harnessing the ring of fire - … · marcos overthrown/ people power revolution . 1997. asian...

TRANSCRIPT

HARNESSING THE RING OF FIRE:

Assessing the Impacts of Development Financing on Geothermal Development in

Indonesia and the Philippines By: Kathryn Chelminski

PhD Candidate in IR– Graduate Institute, Geneva Visiting Fellow – EPRG, University of Cambridge

25 October 2016 University of Cambridge, EPRG Energy & Environment seminar

International development finance for clean energy

• Priority of sustainable energy development underlined in Sustainable Development Goals and Paris Agreement o Need for financing for developing countries – barriers to

development • Institutional landscape of development support changing in

recent years o New finance mechanisms and international organizations o Between 2007-2015, national and multilateral development

banks have invested USD 877 billion in investments in clean energy (BNEF 2015).

• Expected to exceed USD 1 trillion by 2020 o South-South flows reached all time high o Post-Paris Agreement financial architecture?

Indonesia and the Philippines: Case Selection

• Archipelagos in Ring of Fire resulting in geothermal abundance (2nd and 3rd largest producers) o YET, despite Indonesia’s superior geothermal reserves

(~29GW) it only developed 5% of its potential compared to the Philippines that has developed 56% of potential capacity (~4GW)

• Both engaged in clean energy governance and recipients of development assistance for renewable energy development

• Geothermal technology faces with a number of difficult barriers to development in comparison to other renewable energy technologies o High exploration risks and costs of development o Regulatory barriers o Human capacity barriers

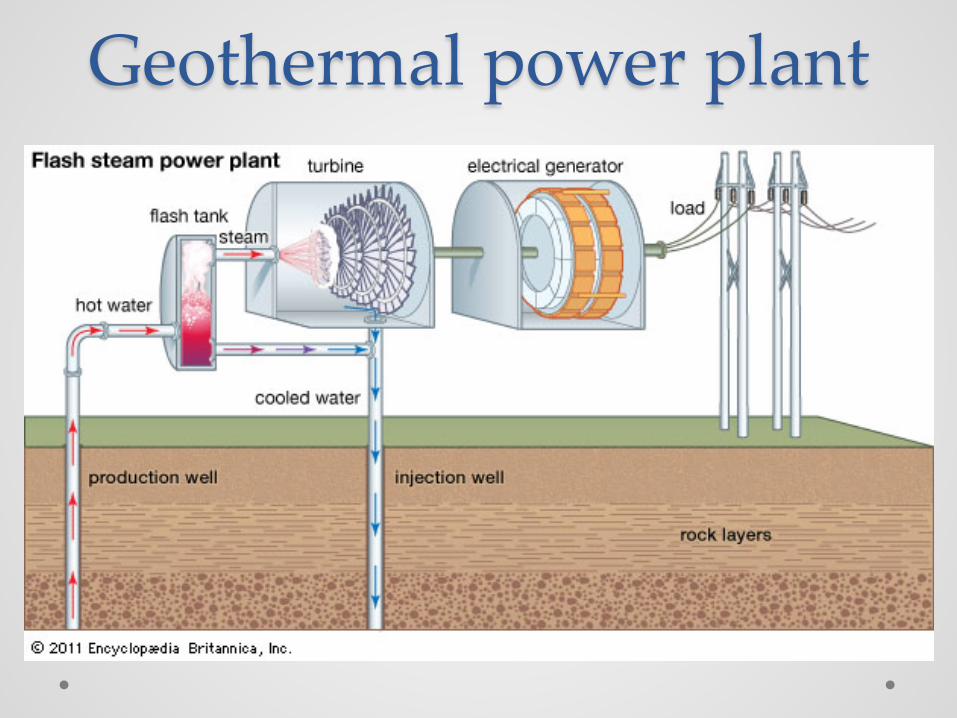

Geothermal power plant

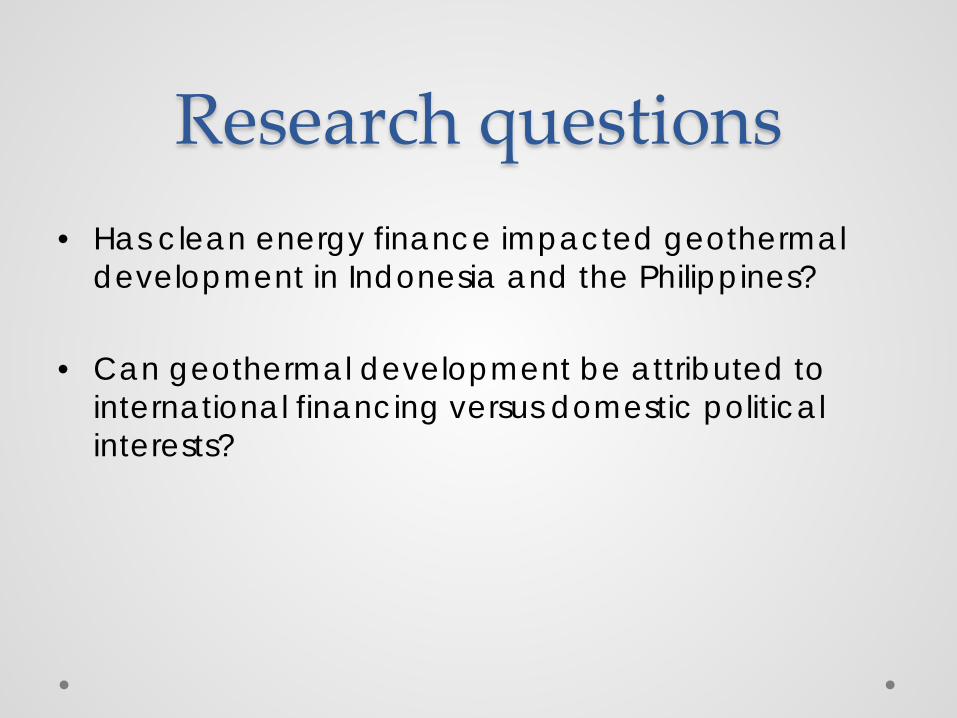

Research questions

• Has clean energy finance impacted geothermal development in Indonesia and the Philippines?

• Can geothermal development be attributed to international financing versus domestic political interests?

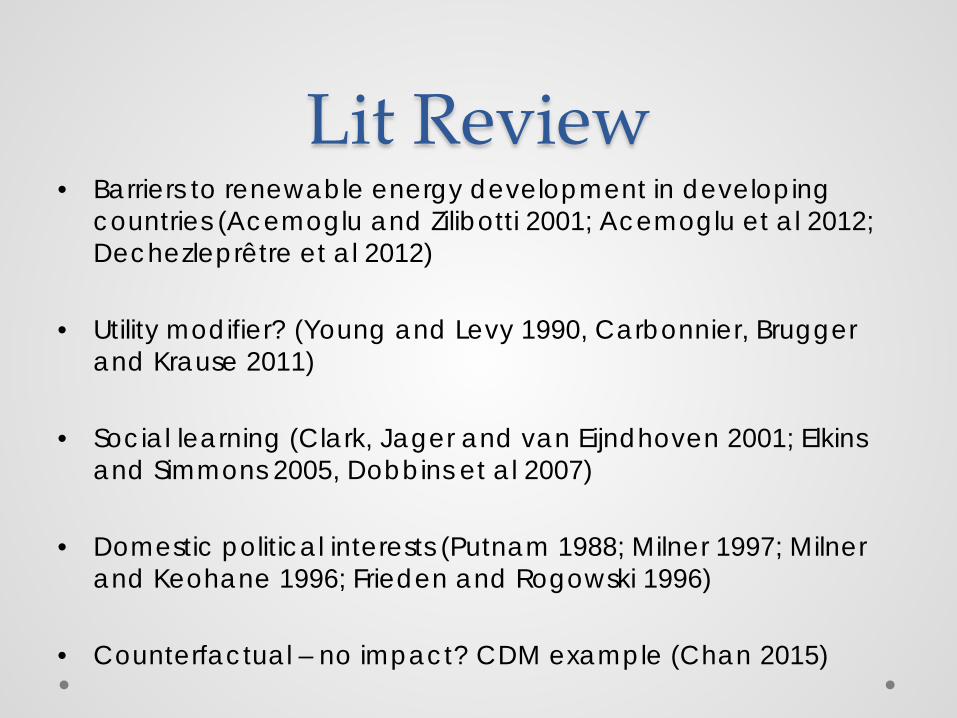

Lit Review • Barriers to renewable energy development in developing

countries (Acemoglu and Zilibotti 2001; Acemoglu et al 2012; Dechezleprêtre et al 2012)

• Utility modifier? (Young and Levy 1990, Carbonnier, Brugger and Krause 2011)

• Social learning (Clark, Jager and van Eijndhoven 2001; Elkins and Simmons 2005, Dobbins et al 2007)

• Domestic political interests (Putnam 1988; Milner 1997; Milner and Keohane 1996; Frieden and Rogowski 1996)

• Counterfactual – no impact? CDM example (Chan 2015)

Research Design

• Qualitative analysis • Process tracing • Field research in Indonesia (2014 & 2015)

and the Philippines (2016) o 137 interviews at headquarter and field level

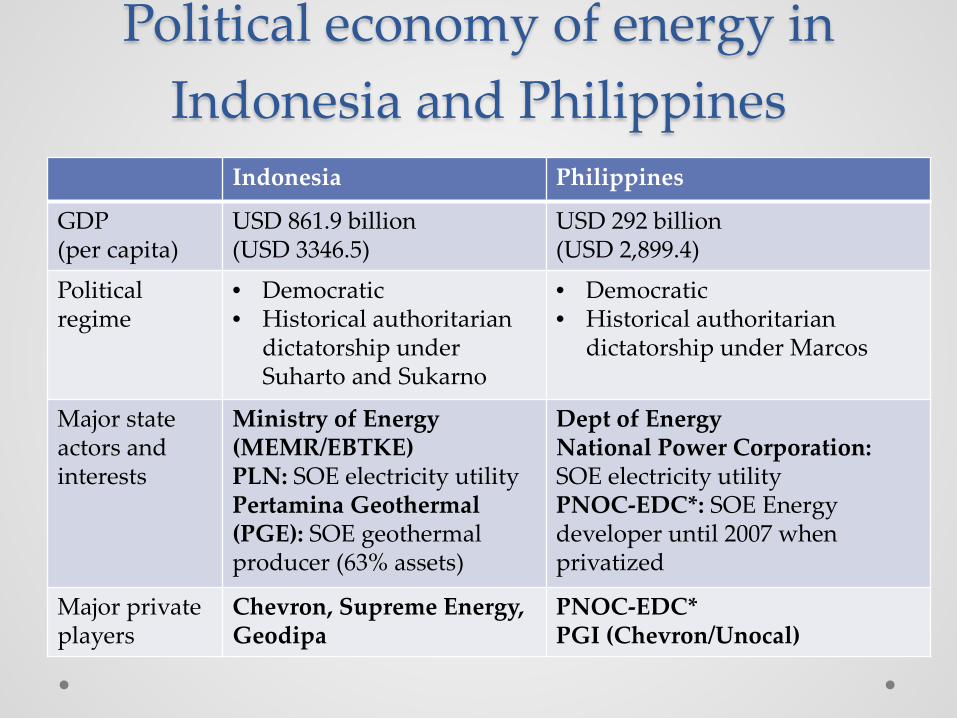

Political economy of energy in Indonesia and Philippines

Indonesia Philippines

GDP (per capita)

USD 861.9 billion (USD 3346.5)

USD 292 billion (USD 2,899.4)

Political regime

• Democratic • Historical authoritarian

dictatorship under Suharto and Sukarno

• Democratic • Historical authoritarian

dictatorship under Marcos

Major state actors and interests

Ministry of Energy (MEMR/EBTKE) PLN: SOE electricity utility Pertamina Geothermal (PGE): SOE geothermal producer (63% assets)

Dept of Energy National Power Corporation: SOE electricity utility PNOC-EDC*: SOE Energy developer until 2007 when privatized

Major private players

Chevron, Supreme Energy, Geodipa

PNOC-EDC* PGI (Chevron/Unocal)

Ownership of geothermal assets in Indonesia

SOE 63%

Private 37%

Geothermal steamfield operators in Indonesia

SOE 61%

IPPs 39%

Geothermal power plant operators in Indonesia

Source: Yunis 2015

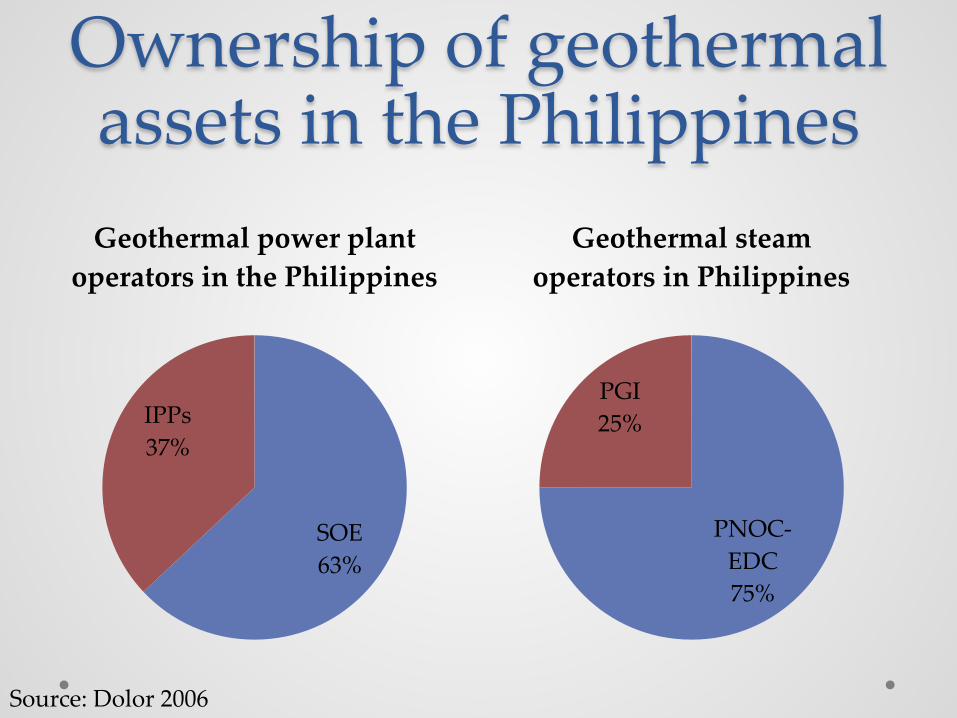

Ownership of geothermal assets in the Philippines

PNOC-EDC 75%

PGI 25%

Geothermal steam operators in Philippines

SOE 63%

IPPs 37%

Geothermal power plant operators in the Philippines

Source: Dolor 2006

National Energy Mix

Oil 19%

Hydro 19%

Geothermal 10%

Coal 32%

New RE 5%

Natural Gas 15%

Philippines Installed Generating Capacity (2015)

Source: Tharakan/ADB 2015 Source: DoE 2015

Oil 50%

Gas 20%

Coal 26%

Hydro 2%

Geothermal 1% New RE

1%

Indonesia Installed Generating Capacity (2011)

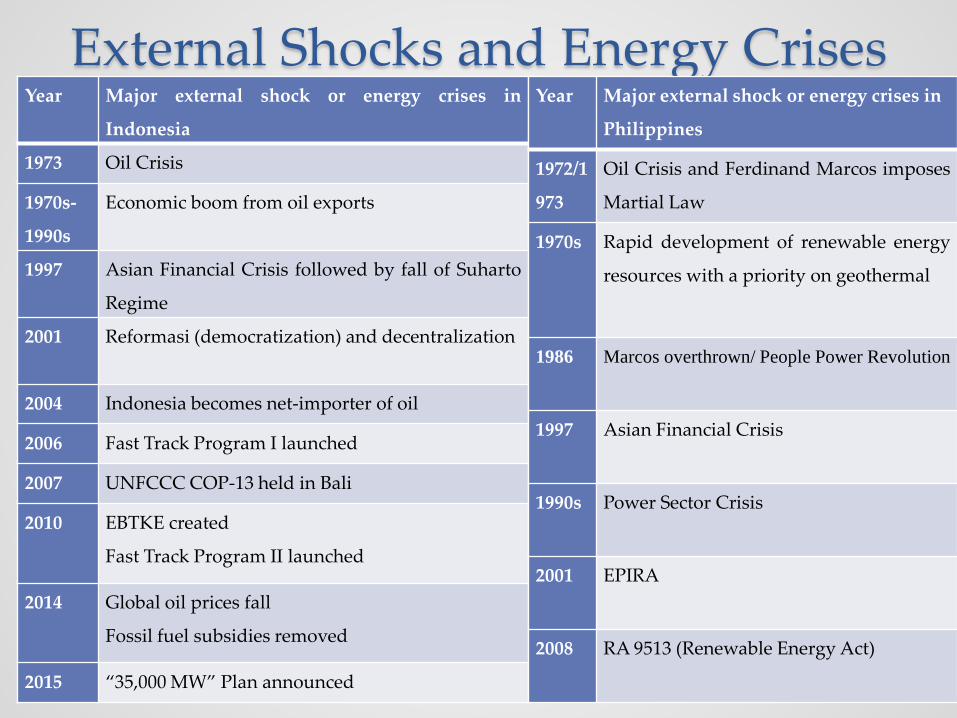

External Shocks and Energy Crises Year Major external shock or energy crises in

Indonesia

1973 Oil Crisis

1970s-

1990s

Economic boom from oil exports

1997 Asian Financial Crisis followed by fall of Suharto

Regime

2001 Reformasi (democratization) and decentralization

2004 Indonesia becomes net-importer of oil

2006 Fast Track Program I launched

2007 UNFCCC COP-13 held in Bali

2010 EBTKE created

Fast Track Program II launched

2014 Global oil prices fall

Fossil fuel subsidies removed

2015 “35,000 MW” Plan announced

Year Major external shock or energy crises in

Philippines

1972/1

973

Oil Crisis and Ferdinand Marcos imposes

Martial Law

1970s Rapid development of renewable energy

resources with a priority on geothermal

1986 Marcos overthrown/ People Power Revolution

1997 Asian Financial Crisis

1990s Power Sector Crisis

2001 EPIRA

2008 RA 9513 (Renewable Energy Act)

0

200

400

600

800

1000

1200

1400

1600

1800

200019

80

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

(100

0 bb

l/d)

Indonesia's Crude Oil Production and Consumption

Crude Oil production Consumption

Source: EIA 2016

0

500

1000

1500

2000

2500

1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 2002 2008 2010 2012

Inst

alle

d ca

paci

ty (M

W)

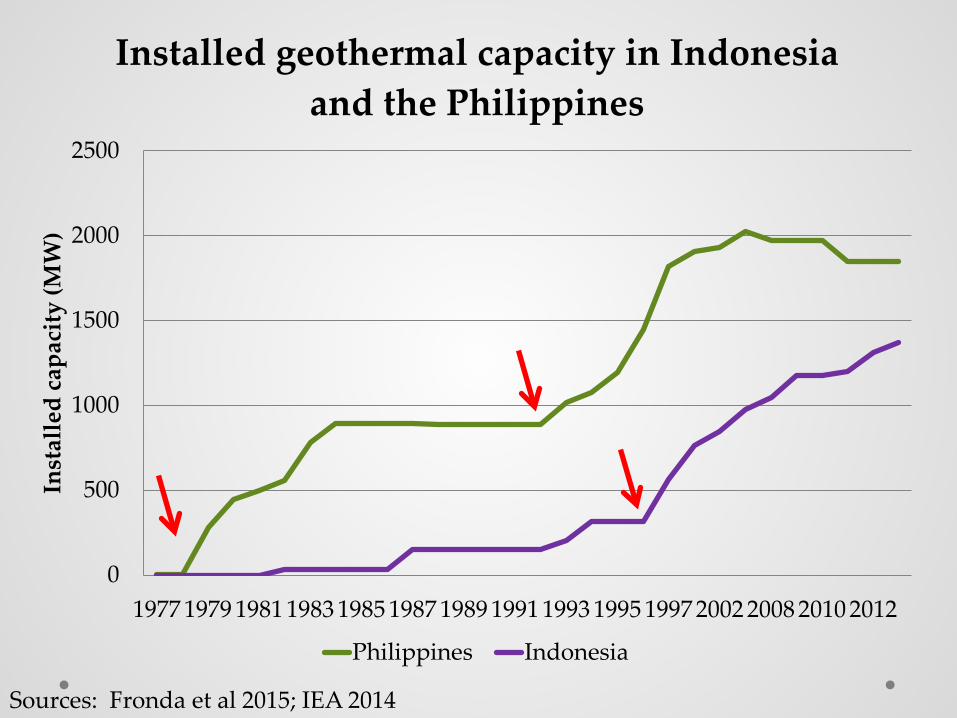

Installed geothermal capacity in Indonesia and the Philippines

Philippines Indonesia

Sources: Fronda et al 2015; IEA 2014

Barriers to geothermal development Regulatory Barriers

Financial Barriers

Sociocultural Barriers

Human Capacity Barriers

Philippines • Protected areas and ancestral lands

• Permitting • Power sector

regime and offtake (EPIRA)

• Foreign ownership vs 40/60 clause

• Tariffs – FIT? • High costs of

development with new technology (lack of quality resources)

• Risks of no offtake

• Indigenous Peoples

• Historical* lack of technical workforce

Indonesia • Tariffs, permitting • Geothermal Law

2003 • Forestry Law • Foreign

ownership 45 (1>10 MW)/ 95 (<10 MW)

• Exploration risks

• High costs of development

• No financial mechanism

• Protests from local communities

• Energy development contestation

• Historical* lack of technical workforce

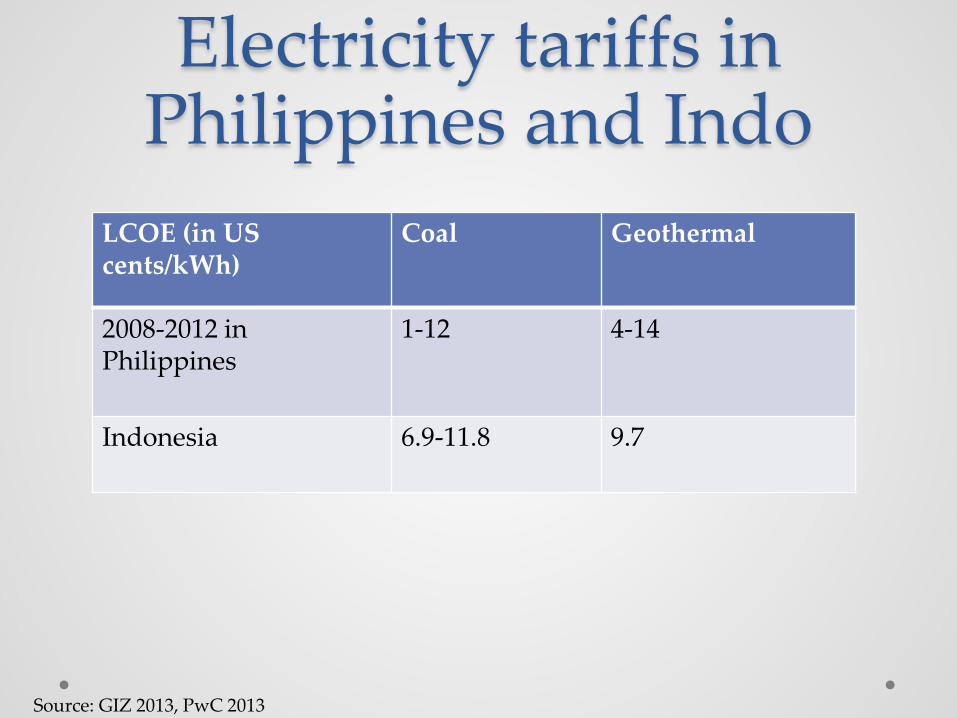

Electricity tariffs in Philippines and Indo

LCOE (in US cents/kWh)

Coal Geothermal

2008-2012 in Philippines

1-12 4-14

Indonesia 6.9-11.8 9.7

Source: GIZ 2013, PwC 2013

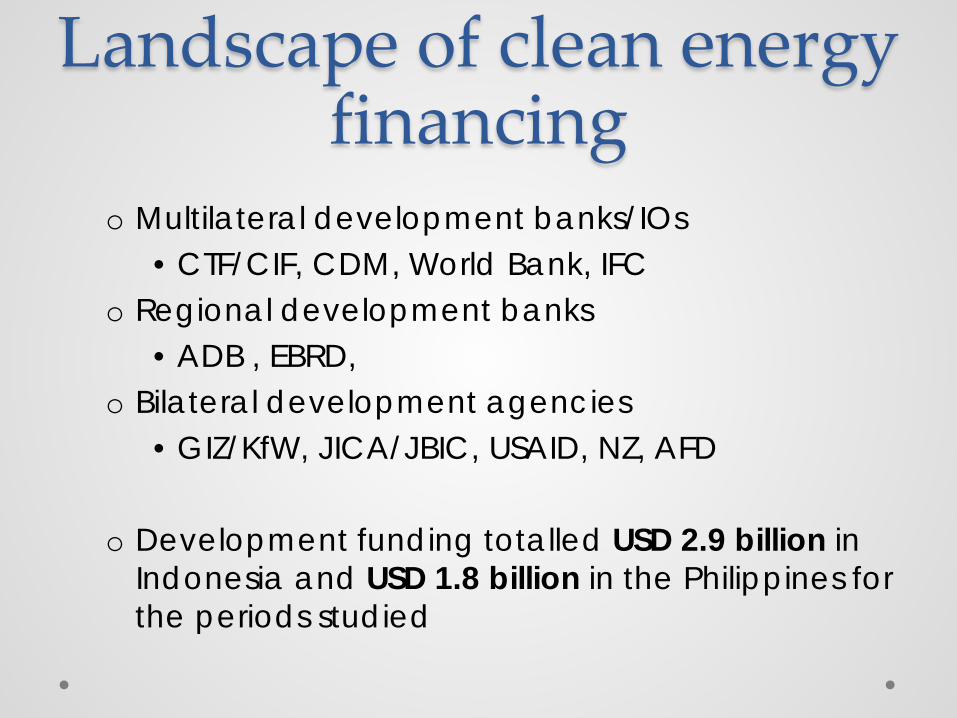

Landscape of clean energy financing

o Multilateral development banks/IOs • CTF/CIF, CDM, World Bank, IFC

o Regional development banks • ADB , EBRD,

o Bilateral development agencies • GIZ/KfW, JICA/JBIC, USAID, NZ, AFD

o Development funding totalled USD 2.9 billion in

Indonesia and USD 1.8 billion in the Philippines for the periods studied

Indonesia Geothermal Projects IRR and CDM finance

Project title IRR % excl.

CER

IRR

benchmark Investment in US$ millions

Kamojang Unit 4 Geothermal 15.31 17.10* 84.0

Wayang Windu Phase 2 Geothermal Power Project 17.62 18.96 181.4

Patuha Geothermal Project 6.73 14.71 109.7

Project Ulubelu Unit 3 – 4 15.98 19.67 271.0

Project Lumut Balai Unit 1 – 2 13.99 20.09 281.6

Gunung Rajabasa Geothermal Power Plant 12.18 17.10 682.0

Liki Pinangawan Muaralaboh Geothermal Power

Plant

11.36 17.10 794.0

Rantau Dedap Geothermal Power Plant 10.07 17.10 755.6

Project Lumut Balai Unit 3 – 4 16.08 17.92 276.4

Project Kamojang Unit 5 PT. Pertamina

Geothermal Energy

14.47 17.91 83.2

Project Karaha Unit 1 PT. Pertamina Geothermal

Energy

14.92 17.91 81.6

Lahendong Unit 5 & Unit 6 Geothermal Project 8.71 17.10 211.0

Source: UNEP DTU 2016

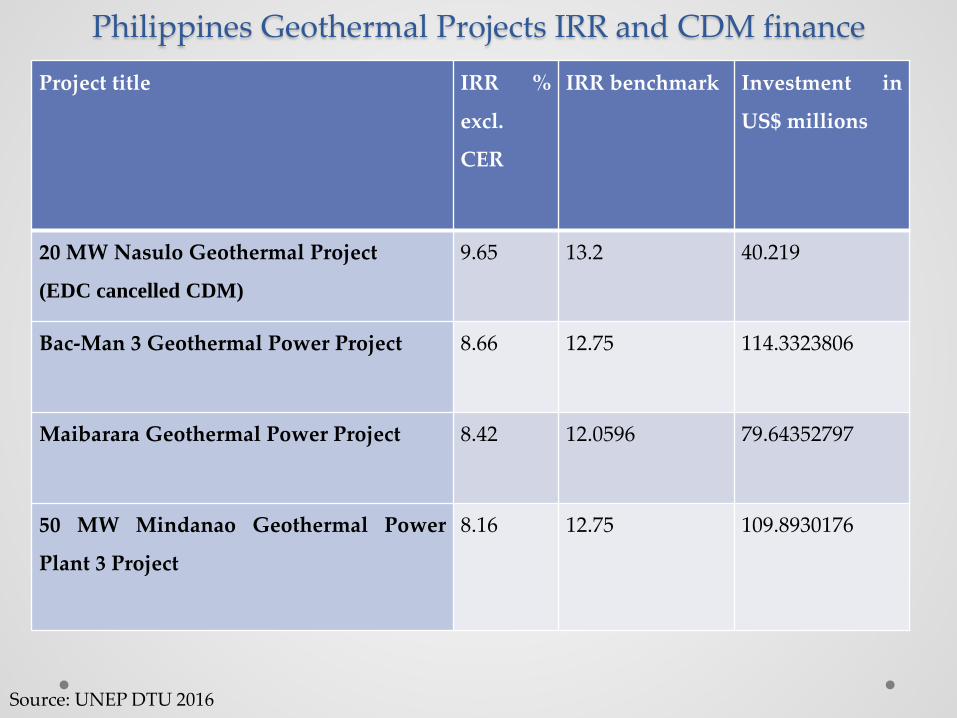

Philippines Geothermal Projects IRR and CDM finance Project title IRR %

excl.

CER

IRR benchmark Investment in

US$ millions

20 MW Nasulo Geothermal Project

(EDC cancelled CDM)

9.65 13.2 40.219

Bac-Man 3 Geothermal Power Project 8.66 12.75 114.3323806

Maibarara Geothermal Power Project 8.42 12.0596 79.64352797

50 MW Mindanao Geothermal Power

Plant 3 Project

8.16 12.75 109.8930176

Source: UNEP DTU 2016

0

200

400

600

800

1000

1200

1400

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Aid

in U

SD m

illio

ns

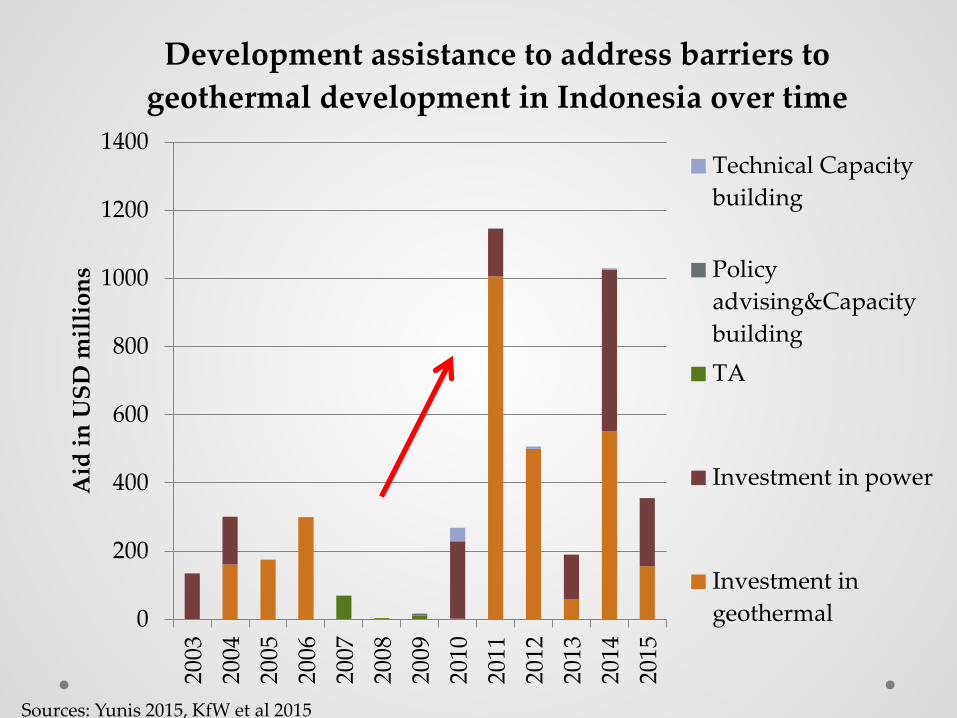

Development assistance to address barriers to geothermal development in Indonesia over time

Technical Capacitybuilding

Policyadvising&CapacitybuildingTA

Investment in power

Investment ingeothermal

Sources: Yunis 2015, KfW et al 2015

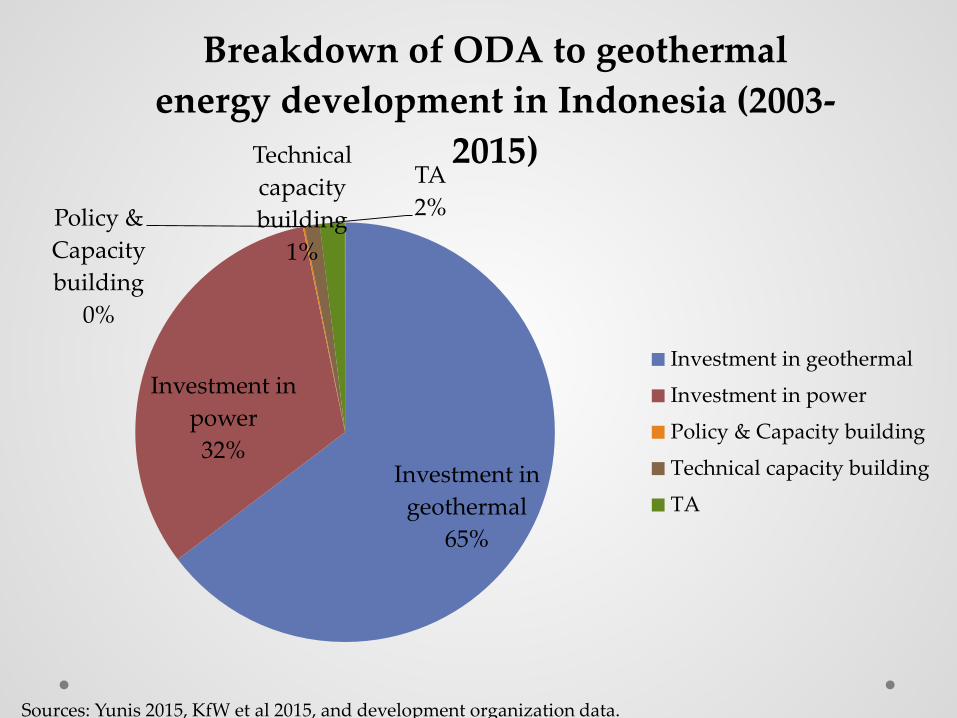

Investment in geothermal

65%

Investment in power 32%

Policy & Capacity building

0%

Technical capacity building

1%

TA 2%

Breakdown of ODA to geothermal energy development in Indonesia (2003-

2015)

Investment in geothermal

Investment in power

Policy & Capacity building

Technical capacity building

TA

Sources: Yunis 2015, KfW et al 2015, and development organization data.

0

100

200

300

400

500

600

USD

in m

illio

ns

Earmarked breakdown of ODA to geothermal development in Philippines over time

Technical capacitybuildingPolicy advising&Capacity buildingTA

Investment in powersectorInvestment ingeothermal

Sources: World Bank 2016a, ADB 2016, JICA 2016

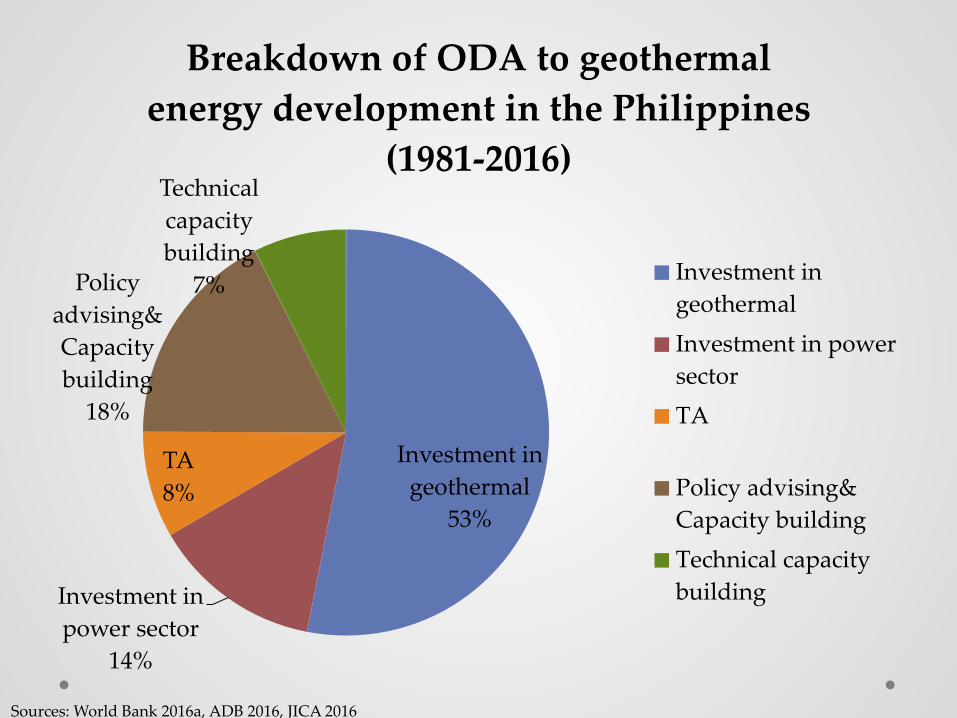

Investment in geothermal

53%

Investment in power sector

14%

TA 8%

Policy advising& Capacity building

18%

Technical capacity building

7%

Breakdown of ODA to geothermal energy development in the Philippines

(1981-2016)

Investment ingeothermalInvestment in powersectorTA

Policy advising&Capacity buildingTechnical capacitybuilding

Sources: World Bank 2016a, ADB 2016, JICA 2016

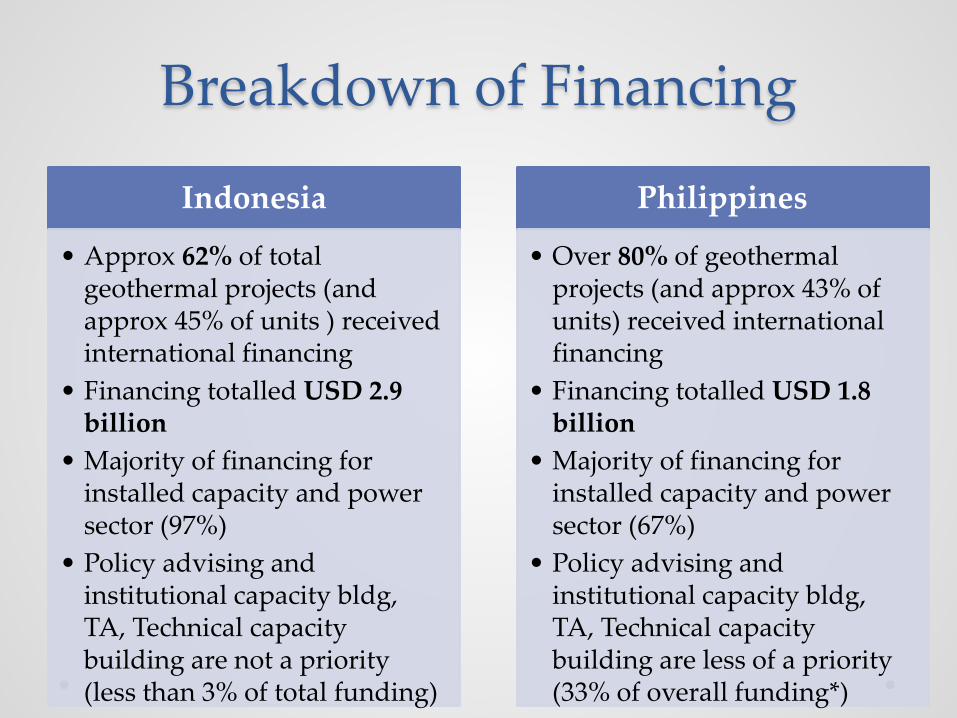

Breakdown of Financing

Indonesia

• Approx 62% of total geothermal projects (and approx 45% of units ) received international financing

• Financing totalled USD 2.9 billion

• Majority of financing for installed capacity and power sector (97%)

• Policy advising and institutional capacity bldg, TA, Technical capacity building are not a priority (less than 3% of total funding)

Philippines

• Over 80% of geothermal projects (and approx 43% of units) received international financing

• Financing totalled USD 1.8 billion

• Majority of financing for installed capacity and power sector (67%)

• Policy advising and institutional capacity bldg, TA, Technical capacity building are less of a priority (33% of overall funding*)

Discussion • Financial incentives

• Social learning aspects of financing

• Domestic political interests

• Measurable impact? Counterfactual

• Limitations with research

Thank you!

Questions?

Kathryn Chelminski PhD Candidate in International Relations – Graduate Institute, Geneva Visiting Fellow – EPRG, University of Cambridge [email protected] or [email protected]