health super db fund · health super db fund (a sub-fund of the first state superannuation scheme)...

TRANSCRIPT

19 August 2016

HEALTH SUPER DB FUND(A SUB-FUND OF THE FIRST STATE SUPERANNUATION SCHEME)

STATEMENT OF ADVICE

REPORT TO THE TRUSTEE ON THEACTUARIAL INVESTIGATION AS AT30 JUNE 2016

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER ii

Contents

1. Key results and recommendations ............................................................................. 1 1.1 Purpose ................................................................................................... 1 1.2 Current financial position .......................................................................... 2 1.3 Financing objective adopted for this investigation ..................................... 2 1.4 Main items of Fund experience ................................................................ 3 1.5 Current Institution contributions ................................................................ 3 1.6 Actuarial assumptions .............................................................................. 3 1.7 Recommended level of contributions ........................................................ 4 1.8 Projection of coverage of benefit liabilities ................................................ 5 1.9 Key risks and sensitivity analysis ............................................................. 5 1.10 Illustration of potential investment volatility ............................................... 7 1.11 Other recommendations ........................................................................... 8 1.12 Additional information ............................................................................... 9 1.13 Actuary’s certifications.............................................................................. 9

2. Information and data ................................................................................................ 12 2.1 Background ............................................................................................ 12 2.2 Data ....................................................................................................... 12 2.3 Data validity ........................................................................................... 12 2.4 Available assets ..................................................................................... 13 2.5 Membership ........................................................................................... 13

3. Fund experience since last investigation .................................................................. 16 Defined Benefit Scheme - active section .......................................................... 16 3.1 16 3.2 Defined Benefit Scheme - deferred section ............................................ 18 3.3 Health Super Lifetime Pension ............................................................... 19 3.4 Economic experience ............................................................................. 20 3.5 General comments ................................................................................. 21

4. Actuarial assumptions and methods ........................................................................ 23 4.1 Method of calculating the Actuarial Value of Accrued Benefits ............... 23 4.2 Economic assumptions .......................................................................... 23 4.3 Other assumptions ................................................................................. 24 4.4 Impact of assumption changes ............................................................... 30

5. Investigation results ................................................................................................. 31 5.1 Measures of benefit liabilities ................................................................. 31 5.2 Coverage of benefit liabilities.................................................................. 32 5.3 Valuation results in summary ................................................................. 35

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER iii

6. Contributions ........................................................................................................... 36 6.1 Financing objective ................................................................................ 36 6.2 Financing the benefits ............................................................................ 37 6.3 Long term contributions .......................................................................... 38 6.4 Current contributions .............................................................................. 38 6.5 Recommended level of contributions ...................................................... 39

7. Projections ............................................................................................................... 40 7.1 Target coverage ..................................................................................... 40 7.2 Projected coverage of benefits ............................................................... 40 7.3 Investment volatility ................................................................................ 41 7.4 Investment liquidity ................................................................................. 43

8. Fund details ............................................................................................................. 44 8.1 Background information ......................................................................... 44 8.2 Summary of benefits .............................................................................. 45 8.3 Minimum benefits ................................................................................... 47 8.4 Investment policy ................................................................................... 47 8.5 Crediting policy....................................................................................... 48 8.6 Insurance ............................................................................................... 48

9. Additional disclosures .............................................................................................. 50 9.1 Statements required by SIS Regulation 9.31 .......................................... 50

10.Detailed decrement experience ............................................................................... 52 10.1 Defined Benefit Scheme - active section ................................................ 52 10.2 Defined Benefit Scheme - deferred section ............................................ 54 10.3 Health Super Lifetime Pension ............................................................... 55

CertificatesSummary of actuary’s report for the purposes of Australian Accounting Standard AAS25.

This report is only in relation to the Health Super DB Fund, a sub-fund of the First StateSuperannuation Scheme. The Health Super DB Fund covers defined benefit members inthe Health Super Defined Benefit Scheme and the Health Super Lifetime Pensions. Anyreference to “the Fund” in this report refers only to the Health Super DB Fund. We havenot considered the accumulation sections of the First State Superannuation Scheme.

Any reference to “Institutions” includes all institutions who participate in the Fund asappropriate to the context.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 1

1

Key results and recommendations

1.1 Purpose

This report sets out the results of the actuarial investigation as at 30 June 2016 of theHealth Super DB Fund (“the Fund”), a sub-fund of the First State SuperannuationScheme. The Health Super DB Fund covers defined benefit members in the HealthSuper Defined Benefit Scheme and Health Super Lifetime Pensions.

This report does not consider the accumulation sections of the First StateSuperannuation Scheme.

We have prepared this report exclusively for the Trustee of the Fund for the followingpurposes:

§ Present the results of an actuarial investigation of the Fund as of 30 June 2016;§ Review Fund experience for the three year period since the last full analysis of the

Fund’s decrement experience was conducted as part of the actuarial investigation asat 30 June 2013;

§ Recommend contributions to be made by the Institutions intended to allow the Fundto meet its benefit obligations in an orderly manner, and to reach and maintain anappropriate level of security for members’ accrued benefit entitlements;

§ Satisfy the requirements of the Fund’s Trust Deed for actuarial investigations of theFund’s financial position; and

§ To meet legislative requirements under relevant Commonwealth superannuationlegislation.

The previous actuarial investigation of the Fund was conducted as at 30 June 2015 andcovered the one-year period to that date. The results of the investigation were set out ina report dated 1 September 2015.

Section 8.2 of this report provides a summary of the benefits for the active members ofthe Health Super Defined Benefit Scheme.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 2

1.2 Current financial position

A summary of the Fund’s financial position as at 30 June 2016 is set out below:

Health SuperDB Fund

As at 30 June 2016 As at 30 June 2015

$M AssetCoverage

$M AssetCoverage

Assets 1,150.2* 1,203.7Vested Benefits 1,090.4 105.5% 1,117.2 107.7%

Actuarial Value ofAccrued Benefits 1,069.5 107.5% 1,093.4 110.1%

* See Section 2.4 for calculation of the net value of assets for actuarial investigation purposes.

According to the Superannuation Industry (Supervision) legislation, the Fund is in a“satisfactory financial position” as at 30 June 2016 as the total Vested Benefits are lessthan the value of the assets. However, the coverage level is below the financingobjective of 110%.

1.3 Financing objective adopted for this investigation

The financial objective we have adopted for this investigation is to target and thenmaintain assets at least equal to 110% of the Vested Benefits of the Fund.

Most of the Fund’s liabilities (defined benefit and lifetime pension) are not linked to thereturns on the underlying assets. A margin in excess of 100% coverage of the Fund’sVested Benefits is therefore desirable to provide some security against adverseexperience such as poor investment returns. We consider that the target margin of110% strikes a suitable balance between the Trustee’s desire to provide security tomembers and the Institutions’ desire to avoid an unnecessary build-up of surplus. It isalso important that a margin is retained as, due to the maturity of the active membershipand the significant number of pensioners and deferred pensioners, any shortfalls aredifficult to fund by increasing contributions (other than by large lump sums).

Based on the assumptions adopted for this investigation, achieving the financingobjective of 110% of the Fund’s Vested Benefits would also result in at least 110%coverage of the Actuarial Value of Accrued Benefits and SG Minimum Benefits. Hence itis not considered necessary to adopt specific financing objectives in relation to thesebenefit liability measures.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 3

1.4 Main items of Fund experience

The more significant factors affecting the Fund’s financial experience during the periodsince the previous actuarial investigation in 2015 were as follows:

ItemAssumed at

previousinvestigation

Fundexperience

Comment on effect

Investment returns 5.0% pa* 4.2% p.a. Negative – investments grew ata rate less than assumed

Average Final FundSalary increases

4.4% pa 3.5% p.a. Favourable– benefit liabilitiesgrew less rapidly than expected

Indexation rate 2.5% p.a. 1.0% p.a. Favourable – pensions anddeferred benefits increased at arate less rapidly than expected

*net of tax return on assets supporting the Defined Benefit Scheme

Section 3 of the report provides further details of the Fund experience.

1.5 Current Institution contributions

The Institutions that participate in the Fund are currently contributing at the followingrates for the Defined Benefit Scheme active members:

Member contribution rate (% of Salary) 0% 3% 4% 6%Institution contribution rate (% of Salary) 1% 6% 6% 10%

1.6 Actuarial assumptionsThe main assumptions used for this investigation are:

Assumption % pa

Discount RateLump sum benefits (after tax and fees) 4.5*Pension benefits (before tax including refund of imputation credits) 5.7**

Investment return***Lump sum benefits (after tax and fees) 4.5Pension benefits (before tax including refund of imputation credits) 5.2

General salary increases 3.5Lifetime Pension and deferred benefit increases 2.25

*based on an average 5 year investment horizon**based on an average 10 year investment horizon***for next 5 years, used for the purposes of asset projections only

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 4

These assumptions should be considered in conjunction with the following points:

§ The discount rate and investment return assumptions are based on the benchmarkasset allocation of the Fund’s assets and Mercer Investment Consulting’s expectedinvestment returns for different asset classes. The expected investment expensesapplying to these assets have also been taken into account.

§ The discount rate adopted for assets supporting active and deferred lump sumbenefits is net of investment tax and fees. It assumes that these assets have anaverage 5 year investment horizon and allows for the lower than long term returnexpected on fixed interest and cash investments over this timeframe.

§ The discount rate adopted for assets backing pension liabilities is net of investmentfees but assumes that any income earned on these assets is exempt from tax andallows for the refund of imputation credits. It assumes these assets have an average10 year investment horizon and allows for the lower than long term return expectedon fixed interest and cash investments over this timeframe.

§ An allowance for age related promotional salary increases has been made in additionto the general salary increases stated above

See Section 4 for full details of all the assumptions used in the investigation.

1.7 Recommended level of contributions

We recommend that the Institutions continue to contribute to the Fund at the followingrates for the Defined Benefit Scheme active members:

MemberContribution Rate

(% of Salary)0% 3% 4% 6%

InstitutionContribution Rate

(% of Salary)1% 6% 6% 10%

The Fund’s Vested Benefits coverage is currently below the target coverage level of110%. A reduction in the recommended Institution contribution level could be consideredonce this target is reached, expected to be around 30 June 2019 based on theassumptions adopted for this investigation.

Over the long term we would expect the Institution contribution rates to reduce towardsthe long term contribution rates (refer to Section 6.3). Whilst it may be theoreticallypossible to reduce the recommended rates to the long term contribution ratesimmediately once the 110% target coverage level is reached, it may be moreappropriate to consider a staggered reduction towards these rates pending theemergence of future experience.

Note that if an actuary, whilst performing an actuarial function for the Fund, discoversthat any Institution has paid less than the recommended contributions, the SIS Actrequires that the actuary inform the Trustee and APRA.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 5

1.8 Projection of coverage of benefit liabilities

We have prepared a projection of the assets and benefit liabilities of the Fund based on:

§ the recommended Institution contribution rates set out above;§ the actuarial assumptions adopted for this investigation; and§ allowing for future member movements into the deferred and lifetime pension

sections at rates assumed for this investigation (see Section 4 for details ofmembership movement assumptions).

The following chart shows that the projected coverage of the Fund’s Vested Benefits isexpected to reach the target coverage of 110% in the next three years.

Section 7 of the report provides further details and commentary on the projection results.

1.9 Key risks and sensitivity analysis

There are a number of risks relating to the operation of the Fund. The more significantfinancial risks for the Fund are:

§ Investment risk – borne by the Institutions. The risk is that investment returns will beless than anticipated and the Institutions will need to increase contributions to offsetthis shortfall.

For example, if the assumed future investment return were reduced by 1% pa with nochange in other assumptions, then the Fund’s Vested Benefits would increase by

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 6

approximately 7.0%. This would translate to an increase of around $76.9 million inVested Benefits as at 30 June 2016.

The actual investment return achieved by the Fund in the future may vary (positivelyor negatively) from the rate assumed at this investigation. Section 7.3 provides anillustration of the impact of investment volatility on the projected coverage of VestedBenefits over the next 5 years.

§ Pensioner longevity risk – borne by the Institutions. The risk that the pensionerswill live longer than expected requiring more pension payments thereby increasingthe pension liabilities of the Fund and requiring additional contributions from theInstitutions.

§ Salary growth risk – borne by the Institutions. The risk here is that wages orsalaries (on which future benefit amounts will be based) will rise more rapidly thananticipated, increasing benefit amounts and thereby requiring additional contributionsfrom the Institutions.

For example, if the general salary increase rate were increased by 1% pa with nochange in other assumptions, then the Actuarial Value of Accrued Benefits forDefined Benefit Scheme active members would increase by 1.3%. This wouldtranslate to an increase of around $13.5 million in the Fund’s Actuarial Value ofAccrued Benefits as at 30 June 2016.

The Fund’s Vested Benefits as at 30 June 2016 however are not affected by futuresalary increases of active members.

§ Indexation risk – borne by the Institutions. The risk that the indexation applied tolifetime pensions and deferred defined benefits will be greater than expected creatinga shortfall in assets that will require additional contributions from the Institutions.

As the Fund’s lifetime pension liabilities increase as a proportion of the Fundliabilities, indexation risk will have an increasing impact on the Fund’s futureliabilities.

As it is the “gap” between assumed investment earnings and the indexation rate thatinfluences the cost of providing defined benefits, the effect of increasing the assumedpension indexation rate by 1% pa is approximately the same as reducing theassumed investment earnings by 1% pa, the results of which are presented aboveunder “Investment risk”.

§ Benefit selection risk – borne by the Institutions. The risk that the number ofmembers, who have the option to choose a pension benefit, will choose the pensionbenefit in greater numbers than assumed in the actuarial investigation. A highernumber of members choosing pensions than expected will increase the Fund’sliabilities. Any difference will impact on the Fund’s liabilities and the Institutions mayneed to increase contributions to finance such increases.

§ Legislative risk – borne by the Institutions. The risk is that legislative changes couldbe made which increase the cost of providing the defined benefits.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 7

The Fund’s Risk Management Strategy and Risk Management Policy should identify afull range of risks faced by the Trustee.

1.10 Illustration of potential investment volatility

The Fund’s investments reflect an investment policy as outlined in detail in Section 8.4 ofthis report.

The following projection indicates that, in three years’ time, there is an 80% chance thatcoverage will be in the range of 99% to 121%. Please refer to Section 7.3 of this reportfor further details.

The Trustee should understand that investment returns experienced by the Plan may beworse than that allowed for in the Low Return Scenario shown in the projection.Therefore, it is possible that coverage of Vested Benefits may fall below 100%. As such,it will be necessary for the Trustee to monitor coverage levels regularly during the periodto the next investigation so that corrective action can be implemented as early aspossible in the event this occurs. The Fund’s Funding and Solvency Certificate specifies“Notifiable Events” which the Trustee needs to monitor on a regular basis. These aredesigned to detect any adverse changes in the Fund’s financial position.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 8

1.11 Other recommendations

1.11.1 Investment policy

We confirm that the Fund’s current investment policy of 42% ‘growth’ assets and 58%‘defensive’ assets remains appropriate, provided that the Institutions recognise andaccept the potential variability in returns and contribution requirements.

The expected average term of the Fund’s liabilities in respect of the Defined BenefitScheme (active and deferred sections) is approximately 4.0 years. While a proportion ofmembers are eligible to receive pension benefits, a large proportion will receive lumpsum payments. Accordingly there will be a significant level of benefit outflow, exceedingnet contributions. This illustrates a need for the Trustee to ensure that the Fund’sinvestments provide a suitable level of liquidity to meet projected benefit obligations.

1.11.2 Crediting policy

A detailed review of the approach for crediting earnings to members’ accounts is outsidethe scope of this investigation. Based on a review of the main features, we consider thatthe approach adopted is generally suitable taking into consideration the principles ofequity between different generations of members and any material risks which may havea significant impact on the Fund (i.e. a market shock or sudden downturn in investmentmarkets).

1.11.3 Insurance

As at 30 June 2016, both death and disability benefits of Defined Benefit Scheme activemembers were fully insured, but there was an insurance “shortfall” of $70.7 million ontheir total disability benefits. This result assumes that all active Fund members becamedisabled at the same time. However, in practice the number of members becomingdisabled and taking a pension is a small portion of the Defined Benefit Scheme activemembership and the risk of a large number of disablements occurring together is sosmall that it could be ignored.

We confirm that the current group life insurance formula is appropriate and providesadequate protection for the Fund.

Section 8.6 of the report provides further details.

1.11.4 Action required

The Trustee should consider this report and confirm their agreement (or otherwise) to thecontribution and other recommendations.

The Trustee should obtain formal agreement of each Institution that it will contribute tothe Fund in accordance with the recommendations of this report.

The progress of the Fund’s coverage of Vested Benefits should be reviewed after eachannual review of the Fund and Institution contribution levels adjusted accordingly.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 9

1.12 Additional information

Significant events since the investigation date – we are not aware of any significantevents that have occurred since 30 June 2016, which we have not already taken intoaccount, which would have a material impact on the recommendations in this report.

Next actuarial investigation – as the Fund has current pensioners, the SIS legislationrequires that annual actuarial investigations be carried out. As such, the next annualactuarial investigation of the Fund will occur as at 30 June 2017.

Enclosed certificates - a certificate for Australian Accounting Standard AAS25purposes is enclosed and forms part of this report.

Funding and Solvency Certificate – expires on 30 June 2018, needs to be replaced by30 June 2017.

Benefit Certificate – expires on 30 June 2018. This certificate is required primarily bythe Institutions to demonstrate compliance with its Superannuation Guaranteeobligations to employees who are members of the Fund.

1.13 Actuary’s certifications

1.13.1 Professional standards and scope

This report has been prepared in accordance with generally accepted actuarialprinciples, Mercer internal standards, and the relevant Professional Standards of theInstitute of Actuaries of Australia, in particular PS400 which applies to “...actuarialinvestigations of the financial condition of wholly or partially funded defined benefitsuperannuation funds.”

1.13.2 Use of report

This investigation report should not be relied upon for any other purpose or by any partyother than the Trustee of the Fund. Mercer is not responsible for the consequences ofany other use. This report should be considered in its entirety and not distributed inparts.

The advice contained in this report is given in the context of Australian law and practice.No allowance has been made for taxation, accountancy or other requirements in anyother country.

1.13.3 Actuarial uncertainty and assumptions

An actuarial investigation report contains a snapshot of a Fund’s financial condition at aparticular point in time, and projections of the Fund’s estimated future financial positionbased on certain assumptions. It does not provide certainty in relation to a Fund’s futurefinancial condition or its ability to pay benefits in the future.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 10

Future funding and actual costs relating to the Fund are primarily driven by the Fund’sbenefit design, the actual investment returns, the actual rate of salary inflation and anydiscretions exercised by the Trustee or the Institutions. The Fund’s actuary does notdirectly control or influence any of these factors in the context of an actuarialinvestigation.

The Fund’s future financial position and the recommended Institution contributionsdepend on a number of factors, including the amount of benefits the Fund pays, thecause and timing of member withdrawals, Fund expense, the level of taxation and theamount earned on any assets invested to pay the benefits. These amounts and othersare uncertain and unknowable at the valuation date but are predicted to fall within areasonable range of possibilities.

To prepare this report, assumptions, as described in Section 4, are used to select asingle scenario from the range of possibilities. The results of that single scenario areincluded in this report.

However, the future is uncertain and the Fund’s actual experience will differ from thoseassumptions; these differences may be significant or material. In addition, differentassumptions or scenarios may also be within the reasonable range and results based onthose assumptions would be different.

Actuarial assumptions may also be changed from one valuation to the next because ofmandated requirements, Fund experience, changes in expectations about the future andother factors. We did not perform, and thus do not present, an analysis of the potentialrange of future possibilities and scenarios.

Because actual Fund experience will differ from the assumptions, decisions about benefitchanges, investment policy, funding amounts, benefit security and/or benefit relatedissues should be made only after careful consideration of alternative future financialconditions and scenarios, and not solely on the basis of a set of valuation results.

1.13.4 Data and Fund provisions

To prepare this report, we have relied on financial and participant data provided by theTrustee. The data used is summarised in this report. We have reviewed the financial andparticipant data for internal consistency and general reasonableness and believe it issuitable for the purpose of this report. We have not verified or audited any of the data orinformation provided. We have also relied upon the documents, including amendments,governing the Fund as provided by the Trustee. The Trustee is ultimately responsible forthe validity, accuracy and comprehensiveness of this information. If the data or Fundprovisions are not accurate and complete, the valuation results may differ significantlyfrom the results that would be obtained with accurate and complete information; this mayrequire a revision of this report.

1.13.5 Further information

If requested, the actuary is available to provide any supplementary information andexplanation about the actuarial investigation.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 11

Prepared by

...................................................................Richard R CodronFellow of the Institute of Actuaries of AustraliaRepresentative of Mercer Consulting (Australia) Pty LtdAFS Licensee #411770

19 August 2016

I have reviewed this report under Mercer’s professional Peer Review Policy. I amsatisfied that it complies with applicable professional standards and uses assumptionsand methods which are suitable for the purpose.

...................................................................Paul GilbertFellow of the Institute of Actuaries of AustraliaRepresentative of Mercer Consulting (Australia) Pty LtdAFS Licensee #411770

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 12

2

Information and data

2.1 Background

The table below gives an overview of the type of benefits provided by each section of theFund.

Section of the Fund Type of Benefit

Health Super Defined Benefit Scheme Defined benefitHealth Super Lifetime Pension Lifetime pension

2.2 Data

For the purposes of this investigation, the Trustee provided the following:

1. Data for all persons who were active or deferred members of the Defined BenefitScheme or pensioners in the Lifetime Pension section of the Fund at any time duringthe period from 30 April 2015 to 30 April 2016;

2. Details of rates of indexation applied to Lifetime Pension and deferred defined benefitbalances;

3. An estimate of the net of tax investment earnings of the Fund assets for the year to30 June 2016; and

4. The net value of Fund assets as at 30 April 2016.

Members’ account balances, defined benefit multiples and pension amounts wereappropriately adjusted for the two month period from 30 April 2016 to 30 June 2016.

2.3 Data validity

We have performed reasonableness checks on the data provided by the Trustee forvaluation purposes. Our checks highlighted some inconsistencies and adjustments have

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 13

been made to allow for these. We have relied on the data provided by the Trustee andthe discussions on which the data adjustments were based to perform this valuation.

A membership reconciliation was performed by Mercer to account for the changes inmembership of the Defined Benefit Scheme and Lifetime Pension sections over the 12months since the previous actuarial investigation. Where members cannot be trackedbased on the data, we make assumptions on the members’ current status based oninformation available.

2.4 Available assets

The Fund administrator advised us on 20 June 2016 that the net value of the Fundassets as at 30 April 2016 was $1,138.9 million. We understand that this value does notinclude any portion of the Scheme’s Administration Reserve or Operational RiskFinancial Requirement Reserve.

We have rolled forward the value of assets from 30 April 2016 to 30 June 2016 byallowing for contributions, outstanding lump sum benefit payments in respect ofmembers who exited prior to 1 May 2016, expected pension payments, expenses, taxesand investment earnings based on returns for May and June advised by First State.

The total Fund assets adopted for the purposes of the 2016 Annual ActuarialInvestigation is $1,150.2 million as set out below.

$m

Net Assets as at 30 April 2016 1,138.9

Due and unpaid benefits at 30 April 2016 (4.1)

Cash flow assumed for May and June (3.8)

Investment earnings assumed for May and June 16.4

Tax adjustment 2.8

Net Assets as at 30 June 2016 1,150.2

2.5 Membership

The actuarial overview of the Fund as at 30 June 2016 was based on the following data:§ 2,238 Health Super Defined Benefit Scheme active members with total full time

equivalent salaries of $206.9 million;§ 2,295 members with deferred benefits in the Health Super Defined Benefit

Scheme; and§ 3,543 pensioners in the Health Super Lifetime Pension section with annual

pensions of $41.1 million.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 14

2.5.1 Defined Benefit Scheme – active membership

A summary of the Defined Benefit Scheme active membership by member contributionrate as at 30 June 2016 is as follows:

0% Contributors3% and 3.5%Contributors 4% contributors 6% contributors

AgeGroup

Number TotalSalaries*

($000)

Number TotalSalaries*

($000)

Number TotalSalaries*

($000)

Number TotalSalaries*

($000)

40 - 44 5 221.5 2 83.7 4 181.2 10 632.245 - 49 39 2,375.9 38 2,438.1 20 1,220.3 73 4656.950 - 54 63 4,940.5 77 5,481.4 42 3,052.9 251 18,314.055 - 59 51 4,000.4 110 7,629.1 73 5,677.6 505 42,098.560 – 64 30 2,694.2 67 4,360.0 73 5,164.3 527 45,461.5> 65 145 12,421.8 2 93.2 3 136.1 28 2,248.8Totals 333 26,654.3 296 20,085.5 215 15,432.4 1,394 113,411.9

* Salaries in the above table are estimated actual Fund salaries (adjusted to reflect service fractions) as at30 June 2016 totalling $175.6 million.

The Defined Benefit Scheme active membership as at 30 June 2016 by age group isshown in the following graph:

As shown in the graph, 72% of the Defined Benefit Scheme active membership is overage 55 and therefore eligible for retirement as at 30 June 2016. A further 19% willbecome eligible for retirement in the next five years.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 15

2.5.2 Defined Benefit Scheme – deferred membership

The Defined Benefit Scheme deferred membership as at 30 June 2016 by age group isshown in the following graph:

As shown in the graph, 53% of the Defined Benefit deferred section membership is overage 55 and therefore eligible for retirement benefits as at 30 June 2016. A further 30%will become eligible for retirement benefits in the next 5 years. We note that whilstmembers over the age of 55 could withdraw their benefits at any time, members belowthe age of 55 can transfer a discounted lump sum into another eligible superannuationfund at any time.

2.5.3 Health Super Lifetime Pension

A summary of pensioners in this section as at 30 June 2016 is as follows:

Pension TypeNumber ofPensioners Average Age

Annual Pension$000

Retirement 2,359 75.7 31,469Spouse 568 82.9 3,961Disablement 612 74.3 5,633Child 4 16.6 14Total 3,543 76.5 41,077

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 16

3

Fund experience since last investigation

The last complete analysis of the Fund’s experience with regards to the rate membersexit the Fund or select particular benefit options was conducted as part of the 30 June2013 actuarial investigation. Assumptions relating to these items should be based onthe experience of the Fund over a number of years.

The following examines the Fund’s experience over the 34 month and 70 month periodsended 30 April 2016. For ease of reference we have referred to these periods as threeyears and six years respectively.

3.1 Defined Benefit Scheme - active section

3.1.1 Normal and late retirement

There were 289 normal and late retirements of Defined Benefit Scheme activemembers over the last three years. These have not been included in the analysis belowbecause our projection model assumes a member will retire once they attain age 65.The fact that some members may actually retire after age 65 has no significantfinancial impact on the Fund.

3.1.2 Early retirement

Three years ended30 April 2016

Six years ended30 April 2016

Type of Exit Actual Expected Actual Expected

Retirement 623 543 1,318 1,252

Over the three and six year periods, the actual number of early retirements was higherthan expected. Therefore, we have increased our early retirement rates at various ages(refer to Section 4.3.8).

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 17

Greater early retirements than expected would generally have a small negative impacton the Plan’s financial position.

3.1.3 Resignation

Three years ended30 April 2016

Six years ended30 April 2016

Type of Exit Actual Expected Actual Expected

Resignation 92 68 201 197

The actual number of resignations was greater than expected over the three year period to30 April 2016. Greater resignations than expected would have generally had a smallpositive impact on the Fund’s financial position.

Over the six year period the number of resignations was very close to that expected. At the2013 investigation we reduced the assumed rates of resignation from ages 45-54 based onthe Fund’s experience. While the three year experience suggests that an increase inresignation rates may be required, we note that around half of the 92 resignations occurredin the first six months of 2015. Outside of this period actual experience has been broadly inline with our assumptions. Therefore, we have maintained the same assumed resignationrates for this investigation.

3.1.4 Death in service

During the three year period to 30 April 2016 there was 1 death in service for membersover age 65. These deaths are not included in the analysis below.

Three years ended30 April 2016

Six years ended30 April 2016

Type of Exit Actual Expected Actual Expected

Death 12 15 22 36

At the 2013 investigation we adopted mortality rates equal to 50% of the Australian LifeTable 2005-2007. The actual number of deaths was slightly lower than expected over thethree year period and significantly lower than expected over the six year period. Giventhat a lower number of deaths than expected would generally have a very small positiveimpact on the Fund’s financial position, we have maintained the same mortalityassumptions for this investigation.

3.1.5 Disablement

Three years ended30 April 2016

Six years ended30 April 2016

Type of Exit Actual Expected Actual Expected

Disablement 12 13 17 32

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 18

The actual number of disablements has been less than expected over the six-yearperiod, but in line with expected over the three-year period. A lower number ofdisablements than expected would generally have a very small positive impact on theFund’s financial position. We have maintained our disablement rates for thisinvestigation.

3.1.6 Old Scheme Benefit options

Proportion of eligible members who have taken the OldScheme Benefit over the three years ended 30 April 2016

Type of Exit Actual Expected

Resignation 80% 80%Retirement 76% 80%

Over the three years to 30 April 2016, the actual number of eligible members who chosethe Old Scheme benefit on resignation or retirement was close to expected.Therefore, we have maintained the 80% assumption for this investigation.

3.2 Defined Benefit Scheme - deferred section

3.2.1 Payment of deferred benefits

The table below compares the actual number of members aged 55 to 64 who were paidtheir deferred benefit against the expected number of members.

Three years ended30 April 2016

Six years ended30 April 2016

Actual Expected Actual Expected

Retirement 388 488 885 1008

The actual number of members who were paid their deferred retirement benefit aged 55to 64 was less than expected. A lower number of deferred benefit payments thanexpected would generally have a slight positive impact on the financial position of theFund.

We have reduced the assumed early retirement rates at various ages in light of thisexperience.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 19

3.2.2 Transfer of deferred benefits

For the 2013 and subsequent investigations, we assumed that 1.6% of the deferredmembers in the Defined Benefit Scheme would transfer (or rollover) their benefit out ofthe Fund each year.

As shown in the above table, the number of members who transferred their deferredbenefit is in line with that expected.

Therefore we have maintained our transfer assumptions for this investigation.

3.2.3 Benefit chosen for Option 3 deferred members

Option 3 deferred members are eligible to choose between a lump sum benefit and alump sum plus pension. Based on the data provided, over the three year period to 30April 2016 there were 44 deferred members classified as Option 3 who left the definedbenefit scheme. Of these, 73% chose to take the lump sum plus pension benefitcompared to our assumption of 75%.

Valuing the benefit as a lump sum plus pension generally produces a higher liabilityvalue than valuing it as a lump sum only. Therefore, a lower number of pensionselections would have a slight positive impact on the financial position of the Fund.

We have maintained the 75% assumption for this investigation.

3.3 Health Super Lifetime Pension

In analysing the mortality experience of pensioners we have assumed that members whoceased being paid a pension over the six years due to a “temporary suspension” of theirpension and who were not included in the listing of current pensioners or suspendedpensioners have died.

This makes a complete and full mortality analysis a difficult and inexact. Indeed itrequires a detailed understanding of administration processes to properly allow forissues such as delays in death notification. Our analysis can only make an attempt toallow for the impact of such issues and this should be borne in mind when consideringthe results.

Three years ended30 April 2016

Six years ended30 April 2016

Actual Expected Actual ExpectedDeferred Option 56 56 132 139

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 20

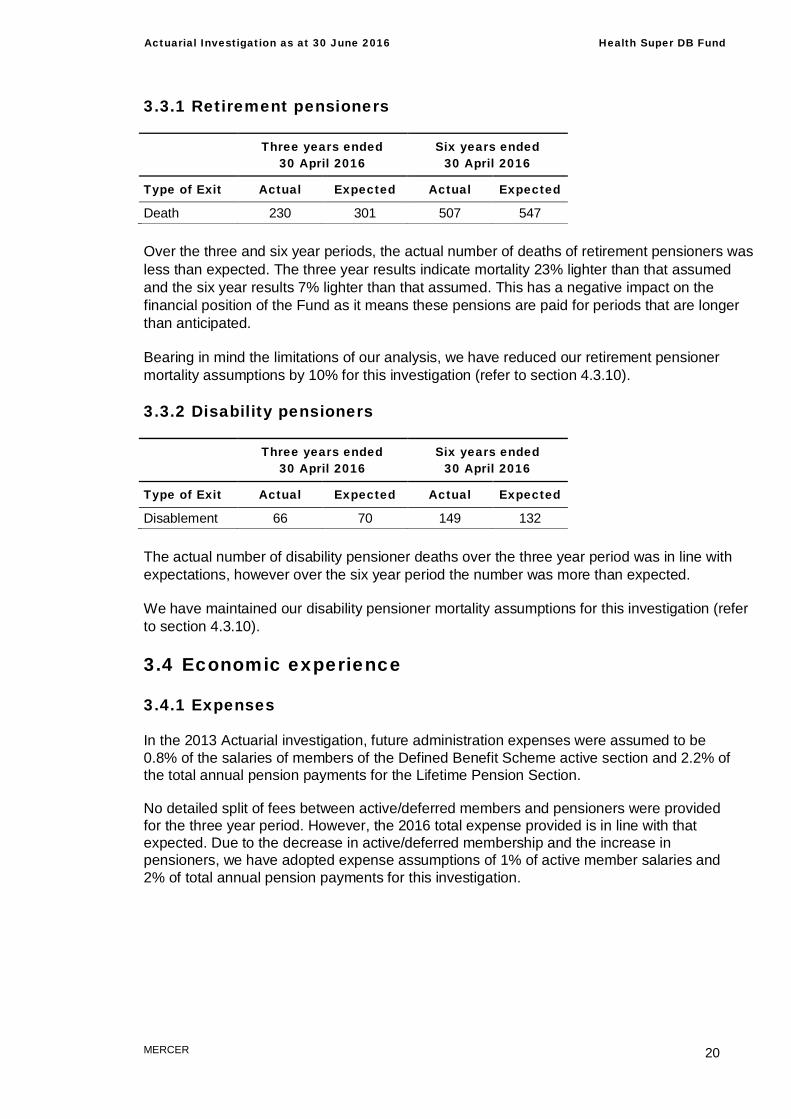

3.3.1 Retirement pensioners

Three years ended30 April 2016

Six years ended30 April 2016

Type of Exit Actual Expected Actual Expected

Death 230 301 507 547

Over the three and six year periods, the actual number of deaths of retirement pensioners wasless than expected. The three year results indicate mortality 23% lighter than that assumedand the six year results 7% lighter than that assumed. This has a negative impact on thefinancial position of the Fund as it means these pensions are paid for periods that are longerthan anticipated.

Bearing in mind the limitations of our analysis, we have reduced our retirement pensionermortality assumptions by 10% for this investigation (refer to section 4.3.10).

3.3.2 Disability pensioners

Three years ended30 April 2016

Six years ended30 April 2016

Type of Exit Actual Expected Actual Expected

Disablement 66 70 149 132

The actual number of disability pensioner deaths over the three year period was in line withexpectations, however over the six year period the number was more than expected.

We have maintained our disability pensioner mortality assumptions for this investigation (referto section 4.3.10).

3.4 Economic experience

3.4.1 Expenses

In the 2013 Actuarial investigation, future administration expenses were assumed to be0.8% of the salaries of members of the Defined Benefit Scheme active section and 2.2% ofthe total annual pension payments for the Lifetime Pension Section.

No detailed split of fees between active/deferred members and pensioners were providedfor the three year period. However, the 2016 total expense provided is in line with thatexpected. Due to the decrease in active/deferred membership and the increase inpensioners, we have adopted expense assumptions of 1% of active member salaries and2% of total annual pension payments for this investigation.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 21

3.4.2 Investment returns

The 2015 investigation assumed that investment returns would average 5.0% pa (net oftax and investment fees) on non-pension assets. The fact that the Fund’s investmentreturn (net of tax and investment fees) on non-pension assets was 4.2% over the year to30 June 2016 has had a negative impact on the Fund’s financial position.

3.4.3 Salary increases

We have analysed salary increases over the year to 30 June 2016.

We note that in many individual cases the change in salary from 30 June 2015 to30 June 2016 is outside the range we would expect. However, this is the information thatwas provided to the Trustee by the Institutions. As a result and in line with past practice,we analysed the change in AFFS as the benefits are directly dependent on this value.We found that the overall increase in AFFS over the 12 months for members whoremained active was 3.5%.

At the 2015 investigation, it was assumed that salary increases would be 4.0% pa plusage related promotional increases such that average total salary increases per annumwould be expected to be around 4.4%. Therefore, AFFS increased at a rate lower thanexpectations which would have had a favourable impact on the Fund’s financial position.

3.4.4 Contributions

Since the previous investigation, participating Institutions have contributed to the Fund inaccordance with the actuarial recommendations. As the recommended contributionrates exceed the long term rates required to fund the accrual of defined benefits, this hashad a positive impact on the Fund’s financial position.

3.4.5 Pension and deferred benefit indexation

Lifetime pensions and deferred defined benefits are indexed based on changes in theConsumer Price Index (CPI).

At the 2015 investigation, it was assumed that the indexation rate would be 2.5% pa. Asthe actual indexation rate of 1.0% was less than expected, this had a positive impact onthe Fund’s financial position.

3.5 General comments

We have determined that Fund assets are in excess of the Fund’s vested benefits by$59.9 million as at 30 June 2016.

The actuarial investigation as at 30 June 2015 revealed that Fund assets were in excessof the Fund’s Vested Benefits by $86.5 million. Therefore, the Fund’s financial positionhas declined by $26.6 million over the year to 30 June 2016. This reduction is primarilydue to:

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 22

§ the change in assumptions adopted for this investigation; and§ the Fund’s actual investment return over the year being lower than assumed.

The negative experience items were partially offset by:

§ salary increases over the year being lower than expected;§ the Institution contributions in respect of defined benefit members being higher than

those required to fund the future accrual of their benefits; and§ the indexation rate applied to lifetime pensions and deferred benefits being less than

expected.

Ultimately, the cost to Institutions of maintaining the Fund depends on actual experience,not actuarial assumptions. The actuarial assumptions primarily influence the timing ofcontributions to the Fund.

However, it is possible for experience to differ from that assumed without changes to theInstitution’s contributions being required, as the financial impact of variations in some areascan offset variations in others.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 23

4

Actuarial assumptions and methods

This section sets out the actuarial assumptions and methods used for this investigationas at 30 June 2016.

4.1 Method of calculating the Actuarial Value ofAccrued Benefits

The calculation of the Actuarial Value of Accrued Benefits has been carried out using amethod of apportionment of benefits between past and future membership that satisfiesthe requirements of Professional Standard No. 402 of the Institute of Actuaries ofAustralia and is acceptable for Australian Accounting Standard AAS25 purposes.More details on the method can be found in the attached summary of the actuarial reportprepared for AAS25 purposes.

4.2 Economic assumptions

The most significant assumption influencing the cost of defined benefits is the differencebetween:

§ the assumed investment earnings; and§ the salary increases used in the projections of future benefit payments.

This difference is commonly referred to as the “gap”.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 24

The key economic assumptions adopted for this investigation are:

Assumption % pa

Discount RateLump sum benefits (after tax and fees) 4.5*Pension benefits (before tax including refund of imputation credits) 5.7**

Investment return***Lump sum benefits (after tax and fees) 4.5Pension benefits (before tax including refund of imputation credits) 5.2

General salary increases 3.5Lifetime Pension and deferred benefit increases 2.25

*based on an average 5 year investment horizon**based on an average 10 year investment horizon***for next 5 years, used for the purposes of asset projections only

These assumptions should be considered in conjunction with the following points:

§ The discount rate and investment return assumptions are based on the benchmarkasset allocation of the Fund’s assets and Mercer Investment Consulting’s expectedinvestment returns for different asset classes. When setting the assumptions theexpected investment expenses applying to these assets have also been deductedfrom the expected investment return.

§ The discount rate adopted for assets supporting active and deferred lump sumbenefits is net of investment tax and fees. It assumes that these assets have anaverage 5 year investment horizon and allows for the lower than long term returnexpected on fixed interest and cash investments over this timeframe.

§ The discount rate adopted for assets backing pension liabilities is net of investmentfees but assumes that any income earned on these assets is exempt from tax andallows for the refund of imputation credits. It assumes these assets have anaverage 10 year investment horizon and allows for the lower than long term returnexpected on fixed interest and cash investments over this timeframe.

§ An allowance for age related promotional salary increases has been made inaddition to the general salary increases stated above.

4.3 Other assumptions

4.3.1 New members

The Defined Benefit Scheme is primarily closed to new members. Members of theformer Basic Benefit Scheme are able to join but past Fund experience indicates thatvery few do so. Therefore, we have assumed that no new members join the DefinedBenefit Scheme in the future.

The same assumption was used in the 2015 investigation.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 25

4.3.2 Expenses

For the Defined Benefit Scheme, we have assumed administration expenses at 1.0% ofactive members’ salaries.

For the Lifetime Pension section, we have assumed administration expenses at 2.0% oftotal annual pension payments.

Administration expenses at 0.8% of active members’ salaries and administrationexpenses of 2.2% of total annual pension payments were used in the 2015 investigation.

4.3.3 Tax

All future Institution contributions are currently subject to 15% contribution tax, afterdeduction of any insurance premiums and administration and management costs. Allcontribution recommendations quoted in this report are gross of contribution tax.

4.3.4 Proportions married

It is assumed that 70% of pensioners, and 90% of Defined Benefit Scheme activemembers are married, or have dependants.

4.3.5 Spouse ages

Husbands are assumed to be three years older than wives.

4.3.6 Medical classifications (death and disablement benefits)

It is assumed that all members are entitled to standard death and disablement benefits.

4.3.7 Membership movement assumptions

The following pages give details of the assumed rates of turnover in respect of activeand deferred members of the Defined Benefit Scheme and pensioners in the LifetimePension section.

4.3.8 Defined Benefit Scheme - active members

Transfer of deferred benefitsWe have assumed that 2% of active members leaving prior to age 55 immediatelytransfer their deferred benefit out of the Fund.

The same assumption was used in the 2015 investigation.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 26

Division D – Old Scheme BenefitsDivision D members are entitled to elect to receive Old Scheme Benefits (lump sum pluspension benefits). We have assumed the following for this investigation:

Benefit Type

Proportion of EligibleMembers electing

Old Scheme Benefits

Retirement 80%Death 50%Disablement 70%Resignation 80%

The same assumptions were used in the 2015 investigation.

Promotional salary increasesMembers are assumed to receive promotional salary increases, in addition to generalinflationary salary increases, according to an age-related scale. The assumptions remainunchanged from 2015. Specimen promotional increases are:

Age Last Birthday Promotional Salary Increase (%)

35 1.040 0.645 0.650 0.755 0.560 0.2

Mortality and disablement

The number of members (per 100,000) assumed to leave the Fund due to death anddisablement are:

Age Last Death Disablement

Birthday Male Female Male and Female

35 56 27 2040 73 40 3845 102 62 5850 152 94 12755 227 136 27260 361 218 307

The same assumptions were used in the 2015 investigation.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 27

Resignations

The number of members (per 100,000) assumed to leave the Fund on account ofresignation are:

Age Last Resignation

Birthday Male Female

35 5,980 4,60040 5,525 4,18045 3,500 2,56050 3,500 2,560

The same assumption was used in the 2015 investigation.

Early retirement

The actual number of early retirements was higher than expected. Therefore, we haveincreased our early retirement rates at various ages

The number of members (per 100,000) assumed to leave the Fund on account of earlyretirement are:

Age Last Retirement

Birthday Male and Female

55 10,00056 6,00057 7,00058 7,00059 8,00060 17,00061 10,00062 13,00063 15,00064 22,00065 100,000

Retrenchment

Due to the nature of retrenchments, it is difficult to predict the number of retrenchmentsthat may occur. Therefore, no members are assumed to be retrenched by theInstitutions.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 28

4.3.9 Defined Benefit Scheme - deferred members

Transfer of deferred benefitsWe assumed that 1.6% of deferred members per annum in the Defined Benefit Schemewill transfer their benefit out of the Fund.

The same assumption was used in the 2015 investigation.

Death and disablements

We have adopted the same mortality assumptions for the Defined Benefit Schemedeferred members as for the active members. The number of members (per 100,000)assumed to leave the Fund due to death are:

Age Last DeathBirthday Male Female

35 56 2740 73 4045 102 6250 152 9455 227 13660 361 218

It is assumed that no deferred member will leave the Fund due to disablement.

The same assumptions were used in the 2015 investigation.

Early retirement

We have reduced the assumed rates of retirement for deferred members in line with theFund’s actual experience at different ages. The number of members (per 100,000)assumed to leave due to early retirement are:

Age Last RetirementBirthday Male and Female

55 28,00056 9,00057 10,00058 8,00059 8,00060 16,00061 12,00062 10,00063 10,00064 12,00065 100,000

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 29

Benefit option selection for Option 3 members

The Fund’s experience over the three years to 30 June 2016 indicated that 73% ofOption 3 members elected to take an Old Scheme Benefit. We have maintained ourassumption from the 2015 investigation that 75% of Option 3 members take a lump sumplus pension (Old Scheme Benefit) and 25% take a lump sum only.

4.3.10 Health Super Lifetime Pension

Retirement pensioners

The number of retirement pensioners (per 100,000) assumed to leave the Fund due todeath are:

Age LastRetirement pensioner mortality

(base rates)Annual retirement pensioner

mortality improvement discount

Birthday Male Female Male Female

60 329 208 3.33% 2.52%65 562 389 3.29% 2.52%70 1,048 598 3.08% 2.45%75 2,164 1,325 2.73% 2.30%80 4,143 2,720 2.21% 2.07%85 7,838 6,234 1.61% 1.62%90 14,174 10,392 1.07% 1.03%95 22,384 20,211 0.78% 0.68%

100 30,259 28,911 0.51% 0.47%105 100,000 100,000 0.24% 0.26%

The base pensioner mortality rates are multiplied by (1 – the annual retirement pensionermortality improvement discount) for the number of years since 30 June 2007.

We have reduced the mortality rate assumptions by 10% since the 2015 investigation.

Disablement pensioners

We have maintained from our 2015 investigation mortality rates equal to 100% ofAustralian Life Table 2005-2007. The number of disablement pensioners (per 100,000)assumed to leave the Fund due to death are:

Age Last Disablement pensioners mortality

Birthday Male Female

60 721 43665 1,200 67970 1,920 1,11575 3,312 1,98280 5,760 3,661

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 30

Age Last Disablement pensioners mortality

Birthday Male Female

85 9,907 7,08890 16,286 13,09495 23,106 20,895

100 28,205 28,281105 100,000 100,000

4.4 Impact of assumption changes

The following table summarises the changes in assumptions from those used in theprevious investigation and their impact on the investigation results.

Assumption Change ImpactDiscount rate Reduced by 0.5% Negative

General salary increaserate

Reduced by 0.5% Favourable

Pension Indexation rate Reduced by 0.25% Favourable

Actives –Retirement decrement

Increased rates for various ages Minor negative

Deferred –early retirement rates

Increased for various ages Minor negative

Pensioners –mortality rates

Reduced rates by 10% Negative

Expense Increase expense assumptions for activemembers and decreased expenseassumptions for pensioners

Negligible in total

The overall impact of the changes in assumptions was to increase the Actuarial Value ofAccrued Benefits by $28.0m.

The assumption changes increased the assessed long-term employer cost of providingfuture service benefits by around 0.2% of salaries.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 31

5

Investigation results5.1 Measures of benefit liabilitiesThe following measures of benefit liabilities have been used in this investigation.

Vested Benefits – the benefits payable as of right if all members resigned or, if eligible,retired at the investigation date. Coverage of less than 100% of these benefits wouldmean that the Fund is in an “Unsatisfactory Financial Position” as defined underCommonwealth superannuation legislation. The Fund’s current financing objective is totarget and then maintain coverage of 110% Vested Benefits in respect of definedbenefits. It is also important that a margin is retained as, due to the maturity of the activemembership and the significant number of pensioners and deferred pensioners, anyshortfalls are difficult to fund by increasing contributions (other than by large lump sums).

Section 1.8 of this report provides a projection of coverage of Vested Benefits over thenext few years, and reflects the effects of any significant changes in Vested Benefits formembers.

Actuarial Value of Accrued Benefits – an actuarial value of all future expected benefitpayments, attributable to membership to date, discounted to the investigation date.These benefits are calculated using the actuarial methods and assumptions set out inSection 4 of this report. This value is consistent with Accrued Benefits for the purposesof AAS25.

The benefit applicable on early retirement for members of the Fund will often exceed theActuarial Value of Accrued Benefits, and so coverage of Vested Benefits may be a moreimportant indicator of the financial strength of the Fund. However, the Vested Benefit formembers not yet eligible for early retirement will generally be less than the ActuarialValue of Accrued Benefits, and so changes in members’ ages over time could result insignificant changes in the coverage level of Vested Benefits.

SG Minimum Benefits – the benefits determined in accordance with the Fund’s BenefitCertificate, being the minimum amounts required from this Fund to satisfy theInstitution’s obligations under Superannuation Guarantee legislation. If assets do notprovide at least 100% coverage of SG Minimum Benefits (known as MRBs), the Fund is

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 32

classified as being ‘technically insolvent’ under relevant Commonwealth superannuationlegislation.

5.1.1 Vested Benefits

We estimate the total Vested Benefits of the Fund as at 30 June 2016 to be$1,090.4 million.

The Vested Benefits can be attributed to the various sections of the Fund as follows:

30 June 2016 ($M)

Health Super Lifetime Pensions 536.6Health Super Defined Benefit Scheme – active members 482.0Health Super Defined Benefit Scheme – deferred members 71.8Total 1,090.4

5.1.2 Actuarial Value of Accrued Benefits

We estimate the Actuarial Value of Accrued Benefits of the Fund as at 30 June 2016 tobe $1,069.5 million.

The Actuarial Value of Accrued Benefits can be attributed to the various sections of theFund as follows:

30 June 2016 ($M)

Health Super Lifetime Pensions 536.6Health Super Defined Benefit Scheme – active members 461.1Health Super Defined Benefit Scheme – deferred members 71.8Total 1,069.5

5.2 Coverage of benefit liabilities

5.2.1 Coverage of benefit liabilities at 30 June 2016

As at 30 June 2016, the Fund’s Vested Benefits and the Actuarial Value of AccruedBenefits were covered by the Fund’s assets. The following table sets out the coverage ofthe benefits as at 30 June 2016, with the corresponding values at 30 June 2015, 30 June2014 and 30 June 2013 for comparison.

Coverage of Benefits by Assets

As at 30 June 2016 2015 2014 2013

Vested Benefits 105.5% 107.7% 105.9% 101.0%Actuarial Value of AccruedBenefits 107.5% 110.1% 108.2% 102.5%

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 33

According to the Superannuation Industry (Supervision) legislation, the Fund is in a“satisfactory financial position” as at 30 June 2016 as the Vested Benefits are less thanthe value of the assets.

5.2.2 Cover for Defined Benefit Scheme liabilities

If it is assumed that lifetime pension benefits are fully funded, then the value of Fund assetsavailable to meet liabilities in respect of Defined Benefit Scheme members, includingdeferred members, is $613.6 million.

The following table sets out the coverage by these assets of the benefits for Defined BenefitScheme members as at 30 June 2016, with the corresponding values at 30 June 2015, 30June 2014 and 30 June 2013 for comparison.

Coverage of Benefits forDefined Benefit Scheme Members

As at 30 June 2016 2015 2014 2013

Vested Benefits 110.8% 114.1% 110.0% 101.7%Actuarial Value of AccruedBenefits

115.1% 118.7% 114.2% 104.2%

The following graph shows the Vested Benefits and Actuarial Value of Accrued Benefitsof the Defined Benefit Scheme members, including active and deferred members, at30 June 2016, split by age.

As shown in the graph above only those members who are under age 50 have anActuarial Value of Accrued Benefits that is greater than or equal to their Vested Benefit.The graph also shows that approximately 81% of the Defined Benefit Scheme Vested

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 34

Benefits relates to the members who are over age 55 and therefore eligible forretirement.

5.2.3 Cover for Minimum Requisite Benefits of Defined BenefitScheme active members

The Fund is used to meet the Superannuation Guarantee requirements in respect ofmembers in the Defined Benefit Scheme. The minimum benefit payable in respect ofthese Fund members, known as the Minimum Requisite Benefit (“MRB”), is described inthe Fund’s Benefit Certificate.

For the Defined Benefit Scheme active members (members who have non-deferredbenefits), employers’ Superannuation Guarantee contributions are paid to accumulationaccounts external to the Fund. The MRB within the Defined Benefit Scheme for theactive members consist of the Adjusted Member Contributions and some pre-1992benefit components, as defined in the Fund’s Benefit Certificate. The value of MinimumRequisite Benefits in respect of the Defined Benefit Scheme active members as at30 June 2016 is $260.5 million.

If it is assumed that lifetime pension benefits and Defined Benefit Scheme deferredmember benefits are fully funded, then the value of assets available to meet theminimum benefits in respect of the Defined Benefit Scheme active members is $541.8million.

The following table sets out the coverage by these assets of the Minimum RequisiteBenefits for the Defined Benefit Scheme active members as at 30 June 2016, with thecorresponding values at 30 June 2015, 30 June 2014 and 30 June 2013 for comparison.

Coverage of Defined Benefit Scheme Activesection Members’ Minimum Requisite

Benefits

As at 30 June 2016 2015 2014 2013

MinimumRequisite Benefits

208.0% 214.3% 204.0% 188.4%

5.2.4 Coverage of benefits on Fund termination

If the Fund is terminated, the liability under the governing rules is limited to whateverassets are then held in the Fund.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 35

5.3 Valuation results in summary

The actuarial projection of possible future experience produced the following results,where projected future payments have been converted to a present value using theassumed discount rates.

ItemValue on Actuarial

Assumptions$M

Present value of future pension payments accrued atinvestigation date in respect of Health Super LifetimePension members

536.6

Present value of future defined benefit payments accrued atinvestigation date in respect of Health Super Defined BenefitScheme deferred members

71.8

Present value of future defined benefit payments accrued atinvestigation date in respect of Health Super Defined BenefitScheme active members

461.1

Present Value of future defined benefit payments accruingafter investigation date in respect of Health Super DefinedBenefit Scheme active members

58.3

Present Value of future Fund operating costs and tax oncontributions

26.3

Total present value of future payments out of Fund 1,154.1

Value of Fund assets available to support Fund liabilities at30 June 2016 1,150.2

Present Value of future Institutional contributionsat recommended rates 62.0

Present Value of future member contributions(at rates specified in the Trust Deed) 36.2

Total available assets (in absence of othercontributions) 1,248.4

Excess/(Deficiency) of assets to value of future payments 94.3

This result demonstrates that based on the assumptions adopted for this investigationthe recommended Institution contribution rates are higher than the long term ratesrequired to finance the defined benefit entitlements. However, these higher contributionrates are appropriate because the coverage of Vested Benefits by assets is currentlybelow the financing objective adopted for this investigation and it is also prudent toprovide some security against adverse experience.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 36

6

ContributionsThe actuarial process includes projections of possible future Fund experience based onrelevant actuarial assumptions. These projections allow for investment returns,salary/wage increases, pension indexation rates, crediting rates, rates at which memberscease service for different reasons, and various other factors affecting the experience ofthe Fund. It is not expected that these assumptions will be precisely borne out inpractice, but rather that in combination they will produce a model of possible futureexperience that is considered a suitable basis for setting contribution rates.

6.1 Financing objectiveThe financing objective we have adopted for this investigation is to target and thenmaintain assets at least equal to 110% of the Fund’s total Vested Benefits.

Most of the Fund’s liabilities (defined benefit and lifetime pension) are not linked to thereturns on the underlying assets. A margin in excess of 100% coverage of the Fund’sVested Benefits is therefore desirable to provide some security against adverseexperience such as poor investment returns. We consider that the target margin of110% strikes a suitable balance between the Trustee’s desire to provide security tomembers and the Institutions’ desire to avoid an unnecessary build-up of surplus.

Based on the assumptions adopted for this investigation, achieving the financingobjective of 110% of the Fund’s Vested Benefits would also result in at least 110%coverage of the Actuarial Value of Accrued Benefits and SG Minimum Benefits. Hence itis not considered necessary to adopt specific financing objectives in relation to thesebenefit liability measures.

6.1.1 Provisions of the Trust Deed

The rules of the Fund’s Trust Deed include requirements that:

§ the Trustee must “take any action in order to comply with superannuation law” (Rule1.A.21.4(a)) which includes ensuring an actuarial investigation of the Fund isconducted when required by legislation. Accordingly actuarial investigations arecarried out annually; and

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 37

§ participating Institutions “contribute to the Fund at any particular time the amount orrate of contributions determined by the Trustee after obtaining the advice of theactuary” (Rule 3.B.7.1).

6.1.2 Professional standards

This report satisfies the requirements of Professional Standard 400 of the Institute ofActuaries of Australia relating to the investigation of the financial position of definedbenefit superannuation funds. It also meets the requirements of SIS Reg 9.29A for anannual actuarial investigation.

Under Professional Standard 400 issued by the Institute of Actuaries of Australia, theFunding method selected by the actuary should “… generally aim to ensure that, to theextent possible:

(a) members' benefit entitlements (including any pension increases provided by theTrust Deed or in accordance with either precedent or the intentions of the Trusteeand/or Fund Sponsor) are fully funded before the members retire; and

(b) the assets of the Fund from time to time, after making full provision for theentitlements of any beneficiaries or members who have ceased to be employed,exceed the aggregate of benefits which employed members would reasonably expectto be payable to them on termination of membership, including the expenses ofpaying those benefits, and having regard to the provisions of the Trust Deed and thelikely exercise of any Options or Discretions.” (Paragraph 5.5.4 of PS400).

Accordingly the actuary needs to be satisfied that any funding program is expected toprovide a level of assets which meets or exceeds immediate benefit entitlements basedon members’ reasonable expectations. Should assets fall below that level, the fundingprogram needs to aim to lift assets to at least the required level over a reasonable timeperiod and to maintain assets at or above the required level thereafter.

The financing objective has been set on the basis that members’ reasonableexpectations on termination would be to receive their Vested Benefit entitlementincluding the lump sum value of any pension entitlements, on the actuarial assumptionsadopted for this investigation.

6.2 Financing the benefits

6.2.1 Ultimate cost of providing Fund benefits

The ultimate cost to the Institutions of providing Fund benefits is:

§ the amount of benefits paid out; plus§ the expenses of running the Fund, including tax;

less

§ members’ contributions; and§ the return on investments.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 38

The ultimate cost to each Institution will not depend on the actuarial investigationassumptions or methods used to determine the recommended Institution contributionrates, but on the actual experience of the Fund. The financing method and actuarialassumptions adopted will however affect the timing of the cost to the Institutions.

6.2.2 Financing method

There are various financing methods that could be followed when determining Institutioncontributions. This investigation uses the “Target Funding” method, which was also usedat the previous investigation.

Under this method, the Institution contribution rates required to provide a target level ofcoverage of a particular benefit liability measure is determined. The Fund’s targetfinancing objective is detailed in Section 1.3 of this report.

Over time, the level of contributions may vary significantly and will depend on the Fund’sactual experience relative to that expected. If actual experience differs significantly fromthat expected, the level of Institution contributions may need to be adjusted to ensure theFund remains on course towards its financing target.

We consider that the Target Funding method is suitable in the Fund’s currentcircumstances as it allows the recommended contribution rate to be determinedspecifically to meet the Fund’s financing objective.

6.3 Long term contributions

Based on the assumptions adopted for this investigation we have calculated thefollowing long term contribution rates for the active members of the Defined BenefitScheme:

Member Contribution Rate (% of Salary) 0% 3% 4% 6%Institution Contribution Rate (% of Salary) 1.1% 1.1% 1.4% 5.4%

6.4 Current contributions

The Institutions that participate in the Fund are currently contributing at the followingrates for the Defined Benefit Scheme active members:

Member contribution rate (% of Salary) 0% 3% 4% 6%Institution contribution rate (% of Salary) 1% 6% 6% 10%

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 39

6.5 Recommended level of contributions

We recommend that the Institutions continue to contribute to the Fund at the followingrates for the Defined Benefit Scheme active section members:

MemberContribution Rate

(% of Salary)0% 3% 4% 6%

InstitutionContribution Rate

(% of Salary)1% 6% 6% 10%

The Fund’s Vested Benefits coverage is currently below the target coverage level of110%. A reduction in the recommended Institution contribution level could be consideredonce this target is reached, expected to be around 30 June 2019 based on theassumptions adopted for this investigation.

Over the long term we would expect the Institution contribution rates to reduce towardsthe long term contribution rates (refer to Section 6.3). Whilst it may be theoreticallypossible to reduce the recommended rates to the long term contribution ratesimmediately once the 110% target coverage level is reached, it may be more appropriateto consider a staggered reduction towards these rates pending the emergence of futureexperience.

The “low return” scenario projections in Section 7.3 show that even if investmentexperience is adverse the recommended contribution rates will maintain coverage ofVested Benefits of at least 99% over the next three years.

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 40

7

Projections7.1 Target coverage

The financing objective of the Fund is to target and maintain assets at least equal to110% of the Fund’s total Vested Benefits.

7.2 Projected coverage of benefits

The graph below shows the effect on the financial position of the Fund for variousInstitutional contribution options from 1 July 2017 if the Fund experience is as assumedfor this investigation.

We have considered the following three contribution options regarding Institutionalcontribution rates. For the period 1 July 2016 to 30 June 2017 each contribution optionincludes contribution rates of:

Member Contribution Rate (% of Salary) 0% 3% 4% 6%Institution Contribution Rate (% of Salary) 1% 6% 6% 10%

The assumed contribution rates from 1 July 2017 onwards for each option are outlined inthe table below:

Percentage of SalaryMember Contribution Rate 0% 3% 4% 6%Option A – current contribution rates 1% 6% 6% 10%Option B – reduction in current contribution rates 1.1% 3% 3% 8%Option C – contribution at long term normal costs 1.1% 1.1% 1.4% 5.4%

Actuarial Investigation as at 30 June 2016 Health Super DB Fund

MERCER 41