hedging against risk in the wholesale energy...

TRANSCRIPT

Hedging Against Risk in the

Wholesale Energy Markets

Presentation for the

Wisconsin Public Utility Institute

Enrique Bacalao, Chief Economist

Public Service Commission of Wisconsin

May 17, 2018

The views expressed in this presentation

and in my comments are mine alone,

and are not those of the

Public Service Commission of Wisconsin.

2

Presentation Agenda

• Overview of the Topic

• The Nature of Risk and of its Mitigation

• Using Financial Hedging to Mitigate Risks

• Types of Financial Hedging Instruments

• Applicability to the Wholesale Energy Market

• Uses and Abuses of Financial Hedging Instruments

3

Overview of the Topic

4

Evolution of Wholesale Energy Markets

Implications for traditional public utilities:

• Competitive resource allocation

• Transparent pricing signals (generation and transmission)

• Diversification of sources and loads (lowering risk profiles)

• Achieving economies of scale (affecting costs and innovation)

• Regional oversight and control (complementing state-level regulation)

Impact on:

• Availability of assets (diversification and economies of scale)

• Pricing of products and services (transparency and scale)

• Recognition of value added5

Consequences of Wholesale Energy Markets

Changes in how we do business:

• Planning and adapting the generation fleet

• Dispatching generating units

• Securing transmission services

• Pricing transmission services

Impacts:

• Reliance on other utilities for generation and transmission

• Variability of pricing and likelihood of proper performance

• Rate of return earned from operations

• Volatility and predictability of earnings6

The Nature of Risk

and of its Mitigation

7

What is Risk?

Variance of actual outcomes compared to the expected outcome

• Variability of future outcomes

• Absolute values of variance (standard deviations)

Operating variables

• Volumetric (physical units)

• Pricing (dollars)

• Timing (premature or delayed occurrence)

• Geographic (situs or delivery location)

Financial variables

• Variance of magnitude and direction of expected cash flows

• Variance in the timing of those cash flows 8

Risk is Variance

Using a classical bell-shaped symmetrical distribution curve to illustrate the point:

• The expected value for any operational or financial variable is the central value μ.

• Because this distribution curve is symmetrical, that value is both the mean and the median of expected / possible outcomes.

• Risk is the variance on both sides of that expected value μ.

• If the actual outcome might not turn out to be the expected value of μ, regardless of whether its above or below μ, you are exposed to risk.

• The shape of the distribution curve describes the risk exposure being faced.

9

Risk is Variance

Needless to say, not all distribution curves (risk profiles) are equally dispersed (degree of variance or riskiness).

• The shape of the distribution curve describes the risk exposure being faced.

• The skinnier distribution curve (blue in this particular example) has the narrowest range of dispersion, and therefore the smallest variance. As a result, it describes the smallest degree of risk because the distribution of likely outcomes is tighter around the expected central value.

• In increasing degrees of risk, the green curve, the red curve and the tan curve have progressively broader variance ranges, and therefore increasing ranges of possible outcomes.

10

Risk is Variance

Needless to say, not all distribution curves (risk profiles) are symmetrical.

• The relative likelihood may not be symmetrical around an expected value (skewed in one direction or another)

• In this example, the blue curve describes a different range of likelihoods than the other four.

• The shape of the distribution curve describes the risk exposure being faced and suggests the type(s) of hedging that might be most effective.

• The variance associated with each of these curves establishes the relative risk associated with each of these expectation distribution curves.

11

How Does One Set Reasonable Expectations?

• By definition, future events are unknown and unknowable.

• That cannot, and should not, excuse any responsible manager from

taking a view of future events in order to mitigate risk.

• Use expected values:

• Rely on several sources (consultants, market values, etc.)

• Develop a reasonable value as one’s expected value

• Weight it by a subjective probability distribution

• Expected values will be wrong: the idea is to minimize the error.

• Resign yourself to folks applying 20/20 hindsight to judge you

• Write off buyer’s/seller’s regret as a sunk transaction cost

12

Forecasting is not Easy

• You rely on the past, knowing history doesn’t repeat itself exactly.

• You know that, the further out you push your forecasting horizon, the less accurate you are likely to be.

• You check to see what independent forecasters are expecting, but you’re not sure to what degree they, too, are relying on past patterns in forecasting the future.

• You check to see what financial markets reflect about expectations, but the markets tend to become thinner the farther out you go on the timeline.

13

Forecasting is not Easy

Multiple choice exam question:

• Those who do not learn the lessons of history are condemned to repeat its mistakes.

• History does not repeat itself exactly.

• History may not repeat itself exactly, but it certainly rhymes.

• All of the above.

14

Are the Past and Near-Term Expectations

a Good Guide for the Longer-Term Future?

15

Near-term perspective

Long-term perspective

How Does One Mitigate Risk?

• FACT: one cannot eliminate risk: one can only mitigate it

• Analyze the particular risk in its fullest context

• Identify the individual components that create the risk

• Evaluate how best to constrain the associated variance, considering:• Risk effectiveness of each alternative

• Cost effectiveness of each alternative

• Check for unintended or perverse consequences

• Establish a periodic review protocol, as appropriate

• Plan for a potential counterparty default

• Execute the hedge and write off any regrets as a sunk cost

16

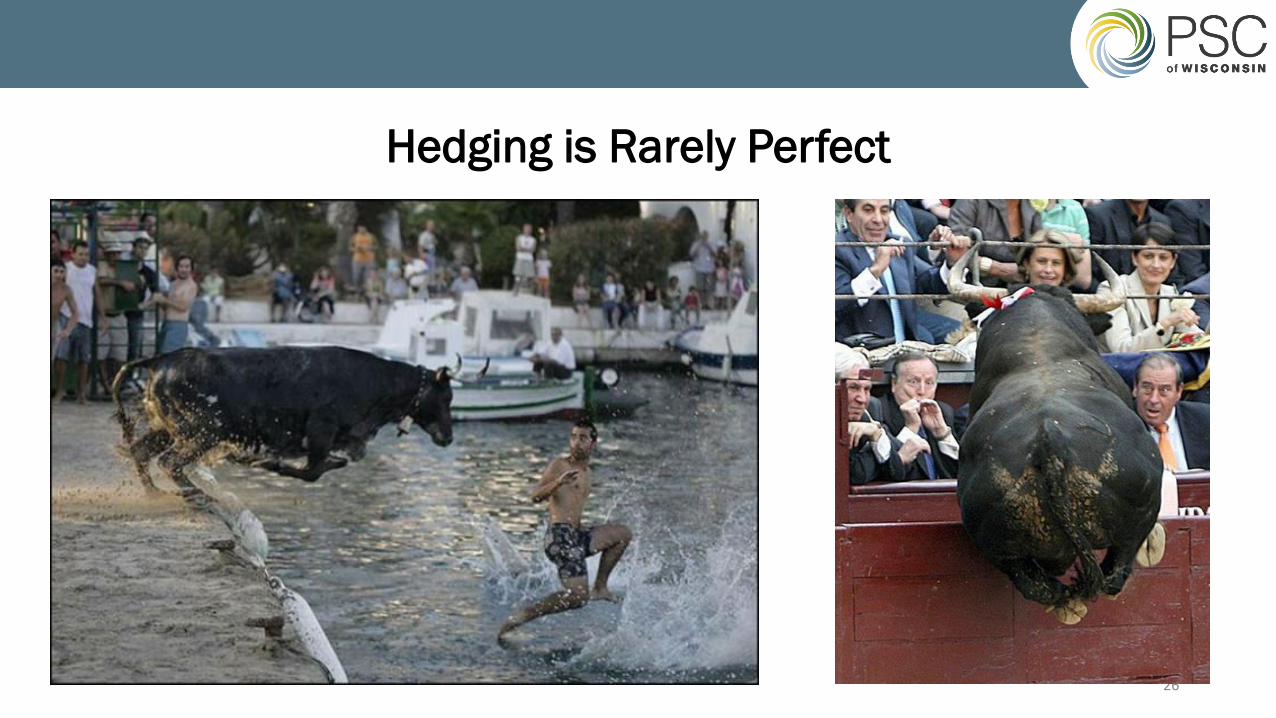

Actual (vs. Expected) Outcomes May Well Surprise You

• At least three millennia of bull fighting history

• The odds are materially in favor of the bullfighter. Those risks run include:• Goring by the bull

• Death from any injuries sustained

• The bull is progressively antagonized

• In this particular case:• The bull refused to become infuriated

• The bullfighter failed to get the bull to respond and charge him

• The bullfighter threw in the towel

• The bull came over to commiserate

• The bullfighter quit his career

• The bull was retired to pasture17

How Does One Mitigate Risk?

• FACT: one cannot eliminate risk: one can only mitigate it

• Analyze the particular risk in its fullest context

• Identify the individual components that create the risk

• Evaluate how best to constrain the associated variance, considering:• Risk effectiveness of each alternative

• Cost effectiveness of each alternative

• Check for unintended or perverse consequences

• Establish a periodic review protocol, as appropriate

• Plan for a potential counterparty default

• Execute the hedge and write off any regrets as a sunk cost

18

Risk Perceptions

19

To fully appreciate the magnitude of the risks under review, it’s usually advisable to try and capture the whole picture of any situation:• Scope• Scale• Context• Implications• Timing• Misleading expectations

Out to enjoy a calm and sunny day at sea …

How Does One Mitigate Risk?

• FACT: one cannot eliminate risk: one can only mitigate it

• Analyze the particular risk in its fullest context

• Identify the individual components that create the risk and map the

mitigating alternatives to the individual components

• Evaluate how best to constrain the associated variance, considering:• Risk effectiveness of each alternative

• Cost effectiveness of each alternative

• Check for unintended or perverse consequences

• Establish a periodic review protocol, as appropriate

• Plan for a potential counterparty default

• Execute the hedge and write off any regrets as a sunk cost20

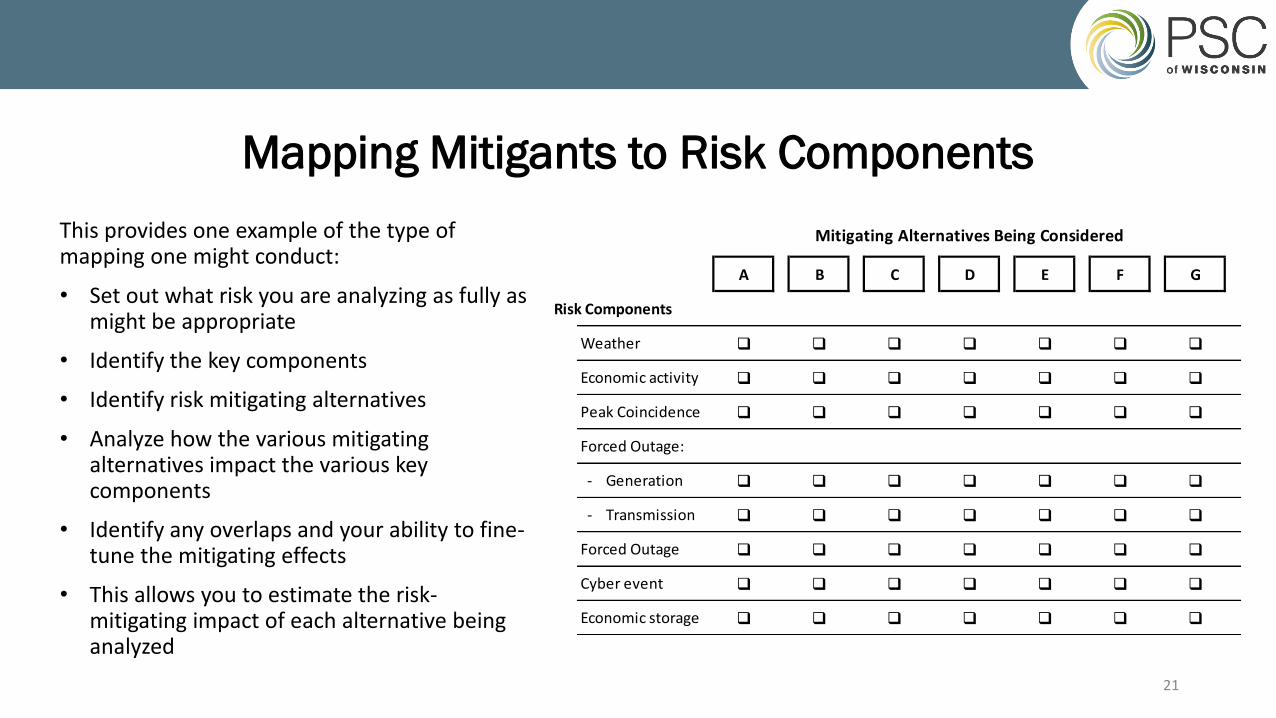

Mapping Mitigants to Risk Components

This provides one example of the type of mapping one might conduct:

• Set out what risk you are analyzing as fully as might be appropriate

• Identify the key components

• Identify risk mitigating alternatives

• Analyze how the various mitigating alternatives impact the various key components

• Identify any overlaps and your ability to fine-tune the mitigating effects

• This allows you to estimate the risk-mitigating impact of each alternative being analyzed

21

A B C D E F G

Risk Components

Weather q q q q q q q

Economic activity q q q q q q q

Peak Coincidence q q q q q q q

Forced Outage:

- Generation q q q q q q q

- Transmission q q q q q q q

Forced Outage q q q q q q q

Cyber event q q q q q q q

Economic storage q q q q q q q

Mitigating Alternatives Being Considered

Some Alternatives Available to Mitigate Risk

• Hold reserves (key equipment, fuel, spare capacity, electric storage)

• Firm forward purchases (set price, timing, and delivery location)

• Make pooling arrangements (pools, ISOs, RTOs)

• Diversify (resources, suppliers, customers)

• Acquire insurance (self-insurance, third-party casualty contracts)

• Undertake swaps (physical and financial)

• Acquire or sell options (transmission rights, capacity and/or energy)

• Take contingency planning very seriously, and drill frequently

• Hedge using financial instruments (over-the-counter, RTO and listed

contracts)

22

How Does One Mitigate Risk?

• FACT: one cannot eliminate risk: one can only mitigate it

• Analyze the particular risk in its fullest context

• Identify the individual components that create the risk and map the

mitigating alternatives to the individual components

• Evaluate how best to constrain the associated variance, considering:• Risk effectiveness of each alternative

• Cost effectiveness of each alternative

• Check for unintended or perverse consequences

• Establish a periodic review protocol, as appropriate

• Plan for a potential counterparty default

• Execute the hedge and write off any regrets as a sunk cost23

Risk-Effectiveness Analysis

Risk effectiveness:The degree of negative correlation between the risk profile and the hedge profile according to the relevant variables

• Volumetric (physical units)

• Pricing (dollars)

• Timing (premature or delayed occurrence)

• Geographic (situs or delivery location)

24

At Risk Hedge

Variables

Volumetric 1,000 kWh 1,000 kWh

Pricing $4.00/kWh $3.95/kWh

Timing 17-May-18 25-May-18

Geographic Node X Node Y

Cost-Effectiveness Analysis

Cost effectiveness:The relationship between the expected value of the hedge (the avoided cost) and the all-in cost of the hedge.

• Expected value = (subjective probability) x (the avoided cost) x (risk effectiveness)• Subjective probability is the expected probability of the risk occurring in the first place

• The avoided cost is the financial impact of the risk, should it occur without any risk mitigation being put in place

• Risk effectiveness is the correlation factor of the hedge being considered (see previous slide)

• All-in cost of the hedge = (price) + (associated charges) + (any transaction costs)• Price is the outright cost or premium charged by the counterparty for entering into the hedging transaction

• Associated charges are any indirect costs charged by the counterparty for entering into the hedging transaction

• Any transaction costs are any transactional expenses (margins, settlement charges, etc.)

• Cost effective if the Expected Value ≥ the All-in Cost of the Hedge

25

Hedging is Rarely Perfect

26

How Does One Mitigate Risk?

• FACT: one cannot eliminate risk: one can only mitigate it

• Analyze the particular risk in its fullest context

• Identify the individual components that create the risk

• Evaluate how best to constrain the associated variance, considering:• Risk effectiveness of each alternative

• Cost effectiveness of each alternative

• Check for unintended or perverse consequences

• Establish a periodic review protocol, as appropriate (dynamic hedging)

• Plan for a potential counterparty default (e.g., Herstatt Bank)

• Execute the hedge and write off any regrets as a sunk cost

27

Using Financial Hedging

to Mitigate Risks

28

Risk Mitigation with Financial Hedging

• Financial hedging requires one to determine the cash flows that

will offset the particular operating risk to be mitigated: • Without taking physical delivery

• Settling in cash instead of taking physical delivery

• Financial hedging types include:• Swaps

• Contracts for differences

• Futures contracts

• Options

• NOTE: financial hedging instruments are evolving continuously

29

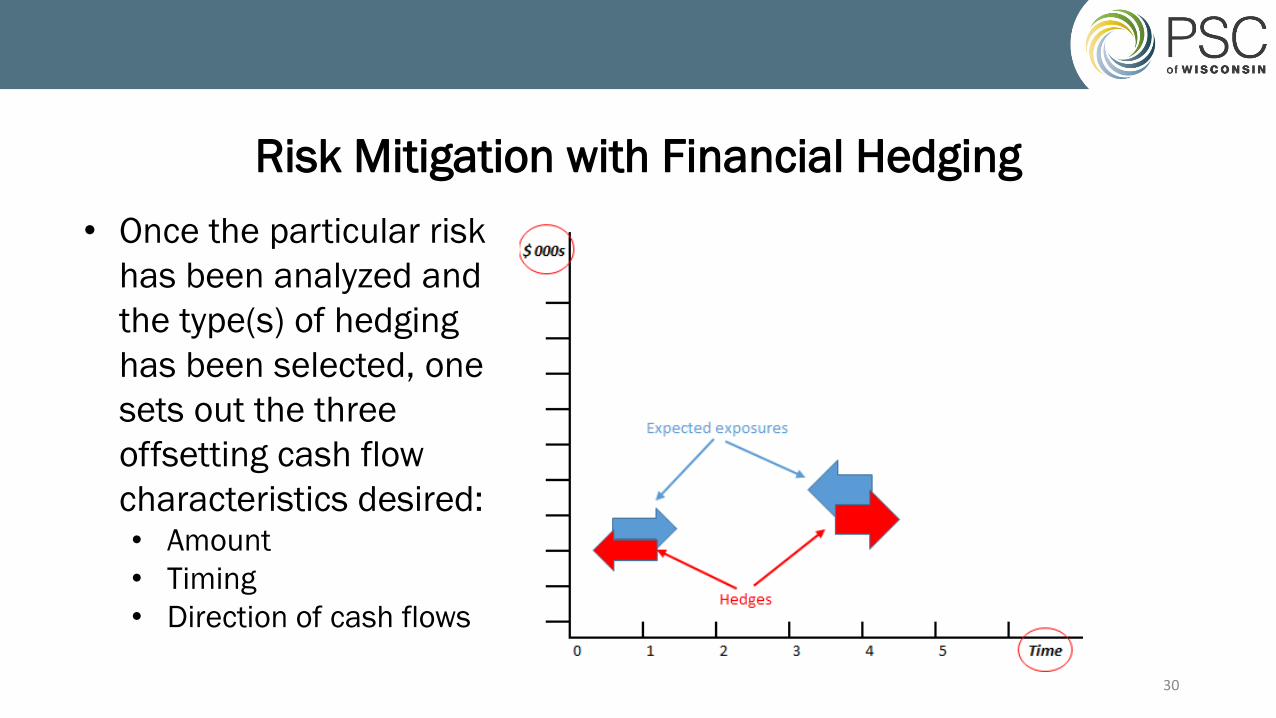

Risk Mitigation with Financial Hedging

• Once the particular risk

has been analyzed and

the type(s) of hedging

has been selected, one

sets out the three

offsetting cash flow

characteristics desired:• Amount

• Timing

• Direction of cash flows

30

Types of Financial

Hedging Instruments

31

Trading Products are Contracts

• Physical power contracts include:• Energy

• Capacity

• Transmission (firm and non-firm)

• Ancillary services

• Spot contracts

• Forward and futures contracts• Fixed prices

• Indexed prices

32

Range of Products

• Spot and outright contracts

• Futures contracts• Weather

• Electric power and services

• Transmission services

• Fuel

• Option contracts• Standard

• Exotic

33

Range of Participants

• Physical market participants• Generating entities

• Transmission owners

• Distribution entities

• Financial market participants• Physical market participants

• Traders

• Investors

• Hedge funds

• Brokers

34

Applicability to the

Wholesale Energy Markets

35

Physical and Financial Markets

• Increasing links between the physical electricity markets and the

financial markets• Enhanced liquidity

• Price discovery

• Price convergence

• Classic perspective was that the physical market drove the financial

markets.• Over time, this has become a reciprocal relationship.

• In other financial markets, such as those for the U.S. Treasury debt

securities, the financial derivatives markets have significantly outgrown the

cash markets

• Will the tail wag the dog from time to time? 36

Financial Markets and Mechanisms

• An array of products, mechanisms and participants

• In financial markets, no physical delivery to settle (pay-outs instead)

• Hedging occurs in both the physical and the financial markets:• Physical market participants hedge in both physical and financial markets

• Financial market participants may use physical contracts to offset financial

market positions, but ensure that no physical delivery will be required.

• These overlaps encourage convergence between both markets

• Electricity markets of both types include:• Exchanges

• Regional transmission organizations (RTOs)

• Over-the-counter (OTC) bilateral trading

37

Exchanges

38

• Organized and regulated markets• Credit risk mitigated

• Mark-to-market truing up and margin requirements

• Listed contracts are standardized:• Commodity quality and quantity is clearly defined

(e.g., electricity products, emissions allowances, weather futures)

• Location or delivery point

(nodes, flow gates, etc.)

• Timing of settlement

(pre-establish settlement dates)

• The exchanges act as clearing houses (mitigating counterparty risk)

RTOs

39

• Electricity is bought and sold through RTOs• Specifically linked to their own region’s operations

• Supports price discovery and offsets local market power

• Not bilateral contracts, but rather pooled

• Virtual transactions• Financial traders can buy and sell power in the day ahead market

• These bids and offers have to be settled in cash in the real-time market

• Financial transmission rights (FTRs)• Will be covered in more detail later today

• Replaces the certainty that existed in the classical vertical monopoly

• Introduces liquidity and adds transparency to congestion costs between

nodes

OTC Bilateral Trading

40

• Trading conducted outside an organized exchange or an RTO

• Not standardized, allowing customized contracts

• Contracts negotiated and completed with each counterparty• Usually use an umbrella or reference agreement to allow for a modicum of

standardization

• Under that umbrella, the two parties can agree to individualized terms and

conditions

• The trade-off is that OTC markets are less liquid, less transparent

and require both parties to track each other’s creditworthiness,

compared to exchange-traded or RTO-traded transactions.

Uses and Abuses of

Financial Hedging

Instruments

41

Challenges

• Uses include enhancing transparency and price convergence

• Quality of the information available to all parties:• Timeliness

• Transparency

• Granularity

• Staying on track with the over-arching objectives pursued

• Avoiding speculation by regulated utilities

• Discouraging abuses by financial counterparties

• Avoiding selective disclosure, as required by: • the U.S. Securities and Exchange Commission (SEC); and

• The U.S. Commodities Futures Trading Commission (CFTC)42

Types of Abuses

• Manipulative trading• Inflating volumes

• Trade at off-market prices

• “Banging the open” and “marking the close”

• Information-based manipulation• “Pump and dump”

• False reporting and misinformation

• Wash trading

• Withholding of supply from the market• Physical withholding (e.g., Enron and California circa 2000)

• Economic withholding (e.g., deliberately over-pricing supply)

43

Questions?

Comments?

Complaints?

44

Contact Information

Enrique Bacalao

Chief Economist

Public Service Commission of Wisconsin

608-267-2210

www.psc.gov

45