hello investors matthew...

TRANSCRIPT

Hello Investors Matthew Sigel

From our global sales desk Portfolio Strategist, CLSA

24 May 2017

Page 1 of 37

Bear in a China shop

Hello Investors,

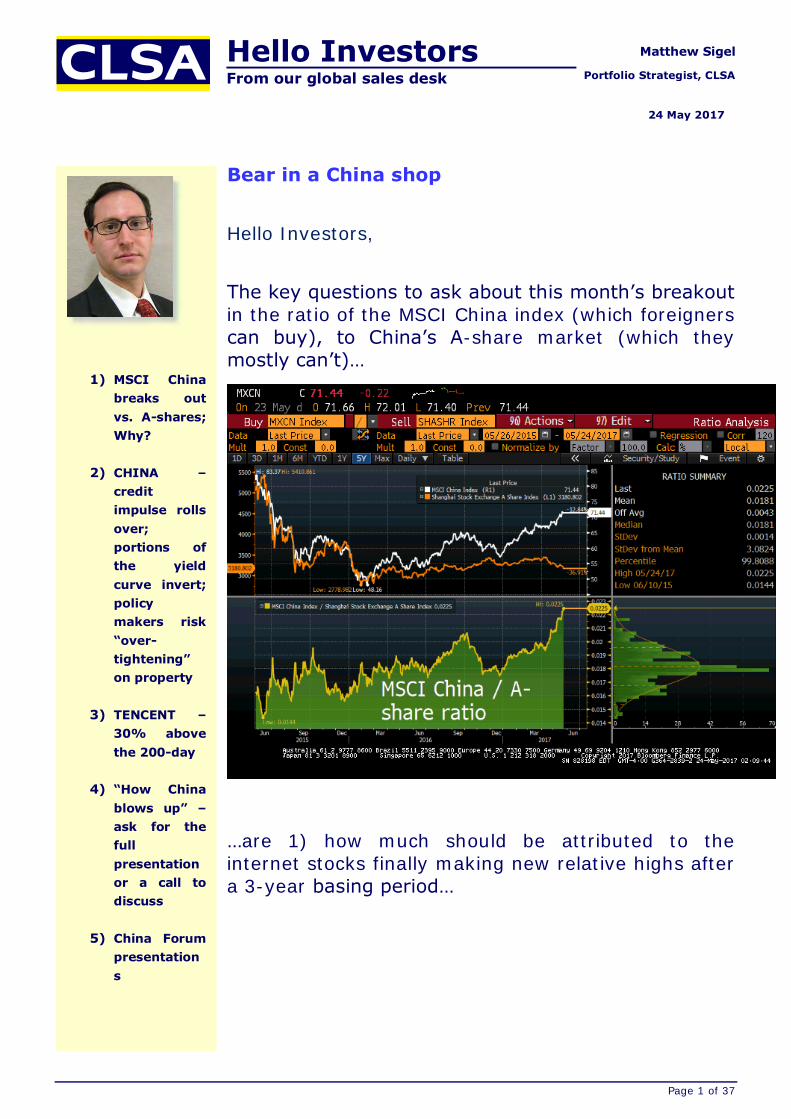

The key questions to ask about this month’s breakout

in the ratio of the MSCI China index (which foreigners

can buy), to China’s A-share market (which they

mostly can’t)…

…are 1) how much should be attributed to the

internet stocks finally making new relative highs after

a 3-year basing period…

1) MSCI China

breaks out

vs. A-shares;

Why?

2) CHINA –

credit

impulse rolls

over;

portions of

the yield

curve invert;

policy

makers risk

“over-

tightening”

on property

3) TENCENT –

30% above

the 200-day

4) “How China

blows up” –

ask for the

full

presentation

or a call to

discuss

5) China Forum

presentation

s

Hello Investors - with Matthew Sigel 24 May 2017

Page 2 of 37

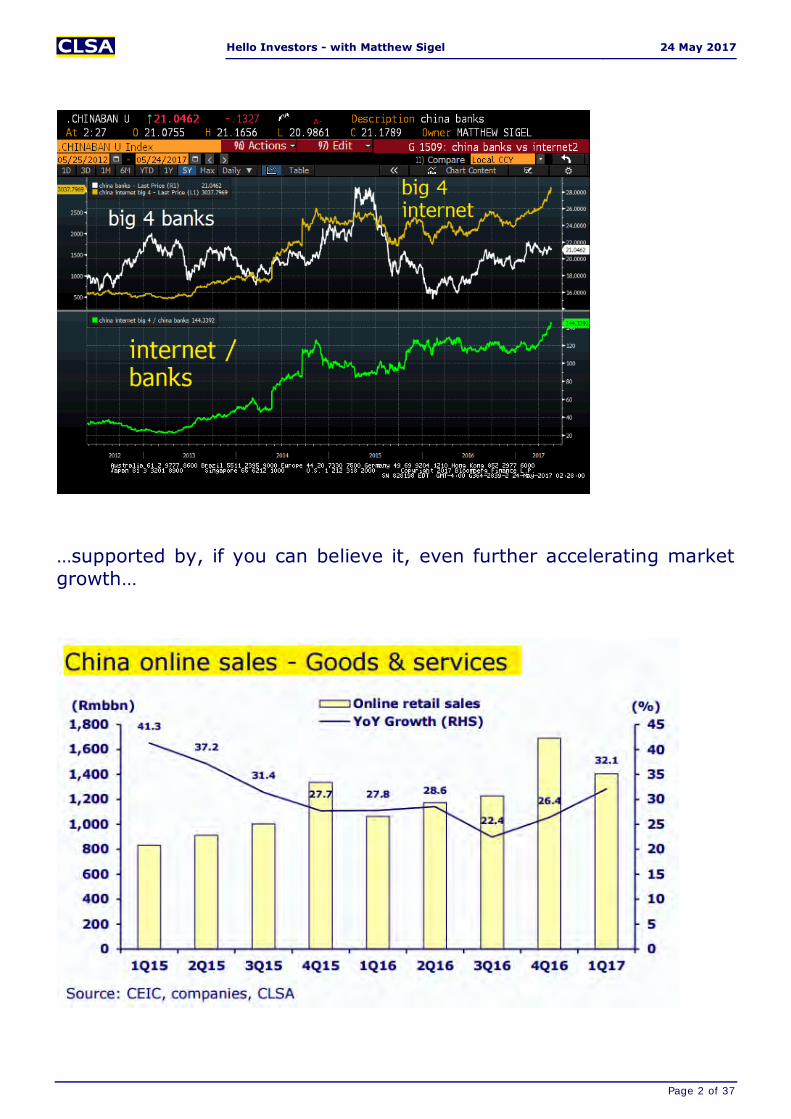

…supported by, if you can believe it, even further accelerating market

growth…

Hello Investors - with Matthew Sigel 24 May 2017

Page 3 of 37

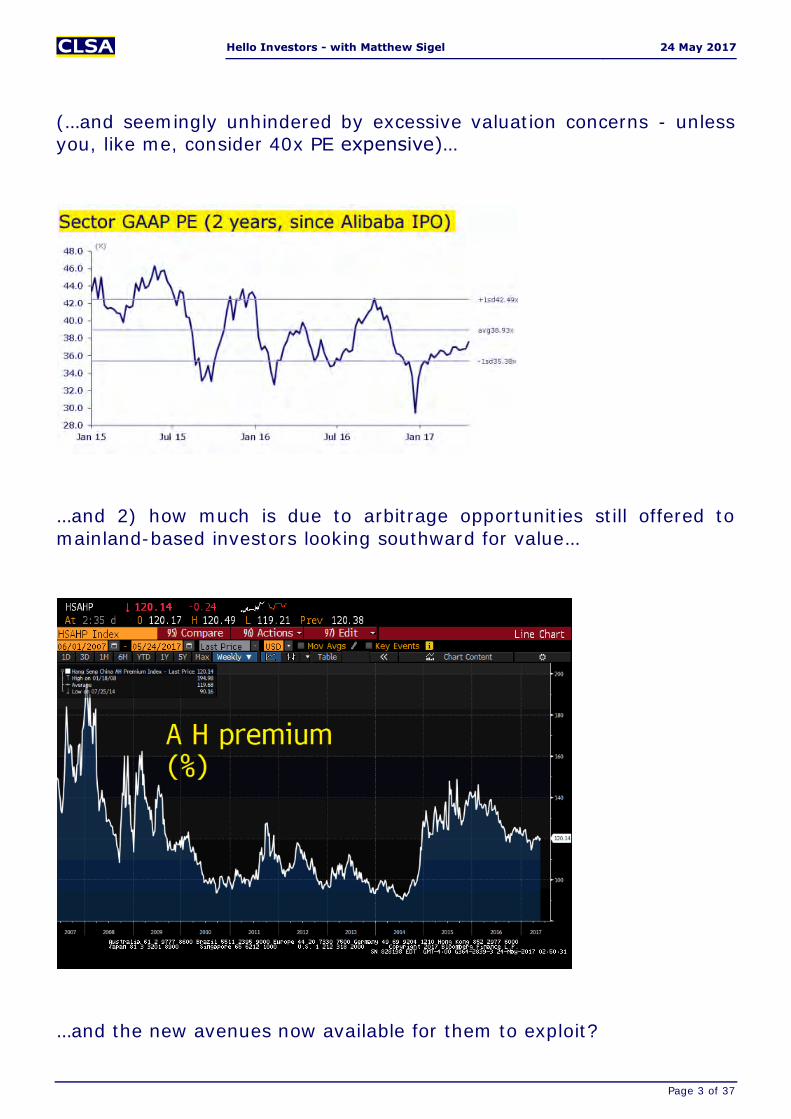

(…and seemingly unhindered by excessive valuation concerns - unless you, like me, consider 40x PE expensive)…

…and 2) how much is due to arbitrage opportunities still offered to

mainland-based investors looking southward for value…

…and the new avenues now available for them to exploit?

Hello Investors - with Matthew Sigel 24 May 2017

Page 4 of 37

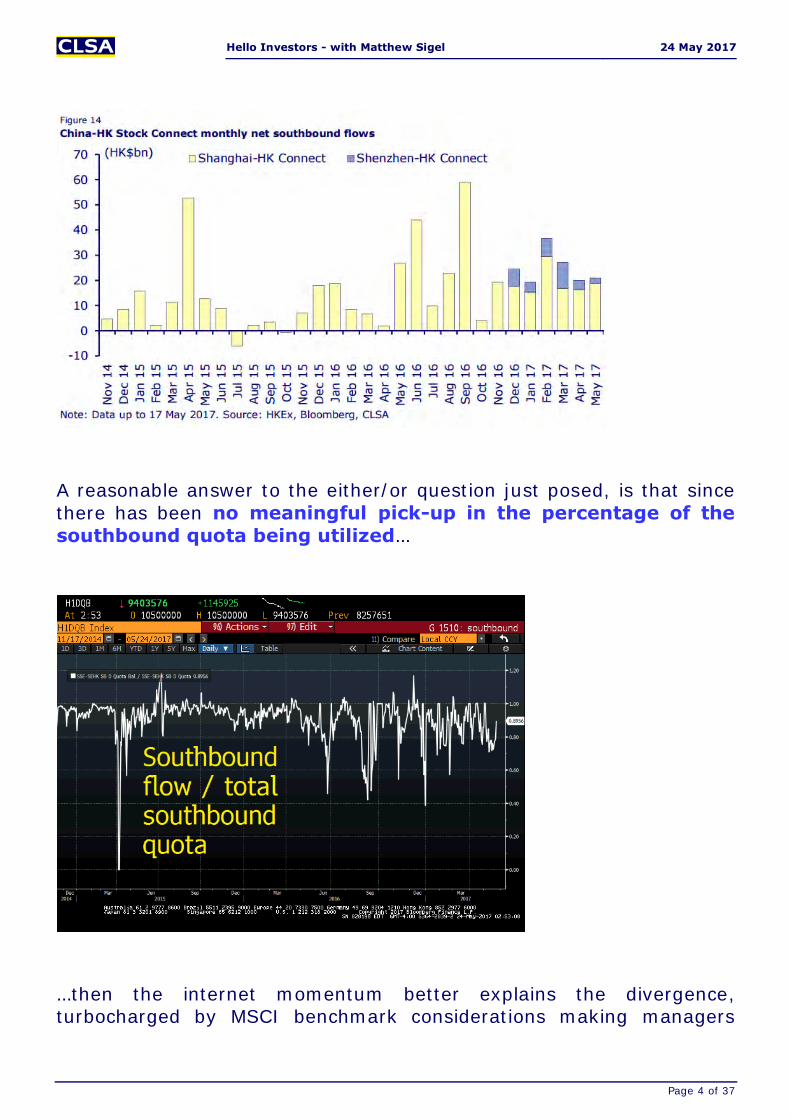

A reasonable answer to the either/or question just posed, is that since

there has been no meaningful pick-up in the percentage of the

southbound quota being utilized…

…then the internet momentum better explains the divergence, turbocharged by MSCI benchmark considerations making managers

Hello Investors - with Matthew Sigel 24 May 2017

Page 5 of 37

more willing own even more of what were previously “off benchmark” bets…

…and asset owners more willing to push chunky allocations into an

“asset class" still marked by seemingly stunning cheap valuation…

…with better relative returns to boot!

Hello Investors - with Matthew Sigel 24 May 2017

Page 6 of 37

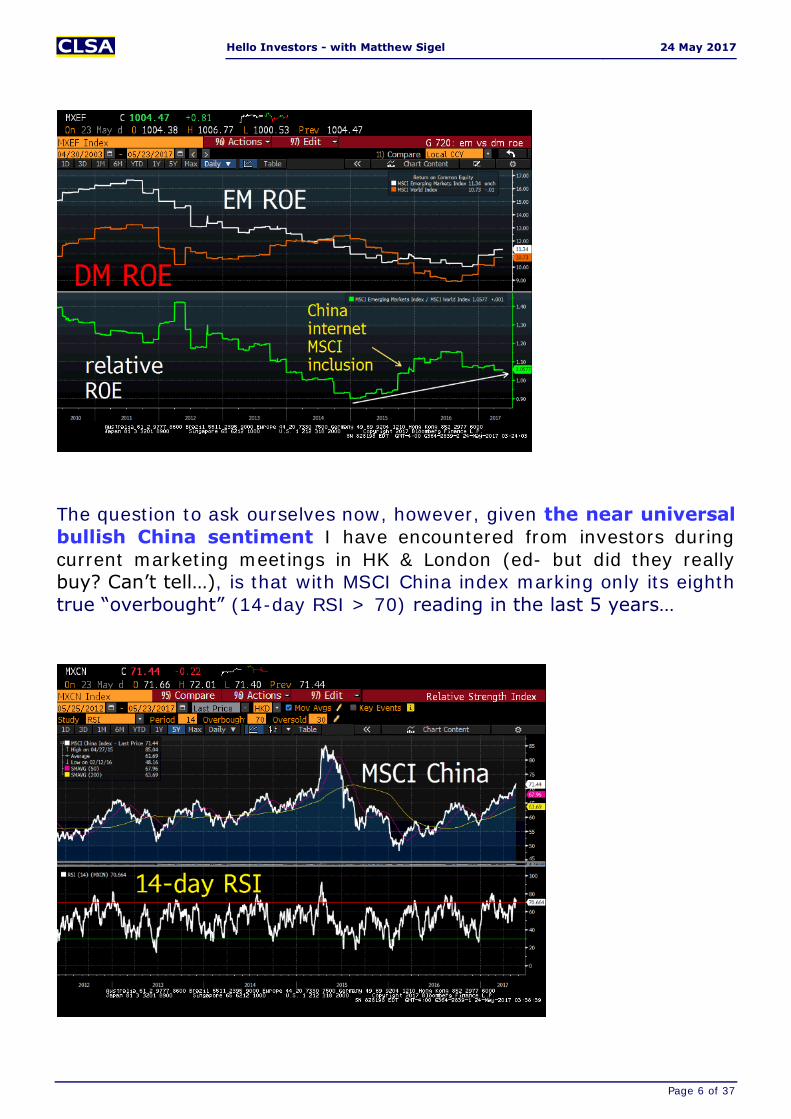

The question to ask ourselves now, however, given the near universal

bullish China sentiment I have encountered from investors during

current marketing meetings in HK & London (ed- but did they really buy? Can’t tell…), is that with MSCI China index marking only its eighth

true “overbought” (14-day RSI > 70) reading in the last 5 years…

Hello Investors - with Matthew Sigel 24 May 2017

Page 7 of 37

…and the spread between that index and the domestic Chinese price of iron ore (a key barometer for the direction of China macro) having once

again reached a level of divergence which presaged the last tactical

index correction in Q4 of last year ... should you take some off the

table, especially from the high flyers?

Hello Investors - with Matthew Sigel 24 May 2017

Page 8 of 37

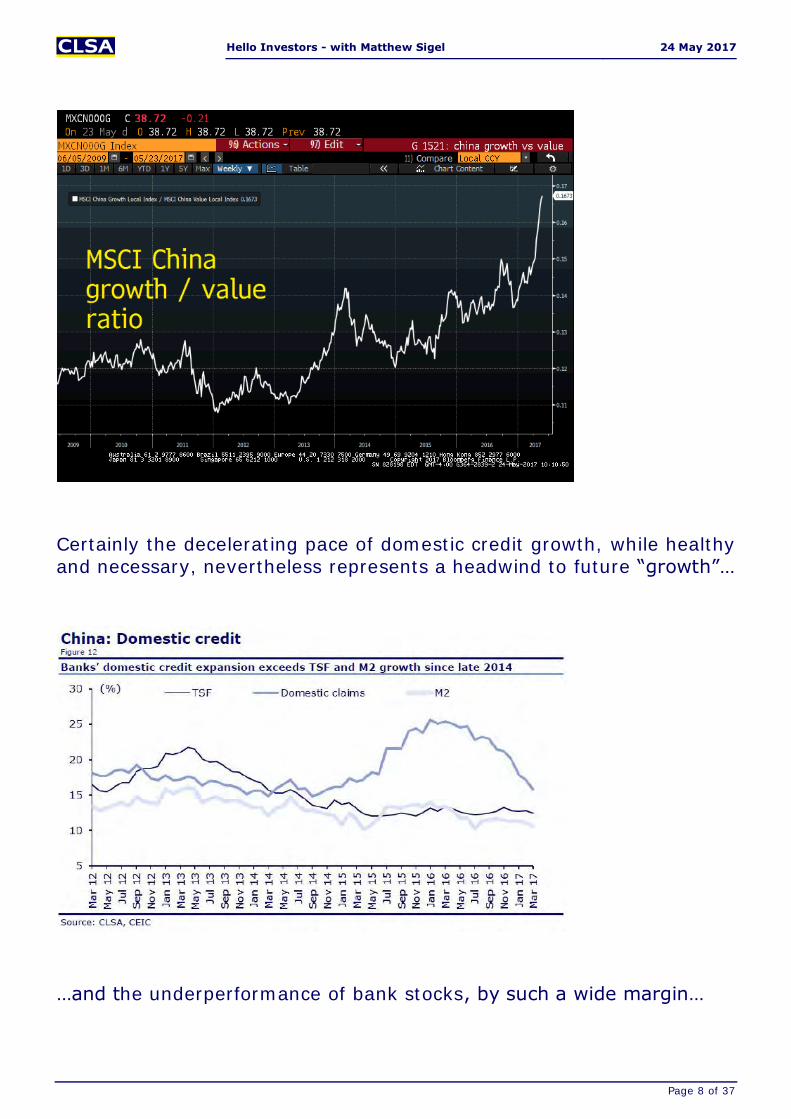

Certainly the decelerating pace of domestic credit growth, while healthy and necessary, nevertheless represents a headwind to future “growth”…

…and the underperformance of bank stocks, by such a wide margin…

Hello Investors - with Matthew Sigel 24 May 2017

Page 9 of 37

…reflects forward expectations that NPL ratio can’t improve much more…

…and that increasingly inverted portions of the yield curve…

Hello Investors - with Matthew Sigel 24 May 2017

Page 10 of 37

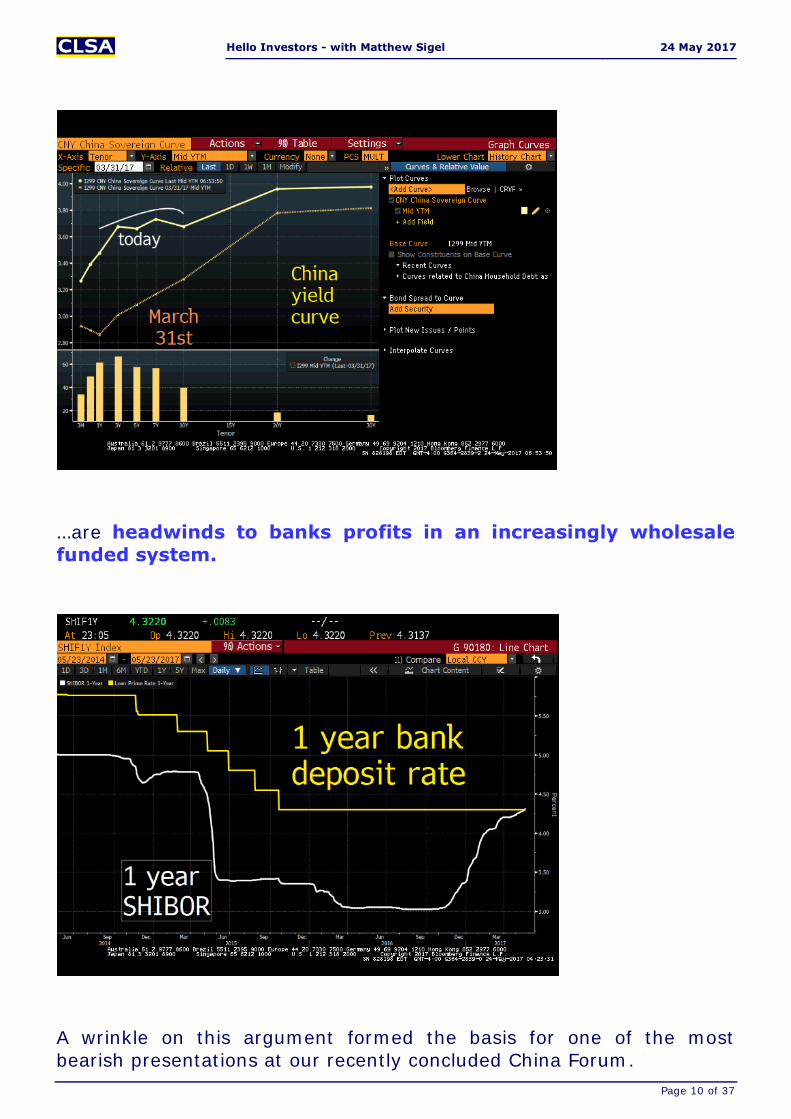

…are headwinds to banks profits in an increasingly wholesale

funded system.

A wrinkle on this argument formed the basis for one of the most

bearish presentations at our recently concluded China Forum.

Hello Investors - with Matthew Sigel 24 May 2017

Page 11 of 37

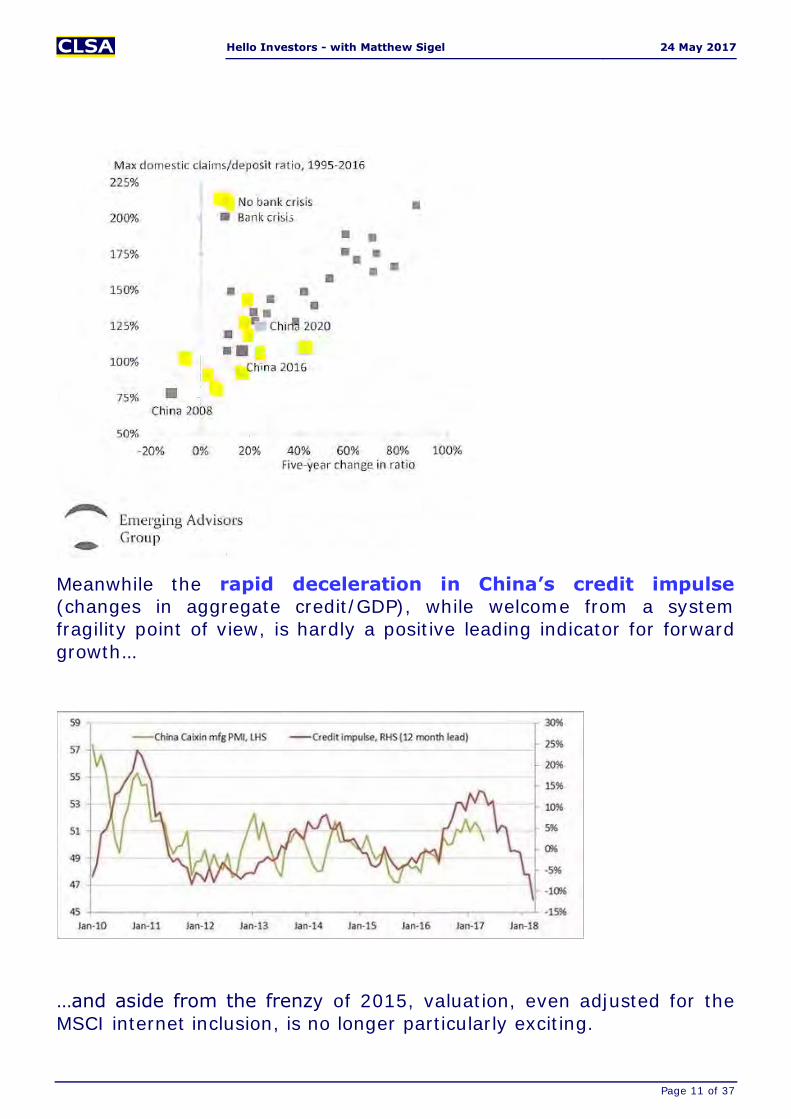

Meanwhile the rapid deceleration in China’s credit impulse (changes in aggregate credit/GDP), while welcome from a system

fragility point of view, is hardly a positive leading indicator for forward

growth…

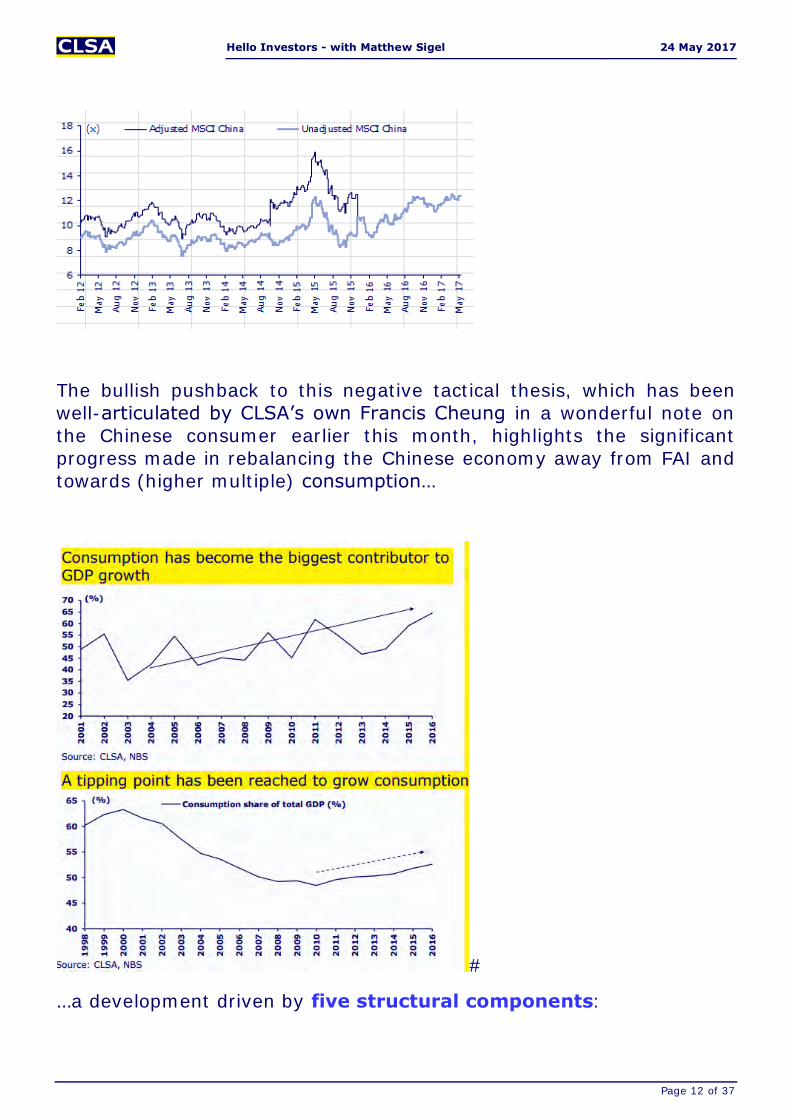

…and aside from the frenzy of 2015, valuation, even adjusted for the

MSCI internet inclusion, is no longer particularly exciting.

Hello Investors - with Matthew Sigel 24 May 2017

Page 12 of 37

The bullish pushback to this negative tactical thesis, which has been

well-articulated by CLSA’s own Francis Cheung in a wonderful note on

the Chinese consumer earlier this month, highlights the significant

progress made in rebalancing the Chinese economy away from FAI and

towards (higher multiple) consumption…

#

…a development driven by five structural components:

Hello Investors - with Matthew Sigel 24 May 2017

Page 13 of 37

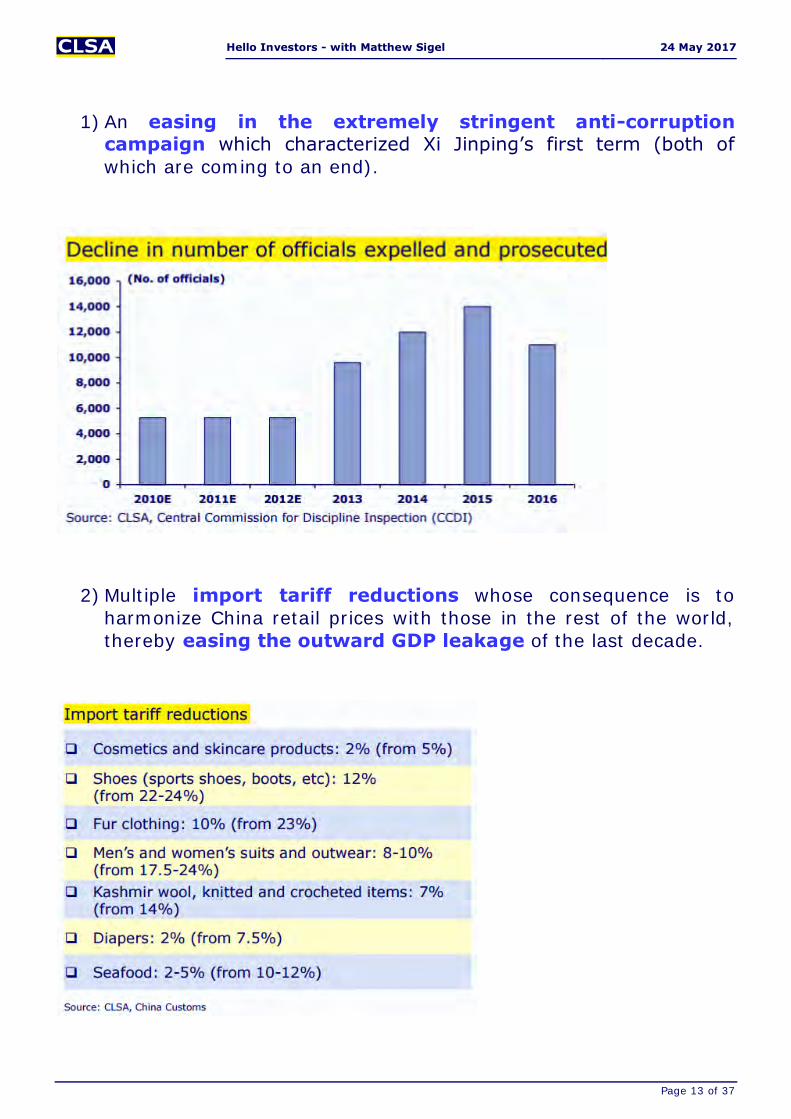

1) An easing in the extremely stringent anti-corruption campaign which characterized Xi Jinping’s first term (both of

which are coming to an end).

2) Multiple import tariff reductions whose consequence is to

harmonize China retail prices with those in the rest of the world,

thereby easing the outward GDP leakage of the last decade.

Hello Investors - with Matthew Sigel 24 May 2017

Page 14 of 37

3) A baby boom engineered by one child policy reforms and a favorable horoscope

4) An improved social safety net which has seen the social security

fund balance double since 2011

Hello Investors - with Matthew Sigel 24 May 2017

Page 15 of 37

5) And, perhaps most importantly, a dramatic property-driven

wealth effect, in which the cultural preference for home

ownership…

Hello Investors - with Matthew Sigel 24 May 2017

Page 16 of 37

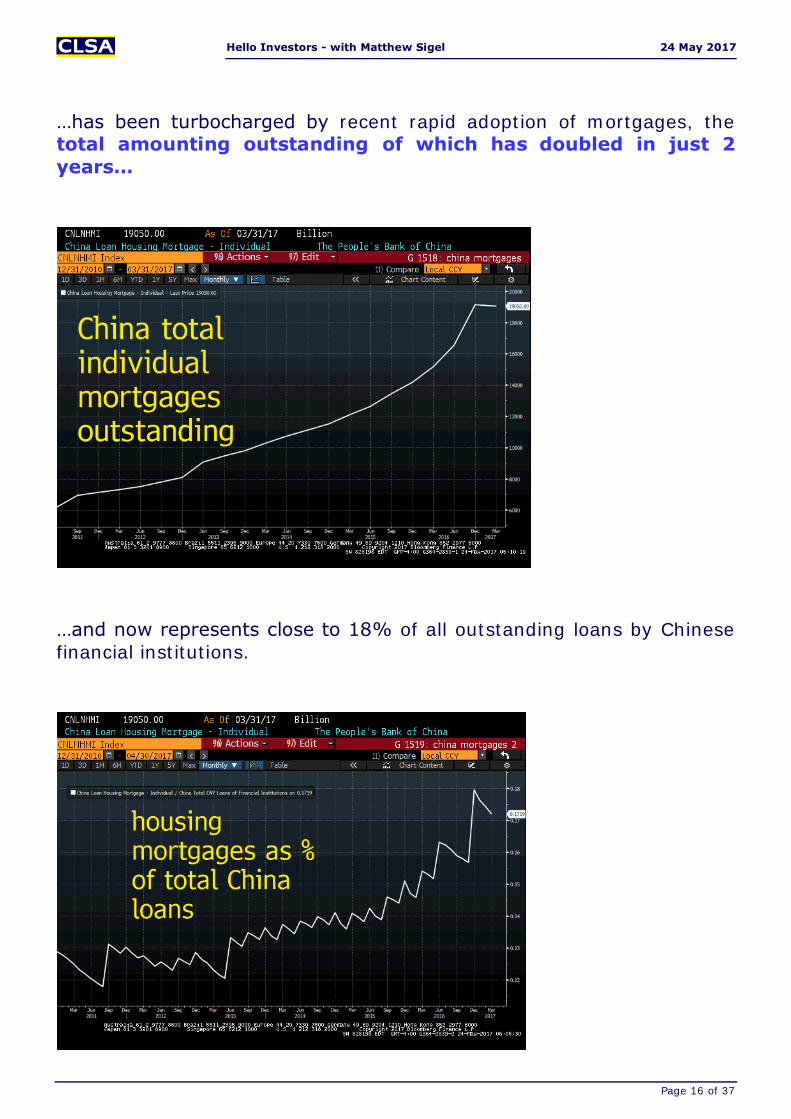

…has been turbocharged by recent rapid adoption of mortgages, the total amounting outstanding of which has doubled in just 2

years…

…and now represents close to 18% of all outstanding loans by Chinese

financial institutions.

Hello Investors - with Matthew Sigel 24 May 2017

Page 17 of 37

The acceleration in mortgage adoption (albeit at largely

conservative 50-70% LTVs), which began really in 2015 with the end of

the last property tightening cycle, corresponds perfectly to this

survey by the PBOC, which asks Chinese consumers if they prefer to

spend more or invest more.

And, although the rapid acceleration in mortgage penetration has

moved China’s household debt ratio sharply higher vs. recent history…

Hello Investors - with Matthew Sigel 24 May 2017

Page 18 of 37

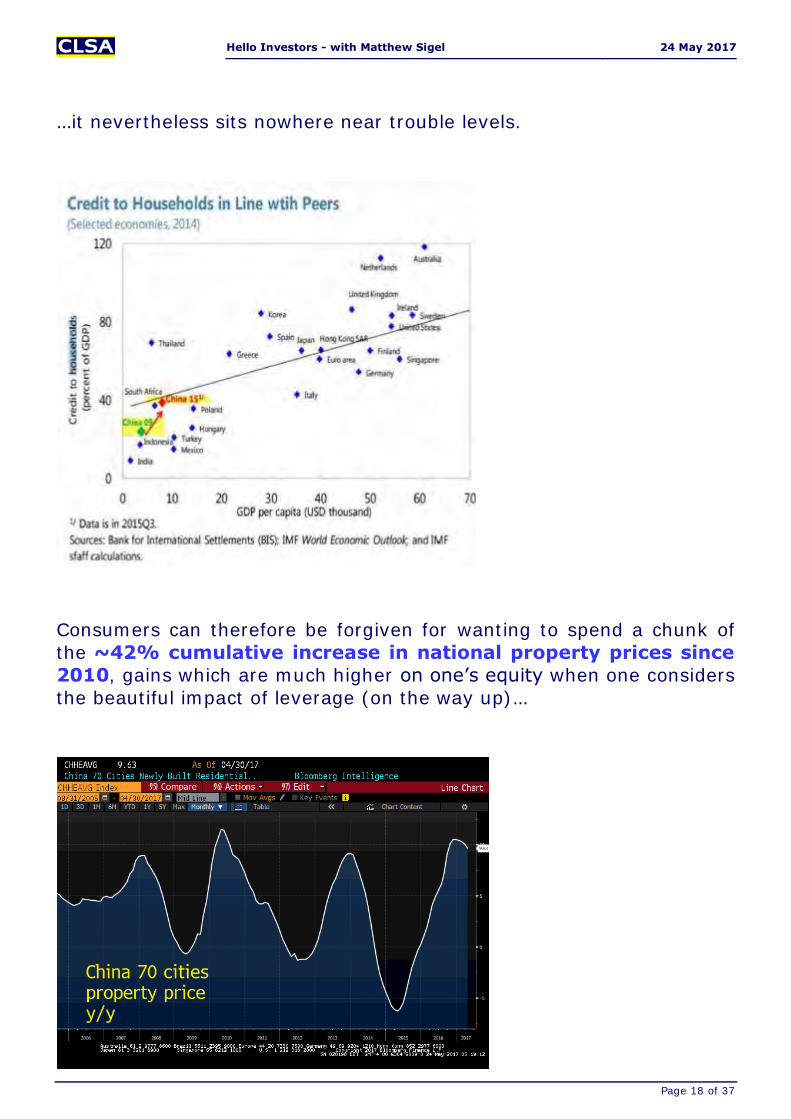

…it nevertheless sits nowhere near trouble levels.

Consumers can therefore be forgiven for wanting to spend a chunk of

the ~42% cumulative increase in national property prices since

2010, gains which are much higher on one’s equity when one considers

the beautiful impact of leverage (on the way up)…

Hello Investors - with Matthew Sigel 24 May 2017

Page 19 of 37

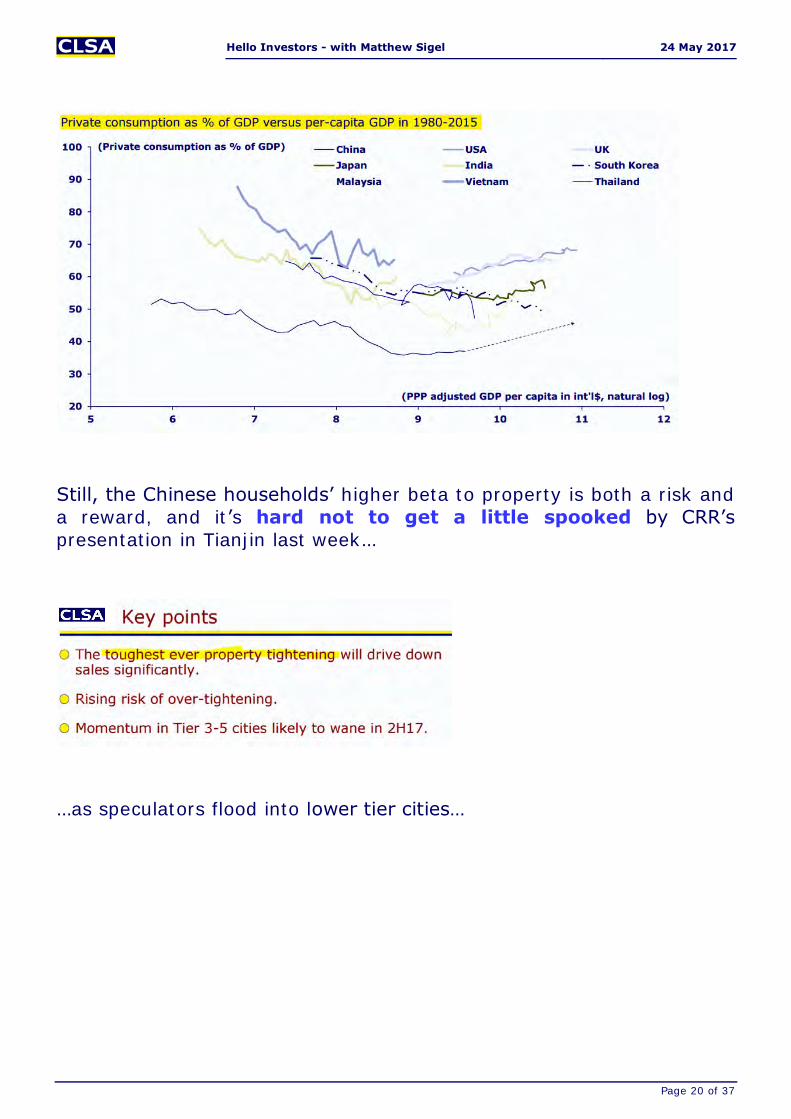

…given the higher beta that Chinese households have to the asset class.

In the absence of a property crash which supply/demand does not

seem to support, further consumption catch-ups look likely long term

given low per capita GDP levels.

Hello Investors - with Matthew Sigel 24 May 2017

Page 20 of 37

Still, the Chinese households’ higher beta to property is both a risk and

a reward, and it’s hard not to get a little spooked by CRR’s

presentation in Tianjin last week…

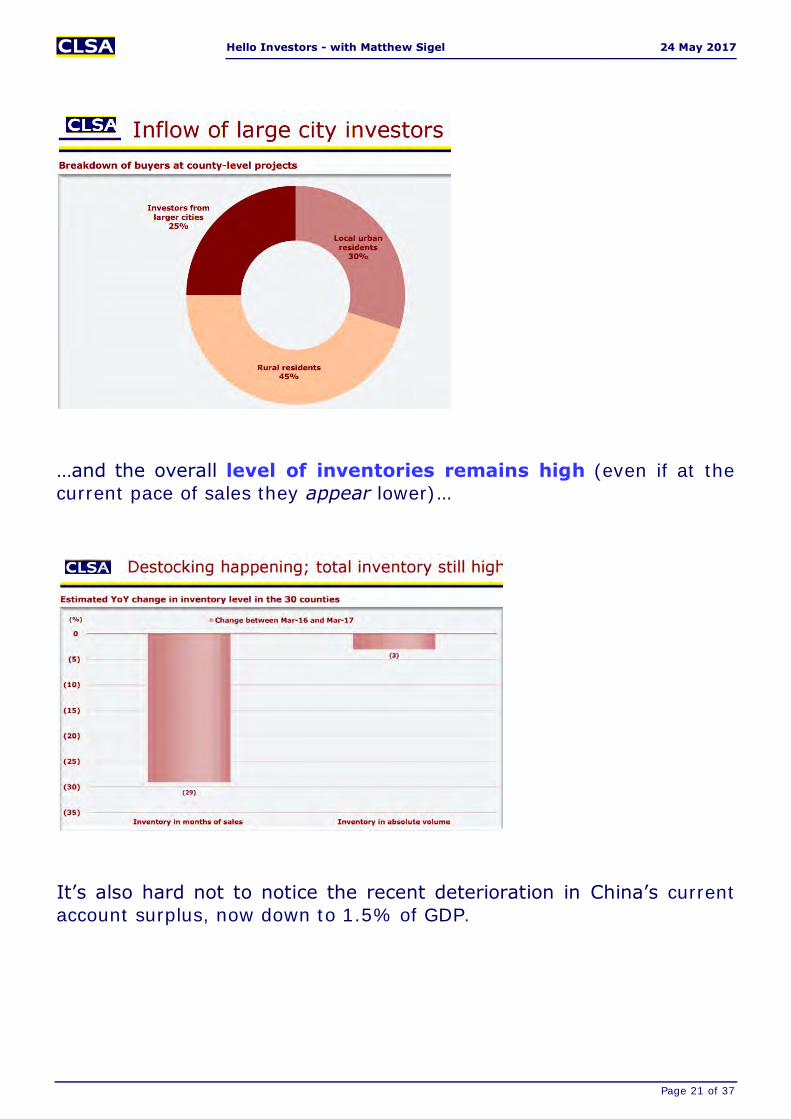

…as speculators flood into lower tier cities…

Hello Investors - with Matthew Sigel 24 May 2017

Page 21 of 37

…and the overall level of inventories remains high (even if at the

current pace of sales they appear lower)…

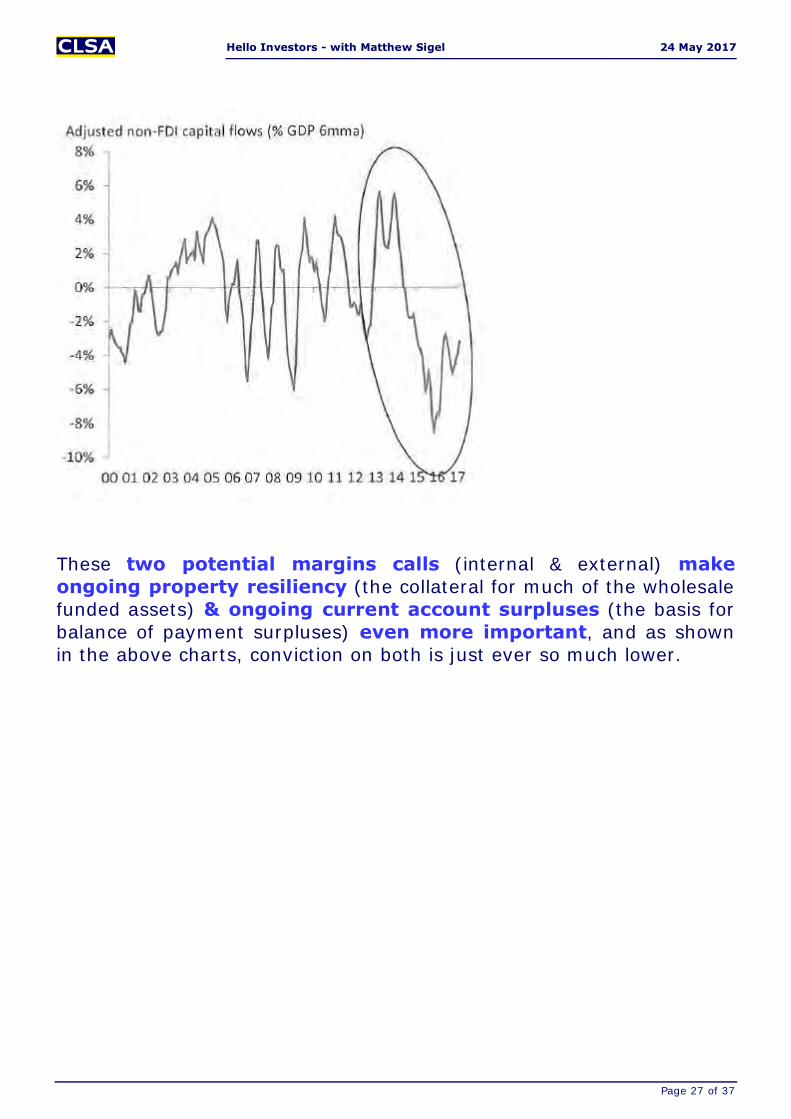

It’s also hard not to notice the recent deterioration in China’s current

account surplus, now down to 1.5% of GDP.

Hello Investors - with Matthew Sigel 24 May 2017

Page 22 of 37

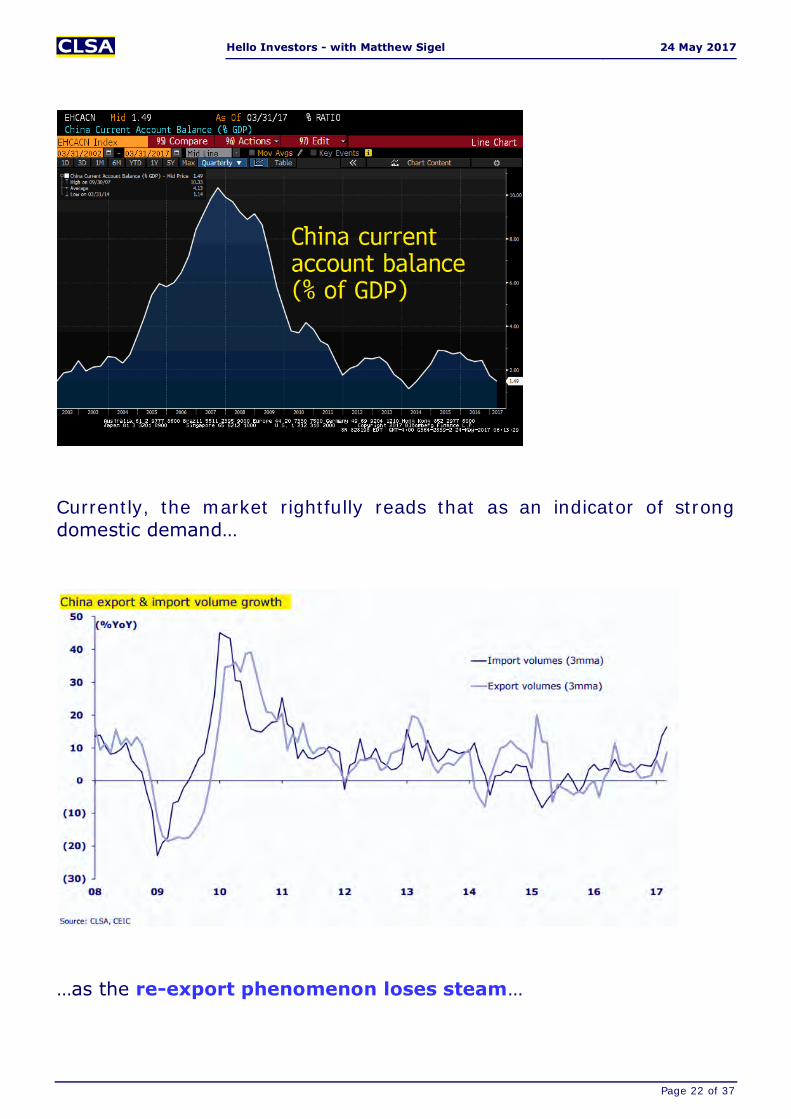

Currently, the market rightfully reads that as an indicator of strong

domestic demand…

…as the re-export phenomenon loses steam…

Hello Investors - with Matthew Sigel 24 May 2017

Page 23 of 37

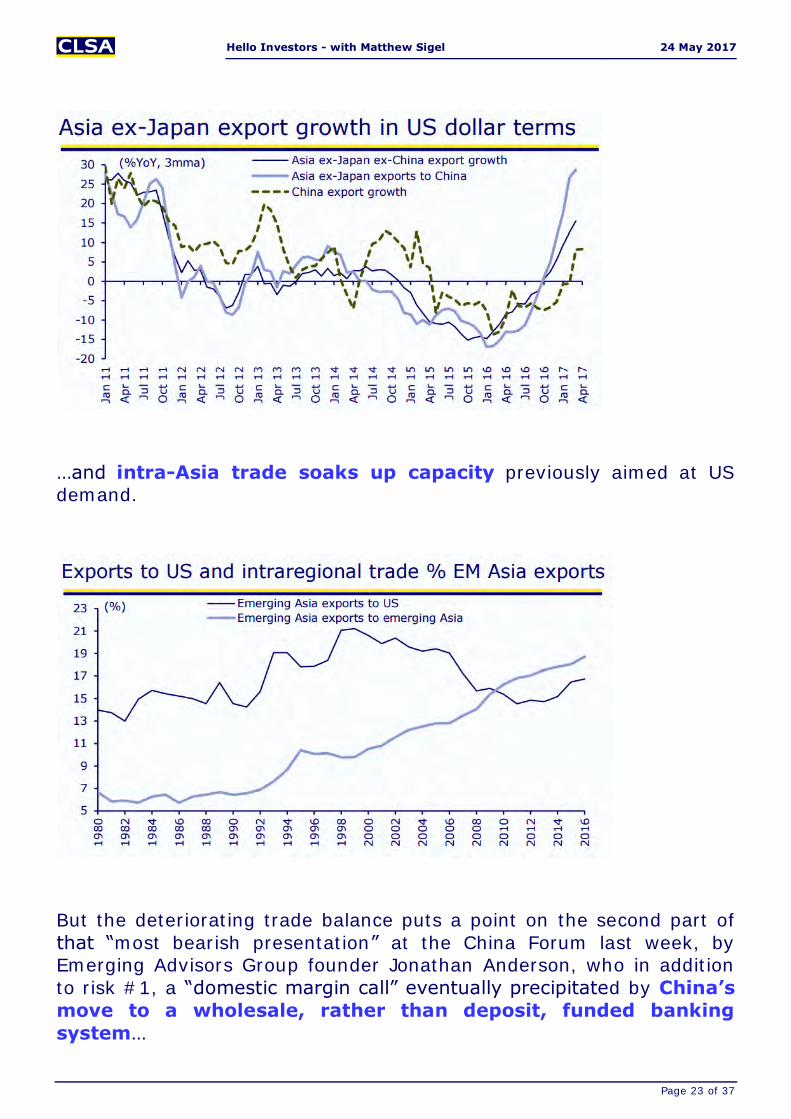

…and intra-Asia trade soaks up capacity previously aimed at US demand.

But the deteriorating trade balance puts a point on the second part of

that “most bearish presentation” at the China Forum last week, by Emerging Advisors Group founder Jonathan Anderson, who in addition

to risk #1, a “domestic margin call” eventually precipitated by China’s

move to a wholesale, rather than deposit, funded banking

system…

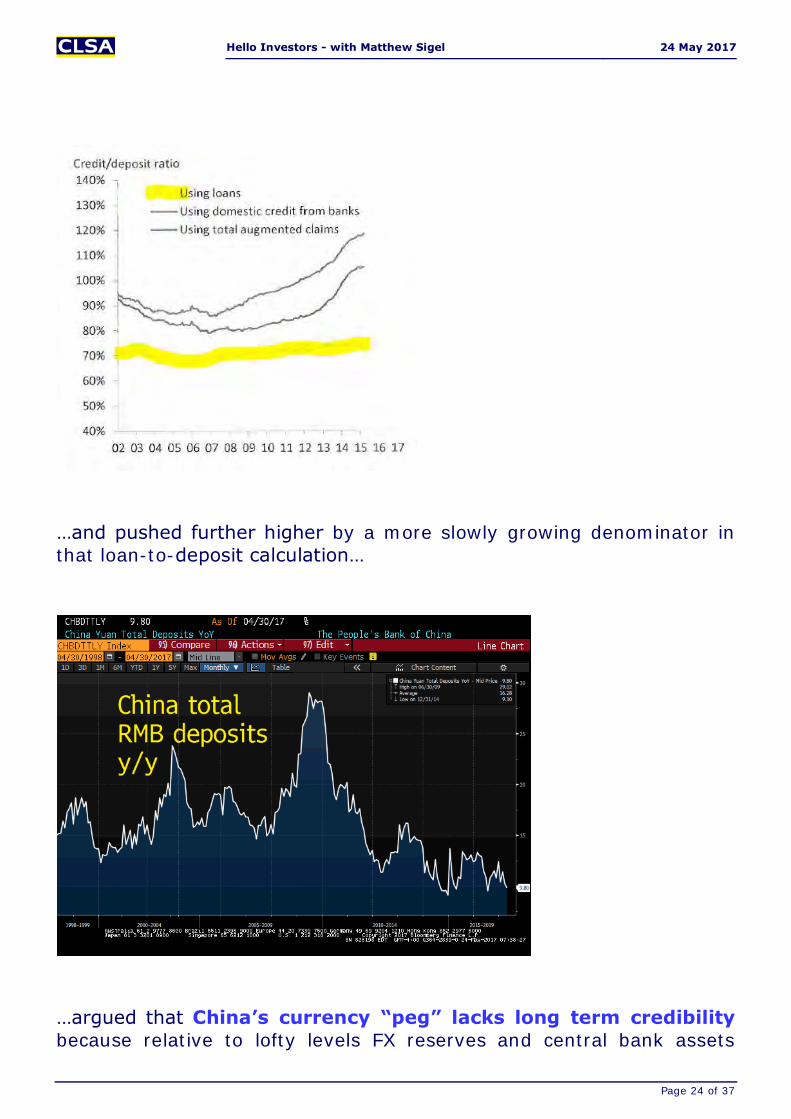

Hello Investors - with Matthew Sigel 24 May 2017

Page 24 of 37

…and pushed further higher by a more slowly growing denominator in

that loan-to-deposit calculation…

…argued that China’s currency “peg” lacks long term credibility

because relative to lofty levels FX reserves and central bank assets

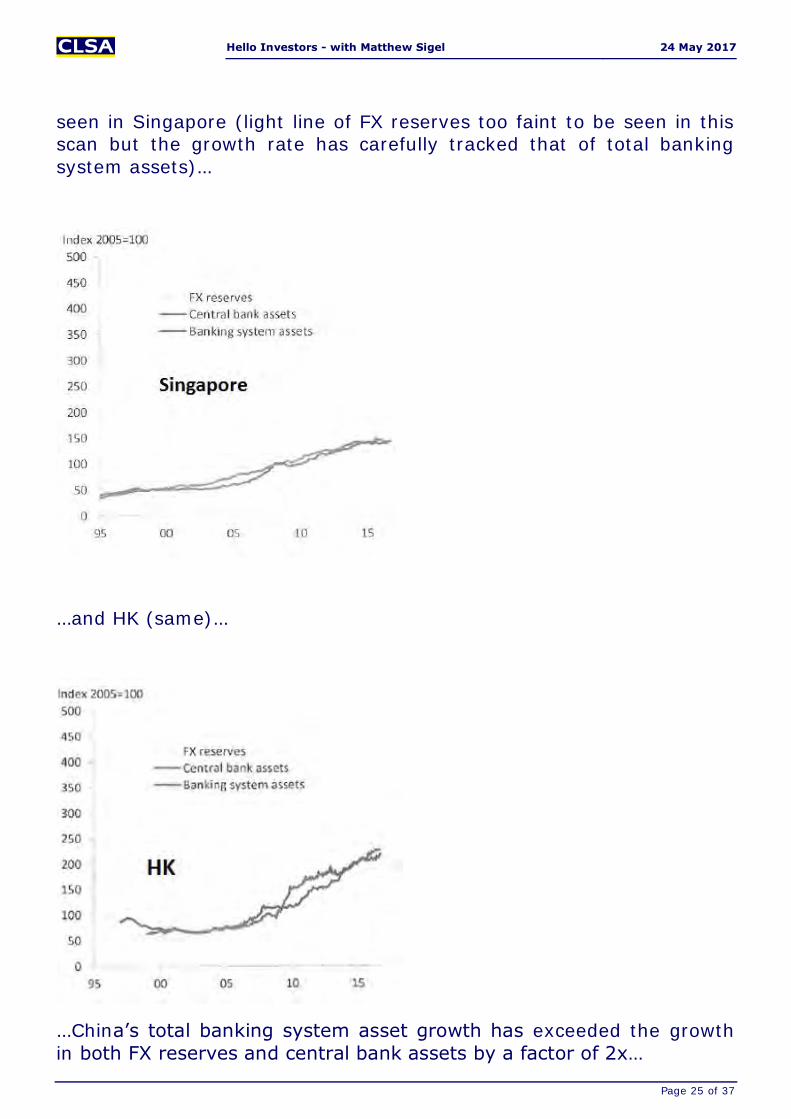

Hello Investors - with Matthew Sigel 24 May 2017

Page 25 of 37

seen in Singapore (light line of FX reserves too faint to be seen in this scan but the growth rate has carefully tracked that of total banking

system assets)…

…and HK (same)…

…China’s total banking system asset growth has exceeded the growth

in both FX reserves and central bank assets by a factor of 2x…

Hello Investors - with Matthew Sigel 24 May 2017

Page 26 of 37

…making the system more vulnerable to even small swings in capital flows…

…volatility of which has been more pronounced in recent years, not

less.

Hello Investors - with Matthew Sigel 24 May 2017

Page 27 of 37

These two potential margins calls (internal & external) make

ongoing property resiliency (the collateral for much of the wholesale

funded assets) & ongoing current account surpluses (the basis for

balance of payment surpluses) even more important, and as shown

in the above charts, conviction on both is just ever so much lower.

Hello Investors - with Matthew Sigel 24 May 2017

Page 28 of 37

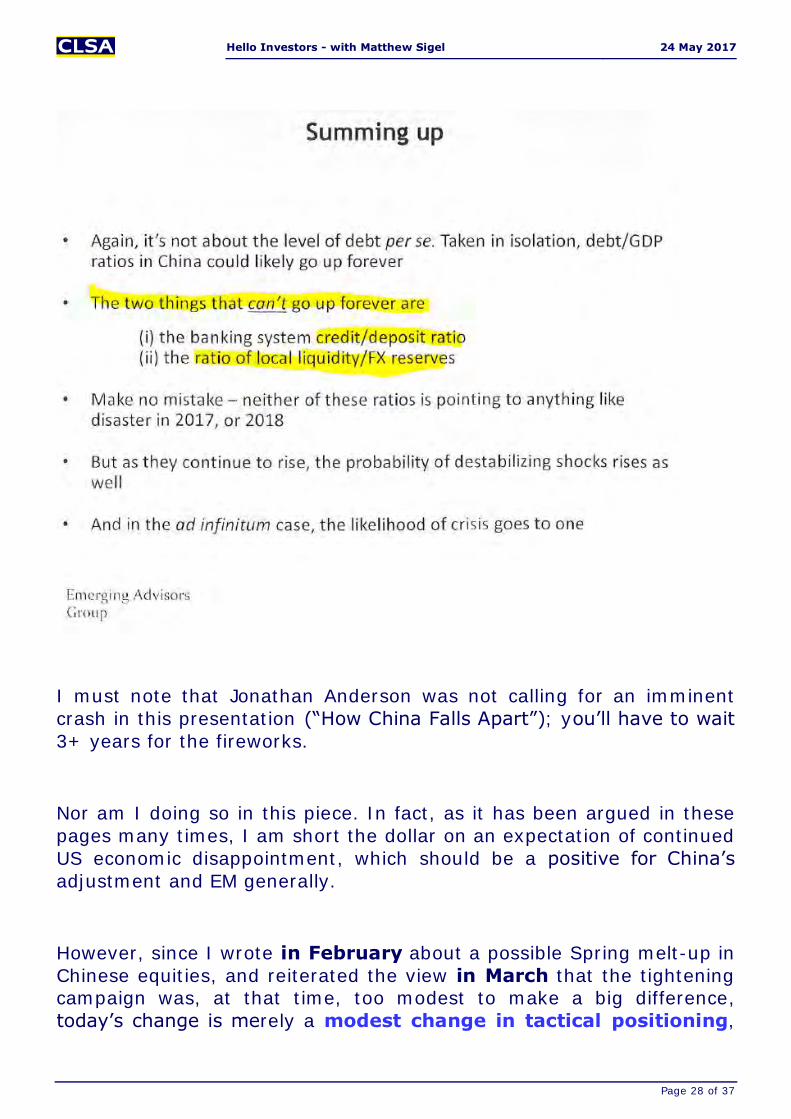

I must note that Jonathan Anderson was not calling for an imminent

crash in this presentation (“How China Falls Apart”); you’ll have to wait

3+ years for the fireworks.

Nor am I doing so in this piece. In fact, as it has been argued in these

pages many times, I am short the dollar on an expectation of continued

US economic disappointment, which should be a positive for China’s

adjustment and EM generally.

However, since I wrote in February about a possible Spring melt-up in

Chinese equities, and reiterated the view in March that the tightening campaign was, at that time, too modest to make a big difference,

today’s change is merely a modest change in tactical positioning,

Hello Investors - with Matthew Sigel 24 May 2017

Page 29 of 37

equivalent to a couple hundred basis points of trimming in EM-benchmarked portfolios, back to a neutral or so weighting.

It’s also important to note that as I am bearish on the US, H-shares could well outperform in a down US market, as long as the US decline

reflects a reset of growth/Fed hike expectations, but NOT a recession.

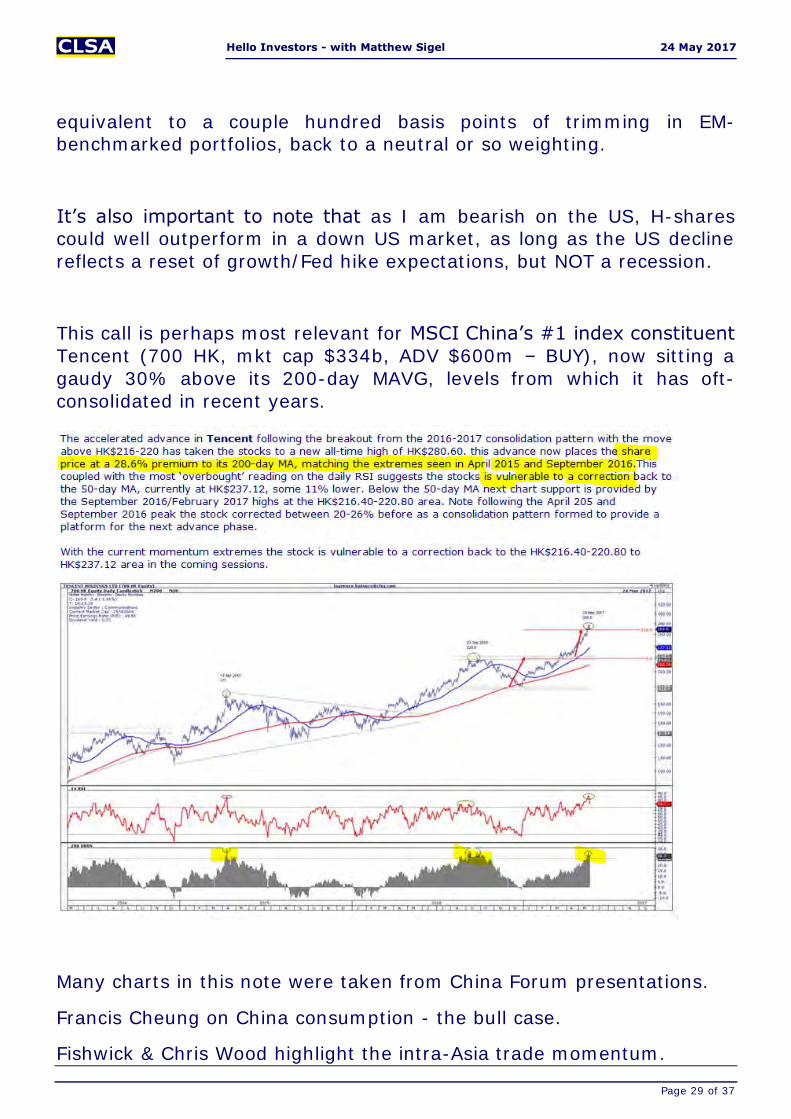

This call is perhaps most relevant for MSCI China’s #1 index constituent

Tencent (700 HK, mkt cap $334b, ADV $600m – BUY), now sitting a

gaudy 30% above its 200-day MAVG, levels from which it has oft-

consolidated in recent years.

Many charts in this note were taken from China Forum presentations.

Francis Cheung on China consumption - the bull case.

Fishwick & Chris Wood highlight the intra-Asia trade momentum.

Hello Investors - with Matthew Sigel 24 May 2017

Page 30 of 37

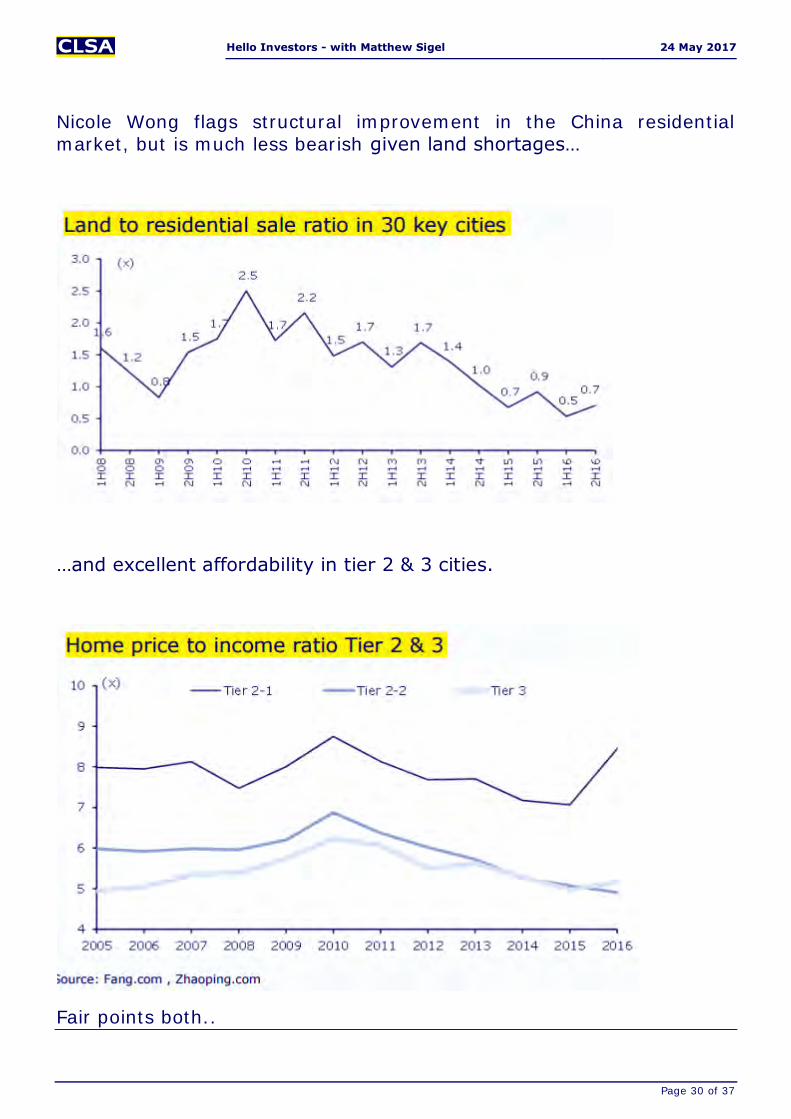

Nicole Wong flags structural improvement in the China residential market, but is much less bearish given land shortages…

…and excellent affordability in tier 2 & 3 cities.

Fair points both..

Hello Investors - with Matthew Sigel 24 May 2017

Page 31 of 37

Elinor Leung sees new catalysts for China internet (VIPS & BIDU are cheapest on PEG).

Nelson Wang sees slowing China oil demand but accelerating gas

demand and robust refining earnings; HELLO INVESTORS would put

some of your Tencent proceeds into Sinopec (386 HK, mkt cap

$100b, ADV $65m) and wait for next year’s 20% FCF yield and 7%

dividend yield. Nelson’s presentation.

Rajesh Panjwani says the recent regulatory noise about capping

downstream gas distributor margins is mostly (but not all) hot air. BUY

CR Gas and ENN.

We have new A-share tech coverage from Nick Feng & team on

Hikvision, Lens Tech and Wangsu. It’s time to get to know some of

these names before MSCI forces you to.

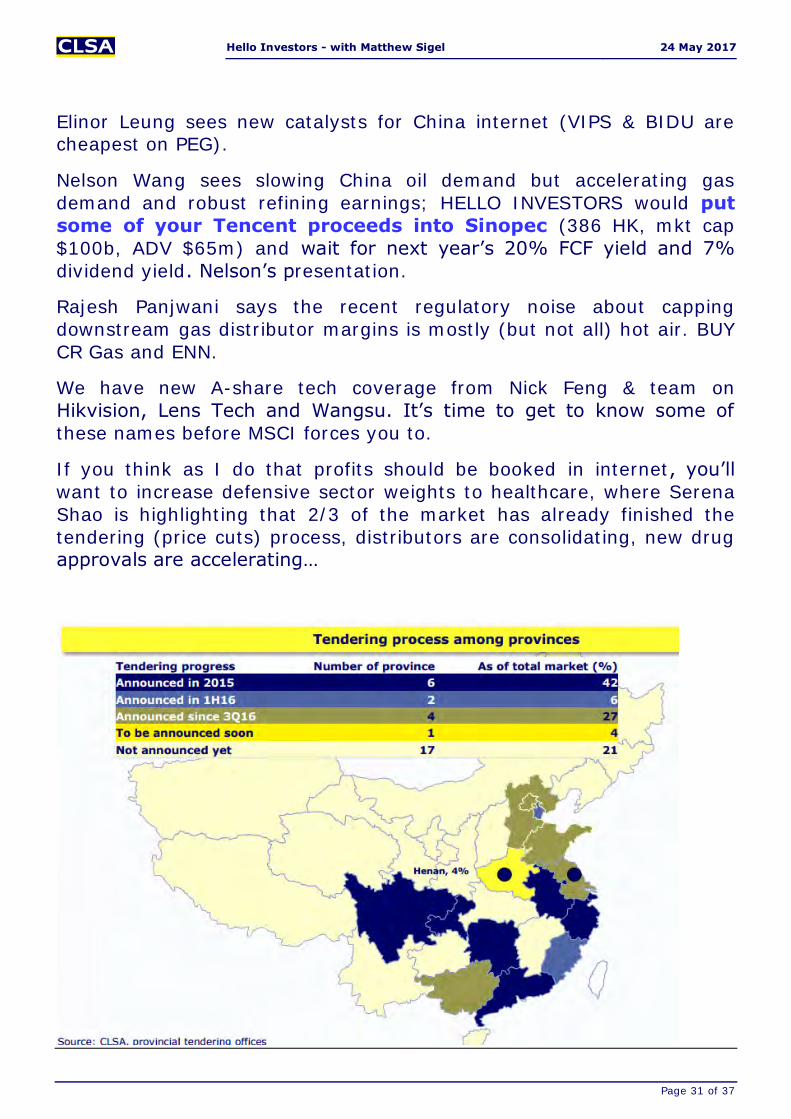

If you think as I do that profits should be booked in internet, you’ll

want to increase defensive sector weights to healthcare, where Serena

Shao is highlighting that 2/3 of the market has already finished the

tendering (price cuts) process, distributors are consolidating, new drug approvals are accelerating…

Hello Investors - with Matthew Sigel 24 May 2017

Page 32 of 37

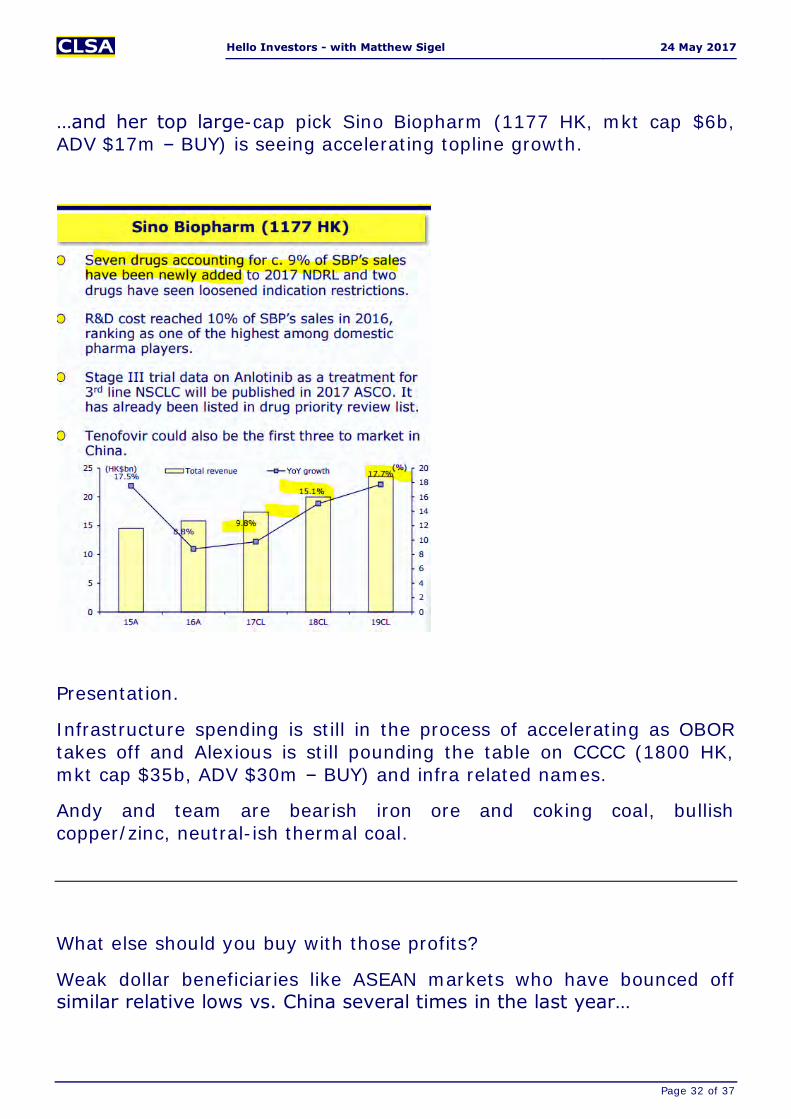

…and her top large-cap pick Sino Biopharm (1177 HK, mkt cap $6b, ADV $17m – BUY) is seeing accelerating topline growth.

Presentation.

Infrastructure spending is still in the process of accelerating as OBOR

takes off and Alexious is still pounding the table on CCCC (1800 HK,

mkt cap $35b, ADV $30m – BUY) and infra related names.

Andy and team are bearish iron ore and coking coal, bullish

copper/zinc, neutral-ish thermal coal.

What else should you buy with those profits?

Weak dollar beneficiaries like ASEAN markets who have bounced off similar relative lows vs. China several times in the last year…

Hello Investors - with Matthew Sigel 24 May 2017

Page 33 of 37

…with Singapore banks, for example, seeing recovering loan growth

but with 6 months more of very easy comps…

Hello Investors - with Matthew Sigel 24 May 2017

Page 34 of 37

…and lovely revisions meaning…

…valuation has barely budged.

Hello Investors - with Matthew Sigel 24 May 2017

Page 35 of 37

And Japanese internet stocks whose multiples & customers’ purchasing power would see downside protection given the strong Yen and lower

interest rates which would likely accompany any reversion in Chinese

risk appetite, but who would likely see some upside capture if I am

wrong, given the intra-sector correlation.

JayDefibaugh likes Cyberagent (4751 JP, mkt cap $4b, ADV $34m –

BUY) for its dominance in internet advertising, penetration of which is low in Japan but rising fast.

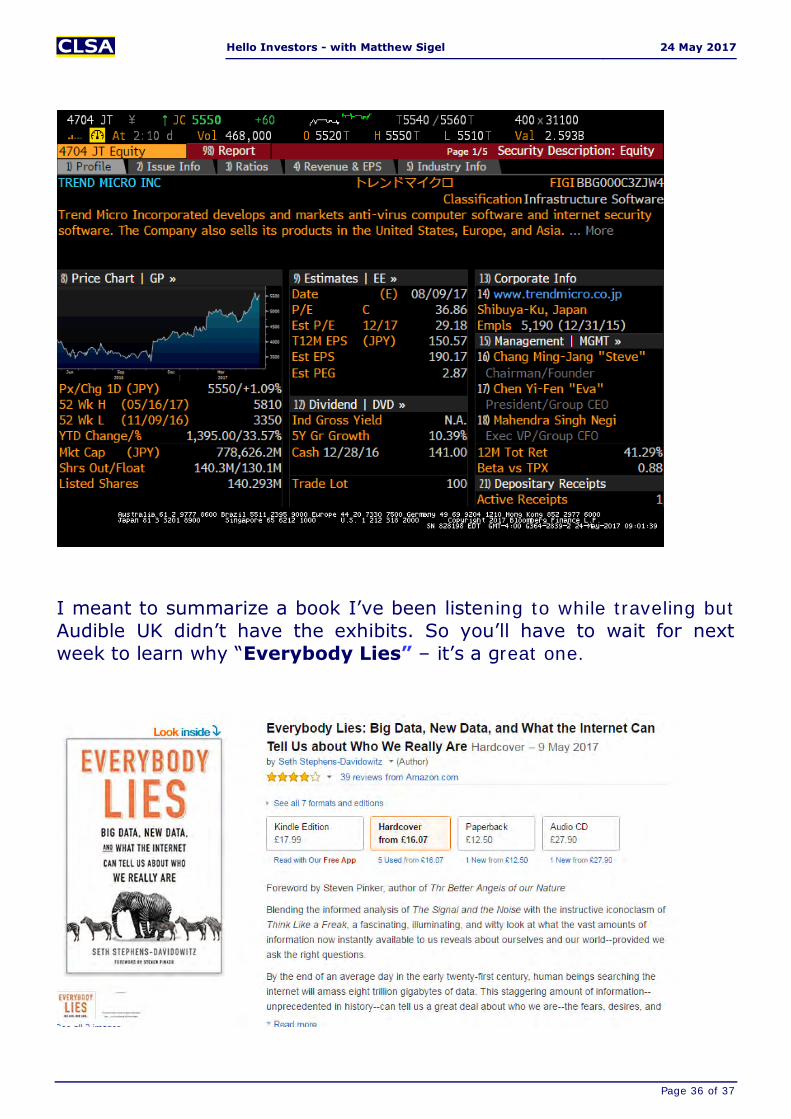

Trend Micro (4740 JP, mkt cap $7b, ADV $40m – OUTPERFORM) has also had a nice run but is supported by its strong secular tailwinds

given the world’s focus on cybersecurity, its 8% FCF yield, rock solid

balance sheet, higher growth trajectory vs. the last 5 years thanks to

well-executed M&A and lower reliance on endpoint security as they

transition to more of an enterprise company, and high recurring

revenue stream.

Hello Investors - with Matthew Sigel 24 May 2017

Page 36 of 37

I meant to summarize a book I’ve been listening to while traveling but

Audible UK didn’t have the exhibits. So you’ll have to wait for next

week to learn why “Everybody Lies” – it’s a great one.

Hello Investors - with Matthew Sigel 24 May 2017

Page 37 of 37

Important disclosures:

This document is for information purposes only and is not a solicitation or any offer to buy or sell. This document was written by a sales/trading person(s) and not an analyst. It does not constitute research, nor should it be interpreted as such, and is not intended to provide professional, investment or any other type of advice or recommendation. The views contained in this document are the sales/trading person’s personal views which may or may not differ from the official views and interests of CLSA. Such personal views may differ from the opinions expressed by other divisions of CLSA including our investment research department. The views expressed are based on information that was collected using one or more of the following: consensus data, independent information sources and information provided by the company. Although care was taken as to the veracity of such information, CLSA does not guarantee and makes no representations as to its accuracy, completeness or correctness. The sales/trading person does not undertake any obligation to update the material in this report. You should make your own independent evaluation of the relevance and adequacy of the information contained in this report and make such other investigations as you deem necessary, including obtaining independent financial advice. This document is intended to be distributed into the United States of America by CLSA solely to persons who qualify as “Major U.S. Institutional Investors” as defined in Rule 15a-6 under the Securities and Exchange Act of 1934, as amended, and who deal with CLSA Americas, LLC. However, the delivery of this document to any person in the United States shall not be deemed a recommendation to effect any transactions in the securities discussed herein or an endorsement of any opinion expressed herein. Any recipient of this document in the United States wishing to effect a transaction in any security mentioned herein should do so by contacting CLSA Americas, LLC (a broker-dealer registered with the Securities and Exchange Commission) and an affiliate of CLSA. This document is being distributed as a marketing communication. When distributed in the EU this document is for persons having professional experience in matters relating to investments as defined in Article 19 of the FSMA 2000 (Financial Promotion) Order 2005. If you do not have professional experience in matters relating to investments you should not rely on this document. This document is intended to be distributed in Singapore through CLSA Singapore Pte Ltd to institutional investors, accredited investors, expert investors or overseas investors only, each as defined under Section 4A(1) of the Securities and Futures Act (Cap. 289). Pursuant to Paragraphs 33, 34, 35 and 36 of the Financial Advisers Regulations of the Financial Advisers Act (Cap 110) with regards to an institutional investor, accredited investor, expert investor or overseas investor, sections 25, 27 and 36 of the Financial Adviser Act (Cap 110) shall not apply to CLSA Singapore Pte Ltd. The distribution of this material in other jurisdictions may be restricted by law and persons into whose possession this material comes should inform themselves about and observe any such restrictions.

IMPORTANT: © CLSA Limited. The content of this document is subject to CLSA's Legal and Regulatory

Notices as set out at www.clsa.com/disclaimer.html, a hard copy of which may be obtained on request from CLSA Publications or CLSA Compliance Group, 18/F, One Pacific Place, 88 Queensway, Hong Kong, telephone (852) 2600 8888. Neither the document nor any portion hereof may be reprinted, sold, resold, copied, reproduced, distributed, redistributed, published, republished, displayed, posted or transmitted in any form or media or by any means without the written consent of CLSA.