hd i i chihedging in china - ahk greater...

TRANSCRIPT

H d i i ChiHedging in China

Eric Ming Financial Markets

Standard Chartered Bank (China) LimitedMay 2009

ContentContent

St d d Ch t d B k I t d tiStandard Chartered Bank Introduction

FX Market Analysis

USD/CNY Historical TrendUSD/CNY ForecastUSD/CNY Hedging ToolsUSD/CNY Hedging ToolsMajor Currency against USD

USD Interest Rate – Right time to hedge?US te est ate g t t e to edge

CNY Interest Rate - Introduction

CNY Yield Enhancement Product

2

Standard Chartered BankStandard Chartered Bank

Dalian

BeijingQingdaoTianjin

NanjingSuzhouShanghai

ChengduChongqing

HangzhouNanchangNingbo

ShenzhenBranches: 15Rep Offices: 1

SCB (China)XiamenGuangzhou

Zhuhai

3

Sub-branches: 37Village Bank: 1

Standard Chartered BankStandard Chartered Bank

1858

1980s

Opened 1st branch in Shanghai

Pioneered the re-opening of branches & representative offices

1995

2004

Established China Headquarters in Shanghai

Obtained the license for Foreign Currency Derivatives

2005 Obtained the license for CNY Fixed Income Trading

Obtained the license for CNY FX Forward

2006 Obtained the license for CNY FX Swap

Launched RMB consumer banking services to PRC citizensShanghai Branch 1911

2007 One of the first 4 foreign banks become locally incorporated

First foreign bank who gets license for onshore Commodity

Branch 1911

2008

g g yDerivatives

Obtained the license for Equity Derivatives

4

Obtained premium dealership for PBOC paper and underwriting license of China Government Bond

Beijing Branch 1923

Financial Markets China AchievementsFinancial Markets China AchievementsChina Foreign Exchange Trade System (CFETS)China Foreign Exchange Trade System (CFETS)

Excellent Trading Bank AwardsExcellent Trading Bank AwardsExcellent Trading Bank AwardsExcellent Trading Bank Awards

– Excellent Member 2007 in the interbank RMB China Foreign Exchange Trade

System/National Interbank Funding Center

market– Excellent Member 2008 on the interbank FX

market

Excellent Member 2005 in the interbank RMB market

China Foreign Exchange Trade

2007

System/National Interbank Funding Center

Excllent Member 2005 in the interbank FX market

Outstanding Dealer AwardsOutstanding Dealer Awards

2008

gg

– Our fixed income trader is awarded as the “Outstanding Dealer 2008”g

– Our FX traders are awarded as the “Outstanding Dealer from” on the FX interbank market for consecutive 4 years

5

interbank market for consecutive 4 years

SCB Financial Market CapabilitySCB Financial Market Capability

Financial Markets

Exposure ManagementAsset Management

Currency Linked Deposit Rate Linked Deposit Currency Interest Rate

PCD(only FCY

Plain IRS, FRA,CNY Fixed Rate Loan

Spot, Forward, CCS(both FX&CNY)

Option Strategy: Range Forward Knockout

PPCD(o y Cnotional)

Cap, Collar, Swaption In-

Forward, Knockout Forward, Bonus Forward, etc.No Touch, Touch, Wedding

Cake, Range Accrual, etcCNY

Extendible Deposit Swaption, In

arrear Swap, Quanto, etc

Option Strips: Participating Strip, Knock Out Forward Strip, At-Expiry Knock Out Strip, etc.

Commodity Linked Deposit & Equity Linked Deposit

p

6

LIBOR Spread, Inverse Floater, Capped Floater, Multi-Callable, etc. Commodity Hedging

FX Market AnalysisFX Market Analysis

7

USD/CNY Historical GraphUSD/CNY Historical Graph

PBoC start to float the spotfloat the spot

Accelerating CNY appreciation, g pp ,1 Y NDF implied 16% annual appreciation

Where is the next?

8

USD/CNYUSD/CNY Recent 1 Year MovementRecent 1 Year Movement

9

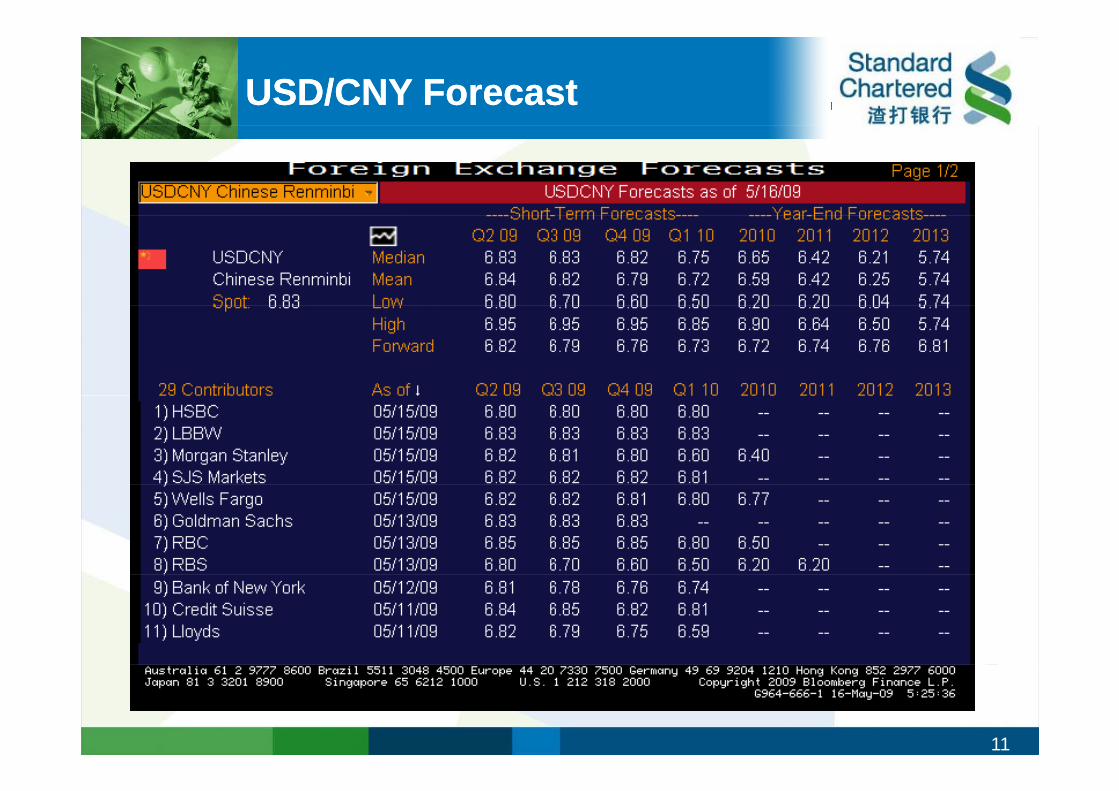

USD/CNY ForecastUSD/CNY Forecast

10

USD/CNY ForecastUSD/CNY Forecast

11

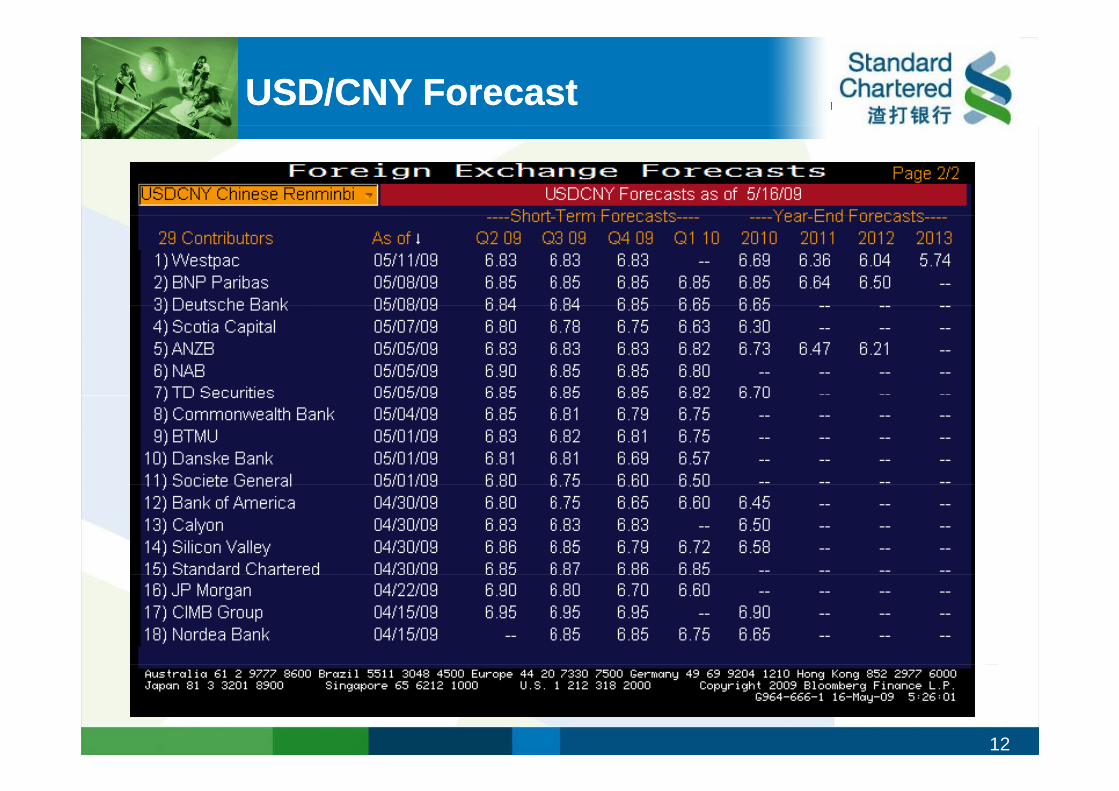

USD/CNY ForecastUSD/CNY Forecast

12

USD/CNY onshore Hedging ToolUSD/CNY onshore Hedging Tool

• Vanilla Forward

• Par Forward

• Structured Forward

13

CNY CNY VanillaVanilla ForwardForward

Forward contract characteristics:

an obligation to buy or sell a currency in the future principle amount exchange rate and settlement day will fixed on the trade dayprinciple amount,exchange rate and settlement day will fixed on the trade day

How to calculate Forward?

Forward = Spot + Swap points

Client sell USD against CNY

e g 18 May 2009 USD/CNY Spot 6 8255e.g 18 May 2009 USD/CNY Spot 6.8255 3 month Swap Point 0.00503 month Forward 6.8305

14

* For tenor between 1-3 months, notional under USD 50 mio will not affect the market liquidity

CNY Vanilla ForwardCNY Vanilla Forward

Advantages:

FX rate fixed on the trade day, disregard of the volatility of the FX marketsthe FX marketsZero cost Easy to understand and executeTenor can be adjusted (extended or early settled) based on real cash flow of the client

Risks:

On settlement day if the Forward rate is worse than theOn settlement day,if the Forward rate is worse than the Spot rate,Forward contract may not in the money

15

SCB Forward ProcedureSCB Forward Procedure

Pre-deal preparation:Pre deal preparation:

Set up Limits Open the accountsSign dealing mandate supported by Board of Resolution and FX terms and ConditionsSign dealing mandate supported by Board of Resolution and FX terms and ConditionsIf the tenor is less than 1 year, no need to sign further; if the tenor is longer than 1 year, need to sign ISDA

Trade DayTrade Day:

Over the phone,quote the FX forward rate with SCB

Settlement:

Deliver the required supporting documents to SCB which is as the same as spot transaction requiresrequiresMake sure account balance is sufficient to cater for the settlement of the forward contractDeliver the instruction to SCB,in turn SCB will effect the payment upon the instructionThe final settlement can be adjusted (early take up or extend) according to the real cash flow schedule

16

schedule.

Forward Policy EnvironmentForward Policy Environment

Business All FX d l hi h b d th h FX t h l itt d tScope All FX deals which can be done through FX spot exchange are also permitted to be traded through FX forward exchange;

According to the updated regulation, the supporting document for the hedging is only required to be submitted to the bank on the settlement date.

Documents Required

Trade Day: no supporting document is needed. Settlement Day: The requirement is as the same as documents for FX Spot

bySAFE

For USD 1 mio and above 1. IC card2 Contract and Invoice (original or copy plus company seal)2. Contract and Invoice (original or copy plus company seal)3. TT, i.e. Instruction, fax is acceptable if sign i-6

17

USD IndexUSD Index

• USD continuously depreciate starting from year 2000, until the financial crisis in 2008

• From long term perspective, USD has the depreciation pressure• One of the most Important factor to influence the index:Risk appetite

18

Major Currency Major Currency

GBP/USD EUR/USD

USD/CHF USD/XAU

19

USD Interest Rate HedgingUSD Interest Rate Hedging

20

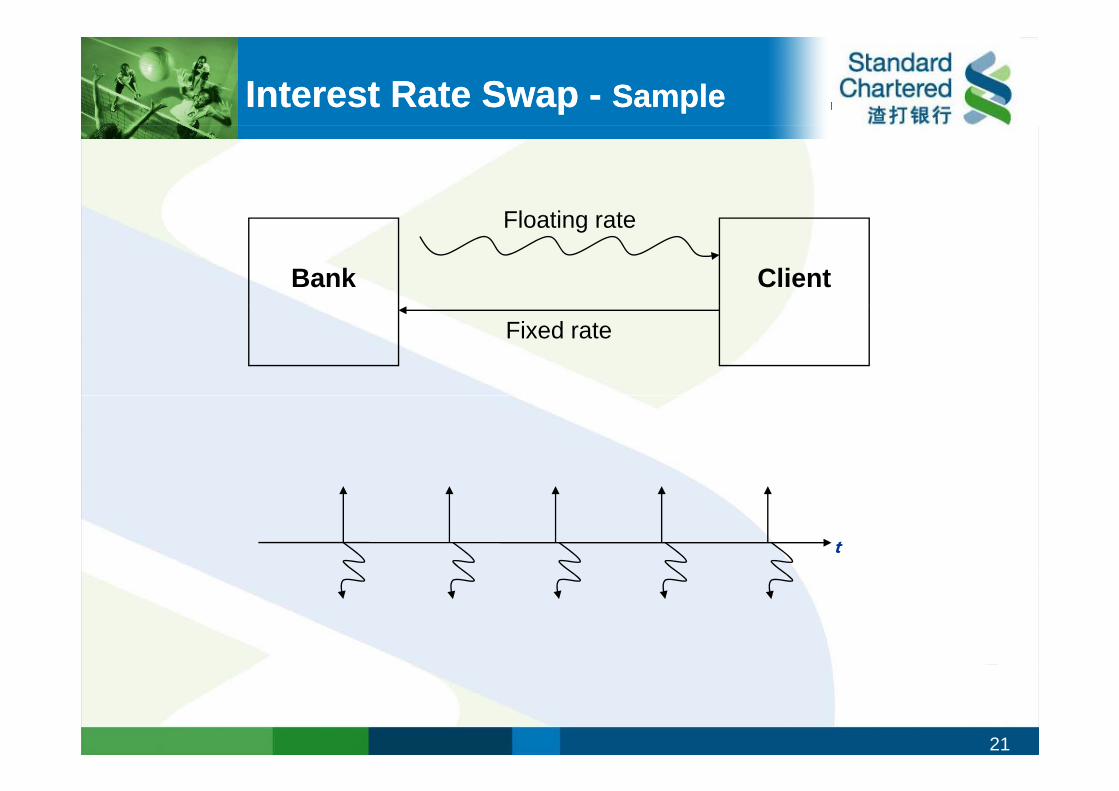

Interest Rate Swap Interest Rate Swap -- Sample Sample

Floating rateFloating rate

Bank Client

Fixed rate

t

21

USD Interest Rate OutlookUSD Interest Rate Outlook

Fed Funds Target rate was cut from 1% to currently 0.25% , as far as the rate cuts are concerned, the “game” is over. However, Fed pledged to keep the low rate for an extended period of timepQuantitative easing strategies are made official and will become the main focus for the H1 2009As part of quantitative measures, Fed is ready and willing to buy vast amount of treasury supply, which signals that the yields will stay very low for much of 2009y pp y, g y y yIn addition to the monetary easing, progress has been made in improving liquidity, as indicated by the gradual easing of LIBOR in the recent weeks

USD 1Month & 3Month & 6Month LIBOR

7.10

USD 1M LIBOR USD 3M LIBOR USD 6M LIBOR

Source: Bloomberg

4.10

5.10

6.10

1.10

2.10

3.10

22

0.10

1.10

Jan-00 Oct-00 Aug-01 Jun-02 Apr-03 Feb-04 Dec-04 Oct-05 Jul-06 May-07 Mar-08 Jan-09

USD Interest Rate USD Interest Rate --right time to hedge?right time to hedge?g gg g

10 years Government Bonds Yield vs. Swap rate

White line is USD 10 years swap ratey pOrange line is USD 10 years Bond yield

23

USD liabilityUSD liabilityRight time to hedgeRight time to hedgeRight time to hedgeRight time to hedge

3M LIBOR and v.s. 2 years Swap rate

2 years Swap rate is at historical low close to 3M LIBOR3M LIBOR

24

USD Vanilla Swap USD Vanilla Swap -- LiabilityLiability

Currency USD

Indicative Terms & Conditions Trade Rationale

USD rates are at historical low with theCurrency USDStart SpotMaturity 2 Year

USD rates are at historical low, with the fact that there is limited magnitude of rates to be cut further, it is a very good timing for the client to pay fixed rate to

Client pays

1.33%, p.a, qtly, A/360

Client 3m LIBOR, p.a, qtly,

g p yhedge its liabilitiesClient will lock in the 2 years rate at 1.33%

receivesp q y

A/3603m LIBOR 0.785% Risks:

client will have a negative carry of 54.5bps (from today’s Libor fixing of 0.785%)

25

0.785%)

Note: Indicative pricing as of 15 May 2009

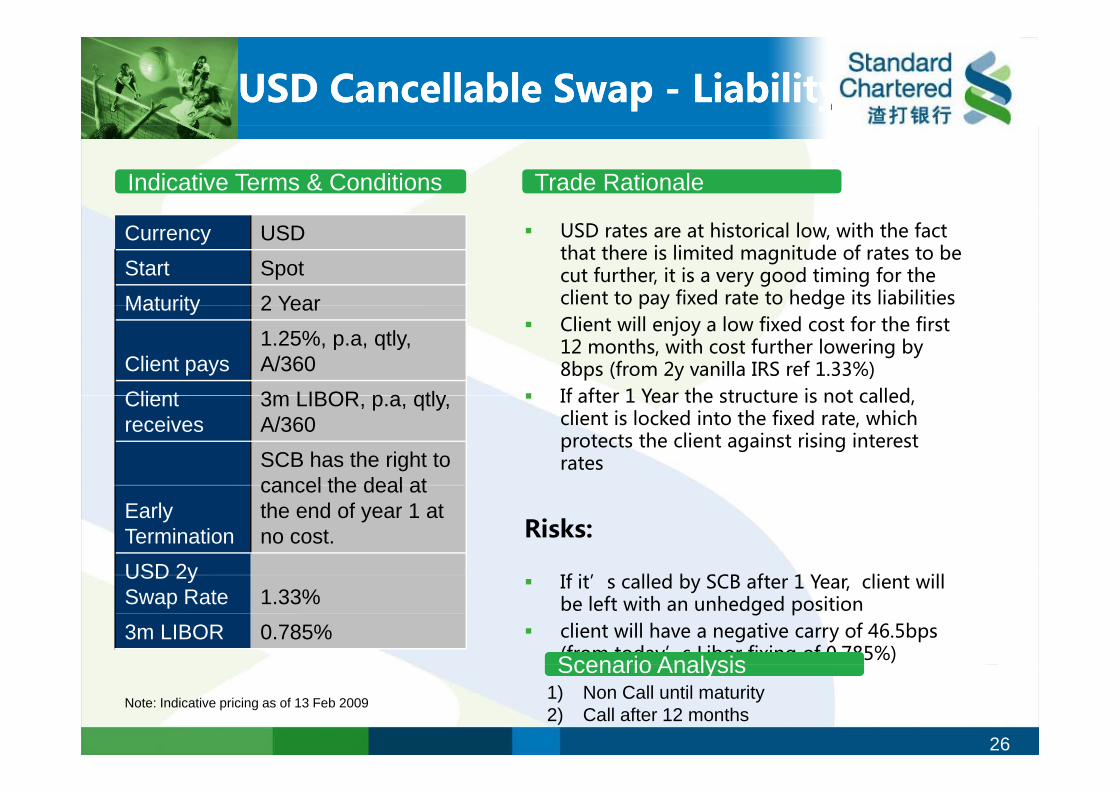

USD Cancellable Swap USD Cancellable Swap -- LiabilityLiability

Indicative Terms & Conditions Trade Rationale

Currency USDStart SpotMaturity 2 Year

USD rates are at historical low, with the fact that there is limited magnitude of rates to be cut further, it is a very good timing for the client to pay fixed rate to hedge its liabilitiesMaturity 2 Year

Client pays1.25%, p.a, qtly, A/360

Client 3m LIBOR p a qtly

p y gClient will enjoy a low fixed cost for the first 12 months, with cost further lowering by 8bps (from 2y vanilla IRS ref 1.33%)If after 1 Year the structure is not calledClient

receives3m LIBOR, p.a, qtly, A/360SCB has the right to cancel the deal at

If after 1 Year the structure is not called, client is locked into the fixed rate, which protects the client against rising interest rates

EarlyTermination

cancel the deal at the end of year 1 at no cost.

USD 2y

Risks:

If i ’ ll d b SCB f 1 Y li illUSD 2y Swap Rate 1.33%3m LIBOR 0.785%

If it’s called by SCB after 1 Year, client will be left with an unhedged positionclient will have a negative carry of 46.5bps (from today’s Libor fixing of 0.785%)Scenario Analysis

26

Scenario Analysis1) Non Call until maturity2) Call after 12 months

Note: Indicative pricing as of 13 Feb 2009

CNY Interest Rate hedgingCNY Interest Rate hedging

27

CNY Interest Rate Swap CNY Interest Rate Swap

• SCB has both Onshore and Offshore franchise

O h IRS k t t t d i 2006 d SCB Chi• Onshore IRS market started in 2006, and SCB China was one of the four market makers. In Q1 2009, SCB China’s trading volume is 170bn RMB while the whole market is 800bn RMB

• In offshore IRS market, SCB is one of the top 5 banks

• CNY IRS is actively traded between inter-bank members

28

Index GraphsIndex Graphs

29

Market Reference IndexMarket Reference Index

• 7 day repo: It is the short term interbank funding rate Banks which borrow7 day repo: It is the short term interbank funding rate. Banks which borrow money put securities (normally government bonds) into banks which lend money as collaterals. 7 day repo rate is one of the most important market interest rates in china, which effectively reflects market liquidity and cost of f difunding.

• Shibor 3M: Most people may be more familiar 3M Libor, 3M Hibor, etc. PB C i k t d l Shib R t t b th b h k t d it iPBoC is keen to develop Shibor Rates to be the benchmark rates, and it is also viewed as a steppingstone to accomplish the marketization of interest rate market.

• Shibor OIS (overnight index swap) : Like 7 day repo, o/n rate is one day interbank funding cost, but it is without collaterals.

• 1Y Depo: 1 Year PBoC deposit rate

30

CNY Interest Rate SwapCNY Interest Rate Swap

• SCB is one of the 63 China onshore IRS trading banks

• Four indexes – onshore total trading volume since 1 Jan 2008 is over CNY 417 Bn; the most liquid one is the 7day repo IRS; q y p

Index CNY Bn

7 day repo IRS 3093M Shibor IRS 56Shib OIS 35Shibor OIS 351Y Depo IRS 17Total 417

31

CNY Interest Rate Swap CNY Interest Rate Swap --SampleSampleSample Sample

• A vanilla CNY Depo IRS

SCB receive fixed rate @ 2.50% from client for 5 years with Notional: CNY 100 000 000 00; Trade Day: 01 Feb 2009Notional: CNY 100,000,000.00; Trade Day: 01 Feb 2009

Fixed Leg Floating LegFixed Leg Floating Leg

Client Pays Client receives

Notional: CNY 100 mio Notional: CNY 100 mio

Tenor: 5 years, annual fixing, Tenor: 5 years, annual fixing, Act/365 Act/365Fixed rate 2.50% Floating rate: PBoC 1y Deposit

rate (current 2.25%)

32

( )

CNY Interest Rate Swap CNY Interest Rate Swap --SampleSample

• Liability side hedging i.e. corporate clients

Sample Sample

1Y PBoC Depo

Bank Client

Fixed rate 2.50%

1Y PBoC

Loan Bank

1Y PBoC Lending

Loan Bank

Client Total Payoff = 2.5% + ( 1Y PBoC Lending – 1Y PBoC Depo )y ( g p )

Given most times PBoC will do symmetry rates hike or cut for Lending and Depo, the spread between them is very stable. This means Client almost locked up its funding cost

33

funding cost.

CNY liability Cost ReductionCNY liability Cost Reduction-- CNY Quanto ProductsCNY Quanto ProductsQQ

• Underlying currency of the swap : CNY

• In the swap formula, the reference index used is in another currency ye.g. USD LIBOR, HKD 5Y CMS etc

• Settlement currency is still in CNY

34

CNY Structured DepositCNY Structured Deposit

35

CNY Structured DepositCNY Structured Deposit

PBoC rate

Tenor Interest (p.a.)Current 0.36%Current 0.36%

1 Day Call 0.81%

7 Day Call 1.35%

Agreed 1.17%Agreed 1.17%

3 Months 1.71%

6 Months 1.98%

1 Year 2 25%

36

1 Year 2.25%

Looking for Higher ReturnLooking for Higher Return

Time Deposit InterestEnhanced Interest

VSPrincipal Principal

VS.

CNY Time Deposit CNY Structured Deposit

Return from structured deposit > = < Time deposit interest

37

3 months LIBOR Historical Graph3 months LIBOR Historical Graph

3 months LIBOR

38

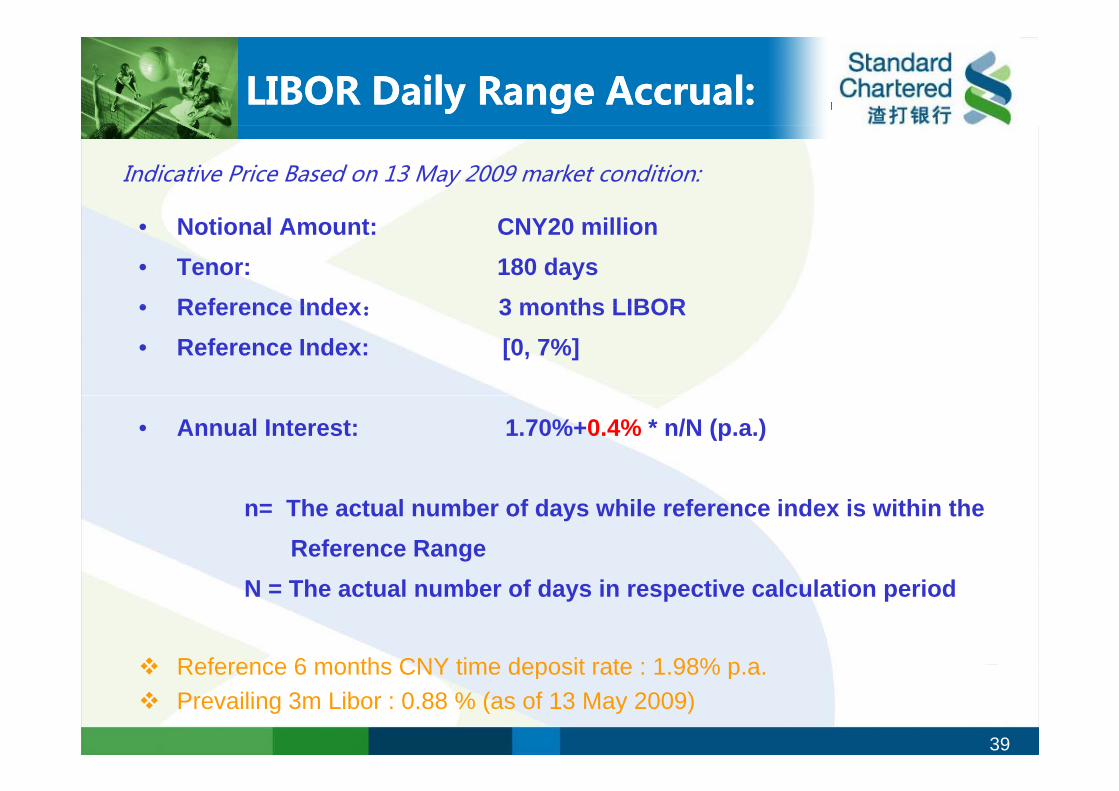

LIBORLIBOR Daily Range Accrual:Daily Range Accrual:

Indicative Price Based on 13 May 2009 market condition:

• Notional Amount: CNY20 million• Tenor: 180 days• Reference Index 3 months LIBOR• Reference Index: 3 months LIBOR• Reference Index: [0, 7%]

• Annual Interest: 1.70%+0.4% * n/N (p.a.)

n= The actual number of days while reference index is within the Reference Range

N = The actual number of days in respective calculation period

Reference 6 months CNY time deposit rate : 1 98% p a

39

Reference 6 months CNY time deposit rate : 1.98% p.a.Prevailing 3m Libor : 0.88 % (as of 13 May 2009)

LIBORLIBOR Daily Range Accrual:Daily Range Accrual:

Indicative Price Based on 13 May 2009 market condition:

• Notional Amount: CNY20 million• Tenor: 365 days• Reference Index 3 months LIBOR• Reference Index: 3 months LIBOR• Reference Index: [0, 8%]

• Annual Interest: 2.25%+0.05% * n/N (p.a.)

n= The actual number of days while reference index is within the Reference Range

N = The actual number of days in respective calculation period

Reference 12 months CNY time deposit rate: 2 25% p a

40

Reference 12 months CNY time deposit rate: 2.25% p.a.Prevailing 3m Libor : 0.88 % (as of 13 May 2009)

CNY Structured Deposit SummaryCNY Structured Deposit Summary

Indicative Price

CNY Structured Deposit Linked to 3 month LIBOR Rangep g

1 Week 2-3 Weeks 1 month 3 months 6 months 12 months

Tenor 7 Days 14/21 Days 30 Days 90 Days 180 Days 365 Days

Interest 1.70% 1.80% 1.90% 2.00% 2.10% 2.30%

41

Extendible Structured Deposit

• Yield Enhancement Offer investors the opportunity to enjoy an• Yield Enhancement - Offer investors the opportunity to enjoy an enhanced yield in initial interest period as compared with traditional CNY term deposit;

• Protection against Rates Cut - Offer investors the one-time option, not obligation, to extend the deposits at guaranteed interests rate in

d t i d t dibl i t t i d t t t i tpredetermined extendible interest period to protect against potential PBOC rates cut;

• Tenor Flexible - from 1 month and as long as total of initial and extendible interest periods within 6 months

• No FX exposure - Denomination of principal and interest payments both remain in CNY

42

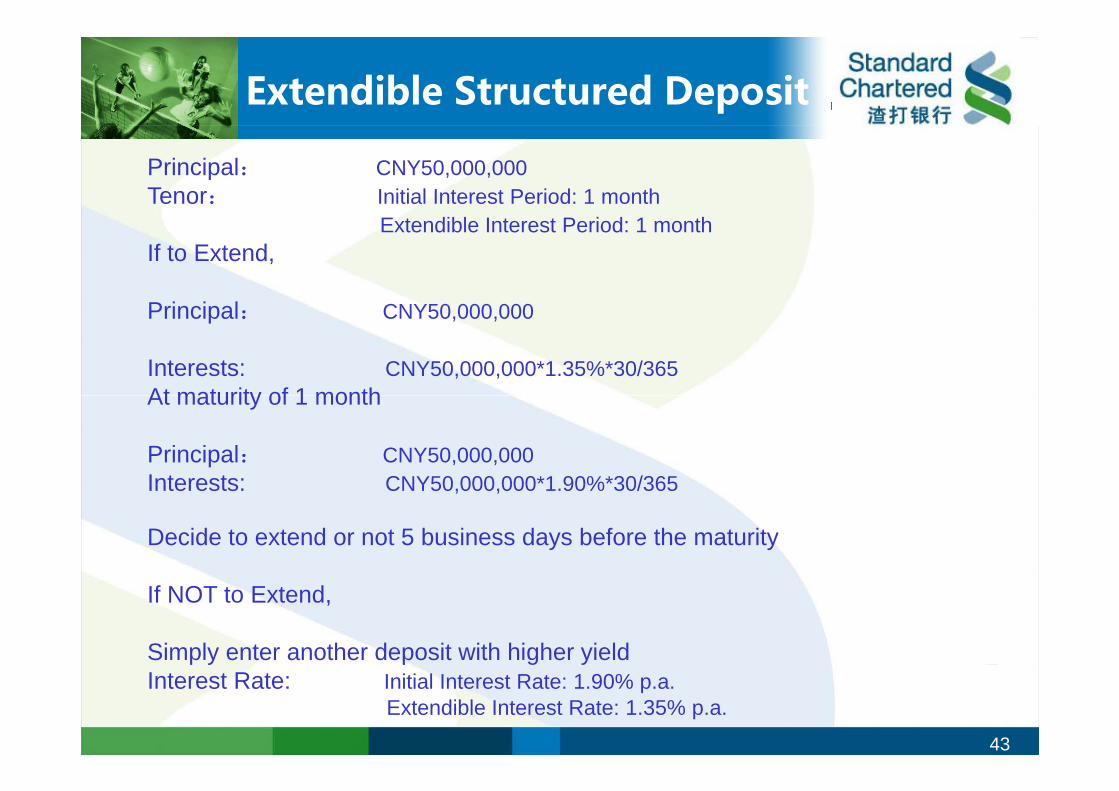

Extendible Structured Deposit

Principal: CNY50,000,000Tenor: Initial Interest Period: 1 month

Extendible Interest Period: 1 monthIf to Extend,

P i i l CNY50 000 000Principal: CNY50,000,000

Interests: CNY50,000,000*1.35%*30/365At maturity of 1 monthAt maturity of 1 month

Principal: CNY50,000,000Interests: CNY50 000 000*1 90%*30/365Interests: CNY50,000,000 1.90% 30/365

Decide to extend or not 5 business days before the maturity

If NOT to Extend,

Simply enter another deposit with higher yield

43

y g yInterest Rate: Initial Interest Rate: 1.90% p.a.

Extendible Interest Rate: 1.35% p.a.

Indicative Pricing

Tenor Initial Interest Rate Extendible Interest Rate

1+1 month 1.90% 1.35%

2+2 months 1.95% 1.35%

3+3 months 2.00% 1.71%

• Above pricing is indicative only subject to market movement. • If the extendible structured deposits can not be held till maturity, break funding cost will be charged subject to market conditions.

44

Disclaimer

This document is issued by Standard Chartered Bank (SCB) and contains indicative terms of prospective transactions. It is for discussion purposes only and does not constitute any offer, recommendation, or solicitation to any person to enter into any transaction or adopt any hedging, trading or investment strategy, nor does it constitute any prediction of likely future movements in rates or prices or any representation that any such future movements will notmovements in rates or prices or any representation that any such future movements will not exceed those shown in any illustration. The indicate terms are neither complete nor final and are subject to further discussion and negotiation. The terms of any transaction entered into will be recorded in a written confirmation or other document. SCB has no fiduciary duty towards you, and assumes no responsibility to advise on and makes no representation as to the appropriateness or possible consequences of the prospective transaction. SCB and.or a connected company, may have a position in any of the instruments or currencies mentioned in this document You are advised to make your own independent judgement with respect toin this document. You are advised to make your own independent judgement with respect to any matter contained herein. In the UK SCB conducts designated investment business only with Market Counterparties and Intermediate Customers and this document is directed only at such persons. Other persons should not rely on this document. Standard Chartered Bank is incorporated in England with limited liability by Royal Charter 1853 Reference ZC18. The principal office of the Company is situated in England at 1 Aldermandbury Square, London EC2V 7SB. Standard Chartered Bank is authorised and regulated by the FSA under FSA regulation number 114276 VAT number GB 244106593

45

regulation number 114276. VAT number GB 244106593