have we hit rock bottom? - the edge...

TRANSCRIPT

HAVE WE

PREVINDRAN SINGHE

ZERIN PROPERTIES

HIT

ROCK

BOTTOM?

“HAVE WE HIT ROCK BOTTOM?”

“YES AND NO”

LATEST HAPPENINGS

For Most Developers, Sales are Increasing or the Same as Last Year

LISTED DEVELOPERS

SALES PERFORMANCE

2015 2016 2017f

Gamuda Land Sdn Bhd RM1.2 bilRM2.1 bil

(Initial target: RM1.3bil)RM3 bil

Eco World Development Group Bhd RM3 bil (Gross) RM3.8 bil (Gross) RM4 bil (Gross)

SP Setia BerhadRM4.3 billion

(14 month period)

RM3.82 bil

(Initial target: RM3.5 bil)RM4bil

Tropicana Corp Berhad RM1.55 bil RM1.46 bil RM1.2 bil

(Unbilled sales of RM2.54 bil from 2016)

Mah Sing Group Bhd RM2.3 bilRM1.8 bil

(Initial target: RM2.3 bil)

RM1.8 bil

(To maintain or improve last years’ sales)

UEM Sunrise BhdRM2.37 bil

(Initial target: RM2 bil)

RM1.36 bil

(Initial target: RM1 bil)RM1.2 bil

IJM Land RM1.8 bil RM1.4 bilRM1.4 bil

(Unbilled sales of RM1.8 bil from 2016)

MRCB RM597 mil RM1.3 bil RM1 bil – RM1.5 bil

Sunway Property RM1.2 bil RM1.1bil RM1.1 bil

IOI Properties Group Bhd RM1.9 bil RM2.214 bil RM2.3 bil

ANALYSTS ARE POSITIVE Not One Reason But 10! Phua Chu Kang Only Had 3 Reasons….

DEALS ARE HAPPENING – OPPORTUNITES ABOUND (1)

LOCATION PROPERTY TRANSACTION

VALUE

REMARKS

OFFICE

Jalan

Munshi

Abdullah, KL

Cap Square

TowerRM511 Million

En bloc sale of the 41-storey Grade A office

building comprising a net lettable area of

601,574 sq ft and 461 parking bays,

Kuala

Lumpur

Malaysia-based

co-working

space platform

8spaces

For an undisclosed

amount. The deal is

funded through

cash and equity.

Aims to provide the ideal launchpad for

FlySpaces in Kuala Lumpur and the

surrounding region, besides incrementally

expanding its networks in the region

Jln Tun

Razak, KLDijaya Plaza RM140 Million

19-storey office building and 3,674 sq m

freehold land

KL Sentral,

KLMenara Shell RM640 Million

Disposal of Menara Shell by MRCB to MRCB-

Quill Real Estate Investment Trust (MQREIT)

Kelana

Jaya, PJ

Ascent

Tower@Paradig

m

RM347 Million

Acquisition of retail lots, a concourse level and

office space from Level 2 to Level 31 of the

32-storey building, together with 865 car park

bays by EPF

Damansara

Perdana

22 storeys of

stratified parcels

in the Iconic

Office (Block N)

within Empire

City

development

RM44.29 MillionAcquisition by MyEG Services Berhad

(MyEG)

LOCATION PROPERTY TRANSACTION VALUE REMARKS

OTHERS

Jln Tun H.S. Lee, KLHistorical building by Lee Rubber

GroupN/A

The property has a land area of 10,637 sq ft, a total built-up area of

46,607 sq ft and net lettable area of 38,126 sq ft

HOTEL

Corner of Jln Sultan

Ismail and Jln Ampang

in KL

910-room Renaissance Kuala

Lumpur HotelRM765 million

The hotel has been on the market for some time. Ventura International

is a foreign based company. This, along with the other hospitality

transactions for this year, shows confidence in the local hospitality

market and by default, the tourism industry.

KL Sentral, KL Aloft Kuala Lumpur Sentral Hotel RM418.7 million

This shows confidence in the local hospitality market. This particular

transaction is accentuated further by the fact that this was transacted

by a local firm, signalling strong belief and support from local players

in the market.

MALL

Subang Jayada : men USJ – 5 sty mall and 2

sty basement car parkRM488 Million Acquired by Pavilion REIT

DEALS ARE HAPPENING – OPPORTUNITES ABOUND (2)

• Chinese e-commerce giant Alibaba Group Holding Limited plans to set up a regional

distribution hub in Malaysia

• The hub would be sited within KLIA Aeropolis, a 24,700-acre development led by airport

operator Malaysia Airports Holdings Bhd (MAHB)

• Expected to generate more than 7 billion ringgit ($1.58 billion) worth of domestic and

foreign investments.

DEALS ARE HAPPENING – OPPORTUNITES ABOUND (3)

JULY 2016

Bank Negara

lowered Overnight

Policy Rate to 3.0

percent from 3.25

percent.

OCTOBER 2016 (Budget 2017 Announcement)

• Special step-up end-financing scheme for PR1MA houses, in

collaboration with BNM, EPF and banks

• Stamp duty exemption on instruments of transfer and loan agreement for

first-home-ownership for the period 1 January 2017 until 31 December

2018:

►Houses priced below RM300,000 – 100% exemption; and

►Houses priced from RM300,000 to RM500,000 – exemption on first

RM300,000 with balance subject to normal stamp duty rates

• Rate of stamp duty on instruments of transfer of real estate exceeding

RM1m will be increased to 4% effective 1 January 2018 (from the current

3%)

• An increment in the housing loans eligibility for the public servants,

housing for the B40 and a special scheme for the PR1MA programme

• RM200m to build 5,000 units of MyBeautiful New Home through the

NBOS for B40 at RM40,000 to RM50,000 per unit – the Government will

finance RM20,000 while the remainder will be paid in instalments by the

owners

• RM710m to build 9,850 new units and complete 11,250 People’s

Housing Programme(PPR) houses

• RM200m to build 5,000 “People’s Friendly Home” units under Syarikat

Perumahan Negara Bhd (SPNB) with a subsidy of RM20,000 per unit

and allocations for Second-Generation House infrastructure

development

NEUTRAL STANCE BY THE GOVERNMENT (1)

NEUTRAL STANCE BY THE GOVERNMENT (2)

OCTOBER 2016 (Budget 2017 Announcement)

• RM2.1b for infrastructure and socioeconomic

development in five economic corridors namely

Iskandar Malaysia, Northern Corridor Economic

Region (NCER), East Coast Economic Region

(ECER), Sabah Development Corridor (SDC) and

Sarawak Corridor of Renewable Energy (SCORE)

• RM55b (estimated) for the implementation of the new

East Coast Rail Line (600km) project connecting

KlangValley to the East Coast

• Tourism & Hospitality

►eVisa scheme for South Asian & Balkan countries

(Current: China, India, Nepal, Myanmar,

Bangladesh)

►Pioneer Status and Investment Tax Allowance

application period for new 4 and 5 star hotels

extended by two years, to 31 December 2018

►RM400m to intensify promotion and improve tourism

facilities via clean air and eco-tourism initiatives

LAWYERS JEALOUS OF ESTATE AGENTS – “I SAY MAN”

15 MARCH 2017

Property Transaction Fees Up

Revision of the fee structure in the Solicitors’

Remuneration Order by the Bar Council last year

coming to effect on 15 March 2017

2016/2017AN OVERVIEW

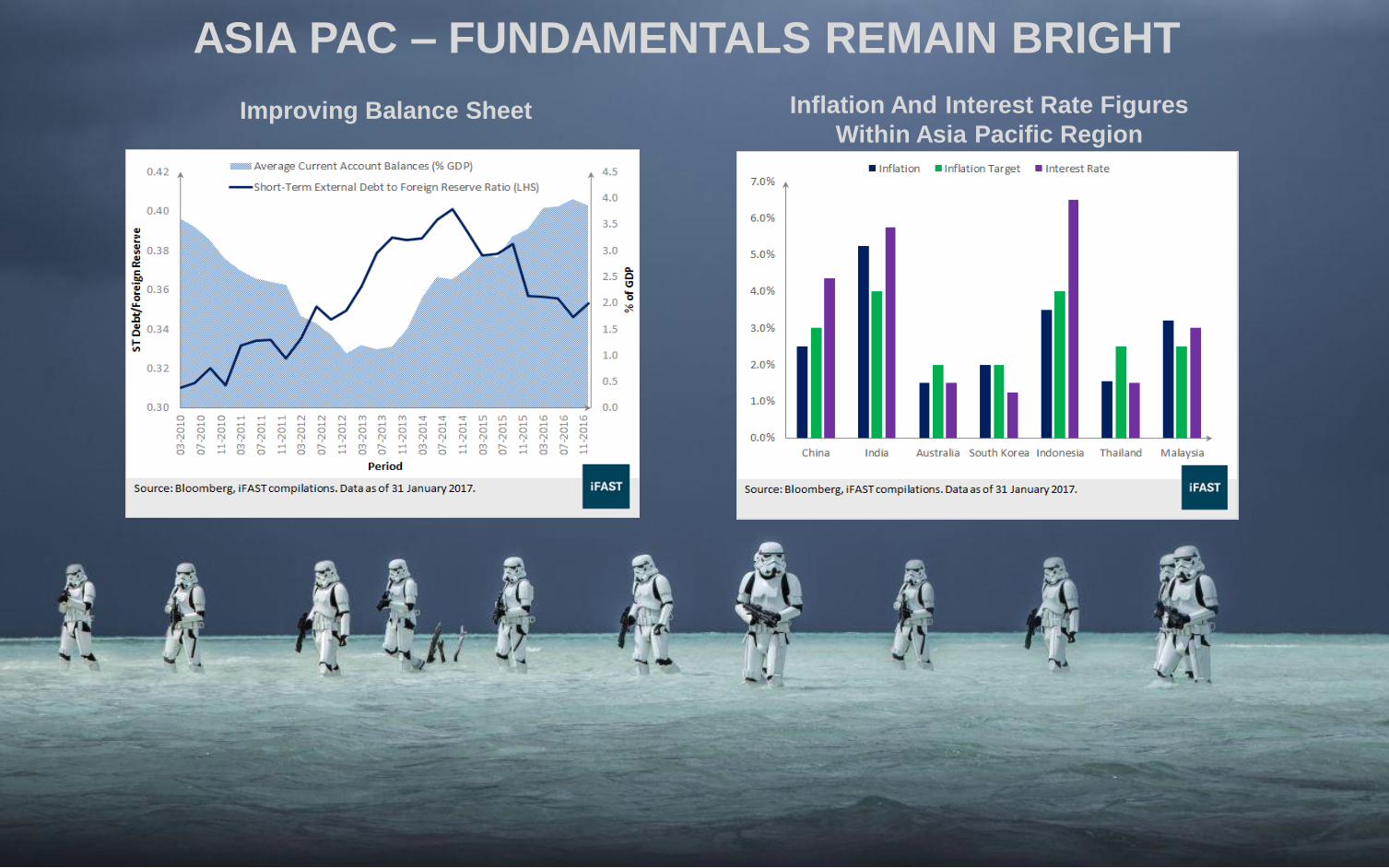

ASIA PAC – FUNDAMENTALS REMAIN BRIGHT

Inflation And Interest Rate Figures

Within Asia Pacific RegionImproving Balance Sheet

REAL GDP COMPARISON FOR SELECTED COUNTRIES

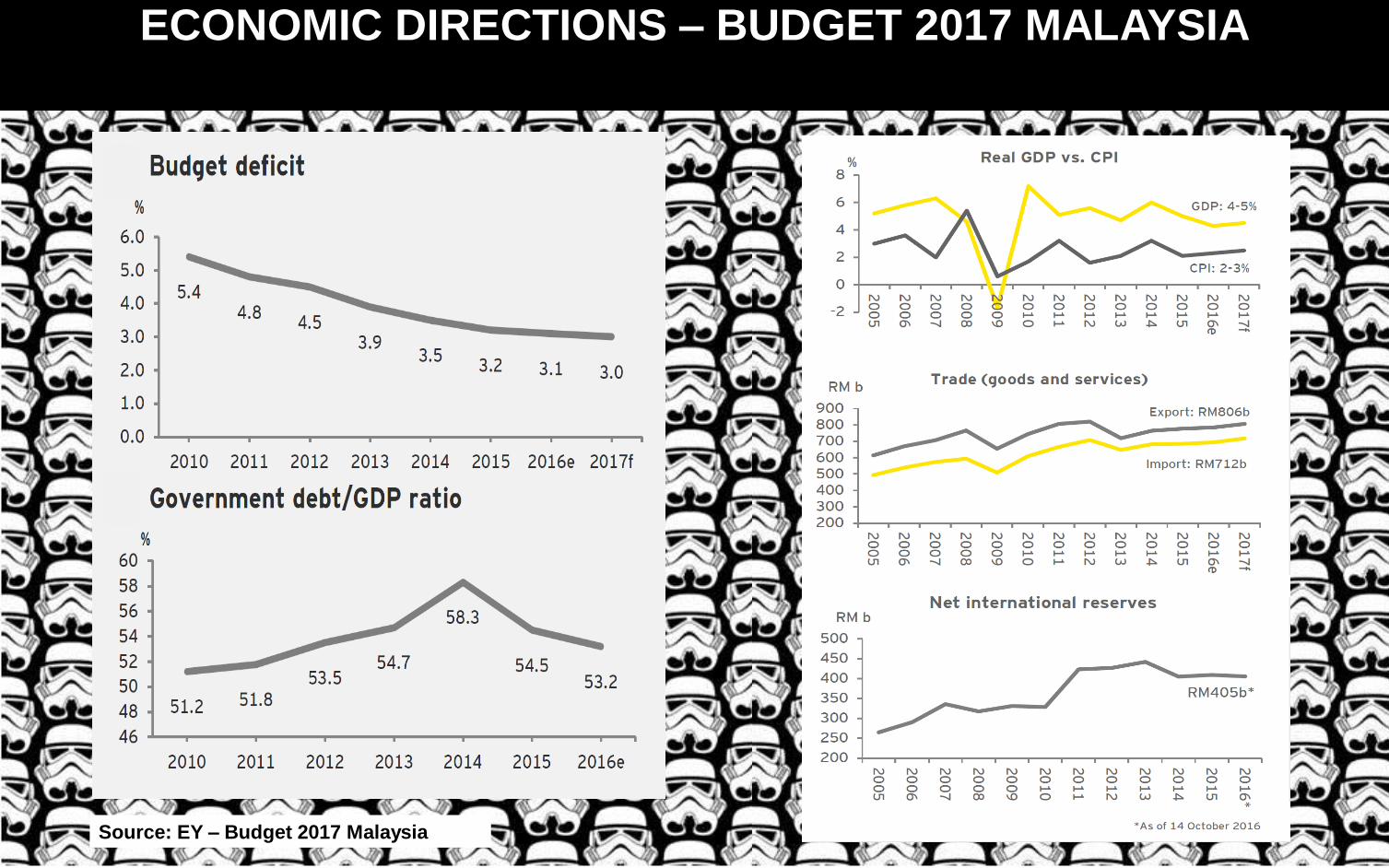

ECONOMIC DIRECTIONS – BUDGET 2017 MALAYSIA

Source: EY – Budget 2017 Malaysia

Source: EY – Budget 2017 Malaysia

ECONOMIC DIRECTIONS – BUDGET 2017 MALAYSIA

Inflation projected to increase to 4% as compared

to 2016 at 2%

UNEMPLOYMENT RATE & INFLATION RATE

Unemployment rate continues to hold steady at

3.5% since July 2016 (2015: 3.1%) despite weak

labour market conditions.

APPROVED PRIVATE INVESTMENTS IN SERVICES SECTORS, 2016 & 2015

Source: MIDA

Q1 – Q3 2016

(TRANSACTION VOLUME: 239,983 UNITS)

MALAYSIAN PROPERTY TRANSACTIONS: TRANSACTION VOLUME

Q1 – Q3 2015

(TRANSACTION VOLUME: 272,256 UNITS)

Q1 – Q3 2016

(TRANSACTION VALUE:RM95,393.75 Mil )

Q1 – Q3 2015

(TRANSACTION VALUE: RM114,085.31 Mil)

MALAYSIAN PROPERTY TRANSACTIONS: TRANSACTION VALUE

H1 2016

(TRANSACTION VOLUME: 7,455 UNITS)

KUALA LUMPUR PROPERTY TRANSACTIONS – TRANSACTION VOLUME

H1 2015

(TRANSACTION VOLUME: 9,291 UNITS)

H1 2016

(TRANSACTION VALUE: RM10,347.05 Mil)

H1 2015

(TRANSACTION VALUE: RM11,006.79 Mil)

KUALA LUMPUR PROPERTY TRANSACTIONS – TRANSACTION VALUE

THE MALAYSIAN HOUSE PRICE INDEX

Note: P – Preliminary ; a - Section 1 - 100, Mukim Kuala Lumpur & Mukim Ampang ; b - Mukim Batu, Mukim Setapak, & Mukim Ulu Klang ; c - Mukim Petaling & Mukim

Cheras

Source: The Malaysian House Index Q3 2016 report

Average Terraced House Price by District/Region

State District / Region Q3 2015 (RM) Q3P 2016 (RM) Y-O-Y%

Kuala Lumpur

KL Centrala 985,103 1,001,304 1.64%

KL Northb 521,757 553,535 6.09%

KL Southc 504,711 569,501 12.84%

Selangor

Petaling 571,219 620,013 8.54%

Kelang 268,693 291,490 8.48%

Gombak 323,730 350,892 8.39%

Hulu Langat 343,277 364,662 6.23%

Average Detached House Price by State

State Q3 2015 (RM) Q3P 2016 (RM) Y-O-Y%

Malaysia 540,968 560,987 3.70%

Kuala Lumpur 3,772,923 3,954,250 4.81%

Selangor 728,900 774,278 6.23%

Johor 368,771 386,633 4.84%

Pulau Pinang 572,508 603,174 5.36%

Negeri Sembilan 403,276 390,668 -3.13%

Perak 187,836 191,771 2.09%

Melaka 274,991 278,783 1.38%

Kedah 338,055 345,767 2.28%

Pahang 211,257 220,511 4.38%

Terengganu 280,184 292,836 4.52%

Kelantan 112,973 122,061 8.04%

Sabah 501,776 483,696 -3.60%

Sarawak 517,295 529,288 2.32%

Average High-Rise Unit Price by State

State Q3 2015 (RM) Q3P 2016 (RM) Y-O-Y%

Malaysia 300,823 320,782 6.63%

Kuala Lumpur 386,942 410,487 6.08%

Selangor 244,725 264,268 7.99%

Johor 217,116 245,888 13.25%

Pulau Pinang 314,418 335,037 6.56%

Negeri Sembilan 80,987 88,917 9.79%

Melaka 106,750 107,796 0.98%

Sabah 344,349 342,043 -0.67%

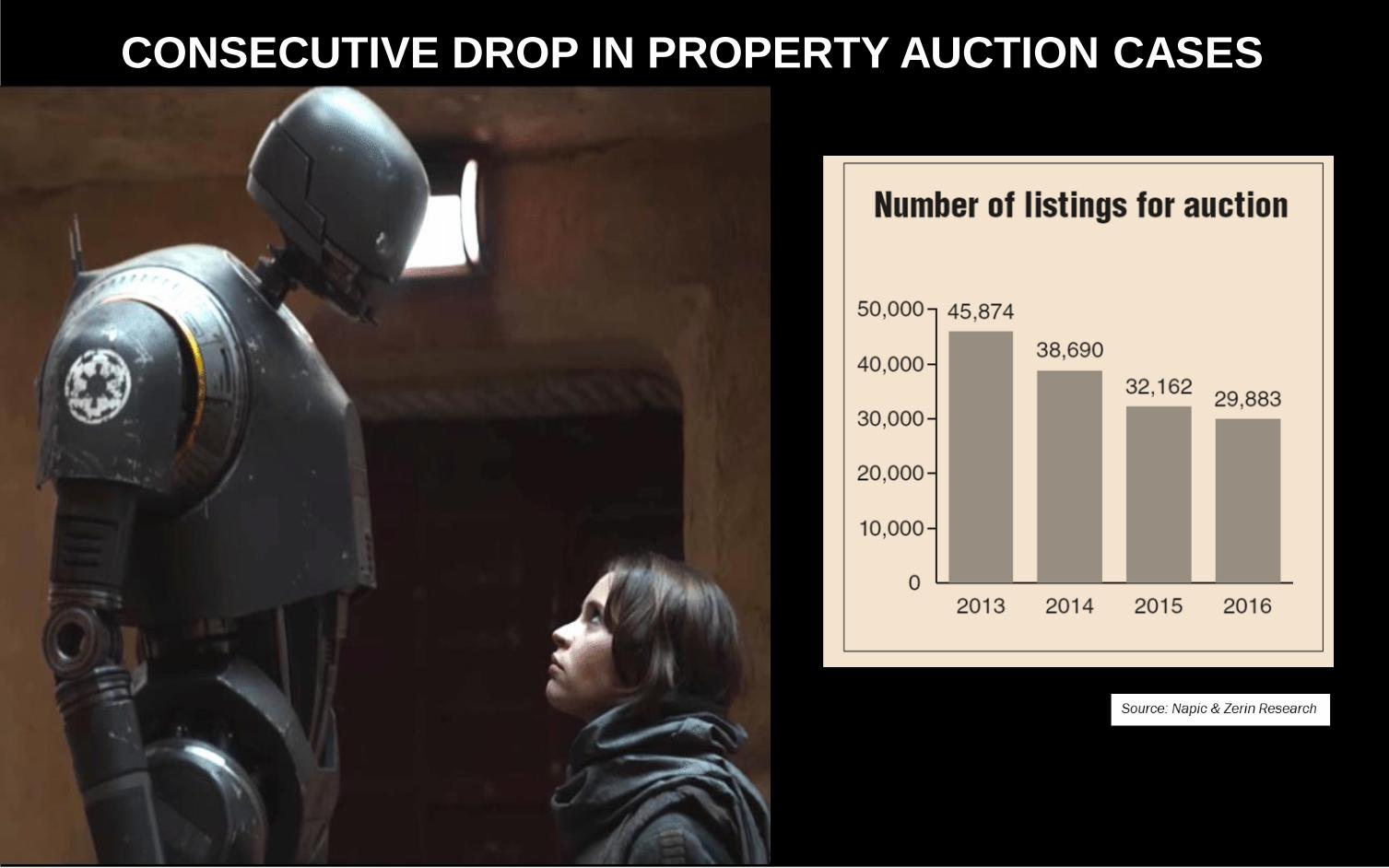

CONSECUTIVE DROP IN PROPERTY AUCTION CASES

HOUSEHOLD LOANS & HOUSING LOANS

RESIDENTIAL SUB-SECTOR OVERVIEW

PERFORMANCE OF RESIDENTIAL SUB-SECTOR IN GREATER KL

■ Continues to dominate property market

■ The average price of both landed and non-landed residential properties in Greater KL mostlyrecorded increase y-o-y

■ 2016 was marked by slower sales take-up rates and reduced number of new launches

■ 2016 saw the moving towards providing affordable housing

■ Higher demand for smaller units

■ Creative products within the affordable segment are well-received

■ Good connectivity to existing highways and railways (MRT & LRT) recorded premiums

■ Rental market stagnant growth

OFFICE SUB-SECTOR OVERVIEW

PERFORMANCE OF OFFICE SUB-SECTOR IN GREATER KL (1)

■ H1 2016 SUPPLY stands at approximately 148.65 million

■ Average occupancy at 81%, declined slightly from 81.6% recorded in the correspondingperiod last year.

■ The cumulative supply of office space for KL City is at 73.38million sq ft

■ Kuala Lumpur remained healthy in 2016 with occupancy rate just slightly below 80%

■ The Greater KL Office Market was active in 2016;

■ A number of office buildings saw completion in 2016 – Menara Hong Leong@Damansara City, Phase 1 (office space) KL Eco City, Mercu Mustapha Kamal Tower 2, Neo Damansara

■ There were several significant office leasing transactions in 2016, majority of which took place within office buildings in KL Fringe

■ Several major transactions were recorded in 2016 – Dijaya Plaza, Menara Shell, Cap Square Tower, Ascent Tower@Paradigm, Iconic Office (Block N) @ Empire City etc

■ Marketability of offices in the Decentralized Areas particularly within Damansara Heightswas enhanced due to improved connectivity

PERFORMANCE OF OFFICE SUB-SECTOR IN GREATER KL (2)

■ Liberalisation of sercives sector is creating demand

■ The rental market remained flat

■ Landlords are throwing freebies

■ Petronas Twin Towers led Kuala Lumpur and the country’s office rental market with thehighest rental at RM15psf per month

RETAIL SUB-SECTOR OVERVIEW

PERFORMANCE OF RETAIL SUB-SECTOR IN GREATER KL

■ Challenging year for retail market in 2016

■ Q3 2016, 244 shopping centres with a total supply of about 66.37 millionsquare feet

■ Occupancy of 86%.

■ 2.9 million sq ft of retail space opened in 2016

■ 7 million sq ft of retail spaces this year and 8 million sq ft beyond 2017

■ Occupancy rate slightly dropped less than 1%

■ Short term oversupply of retail space in Greater KL

■ Will impact occupancy and rent even further.

■ A number of new malls opened in 2016/2017 with less than 30%occupancy

■ Well-established shopping centres continued to record above 95%occupancy.

■ Tourists’ spending on shopping in Malaysia amounted to RM26 billion,an increase of 20.3% compared to RM21.6 billion in 2015

■ Currency exchange rate has made shopping attractive in Malaysia fortourists

HOSPITALITY SUB-SECTOR OVERVIEW

PERFORMANCE OF HOSPITALITY SUB-SECTOR IN GREATER KL

■ The total GDP contribution of Malaysian Tourism industry was a sizeable 13.5% with RM163

billion in 2016

■ Improved overall performance

■ Tourist arrivals to Malaysia for 2016 registered a hike of 4.0%

■ The country received 26.8 million tourists compared to 25.7 million tourists in 2015

■ The growth of tourism in Malaysia is matched by an increased demand. Thus, increased supplyof rooms throughout the country

■ Homestays with the ‘AirBnB model’ pose a threat to hoteliers’ market share — with 5,542registered homestays in Malaysia as at May 2016

■ Incentives and fiscal policies in Budget 2017 encourages hospitality investments in Malaysia

■ The main opportunities are in the 4 and 5 Star hotel sector but also increasingly in the lifestylehotels in the likes of Aloft and International Branded Serviced Apartments

■ Forecasting 20% increase in investment value this year

OUTLOOK 2017

OUTLOOK FOR RESIDENTIAL MARKET (1)

■ Opportunities will be on both Primary and Secondary market

■ Prices will remain largely resilient

■ Landed properties in good locations still got premium

■ Freehold terrace and semi-detached houses in gated and guarded development in goodlocations will be hot sellers

■ High-end condominium segment will continue to be flat as demand remains fairlyhealthy, albeit anticipation of significant supply to enter the market

■ High-end condominiums – smaller units will be in more demand than larger units due tobudget constraints

■ Notwithstanding, strong healthy demand for bigger units in suburbs of Bangsar andDamansara Heights

■ Affordable housing segment will remain in focus in coming years with construction ofaffordable houses by PR1MA, JPN and SPNB

■ Houses near future MRT and LRT – Hot Sellers

■ Greater KL development under ETP, future MRT and LRT lines plus new proposedhighways will keep the Residential Market vibrant and positive

■ Volume and value of transactions estimated to increase in this year

■ Newer residential developments have their own signature concepts which makes themarket more interesting and vibrant

■ Stratified residential properties have an edge in the residential market as the trendand preferences has shifted in that direction – facilities and services provided bystratified residential properties gives an advantage

OUTLOOK FOR RESIDENTIAL MARKET (2)

OUTLOOK FOR PURPOSE BUILT OFFICE MARKET (1)

■ Flat this year and improve beyond 2017

■ Rising demand from other service related industries

■ Completion of the second phase of Sungai Buloh-Kajang MRT Line by mid-2017coupled with the rapid progress of Klang Valley MRT Line 2 & Line 3 and High-SpeedRail (KL-Singapore)

■ Focus on Prime office buildings with good accessibility and connectivity (near LRT,future MRT) as well as with dual-compliant (MSC + Green)

■ The recent decline of the ringgit against major currencies has made Malaysia a valuefor money location

■ Favourable Government policies and ETP’s initiatives

■ Challenging for the old office building

■ Most of the new office spaces in KL City in 2018

■ The office segment will remain as a tenant’s market

■ Integrated developments and larger floor plates to accommodate “work smart concept”or “hot desking concept”

■ Landlords will be proactive by offering more incentives:

■ Longer rent free periods

■ More flexible airconditioning and car park allocation

■ Fitted fixtures and furnitures are preferential in tenancy agreement

OUTLOOK FOR PURPOSE BUILT OFFICE MARKET (2)

OUTLOOK FOR RETAIL MARKET

■ Forecast annual retail sales growth dropped 3.9% (RM101.6 bil) from RM97.8 bil in2016 but still growth

■ Well-established shopping centres continue to record high occupancy.

■ Less established shopping mall under pressure creating high vacancies in the market

■ Consumer spending is expected to gradually recover but not enormous enough

■ Optimistic macroeconomic indicators such as private consumption and the ringgit'sperformance does show encouraging upside potential this year.

OUTLOOK FOR HOSPITALITY MARKET

■ Malaysia Tourism Transformation Plan to attract 36 million tourists and generateRM168 billion by 2020

■ Visiting ASEAN@50 Year Campaign in conjunction with the 50th anniversary of ASEANas well as 2017 SEA and Para ASEAN Games

■ To achieve target of 32 million of tourist by 2018

■ The Government will extend eVisa, currently available to Chinese tourists, to countriesin the Balkans and South Asia regions

■ Overall, very exciting years to come for the tourism sector

■ Estimate an increase in direct investments in the hospitality sector

■ High demand for 4 – 5 star hotels to cater for increase in business travellers

■ High demand for hotels with convention, seminar, exhibition and meeting room facilities(i.e. MICE Facilities), in line with Government’s aim to become a top MICE destination

■ Prominent luxury hotel brands that will be GREAT to debut in Malaysia to attract nicheclientele would be the likes of the “Bulgari’s”, “Langham’s” etc.

“HAVE WE HIT ROCK BOTTOM?”

“Yes, for Residential, Office

and Hotel markets.”

“Retail market will face a bit more

downward pressure.”

MAY THE FORCE BE WITH YOU