help to buy - chartered institute of housing pdfs/presentations/se affordable... · growth and fall...

TRANSCRIPT

Help to Buy: ‘Helping people to have a home of their own’

Nick Atkinson

Mortgage Markets and Homeownership

Department for Communities and Local Government

2

Context

• Demand to own is as strong as ever. However, home ownership,

as a percentage of tenures, is at it’s lowest level for 25 years.

• The clear long-term solution is to increase housing supply but

that will take time.

• In the meantime what can we do to support people’s aspirations

in a market of rising house prices?

- How did we get here

- What the Government is doing to support home ownership

- Challenges and Opportunities

3

Why do we care so much?

• People want to own homes.

• Politicians support people’s

aspirations to own. The PM said:

“Owning a home is about more than

four walls to sleep at night. It’s

about independence, self-reliance,

moving on and moving up. Above

all, it’s about aspiration”.

• Importance of construction and

housing. Housing output contributes

around 3% to GDP, construction

contributes 8%.

Pros

• Creates wealth – 60% of UK wealth in

housing

• OECD highlight that children have

better school outcomes if parents are

home owners

• We are not saving in this country –

ownership enables people to save by

building up equity

• OECD highlight argument that areas

with high levels of ownership have

more engaged communities

4

Quick History

• Ownership is a 20th

Century phenomenon. In

1918, ownership stood at

23% of tenure mix with

private renting dominant.

Ownership was 69% in

2000.

• There were 2.5 million

extra home owners

created between 1981

and 1991. A further 1.5

million home owners

were created between

1991 and 2001, to stand

at over 14 million.

5

Drivers of home ownership in the 20th Century

1920s 1930s 1940s 1950s 1960s 1970s 1980s 1990s

Rise in incomes for workers from 1920 to 1980

Expansion of the building societies

Financial Deregulation

Post war house building

Growth in financial markets

Support for private

housebuilding Rent controls and security of tenure in the private

rented sector

Right to Buy

Mortgage interest

tax relief

WIDER ECONOMIC

CHANGES

GOVERNMENT

INTERVENTIONS

6

Recently house price rises have outstripped

wage increases

• From 2000 house prices increased rapidly – far out-pacing earnings.

• Driven by decades of under-supply and more recently access to mortgage

finance.

• Between 2000 and 2012

average house prices went from

£107,000 to £256,000, an

increase of 139%.

• Between 2000 and 2012

average wages went from

£18,848 to £26,472, an increase

of 40%.

7

Growth and fall in mortgage lending

• 200% increase in mortgage

lending 2000-2007.

• Cheap credit through the

securitisation market.

• Dramatic fall after the

financial crash in 2007, flat-

lined for four years and

returned to growth in 2013 .

• Many first time buyers had already been priced out of the market but big impact on LTV knocked even more out.

• The fall in lending in 2007 hit existing owners hard – both those looking to move or remortgage.

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

110.0

Jan-0

2

May-0

2

Sep-0

2

Jan-0

3

May-0

3

Sep-0

3

Jan-0

4

May-0

4

Sep-0

4

Jan-0

5

May-0

5

Sep-0

5

Jan-0

6

May-0

6

Sep-0

6

Jan-0

7

May-0

7

Sep-0

7

Jan-0

8

May-0

8

Sep-0

8

Jan-0

9

May-0

9

Sep-0

9

Jan-1

0

May-1

0

Sep-1

0

Jan-1

1

May-1

1

Sep-1

1

Jan-1

2

May-1

2

Sep-1

2

Jan-1

3

Month

%First Time Buyers – Deposits as % of Income

8

Impact on affordability and accessibility to

finance

• Current ownership levels are at their

lowest since 1987.

• First time buyers have struggled to enter

the market even during a time of peak

lending.

• Mortgage lending concentrated

among existing owners, either

moving home or remortgaging.

• But when credit availability was

restricted in 2007-08 many buyers

were priced out of moving up the

ladder to buy a family home.

Deposit constrained FTBs shifting from

ownership to renting

• The tenure for 16-34 year olds is now

dominated by renting, a shift from

ownership.

• In 2012-13, the private rented sector

replaced social renting as the second

largest tenure in England.

• The costs of renting make it harder for

people to save to buy a property.

• High house prices, deposit

requirements, and rents mean many

are not able to take advantage of

record low interest rates.

9

90.0

92.0

94.0

96.0

98.0

100.0

102.0

104.0

106.0

2005 2006 2007 2008 2009 2010 2011 2012 2013

Rents in England (2011 = 100)

10

And existing owners hit too

• Affordability issues for those wanting to upsize.

• The income needed to move house has increased 40%

more than the increase for average wages. Mortgage

availability helped to bridge this gap until 2007, that

support has now been taken away.

• There are issues for those who bought flats in the 2000s

but cannot now move up the property ladder and buy a

house for their family.

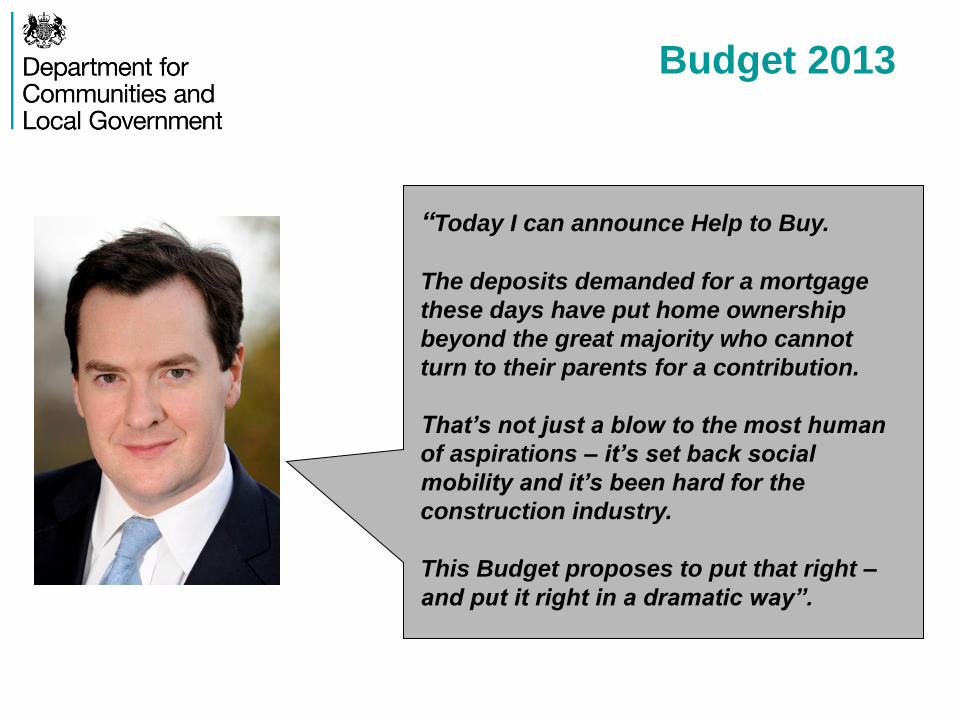

Budget 2013

“Today I can announce Help to Buy.

The deposits demanded for a mortgage

these days have put home ownership

beyond the great majority who cannot

turn to their parents for a contribution.

That’s not just a blow to the most human

of aspirations – it’s set back social

mobility and it’s been hard for the

construction industry.

This Budget proposes to put that right –

and put it right in a dramatic way”.

Not new – range of schemes previously

• Range of demand side equity loan based initiatives designed to fill the gap between

shared ownership and market ownership, tackling accessibility (by providing a deposit)

and affordability (enabling customers to access better value 75% LTV mortgages).

- 2007 – 2010: First Time Buyers Initiative - support first time buying

key workers and social tenants into home ownership.

- 2008 – 2010: HomeBuy Direct (and HomeBuy Kickstart 2009-2012)

to help get stalled sites moving, provide a boost to the housing and

construction industry over the period of recession.

- 2011 – 2013: Firstbuy - built on Homebuy Direct but increased value

for money.

12

Help to Buy: Equity Loan (HtB1)

• Tackling affordability and accessibility

• Launched on 1 April 2013 (initially 3

year programme)

• Provides first and second time

buyers with a 20% loan.

• New Build only.

• Cannot be used to buy a second

home.

• England based scheme – the

potential to deliver up to 74,000 sales

• Scotland & Wales have also

launched similar schemes

• Repayment based on house price at

sale.

Help to Buy: Mortgage Guarantee (HtB2)

• Getting high LTV mortgages back on the

high street

• National Scheme - launched on Oct 2013

and commenced in Jan 2014.

• Enable lenders to provide high LTV

mortgages

• Government-backed guarantees to offer

£130bn worth of mortgages

• Reduces deposit requirement to as little as

5%.

• Applies to both new and existing

properties.

• First time buyers, or those looking to move

up the property ladder.

• Cannot be used to buy a second home.

Help to Buy: Equity loan progress

SALES:

• In first 14 months, almost 36,000 homes

have been reserved and 22,831 sales

so far.

• On target to meet 74,000 supported by

March 2016.

• House builders have reported a

increase in sales.

• They are building more homes

as a result.

Strong support from Builders and

lenders

• Over 1400 builders registered to take part.

More than 850 already in contract with the

Homes and Communities Agency.

• Over 90% are SMEs.

• Sizable proportion of the lending market.

High level of awareness amongst

customers

• TV/Radio/Press/Digital campaigns

• Lots of good (and bad!) press coverage • Help to Buy road shows • Marketing from agents and developers • Rightmove and Zoopla

• Website: www.helptobuy.org.uk

Help to Buy Agents

• New, seven agent network from 1st April

Area Help to Buy Agent

North East, Yorkshire & Humber Yorkshire Housing

North West Plus Dane

Midlands Orbit

East South East BPHA

South Radian

South West Sovereign & Westward

London Aldwyck

House prices and impact on wider market

• Still small scale compared to

wider market.

• But independent analysts and

commentators recognise the

role that Help to Buy plays in

increasing house building

• Morgan Stanley research states; 34% increase in new build house

building in year one of scheme, of which 30% is attributed to be

supported by Help To Buy

- ‘HTB1 (equity scheme) has been the single most important

catalyst in the revival of house building, in our view.’

Extended to 2020 at Budget 14

• Budget 14 announced extra £6bn to increase support from 74,000 -

194,000 home buyers by 2020.

• Mortgages remain expensive at higher LTV and continued demand for

product.

• Provides certainty:

- builders can plan for more house building.

- lenders are willing to invest in systems.

• Evaluation planned in 2015 as part of the next Spending Review

“We inherited a situation where for many

people, buying a home seemed all but

impossible - people who worked hard, had

good jobs and could afford the monthly

mortgage payments, but didn’t have the large

deposit needed up front. For those without rich

parents, the dream of home ownership

remained just that: a dream. That is why we

brought in help to buy”

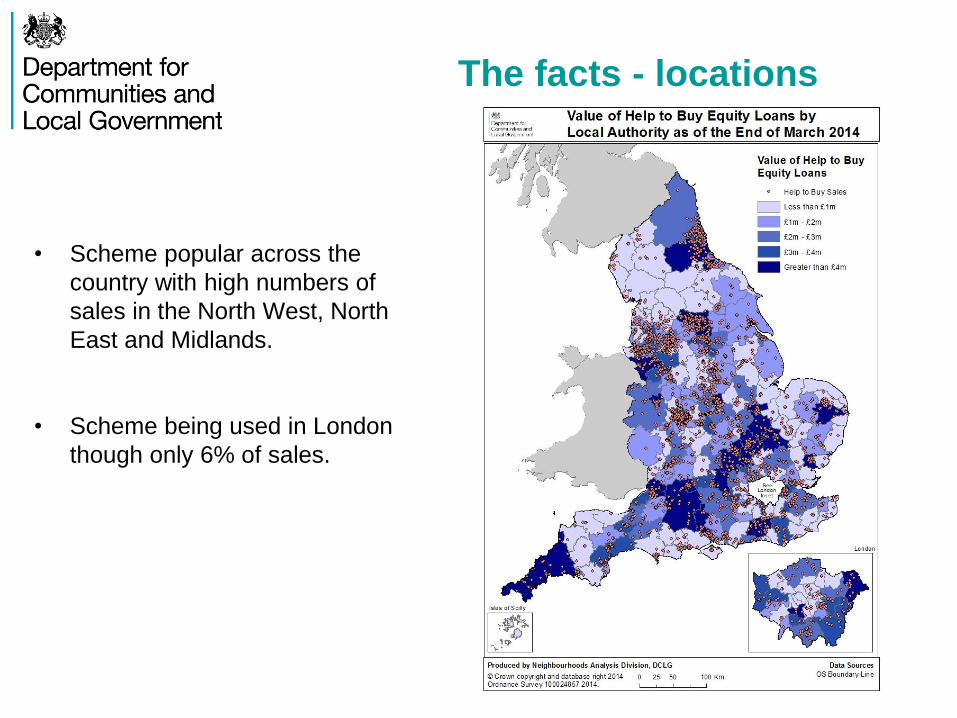

The facts - locations

• Scheme popular across the

country with high numbers of

sales in the North West, North

East and Midlands.

• Scheme being used in London

though only 6% of sales.

• Mean average full purchase price £204,805 (12 month average)

• Mean average equity loan £40,806 (12 month average)

The facts – property prices

• Mean average purchaser household income £45,424 (12 months)

• 86% are First time buyers

The facts – incomes

The facts – property types and lending

Detached

Flat

Semi Terraced

• Property size – dominated by 3

bedroom

4

3

2

1

• Property type – highest numbers

terraced

Perspectives

BUYERS

• Simple product

• Broad eligibility criteria

• Easy to understand

and access

• Available all over

England

• Choice of home

builders

BUILDERS

• Simple product

• Easy to understand

and access

• Available all over

England

• Integrated into sales

processes

• Admin support for

SME builders

LENDERS

• Challenges of volume

and scale

• Risk appetite

• Integration with other

systems

• House builder

compliance

• FCA requirements and

compliance

• Bank of England

Opportunities for housing providers

and LAs

• Using scheme to promote and drive

market operations.

• Data and statistics – published detailed

stats on a quarterly basis at local authority

level so can see where demand,

development FTBs are etc.

• Creating and exploiting links between

builders, housing associations and LAs.

• Understanding where the scheme is

available and linking to existing demand.

Where do we go from here

• Significant total of completions

expected in 2014-15 - started

year with 10,000 firm

reservations.

• A product the market understands

and customers know.

• Proven delivery mechanism.

• Seeking to widen lender

participation and bring in more

builders.