health economics by jamie wagner, ph.d candidate and jennifer davidson, m.ed

TRANSCRIPT

Health Economics

ByJamie Wagner, Ph.D Candidate

andJennifer Davidson, M.Ed.

U.S. Health Care Spending

Year Total Spending (In Billions)

Spending as a Percent of GDP

Spending Per Capita

1960 $27.4 5.0 $147 1970 74.9 7.0 356 1980 255.8 9.0 1110 1990 724.3 12.1 2855 2000 1377.2 13.4 4878 2005 2035.4 15.5 6889 2008 2411.7 16.4 7936 2009 2504.2 17.4 8170 2010 2599 17.4 8411 2011 2692.8 17.3 8658 2012 2793.4 17.2 8915 2014 3093 18.3 9697 2015 3273 18.4 10172 2020 4416 19.2 13142

Source: http://cms.hhs.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/index.html (retrieved: March 24, 2014)

Why are we spending so much?

• Aaron (1991)• Expansion of 3rd party payment system (Insurance)• Increased use of medical technology

• New technology increases costs

• Aging of the population• Expanded medical malpractice

• Other factors• Physician-induced demand• Unhealthy lifestyles• Ethical considerations—we are dealing with human life

Health System Goals

• Access to care—Is medical care a “right”?• Who’s covered?• What’s covered? What is basic medical/health care?

• Quality of Care• Medical efficacy• Medical outcomes

• Costs of care• Who pays? Individual spending their own money vs.

spending someone else’s money• How much does it cost?

Making Decisions is Tough!

• On your own fill out the Federal Budget Exercise• You have $1000,000,000 for new domestic programs—

rank the 8 programs from the highest priority (#1) to lowest priority (#8)

• In groups of 3-4 repeat the process (you may only have one list per group

What is an opportunity cost?

What is Obamacare?

• Affordable Care Act signed by President Obama on March 23, 2010 (10 yr process to expand health insurance coverage)• Two primary mechanisms to increase health

insurance coverage• Expanding Medicaid• Creation of the State Exchanges

• ACA sets standards for qualified health plans

What is Obamacare? Cont.

• A few changes to insurance:• Coverage for Pre-existing Conditions• Adults under 26 covered under parent’s insurance• Preventative care at no additional cost to you• No more lifetime limits on coverage• Insurance can no longer end your coverage for a mistake

you made

• Goal: Make Insurance Affordable for All

Health Care Mandate• Passed by the US Supreme Court June 2012 (5-4

vote)• Americans must pay for insurance or pay a penalty

(Assessed on tax return and administered by IRS)• Some Americans are exempt from this mandate (Poor,

old, those between jobs, those in jail, etc.)• Firms with 50 full-time employees will have to pay a

penalty of $2000/employee if they do not provide coverage• Feb. 14 extension:

• Medium firms (50-99 workers) given until 2016 (extended from 2015 in July 2, 2013 extension) to comply

• Large firms (100+ workers) beginning in 2015 have to offer coverage to 70% (down from 95%) of full-time workers

Who is paying for all of this?

• A few prominent taxes to help pay for everyone who was previously uninsured• .9% increase in Medicare payroll tax for individuals

making more than $200k or couples making more than $250k• 2.9% excise tax applied to everything sold by medical

device manufacturers• 10% tax on indoor tanning

State Exchanges • States required to establish health insurance

exchanges by January 2014• Required to be a state agency or non-profit entity• Exchanges must provide standardized info on all

insurance options including benefits, premiums, and subsidies so people can compare benefits.

State Exchanges cont.• States needed to decide by the end of 2012

whether they were going to set up:• Federal Exchange (default)• State-Based Exchange• Partnership Exchange

• How are the exchanges supposed to reduce costs?• Increase insurance competition• Increase risk pools

Do you know what your state chose???

Yellow/gold—federal exchange (default)Dark blue—state exchangeLight blue—partner exchange (state and federal)

State Exchanges Today cont.

• State-based exchanges are likely to shut down…• Massachusetts needs to start over with new software

used in other states• Maryland has to shift to a different IT system because of

a massive crash around launch day• Oregon cannot produce a website where insurance

seekers can sign up—Federal government may be taking over Oregon

Health Care Market

What does the demand curve represent?

Willingness and Ability to Pay for

Health Care

If there’s a shortage, how do we decide who

will get treatment?

P

Q

S

D

Health Care

P*

Q*

Pc

PcShortage

Shortage

Who get’s a Kidney?• Assume that all suffer equally from urgent cases of

kidney failure and that those who do not receive a transplant will die within a year• Criteria you may use to decide: 1) a person’s merit

2) their contribution to society (past and present) 3) their ability to pay 4) their need 5)their age• Work in groups of 2-4 and decide who

gets the kidney and why

If you gave the kidney to…

Dr. M., he died of a massive coronary two years after receiving the kidney.

Bonnie T., she went on to medical school and became and obstetrician.

Fred S., he quit medical school and divorced his wife.

Agnes M., she won the state lottery and became and instant millionaire.

Ellen R., she became a lawyer, working to defend the poor.

How can we decrease the price of health

care?• Can we decrease the price of health care in a way

that will not cause a shortage—i.e. without setting a regulated price (price ceiling)?

P

Q

S

D

P*

Q*

Decrease Demand

Increase Supply

D’

P’

Q’ Q’

S’

P’

Are there any consequences???

Market Failure• Departure from perfect competition• Market failure is rampant in health care—the

government must step in • Is health care a right?• How much intervention is the right amount?

• Medical care delivery is inefficient—why?• Malpractice lawsuits

• Financing care for the poor is a major issue—what is the optimal tax to fund this or should we fund this at all?

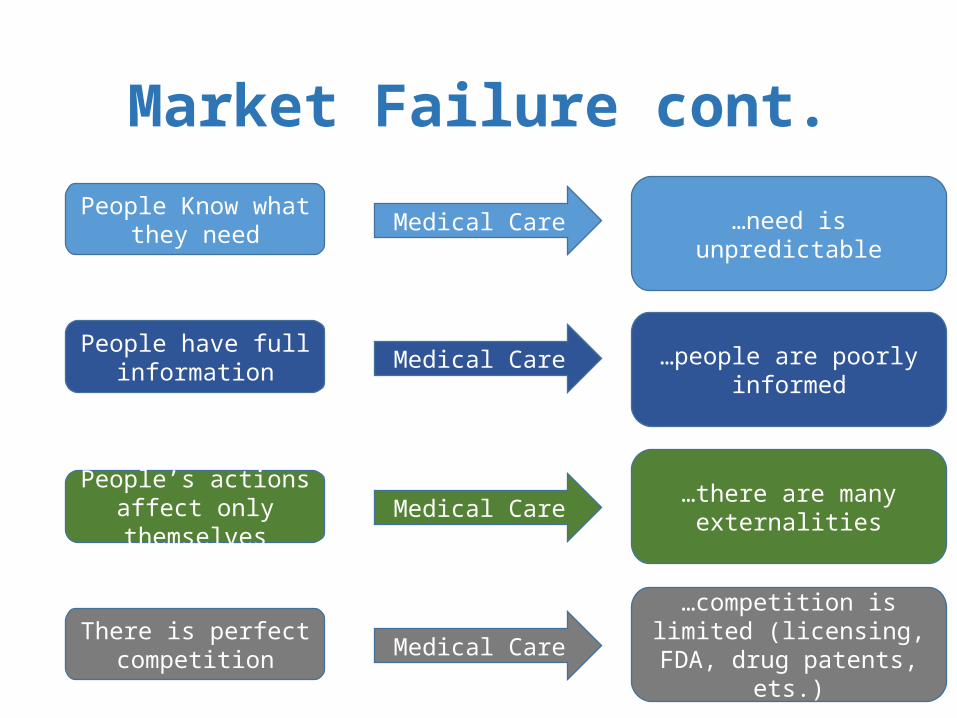

Market Failure cont.

People Know what they need

People have full information

People’s actions affect only themselves

There is perfect competition

Medical Care

Medical Care

Medical Care

Medical Care

…need is unpredictable

…people are poorly informed

…there are many externalities

…competition is limited (licensing, FDA, drug patents,

ets.)

Adverse Selection in Health Insurance

MarketsOriginally created by Ashely Hodgson (JEE, Vol. 45, No.2, Apr-June

2014)

Adapted by Jennifer Davidson, M.Ed.and Jamie Wagner, Ph.D. Candidate

Your role – 30 people in our risk group

• Our risk pool• Most people fall into the healthy category; • the top 5 percent of patients in the US spend 50% of

health care dollars (Kaiser Family Foundation Estimate, 2012)

• Your role provided to you• Age• Any medical issues you have• Probability of a minor incident costing $8,000• Probability of a major incident costing $200,000

Budgeting

• Once assigned character construct your budget• Based on average salary

• Median income for a single adult in the US was $30,880 in 2012 (US Census)• Adjusting for taxes translates into roughly $2,345 per month

• Must include• Housing• Transportation• Food• Utilities• Healthcare• Clothing• Entertainment

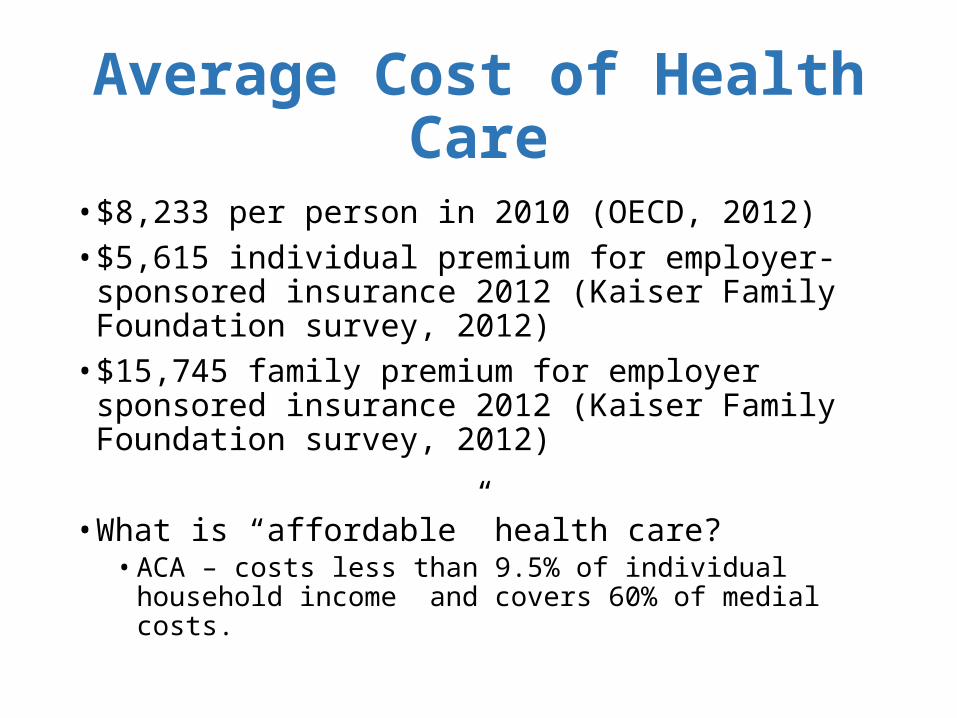

Average Cost of Health Care

• $8,233 per person in 2010 (OECD, 2012)• $5,615 individual premium for employer-sponsored

insurance 2012 (Kaiser Family Foundation survey, 2012)• $15,745 family premium for employer sponsored

insurance 2012 (Kaiser Family Foundation survey, 2012)

• What is “affordable” health care?• ACA – costs less than 9.5% of individual household income

and covers 60% of medial costs.

Health Insurance Decision

• Self select, depending on your health status, into Gold, Silver, or Bronze

• Gold• No copayment required/no deductible required

• Silver• 20 percent copay/$500 deductible

• Bronze• 30 percent copay/$1000 deductible

Make Selections

Debrief

• What happened to prices and why?• Gold – increase or decrease• Silver – increase or decrease• Bronze – increase or decrease

• If we were to run it again based on the new prices for each plan, what would happen? • Almost everyone choose bronze (except maybe the

sickest)• Some healthy patients drop out?

• How high would a tax penalty have to be to stop them from dropping out?

Adverse Selection

• “Death spiral”• The presence of high-cost consumers in the market

pulls up the average cost of service, pulling up the price.• An increase in price decreases the number of low-

cost consumers who purchase insurance.• The decrease in the number of low-cost consumers

pulls up the average cost of insurance. • In the extreme case, this upward spiral continues

until all insurance customers are high-cost people.

Three-Legged Stool of the ACA

• The requirement that insurers accept all applicants, regardless of pre-existing conditions (also known as guaranteed issue)

• The mandate requiring all citizens to buy health insurance (also known as the individual mandate)

• The government subsidies assisting low-income people in buying insurance

Health Econ Wrap-up cont.

People choose. Choices are made everyday all the time!• Do I get health insurance or not?• Should I continue to smoke or quit smoking?

People’s choices involve costs.• If I did not have health insurance before and I get it now,

I avoid paying the mandated tax.• If I choose not to get insurance I pay the tax.

People respond to incentives in predictable ways.• A high enough tax will incentivize me to not buy the

health insurance. If the insurance costs more than the tax I will pay the tax.

Health Econ Wrap-upPeople create economic systems that influence

individual choices and incentives.• We have a system and the Affordable Care Act with the

interest of influencing behavior—forcing folks to buy insurance

People gain when they trade voluntarily.• What choice did people make prior to the ACA? Did

they voluntarily purchase insurance?People’s choices have consequences that lie in the

future.• There are consequences for buying insurance.• There are consequences for not buying insurance.

Thank you!!!