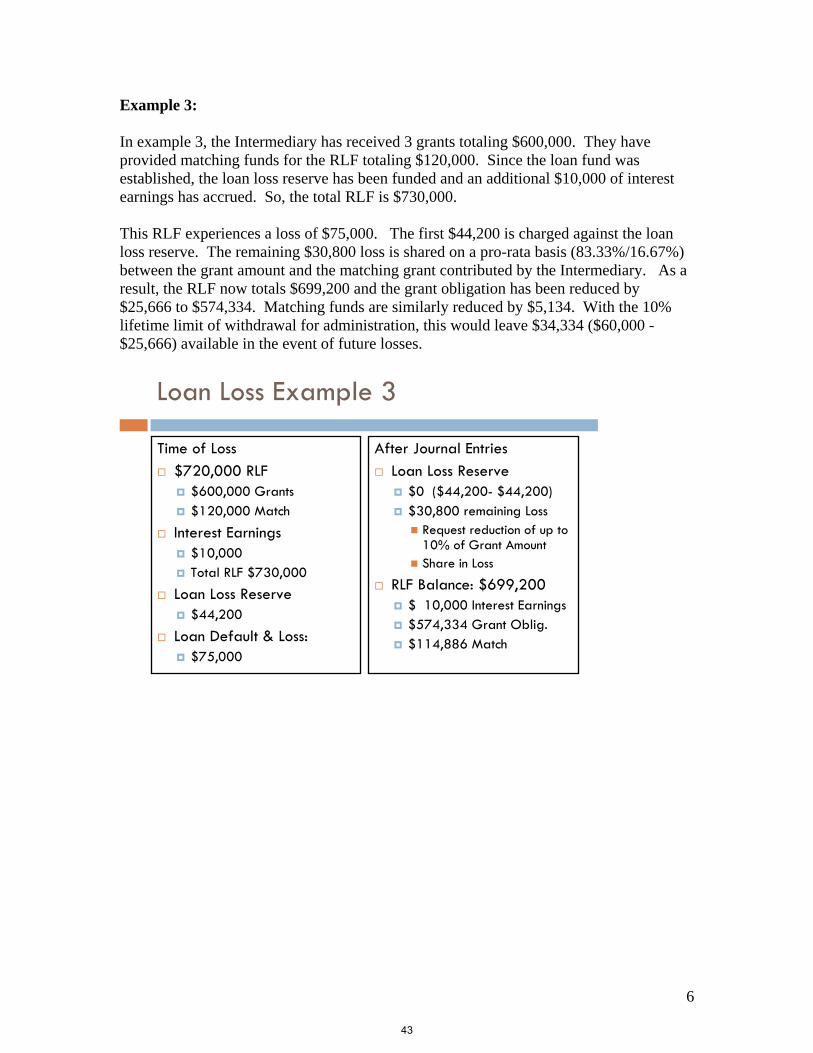

handouts - iowa economic development | iowa area … workshop... · 2015-12-01 · page 2 of 2...

TRANSCRIPT

Handouts

You've Got a Revolving

Loan Fund, Now What?

You’ve Got a Revolving Loan Fund, Now What?

Page

1.A. RD AN 4640………………………………………………………………………………………………………………. 3

1.B. Letter of Credit………………………………………………………………………………………………………… 5

1.C. RUS Reporting Memo September 5, 2013……………………………………………………………….. 7

1.D. RLF Plan…………………………………………………………………………………………………………………… 9

2.A. Collateral Agreement………………………………………………………………………………………………. 18

2.B. Financial Statement Analysis……………………………………………………………………………………. 21

2.C. RLF Application…………………………………………………………………………………………………………. 23

2.D. Civil Rights Data Request…………………………………………………………………………………………. 29

2.E. Sample Commitment Letter…………………………………………………………………………………….. 30

2.F. Sample Withdrawal Letter……………………………………………………………………………………….. 32

2.G. Sample Rejection Letter…………………………………………………………………………………………… 33

2.H. Loan Approval Summary Sheet…………………………………………………………………………………. 34

2.I. Loan File Checklist – Mortgage…………………………………………………………………………………… 35

2.J. Loan File Checklist – Equipment…………………………………………………………………………………. 36

2.K. Accounting MOU………………………………………………………………………………………………………. 37

3.A. DUNS Notification to Ultimate Recipients…………………………………………………………………. 46

3.B. DUNS Registration Steps……………………………………………………………………………………………. 47

3.C. SAM Registration……………………………………………………………………………………………………….. 49

3.D. SAM Renewal…………………………………………………………………………………………………………….. 50

3.E. USDA Servicing Visit Guide………………………………………………………………………………………….. 51

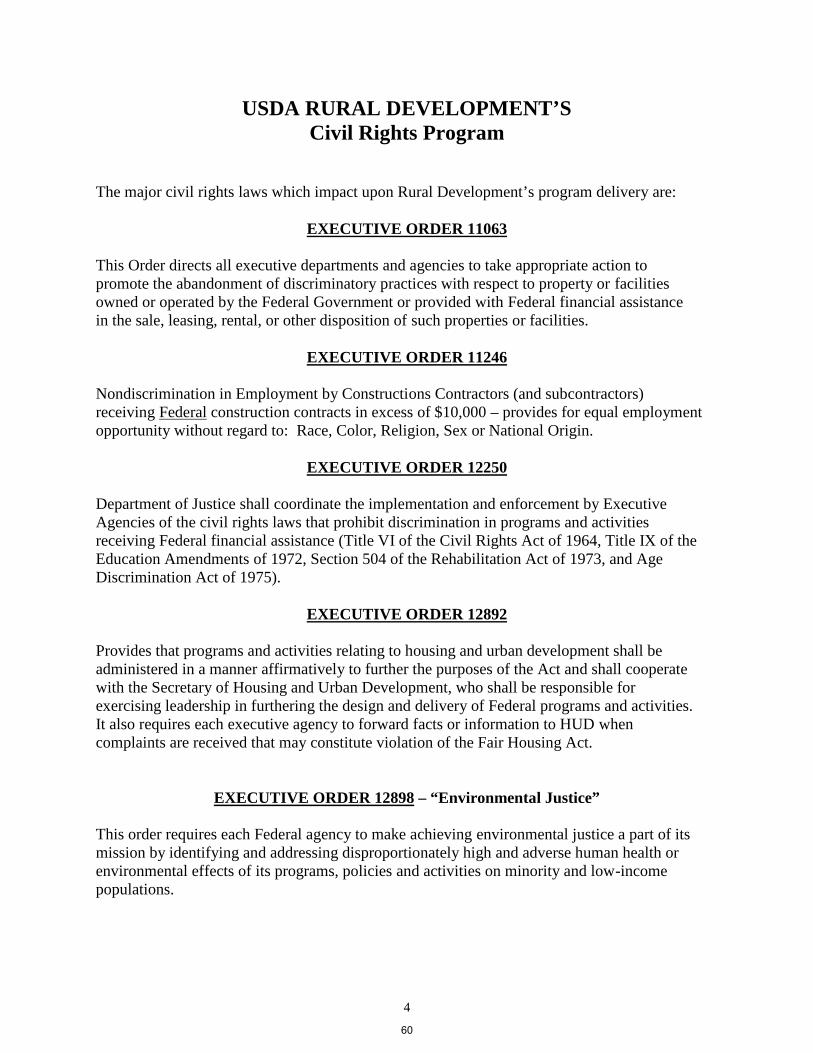

3.F. Major Civil Rights Laws……………………………………………………………………………………………….. 57

3.G. Assurance Agreement (400-4)……………………………………………………………………………………. 62

3.H. Compliance Review (400-8)………………………………………………………………………………………… 63

3.I. Non-Discrimination Statement…………………………………………………………………………………….. 72

3.J. EOC Tracking Tools………………………………………………………………………………………………………. 73

INDEX

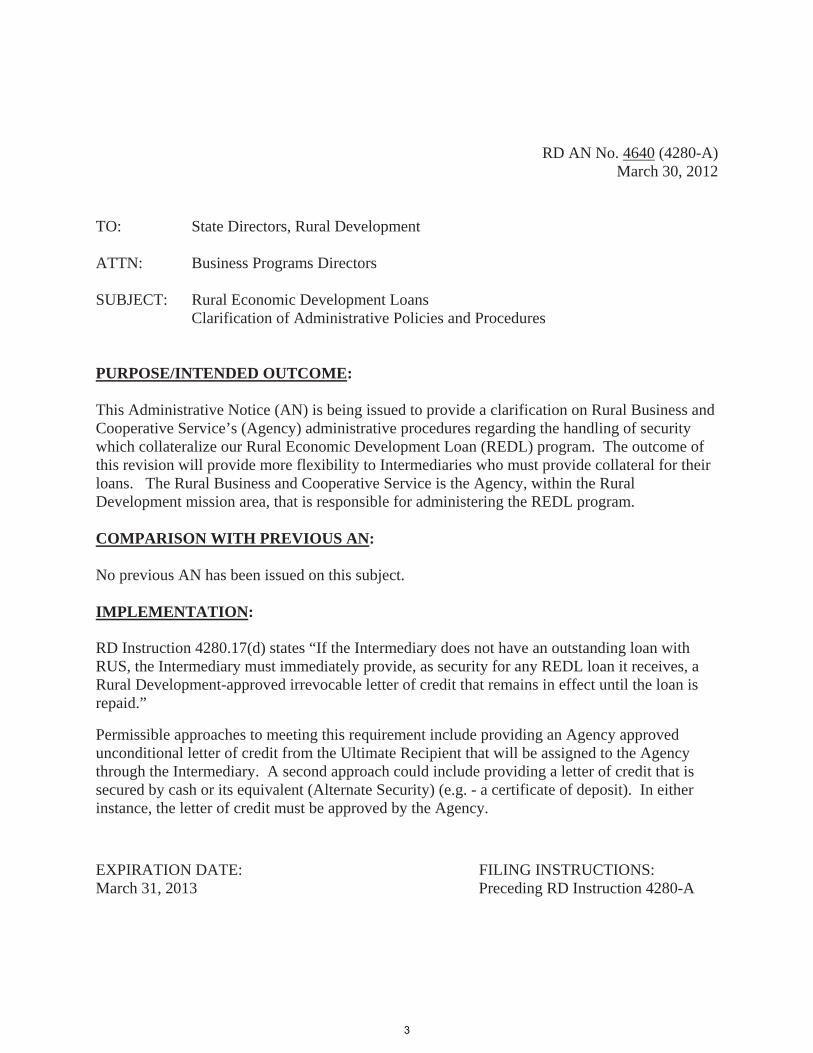

RD AN No. 4640 (4280-A) March 30, 2012

TO: State Directors, Rural Development

ATTN: Business Programs Directors

SUBJECT: Rural Economic Development Loans Clarification of Administrative Policies and Procedures

PURPOSE/INTENDED OUTCOME:

This Administrative Notice (AN) is being issued to provide a clarification on Rural Business and Cooperative Service’s (Agency) administrative procedures regarding the handling of security which collateralize our Rural Economic Development Loan (REDL) program. The outcome of this revision will provide more flexibility to Intermediaries who must provide collateral for their loans. The Rural Business and Cooperative Service is the Agency, within the Rural Development mission area, that is responsible for administering the REDL program.

COMPARISON WITH PREVIOUS AN:

No previous AN has been issued on this subject.

IMPLEMENTATION:

RD Instruction 4280.17(d) states “If the Intermediary does not have an outstanding loan with RUS, the Intermediary must immediately provide, as security for any REDL loan it receives, a Rural Development-approved irrevocable letter of credit that remains in effect until the loan is repaid.”

Permissible approaches to meeting this requirement include providing an Agency approved unconditional letter of credit from the Ultimate Recipient that will be assigned to the Agency through the Intermediary. A second approach could include providing a letter of credit that is secured by cash or its equivalent (Alternate Security) (e.g. - a certificate of deposit). In either instance, the letter of credit must be approved by the Agency.

EXPIRATION DATE: FILING INSTRUCTIONS: March 31, 2013 Preceding RD Instruction 4280-A

3

Rural Economic Development Loans 2

Under the second approach, it will be up to the State Office where the project is located to determine, on a case-by-case basis, whether the Alternate Security is warranted and acceptable. If Alternate Security is warranted the following additional requirements have to be met:

1. Prior to the disbursement of funds, the State Office will need a signed opinion letter from theIntermediary’s legal counsel that the Alternate Security pledged as collateral for the Letter ofCredit is legally enforceable in the State where the project is located. The opinion letter willalso certify that the Alternate Security is irrevocably pledged as collateral for the entire termof the loan and the Agency will be the first lien holder on the Alternate Security subject onlyto those liens approved by the Agency.

2. A Regional Office of the General Counsel (OGC) review is not required with theIntermediary’s legal counsel opinion, except in situations where the Agency ApprovalOfficial determines there are legal issues with the opinion that should be addressed by OGC.Any other type of Alternate Security offered as collateral for the Letter of Credit that is notcash or its equivalent must be approved by the National Office. When in doubt, you shouldconsult the National Office.

Any questions or comments, please contact Robert Fry, Loan and Grant Analyst, Specialty Programs Division, at (202) 690-2387.

(Signed by Judith A. Canales)

JUDITH A. CANALES Administrator Business and Cooperative Programs

4

Page 1 of 2

IRREVOCABLE STANDBY LETTER OF CREDIT

ISSUER: DATE: __________, 20___________________ Bank__________________________________________

BENEFICIARIES: Amount: $___________.00________________ Rural Electric Cooperative__________________________________________

USDA Rural Development_______________________________________________________________

ACCOUNT PARTY/APPLICANT:_______________________________________________________________

We, ___________________ BANK, hereby establish this Irrevocable Standby Letter ofCredit (Letter of Credit) No. in favor of the Beneficiaries in the amount of_____________________ Dollars and No/100 ($________________.00). This Letter of Creditis available with us at our above office by payment of a Beneficiary’s draft drawn on us at sightand shall expire on ______________, 20____, unless sooner renewed or continued.

Beneficiaries may draw upon this Letter of Credit with a Draft (or Drafts), together withthe documentation noted below. Each Draft shall be signed on behalf of a Beneficiary andmarked, “Drawn under ________________ BANK Standby Letter of Credit No. ______ dated_______________, 20____”. The presentation of any draft shall reduce the amount availableunder this Letter of Credit by the amount of the draft.

Each Draft must be accompanied by the following:

1. A sight draft drawn by a beneficiary on Issuer.

2. Beneficiary’s Signed Statement reading as follows:

a. If being drawn by ___________________________ Rural ElectricCooperative: “We are drawing against Standby Letter of Credit No.______ as ____________________ has failed to comply with the termsand conditions of its ___________________ Agreement between it and____________________________ RURAL ELECTRICCOOPERATIVE”.

b. If being drawn by USDA Rural Development: “We are drawing againstStandby Letter of Credit No. ______ as ____________________ Rural

5

Page 2 of 2

Electric Cooperative has failed to comply with the terms and conditions ofits ___________________ Agreement between it and USDA RuralDevelopment”.

The amount of this Letter of Credit shall reduce in value [quarterly/annually] beginning_______________, 20____, as the Promissory Note executed by the Account Party/Applicant infavor of the Beneficiary __________________ Rural Electric Cooperative. The Letter of Creditvalue will reduce by the amount of the [quarterly/annual] payments due under said Note;however, the reduction shall lag behind the actual payments by one [quarter/year]. (Forexample, if payments in the amount of $40,000 are due each quarter or year, the balance of theletter of credit shall reduce by $40,000 at the end of the second quarter/year and by the sameamount each succeeding quarter/year).

Partial and multiple drawings are permitted.

This Letter of Credit expires at our above office on _______________, 20___, but shallbe automatically extended, without written amendment, for a 12 month term ending_______________ in each succeeding calendar year unless the Beneficiaries have receivedwritten notice sent by us, the Issuer. This notice will be sent to the Beneficiaries at their addressabove by registered mail or express courier indicating that we elect not to extend the expirationdate of this Letter of Credit beyond the date specified in such notice. This date, whether_________________, 20___ or any subsequent ________________ shall be at least sixty (60)calendar days after the date the Beneficiaries receive such notice.

Upon a Beneficiary receiving such notice of the non-extension of the expiration date ofthis Letter of Credit, the Beneficiary may also draw under this Letter of Credit by presentation tous at our above address, on or before the expiration date specified in such notice, of a draft drawnon us at sight accompanied by a signed and dated statement worded as 1. and 2. above.

Unless otherwise stated, all documents are to be presented for payment at____________________ Bank, ____________________________________.

We hereby agree with you, the beneficiaries, that each drawing presented hereunder infull compliance with the terms hereof will be duly honored by our payment to the Beneficiarymaking the demand of the amount of such demand.

This Letter of Credit shall be governed by the laws of the State of Iowa and the UnitedStates of America.

ISSUER: _____________________ BANK__________________________________________

By: _______________________________ Date: ___________, 20Name:Title:

6

USDA is an equal opportunity provider and employer.

If you wish to file a Civil Rights program complaint of discrimination, complete the USDA Program Discrimination Complaint Form, found online at http://www.ascr.usda.gov/complaint_filing_cust.html, or at any USDA office, or call (866) 632-9992 to request the form. You may also write a letter containing all of the information requested in the form. Send your completed complaint form or letter to us by mail at U.S. Department of Agriculture, Director, Office of Adjudication, 1400 Independence Avenue, S.W., Washington, D.C. 20250-9410, by fax (202) 690-7442 or email at [email protected].

Rural Development

Rural Utilities Service

1400 Independence Ave SW, Stop 1510 Washington, DC 20250

Voice 202.720.9540 Fax 202.720.1725

September 5, 2013

To: All Electric Program Borrowers

Subject: Adjustment of Certain Financial Ratios when Electric Cooperatives are Involved in Rural Utilities Service Relending Activities

As the Administrator for the USDA, Rural Utilities Service I am committed to improving the quality of life and economic stability as it affects rural utilities and their consumers. This includes a strong concern for rural communities. I have traveled through your service areas over the past several months and had the opportunity to speak with so many of you. I have learned that you also share my concern for the rural American community. It is difficult to be successful if those rural communities are not healthy and economically strong.

RUS can benefit rural communities through our partnerships with the Rural Economic Development Loan and Grant Program, the Intermediary Relending Program, and the Rural Utilities Services Proposed Energy Efficiency and Conservation Loan Program.

I understand that there may be some issues within the Rural Utilities Program reporting requirements that may discourage your participation in opportunities to improve the quality of life and the economic stability of your service areas. Therefore, I have worked with my staff to take the following steps and ensure that these issues do NOT hinder our efforts and partnership to address our concern for rural American communities. I will continue to work with my staff to ensure that the appropriate changes to our annual financial and operating reports reflect the changes identified, with the goal to implement these changes for the 2013 calendar year reporting period.

RUS borrowers would have the option to continue following current annual financial reporting procedures, or, they may choose, strictly for RUS reporting purposes and requirements only, to use the revised process as described below:

1. Exclude assets and liabilities associated with Rural Development relendingactivities from the equity ratio and debt service coverage calculation so longas the third party obligor on such loans is performing or credit supportfacilities are in place to ensure performance. These liabilities would includeloans from USDA’s Rural Economic Develop Loan and Grant Program,Intermediary Relending Program, and energy efficiency relending activities.

7

2

2. Provide a note, within the annual financial and operating reports, that identifies the totalfunds associated with these activities. These total funds will be excluded from the RUSdebt service coverage and equity calculations.

Specific guidance on this procedure will be provided as part of the Data Collection System instructions for calendar year 2013 reporting.

The Rural Utilities Service continues to be proactive in identifying ways to become more efficient, by eliminating unnecessary procedures and processes, and improving our means to become more automated in our application and underwriting to be more effective for our borrowers. We are looking at new rules and programs in energy efficiency proposed rules on rural determinations, project financing, and expanding our reach into emerging bioeconomy and renewable markets. All of these efforts will help us transition to where we need to be in order to maximize the benefits to rural America. Our effort to adjust certain financial ratios for electric cooperatives involved in relending activities is one way to address our concern for community.

Sincerely,

John C. Padalino Administrator Rural Utilities Service

8

1

Insert Name of RLF Intermediary

REVOLVING LOAN FUND PLAN

INTRODUCTION AND OBJECTIVE:Insert Name of Intermediary (REC/TELCO/MUNI) has played an active role in the development of ruralIowa. Through its board and staff, the REC/TELCO/MUNI has provided not only leadership butfinancial participation in economic and community development. Now, through the creation of aRevolving Loan Fund (RLF), the REC/TELCO/MUNI is seeking to improve the quality of life in ruralareas by contributing to the long-term improvement in the economy, including job creation and retention,diversification of the economy, improving the education and skills of the rural workforce, and upgradingthe public infrastructure to improve the health, safety, and/or medical care of rural residents.

POLICY STATEMENTS: The REC/TELCO/MUNI will accept and consider applications for loans from the RLF for

projects that will significantly benefit rural areas, without restriction to the REC/TELCO/MUNI’sservice area.

The RLF seeks to minimize its financial participation in all projects. The RLF is not intended tocompete with other public and private lenders. The RLF will collaborate with other lenders toprovide the financial package necessary to advance the project, but at the same time to minimizethe RLF financing component.

The Board of Directors of the REC/TELCO/MUNI is the sole authority for approval or denial ofloans from the RLF and is responsible for all decisions and actions of the RLF. The RLF will beoperated and maintained solely by the REC/TELCO/MUNI.

To avoid potential conflicts of interest, or the appearance of a conflict of interest, an RLF loanwill not be made to any board member, officer, general manager, or supervisory employee of theREC/TELCO/MUNI or close relative thereof, or to any REC/TELCO/MUNI subsidiary oraffiliated organization in which the REC/TELCO/MUNI has a financial interest.

The REC/TELCO/MUNI will not condition the approval of a loan from the RLF with therequirement that the prospective recipient purchase electrical or telephone service from theREC/TELCO/MUNI or any other electrical/telephone utility.

Amendments to this Rural Development Plan will require the approval of theREC/TELCO/MUNI board of directors. However, no action will be taken to amend this planwithout the prior written approval of the Rural Business Cooperative Service (RBS), itssuccessors or assigns.

The REC/TELCO/MUNI RLF is an equal opportunity lender and requires loan recipients toadhere to all equal opportunity laws.

All information regarding RLF loan requests will at all times be kept confidential by the membersof the REC/TELCO/MUNI board, the loan review committee, and REC/TELCO/MUNI staff. Ifnecessary, the RLF may seek the advice and counsel of outside consultants and sources in orderto adequately perform due diligence regarding the project.

9

2

REVOLVING LOAN FUND MANAGEMENT:

Administration of the Revolving Loan FundManagement of the RLF will be “in house” by REC/TELCO/MUNI staff in addition to theirregular responsibilities, although other community resources may be used. With prior writtenapproval of RBS, up to, but, not more than 10% of the grant funds received shall be used for RLFadministration.

Loan Review CommitteeThe REC/TELCO/MUNI board of directors has appointed a Loan Review Committee (LRC),consisting of both cooperative and community leaders, to review all RLF loan applications. TheLRC will perform necessary credit analysis and due diligence in order to make a writtenrecommendation to the REC/TELCO/MUNI board of directors, which has final authorityregarding all actions of the RLF. The LRC will meet on an as needed basis under the terms of theapplication procedures listed below.

The Loan Review Committee serves on a volunteer basis. The LRC will have a minimum of 3members and a maximum of 7 members. If a member of the LRC has a financial interest in theproject being reviewed, he/she will abstain from the loan review/recommendation to theREC/TELCO/MUNI Board of Directors. Members of the LRC will serve indefinite terms.However, the REC/TELCO/MUNI board of directors has the right to replace members of theLRC in the event of resignation or other necessary circumstances.

The Loan Review Committee members were chosen, in part, because of their experience withlending and/or economic and community development projects. Initial members of the LoanReview Committee are:

Name Company Title1.2.3.4.5.

A current and up to date roster of the members of the LRC will be attached to this RuralDevelopment Plan as new members are appointed. These committee appointments do not reflectan amendment to the RLF Plan and therefore do not have to be approved by USDA.

10

3

REVOLVING LOAN FUND GUIDELINESInitial LoanThe initial loan of "Federal Funds" can be made to eligible entities for qualifying communitydevelopment or community facility projects in rural areas of the State of Iowa.

Eligible entities for initial funds include: non-profit organizations, public bodies, orFederally-recognized Indian Tribes.

Qualifying projects include community development or community facility projectswhich correspond to one or more of the following targets:

o Create or save employment; are open to and serve all rural residents; and areowned by the ultimate recipient of funds.

o Business Incubators.o Facilities and equipment which provide education and training to residents of

rural areas which will facilitate economic development.o Facilities and equipment to provide medical care to residents of rural areas.o Projects that utilize advanced telecommunications or computer networks to

facilitate medical or education services or job training.o Project feasibility studies and technical assistance.

Interest Rate: The initial loan of the Federal Funds will be made at zero percent.

Administration Fee: An annual loan servicing fee of up to 1% of the unpaid principalloan balance may be charged for loan administration.

Subsequent Loans / Revolved RLF Funds:In general, eligible projects for subsequent loans can include any business venture, governmentalpublic body, or non-profit entity involved in a community or economic development project thatcreates or saves jobs and/or provides needed community facilities that benefit rural areas in theState of Iowa.

Eligible Applicants include:o Corporationso Limited Liability Companieso Partnershipso Sole Proprietorshipso Cooperativeso Nonprofit Entitieso Governmental Units, including: Local Townships, Municipalities, County

Government, Regional Authorities, School Districts, and City or CountyHospitals

o Federally-recognized Tribal Authorities

11

4

Application projects must create or retain employment or provide needed communityfacilities and services such as:

o Industrial/Commercial Developmento Small Business Expansion or Startupo Business Incubatorso Community Infrastructureo Community Facilitieso Medical Facilitieso Training/Educational Facilitieso Tourism

Loan PurposesUses of RLF loan proceeds may be for land, buildings, manufacturing machinery andequipment, office and work equipment or infrastructure improvements. Working capitalloans will only be considered in conjunction with the purchase of other assets aspreviously specified.

In an effort to promote National energy priorities, energy efficiency upgrades / renewableenergy projects at commercial businesses are an eligible purpose for revolved RLF funds.

Special Loan Limits—Residential Housing ProjectsRecognizing the link between economic development, workforce availability and housingdevelopment and in accordance with USDA program limits, up to 20% of the RLF (anamount equal to the REC/TELCO/MUNI “matching funds”) may be used for residentialhousing projects. Please note, consumer financing of a residence is not permitted.

In-Eligible Uses of RLF Funding:o Refinancing of existing debt, or payment to business owners or partners;o Projects without any supplemental financing;o Activities determined to be for investment purposes;o General improvement loans related to normal replacement needs of a business and

unrelated to business expansion/job creation unless related to energy efficiency asstated above;

o Projects that would result in the transfer of existing employment or business activitymore than 25 miles from its existing location;

o Agricultural production except where the project is a farmer-owned cooperative orsimilar, and the agriculture production is part of an integrated business that processesthe agriculture products, and the agriculture production portion of the loan will notexceed 50% of the loan amount;

o Projects that are primarily working capital with limited security and/or without othercapital purchases as part of the project;

o Construction projects of an individual residential nature;o Vehicles used for general purposes or that may be considered for personal use;o Illegal activities and legalized activities (e.g. gambling casinos) that in the opinion of

the Board of Directors adversely affect RLF interests;o Projects in which any director, officer, general manager, or supervisory employee of

the Intermediary, or close relative thereof, has a financial interest; projects in whichany subsidiary or affiliated organization of Intermediary has a financial interest; orprojects which, based on the judgment of the Board, would create a conflict ofinterest, potential for conflict of interest, or any appearance of a conflict of interest.

12

5

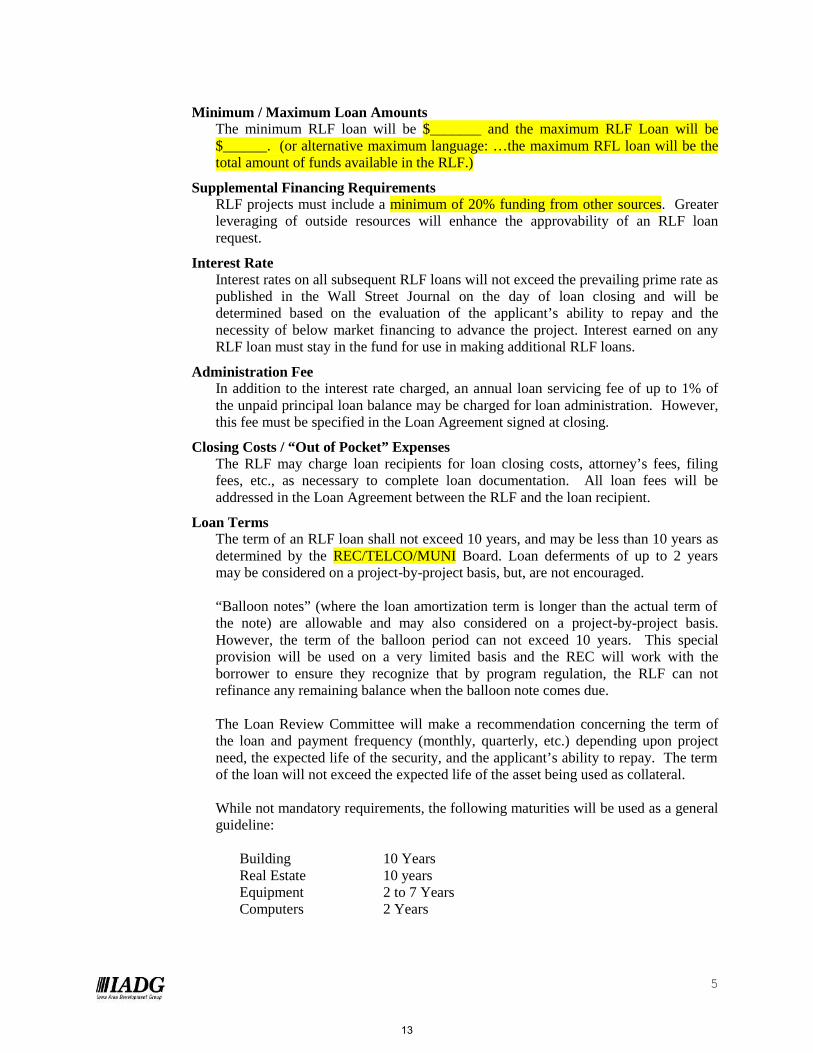

Minimum / Maximum Loan AmountsThe minimum RLF loan will be $_______ and the maximum RLF Loan will be$______. (or alternative maximum language: …the maximum RFL loan will be thetotal amount of funds available in the RLF.)

Supplemental Financing RequirementsRLF projects must include a minimum of 20% funding from other sources. Greaterleveraging of outside resources will enhance the approvability of an RLF loanrequest.

Interest RateInterest rates on all subsequent RLF loans will not exceed the prevailing prime rate aspublished in the Wall Street Journal on the day of loan closing and will bedetermined based on the evaluation of the applicant’s ability to repay and thenecessity of below market financing to advance the project. Interest earned on anyRLF loan must stay in the fund for use in making additional RLF loans.

Administration FeeIn addition to the interest rate charged, an annual loan servicing fee of up to 1% ofthe unpaid principal loan balance may be charged for loan administration. However,this fee must be specified in the Loan Agreement signed at closing.

Closing Costs / “Out of Pocket” ExpensesThe RLF may charge loan recipients for loan closing costs, attorney’s fees, filingfees, etc., as necessary to complete loan documentation. All loan fees will beaddressed in the Loan Agreement between the RLF and the loan recipient.

Loan TermsThe term of an RLF loan shall not exceed 10 years, and may be less than 10 years asdetermined by the REC/TELCO/MUNI Board. Loan deferments of up to 2 yearsmay be considered on a project-by-project basis, but, are not encouraged.

“Balloon notes” (where the loan amortization term is longer than the actual term ofthe note) are allowable and may also considered on a project-by-project basis.However, the term of the balloon period can not exceed 10 years. This specialprovision will be used on a very limited basis and the REC will work with theborrower to ensure they recognize that by program regulation, the RLF can notrefinance any remaining balance when the balloon note comes due.

The Loan Review Committee will make a recommendation concerning the term ofthe loan and payment frequency (monthly, quarterly, etc.) depending upon projectneed, the expected life of the security, and the applicant’s ability to repay. The termof the loan will not exceed the expected life of the asset being used as collateral.

While not mandatory requirements, the following maturities will be used as a generalguideline:

Building 10 YearsReal Estate 10 yearsEquipment 2 to 7 YearsComputers 2 Years

13

6

Security / CollateralThe Intermediary will work with the potential loan recipient to obtain securitythat is adequate for the term of the loan. The nature of the collateral pledged shallbe determined by the loan committee on a project-by-project basis. If the samecollateral is used in joint financing, the RLF will seek a parity position with otherlenders. Types of security may include:

o Mortgage Lien on Real Propertyo Machinery and equipment which have a developed market;o Letter(s) of credit from acceptable financial institution(s);o Securities issued by the Federal government or its agencies.o Accounts receivable and inventory for short-term loans; and

The loan recipient will be required to maintain fire insurance, and floodinsurance if necessary, on secured assets. In some cases, credit life or key maninsurance will be required with the RLF as loss payee.

Personal guarantees from partners, directors or majority stockholders may berequired for all corporate or partnership borrowings.

APPLICATION PROCEDURESAll applicants for RLF funding will be required to complete an application form and provide acorresponding business plan with verifiable data which demonstrates that their proposed projects areeconomically feasible, sustainable, and will provide benefits to rural areas, either through job creation orinfrastructure improvements. A copy of the application which includes a list on supporting information isattached to this plan.

1. Applications will be accepted for review when the RLF has a minimum balance of $25,000.

2. Applications will be accepted at the REC/TELCO/MUNI office during normal businesshours. The REC/TELCO/MUNI is located at insert address.

3. (Staff position) of the REC/TELCO/MUNI will review applications for completeness andpresent complete applications to the loan review committee. An application is not consideredcomplete until all required information has been submitted to the REC/TELCO/MUNI staffas listed on the attached application.

4. The loan review committee will analyze each project and make a written recommendation tothe REC/TELCO/MUNI board of directors.

5. The REC/TELCO/MUNI Board of Directors will normally review RLF applications at theirscheduled monthly Board Meeting. However, if needed and at the Board’s option, the Boardmay call a special meeting to review a loan application.

6. The REC/TELCO/MUNI board of directors shall have final authority to approve or deny RLFloan requests, and to determine appropriate terms and conditions.

7. For approved loans, a loan agreement addressing all of the terms and conditions, includingmonitoring procedures, repayments, delinquencies, defaults and remedies for that project willbe prepared by the RLF. In addition, the RLF shall have prepared all notes, mortgages,security agreements, UCC filings and other legal documents necessary to close the loan. The

14

7

RLF will use appropriate note, mortgage, and other forms which are approved by the State ofIowa Bar Association.

8. Before RLF funds can be disbursed to the loan recipient, all requirements and terms of theloan agreement must be met and supplemental financing must already be contributed orverified ready to contribute to the project.

Review CriteriaThe basis for determining the eligibility/approvability, loan amount, interest rate, and terms andconditions of a revolving loan fund request, and general RLF operational procedures, are asfollows:

The loan review committee and REC/TELCO/MUNI board will consider the financial need of theproject, the probability of success, the security offered, and the overall benefits of the project torural areas, including the number of jobs to be created or retained, diversification of the economy,the extent of the upgrading of the skills of the rural workforce, the quality of the jobs in terms ofpay scale and benefit package, and, for community development projects, improvements to thecommunity infrastructure, facilities, and/or acquisition of equipment that improves the education,health, safety, and/or medical care of rural residents.

Loan MonitoringThe REC/TELCO/MUNI board of directors and/or the loan review committee shall monitor allRLF loans to ensure that loan proceeds are spent as identified in the RLF application, that allother sources of financing have been committed to the project, and that the benefits of the project,such as job creation, are accomplished as stated in the RLF application. The REC/TELCO/MUNIboard and/or LRC shall ensure that RLF lien positions and loan collateral are secure

This loan monitoring will require regular reporting by the loan recipient.

Annual income statements and balance sheets will be collected from the loan recipient.Depending on the nature of the project and security arrangements, the Intermediaryreserves the right to require the submission of annual financial reports as audited by acertified public accountant.

The Intermediary will also conduct periodic/annual site visits to meet with the loanrecipient, verify collateral and collect any information as required.

At the option of the Intermediary, periodic management information reports may berequired of the loan recipient. Management reports may be required on a semi-annualbasis beginning six months after the advance of RLF funds and continuing semi-annuallythereafter for a period of 3 years or until completion of the project, whichever is the laterperiod. If requested, management reports will include:

o information on the number of jobs created or retained during the reporting period;o a comparison of accomplishments during the reporting period to the objectives

established for the project,o a description of any problems, delays, or adverse conditions which will materially

affect the attainment of planned project objectives and a statement of action taken orcontemplated to resolve the situation.

The Intermediary reserves the right to require these reports on a more frequent basis if it isdetermined to be in the best interest of the RLF.

15

8

An annual review and report of the outstanding loans of the RLF, including job creation/retentiontotals and community benefits, will be compiled by the loan committee for presentation to theREC/TELCO/MUNI board of directors.

Collection ProceduresThe RLF Staff position is charged with the responsibility for loan collections and relatedworkouts, collection of charged-off loans, management and disposal of other real estate ownedand any other activities related to delinquent accounts.

As part of this responsibility, the RLF Staff position shall have authority to initiate foreclosures,and collection suits after consultation with the REC/TELCO/MUNI’s legal counsel. The RLFStaff position will advise the board of such action at their next regular meeting.

1. Past due notices will be generated and sent to the loan recipient according to thefollowing schedule:

o First notice sent on the 10th day after a note or payment is due.o Second notice sent on the 20th day after a note or payment is due.

2. If the delinquent account becomes 30 days delinquent, RLF Staff Position will makephone contact with the loan recipient to inquire about the situation and arrangeappropriate corrective action.

o As a prudent lender and at the intermediary’s sole discretion, a one-timecorrective action/workout of a delinquent account is permitted. As part of theworkout, loan terms may be modified by deferral, reamortization and/or balloonpayments. However, the term of the modified loan can not exceed a 10 yearperiod from the date of the original loan closing.

3. If the delinquent account is not taking steps to cure default and the account becomes 60days delinquent, a written 30 day Notice to Cure will be issued and sent to the loanrecipient via certified, first class mail with a return receipt requested.

4. If the delinquent account does not respond to the Notice to Cure by paying the amountstated in the cure notice, the file will be forwarded to REC/TELCO/MUNI’s legalcounsel to start foreclosure actions.

o As mentioned earlier, up to 10% of Rural Development Grant funds may beapplied toward operating expenses of the RLF over the life of the fund.Operating expenses include the costs of administering the RLF and technicalassistance provided to loan recipients by independent providers. Under theauthority of this section, costs of administering the RLF includes any costsrelated to collections and/or foreclosure of a delinquent account.

o The Intermediary will maintain an aggregated total of any and all relatedcollections / foreclosure costs which are charged against this 10% allowance.

16

9

File RetentionAll RLF files will be retained for a period of not less than 3 full years after the loan has been paidin full. After 3 years, the files will be destroyed by shredding or incineration. Files will be securedin a locked, safe place and access will be limited to Intermediary staff with RLF responsibilities.Other security measures will be initiated as needed to protect confidentiality of loan documents.

After review and official action, this RLF Plan is adopted by REC/TELCO/MUNI on Insert date

_____________________________Secretary

17

Page 1 of 3

SHARED COLLATERAL AGREEMENT

This Shared Collateral Agreement is entered into by and between ___________________and ___________________________ (sometimes referred to hereafter as “Lender” orcollectively as “Lenders”) regarding certain loans made to the ___________________________(“Borrower”).

RECITALS

WHEREAS, Borrower has borrowed $_____________ from __________________, andan aggregate amount of $________________ from ____________________ (evidenced byPromissory notes of $_____________ and $_______________); and

WHEREAS, Borrower has granted to ________________ a Mortgage on LegalDescription County, Iowa, in order to secure ________ loan in the amount of $_____________;a Mortgage to ___________ on Lots ______, Property Description County, Iowa, in order tosecure _________ loan in the amount of $______________; and a Mortgage to ____________on Lots _______, Legal Description County, Iowa, in order to secure _________ loan in theamount of $_______________; and,

WHEREAS, the Lenders have agreed to share a first priority position concerning thesubject real estate ("Property"), which is legally described as follows:

Legal Description

and all buildings, structures and improvements now standing or at any time hereafterconstructed or placed upon the Land (the "Buildings"), including all hereditament,easements, appurtenances, riparian rights, mineral rights, water rights, rights in and to thelands lying in streets, alleys and roads adjoining the land, estates and other rights andinterests now or hereafter belonging to or in any way pertaining to the Land;

and,

WHEREAS, Lenders agree to be bound by the terms and conditions of this CollateralAgreement.

IT IS, THEREFORE AGREED AS FOLLOWS:

1. DESCRIPTION OF LOANS AND MORTGAGES.

_____________ has loaned $_______________ to the Borrower, and the Borrower hasexecuted a Mortgage in favor of _____________, encumbering Property. Said Mortgage wasfiled in the records of the _______________County Recorder on ____________, 2009 asInstrument No. ___________________. __________________ has loaned $______________

18

Page 2 of 3

and $____________ (for a total of $______________) to Borrower, and Borrower has executedMortgages in favor of _____________, encumbering the Property. Said Mortgages were filed inthe records of the ______________County Recorder on ______________, 2009, as InstrumentNo. ___________________ and on ________________, 2009, as Instrument No.________________________.

2. SHARED PRIORITY POSITION WITH RESPECT TO THE COLLATERAL.

Lenders agree that the Lenders’ liens against the Property evidenced by the abovedescribed mortgages shall be a shared first priority position lien. In the event of a default underthe Loan Agreements, Promissory Notes, or Mortgages separately executed between theBorrower and the Lenders, the Lenders agree that their first priority position with respect to anyproceeds shall be determined by each Lenders’ respective unpaid loan balance at the time of saidforeclosure proceeding. Each Lender agrees to execute any other documentation in order toevidence the shared security position of the Lenders.

3. ACTION AGAINST COLLATERAL.

In the event either of the Lenders is unable to collect on their loans after exercisingreasonable efforts to do so, and the Lender desires to exercise its rights against the collateral, theLender agrees to give prompt notice to the other Lender prior to taking any action. To the extentaction is commenced against the collateral, each of the Lenders agree to share ratably in theincome and expense incurred during the collection process, including all necessary expensesincurred in payment of taxes, insurance premiums, waste prevention, repairs, maintenance,improvements, management, foreclosure, attorney’s fees, and other similar expenses, and eachLender agrees to pay promptly its proportion of any such expenses deemed to be appropriate.

IN WITNESS WHEREOF, the Parties have executed this Agreement on the date setbeside their signatures below.

LENDERS:

_____________________________________

_____________________________________

_________________________________

19

Page 3 of 3

STATE OF IOWA, _____________COUNTY, ss:

On this _______ day of ___________, 2009, before me, the undersigned, a Notary Publicin and for said County and State, personally appeared ________________ and_______________, who by me being duly sworn did say that they are the President andSecretary respectively of ________________________, and that no seal has been procured forsaid corporation ( the seal of said corporation is attached) and that the foregoing instrument wasexecuted by them on behalf of said corporation with full corporate authority to do so and theyacknowledged the execution of said instrument to be the voluntary act and deed of saidcorporation by it voluntarily executed.

__________________________________________Notary Public in and for said State

STATE OF IOWA, _________________ COUNTY, ss:

On this ________ day of ____________, 2009, before me, the undersigned, a NotaryPublic in and for said County and State, personally appeared ________________, who by mebeing duly sworn did say that he is the _______________ of ________________, and that noseal has been procured for said corporation (the seal of said corporation is attached) and that theforegoing instrument was executed by him on behalf of said corporation with full corporateauthority to do so and he acknowledged the execution of said instrument to be the voluntary actand deed of said corporation by it voluntarily executed.

__________________________________________Notary Public in and for said State

20

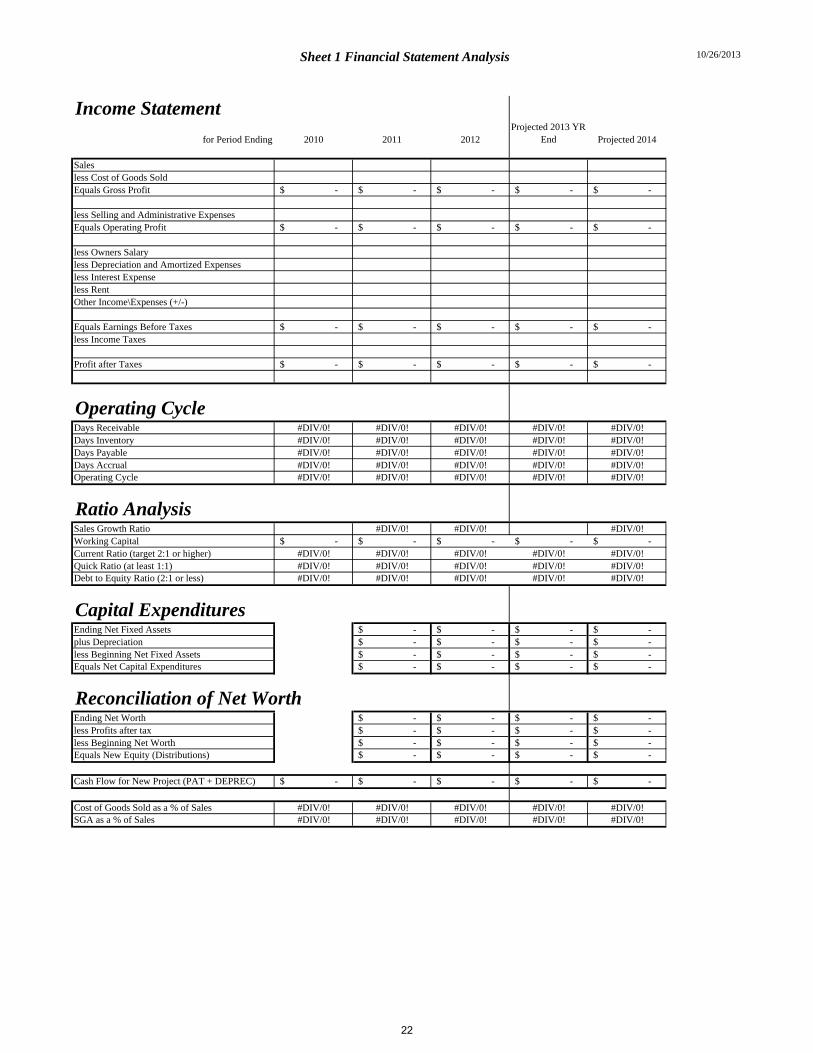

Sheet 1 Financial Statement Analysis 10/26/2013

2010 2011 2012Projected 2013 YR

End Projected 2014

Balance SheetAssets Year 1 Year 2 Year 3 Year 1 Year 2

Cash & Marketable SecuritiesAccount ReceivableInventoryPrepaid Expenses

Total Current Assets -$ -$ -$ -$ -$

Net Fixed AssetsNotes ReceivableInvestment in SubsidiariesIntangibles

Total Assets -$ -$ -$ -$ -$

Liabilities & Net Worth

Note Payable - BankNote Payable -OtherAccounts PayableAccrualsIncome Tax PayableCurrent Portion of Long Term DebtCustomer Deposits

Total Current Liabilities -$ -$ -$ -$ -$

Long Term DebtSubordinated Officer Debt

Total Liabilities -$ -$ -$ -$ -$

Net WorthCommon StockCapital Surplus & Paid in CapitalRetained Earnings(Less Treasury Stock)

Total Net Worth -$ -$ -$ -$ -$

Total Liabilities & Net Worth -$ -$ -$ -$ -$

21

Sheet 1 Financial Statement Analysis 10/26/2013

Income Statement

for Period Ending 2010 2011 2012Projected 2013 YR

End Projected 2014

Salesless Cost of Goods SoldEquals Gross Profit -$ -$ -$ -$ -$

less Selling and Administrative ExpensesEquals Operating Profit -$ -$ -$ -$ -$

less Owners Salaryless Depreciation and Amortized Expensesless Interest Expenseless RentOther Income\Expenses (+/-)

Equals Earnings Before Taxes -$ -$ -$ -$ -$less Income Taxes

Profit after Taxes -$ -$ -$ -$ -$

Operating CycleDays Receivable #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0!Days Inventory #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0!Days Payable #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0!Days Accrual #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0!Operating Cycle #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0!

Ratio AnalysisSales Growth Ratio #DIV/0! #DIV/0! #DIV/0!Working Capital -$ -$ -$ -$ -$Current Ratio (target 2:1 or higher) #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0!Quick Ratio (at least 1:1) #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0!Debt to Equity Ratio (2:1 or less) #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0!

Capital ExpendituresEnding Net Fixed Assets -$ -$ -$ -$plus Depreciation -$ -$ -$ -$less Beginning Net Fixed Assets -$ -$ -$ -$Equals Net Capital Expenditures -$ -$ -$ -$

Reconciliation of Net WorthEnding Net Worth -$ -$ -$ -$less Profits after tax -$ -$ -$ -$less Beginning Net Worth -$ -$ -$ -$Equals New Equity (Distributions) -$ -$ -$ -$

Cash Flow for New Project (PAT + DEPREC) -$ -$ -$ -$ -$

Cost of Goods Sold as a % of Sales #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0!SGA as a % of Sales #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0!

22

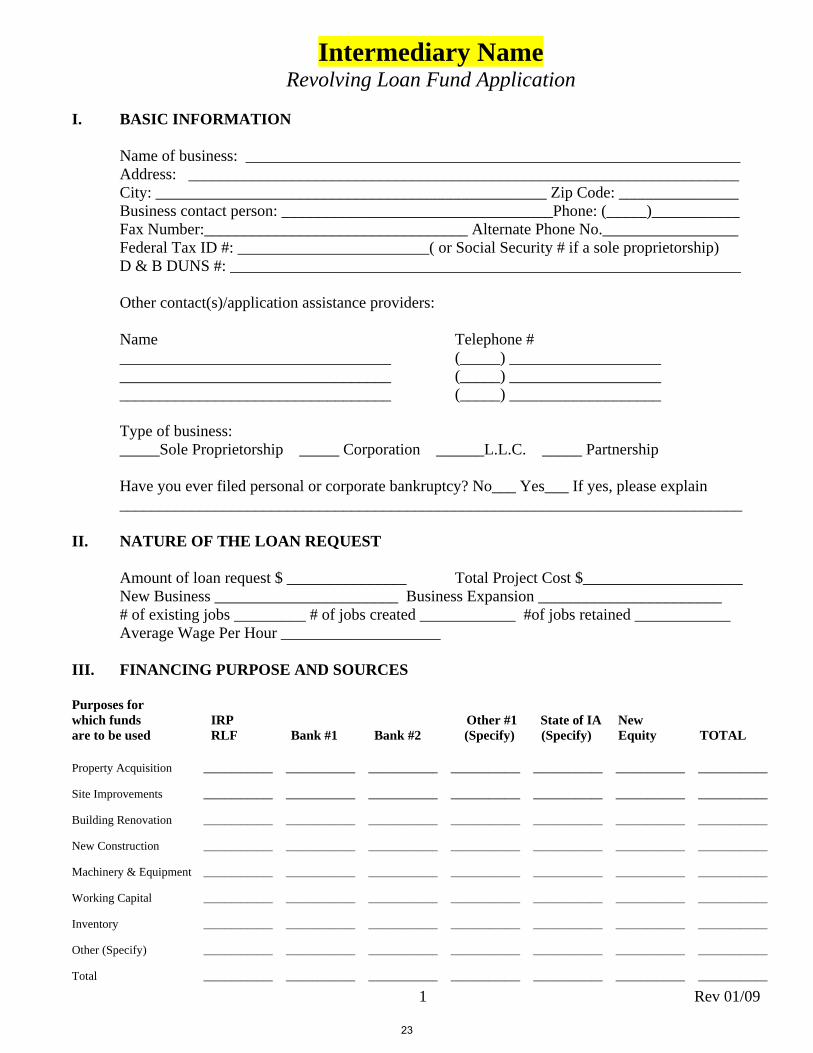

1 Rev 01/09

Intermediary Name Revolving Loan Fund Application

I. BASIC INFORMATION

Name of business: ______________________________________________________________ Address: _____________________________________________________________________ City: _________________________________________________ Zip Code: _______________ Business contact person: __________________________________Phone: (_____)___________ Fax Number:_________________________________ Alternate Phone No._________________ Federal Tax ID #: ________________________( or Social Security # if a sole proprietorship) D & B DUNS #: ________________________________________________________________

Other contact(s)/application assistance providers:

Name Telephone # __________________________________ (_____) _____________________________________________________ (_____) _____________________________________________________ (_____) ___________________

Type of business: _____Sole Proprietorship _____ Corporation ______L.L.C. _____ Partnership

Have you ever filed personal or corporate bankruptcy? No___ Yes___ If yes, please explain ______________________________________________________________________________

II. NATURE OF THE LOAN REQUEST

Amount of loan request $ _______________ Total Project Cost $____________________ New Business _______________________ Business Expansion _______________________# of existing jobs _________ # of jobs created ____________ #of jobs retained ____________Average Wage Per Hour ____________________

III. FINANCING PURPOSE AND SOURCES

Purposes for which funds IRP Other #1 State of IA New are to be used RLF Bank #1 Bank #2 (Specify) (Specify) Equity TOTAL

Property Acquisition _____________ _____________ _____________ _____________ _____________ _____________ _____________

Site Improvements _____________ _____________ _____________ _____________ _____________ _____________ _____________

Building Renovation _____________ _____________ _____________ _____________ _____________ _____________ _____________

New Construction _____________ _____________ _____________ _____________ _____________ _____________ _____________

Machinery & Equipment _____________ _____________ _____________ _____________ _____________ _____________ _____________

Working Capital _____________ _____________ _____________ _____________ _____________ _____________ _____________

Inventory _____________ _____________ _____________ _____________ _____________ _____________ _____________

Other (Specify) _____________ _____________ _____________ _____________ _____________ _____________ _____________

Total _____________ _____________ _____________ _____________ _____________ _____________ _____________

23

1 Rev 01/09

IV. FINANCING TERMS AND CONDITIONS

Other #1 Other #2 State of IA RLF Bank #1 Bank #2 (Specify) (Specify) Equity TOTAL

Amount _____________ _____________ _____________ _____________ _____________ _____________ _____________ % of Project Costs _____________ _____________ _____________ _____________ _____________ _____________ _____________ Term (years) _____________ _____________ _____________ _____________ _____________ _____________ _____________ Interest Rates _____________ _____________ _____________ _____________ _____________ _____________ _____________ Debt Service _____________ _____________ _____________ _____________ _____________ _____________ _____________

Collateral Offered: Asset _____________ _____________ _____________ _____________ _____________ _____________ _____________ Lien Position _____________ _____________ _____________ _____________ _____________ _____________ _____________

Collateral Offered: Asset _____________ _____________ _____________ _____________ _____________ _____________ _____________ Lien Position _____________ _____________ _____________ _____________ _____________ _____________ _____________

Participating Bank #l: _____________________________________________________________________________________

Contact Person: ____________________________________________________________ Phone #: (_____) ________________

Participating Bank #2: _____________________________________________________________________________________

Contact Person: ____________________________________________________________ Phone #: (_____) ________________

Other Lender #l: _________________________________________________________________________________________

Contact Person: ____________________________________________________________ Phone #: (_____) ________________

Other Lender #2: _________________________________________________________________________________________

Contact Person: ____________________________________________________________ Phone #: (_____) ________________

V. QUESTIONS

A. Will you agree to make a conscientious effort to hire your employees from this area when possible, paying particular attention to displaced farm families, the underemployed and the unemployed in county? ________ Yes _________No

B. Will any current employees lose their jobs if this project is not approved? ________ Yes _________No

C. Explain why our assistance is needed and why it is not feasible to obtain assistance elsewhere (i.e. specific reasons why the project could not be or would not be accomplished without our assistance).

D. Is this company willing to give preference in hiring to low and moderate income persons________ Yes _________No

E. Are you related to any current or former Director of the Insert Intermediary Name Board, current or former officer of Insert Intermediary Name, Loan Review Committee member for the Revolving Loan Fund, or the Development Finance Director of Insert Intermediary Name? ___________ Yes ___________ No

24

1 Rev 01/09

IV. BUSINESS PLAN OUTLINE

A. Executive Summary of the Company and the Project

B. Brief History of Business 1. Describe the past operation of the business and/or the events leading to its

creation2. Current or proposed ownership3. Number of employees; average wage; benefit and training package

C. Market Analysis and Strategy 1. Description of current buyers and target markets (provide verification of

purchase orders, contracts, etc., which relate to reasons for the loanrequest)

2. Competition3. Pricing4. Distribution5. Advertising6. Sales Promotion

D. Products 1. Description of product line2. Proprietary position of patents, copyrights, legal and technical

considerations3. Comparison to competition

E. Manufacturing Process 1. Materials2. Production Methods

F. Describe the Project 1. Describe the project to be undertaken & Timeline2. Has the project started? If yes, please explain3. Breakdown the number of new employees to be hired within next 24

months including average wage4. Include construction blueprints and/or a list of equipment to be purchased

as part of the project. If contractor, architect, or equipment vendor havebeen selected, please include information on that business.

G. Financial Statements 1. Sources/Uses Statement for the project2. Monthly Cash Flow Analysis for Next 12 Months3. Profit and Loss Statement: last three years and current quarter, plus two-

year projection.4. Balance Sheet: last three years and current quarter, plus two-year

projection.5. Schedule of Existing Business Debt including outstanding balance,

interest rate, term, maturity date, and collateral on all existing debt.

25

1 Rev 01/09

H. Statement of Proposed Collateral A detailed list of all collateral offered, its value, and security position by funding

source.

I. Resumes and Personal Financial Statements Include resumes of all principals as well as current, dated, and signed personal financial statements on all principals with a significant financial interest in this business.

J. Commitment Letters Include Commitment letters from banks or others which state the terms and conditions of their participation.

K. Affiliates Description of any affiliates or subsidiaries of business or principals requesting assistance, as well as balance sheets and income statements for past two fiscal years on such affiliates or subsidiaries.

L. Appraisals/Proposed Lease/Purchase Options or Agreements An independent appraisal will be required for any real estate which is a subject of the proposed financing or which is offered as a major source of collateral to secure the loan. Also include copies of existing or proposed leases(s), purchase options or agreements, or any other financial arrangements.

M. Partnership Certificate of Authorization or Corporate Certificate of Authority and Incumbency; include minutes of the corporate meeting adopting this certification, where Applicable.

N. Other Required Documents 1. Copy of last year’s submitted business income tax statement2. Copy of last year’s submitted personal income tax statement3. Articles of Incorporation (or Organization if L.L.C.)4. Bylaws5. Written verification from primary lender that project could not be funded

from commercial sources—either due to underwriting guidelines, rates,and/or term.

6. Evidence of payment of last quarters payroll tax7. Evidence of Worker’s Compensation insurance coverage

26

1 Rev 01/09

CERTIFICATION TO BE SIGNED BY APPLICANT

The undersigned, duly authorized officers of Applicant, hereby certify that the filing of this application was duly authorized by its Board of Directors (or governing body), that the statements made in the foregoing application and in all exhibits and documents submitted in connection therewith are true and correct to be the best information and belief of the undersigned and are submitted as a basis for the loan.

Likewise, the undersigned has willfully furnished this confidential information to Insert Intermediary Name for the purpose of applying for a loan. I understand that this information will be reviewed by RLF staff. I further understand that this information will become available to the Revolving Loan Fund Loan Review Committee and the Insert Intermediary Name Board of Directors. I further authorize RLF staff to be in contact with those individuals and institutions involved in the proposed project.

In addition, the undersigned also acknowledges that the loan applicant will be responsible for all “out of pocket” expenses such as, but not limited to, attorney fees, abstract charges, filing fees, appraisals and environmental reviews.

NAME OF APPLICANT

__________________________________________________________ (Individual, general partner, trade name, corporation, or political subdivision)

By ______________________________ Date ______________________

Typed Name ______________________________

Title ____________________________________

Attest by _________________________________

Typed Name ______________________________

Title ____________________________________

27

1 Rev 01/09

RIGHT TO FINANCIAL PRIVACY ACT OF 1978

-NOTICE-

This Act is designed to protect your right to financial privacy. This is notice to you, as required by the Right to Financial Privacy Act of 1978, of Insert Intermediary Name’s access rights to financial records held by financial institutions that are or have been doing business with you or your business, including any financial institution participating in this loan or loan guaranty in connection with your loan application. The law provides that the access rights continue for the term of any approved loan without further notice as long as Insert Intermediary Name retains any interest in the loan.

ACKNOWLEDGMENT

I (We) certify that I (we) have read this notice and that I (we) have been given a copy of it.

Business Name: _____________________________

By: _______________________________________ (Name and Title)

Date: ______________________________________

Proprietor, Partners, Principals and Guarantors

Date: _________________ ______________________________________________ (Signature)

Date: _________________ ______________________________________________ (Signature)

Date: _________________ ______________________________________________ (Signature)

Date: _________________ ______________________________________________ (Signature)

28

1 Rev 01/09

NONDISCRIMINATION STATEMENT

In accordance with Federal Law and U.S. Department of Agriculture policy, this institution is prohibited from discriminating on the basis of race, color, national origin, age, disability, and where applicable, sex, marital status, familial status, parental status, religion, sexual orientation, genetic information, political beliefs, reprisal, or because all or a part of an individual's income is derived from any public assistance program. (Not all prohibited bases apply to all programs.) Persons with disabilities who require alternative means for communication of program information (Braille, large print, audiotape, etc.) should contact USDA's TARGET Center at (202) 720-2600 (voice and TDD). To file a complaint of discrimination write to USDA, Director, Office of Civil Rights, 1400 Independence Avenue, S.W., Washington, D.C. 20250-9410 or call (800) 795-3272 (voice) or (202) 720-6382 (TDD). USDA is an equal opportunity provider and employer.

***IMPORTANT NOTICE***

The following information is requested by the Federal Government for certain types of loans and grants, in order to monitor compliance with civil rights laws. You are not required to furnish this information, but are encouraged to do so. The law requires that a program recipient may neither discriminate on the basis of this information nor on whether you choose to furnish it. However, if you choose not to furnish it, under federal regulations, this program representative is required to note race/ethnicity on the basis of visual observation or surname.”

______ I do not wish to furnish this information.

Ethnicity: Gender: ______ Hispanic or Latino ______ Male ______ Not Hispanic or Latino ______ Female

Race: (Mark one or more) ______ White ______ Black or African American ______ American Indian/Alaska Native ______ Asian ______ Native Hawaiian or other Pacific Islander

Information provided by:

Borrower_____ Lender_____ _____________________________________________________________________________ Free Resources for Small Business

The Small Business Administration USDA Rural Development Programs www.sba.gov www.rurdev.usda.gov

The Small Business Development Centers in Iowa http://www.iabusnet.org

29

Sample Commitment Letter

Date

Name Address City

Dear_____:

This letter is to advise you that your loan application to the _______________________ Revolving Loan Fund has been approved subject to the following terms:

Loan Amount $______ Interest Rate _______% Amortization Term _______ years Origination Fee _______ Annual Administration Fee _______

This approval is subject to the following terms and conditions:

1. Type In any conditions of the loan from approval sheet such as

a. Verification of other funding necessary to complete the project.b. Satisfactory Appraisal of the subject property with a value of at least

$___________.c. “personal guarantees of____________

2. Loan Approval from USDA (if applicable)

3. The following documentation is required prior to closing: (Delete those that don’t apply)a. Corporate Authorization to Borrow authorizing appropriate officers to sign on

behalf of the corporation.b. Satisfactory abstract and title opinion (if real estate)c. Satisfactory Lien Search (if equipment)d. Evidence of Environmental Clearance from USDA. (not required on revolved

funds)

4. Execution of all required loan documents (Delete those that don’t apply)a. Opinion Letter from borrower’s attorneyb. Promissory Notec. Mortgage/UCC 1d. Loan Agreemente. Construction Agreement

5. Payment of out of pocket expenses at closing.

6. Proof of Adequate Insurance with ______________________ listed as loss payee.

Please sign and return one copy of this letter indicating your acceptance of these terms.

30

Sincerely,

XXXXXXXXX

We ___________________________, hereby agree to and accept the terms of this loan offered in this commitment letter.

___________________________________________ ____________________________(Print Name /Title)

31

12/08

Sample Withdrawal Letter

DATE

APPLICANT NAME APPLICANT ADDRESS

SUBJECT: $DOLLAR LOAN APPLICATION REQUEST WITHDRAWAL LETTER

Dear APPLICANT:

Effective today we have withdrawn your application for assistance. This action will in no way hinder you from reapplying for assistance in the future.

The specific reason(s) for withdrawing your application are as follows:

You have advised us that you wish to withdraw your application. The application is incomplete and efforts to receive a complete application have failed. The application material is more than # days old. There are insufficient funds available to fund your request. Other

The Federal Equal Credit Opportunity Act prohibits creditors from discriminating against credit applicants on the basis of race, color, religion, national origin, sex, marital status, or age (provided the applicant has the capacity to enter into a binding contract); and because all or parts of the applicant’s income is derived from any public assistance program; or because the applicant has in good faith exercised any rights under the Consumer Credit Protection Act. The Federal agency that administers compliance with this law concerning this creditor is the Federal Trade Commission. If a person believes he or she was denied assistance in violation of this law, they should contact the Federal Trade Commission, Washington, DC 20580.

Sincerely,

LENDER REPRESENTATIVE

32

12/08

Sample Rejection Letter

DATE

APPLICANT NAME APPLICANT ADDRESS

SUBJECT: $DOLLAR LOAN APPLICATION REQUEST REJECTION LETTER

Dear APPLICANT:

After careful consideration, LENDER was unable to take favorable action on your application for assistance. The specific reason(s) for the decision are as follows:

There is not a reasonable assurance of repayment ability (cash flow) documented. There is insufficient collateral. There is insufficient equity. The proposal does not meet the eligibility requirements of the LENDER’s program. Other

The Federal Equal Credit Opportunity Act prohibits creditors from discriminating against credit applicants on the basis of race, color, religion, national origin, sex, marital status, or age (provided the applicant has the capacity to enter into a binding contract); and because all or parts of the applicant’s income is derived from any public assistance program; or because the applicant has in good faith exercised any rights under the Consumer Credit Protection Act. The Federal agency that administers compliance with this law concerning this creditor is the Federal Trade Commission. If a person believes he or she was denied assistance in violation of this law, they should contact the Federal Trade Commission, Washington, DC 20580.

Sincerely,

LENDER REPRESENTATIVE

33

Revised 10/13

IntermediaryRevolving Loan Fund

Loan Approval Summary Sheet

Applicant Name _____________________________ Loan Number __________

Contact Person _______________________ Phone__________________

Approved Loan Amount______________________ Interest Rate ____________

Term ________ Payments Mnth/Qtr/Ann Loan Fee ____________

Total Project Investment______________ Number of Jobs Created/Retained ________

Collateral for Loan _______________________________

Conditions of Loan (if applicable) 1) _______________________________________

2) _______________________________________

3) _______________________________________

4) _______________________________________

Loan Closed Date ________________ First Payment Due ____________

Insurance Policy Expires ____________________

Documents Needed to Close____ 1) Signed Application with Business Plan attached____ 2) Signed Commitment Letter____ 3) Attorney Title Opinion—authority to borrow____ 4) Note & Loan Agreement____ 5) Abstract Updated and Title Opinion____ 6) Mortgage____ 7) UCC Lien Search (Equipment)____ 8) UCC 1 Filed with Secretary of State (Equipment)____ 9) Proof of Hazard Insurance—Intermediary listed as Loss Payee____ 10) 1048 Debarment Form____ 11) 400-1 Assurance Form____ 12) __________________________________________________________________ 13) __________________________________________________________________ 14) ______________________________________________________________

= on filen/a = not applicable

34

= on filen/a = not applicable or not required

Revised 10/13

Insert Intermediary NameRevolving Loan Fund

Loan File Checklist-Mortgage

Processing

____ 1) Loan Summary &Recommendation / LRC Minutes

____ 2) Board Minutes approving loan

____ 3) Signed Loan Application

____ 4) Business Plan includingattachments:A. ____3 years Historical

Financial StatementsB. ____2 Years Business

ProjectionsC. ____Income Tax ReturnsD. ____Schedule of Existing DebtE. ____Personal Financial

StatementsF. ____Commitment Letters from

other lendersG. ____Appraisal

____ 5) Signed Commitment Letter

____ 6) Verification of Loan Conditions(if applicable)

____ 7) _________________________

____ 8) _________________________

____ 9) _________________________

____ 10) _________________________

Closing Documents

____ 1) Loan Approval Summary Sheet

____ 2) Evidence of Insurance with InsertIntermediary Name as loss payee

____ 3) Attorney Title Opinion (Borrower’sAttorney to Intermediary)

____ 4) Loan Closing / SettlementStatement

____ 5) Promissory Note (Copy in file—Original in safe)

____ 6) Loan Agreement

____ 7) 4004-Assurance

____ 8) Form 1048 Debarment

____ 9) Title Opinion or Attorney TitleOpinion (Abstract)

____ 10) Mortgage (Recorded)

____ 11) ________________________

____ 12) ________________________

____ 13) ________________________

____ 14) ________________________

____ 15) ________________________

35

= on filen/a = not applicable or not required

Revised 10/13

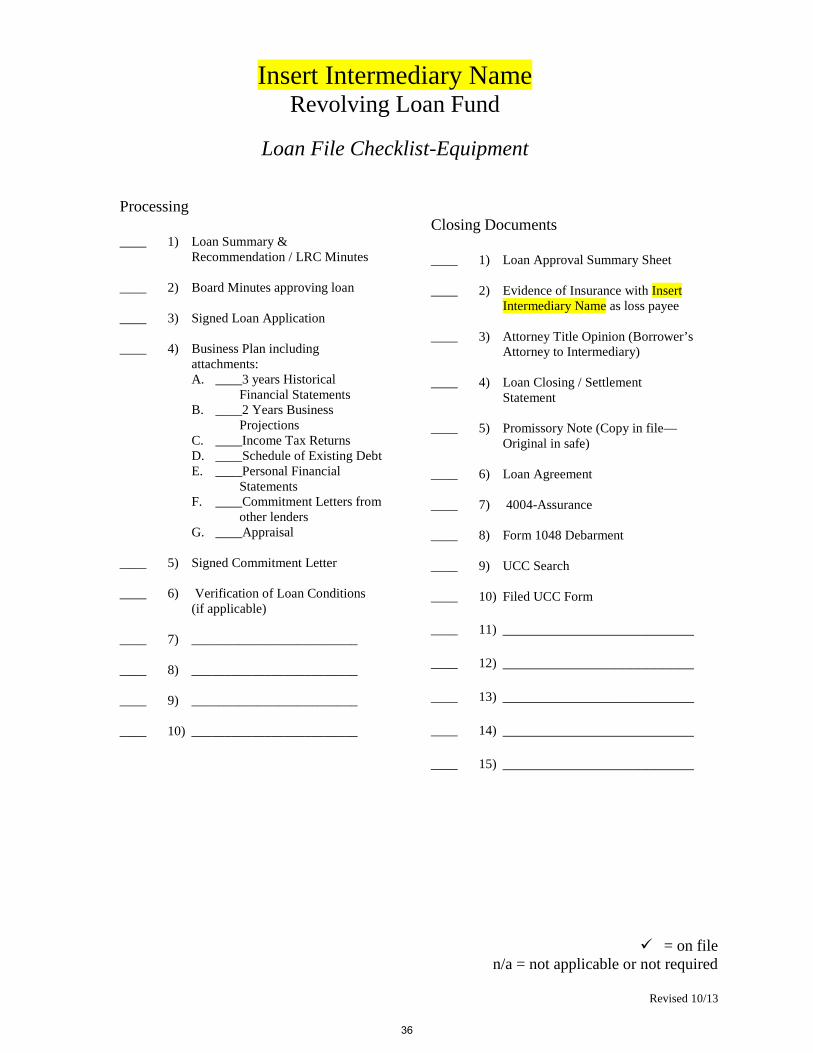

Insert Intermediary NameRevolving Loan Fund

Loan File Checklist-Equipment

Processing

____ 1) Loan Summary &Recommendation / LRC Minutes

____ 2) Board Minutes approving loan

____ 3) Signed Loan Application

____ 4) Business Plan includingattachments:A. ____3 years Historical

Financial StatementsB. ____2 Years Business

ProjectionsC. ____Income Tax ReturnsD. ____Schedule of Existing DebtE. ____Personal Financial

StatementsF. ____Commitment Letters from

other lendersG. ____Appraisal

____ 5) Signed Commitment Letter

____ 6) Verification of Loan Conditions(if applicable)

____ 7) _________________________

____ 8) _________________________

____ 9) _________________________

____ 10) _________________________

Closing Documents

____ 1) Loan Approval Summary Sheet

____ 2) Evidence of Insurance with InsertIntermediary Name as loss payee

____ 3) Attorney Title Opinion (Borrower’sAttorney to Intermediary)

____ 4) Loan Closing / SettlementStatement

____ 5) Promissory Note (Copy in file—Original in safe)

____ 6) Loan Agreement

____ 7) 4004-Assurance

____ 8) Form 1048 Debarment

____ 9) UCC Search

____ 10) Filed UCC Form

____ 11) ________________________

____ 12) ________________________

____ 13) ________________________

____ 14) ________________________

____ 15) ________________________

36

37

1

TO: Bill Menner, State Director USDA Rural Development

From: Bruce Nuzum, Iowa Area Development Group on behalf of Iowa’s Electric Cooperatives,

Independent Telephone Companies, and Municipal Electric Utilities

Date: November 3, 2009

Memorandum of Understanding Regarding REDL&G RLF Accounting Procedures

This memo is being drafted to affirm the program and the authority in the regulations as well as address a lack of formal accounting procedures in the event of a loss to a Rural Economic Development Grant Revolving Loan Fund.

The Rural Utility Service created the Rural Economic Development Loan and Grant (REDL&G) program so that RUS eligible borrowers would have a financial tool to assist with community and business development projects in their local area. The program is administered by USDA Rural Development. REDL&G offers two distinct programs a “pass through loan” and a grant to establish a revolving loan fund. The program is outlined in the regulations at RD Instruction Section 4280.

The federal regulations outline the general parameters related to operation of a revolving loan fund and make provisions for losses. However, accounting procedures/journal entries have not been developed to correspond to the operation of a RLF. As such, this memo is being drafted to clarify the loss authority measures established in the regulations and the accounting journal entries in the event of a loss to the Rural Economic Development Grant Revolving Loan Fund (RLF).

Rural Economic Development Loan Program The Rural Economic Development Loan (REDL) is a “pass through” loan. The cooperative receives a loan from USDA RD and makes a separate loan which mirrors those terms to the benefit of the ultimate recipient or application project. As part of this program, the RUS borrower / loan “Intermediary” is pledging repayment of the loan from Rural Development and guaranteeing it with assets of the cooperative or by posting an irrevocable letter of credit. As such, accounting journal entries have been clearly outlined and identified. While the Federal Register entry references the programs old regulation number (1703), these accounts were most recently identified in Federal Register Volume 73, No. 102 dated Tuesday, May 27th, 2008. Section 626 which starts on page 30289.

Rural Economic Development Grant Program. The Rural Economic Development Grant works differently in that the Intermediary receives a grant for purposes of a revolving loan fund (RLF) and contributes a 20% matching grant to the RLF. This RLF makes loans to businesses and non-profit organizations for economic and community development projects that benefit the local

38

2

rural area. The program regulations authorize Intermediaries to charge an annual administration fee of up to 1% to the borrower to assist with the costs incurred by operating the fund. Loan repayments (both principal and interest) are retained in the RLF—growing the RLF balance—even though the cooperative must claim interest earnings of the RLF as operational revenue of the cooperative.

Journal Entries for accepting the grant amount, interest earnings and outstanding loans were listed in the Federal Register Volume 73, No. 102 page 30289 section 626 which is summarized as follows:

The Intermediary is charged with operating the RLF as a “prudent lender.” However, by its very nature, a RLF is expected to be gap financer—taking risks when the conventional financing market is unwilling. As such, occasional losses to the RLF are expected and provisions are made to accommodate this reality in the program’s regulations.

Section 4280.26(b) of the program regulations gives the Intermediary the authority to deduct up to 10% of the grant amount towards operating expenses of the RLF over the life of the RLF. In previous discussions with USDA, RLF loan losses and related collection/foreclosure expenses could be deducted from the grant amount under this provision.

Since the program’s inception, instructions from USDA RD have been that the RLF Intermediary needs to follow the policies of their approved RLF Plan and that the RLF is making the loan and taking the credit risk. Further, if there is a loan loss USDA RD instructions have been that the RLF is written-down to be smaller—with both the grant award and the Intermediary’s matching grant sharing the loss on a proportionate share basis (83.33% Grant / 16.67% Match).

It is assumed that the RLF will operate in perpetuity. As such, it is hoped that future interest earnings will eventually replenish any losses incurred by the fund. However, the REC is not guaranteeing the fund or the grant amount. In fact, USDA staff has indicated that due to these circumstances of the RLF, a loan loss reserve was not required for the REDL&G program.

Accounting Subaccounts

Accepting grant funds from RUSDebit 131.13 Cash—Economic Development Grant FundsCredit Account 224.18 if grant agreement requires repayment of funds upon termination of RLFOR

Credit Account 208 if there is “absolutely no obligation” for repayment upon termination of the RLF

REDG Grant Agreement Does have “claw-backs”Not following approved RLF Plan—Administrative RulesIn the new 4280 Regulations, not making a loan from RLF for 3 years is cause for termination.

Accounting Subaccounts

Making Advances / Loans to “NonassociatedOrganizations”

Advances: Dr. 124 Economic Development GrantsCr. 131 Cash – Economic Development Grant Funds

Accrual of Interest:Dr. 171 Interest and Dividends ReceivableCr. 419 Interest and Dividends Income

RepaymentsDr. 131 Cash – Economic Development Grant FundsCr. 124 Economic Development GrantsCr. 419 or 171 Interest and Dividends

39

3

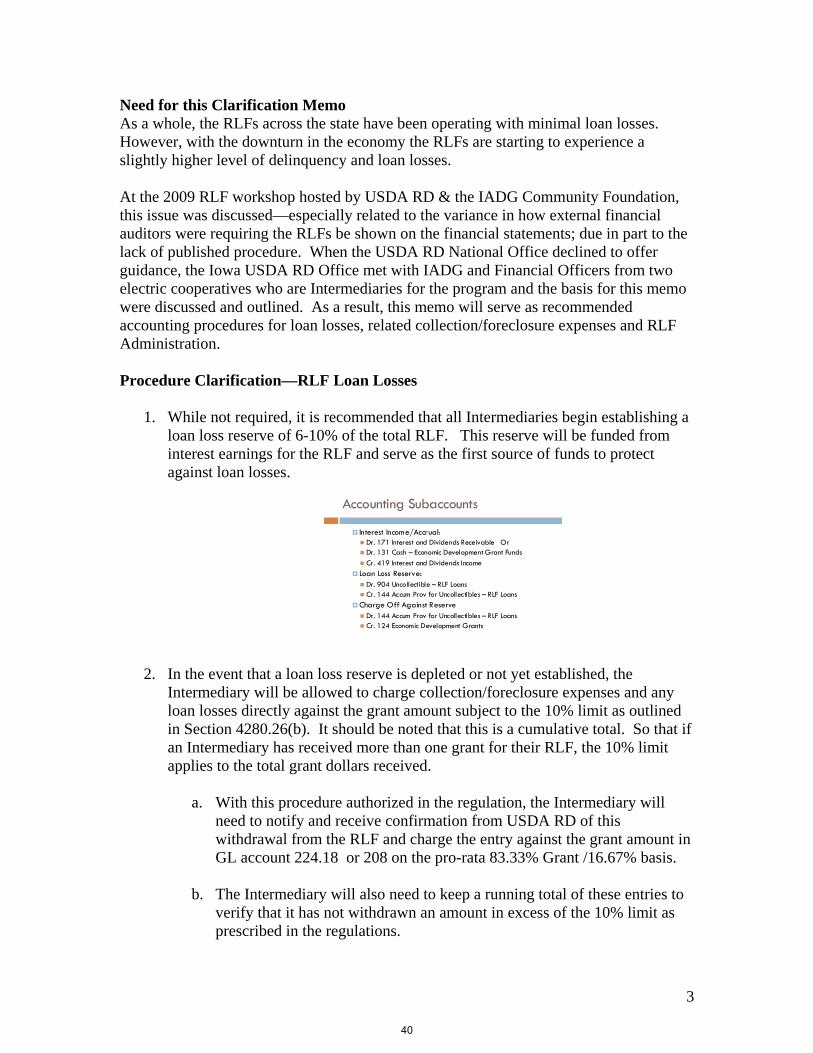

Need for this Clarification Memo As a whole, the RLFs across the state have been operating with minimal loan losses. However, with the downturn in the economy the RLFs are starting to experience a slightly higher level of delinquency and loan losses.

At the 2009 RLF workshop hosted by USDA RD & the IADG Community Foundation, this issue was discussed—especially related to the variance in how external financial auditors were requiring the RLFs be shown on the financial statements; due in part to the lack of published procedure. When the USDA RD National Office declined to offer guidance, the Iowa USDA RD Office met with IADG and Financial Officers from two electric cooperatives who are Intermediaries for the program and the basis for this memo were discussed and outlined. As a result, this memo will serve as recommended accounting procedures for loan losses, related collection/foreclosure expenses and RLF Administration.

Procedure Clarification—RLF Loan Losses

1. While not required, it is recommended that all Intermediaries begin establishing aloan loss reserve of 6-10% of the total RLF. This reserve will be funded frominterest earnings for the RLF and serve as the first source of funds to protectagainst loan losses.

2. In the event that a loan loss reserve is depleted or not yet established, theIntermediary will be allowed to charge collection/foreclosure expenses and anyloan losses directly against the grant amount subject to the 10% limit as outlinedin Section 4280.26(b). It should be noted that this is a cumulative total. So that ifan Intermediary has received more than one grant for their RLF, the 10% limitapplies to the total grant dollars received.

a. With this procedure authorized in the regulation, the Intermediary willneed to notify and receive confirmation from USDA RD of thiswithdrawal from the RLF and charge the entry against the grant amount inGL account 224.18 or 208 on the pro-rata 83.33% Grant /16.67% basis.

b. The Intermediary will also need to keep a running total of these entries toverify that it has not withdrawn an amount in excess of the 10% limit asprescribed in the regulations.

Accounting Subaccounts

Interest Income/Accrual:Dr. 171 Interest and Dividends Receivable OrDr. 131 Cash – Economic Development Grant FundsCr. 419 Interest and Dividends Income

Loan Loss Reserve:Dr. 904 Uncollectible – RLF LoansCr. 144 Accum Prov for Uncollectibles – RLF Loans

Charge Off Against ReserveDr. 144 Accum Prov for Uncollectibles – RLF LoansCr. 124 Economic Development Grants

40

4

3. In the event that the Intermediary has exhausted both the available loan lossreserve and the 10% withdrawal authorization, the Intermediary should submitdocumentation of a loan loss and related expenses to be charged as a directexpense of the RLF on a prorated basis for approval by the Iowa Office of USDARD. Once approved, journal entries will reduce the Federal Grant obligation(Acct 224.18 or 208) and the Intermediary’s matching fund based on the ratio83.33% Grant / 16.67% Intermediary Matching funds.

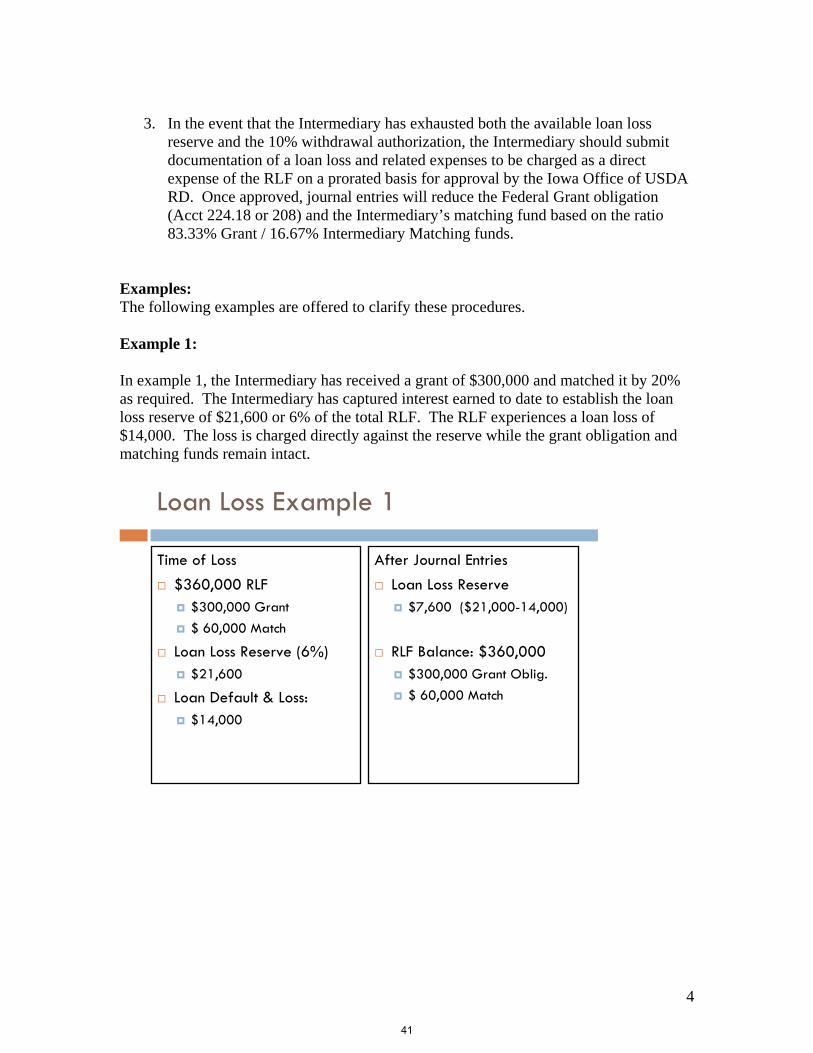

Examples: The following examples are offered to clarify these procedures.

Example 1:

In example 1, the Intermediary has received a grant of $300,000 and matched it by 20% as required. The Intermediary has captured interest earned to date to establish the loan loss reserve of $21,600 or 6% of the total RLF. The RLF experiences a loan loss of $14,000. The loss is charged directly against the reserve while the grant obligation and matching funds remain intact.

Loan Loss Example 1

Time of Loss$360,000 RLF

$300,000 Grant$ 60,000 Match

Loan Loss Reserve (6%)$21,600

Loan Default & Loss:$14,000

After Journal EntriesLoan Loss Reserve

$7,600 ($21,000-14,000)

RLF Balance: $360,000$300,000 Grant Oblig.$ 60,000 Match

41

5

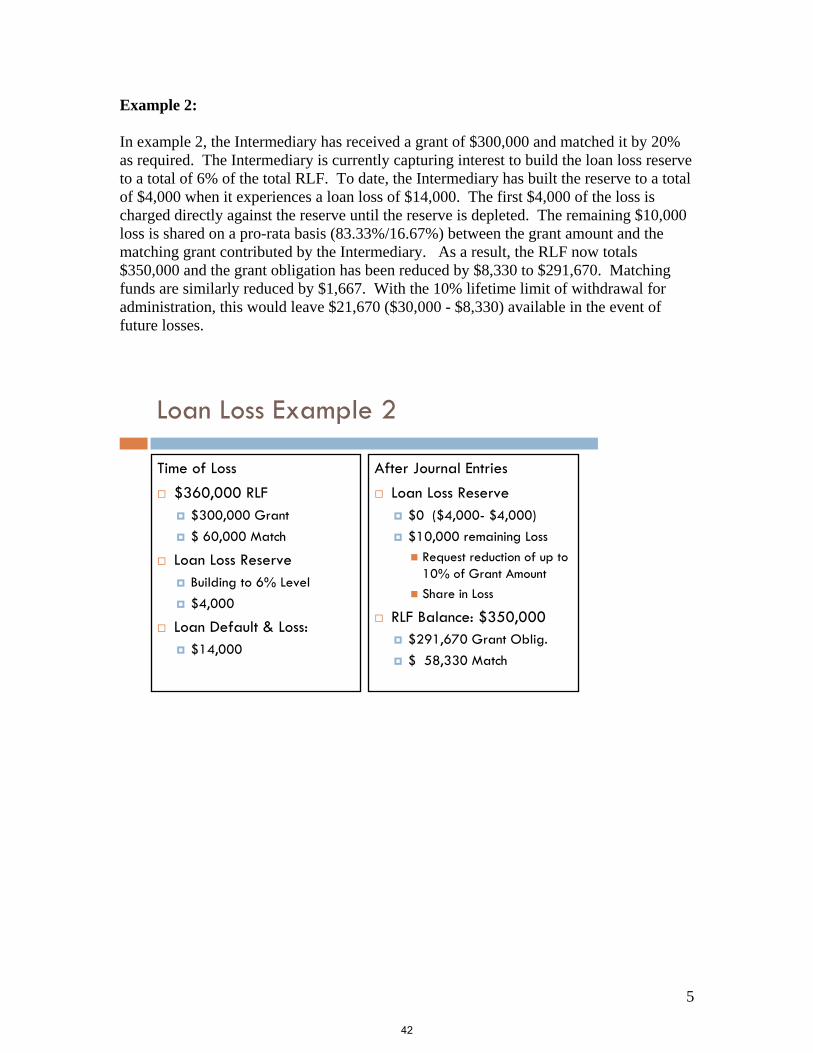

Example 2:

In example 2, the Intermediary has received a grant of $300,000 and matched it by 20% as required. The Intermediary is currently capturing interest to build the loan loss reserve to a total of 6% of the total RLF. To date, the Intermediary has built the reserve to a total of $4,000 when it experiences a loan loss of $14,000. The first $4,000 of the loss is charged directly against the reserve until the reserve is depleted. The remaining $10,000 loss is shared on a pro-rata basis (83.33%/16.67%) between the grant amount and the matching grant contributed by the Intermediary. As a result, the RLF now totals $350,000 and the grant obligation has been reduced by $8,330 to $291,670. Matching funds are similarly reduced by $1,667. With the 10% lifetime limit of withdrawal for administration, this would leave $21,670 ($30,000 - $8,330) available in the event of future losses.

Loan Loss Example 2

Time of Loss$360,000 RLF

$300,000 Grant$ 60,000 Match

Loan Loss Reserve Building to 6% Level$4,000

Loan Default & Loss:$14,000