healthcare industry in the gcc -...

TRANSCRIPT

www.resilienceand.co.uk Page | 1

Healthcare Industry in the GCC Study Report | November 2016

www.resilienceand.co.uk Page | 2

Table of Contents

3 Industry Outlook7 1.1 Saudi Arabia Healthcare Sector – Brief Overview9 1.2 United Arab Emirates Healthcare Sector – Brief Overview10 1.3 Kuwait Healthcare sector – Brief Overview 12 1.4 Qatar Healthcare sector – Brief Overview 13 1.5 Oman Healthcare sector – Brief Overview15 1.6 Bahrain Healthcare sector – brief overview

16 Industry Growth Drivers, Challenges and Trends17 2.1 Healthcare industry growth drivers 17 2.2 Healthcare industry challenges 18 2.3 Healthcare industry trends

19 Top Company’s Profiles20 3.1 Dr. Soliman Fakeeh Hospital, KSA21 3.2 Al Noor Hospitals, UAE22 3.3 Aster DM Healthcare, UAE23 3.4 NMC Health, UAE24 3.5 AVIVO Group, UAE25 3.6 Prime Healthcare Group, UAE26 3.7 Al Maidan Clinic, Kuwait27 3.8 Al Mowasat Healthcare Co., Kuwait28 3.9 YIACO Medical Co., Kuwait29 3.10 Al Hayat International Hospital, Oman30 3.11 Badr Al Samaa Group of Hospitals, Oman31 3.12 Bahrain Specialist Hospital, Bahrain32 3.13 Ibn Al-Nafees Hospital, Bahrain

www.resilienceand.co.uk Page | 3

1Industry Outlook

www.resilienceand.co.uk Page | 4

The Gulf countries have experienced

radical demographic changes and a

dramatic increase in diseases

associated with lifestyle choices.

These factors have triggered the rapid

development of the healthcare sector

in the GCC.

As GCC exert high spending power,

this leads to changes in the diets,

which in turn leads to the

development of lifestyle related

diseases such as diabetes, obesity and

heart related conditions. This, along

with a quick growth of the population

in the area, puts pressure on the

actual healthcare system.

The governments in the GCC are

allocating funds and also are pursuing

the private sector to participate in the

development of hospital and clinic

infrastructure, as well as upgrade the

quality of hospital services to the

developed countries’ level.

GCC is heavily investing in technology

and increasingly imposes obligatory

health insurance schemes, this also

contributing to the development of

the healthcare sector. International

healthcare technology providers such

as General Electrics and Philips,

whose European and US sales have

decreased due to budget constraints,

are hoping for sales increase in the

GCC1.

Public and private investments in the

healthcare sector are forecasted to

exceed USD 150billion in 20162.

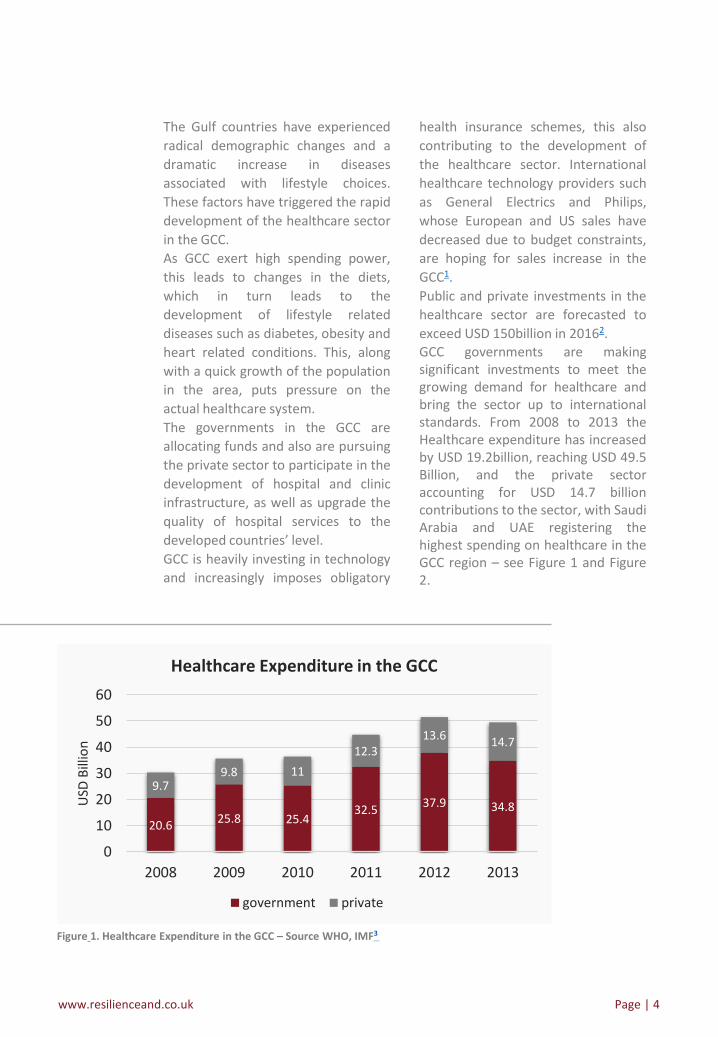

GCC governments are makingsignificant investments to meet thegrowing demand for healthcare andbring the sector up to internationalstandards. From 2008 to 2013 theHealthcare expenditure has increasedby USD 19.2billion, reaching USD 49.5Billion, and the private sectoraccounting for USD 14.7 billioncontributions to the sector, with SaudiArabia and UAE registering thehighest spending on healthcare in theGCC region – see Figure 1 and Figure2.

20.625.8 25.4

32.537.9 34.8

9.79.8 11

12.313.6

14.7

0

10

20

30

40

50

60

2008 2009 2010 2011 2012 2013

USD

Bill

ion

Healthcare Expenditure in the GCC

government private

Figure 1. Healthcare Expenditure in the GCC – Source WHO, IMF3

www.resilienceand.co.uk Page | 5

2.9%4.0%8.9%

10.3%

26.0%

47.9%

Healthcare Expenditure by Country (2013)

Bahrain Oman Qatar Kuwait UAE Saudi Arabia

Figure 2. Healthcare Expenditure by Country – Source WHO4

As seen in Figure 3, in 2013 Bahrainhas registered the highest healthcareexpenditure in the GCC as apercentage of the GDP - 4.9 % ,Kuwait has registered 2.9% and Qatarhad the lowest rate at 2.2% of theGDP. The numbers though arerelatively low compared to spendingin the US, UK and Germany.

BMI Research predicts that Qatargovernment will cut back plannedspending on health infrastructureprojects over the coming years, asfinancial resources are divertedtowards preparation for theforthcoming FIFA 2022 World Cup6.

17.1%

11.3%

10%

9.1%

4.9%

3.2%

3.2%

3.1%

2.9%

2.6%

2.2%

0.0% 5.0% 10.0% 15.0% 20.0%

US

Germany

Global

UK

Bahrain

UAE

Saudi Arabia

GCC

Kuwait

Oman

Qatar

Country-wise Healthcare Expenditure as % of GDP (2013)

Figure 3. Country-wise Healthcare Expenditure as % of GDP (2013)- Source WHO, IMF, The World Bank5

www.resilienceand.co.uk Page | 6

Overall, the government’s focus onenhancing the healthcare sector inthe GCC is shown in the constantgrowth of the health infrastructure. In2013 the region had 684 hospitals,and 60 % of those owned and

operated by the governments - Figure4.Almost 80% of the total of hospitals inthe GCC are located in Saudi Arabiaand the UAE – Figure 5.

386 401 405 409 417 426

214 219 218 233 248 258

0

200

400

600

800

2008 2009 2010 2011 2012 2013

Number of Hospitals in the GCC

Public Private

Figure 4. Number of Hospitals in the GCC7

1.9% 3.4%4.4%

9.6%

15.6%

65.1%

Hospitals in the GCC, by Country (2013)

Qatar Bahrain Kuwait Oman UAE Saudi Arabia

Figure 5. Hospitals in the GCC by Country (2013)8

www.resilienceand.co.uk Page | 7

1.1 Saudi Arabia Healthcare Sector – Brief Overview

Saudi Arabia has a population of over30 million people9, and it is the mostpopulous country in the GCC10. In thelast decades, the government has

invested heavily in the sector, withthe healthcare expenditure increasingfrom USD 14.8 Billion in 2008 to USD23.7 Billion in 2013 - Figure 6.

9.8 12 11.916.7

20.215.2

55.4 6.3

6.9

7.9

8.5

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013

USD

Bill

ion

Healthcare Expenditure in Saudi Arabia

government private

Figure 6. Healthcare Expenditure in Saudi Arabia11

The Ministry of Health (MoH) is thecore provider of health care servicesin the country. Approximately 60% ofall hospitals within the Kingdom areowned and operated by the MoH.These hospitals offer basic healthcareservices, and in some cases,specialised facility centres. MoHamenities are gradually being madeaccessible only to Saudi Nationals ,and expats can access specialisedtreatment only in rural areas wherethere are no private sector facilities.This restriction of the MoH hospitalsfor the foreigners is triggering the 5.5million of expatriates (half of whichare concentrated in Riyadh andJeddah) towards the privatehealthcare sector.12

From 2009 to 2013, the number ofprimary health care centres wasamplified by 9.5%, and approximately150 new centres are forecasted peryear till 2016 as part of the ten-yearstrategy of the Ministry of Health.13

There has been also a noticeableincrease in the number of hospitalsand medical specialists.The Saudi Arabian Ministry of Healthis endorsing quality assurance andimprovement via the implementationof standard operating procedures andcertification of health care facilities,and there is a focus on improving thepatient safety both in the public andprivate health facilities.

www.resilienceand.co.uk Page | 8

As the country is relying on expats forfilling the medical staff job openings,the government is continuing itsefforts to develop a Saudi medicalworkforce through introducing newhealth and nursing schools, expandingnew training centres and facilitatingstudies abroad for the Saudi medicalstudents.14

Expats in the Kingdom are largelydependent on the private care, as thecompulsory health insurance coverfor them has been successfullyintroduced in 2006.15

To be able to fulfil the risinghealthcare needs of the expats, thegovernment is encouraging theinvolvement of private entities in thecountry’s healthcare sector via public-private partnerships and also byincreasing loan limits for the private

healthcare providers.16 Thegovernment has taken steps towardsliberalising the sector, and accordingto new regulations announced in2014, citizens who are not health careprofessionals were allowed to ownand operate hospitals for the firsttime. The new rules were alsotargeted to attract investment fromglobal health care companies.Previously, non-Saudis wereprevented from owning any clinicalcentres in the Kingdom.17 The MoH ispromoting high standards in thehealth sector, therefore the non-performing institutions are targetedand fined or eventually closed. In2015, the MoH has closed 38 privatehealthcare entities following theirfailure to comply with the country’shealth regulations.18

www.resilienceand.co.uk Page | 9

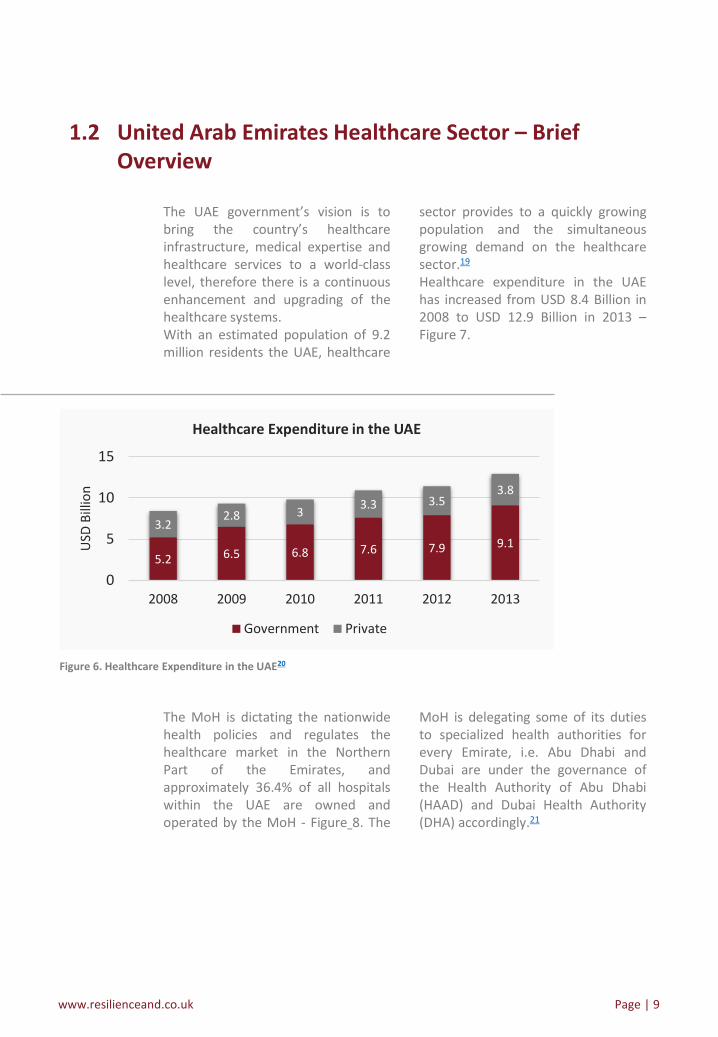

1.2 United Arab Emirates Healthcare Sector – Brief Overview

The UAE government’s vision is tobring the country’s healthcareinfrastructure, medical expertise andhealthcare services to a world-classlevel, therefore there is a continuousenhancement and upgrading of thehealthcare systems.With an estimated population of 9.2million residents the UAE, healthcare

sector provides to a quickly growingpopulation and the simultaneousgrowing demand on the healthcaresector.19

Healthcare expenditure in the UAEhas increased from USD 8.4 Billion in2008 to USD 12.9 Billion in 2013 –Figure 7.

5.2 6.5 6.8 7.6 7.9 9.1

3.22.8 3

3.3 3.53.8

0

5

10

15

2008 2009 2010 2011 2012 2013

USD

Bill

ion

Healthcare Expenditure in the UAE

Government Private

Figure 6. Healthcare Expenditure in the UAE20

The MoH is dictating the nationwidehealth policies and regulates thehealthcare market in the NorthernPart of the Emirates, andapproximately 36.4% of all hospitalswithin the UAE are owned andoperated by the MoH - Figure 8. The

MoH is delegating some of its dutiesto specialized health authorities forevery Emirate, i.e. Abu Dhabi andDubai are under the governance ofthe Health Authority of Abu Dhabi(HAAD) and Dubai Health Authority(DHA) accordingly.21

www.resilienceand.co.uk Page | 10

63.6%

36.4%

Total Number of Hospitals in the UAE (2013)

Private Public

Figure 8 – Total number of hospitals in the UAE22

The UAE government has embraced aliberal approach to welcoming foreigncompanies to invest into the country’shealthcare industry. Abu Dhabi andDubai, which are the main healthcarehubs, have taken crucial steps intoenhancing the sector. Abu Dhabi hasbeen the first Emirate to impose thecompulsory health insurance forexpats. In 2014, HAAD has releasedits 5-year plan with an emphasis onthe quality of care, minimising thegaps in the capacity, incentivizing themedical workforce and retaining it,preparation for emergencies, cost-effective healthcare spending, as wellas disease prevention.23

Dubai is considered one of the tophealthcare destinations in the world,having an advanced healthcaresystem with a large number ofhospitals and primary healthcarecentres with standards aligned withthe international health standards.Dubai has implemented compulsoryhealth insurance in 201424 and hasdeveloped two healthcare free zones– Dubai Healthcare City and DubaiBiotechnology and Research Park,following a demand for high-qualitycare.25

The Emirate is largely viewed as amedical tourism destination,especially for cosmetic surgery.

1.3 Kuwait Healthcare Sector – Brief Overview

The healthcare system in Kuwait isdeveloping at a rapid pace, mainlydue to the increased life expectancy,lower infant mortality and control ofinfectious illnesses. These factorscontribute to the increase of thepopulation numbers and in the sametime the need for medical servicesincreases accordingly. Kuwaiti

population has been ranked the fifthin the world in overweight and obesestandard calculator, according toPortland Press Herald.26 The countryhas increased its healthcareexpenditure from USD 2.8 Billion ion2008 to USD 5.1 Billion in 2013 -Figure 9.

www.resilienceand.co.uk Page | 11

Figure 9. Healthcare Expenditure in Kuwait27

2.23.6

2.73.5 3.9 4.2

0.6

0.6

0.6

0.70.8

0.9

0

1

2

3

4

5

6

2008 2009 2010 2011 2012 2013

USD

Bill

ion

Healthcare Expenditure in Kuwait

Government Private

Kuwaiti government is responsible forover 80% of the total investment inthe healthcare system and the privatehealthcare sector are estimated totake a share of 15-20% of thehealthcare spending.28 The healthcaresector in Kuwait is solely controlledand regulated by the MoH, which isactively promoting the participationof the private sector in the non-emergency healthcare area forexpats, and in this respect the Kuwaitigovernment has initiated a PPPcompany, Kuwait Health Assurancecompany with the scope of privatizingexpat medical care and healthinsurance.29

As Kuwait is a high income country, itdoes not receive financial supportfrom external assistance.30

In 2013, Kuwait’s healthcareinfrastructure included 31 hospitals,of which 16 were public, 12 privateand the remaining 3 were owned bylarge oil companies.31 Availabilitywise, there have been registered 21beds, 56 nurses and 35 physicians per10,000 individuals during the year,and the number of the healthcareresources has increased at a quickerpace than in the rest of the GCCcountries.32

www.resilienceand.co.uk Page | 12

1.4 Qatar Healthcare Sector – Brief Overview

Figure 10. Healthcare Expenditure in Qatar34

Qatar, as one of the richest countriesin the world, has registered thehighest health expenditure per capita(USD) in 2013 – USD 2070.33 Totalhealthcare expenditure has been USD

2.1 Billion in 2008 rising to USD 4.4Billion in 2013, and the governmenthas financed approximately 80% of it- Figure 10.

1.8 2 22.6

3.5 3.70.30.6 0.6

0.7

0.7 0.7

0

1

2

3

4

5

2008 2009 2010 2011 2012 2013

USD

Bill

ion

Healthcare Expenditure in Qatar

Government Private

On most measures of public health,Qatar matches developed countries.As of 2015, life expectancy at birthwas 77 years for males and 80 forfemales, according to the WorldHealth Organisation (WHO).Infectious diseases such as HIV andtuberculosis are virtually non-existent.35

The big health challenge lies ratherwith non-communicable diseases(NCDs), which cause some 69% ofmortalities. As for adult risk factors,as of 2014 some 19.8% of thepopulation had diabetes, according tothe International Diabetes Federation,while WHO data shows that 42.3%were obese. A 2013 survey by theWHO and state authorities showed

tobacco use at 12.1% among adults.36

The highest authority in the healthsector is the Ministry of Public Health(MoPH), established in January 2016.Previously, the Supreme Council ofHealth (SCH) had been the mainregulatory body; however, by emirdecree the SCH was disbanded and itsresponsibilities taken over by theMoPH.37

The public health sector employed30,303 professionals as of end-2014,up 16% on the previous year.38 Theprivate sector employs some 1150doctors who work across 166 clinicsand medical complexes, 131 dentalclinics and four general hospitals,according to the Public WorksAuthority (Ashghal).39

www.resilienceand.co.uk Page | 13

1.5 Oman Healthcare Sector – Brief Overview

In all, for every 10,000 people in thecountry there are 77.4 doctors, 118.7nurses and midwives, and 0.3psychiatrists, according to the WHO’s“World Health Statistics 2015”. WHOstatistics for 2013 show that thenumber of hospital beds per 10,000was about 12, while the number ofdentists was 5.8 per 10,000 people.40

A core component of the ambitiousplans to continue to transform healthcare in Qatar is the creation of a newnational health insurance scheme,which is currently being developed bythe MoPH. Early indications suggest

the new scheme will include theprovision of a comprehensive healthcare system with a full range of high-quality health care services, as well asensuring easy access to these servicesby providing the patients with multipleoptions of health care providers.Qatari nationals will be able to accessthe new health insurance scheme in2017, after the new programme isfully approved and its first phase isimplemented.41

Oman’s health sector has experiencedan important expansion over the pastfour decades. Reinforced by a series offive-year development plans, therehas been considerable governmentinvestment in facilities and services.42

At the same time, the sultanate isstrong about increasing the privatesector’s role in health care provision,particularly in the treatment oflifestyle-related diseases, which are onthe rise as the population ages andgrows richer. Oman has thereforesolicited foreign medical expertise andinvestment to help meet its goals forthe health sector and improveoutcomes for its citizens.43

The healthcare expenditure in Oman is

mainly funded by the government(around 80%) and has increased fromUSD 1.3 Billion in 2008 to USD 2 Billionin 2013 – Figure 11.The quality of and access to healthcare has improved vastly in the lastdecades as well. As of 2014, lifeexpectancy was 76.6 years, and theunder-five mortality rate was one in100 (9.7 per 1000 births), according tostatistics from the MoH. Only 11 casesof malaria – and no deaths from it –were reported in 2013.In 2014, the country had 67 hospitalswith a total of 6322 beds, offeringgeneral and speciality care in bothpublic and private situations.

www.resilienceand.co.uk Page | 14

Figure 11. Healthcare Expenditure in Oman44

1 1.1 1.3 1.4 1.6 1.6

0.3 0.30.3 0.3

0.4 0.4

0

0.5

1

1.5

2

2.5

2008 2009 2010 2011 2012 2013

USD

Bill

ion

Healthcare Expenditure in Oman

Government Private

The improvement in health outcomesis a result of a number of differentfactors. First of all, among these is theimportance that the government hasplaced on ensuring access to basicuniversal health care for all Omanicitizens.In addition to building up the physicalinfrastructure of the health caresector, the government has alsobrought in the foreign expertiseneeded to expand and improve theskills of the country’s home grownmedical professional workforce.45

The government provides universalhealth coverage for Omani citizens andsubsidised care for expats. State healthcare is free of charge for Omanis, butfees are presented at private facilities,many of which are used by foreigners.Most health facilities are owned andoperated by the government, butefforts are currently under way toincrease private participation andinvestment in the health care sector.46

The 2011-2015 Omani Health Planidentified a shortage of Omani staff asthe main challenge facing the MoH,and one that has been worsened bythe rise of new health issues (such

NCDs) which require highly trainedspecialists with expertise in specificfields.With current staff levels for medicalspecialists below demand, moreattention is being paid to training andretaining qualified Omani medical staffwith experience in advancedspecialties. Indeed, only about 29% ofthe country’s doctors were Omaninationals in 2012.47

Along with the new hospitalcomplexes and the training of Omaniworkforce, technical solutions areconsidered strategic to maintainingthe correct balance between healthexpenditure and outcomes. One of thefirst such technical solutions to beapplied has been digitising thecountry’s medical records.As of January 1, 2015, 86% ofgovernment hospitals and healthfacilities had been electronicallyconnected to a central cloud-baseddatabase. The database, whichregisters patients by their civilnumbers, allows all governmenthospitals to share patients’ health filesand histories with each other.48

www.resilienceand.co.uk Page | 15

1.6 Bahrain Healthcare Sector – Brief Overview

Due to its small population, thehealthcare expenditure in Bahrain hasregistered the lowest among GCCcountries, amounting to USD 1.4

Billion, a number still considerablyhigher than the expenditure of USD0.8 Billion in 2008 - Figure 12.

0.6 0.6 0.7 0.7 0.81

0.2 0.20.3 0.3

0.4

0.4

0

0.5

1

1.5

2008 2009 2010 2011 2012 2013

USD

Bill

ion

Healthcare Expenditure in Bahrain

Government Private

Figure 12. Healthcare Expenditure in Bahrain49

Bahrain is experiencing similar issuesas other GCC countries – increase inthe population number and thereforean increasing demand for healthcareservices, with the expats demandingmore private medical facilities.The government is the main providerof healthcare in Bahrain, while theNational Healthcare RegulatoryAuthority regulates the healthcaresystem and the SCH is elaborating the

strategic plans and goals for thesector. Bahrain has imposedcompulsory health insurance schemesfor the expats as well.According to the MoH of Bahrain, in2014 the country had 25 hospitals intotal, 7 of which were public and 16private, with another 28 publicprimary health care units andcentres.50

www.resilienceand.co.uk Page | 16

2Industry Growth Drivers,

Challenges and Trends

www.resilienceand.co.uk Page | 17

2.1 Healthcare Industry Growth Drivers

• By 2020, the GCC population is forecasted to reach 53.5m, a 30% increase overthe level in 2000, therefore increasing the demand for healthcare facilities.Also, due to the increased life expectancy, the GCC are set to observe anincreased customer base of older people, who usually require more medicalcare, therefore increasing the healthcare spending;

• Diseases associated with the lifestyle choices are on the rise, adding tohealthcare expenses;

• Compulsory health insurance schemes are also contributing to healthcarespending;

• GCC governments are envisaging long term plans for the upgrading of theirhealthcare systems, and the effective implementation of the plans are likely totrigger healthcare infrastructure and quality standards advancements;

• Government and private investment into the industry reach multi-billionnumbers, with numerous healthcare facilities being built, therefore furtherenhancing the healthcare infrastructure.

2.2 Healthcare Industry Challenges

• The governments in the GCC are under continuous pressure due to the fallingoil prices, which may postpone some expenditure, influence the budgetallocation and therefore the healthcare expenditure;

• Due to the lack of specialization for certain types of diseases, the local citizensprefer to seek treatment abroad. High cost is also a reason for the patients totravel abroad for treatment, and this incentivizes outbound medical tourism;

• The high demand for local medical specialists is not met, as there is a bigdiscrepancy between the local talent and the demand for the specialists, even ifthe governments are tackling this by offering sponsorships abroad for themedical staff, or opening new medical schools and universities;

• In the GCC healthcare sector, private players are still faced with barriers toentry;

• Even if the sector has registered significant improvement in the last years, thereis still room for quality and accessibility of care at the public hospitals.

www.resilienceand.co.uk Page | 18

2.3 Healthcare Industry Trends

• Governments are supporting the Public-Private Partnership (PPP) model. Thepopulation growth and the increase in the healthcare costs are requiring morefunds into the healthcare system, therefore governments are encouraging theinvolvement of private sector into the industry.

• The implementation of information technology triggered by the need toimprove the quality of care and the need to reduce the costs. Thegovernments are increasingly investing in technologies which update andstreamline their healthcare systems. In Saudi Arabia, as part of efforts tomake health care spending more efficient, the government is going aheadwith a number of digitisation initiatives under the banner of its electronic e-health programme.

• Increased focus on preventing diseases rather than treating them is emergingas another trend for the industry, as GCC residents are becoming more awareof their health, this possibly resulting in reducing the healthcare expenditureand enhancing the quality of care in the region.

• The regional governments are continuously emphasizing on providing morespecialized care centres and increasing the number of medical and researchcentres.

www.resilienceand.co.uk Page | 19

3Top Companies’ Profiles

www.resilienceand.co.uk Page | 20

3.1 Saudi Arabia - Dr. Soliman Fakeeh Hospital (Privately Owned)

Dr. Soliman Fakeeh Hospital has beenfounded in 1978 in Jeddah, and hasover three decades of experience inserving patients across Saudi Arabia.DSFH is a regional pioneer in the fieldof organ-transplantation, includingkidney, bone-marrow, liver, and heart

transplantation. Its open-heartsurgery centre claims the highestnumber of operations done in theprivate sector in the Kingdom with asuccess rate comparable to anyinternational centre of excellence.51

Business Portfolio:• Speciality Units include burn unit care, renal dialysis, extended care, IVF,

hyperbaric oxygen, bone marrow transplant, immunology, respiratory andsleep disorders52

• Laboratory – pathologic diagnosis, haematological diagnosis, toxicology anddrug monitoring laboratory, microbiology and virology laboratory53

• Executive health program – offering a personalized health program with acomplete set of consultations, investigations, and diagnostic proceduresaimed at detecting and preventing diseases.54

• Clinical department – operating departments such as internal medicine,paediatrics, general surgery, anaesthesia, neuroscience etc.55

• Pharmacy Services Department• Radiology

Main Assets:• DSFH was the first private hospital in the Western Region of the Kingdom to

become accredited by the Joint Commission International (JCI) in 2006, 2009and 2012 and by the Australian Council for Healthcare Standards International(ACHSI) in 2008 and 2012. 56

• DSFH is presently considered one of the most distinguished hospitals in theMiddle East, and is visited by over 500,000 patients every year, and it is thefirst hospital to publish a Corporate Social Responsibility report in the healthcare sector in the MENA region in 2008.57

www.resilienceand.co.uk Page | 21

3.2 UAE – Al Noor Hospitals Group Plc (Publicly Listed)

Al Noor Hospitals Group Plc has beenestablished in 1985, and representsthe biggest integrated serviceprovider in Abu Dhabi. The companyhas representation in the UAE (Abu

Dhabi, Al Ain, Dubai, the NorthernEmirates) and also in Oman. In 2015,the company managed threehospitals with 216 beds and 17 clinicsand health care centres.58

Business portfolio:• Central Region – the company operates Airport Road Hospital and Khalifa

Street Hospital in the central region of Abu Dhabi. They provide basic care,radiology and pharma services.

• Western and Eastern Region – the Al Ain Hospital and six medical centres inEast of Abu Dhabi, in addition to four medical centres in the western region,offering basic care to the local citizens and also act as referral centres for AlNoor’s hospitals in Abu Dhabi.

• Dubai and Northern Emirates – Al Noor Hospital Group Plc operates fourhealth centres and one long term medical centre in Dubai and the NorthernEmirates.

• International – under this division the company is managing a medical centreand one long term medical centre in Oman.

Main assets:• A vertically integrated healthcare model providing services across medical

fields.• Wide coverage in Abu Dhabi.

www.resilienceand.co.uk Page | 22

3.3 UAE – Aster DM Healthcare (Privately owned)

Aster DM Healthcare was establishedin 1987, and is a principal healthcaregroup in the Middle East and India,offering a variety of medical servicesthrough hospitals and clinics,diagnostic centres, pharmacies,

educational institutions and supportsystems. the company has presencein the GCC, India and Far East. Thecompany manages 16 hospitals,around 60 hospitals and more than170 pharmacies in many countries.

Business Portfolio:• Middle East – presence in the UAE (operating multiple hospitals, clinics and

pharmacies) , Qatar (clinics, pharmacies, and diagnostic centres), Saudi Arabia(Sanad Hospital in Riyadh), Bahrain (a clinic in Manama) and Oman (operatingtwo hospitals in Muscat and Sohar, as well as clinics and pharmacies). Thecompany presents a capacity of around 500 beds in the GCC. Brands – Aster,Access and Medcare, operating clinics, hospitals and pharmacies.59

• India – presence in Calicut, Kochi, Wayanad, Kolhapur, Pune, Hyderabad andBangalore, and operating eight hospitals in India with a capacity of 1840 beds.Brands – Aster, Medcity and DM WIMS, operating hospitals, pharmacy andmedical college60

• Far East – operating a clinic in the Philippines

Main Assets• Vast experience in the healthcare facilities – over 28 years• Has been awarded as the ‘Emerging Multi-Specialty Healthcare Provider’ at VC

Circle Healthcare Award 2014• Impressive portfolio of hospitals, clinics, pharmacies, diagnostic centres,

healthcare management, educational institutions, healthcare support systems

www.resilienceand.co.uk Page | 23

NMC Health Plc has a proud heritageof over 40 years in the UAE and isalmost as old as the 41-year-oldnation, having been established in1975 as a small pharmacy and clinic.61

Since then NMC Health Plc hasemerged into an integrated privateprovider of healthcare services acrossthe UAE. In April 2012, NMC becomes

the first Abu Dhabi company to belisted on the London Stock Exchangeas NMC Health Plc. NMC is part of theFTSE 250 index and is listed on thepremium segment of the LSE.62

As of today, the company has anetwork of 20 hospitals, medicalcentres and day care surgery clinics.

3.4 UAE – NMC Health Plc (Publicly Listed)

Business Portfolio:• NMC Healthcare - Hospitals, Day Surgery Centres, Medical Centres and

Pharmacies. Has an international network of hospitals in the UAE and Europeconsisting of thirty healthcare facilities across 5 countries, catering to over 11thousand patients a day, and employing over 1200 doctors.

• NMC Trading - one of the largest distributors in the UAE with an exclusivedistribution rights for some of the most premier brands from around theworld, including Nestle, Unilever, Nivea, Pfizer, Siemens, Samsung, Sanofi,Kiwi, Brylcreem, Henkel, Abbott, 3M and Medtronic among others. NMCTrading sells products and services to over 10,000 businesses across theUAE.63

Main Assets:• Over 40 years’ experience in the UAE• One of the top distributors and wholesalers in the UAE

www.resilienceand.co.uk Page | 24

AVIVO Group owns and operates

medical facilities, pharmacies and

laboratories in the UAE and Kuwait.

The group operates 32 healthcare

assets which include two highly

reputed hospitals, 14 specialty

centres, eight high-end dental centres

attached with sophisticated dental

lab, six pharmacies and two state-of-

the-art diagnostic facilities.64 The

group is based on the strong

foundation of over 200 plus qualified

doctors, each being an expert in their

respective fields; 800 plus medical

employees serving over 1.3 million

patients a year.65

3.5 UAE – AVIVO Group

Business portfolio:• AVIVO Hospitals – two hospitals in the UAE (National Hospital in Abu Dhabi

and Conceive Gynaecology and Fertility Hospital in Sharjah)• AVIVO Clinics – located across UAE and Kuwait, offering a complete range of

healthcare solutions, including medical and aesthetic solutions for skin, teethand hair.

• PRIMACARE Clinics – the group provides a variety of specialized health andwellness services through its clinics located in Dubai, Abu Dhabi and Sharjah

• PRIMACARE Pharmacies – located in Abu Dhabi and Dubai, providingpharmacy and diagnostic services.66

Main assets:• Backed by Al Masah Capital Limited• Expanded coverage over the years through an inorganic route

www.resilienceand.co.uk Page | 25

3.6 UAE – Prime HealthCare Group LLC (Privately Owned)

Prime HealthCare Group LLC hasbeen established in 1999, and itrepresents one of the leadinghealthcare providers in the UAE and isa well-known brand with its team ofover 350 physicians and 1000

supporting professionals providingstate-of-the-art medical care to theUAE’s citizens and residents anddedicated to making the country abenchmark for superior healthcaresolutions. 67

Business Portfolio:• Prime Hospital Dubai - Round the clock medical emergency care available,

advanced cardiac care, adult intensive care unit, paediatric intensive care unit,coronary care unit, neonatal intensive care unit, dedicated maternity & childfloor, day surgery unit, family clinic68

• Prime Medical Centres- established at various locations in the UAE• Premier Diagnostic Centre - the first diagnostic centre on the Deira side of

Dubai which offers complete radiology and laboratory services with the addedadvantage of an open MRI facility.69

• Medi Prime Pharmacies• Corporate Services• Prime Home Care – a specialized service extended to those who are in need of

quality health care but are homebound due to illness, or unable to leave theirhomes without considerable difficulty.70

Main Assets:• Expertise coupled with their core values of Transparency, Customer Centricity,

Quality Consciousness, Cost Effectiveness and Speed of action played anintegral part in the Prime HealthCare Group being conferred the Dubai QualityAppreciation (DQA) Award in 2012 for the second time, the first being in2007. 71

• Prime Healthcare Group LLC has been commended by the DubaiGovernment’s Department of Economic Development for excellence in theareas of high service quality, appreciable level of customer satisfaction,strategic branding, employee care, frequent free health check-ups and healthawareness programs under community out-reach program.72

www.resilienceand.co.uk Page | 26

3.7 Kuwait - Al-Maidan Clinic for Oral Health Services Company K.S.C.P. (Al-Maidan Clinic)

Al-Maidan Clinic started operations in1987 as a dental clinic in Kuwait. Atthe moment it operates eight dentalclinics at strategic locationsthroughout the country. In 2008, Al-Maidan Clinic set up the 120-bed AlSeef Hospital in 2009. Al-Maidan is a

subsidiary of the largest privatemedical services provider in Kuwait –United Medical Services Co (UMS),which in turn is one of the largestdiversified holding companies in theMENA region73.

Business portfolio:• Clinics – oral health services, dental treatment• Hospitals – operation of the Al Seef Hospital with medical diagnosis,

healthcare, consultations, specialized treatments

Main Assets:• A one-stop dental service provider• Treated more than 400,000 patients• A staff of over 70 leading dental experts

www.resilienceand.co.uk Page | 27

Al-Mowasat Healthcare Companyhas been established in 1998, and itowns, develops and manageshospitals in Kuwait and Lebanon. Thebiggest hospital owned by thecompany is New Mowasat Hospital inKuwait, with a capacity of 100 beds.The company also diversifies its

operations into primary healthcareclinics under the same brand, NewMowasat Clinics, and is involved inreal estate projects via its subsidiary,Al-Mowasat Real Estate Co, toconstruct and manage hospitals inKuwait. 74

3.8 Kuwait - Al-Mowasat Healthcare Company K.S.C. (Publicly Listed)

Business portfolio:• Healthcare Services – medical care, pharmacy and other auxiliary services• Investment and others

Main Assets:• Joint Commission International (JCI) accredited• In 2008, New Mowasat Hospital became the third hospital in the Middle East

to receive accreditation by the Accreditation Canada International (ACI), theworldwide leader in raising the bar for quality health care.75

• Subsidiary of Nafais Holding Company, a listed company engaged in educationand healthcare businesses.76

www.resilienceand.co.uk Page | 28

YIACO Medical Company has beenestablished in 1953 as a solemarketing agent for manymultinational research-basedpharmaceutical manufacturers. YIACOquickly grew with the boom inKuwait’s own national growth anddevelopment, diversifying andexpanding into other healthcareservices such as Medical Equipment,Hospital supplies and Dental

equipment & materials. Through itsmany years of operation andexperience in the medical field,YIACO’s reputation of excellenceprecedes its name. A name that hascome to mean undisputed marketleadership in the area of medical care,unparalleled sales and services, aswell as innovative state-of-the-arttechnology for the medical andhealthcare fields. 77

3.9 Kuwait – YIACO Medical Company

Business Portfolio:• Pharma and Business Development Division - Pharma Division is the main

pillar of YIACO Medical Company blended by professional managers and staff.Pharma Division represents a large host of multinational research basedpharmaceutical & consumer care companies with a wide range of therapeuticproduct groups in pharmaceutical, consumer healthcare.78

• Medical, Scientific and Dental Division - MSDD division at YIACO is one of theleading Health Care suppliers acting as a sole agent for many multinationalmedical dental, imaging and scientific research based manufacturers.79

• Medical Centres Division - The Medical Service Centres Division in YIACO is achain of the medical diagnostic centres and home care services spread acrossKuwait. MCD offers our patient health care services of highest standards topeople, in all disciplines of medical specializations. Every MCD centre has itsown Radiology and clinical Laboratories.80

Main Assets• YIACO Medical Company awarded as one of the Top Companies in the Arab

world by Forbes Middle East.81

www.resilienceand.co.uk Page | 29

3.10 Oman - Al Hayat International Hospital (Privately Owned)

Al Hayat International Hospital has

been established in 1995, and is a

multi-specialty hospital in Muscat,

and a branch is Sohar. The founder,

Dr. K.P. Raman, has been trained in

the UK as cardiologist. The hospital

has 50 beds and it is recognized for its

advanced facilities of care and

specialization in the treatment of

chronic diseases. 82

Business portfolio:• Cardiology• Diabetology• Other specializations

Main Assets:• Internationally qualified doctors• MoH awarded Al Hayat International Hospital as the Best Private Hospital in

2015• Diverse range of services in medical specialties

www.resilienceand.co.uk Page | 30

3.11 Oman - Badr Al Samaa Group of Hospitals (Privately Owned)

Badr Al Samaa Group of Hospitalshas been founded in 2002, and it isthe largest private healthcareprovider in Oman. Badr Al Samma has

presence in the GCC – Al Hilal Hospitalin Bahrain, a medical centre in Dubaiand a medical centre in Qatar. 83

Business Portfolio:• Specialities – all the healthcare establishments of Badr Al Samma group offer

the following category of medical services – cardiology, urology, neurosurgery, neurology, nephrology, gastroenterology, internal medicine,diabetology, psychiatry etc.84

• Facilities - the group of hospitals provides the following facilities – healthcheck-up, ambulance services, LAB services, pharmacy, radiology andemergency medical services.85

Main Assets:• Well equipped with state-of-the-art facilities• Renowned healthcare destination by providing compassionate care and

services to millions of people in the region• Offers healthcare services to more than 850 corporate clients, together with

major insurance companies

www.resilienceand.co.uk Page | 31

3.12 Bahrain Specialist Hospital (Privately Owned)

Bahrain Specialist Hospital has beeninaugurated in 2003, and is standingas a centre of excellence in theArabian Gulf. It is a highly specializedmedical centre that provides up to

date medical services by experiencedconsultants and specialists, using thelatest technologies with the-state-of-the-art medical equipment andsystems. 86

Business Portfolio:• BSH Juffair – offering services including internal medicine, cardiology,

neurology, psychiatry, pharmacy and laboratory87

• BSH Clinics - West Riffa - offering services including internal medicine, generalpractice, cardiology, orthopaedic, plastic surgery, paediatric, dental, generalsurgery, dermatology, physiotherapy and pharmacy.88

Main Assets:• It is the first and only hospital in Bahrain that availed the Joint Commission

International accreditation (JCI)• It is the only private healthcare facility that was inaugurated by HM King

Hamad Bin Salman Al Khalifa, the ruler of Bahrain.

www.resilienceand.co.uk Page | 32

3.13 Bahrain – Ibn Al-Nafees Hospital Co. B.S.C. (C) (Privately Owned)

Ibn Al-Nafees Hospital Co. has beenfounded in 2001. Ibn Al-NafeesHospital is a private hospital with anew vision in medical care. Thehospital has a unique set-up withmulti-specialty clinics run by Senior

Consultants. Ibn Al-Nafees aims to beBahrain’s preferred private qualityhealthcare provider and is committedto providing high quality, ethicalmedical care at a reasonable andaffordable cost. 89

Business Portfolio:• Speciality Clinics – offering cardiology, chest diseases, anaesthetics, cosmetic

surgery, dermatology, dental, endocrinology, gastroenterology, nephrology,neurology, oncology, orthopaedic, radiology and urology services90

• 24 hours Clinic - takes care of minor emergencies and the patient’s routinemedical complaints

• Aviation clinic• Other services such as laboratory, in-house pharmacy and physiotherapy

centre.91

Main Assets:• to develop private medical For all of its efforts and contribution to Bahrain's

healthcare industry, the hospital receives strong support from thegovernment who is keen services to complement governmental facilities.

www.resilienceand.co.uk Page | 33

References

1- GCC Healthcare Spending Surges as Demand Soars, Peter Feuilherade, http://www.themiddleeastmagazine.com/wp-mideastmag-live/2014/04/gcc-healthcare-spending-surges-as-demand-soars/2- GCC Healthcare Spending Surges as Demand Soars, Peter Feuilherade, http://www.themiddleeastmagazine.com/wp-mideastmag-live/2014/04/gcc-healthcare-spending-surges-as-demand-soars/3- GCC Healthcare Industry, February 16, 2016, Alpen Capital Investment Banking4- GCC Healthcare Industry, February 16, 2016, Alpen Capital Investment Banking5- GCC Healthcare Industry, February 16, 2016, Alpen Capital Investment Banking6- Industry Trend Analysis- Healthcare Ambitions Lowered in Run-Up to World Cup, BMI Research7- Ministry of Health (MOH) of Saudi Arabia, Oman and Bahrain; Supreme Council of Health (SCH) of Qatar; Central Statistical Bureau (CSB) of Kuwait; National Bureau of Statistics (NBS) of the UAE8- Ministry of Health (MOH) of Saudi Arabia, Oman and Bahrain; Supreme Council of Health (SCH) of Qatar; Central Statistical Bureau (CSB) of Kuwait; National Bureau of Statistics (NBS) of the UAE9- http://www.who.int/countries/sau/en/10- http://www.reuters.com/article/us-gulf-union-fact-idUSBRE84D19B2012051411- http://data.worldbank.org/indicator/SH.XPD.PCAP?locations=SA12- http://www.colliers.com/~/media/files/emea/emea/research/speciality/2012q1-saudi-arabia-healthcare-overview.ashx13- http://www.who.int/countryfocus/cooperation_strategy/ccsbrief_sau_en.pdf 14- http://www.who.int/countryfocus/cooperation_strategy/ccsbrief_sau_en.pdf15- http://www.oxfordbusinessgroup.com/analysis/compulsory-coverage-mandatory-health-and-motor-lines-bring-opportunities-and-challenges16- http://www.alpencapital.com/downloads/GCC_Healthcare_Industry_Report_February_2016.pdf17- http://www.oxfordbusinessgroup.com/overview/game-plan-investment-continues-rise-government-addresses-long-term-challenges-obesity-and-growing18- http://www.oxfordbusinessgroup.com/overview/game-plan-investment-continues-rise-government-addresses-long-term-challenges-obesity-and-growing19-http://www.arabdevelopmentportal.com/sites/default/files/publication/184.united_arab_emirates_healthcare_overview.pdf 20- http://data.worldbank.org/indicator/SH.XPD.PCAP?locations=AE21-http://www.arabdevelopmentportal.com/sites/default/files/publication/184.united_arab_emirates_healthcare_overview.pdf 22-http://www.arabdevelopmentportal.com/sites/default/files/publication/184.united_arab_emirates_healthcare_overview.pdf 23- http://www.alpencapital.com/downloads/GCC_Healthcare_Industry_Report_February_2016.pdf24- http://www.oxfordbusinessgroup.com/uae-dubai-201425- http://www.alpencapital.com/downloads/GCC_Healthcare_Industry_Report_February_2016.pdf26- http://www.pressherald.com/2015/04/23/list-of-worlds-most-obese-nations-may-surprise-you/27- http://data.worldbank.org/indicator/SH.XPD.TOTL.ZS?locations=KW28- State of Kuwait-Overview of the Healthcare Sector, US Department of Commerce, International Trade Administration, http://accd.vermont.gov/sites/accd/files/29- http://www.alpencapital.com/downloads/GCC_Healthcare_Industry_Report_February_2016.pdf30- http://www.who.int/countryfocus/cooperation_strategy/ccsbrief_kwt_en.pdf

www.resilienceand.co.uk Page | 34

31- http://www.csb.gov.kw/Socan_Statistic_EN.aspx?ID=1932- http://www.alpencapital.com/downloads/GCC_Healthcare_Industry_Report_February_2016.pdf 33- http://data.worldbank.org/indicator/SH.XPD.PCAP?locations=QA34- http://data.worldbank.org/indicator/SH.XPD.TOTL.ZS?locations=QA35- http://www.oxfordbusinessgroup.com/overview/home-stretch-second-six-year-health-plan-works-more-emphasis-placed-private-sector-involvement36- http://www.oxfordbusinessgroup.com/overview/home-stretch-second-six-year-health-plan-works-more-emphasis-placed-private-sector-involvement37- http://www.oxfordbusinessgroup.com/overview/home-stretch-second-six-year-health-plan-works-more-emphasis-placed-private-sector-involvement

38- http://www.oxfordbusinessgroup.com/overview/home-stretch-second-six-year-health-plan-works-more-emphasis-placed-private-sector-involvement

39-http://www.oxfordbusinessgroup.com/overview/home-stretch-second-six-year-health-plan-works-more-emphasis-placed-private-sector-involvement40- http://www.oxfordbusinessgroup.com/overview/home-stretch-second-six-year-health-plan-works-more-emphasis-placed-private-sector-involvement41- http://www.oxfordbusinessgroup.com/overview/home-stretch-second-six-year-health-plan-works-more-emphasis-placed-private-sector-involvement42- Foreign expertise and investment flow as Oman expands health coveragehttp://www.oxfordbusinessgroup.com/overview/opening-foreign-expertise-and-investment-flow-government-works-expand-coverage43- Foreign expertise and investment flow as Oman expands health coveragehttp://www.oxfordbusinessgroup.com/overview/opening-foreign-expertise-and-investment-flow-government-works-expand-coverage44- http://data.worldbank.org/indicator/SH.XPD.TOTL.ZS?locations=OM45- Foreign expertise and investment flow as Oman expands health coveragehttp://www.oxfordbusinessgroup.com/overview/opening-foreign-expertise-and-investment-flow-government-works-expand-coverage46- Foreign expertise and investment flow as Oman expands health coveragehttp://www.oxfordbusinessgroup.com/overview/opening-foreign-expertise-and-investment-flow-government-works-expand-coverage47- Foreign expertise and investment flow as Oman expands health coveragehttp://www.oxfordbusinessgroup.com/overview/opening-foreign-expertise-and-investment-flow-government-works-expand-coverage48- Foreign expertise and investment flow as Oman expands health coveragehttp://www.oxfordbusinessgroup.com/overview/opening-foreign-expertise-and-investment-flow-government-works-expand-coverage49- http://data.worldbank.org/indicator/SH.XPD.TOTL.ZS?locations=BH50-http://www.health.gov.bh/PDF/Publications/statistics/HS2014/PDF/Chapters/health%20summary%20statistics_2014_new%20July%202016.pdf51- http://www.dsfh.med.sa/eng/about-us/history.html52- http://www.dsfh.med.sa/eng/medical-services/specialty-units.html53- http://www.dsfh.med.sa/eng/medical-services/laboratory.html54- http://www.dsfh.med.sa/eng/medical-services/exec-health-program.html55- http://www.dsfh.med.sa/eng/medical-services/clinical-dept.html56- http://www.dsfh.med.sa/eng/about-us/history.html57- http://www.dsfh.med.sa/eng/about-us/history.html

References

www.resilienceand.co.uk Page | 35

References

58- http://www.alnoorhospital.com/overview.aspx 59- http://asterdmhealthcare.com/60- http://asterdmhealthcare.com/61- http://www.nmchealth.com/history/62- http://www.nmchealth.com/history/63- http://www.nmchealth.com/our-business/64- http://www.avivo-group.com/who-we-are.aspx65- http://www.avivo-group.com/who-we-are.aspx66- http://www.avivo-group.com/our-brands.aspx67- http://www.primehealth.ae/overview.aspx68- http://www.primehealth.ae/PrimeHospital.aspx69- http://www.primehealth.ae/services.aspx70- http://www.primehealth.ae/prime-home-care.aspx71- http://www.primehealth.ae/overview.aspx72- http://www.primehealth.ae/overview.aspx73- http://www.maidangroup.com/74- http://www.newmowasat.com/departments.aspx75- http://www.newmowasat.com/aboutus.aspx?id=6&pid=4076- http://www.newmowasat.com/aboutus.aspx?id=1&pid=6677- http://www.yiacokuwait.com/Yiaco_Medical/78- http://www.yiacokuwait.com/Yiaco_Medical/79- http://www.yiacokuwait.com/Yiaco_Medical/80- http://www.yiacokuwait.com/Yiaco_Medical/81- http://www.yiacokuwait.com/Yiaco_Medical/82- http://www.alhayathospital.com/83- http://badralsamaahospitals.com/about-us/84- http://badralsamaahospitals.com/specialities/85- http://badralsamaahospitals.com/specialities/86- http://www.bahrainspecialisthospital.com/index.php/about-us/hospital-overview87- http://www.bahrainspecialisthospital.com/index.php/facilities/bsh-juffair88- http://www.bahrainspecialisthospital.com/index.php/facilities/bshc-west-riffa89- http://www.ibnalnafees.com/about_new.php?abtid=390- http://www.ibnalnafees.com/clinic.php91- http://www.ibnalnafees.com/clinic.php

www.resilienceand.co.uk Page | 36

www.resilienceand.co.uk

© Copyrights 2016. Resilience& owns the copyrights of this document and all its contents.