hapter 3: the analysis of risk averter’ s ehavior

TRANSCRIPT

Chapter 3: the Analysis of Risk Averter’ s Behavior

2021/9/18 1

Main Contents 1. Risk aversion, risk neutral, risk seeking and fair gamble

2. Risk-averse individuals 'behavior

3. How to estimate the Individual Risk Aversion?

4. Absolute Risk Aversion and Relative Risk Aversion

2021/9/18 2

Fair Game Daniel Bernoulli, a famous mathematician in the 18th century, discovered when he studied the problem of gambling that people tend to care more about the money they lose than the money they may win.

2021/9/18 3

Examples 1 There is a coin toss game. Assume that the coin is completely symmetrical, you can win 2000 yuan with the head of the coin facing up and lose 2000 yuan with the head of coin facing down. Is this a fair game?

What if you can win 2000 yuan with the head of the coin facing up and win nothing with the head of the coin facing down. Is this a fair game?

2021/9/18 4

Definition 1. Fair gamble refers to gambling with a risk premium of 0.

For example, It is a gamble to guess the front and back of a coin. If you are right, you get 1 yuan, and if you are wrong, you lose 1 yuan. When there is no problem with the coin itself, it is a fair gamble.

2021/9/18 5

Fair Gamble Consider the gamble that has a positive return,1, with probability 𝑝 and a negative return, 2, with probability (1 − 𝑝)

Definition 2:The gamble is actually fair when its expected payoff is zero, or

𝑝1 + 1 − 𝑝 2 = 0

So if the mathematical expectation of winning a game is greater than zero, then the participant should pay the money which is equal to the expectation to make the game fair.

2021/9/18 6

Example 2 Consider such a game: win 200 yuan by the probability 0.5, and win nothing by the probability 0.5.

If the admission fee is 100, is it fair game?

What if the admission fee is 50 or 0?

Is everyone willing to participate?

2021/9/18 7

Risk Aversion Definition 3: An individual is said to be risk averse if he is unwilling to accept or is indifferent to any actuarially fair gamble. An individual is said to be strictly risk averse if he is unwilling to accept any actuarily fair gamble.

Let u( ) be the utility function of an individual. From the definition of (strict) risk aversion, we have

𝐸(𝑢 𝑊0 ) ≥ (>)𝐸(𝑢 𝑊0 + 𝑔 ) 𝐸 𝑔 = 0

or

𝑢(𝑊0)≥ > 𝑝 𝑢 𝑊0 + 1 + 1 − 𝑝 𝑢(𝑊0 + 2)

where 𝑊0 denotes the individual's initial wealth.

2021/9/18 8

The above relations demonstrate that risk aversion implies a concave utility function and that strict risk aversion implies a strictly concave utility function. A reversal of the above steps demonstrates that a concave utility function implies risk aversion and that a strictly concave utility function implies strict risk aversion.

Between the definite payment and the uncertain payment with the same expectation return, a risk averter always chooses the former.

2021/9/18 FINANCIAL ECONOMICS 9

Loosely speaking, a risk-averse investor “penalizes” the expected rate of return of a risky portfolio by a certain percentage (or penalizes the expected profit by a dollar amount) to account for the risk involved. The greater the risk, the larger the penalty。

Risk-averse investors consider only risk-free or speculative prospects with positive risk premiums.

2021/9/18 10

Risk Neutral Definition 4: An individual is said to be risk neutral if he is indifferent to any actuarially fair gamble.

𝐸 𝑢 𝑊0 = 𝐸(𝑢 𝑊0 + 𝑔 ) 𝐸 𝑔 = 0

or

𝑢(𝑊0)= 𝑝 𝑢 𝑊0 + 1 + 1 − 𝑝 𝑢(𝑊0 + 2)

Risk-neutral investors judge risky prospects solely by their expected rates of return. The level of risk is irrelevant to the risk-neutral investor, meaning that there is no penalty for risk.

2021/9/18 11

Example 3:

1)If someone is willing to participate in a game in which you can win 4000 yuan with the head of the coin facing up and lose 2000 yuan with the head of coin facing down and ticket price is 1000 yuan.

2)If someone is willing to participate in a game in which you can win 4 yuan with the head of the coin facing up and lose 2 yuan with the head of coin facing down and ticket price is 1 yuan.

2021/9/18 12

Risk Seeking Definition 5: An individual is said to be risk seeking if he is happy to attend all fair gambles.

𝐸(𝑢 𝑊0 ) ≤ (<)𝐸(𝑢 𝑊0 + 𝑔 ) 𝐸 𝑔 = 0

or

𝑢(𝑊0)≤ (<)𝑝 𝑢 𝑊0 + 1 + 1 − 𝑝 𝑢(𝑊0 + 2)

This investor adjusts the expected return upward to take into account the “fun” of confronting the prospect’s risk.

Risk lovers will always take a fair game because their upward adjustment of utility for risk gives the fair game a certainty equivalent that exceeds the alternative of the risk-free investment.

2021/9/18 13

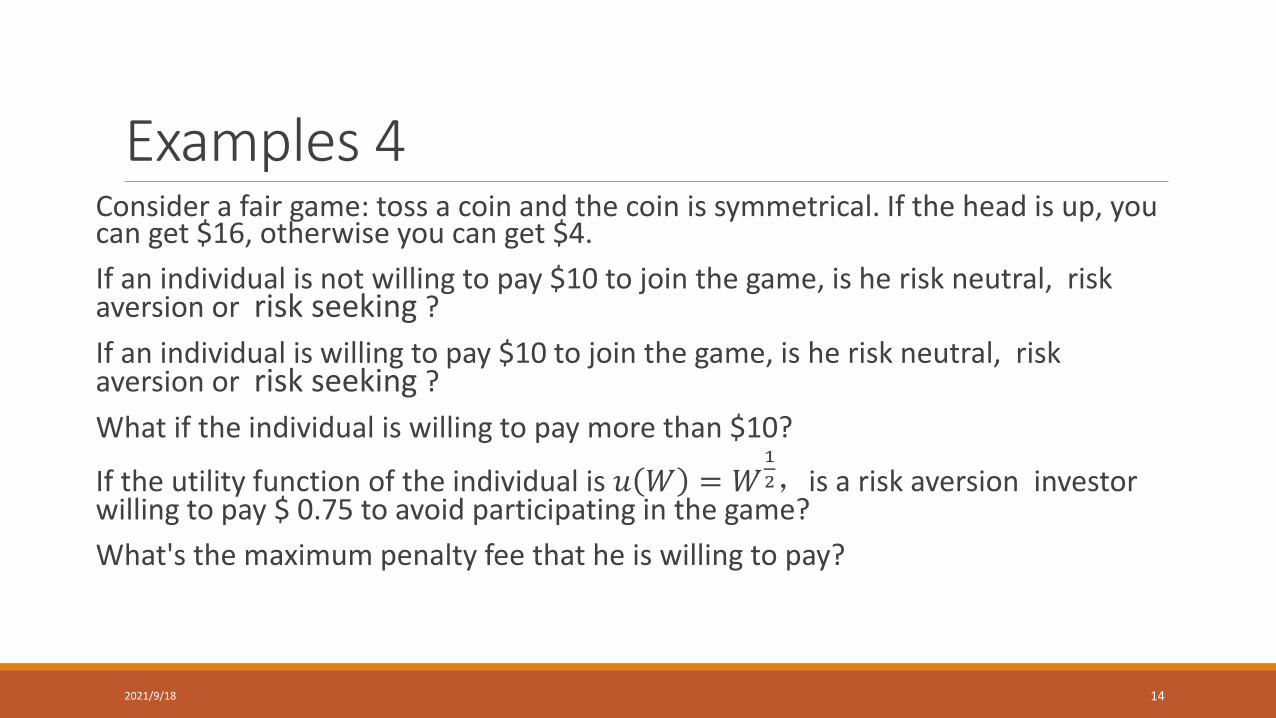

Examples 4 Consider a fair game: toss a coin and the coin is symmetrical. If the head is up, you can get $16, otherwise you can get $4.

If an individual is not willing to pay $10 to join the game, is he risk neutral, risk aversion or risk seeking ?

If an individual is willing to pay $10 to join the game, is he risk neutral, risk aversion or risk seeking ?

What if the individual is willing to pay more than $10?

If the utility function of the individual is 𝑢 𝑊 = 𝑊1

2,is a risk aversion investor willing to pay $ 0.75 to avoid participating in the game?

What's the maximum penalty fee that he is willing to pay?

2021/9/18 14

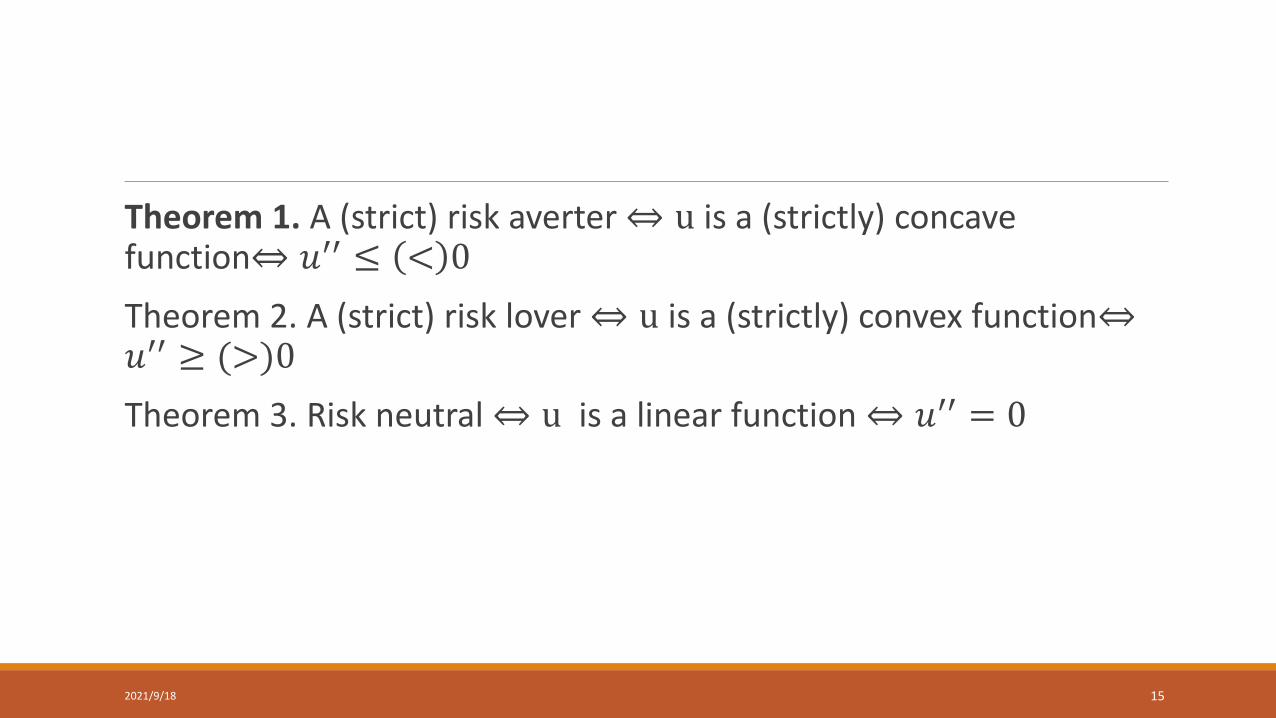

Theorem 1. A (strict) risk averter ⇔ u is a (strictly) concave function⇔ 𝑢′′ ≤ < 0

Theorem 2. A (strict) risk lover ⇔ u is a (strictly) convex function⇔𝑢′′ ≥ (>)0

Theorem 3. Risk neutral ⇔ u is a linear function ⇔ 𝑢′′ = 0

2021/9/18 15

Example 5 Suppose there is an investor, faced with such an fare gamble: the initial amount of investment is $100,000. There is half the chance to get $50,000, and the other half is to lose $50,000. The utility function is a logarithmic function. Please answer the following questions:

1. Explain the the risk preference of the investor

2. Calculate the certainty equivalent wealth.

2021/9/18 16

2Risk-averse individuals’ behavior Consider a portfolio selection of a risk averse individual who strictly prefers more to less (has a strictly increasing utility function).

Suppose there are 𝑁 kinds of risky assets and a risk-free asset in a frictionless market.

Denoted by 𝑟𝑗 and 𝑟𝑓 the returns of 𝑗𝑡 risky asset and the risk-free

asset, respectively. (𝑗 = 1,2,3 … 𝑁)

The initial wealth is assumed to be 𝑊0. Let 𝑎𝑗 be money invested to

𝑗𝑡 risky asset. (𝑗 = 1,2,3 … 𝑁)

2021/9/18 17

Proposition 1:An individual who is risk averse and strictly prefers more to less will

invest to risky asset if and only if the rate of return on at least one risky asset greater than the risk-free interest rate.

Until specified otherwise, consider a strictly risk averse individual who prefers more to less in an economy where there is only one risky asset and one riskless asset and where the risk premium of the risky asset is strictly positive.

2021/9/18 18

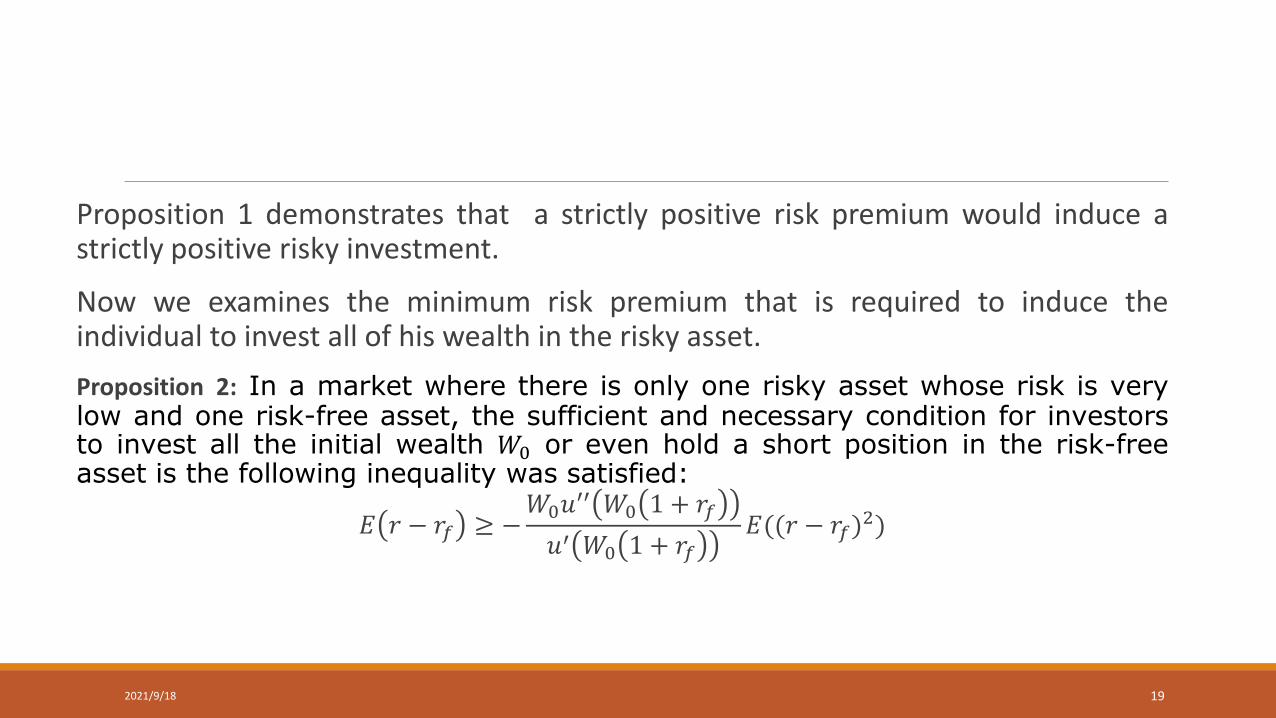

Proposition 1 demonstrates that a strictly positive risk premium would induce a strictly positive risky investment.

Now we examines the minimum risk premium that is required to induce the individual to invest all of his wealth in the risky asset.

Proposition 2: In a market where there is only one risky asset whose risk is very low and one risk-free asset, the sufficient and necessary condition for investors to invest all the initial wealth 𝑊0 or even hold a short position in the risk-free asset is the following inequality was satisfied:

𝐸 𝑟 − 𝑟𝑓 ≥ −𝑊0𝑢′′ 𝑊0 1 + 𝑟𝑓

𝑢′ 𝑊0 1 + 𝑟𝑓

𝐸((𝑟 − 𝑟𝑓)2)

2021/9/18 19

Note that for small risks, absolute risk aversion is a measure of the intensity of an individual's aversion to risk. From the inequation, the higher an individual's absolute risk aversion, the higher the minimum risk premium required to induce full investment in the risky asset. Intuitively, the curvature of an individual's utility function would be related to the minimum risk premium required to induce full investment in the risky asset

2021/9/18 FINANCIAL ECONOMICS 20

Proposition 3:In a market where there is only one risky asset whose risk is very low and one risk-free asset, the sufficient and necessary condition for investors to invest at least 𝜆𝑊0 in the risky asset is the following inequality is satisfied:

𝐸 𝑟 − 𝑟𝑓 ≥ −𝜆𝑊0𝑢′′ 𝑊0 1 + 𝑟𝑓

𝑢′ 𝑊0 1 + 𝑟𝑓

𝐸((𝑟 − 𝑟𝑓)2)

2021/9/18 21

When 𝜆 = 1, we have

𝐸 𝑟 − 𝑟𝑓 ≥ −𝑊0𝑢′′ 𝑊0 1 + 𝑟𝑓

𝑢′ 𝑊0 1 + 𝑟𝑓

𝐸((𝑟 − 𝑟𝑓)2)

𝐸 𝑟 − 𝑟𝑓 is the risk premium.

The minimum risk premium depends on the value of the fucntion

−𝑢′′(.)

𝑢′(.) at 𝑊0 1 + 𝑟𝑓 .

−𝑢′′(.)

𝑢′(.) is called absolute risk aversion defined by Arrow (1970) and Pratt

(1964).

2021/9/18 22

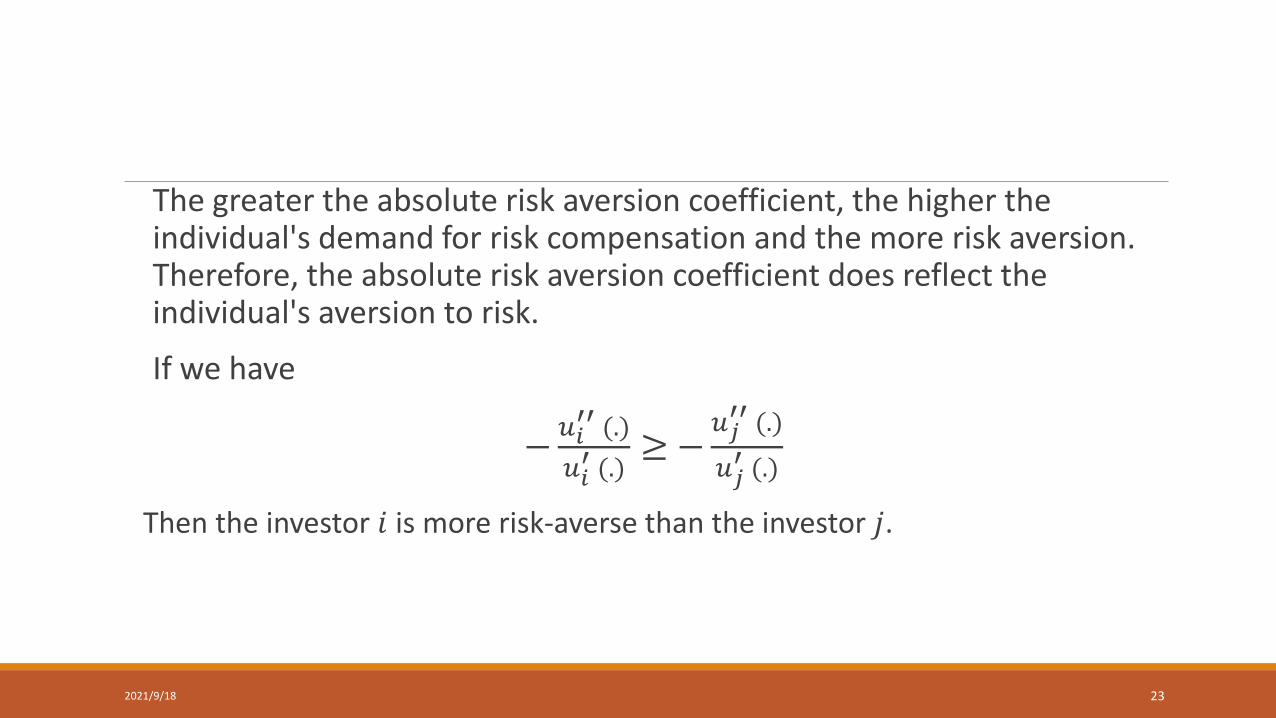

The greater the absolute risk aversion coefficient, the higher the individual's demand for risk compensation and the more risk aversion. Therefore, the absolute risk aversion coefficient does reflect the individual's aversion to risk.

If we have

−𝑢𝑖

′′ (.)

𝑢𝑖′ (.)

≥ −𝑢𝑗

′′ (.)

𝑢𝑗′ (.)

Then the investor 𝑖 is more risk-averse than the investor 𝑗.

2021/9/18 23

3. How to Estimate the Individual Risk Aversion?

Historical returns on various asset classes, analyzed in a mountain of empirical studies, leave no doubt that risky assets command a risk premium. This implies that most investors are risk averse.

Assume that all investors are risk-averse, but the degree of risk aversion of each person may be different, so we need to give some measures of the risk aversion.

Markowitz risk premium

Pratt-Arrow risk premium

2021/9/18 24

Markowitz risk premium

Definition 4: Let 𝑓 𝑊0, 𝐻 be the maximum amount of the penalty that investors are willing to pay in order to avoid a gamble (an uncertainty), if it satisfies the following formula:

𝑢(𝑊0 − 𝑓 𝑊0, 𝐻 ) = 𝑝 𝑢 𝑊0 + 1 + 1 − 𝑝 𝑢(𝑊0 + 2)

then 𝑓 𝑊0, 𝐻 is called the Markowitz risk premium. 𝑊0 − 𝑓 𝑊0, 𝐻 is called the certainty equivalent wealth.

The greater the 𝑓 𝑊0, 𝐻 is, the more risk-averse the investor is.

2021/9/18 25

Example 6 Suppose that an investor is faced with a gamble as follows. His initial wealth is $10 and his utility function is a logarithmic function.

Q1:please calculate the penalty he is willing to pay for the gamble.

Q2: please calculate the certainty equivalent wealth.

0.8 5

10

0.2 30

2021/9/18 26

Absolute Risk Aversion Assuming that 𝑋 is a fair gamble

𝑢 𝑊0 − = 𝐸 𝑢(𝑊0 + 𝑋)

Use Taylor Expansion on the both sides of the equation when = 0 and 𝑋 = 0, we can get

= −1

2𝜎𝑋

2𝑢′′

𝑖(𝑊0)

𝑢′𝑖(𝑊0)

Apparently is always positive.

2021/9/18 27

Pratt-Arrow risk premium Definition 5:Consider a gamble with a level of risk, we can define Pratt-Arrow risk premium as follows,

𝑓 𝑊0, 𝐻 =1

2𝜎𝐻

2(−𝑢′′ 𝑊0

𝑢′ 𝑊0)

2021/9/18 28

Example 7 Consider a utility function: 𝑢 𝑧 = ln (𝑧)

0.5 19990

20000

0.5 20010

Please calculate the Markowitz risk premium and the Pratt-Arrow risk premium

2021/9/18 29

Example 8 Consider a utility function: 𝑢 𝑧 = ln (𝑧)

0.4 80

50

0.6 30

Please calculate the Markowitz risk premium and the Pratt-Arrow risk premium

2021/9/18 30

4. Absolute Risk Aversion and Relative Risk Aversion

Example 9. If the initial wealth of the three investors are all 100 yuan, the money they invest in risky assets are the same , e.g.,50 yuan.

When their wealth increases to 200 yuan, the amount of money they invest in risky assets is changed to 80 yuan, 30 yuan and 50 yuan, respectively.

Question:

How to judge their investment behavior?

2021/9/18 31

Absolute Risk Aversion Definition 6. Absolute risk aversion coefficient is define by

𝑅𝐴 𝑥 = −𝑢′′(𝑥)

𝑢′(𝑥) .

The absolute risk aversion coefficient can help us judge how the money investing in risky assets changes with the change of wealth.

The characteristic of an individual’s absolute risk aversion allow us to determine whether he treats a risky asset as a normal good when choosing between a single risky asset and a riskless asset.

2021/9/18 32

Absolute Risk Aversion Definition7: An individual’s utility function displays decreasing absolute risk aversion when 𝑅𝐴(z) is a strictly decreasing function ,

i. e. ,𝑑𝑅𝐴 𝑧

𝑑𝑧< 0, ∀𝑧 . Similarly,

𝑑𝑅𝐴 𝑧

𝑑𝑧> 0 , ∀𝑧, implies increasing

absolute risk aversion, and 𝑑𝑅𝐴 𝑧

𝑑𝑧= 0 , ∀𝑧 implies constant

absolute risk aversion.

2021/9/18 33

1. If 𝑅𝐴 . is a strictly decreasing function,i. e. , ∀𝑧, 𝑑𝑅𝐴 𝑧

𝑑𝑧< 0 ,then the investor is called

decreasing absolute risk averse

2. If 𝑅𝐴 . is a strictly increasing function, i.e., ∀𝑧, 𝑑𝑅𝐴 𝑧

𝑑𝑧> 0 ,then the investor is called

increasing absolute risk aversion

3.. If 𝑅𝐴 . is a linear function,i.e.,∀𝑧, 𝑑𝑅𝐴 𝑧

𝑑𝑧= 0 , then the investor is called constant absolute

risk aversion.

2021/9/18 FINANCIAL ECONOMICS 34

Arrow-Pratt Measure Obviously, a single utility function may display more than

one of the above characteristics over different parts of its domain.

Several interesting behavioral properties of utility

functions that display the same sign of 𝑑𝑅𝐴 𝑧

𝑑𝑧 over the

entire domain of 𝑅𝐴 . were derived by Arrow (1970).

2021/9/18 35

Absolute Risk Aversion Arrow showed that decreasing absolute risk aversion over the entire domain of 𝑅𝐴 . implies that the risky asset is a normal good. For example, the (dollar) demand for the risky asset increases as the individual's wealth increases.

Increasing absolute risk aversion implies that the risky asset is an inferior good, and constant absolute risk aversion implies that the individual's demand for the risky asset is invariant with respect to his initial wealth. So we have the following theorem:

2021/9/18 36

Absolute Risk Aversion Theorem 1.

∀𝑧 ,𝑑𝑅𝐴 𝑧

𝑑𝑧< 0 ⇒

𝑑𝑎

𝑑𝑊> 0, ∀𝑊

∀𝑧 ,𝑑𝑅𝐴 𝑧

𝑑𝑧> 0 ⇒

𝑑𝑎

𝑑𝑊< 0, ∀𝑊

∀𝑧 ,𝑑𝑅𝐴 𝑧

𝑑𝑧= 0 ⇒

𝑑𝑎

𝑑𝑊= 0, ∀𝑊

2021/9/18 37

Example 9 If the initial wealth of the three investors are the same, for example, 100 yuan. The money they invest in risky assets are also same, for example, 50 yuan, respectively.

When their wealth increases to 200 yuan, the amount of money they invest in risky assets increases to 80 yuan, 100 yuan and 150 yuan.

Question:

How to judge their investment behavior?

2021/9/18 38

Absolute Risk Aversion The property of decreasing absolute risk aversion is related to the dollar demand for the risky asset.

Thus, an individual having a utility function displaying decreasing absolute risk aversion may actually increase, hold constant, or decrease the proportion of his wealth invested in the risky asset as his wealth increases.

2021/9/18 39

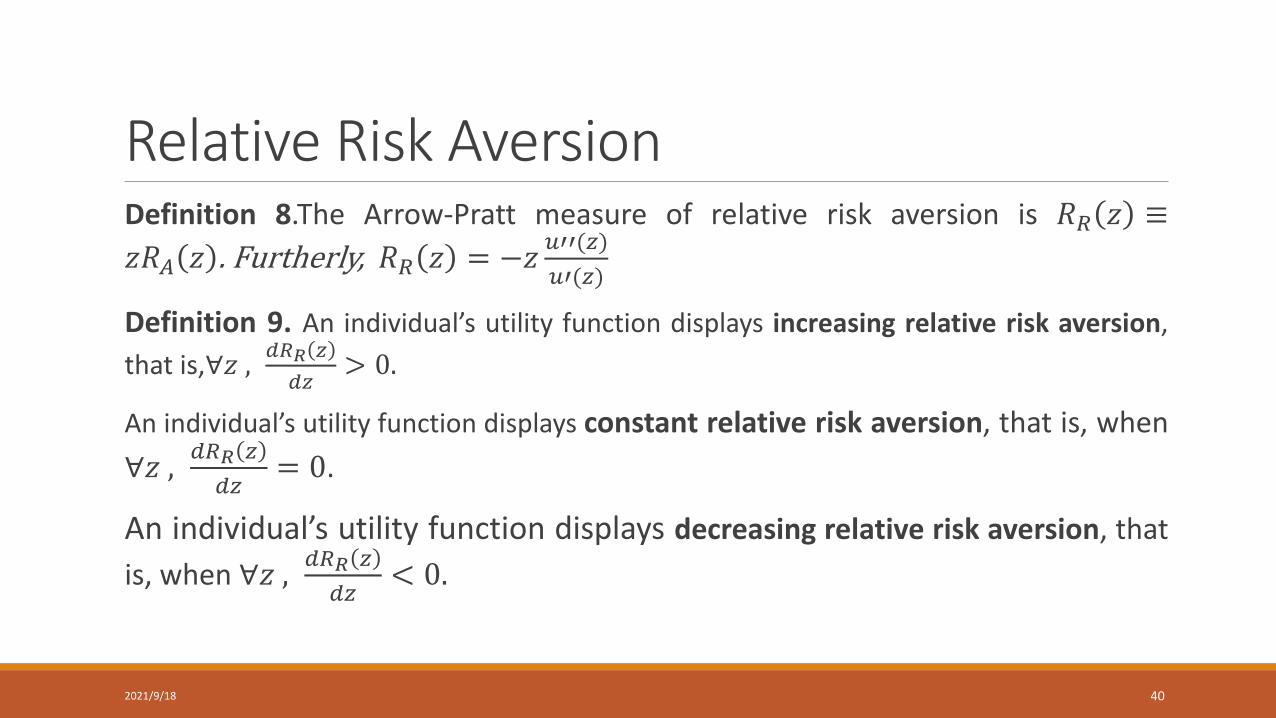

Relative Risk Aversion Definition 8.The Arrow-Pratt measure of relative risk aversion is 𝑅𝑅 𝑧 ≡

𝑧𝑅𝐴 𝑧 . Furtherly, 𝑅𝑅 𝑧 = −𝑧𝑢′′(𝑧)

𝑢′(𝑧)

Definition 9. An individual’s utility function displays increasing relative risk aversion,

that is,∀𝑧 ,𝑑𝑅𝑅 𝑧

𝑑𝑧> 0.

An individual’s utility function displays constant relative risk aversion, that is, when

∀𝑧 ,𝑑𝑅𝑅 𝑧

𝑑𝑧= 0.

An individual’s utility function displays decreasing relative risk aversion, that

is, when ∀𝑧 ,𝑑𝑅𝑅 𝑧

𝑑𝑧< 0.

2021/9/18 40

Relative Risk Aversion Theorem 2

① Under increasing relative risk aversion, that is, when ∀𝑧 ,𝑑𝑅𝑅 𝑧

𝑑𝑧> 0, the wealth elasticity of the individual's demand for the

risky asset is strictly less than unity.

That is, the proportion of the individual’s initial wealth invested in the risky asset will decline as his wealth increases.

2021/9/18 41

Relative Risk Aversion ② Under constant relative risk aversion, that is, when ∀𝑧 ,

𝑑𝑅𝑅 𝑧

𝑑𝑧= 0,

the wealth elasticity of demand for the risky asset would be unity.

③ Under decreasing relative risk aversion, that is, when ∀𝑧 ,𝑑𝑅𝑅 𝑧

𝑑𝑧< 0,

the wealth elasticity of the demand for the risky asset would be strictly greater than unity.

2021/9/18 42

Relative Risk Aversion Question:

What kind of risk aversion do investors belong to in reality?

It is generally accepted that most people are under decreasing absolute risk aversion and constant relative risk aversion.

2021/9/18 43

Note:

The above two theorems are only limited to the cases that depend upon the fact that there are only two assets, one risky and one riskless.

When there are multiple risky assets, the above conclusions aren’t always tenable.

2021/9/18 44

1.27 When there is more than one risky asset, in general we cannot say, for example, that the wealth elasticities of the demands for risky assets are greater than unity when an individual exhibits decreasing relative risk aversion.

When an investor's initial wealth increases, he may want to change his portfolio composition of the risky assets such that the investment in one risky asset increases while the investment in another decreases.

2021/9/18 45

Therefore, is there some assumptions tenable so that under these assumptions, individuals only change the mix between that portfolio and the riskless asset for differing levels of initial wealth?

2021/9/18 46

Two Fund Monetary Separation

The individual's optimal portfolios for differing levels of initial wealth are always linear combinations of the riskless asset and a risky asset mutual fund. This phenomenon is termed Two Fund Monetary Separation.

2021/9/18 47

2021/9/18 FINANCIAL ECONOMICS 48

The following utility functions are usually used to explain the nature of risk aversion in finance.

① Concave quadratic utility function

𝑢 𝑧 = 𝑧 −𝑏

2𝑧2 , 𝑏 > 0

What kind of absolute risk aversion does the quadratic utility function display?

(decreasing, increasing or constant)

2021/9/18 49

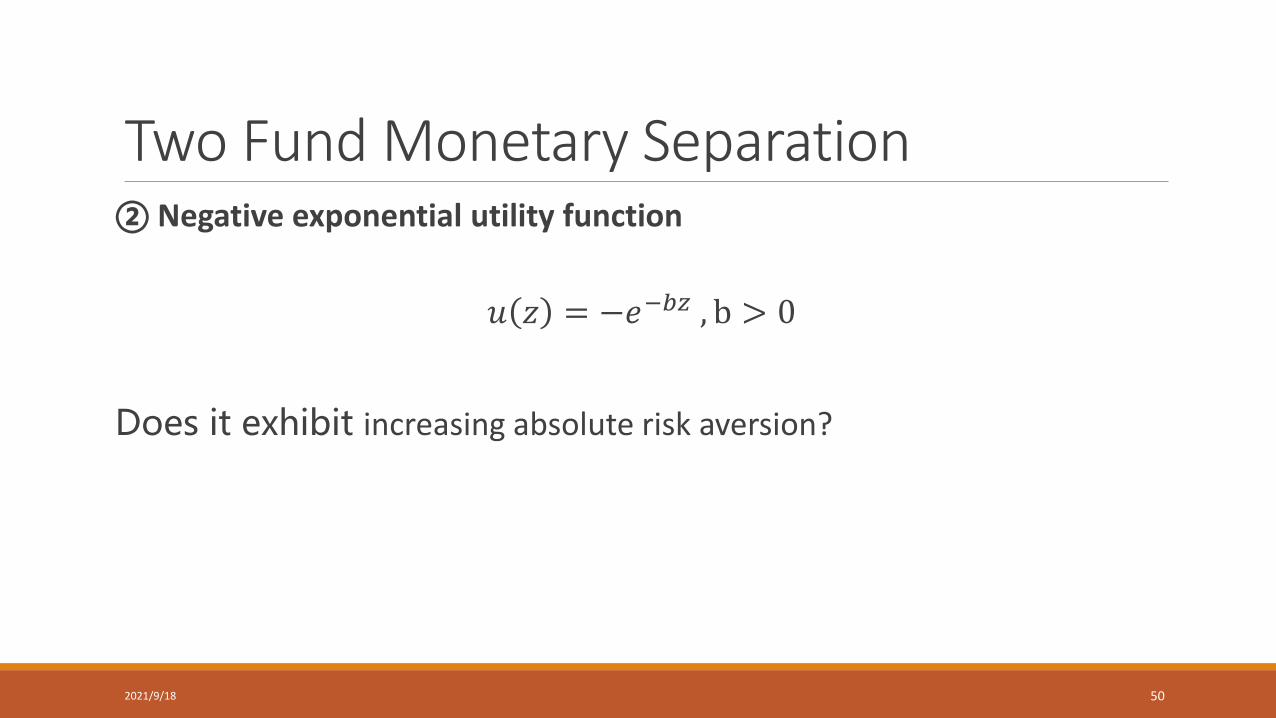

Two Fund Monetary Separation ② Negative exponential utility function

𝑢 𝑧 = −𝑒−𝑏𝑧 , b > 0

Does it exhibit increasing absolute risk aversion?

2021/9/18 50

Two Fund Monetary Separation ③ Extended power utility function

𝑢 𝑧 =1

𝐵 − 1(𝐴 + 𝐵𝑧)1−

1𝐵 , 𝐵 > 0, 𝑧 > max(−

𝐴

𝐵, 0)

Does it exhibit the decreasing absolute risk aversion or the decreasing relative risk aversion?

2021/9/18 51

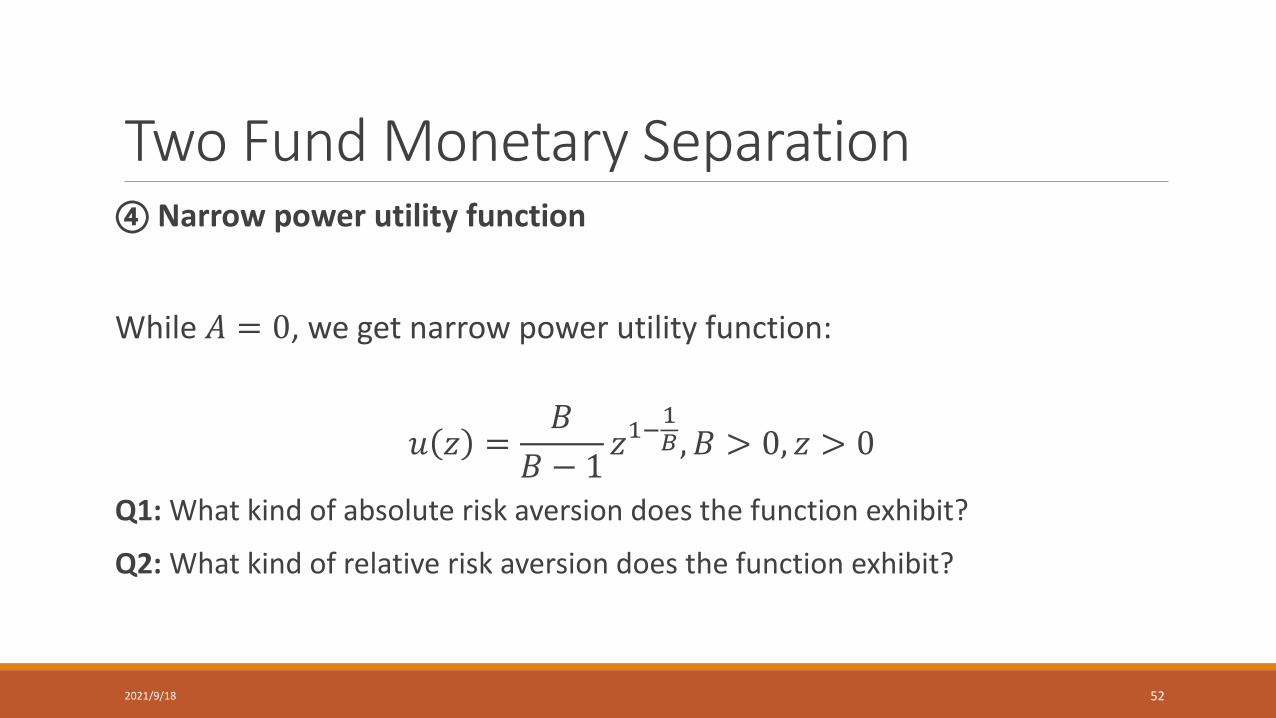

Two Fund Monetary Separation ④ Narrow power utility function

While 𝐴 = 0, we get narrow power utility function:

𝑢 𝑧 =𝐵

𝐵 − 1𝑧1−

1𝐵 , 𝐵 > 0, 𝑧 > 0

Q1: What kind of absolute risk aversion does the function exhibit?

Q2: What kind of relative risk aversion does the function exhibit?

2021/9/18 52