demonstrated

that the substance has the intended clinical effect and that the frequency, intensity and the nature of its side effects are acceptable in the relation to the disease intended to be treated.

In phase III it is tested that the substance has statistical significance. The phase III studies are the most time consuming and expensive phase of clinical trials.

The development of other biotechnology products can be described as analogous to the development of pharmaceuticals. The development of new products begins with a discovery type phase, resulting in a

prototype product or a product produced in tube-type scale. Next, in the development phase the product is produced in the next scale and technical and customer specifications are produced. The product is subject to

validation testing on technical performance once produced in a larger scale than the discovery phase. When the development phase is successfully completed, the product is produced in next scale-up and subject to

evaluation testing, in which the product is tested to meet up with customer’s requirements in customer

environment. Once the evaluation is completed, the product is filed for registration at the national authority.

2.1.5 Intellectual property rights

A key contributing factor to the success of the biotechnology industry is the availability of a solid platform for protection of intellectual property rights. In 1998, the EC legal Affairs Committee approved the European

Directive for Biotechnological inventions and it has been translated to the Community Patent Convention. It is

wishf7ul that the national rules will be harmonized as a pan-European biotechnology patent law would help promote the success of the biotechnology industry. 21

2.2 Recent changes in the biotechnology industry structure

From the focus on the key events of 1998 and their impact on the sector, issues in six areas define the past

year's calendar and point to possible and emerging ways forward. Accordingly, the study need to look in-depth at strategic alliances, technology trends, financing, management, newsflow, intellectual property and

ethics.

2.2.1 Financing

Biotechnology has revolutionized drug development and pushed medical stocks into a growth sprint that will

likely become a marathon. Just look at 2000, a year when the bull market ended for most sectors: Though the Standard and Poor's 500 Stock Index lost 10.2 percent and the Nasdaq plummeted a heart-stopping 39.3

percent, medical stocks gained 26.9 percent. Biotech companies are where computer-chip manufacturers

were five years ago. Continuing progress will make the health care sector the fastest growing and most profitable of the decade. Emerging markets will help boost the sector. As worldwide standards of living

increase, health care spending in less-developed countries will pick up. In general, the biotechs are better investments than the human genome concerns [which create strings of genomes to study]. Many of the

14

genomics companies have a concept, but no profits. Many biotech companies have already turned a gene

product into a tangible compound. 22

Following a record year in 2000, analysts are cautiously optimistic over biotechnology for this year. Last year

saw record financing, the largest single-day decline in valuation, and one of the largest public offerings. Although not matching last year's performance, analysts see a fairly strong investment flow into the biotech

sector. The increased confidence in the biotech industry was reflected in higher investment levels into the

sector. Total funding for 2000 tallied $31.77 billion, compared to $10.72 billion in 1999, a 196% increase. The most significant trend in the biotechnology sector last year was the effusion of stocks with enabling

technologies. The increased confidence in the biotech industry was reflected in higher investment levels into the sector. Total funding for 2000 tallied $31.77 billion, compared to $10.72 billion in 1999, a 196 percent

increase. Public financing (which includes initial public offerings, secondary public and convertible debt) accounted for 78 percent of the total amount raised. The year-over-year funding for IPOs increased 843

percent, secondary public financing increased 118 percent, and convertible debt financing increased 277

percent. Private financing also increased dramatically in 2000. Specifically, private placements increased 183 percent, and venture capital funding increased 165 percent. Partnering with large pharma increased 30

percent year-over-year. 23

Companies, which under normal circumstances would not have been able to receive financing, benefited

from the receptive climate in the investment banking community. However, the declining equity performance of the early stage companies by the end of the year caused the investment banking community to become

more cautious. The reduction of available cash will cause an. acceleration of mergers and acquisitions. Since equity and debt will be more restrictive in 2001. Investments will be redistributed to commercial-stage

biotechnology firms. Not only will investment in 2001 be channeled to the more established biotech firms, the established biotech firms will have to reprioritize their spending. 24

The current and projected financing environment will require that commercial-stage biotechnology firms redirect their development efforts away from traditional research and development spending to acquisition of

existing technologies and products. Large cap pharmaceuticals used mergers and acquisitions to expand their product and revenue base. There will be a greater number of mergers and acquisitions in the biotechnology

sector for 2001. 25

Continued growth in the European Life Sciences sector has seen revenues increase 36% to 3.7 billion euros

in 1998. But in light of this growth and the widespread uncertainty affecting the industry, the need to communicate value to investors - and society at large - must be tackled with speed and agility by biotech

companies. As findings reveal, the need to highlight and communicate value to all stakeholders - strategic

partners, the public and investors - tops the agenda. Public and political debate require dedicated engagement, and newsflow management must be a core competency for biotech companies.

This US-European difference has arisen due in part to a dramatic disparity in the level of investment in the

two industries. Comparative advantage based on resource endowments cannot explain United States (U.S.) leadership in biotechnology. Sources of heterogeneity within the process of research and development

(R&D) investment, such as international differences in the maximum per-period rate of investment and

regulatory uncertainty, offer a plausible explanation that can be incorporated into a real options approach to investment. 26 Despite the 2000 funding boom, European companies have historically been drip-fed cash,

while their US counterparts have been given sufficient funds. This allows the leaders of these organizations to focus on building the business, rather than sorting out one funding round after another or being forced to

tighten the purse strings to such an extent that they are simply left behind.27 The performance of the

European biotechnology companies 55% under-performed the Nasdaq biotechnology index in 199928.

15

2.2.2 Separating from technology

Despite a 39 percent fall in NASDAQ over the year, European biotech share indices were up 50-75 percent.

Although momentum investors will always produce wild swings, there is some evidence investor attitudes are maturing and investors are beginning to view companies in the sector as entities in their own right rather

than an amorphous group called 'biotech'. Analysts have started to apply old-fashioned criteria such as revenue growth and even profitability to the rating of many biotechs. If a company is going to be ready for

the next biotech financing window, which many public companies were not this time round, it must ensure it

has delivered along the way. 29

Whereas biotech 10 years ago may have effused a spirit of discovery with few real products, today's biotech has combined that spirit with the day-to-day management of new technologies and filling and maintaining a product pipeline. It's really a decision of where the knowhow, the skill sets, the technologies, and the

resources. For platform-based designs, it's important to have people knowledgeable about a particular class of molecules. For target-based designs, knowing all the literature in the disease area and familiarity with

animal models is more important.30

2.2.3 The public and private financial markets for biotechnology companies

One of the consequences of an opening of the IPO window, as happened in 2000, is the lowering of the hurdle to make it onto the public markets. Interestingly, the average revenue per European public bioscience

company at the start of 2000 was around 51 million. The average revenue for the IPO class of 2000 was 3

million. They have a lot of delivering to do. European biotechs are flush with cash and feeling reasonably financially secure. The risk now is that the mistakes of the nineties are repeated. The money must be used to

build the business. There is only one way this can be done and that is by pulling together all the necessary threads to build a world leading position in a chosen area. 31

Despite the fact that the biotechnology industry accessed the public markets, there are still a great number of small private companies (Table 2). This is especially true for regions not having well developed public

markets for risky and uncertain businesses. However, these small companies have increasingly accessed venture capital.

Table 2 Biotechnology industry at a glance. The financial data is based primarily on financial statements from 31st December each year. The number of companies and employees as of 31st December each year. The market capitalization is from 30th June to 30th June each year.32

$ billions Public Number of companies

Industry Total

1999 % change 1999 1998

Financial Sales 13,6 13 16,1 14,5

Revenues 18,8 13 22,3 20,2 R&D expenses 6,9 2,6 10,7 10,6 Net gain (loss) (3,1) 65,3 5,6 4,4

Industry Market capitalization 353,5 156,4 353,3 137,9

Number of companies 300 (5,1) 1273 1311 Number of employees 140000 7,5 162000 155000

Initial Public offerings The difference between the US and European Class of '96 top ten biotech IPO’s. Since IPO, the top ten

European companies raised 333 million whereas their contemporaries in the US raised 4.1 billion. There are some great European companies being formed, aimed at solving some of the most critical issues facing the

industry and we can feel proud about how much the European industry has achieved with a comparatively

small amount of funding..33, 34, 35 Equity remained the financing choice in 2000.36

16

Debt issues

The amount of convertible debt raised by the biotech sector increased 277 percent. In a market of rising

stock prices as was evident in 2000, biotech firms, generally speaking, had the latitude to issue convertible debt with a low coupon and a fixed conversion price set at a premium to its current stock price. In the short

term, this benefits the firm because of the lower interest cost associated with a lower coupon rate. In the long term, however, this could be a serious risk because cash will have to be repaid if the conversion price is

not reached. 37

Private Biotechnology Companies and Venture Capital

Within the past year, firms such as Accel Partners and Crosspoint Venture Partners have abandoned health care. But despite the industry's lackluster performance - venture-capital returns have been averaging 20% on

health-care investments, much lower than the overall private equity average of 45% - many firms continue to finance these companies, opting to hedge through diversification. The dollars invested have remained

steady, but health-care investing has become a much smaller piece of the VC pie over the last few years. Of

the total $41.5 billion in venture dollars disbursed last year, $3.5 billion (8.4%) went into medical, health and biotechnology companies - $1.4 billion of which went to biotech companies, see exhibit 10 - compared with

$3.5 billion (17.6%) in 1998 and $3.3 billion (22.9%) in 1997, according to Venture Economics Information Services (VEIS). As a result, in the last three years medical and health investments have slid to fifth place

from being the third largest sector in terms of venture dollars invested. The category now lags behind the

Internet, computer software, computer services and communications, according to VEIS. That's a far cry from the heydays of 1992 and 1994, when health care ranked behind only computer software and services

investments. Given the cyclical nature of the venture industry, firms that include health-care investing in their diversified portfolios are looking to make a comeback in the next few years. Venture capitalists can expect to

see a resurgence of interest in health care once a "blow-off" in Internet stocks takes place. Maintaining industry contacts and keeping a perspective on health care to keep up with quality deal flow. The lack of

interest in health care has also made it more difficult to create syndicates, having a harder time convincing

previous co-investors to return for new deals. Fewer health-care players, however, means less competition and a stronger position for those who remain in the game.38

2.2.4 Strategic alliances

The clearest affirmation of biotech companies' technological value is seen in their ability to attract big

pharmaceutical companies as strategic partners. Pharma companies look to the biotechnology sector to help

fill their development pipeline with potential new products and provide technology platforms. The high value of deals struck offered a viable alternative to public markets as a source of finance for biotech companies.

But companies need to ensure they understand big pharma's agenda when looking to partner their products or technology and the importance of building a pre-eminent position in their chosen field. Many of those

threads will lie within other organizations and may include cutting edge or complementary technologies,

solutions to technological challenges or maybe development capabilities not held in-house. Accessing these tools through alliances or M&A activity is vital. The number of reported alliances took a huge leap in 2000, up

by almost 55 percent on the previous year. This is an indication of how many companies are already looking to expand their networks and to co-develop, cooperate and partner their technology. The nature of these

alliances is changing also. There are far more biotech-to-biotech deals and, because of that, many of these arrangements are more genuine co-development agreements as opposed to straight licensing deals. Driven

by a need to fill a massive pipeline black hole, the big pharma companies are finding the top biotechs are

skilled in product licensing. The big pharma companies' have attempted to create their own set of entrepreneurial biotech companies by radically reorganizing their R&D functions. 39The alternative to virtual

integration through alliance networks, therefore, is real integration through Mergers & Acquisition activity.40,

41

The development of an extensive integrated network of alliances (Table 3) will provide the basis for a strong company and for growth in value as the business model develops. The question is whether this will provide

sufficiently rapid growth to keep ahead of the game. The time available for a biotech company to achieve

17

critical mass is continually shortening and the definition of critical mass is continually increasing. Biotech

companies need to run faster and jump higher than ever before. 42

Table 3 The number of deals in the biotechnology industry.43

Year Strategic alliances Sales/Supply/Distribution M&A Joint ventures Total

1999 241 75 46 20 382 1998 146 47 19 14 226 1997 170 58 39 9 276 1996 100 53 40 23 216 1995 16 86 40 74 216

2.2.5 Biotechnological manufacturing capacity

Until five years ago, the outsourcing of biopharmaceutical manufacturing had been hobbled. Whereas

traditional pharmaceuticals are overseen by FDA's Center for Drug Evaluation and Research (CDER), another branch, the Center for Biologics Evaluation and Research (CBER), is responsible for biopharmaceuticals. And

while the CDER requires a single new drug application (NDA) for a drug to be considered for approval, the CBER required two: a product license application (PLA) and an establishment (facility) license application

(ELA). Moreover, these two applications had to be filed together, and the ELA had to be submitted by the company that manufactured the product. Consequently, if the manufacturing of a biopharmaceutical was

outsourced, the contractor, not the developer, would hold its license-an unacceptable state of affairs. In

1995, FDA changed the rules, introducing the single biologics license application (BLA). So now, you could hold the license to your product without having to manufacture it. Companies that had been sinking

tremendous amounts of capital into manufacturing facilities no longer had to do that they could rely on outsourcing. That is when the contract manufacturing industry for biologics really began to grow. Several

major players offer commercial-scale production capacity, and others have programs in the works. They note

that barriers to entrance are very high, but the market for biopharmaceuticals is expanding at twice the rate of traditional drugs, and the small biotech companies responsible for most of the discovery work are a

contract manufacturer's natural clientele. Monoclonal antibodies (MAbs) are an important and growing therapeutic class in biotech drugs, and several biotech companies have recently added antibody production

capacity. Several biopharmaceuticals-biologically active proteins obtained by recombinant technologies-are

already blockbusters. Biotech manufacturers can manipulate cells to produce high yields of desired cell metabolites such as antibiotics, vitamins, amino adds, and other small molecules. As a result, regulatory

policies established for proteins must be modified for these drugs. At the same time, progress in the development of techniques to characterize these products may make it possible to have better control over

production and manufacturing changes.44,45,46 47

2.2.6 The impact of size and structure as success factors of the biotechnology industry

A glance at the difference between the US and European industry shows just how big the size difference is.

The entire European public biotech industry is only slightly larger than US-based Amgen and the average market capitalization of a US public biotech company is almost 60 percent greater than that of the average

European one. Compound this with the fact that the US biotech industry raised five times the amount the European sector did on the public markets last year, and we return to the question of who will be doing the

integrating. 48, 49

Large liquid stocks attract investors and even if there is good value in some smaller companies, they suffer

from poor liquidity and R&D pipeline gaps 50. Most companies in Europe are still simply too small to command the resources necessary to attain global leadership. There is evidence that things are changing. There are

many more venture rounds in excess of 25 million than there were a few years ago, the equity markets dug

deep into their pockets in 2000. The German model of matching private capital with state funding is paying off with the catapulting of young companies the top echelons of European biotech. 51

18

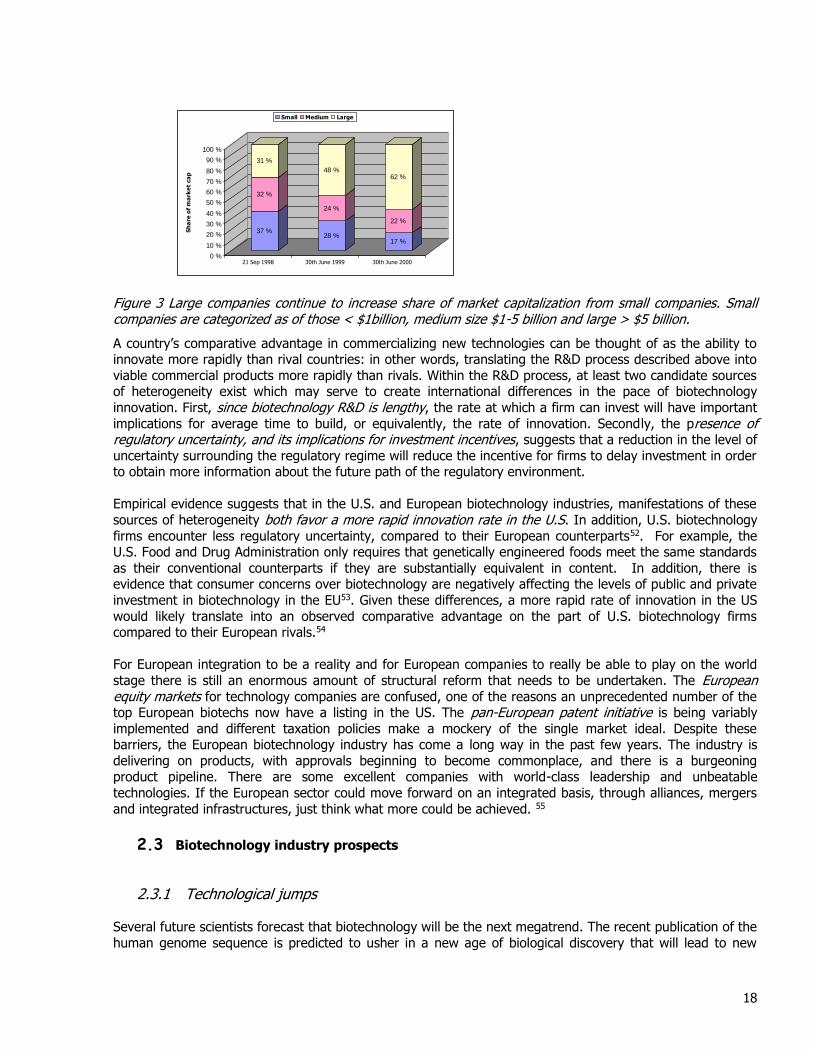

Figure 3 Large companies continue to increase share of market capitalization from small companies. Small companies are categorized as of those < $1billion, medium size $1-5 billion and large > $5 billion.

A country’s comparative advantage in commercializing new technologies can be thought of as the ability to innovate more rapidly than rival countries: in other words, translating the R&D process described above into

viable commercial products more rapidly than rivals. Within the R&D process, at least two candidate sources of heterogeneity exist which may serve to create international differences in the pace of biotechnology

innovation. First, since biotechnology R&D is lengthy, the rate at which a firm can invest will have important

implications for average time to build, or equivalently, the rate of innovation. Secondly, the presence of regulatory uncertainty, and its implications for investment incentives, suggests that a reduction in the level of

uncertainty surrounding the regulatory regime will reduce the incentive for firms to delay investment in order to obtain more information about the future path of the regulatory environment.

Empirical evidence suggests that in the U.S. and European biotechnology industries, manifestations of these

sources of heterogeneity both favor a more rapid innovation rate in the U.S. In addition, U.S. biotechnology

firms encounter less regulatory uncertainty, compared to their European counterparts52. For example, the U.S. Food and Drug Administration only requires that genetically engineered foods meet the same standards

as their conventional counterparts if they are substantially equivalent in content. In addition, there is evidence that consumer concerns over biotechnology are negatively affecting the levels of public and private

investment in biotechnology in the EU53. Given these differences, a more rapid rate of innovation in the US

would likely translate into an observed comparative advantage on the part of U.S. biotechnology firms compared to their European rivals.54

For European integration to be a reality and for European companies to really be able to play on the world

stage there is still an enormous amount of structural reform that needs to be undertaken. The European equity markets for technology companies are confused, one of the reasons an unprecedented number of the top European biotechs now have a listing in the US. The pan-European patent initiative is being variably

implemented and different taxation policies make a mockery of the single market ideal. Despite these barriers, the European biotechnology industry has come a long way in the past few years. The industry is

delivering on products, with approvals beginning to become commonplace, and there is a burgeoning product pipeline. There are some excellent companies with world-class leadership and unbeatable

technologies. If the European sector could move forward on an integrated basis, through alliances, mergers

and integrated infrastructures, just think what more could be achieved. 55

2.3 Biotechnology industry prospects

2.3.1 Technological jumps

Several future scientists forecast that biotechnology will be the next megatrend. The recent publication of the

human genome sequence is predicted to usher in a new age of biological discovery that will lead to new

37 %

32 %

31 %

28 %

24 %

48 %

17 %

22 %

62 %

0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

90 %

100 %

Sh

are

of

ma

rke

t ca

p

21 Sep 1998 30th June 1999 30th June 2000

Small Medium Large

19

methods for drug research and discovery and whole new industries involved in biionformatics and

proteomics. Although industry and the public stand to benefit from this eruption in new biomedical discovery,

these developments present major challenges to pharmaceutical manufacturers. Difficulties in characterizing and setting specifications for complex new substances necessitate new approaches to validating and testing

new manufacturing systems. Even after a new therapy gains approval, problems may be encountered in scaling up to commercial production to meet patient demand for effective therapies. Advances in genomics

also promise to considerably influence how the government regulates the testing and manufacture of medical

products. FDA already is examining whether its rules and procedures can accommodate the anticipated wave of complex new experimental products.56

The new economic basics underlying the biotechnology industry are

1. The daily doubling of knowledge. The patent approvals took 8 years to double in the 1970´s and 4years to double in 1997.

2. The global scope of biomaterials is inversely proportional to its subatomic scale.

Biotechnology differs from other kinds of R&D because the end-results are very difficult to identify and predict in advance. The areas of real commercial impact of biotechnology account fro one-third

of the world’s GDP. Hence the R&D work focusing on subatomic issues are global in scope 3. Accelerating vertical growth rates. As resources committed to biotechnology research

increase, the commercial returns will (might) increase exponentially. 57

Figure 4 The Economic eras.

Biotechnology offers several technological ways to improve the properties of bio-originated materials. The

methods vary largely and the efficiency can still be increased remarkably. The basic ideas of surgery have changed from removal of damaged tissues to replacing damaged tissues with biocompatible materials and

tissue transplants. Biomaterials will focus on developing materials that release proteins and growth factors thus promoting growth of bone and soft tissues, simultaneously preventing growth of bacterial biofilms on

artificial implants. An important issue in biomaterials is to reduce their tendency to activate the human

defense systems, when placed in long-term contact with living tissues.

Another important issue is that the customers (i.e. the patients) expect an implant to function as well as its biological counterpart and to last forever. This misconception has been fostered by the press and some

physicians and will only be corrected by properly educating potential recipients. Biomaterial and implant

research will continue to concentrate on serving the needs of medical device manufacturers and recipients, as well as medical professionals developing technologies to meet those needs. 58

Agrarian Age

Time

Biomaterials Age

Information Age

Industrial Age

Glo

bal

izat

ion a

nd

Eco

no

mic

Ad

ded

Val

ue

20

2.3.2 Demographics change

Demographics play a positive role in the outlook for the healthcare industry. Demographics also bode well for

assisted living, nursing home and related industries, as the demand for long-term care grows with the population's age. Hospitals are joining the assisted-living trend in some capacity. Cost containment will

continue to be a driving force in the healthcare industry as well as the public's concern for safety and health.59

Trends in the life expectancy indicate that the population will grow older globally. The millennium children will place unique demand on the health science industry. Lifestyle related chronic disease is starting at

younger age and health concerns previously associated with older adults are some of the concerns of today´s youngsters. Health consumers around the world are using the increased disposable income to

improve their health care, gain access to new advances and alternative treatments. A key element in

improving the health is the access of nations to new information technology and the ability to be interconnected to other health networks. The developing nations are in a constant state of catching up to the

interconnected global market place. Their major problem will still be access to capital.

2.3.3 Global financial markets

The financial markets have expanded-although still volatile due to business cycles; the financial pie is getting bigger. In addition, governments, individuals and institutions are becoming increasingly involved. More

investments access the international markets and the nations are becoming richer. As a result, the nations

are more able to invest more in health science products and services. Positive regulatory news helped the industry. Over the next ten years, spending on healthcare services will grow substantially faster than the

economy. The global market place for health services and products grow, and the companies producing these are (need to) becoming international.

The global financial markets quickly affect others. Integration result in standardization of systems for trading and connecting them with technology hence opening new opportunities for biotechnology companies.

Business transaction can be conducted internationally at the Internet anytime and at low cost.

2.3.4 Technology trends affecting individuals

The IT and biotechnology is intertwined and they are fuelling each other. The implications are that the

technology breakthroughs have simplified and quickened the pace of research. The biotechnology discovery is identified quickly and the research is accomplished faster, at lower cost and higher quality. The power of

biotechnology to redefine our lives is just becoming to be grasped.

Consumer perception and empowerment to act on the awareness is creating a shift in every industry. A new

consumer paradigm has evolved. Just as physician and companies are becoming interconnected, consumers have access to volumes of new medical information and they use it. 60

2.3.5 Trends in the biotechnology industry sector

Currently, the biotechnology sector is diverged by region and size. The US biotechnology companies are

bigger by size, further in the development of products and hence showing more profits, they have access to

more capital. The biggest biotechnology clustering within Europe is in he UK and the fastest growth is emphasized to occur in Germany. Biotechnology companies have mainly listed on the London Stock

Exchange (UK), the Neuer Markt (Germany), The Swiss Stock exchange (Switzerland) and Bourse de Paris (France). Biotechnology companies exist mainly in Belgium, the Netherlands, Denmark and Sweden. 61

Analysts believe that it is likely that the biotech sector in Europe will grown fueled by product successes,

increasing profitability and M&A activity to achieve critical mass. Small companies are likely to pursue the

21

strongest growth, but the attractive company stocks are for those reaching profitability and products on close

to reaching the market. Once approaching profitability, the next challenge is to sustain growth. The smaller

companies will help drive the biotechnology sector growth in the long run, but the large groups are the ones likely to be the ones to deliver the promises. The emerging themes are likely to be 1) M%A activity, 2) re-rating of the biotechnology stocks, 3) technology becomes a commodity, 4) The European segment will grown, but the challenges will relate to quality and value, 5) growth is likely to concentrate in regions and 6)

the relative importance of special segments will grow (e.g. bioinformatics) The stocks are highly valuated and

not likely to sustain as e.g. retail demand is fuelling valuations in Germany. New entrants are highly likely and more companies will raise equity (IPO’s) and M&A will continue.62

2.3.6 The pharmaceutical market

Analysts estimate that the large multinational pharmaceutical companies' profits increased by approximately

18 percent in 2000. Many of the companies' margins are improving, and their product lines are dominated by

very profitable and successful drugs. Expenditures for prescription drugs in the U.S. are expected to grow at a 10.8 percent compounded annual rate between 1999-2004, as opposed to the 12.6 percent rate over the

preceding five years.63

The future market for generic biopharmaceuticals depends on the resolution of a number of legal, regulatory and technology issues. To what extent biopharmaceuticals will enter the generics mainstream is uncertain. A

position in generics biopharmaceuticals is risky. Most companies are not expected to pursue generic biologics

because the manufacturing processes are too complex and costly. With several patents for key biopharmaceutical products approaching their expiration dates, some in the generics industry are pushing for

a regulatory pathway that will more clearly establish the procedure and process for generic biologics. The current differences in review and approval processes for new drugs versus biologics will most likely extend to

their generic counterparts.

The predicted shift from blockbuster drugs designed to treat millions of patients to more custom-designed

therapies may require revisions in the regulatory system. Managed care providers use their powerful collective clout to secure discounts on bulk purchases of pharmaceutical and medical products, as well as on

physician and hospital services. Managed care has historically favored drug therapies because of their cost-effectiveness. They typically insist on the use of low-cost generics whenever possible. However, in terms of

government oversight and pricing issues, the pharmaceutical industry is still under some political pressure.

Prescription drug pricing is coming under increased pressure from managed care and governmental authorities. 64

2.3.7 Technological development affecting the industry

As recent developments alter biotechnology and biochemistry, it will be important to standardize products

further based on new in vitro and analytical assays. Not only will new analytical technologies such as three-

dimensional nuclear magnetic resonance, microarrays and proteomics provide new ways for scientists to understand molecular structures and accelerate laboratory analysis of cellular substances, but they also may

provide new approaches for developing and scaling up manufacturing systems.65

In addition to accelerating new product development, these technologies can facilitate the characterization of

complex molecules, a key step in simplifying the regulatory process for monitoring and approving manufacturing changes to approved products. FDA began to encourage manufacturers to write comparability

protocols (Cps) for well-characterized drugs and biologics in 1997, and companies are submitting written CP plans now as part of new drug applications or supplements. The protocol can be as short as a few pages,

enough to specify the tests, validation studies, and acceptance criteria of the product. CPs provide a reference point to demonstrate later that a change in manufacturing process, equipment, or location after

approval has no adverse effects on the quality, purity, or potency of the product. 66

22

The biopharmaceutical industry has offered breakthrough treatments for serious diseases. The potential of

this industry comes not only from the development of monoclonal antibodies and recombinant proteins as

therapeutics but also from the technologies associated with drug discovery, design, and understanding of the diseases. Chemists have been an integral part of the development of the biopharmaceutical industry by

exploring the molecular mechanisms that regulate, enhance, and limit the biochemical pathways involved in various diseases.67

The broader challenge for manufacturers is to use these new technologies to overcome technical and economic roadblocks to production. Most companies are unwilling or unable to invest millions of dollars in

new manufacturing facilities until they have strong evidence of - if not FDA approval for - a safe and effective product. However, the complexities in scaling up production can make this a long process. 68

23

3. THEORY ON VALUATION METHODS

There are no absolutes in valuation; the circumstances of the valuation and its purpose will influence the

value. The market is sophisticated and changes in value are linked more closely to changes in expectation than to absolute performance. Valuation levels are linked to the return on invested capital and growth. The

market sees through cosmetics earnings and put weight on long-term results.

The company’s value its equal to the value of its assets. When the value of debt is deducted from the assets

value, the value of equity is remaining. As equity in a firm is a residual claim, i.e., equity holders lay claim to all cash flows left over after other financial claim-holders (debt, preferred stock etc.) have been satisfied. If a

firm is liquidated, the same principle applies, with equity investors receiving whatever is left over in the firm after all outstanding debts and other financial claims are paid off. The principle of limited liability, however,

protects equity investors in publicly traded firms if the value of the firm is less than the value of the

outstanding debt, and they cannot lose more than their investment in the firm. Equity can be viewed as a call option the firm, where exercising the option requires that the firm be liquidated and the face value of the

debt (which corresponds to the exercise price) paid off. The first implication is that equity will have value, even if the value of the firm falls well below the face value of the outstanding debt. Such a firm will be

viewed as troubled by investors, accountants and analysts, but that does not mean that its equity is worthless. Just as deep out-of-the-money traded options command value because of the possibility that the

value of the underlying asset may increase above the strike price in the remaining lifetime of the option,

equity will command value because of the time premium on the option (the time until the bonds mature and come due) and the possibility that the value of the assets may increase above the face value of the bonds

before they come due.

The value placed by a strategic investor is higher than the value of the financial investor, as the strategic

investor is able to attract additional value from the company associated with synergy gains.

Equation 1

Value strategic investor= Value financial investor+ Value synergy gains In the real market you create value by earning a return on your invested capital greater than the opportunity

cost of capital. The more you invest at return the above the cost of capital the more value is created. The

returns shareholders earn depend primarily on changes in expectation more than on the performance of the company. The value of a company’s shares in the stock market equals the intrinsic value on the market’s

expectation of future performance, but the market expectations of future performance are an unbiased estimate of performance. 69The three laws of value creation are Cash is King and Time is Queen70

The valuer should recognize the sensitivity of judgments and assumptions on the valuation derived. The validity of the valuation method can still be objectively scruin. Depending on the circumstances some

methods are better than others, while other methods may be incorrect r irrelevant.71

The purpose of metrics is to help measure value creation, make value-creating decision and to orient towards value creation. Attempts to compare metrics that have different goals will lead to confusion. DCF valuation

measures performance over time and Economic profit is a short-term indicator. Generally, economic

measures are considered to be better than accounting based methods, as empirical evidence suggests that share prices are driven by cash flow not accounting earnings. However, there are no perfect measures and

some have developed frameworks to link various measures to describe different aspects of performance. 72

What drives the market value of companies? One way is to measure investors’ return is a combination of

share price appreciation and dividends earned (TRS). Other methods involve Market Value Added (MVA), which is the difference between the market value of a company’s debt and equity and the amount of capital

24

invested. A variation of MVA; the market-to-capital ratio is the market capitalization of a company’s debt and

equity. MVA pose problems because of use of accounting data. By combination TRS and MVA an interesting

insight into the dynamics is achieved, especially for terms of less than 10 years.73 TRS and MVA are linked to the current speed of the market’s expectations. Analysis has shown that market and sector movements

explain 40% of the returns during any one to three year period.

3.1 Assets based valuations of companies

The actual value of company is often ambiguous, depending upon which parts of the balance sheet were included. Knowing which assets are included, how ownership is held, and what the terms of the transaction

will be will make a big difference in the final sale price. When a third party attempts to use only the actual

sales price to make a decision about the value of his or her own property management business, confusion will be the result. On the right-hand side of the balance sheet, the term equity means the ownership interest.

Also, in the right-hand column, a sale also may include invested capital instead of merely equity. The left-hand side of the balance sheet contains the company's assets included in the sale. Even after the transaction

value has been established, you still may not have a complete picture of how much a seller receives for his or her management company. The method and terms of payment also affect the actual value of the sale.74

Business Structure On the right-hand side of the balance sheet, the term equity means the ownership interest. In a corporation,

equity is represented by stock. If there is more than one class of stock outstanding, the term equity by itself usually means the combined value of all classes of stock. If it is intended that the value represent only one

class of stock in a multi-class capital structure, there should be a statement as to which class of equity the

value represents. 75

Assets to Value The left-hand side of the balance sheet contains the company's assets included in the sale. In a cash-for-

stock transfer, all of the assets and all of the liabilities of the company are assumed to be included (unless specifically excluded) in the price. In a cash-for-stock transaction, contracts (for leases, etc.) need not be

rewritten whereas contracts may need to be renegotiated in a cash-for-assets transaction. Similarly, off

balance sheet liabilities such as lawsuits and insurance claims are part of cash-- for-stock transaction and may not be part of a cash-for-assets deal. When estimating the value of a business in a cash-for-assets

transaction, it may be necessary to estimate the value of each of these assets. The financial assets such as cash, accounts receivable, and inventory have values that are usually straightforward. Normally book value is

a good starting point for estimating the fair market value. If any of these assets aren't part of the transaction

for any reason, once their value is estimated, it can be subtracted. 76

The value of tangible personal property is usually estimated by beginning with the original cost and making an estimate of their depreciated cost (perhaps by using a depreciation method that is different from the one

used to calculate book value). The value of the records is often not estimated separately from the going-

concern value of the other assets since the records are often needed in order to maintain the going concern. The intangible assets of a property management company may or may not contribute substantial economic

value. They might even contribute negative economic value, which is recognized as economic obsolescence. One way to estimate the value of the intangible assets is to measure the company's expected rate of return

on assets. The value of the business itself without these components, the value of these components must be subtracted from the transaction value. 77

3.1.1 Yield capitalization method

The yield capitalization method of firm valuation is advocated as a valid declining asset valuation model over

the direct capitalization or the stock and debt approach to firm valuation. However, yield capitalization is not an appropriately specified declining asset valuation model. The use of yield capitalization is not justified

25

based on the argument that the procedure values only the asset already in place. A correctly formulated

equation is presented for a situation in which only the declining assets in place are to be valued. Yield

capitalization estimates from the correctly specified declining asset model are compared to the true firm value calculated using the Gordon dividend discount model. It has been demonstrated algebraically that if a

firm is expected to earn a return on invested equity capital (ROE) that exceeds (falls below) the required market return on that investment, the yield capitalization valuation method systematically will underestimate

(overestimate) the true equity value of the subject firm. The direct capitalization and the stock and debt

valuation methods contain no such inherent biases. 78

Notwithstanding this and other evidence, many supporters of yield capitalization still advocate its use over direct capitalization or the stock and debt approach to firm valuation. These proponents argue that although