harmonising contract-based shari`ah requirements...

TRANSCRIPT

HARMONISING CONTRACT-BASED SHARI`AH REQUIREMENTS & MARKET

REALITIES: WILL IT WORK?

Professor Dr Engku Rabiah Adawiah Engku Ali

International Islamic University Malaysia

Islamic Finance Intellectual Discourse

18-20 October 2016

Melaka, Malaysia

INTRODUCTION

• It is often said that Islamic finance has to fulfill 2 major requirements in order for it to be viable:

– Shariah requirements

– Market requirements

• However, the main question is, is this achievable? Will it work?

• This presentation attempts to look into this issue, highlighting:

– The challenges in harmonising contract-based Shariahrequirements and market realities with some examples/case studies

– The way forward?

Islamic Finance Intellectual Discourse 2016 2

CHALLENGES?

• Islamic Finance does not operate in a vacuum

• It exists in an ecosystem comprising various inter-connected segments:

– socio-economic norms & culture;

– legal & regulatory environment;

– tax regime;

– political landscape;

– financial reporting framework;

– etc.

• Sometimes, this ecosystem (market realities) does not provide the ideal environment for a successful harmonization to happen Islamic Finance Intellectual Discourse 2016 3

Islamic Finance Intellectual Discourse 2016

THE ECO-SYSTEM IN WHICH ISLAMIC FINANCE CO-EXISTS

Islamic Finance Politics:

• International policies

• Government policies

• Political will

Conventional economy/ financial system:

• Conventional ethos

• Interest-based system

• CompetitionSocial:

• Human capital

• Human nature – strength & weaknesses

• Human preferences

• Technology – information, media

• Managing human perceptions & idiosyncrasies

Legal:

• Law

• Court system

• Taxation

• Accounting requirements/ treatments

Environment:

• Ecological issues

• Force majeure

• Disaster management & relief

4

MAIN CHALLENGE: SOCIO-ECONOMIC NORM & CULTURE

• Market requirements are normally dictated by socio-economic norms & culture of the people

• Are market norms & practices value-neutral?

• Conventional worldview vs Islamic worldview?

• Capitalistic worldview vs khilafah worldview?

Islamic Finance Intellectual Discourse 2016 5

ISLAMIC WORLDVIEW ON WEALTH CREATION & ENJOYMENT?

• Aims at creating value, whilst observing Shariah principles & philosophies:– Wealth as a trust – accountability & responsibility

– Avoidance of oppressive transactions – prohibition of riba etc.

– Promoting a fair & just way of doing finance – win-win deals

– Avoidance of uncertainty, ambiguity & concealment of material information in contracts – prohibition of gharar, misrepresentation & fraud

– Promoting disclosure & transparency in commercial deals

• “Trustee” role to use resources in a fair & accountable manner for the good of all (balance between individual interests & societal interests)

6Islamic Finance Intellectual Discourse 2016

UNIQUE VALUE PROPOSITION OF ISLAMIC FINANCE?

• Financing real economic activities that seek to promote the quality of five basic essentials:

– Religion, life, intellect, property and family relations;

• Based on the extent of the needs:

– Necessities (daruriyyat)

– Needs (hajiyyat)

– Complementaries (tahsiniyyat)

• Prioritisation in the use of economic resources – to achieve optimal use based on need analysis – maqsad hifz al-mal

7Islamic Finance Intellectual Discourse 2016

DIVERGENCE BETWEEN CONVENTIONAL WORLDVIEW VS ISLAMIC WORLVIEW?

CONVENTIONAL WORLDVIEW ISLAMIC WORLDVIEW -

MAQASID AL-SHARI`AH

Islamic Finance Intellectual Discourse 2016 8

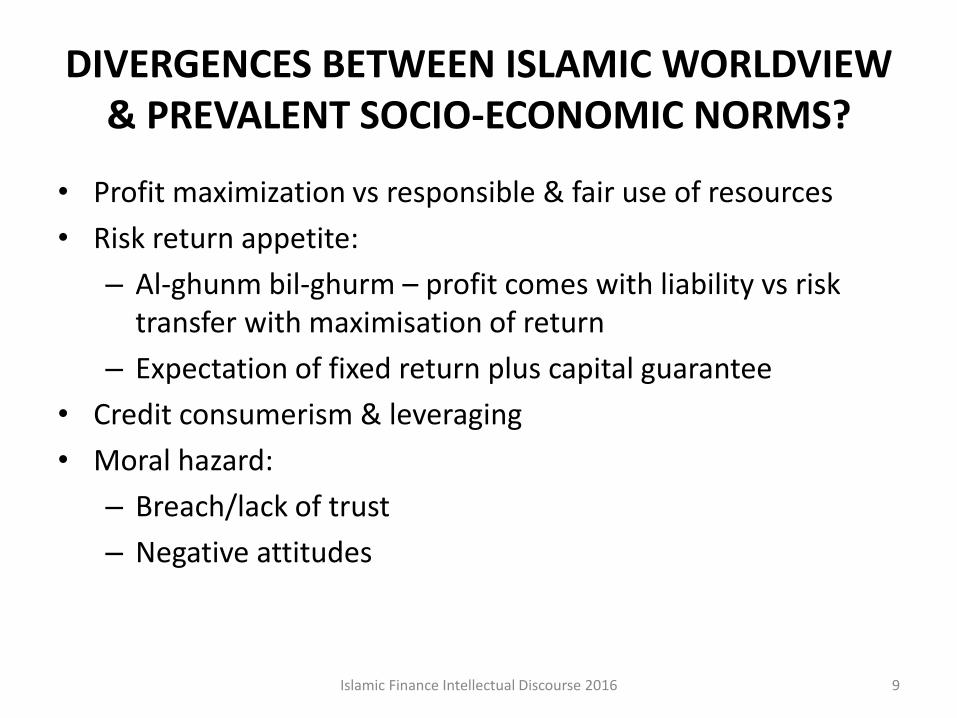

DIVERGENCES BETWEEN ISLAMIC WORLDVIEW & PREVALENT SOCIO-ECONOMIC NORMS?

• Profit maximization vs responsible & fair use of resources

• Risk return appetite:

– Al-ghunm bil-ghurm – profit comes with liability vs risk transfer with maximisation of return

– Expectation of fixed return plus capital guarantee

• Credit consumerism & leveraging

• Moral hazard:

– Breach/lack of trust

– Negative attitudes

Islamic Finance Intellectual Discourse 2016 9

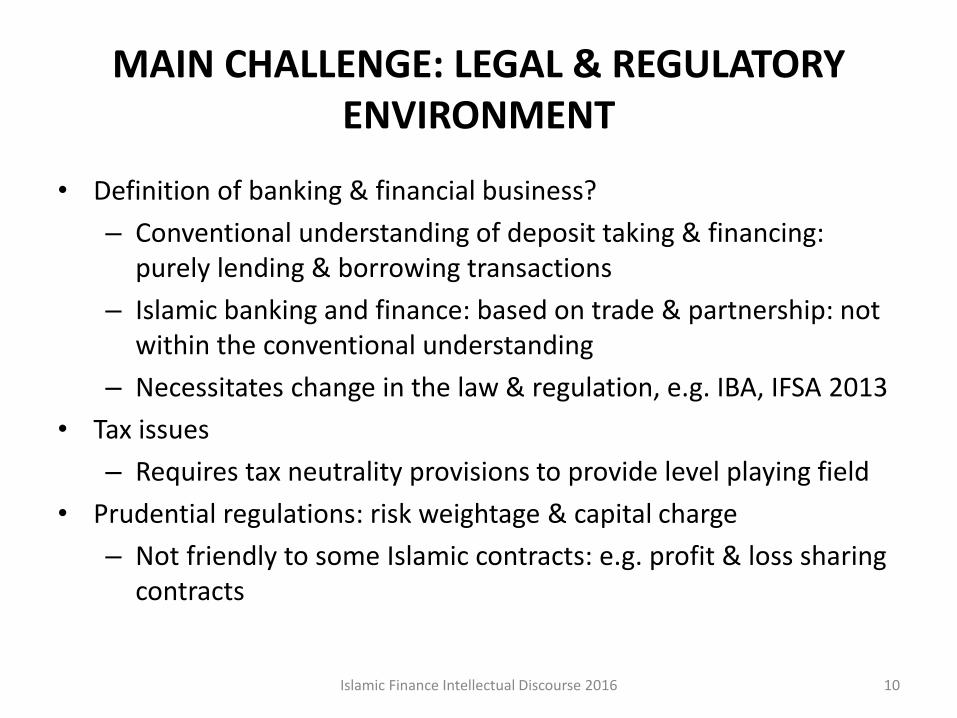

MAIN CHALLENGE: LEGAL & REGULATORY ENVIRONMENT

• Definition of banking & financial business?

– Conventional understanding of deposit taking & financing: purely lending & borrowing transactions

– Islamic banking and finance: based on trade & partnership: not within the conventional understanding

– Necessitates change in the law & regulation, e.g. IBA, IFSA 2013

• Tax issues

– Requires tax neutrality provisions to provide level playing field

• Prudential regulations: risk weightage & capital charge

– Not friendly to some Islamic contracts: e.g. profit & loss sharing contracts

Islamic Finance Intellectual Discourse 2016 10

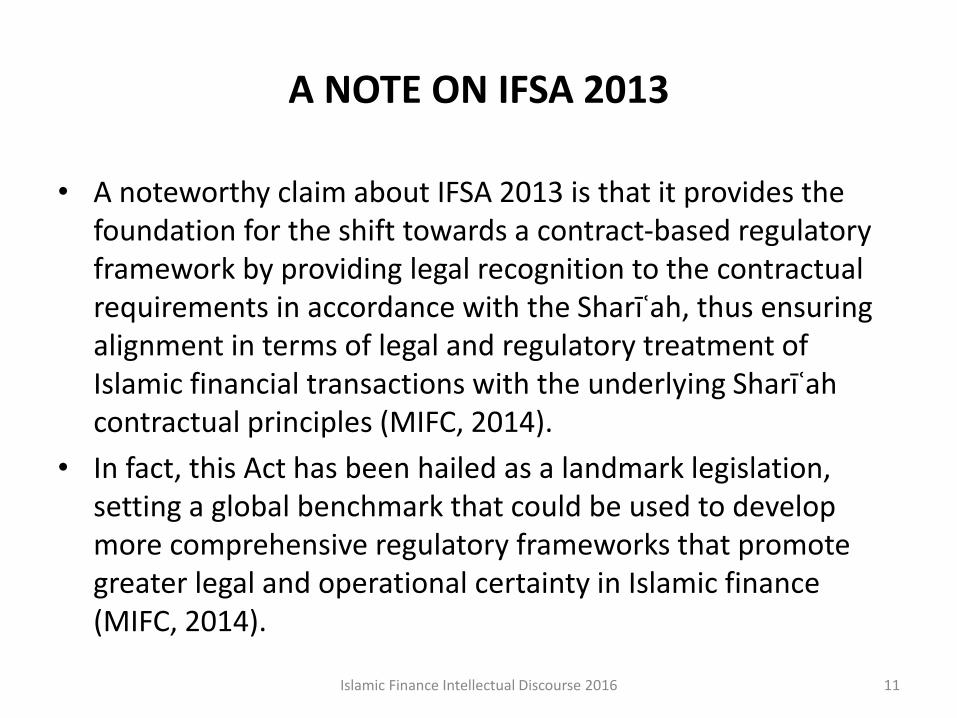

A NOTE ON IFSA 2013

• A noteworthy claim about IFSA 2013 is that it provides the foundation for the shift towards a contract-based regulatory framework by providing legal recognition to the contractual requirements in accordance with the Sharīʿah, thus ensuring alignment in terms of legal and regulatory treatment of Islamic financial transactions with the underlying Sharīʿahcontractual principles (MIFC, 2014).

• In fact, this Act has been hailed as a landmark legislation, setting a global benchmark that could be used to develop more comprehensive regulatory frameworks that promote greater legal and operational certainty in Islamic finance (MIFC, 2014).

Islamic Finance Intellectual Discourse 2016 11

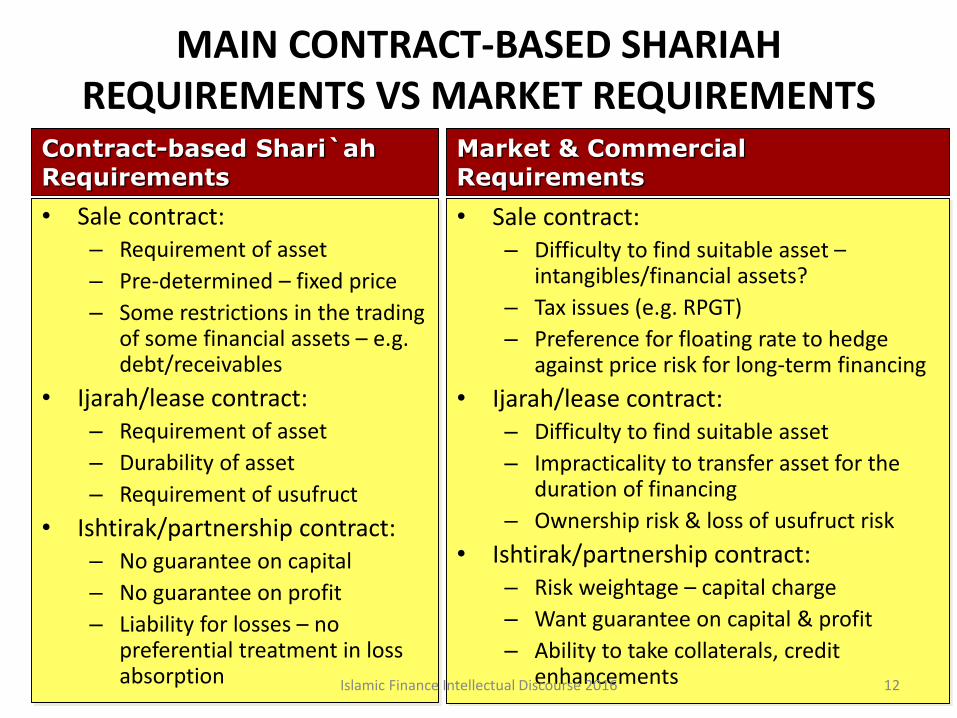

MAIN CONTRACT-BASED SHARIAH REQUIREMENTS VS MARKET REQUIREMENTS

• Sale contract:– Requirement of asset

– Pre-determined – fixed price

– Some restrictions in the trading of some financial assets – e.g. debt/receivables

• Ijarah/lease contract:– Requirement of asset

– Durability of asset

– Requirement of usufruct

• Ishtirak/partnership contract:– No guarantee on capital

– No guarantee on profit

– Liability for losses – no preferential treatment in loss absorption

• Sale contract:– Difficulty to find suitable asset –

intangibles/financial assets?

– Tax issues (e.g. RPGT)

– Preference for floating rate to hedge against price risk for long-term financing

• Ijarah/lease contract:– Difficulty to find suitable asset

– Impracticality to transfer asset for the duration of financing

– Ownership risk & loss of usufruct risk

• Ishtirak/partnership contract:– Risk weightage – capital charge

– Want guarantee on capital & profit

– Ability to take collaterals, credit enhancements

Contract-based Shari`ahRequirements

Market & Commercial Requirements

Islamic Finance Intellectual Discourse 2016 12

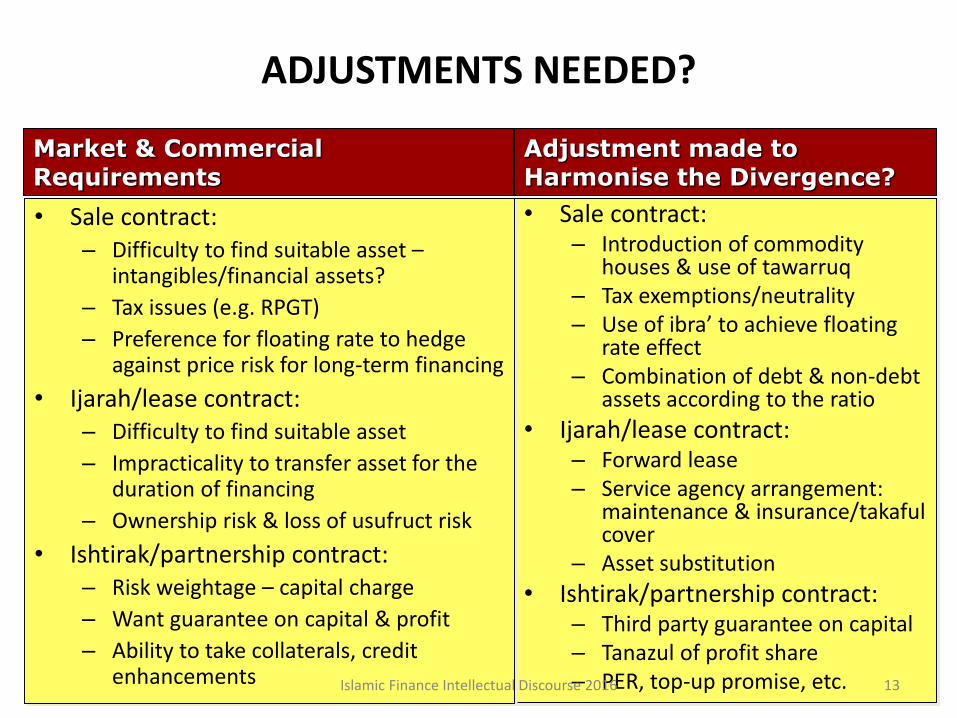

ADJUSTMENTS NEEDED?

• Sale contract:– Introduction of commodity

houses & use of tawarruq– Tax exemptions/neutrality– Use of ibra’ to achieve floating

rate effect– Combination of debt & non-debt

assets according to the ratio

• Ijarah/lease contract:– Forward lease– Service agency arrangement:

maintenance & insurance/takafulcover

– Asset substitution

• Ishtirak/partnership contract:– Third party guarantee on capital– Tanazul of profit share– PER, top-up promise, etc.

Adjustment made to Harmonise the Divergence?

• Sale contract:– Difficulty to find suitable asset –

intangibles/financial assets?

– Tax issues (e.g. RPGT)

– Preference for floating rate to hedge against price risk for long-term financing

• Ijarah/lease contract:– Difficulty to find suitable asset

– Impracticality to transfer asset for the duration of financing

– Ownership risk & loss of usufruct risk

• Ishtirak/partnership contract:– Risk weightage – capital charge

– Want guarantee on capital & profit

– Ability to take collaterals, credit enhancements

Market & Commercial Requirements

Islamic Finance Intellectual Discourse 2016 13

DOES THE HARMONISATION WORK?Case Study of Sukuk

SUKUK MARKET

15

• Phenomenal growth of sukuk market

• Sukuk – one of the most talked about sector of Islamic finance

• Why sukuk? Raising finance (funds):

– Sovereign

– Corporations

• For what?

– Infrastructure development

– Working capital

– Project finance

– Etc

• Benefits? Potentially – cheaper cost, liquid & tradable instrument in financing development, projects & real economy

Islamic Finance Intellectual Discourse 2016

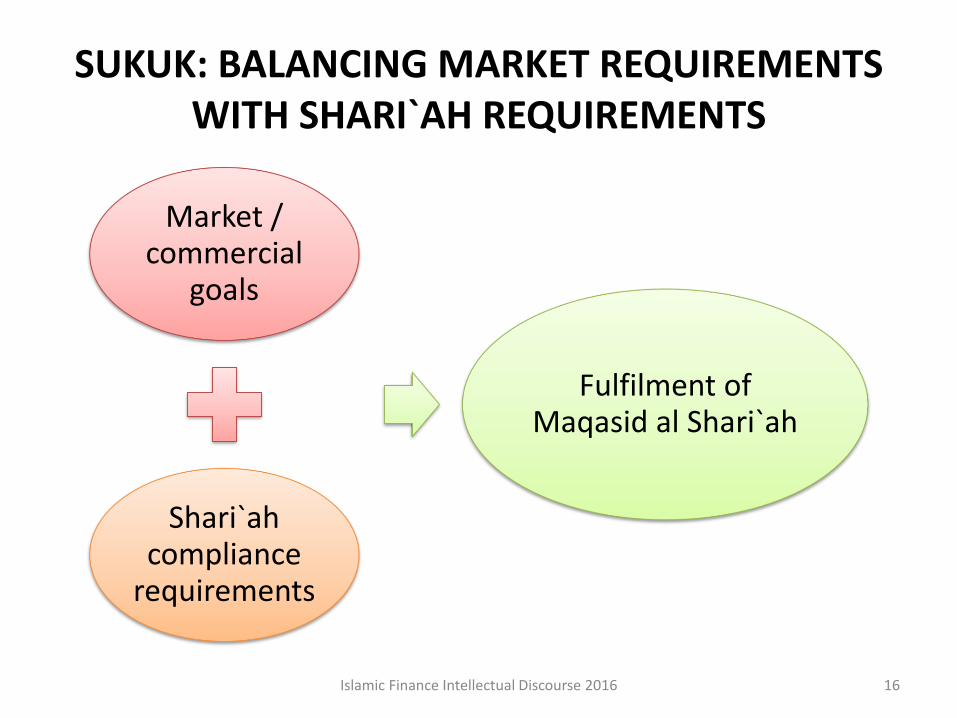

SUKUK: BALANCING MARKET REQUIREMENTS WITH SHARI`AH REQUIREMENTS

Market / commercial

goals

Shari`ahcompliance

requirements

Fulfilment of Maqasid al Shari`ah

16Islamic Finance Intellectual Discourse 2016

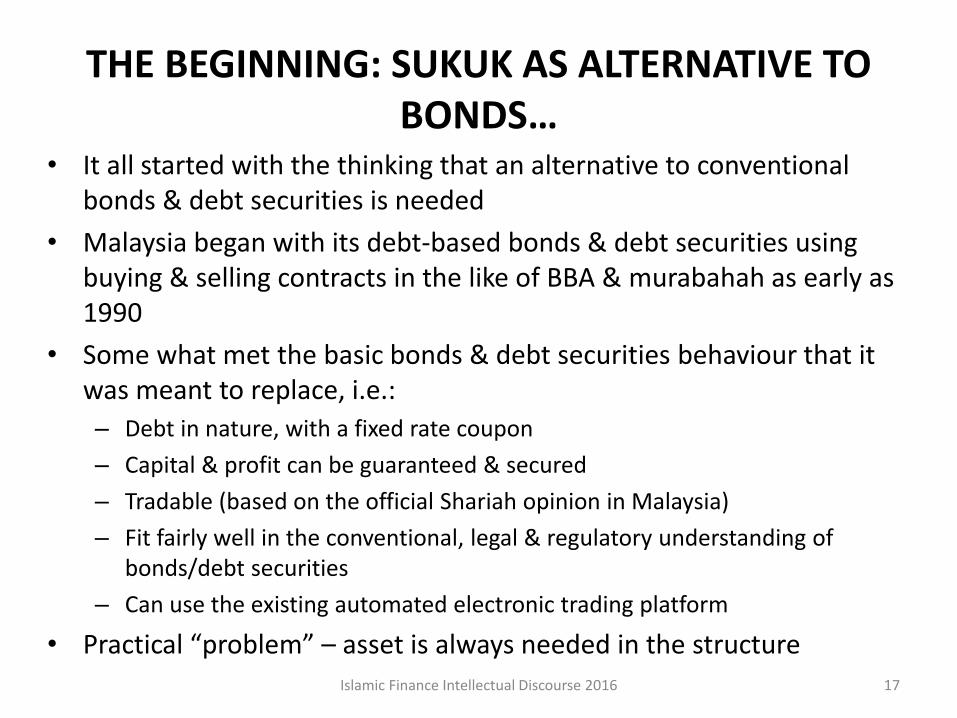

THE BEGINNING: SUKUK AS ALTERNATIVE TO BONDS…

• It all started with the thinking that an alternative to conventional bonds & debt securities is needed

• Malaysia began with its debt-based bonds & debt securities using buying & selling contracts in the like of BBA & murabahah as early as 1990

• Some what met the basic bonds & debt securities behaviour that it was meant to replace, i.e.:

– Debt in nature, with a fixed rate coupon

– Capital & profit can be guaranteed & secured

– Tradable (based on the official Shariah opinion in Malaysia)

– Fit fairly well in the conventional, legal & regulatory understanding of bonds/debt securities

– Can use the existing automated electronic trading platform

• Practical “problem” – asset is always needed in the structure

17Islamic Finance Intellectual Discourse 2016

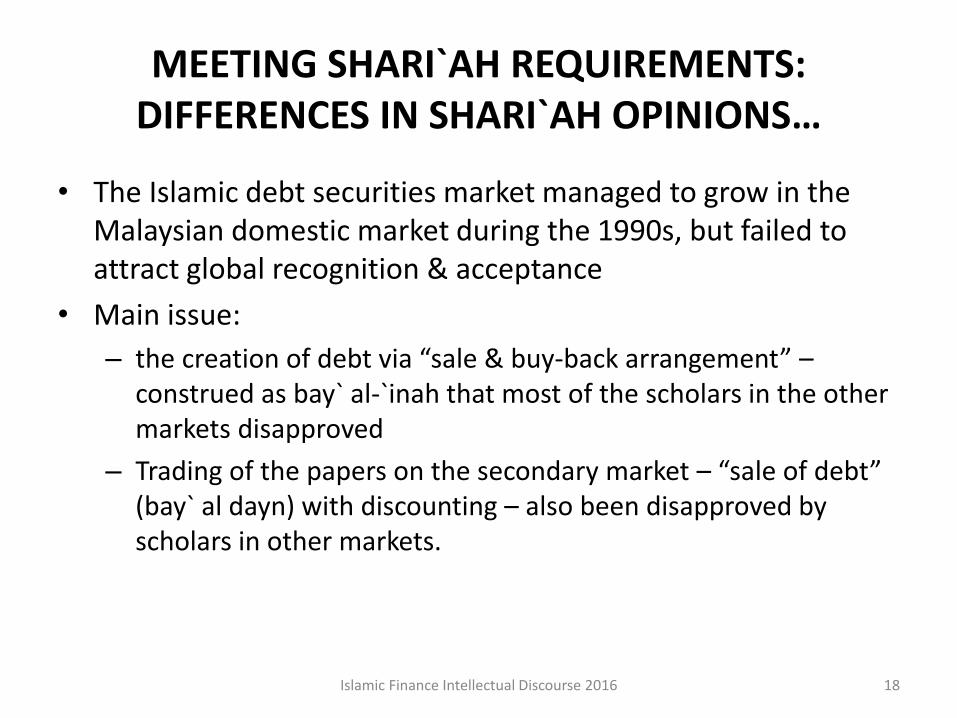

MEETING SHARI`AH REQUIREMENTS: DIFFERENCES IN SHARI`AH OPINIONS…

• The Islamic debt securities market managed to grow in the Malaysian domestic market during the 1990s, but failed to attract global recognition & acceptance

• Main issue:

– the creation of debt via “sale & buy-back arrangement” –construed as bay` al-`inah that most of the scholars in the other markets disapproved

– Trading of the papers on the secondary market – “sale of debt” (bay` al dayn) with discounting – also been disapproved by scholars in other markets.

18Islamic Finance Intellectual Discourse 2016

SUKUK AL IJARAH: THE BREAKTHROUGH?

• 2001 onwards the market started to experiment with lease-based structures

• A new understanding emerged – sukuk ijarah represent real/tangible asset that is sold & leased back to the obligor with profits in the rental payments

• This marked an important transition in market understanding –Islamic securities need not necessarily evidence debt (like conventional bonds)

• Sukuk ijarah managed to meet most market requirements for an alternative to bonds, i.e. fixed/floating rate coupon, can guarantee / secure capital & profit, tradability, etc.

• Practical “problem” remains – asset is always needed in the structure

19Islamic Finance Intellectual Discourse 2016

MUDARABAH & MUSHARAKAH STRUCTURES…

• Essentially equity in nature – no debt

• Necessitates a change in regulation in Malaysia – from PDS Guidelines 2000 to Islamic Securities Guidelines 2004 & later Sukuk Guidelines 2011

• Have certain features that are not “conventional” in bonds market:– No guarantee or security on capital / profit

– No fixed rate on the coupon – only “indicative rate” is allowed

• Yet, have certain features that are perceived positively– Can be structured to be tradable

– Do not necessarily need an asset to begin with

20Islamic Finance Intellectual Discourse 2016

MUDARABAH & MUSHARAKAH STRUCTURES: MEETING THE MARKET REQUIREMENTS…

• Between 2004 – 2008: the market devised techniques to minimise the “unconventional” features of mudarabah & musharakah sukuk:– Purchase undertaking

– Liquidity facility – top-up promise

– Hurdle rate & incentive fee / reward

• 2008 pronouncement by AAOIFI Shari`ah Board

• Post pronouncement?– Back to sukuk ijarah? Sukuk wakalah bil istithmar? Commodity

Murabahah?

– Try ABS?

– Accept the equity features as they are & be transparent about it?

– Other options??

21Islamic Finance Intellectual Discourse 2016

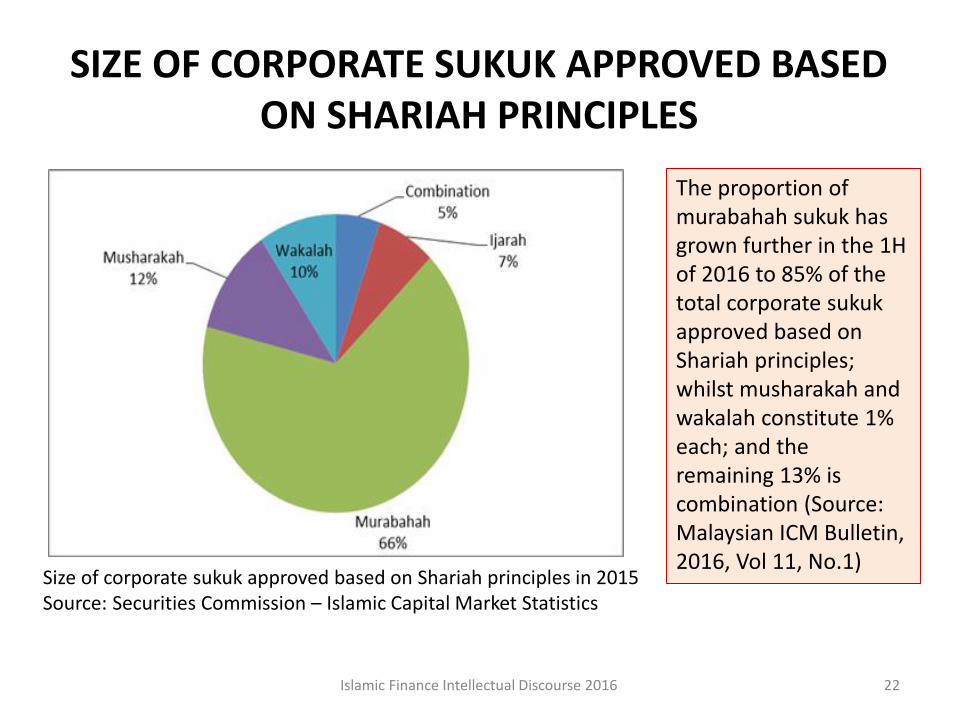

SIZE OF CORPORATE SUKUK APPROVED BASED ON SHARIAH PRINCIPLES

Size of corporate sukuk approved based on Shariah principles in 2015Source: Securities Commission – Islamic Capital Market Statistics

The proportion of murabahah sukuk has grown further in the 1H of 2016 to 85% of the total corporate sukukapproved based on Shariah principles; whilst musharakah and wakalah constitute 1% each; and the remaining 13% is combination (Source: Malaysian ICM Bulletin, 2016, Vol 11, No.1)

Islamic Finance Intellectual Discourse 2016 22

Islamic Finance Intellectual Discourse 2016

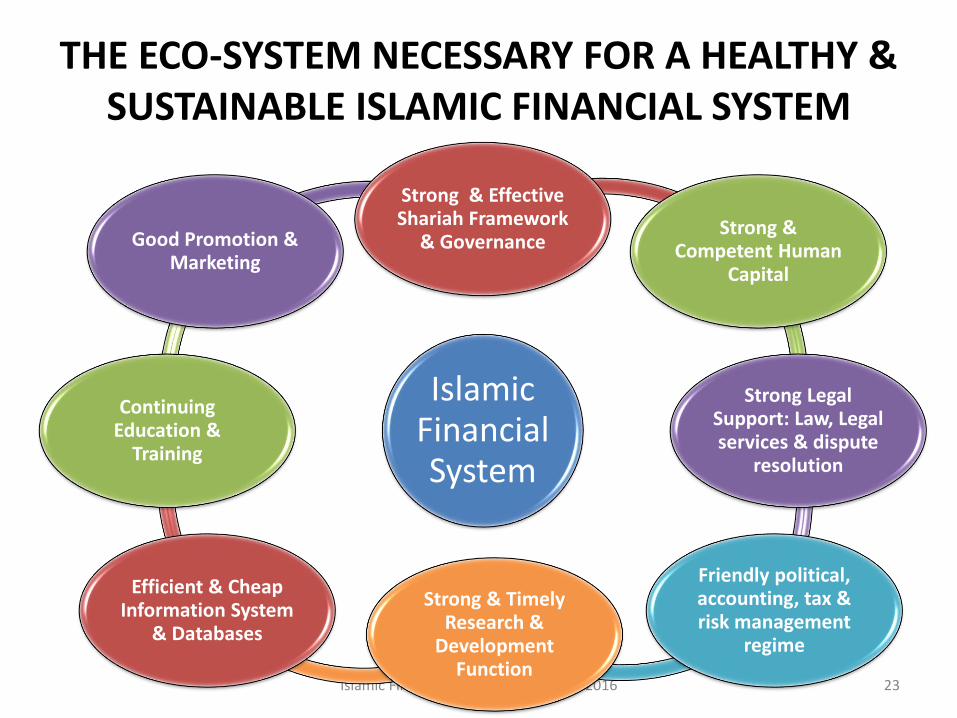

THE ECO-SYSTEM NECESSARY FOR A HEALTHY & SUSTAINABLE ISLAMIC FINANCIAL SYSTEM

Islamic Financial System

Strong & Effective Shariah Framework

& Governance Strong &

Competent Human Capital

Strong Legal Support: Law, Legal services & dispute

resolution

Friendly political, accounting, tax & risk management

regime

Strong & Timely Research &

Development Function

Efficient & Cheap Information System

& Databases

Continuing Education &

Training

Good Promotion & Marketing

23

CONVERGENCE BETWEEN SHARI`AH & COMMERCIAL GOALS

COMMERCIAL GOALS

SHARI`AH GOALS

24Islamic Finance Intellectual Discourse 2016

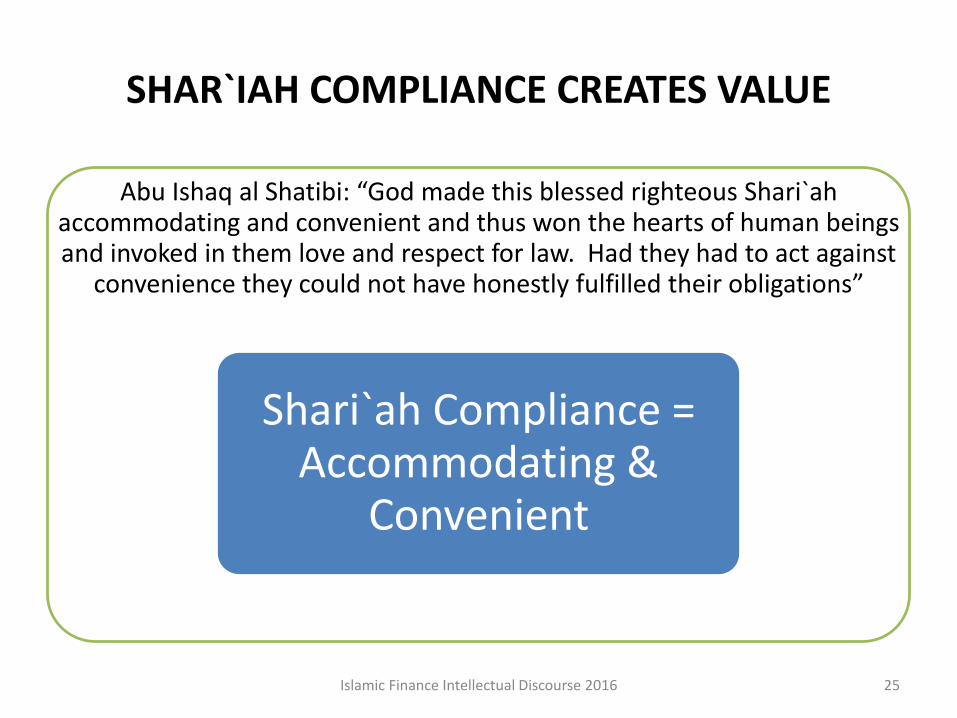

SHAR`IAH COMPLIANCE CREATES VALUE

Abu Ishaq al Shatibi: “God made this blessed righteous Shari`ahaccommodating and convenient and thus won the hearts of human beings and invoked in them love and respect for law. Had they had to act against

convenience they could not have honestly fulfilled their obligations”

Shari`ah Compliance = Accommodating &

Convenient

25Islamic Finance Intellectual Discourse 2016

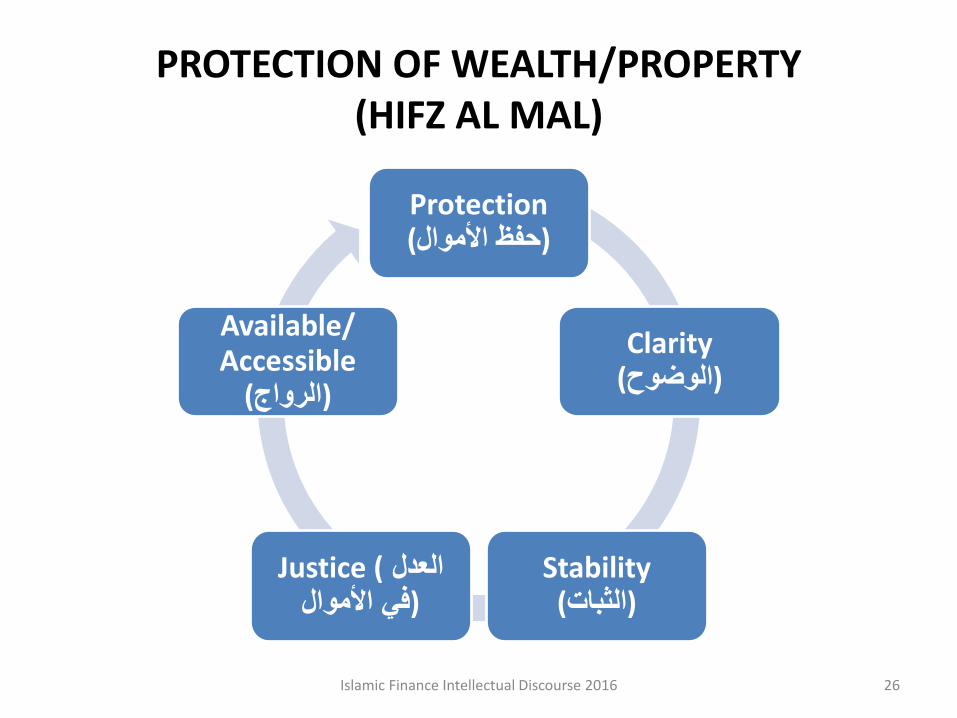

Protection (حفظ األموال)

Clarity (الوضوح)

Stability (الثبات)

Justice ( العدل (في األموال

Available/ Accessible

(الرواج)

PROTECTION OF WEALTH/PROPERTY (HIFZ AL MAL)

26Islamic Finance Intellectual Discourse 2016

OUR POSITION?

Gaps? Where? Why? How?

27Islamic Finance Intellectual Discourse 2016

THANK YOU

WASSALAM