harmonization of relations of the state and individuals in the context of taxation theory y. tyurina...

TRANSCRIPT

Harmonization of relations of the state and individuals in the

context of taxation theory

Y. TyurinaDepartment of finances, Orenburg state university (Orenburg, Russia). Candidate of economic sciences, Associate Professor.

Actuality of the harmonization of relations of the state and individuals in

the context of taxation theory

Nowadays, in Russia more and more urgent becomes the problem of social disparity and territorial differentiation of incomes of population, which have hindering influence upon rates if economic growth of the country.

Taxes have big potential in solving of mentioned problems, which confirms the urgency of the given problem from the position of search of balance between participants of fiscal relations.

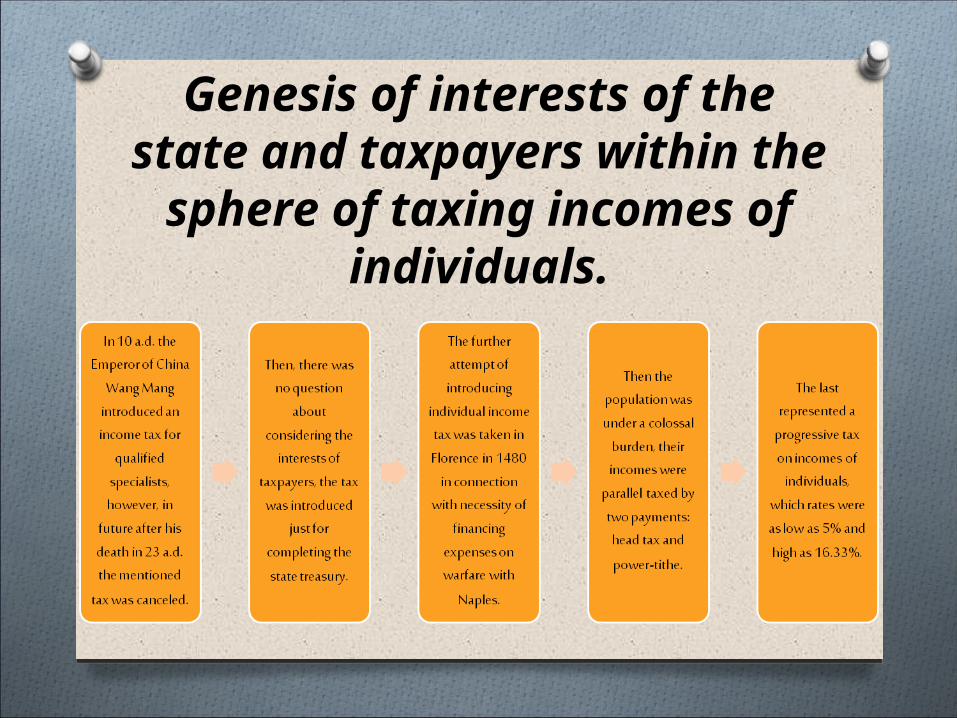

Genesis of interests of the state and taxpayers within

the sphere of taxing incomes of individuals.

Development of theories of taxation of

individuals

Taxation practice

Classification of taxation principles, directed on

harmonization of relation of the state and individuals.Principles of taxation, directed on harmonization

of relations between state and individuals

General Special

-universality

- equality

- one-time taxation

- gratuitousness

- public aim of collecting taxes

- comfortableness and certainty

- efficiency

- directivity of formation of tax

structure

- social justice

- progressivity

- optimality

- adequacy

Social directivity of tax is unequivocally confirms by presence of revenues, released from taxation,

which include:

Conclusion Studying of the main stages of development of the

theories of taxation of individuals allowed deeper understanding of the nature and basis of tax existence.

Catholicity of theories creates a powerful base for improving fiscal legal relations between the state and taxpayers, gives an opportunity for filling the gaps and correcting defects in the practice of tax collection.

In Russia practice of taxing revenues of individuals began with introduction of a head duty. It should be mentioned, that the historical experience evidences about collecting income tax both by progressive scale, and with use of a non-taxable minimum.

However, according to the organs of state authority, such a system didn’t lead to the necessary level of budgetary receipts, though it was providing social stability, and further it was reformed, putting one of the main principles of taxation – principle of justice to the background.

Thank you for your

attention!Y. Tyurina

Department of finances, Orenburg state university (Orenburg, Russia). Candidate of economic sciences, Associate Professor.