half-year review 2011 - zonebourse.com€¦ · half-year review of operations ... martin bouygues ....

TRANSCRIPT

30 August 2011

32 Hoche - Paris

HALF-YEAR REVIEW

2011

BUILDING THE FUTURE IS OUR GREATEST ADVENTURE

French société anonyme with share capital of €365,862,523 - Registered office: 32, avenue Hoche, 75008 Paris, France Registration No. 572 015 246 Paris - I.E. FR 29 572 015 246

BOUYGUES/2011 Half-year review

CONTENTS

Board of Directors ......................................................................................................... 2 Half-year review of operations ..................................................................................... 3 Condensed consolidated first-half financial statements ............................................ 31 Certificate of responsibility .......................................................................................... 58 Auditors' report on the first-half financial statements ................................................ 59

1

BOUYGUES/2011 Half-year review Board of Directors

BOARD OF DIRECTORS

MEMBERSHIP Chairman and Chief Executive Officer Martin Bouygues Director and Deputy CEO Olivier Bouygues Deputy CEO and standing representative of SCDM, director Directors Pierre Barberis Former Deputy CEO, Oberthur Patricia Barbizet CEO and director, Artémis François Bertière Chairman and CEO, Bouygues Immobilier Mrs Francis Bouygues Georges Chodron de Courcel COO, BNP Paribas Lucien Douroux Former Chairman of the Supervisory Board, Crédit Agricole Indosuez Yves Gabriel Chairman and CEO, Bouygues Construction Patrick Kron Chairman and CEO, Alstom Non-voting director Alain Pouyat BOARD COMMITTEES Accounts Committee Helman le Pas de Sécheval (Chairman) Patricia Barbizet Georges Chodron de Courcel Selection Committee Jean Peyrelevade (Chairman) François-Henri Pinault

Hervé Le Bouc Chairman and CEO, Colas Helman le Pas de Sécheval Managing Director, Groupama Centre Atlantique Colette Lewiner Deputy Chairwoman, Capgemini Sandra Nombret Director representing employee shareholders Nonce Paolini Chairman and CEO, TF1 Jean Peyrelevade Chairman of the Board of Directors, Leonardo & Co. François-Henri Pinault Chairman and CEO, PPR Michèle Vilain Director representing employee shareholders Remuneration Committee Pierre Barberis (Chairman) Patricia Barbizet Ethics and Sponsorship Committee Lucien Douroux (Chairman) François-Henri Pinault

2

BOUYGUES/2011 Half-year review Half-year review of operations 3

HALF-YEAR REVIEW OF OPERATIONS

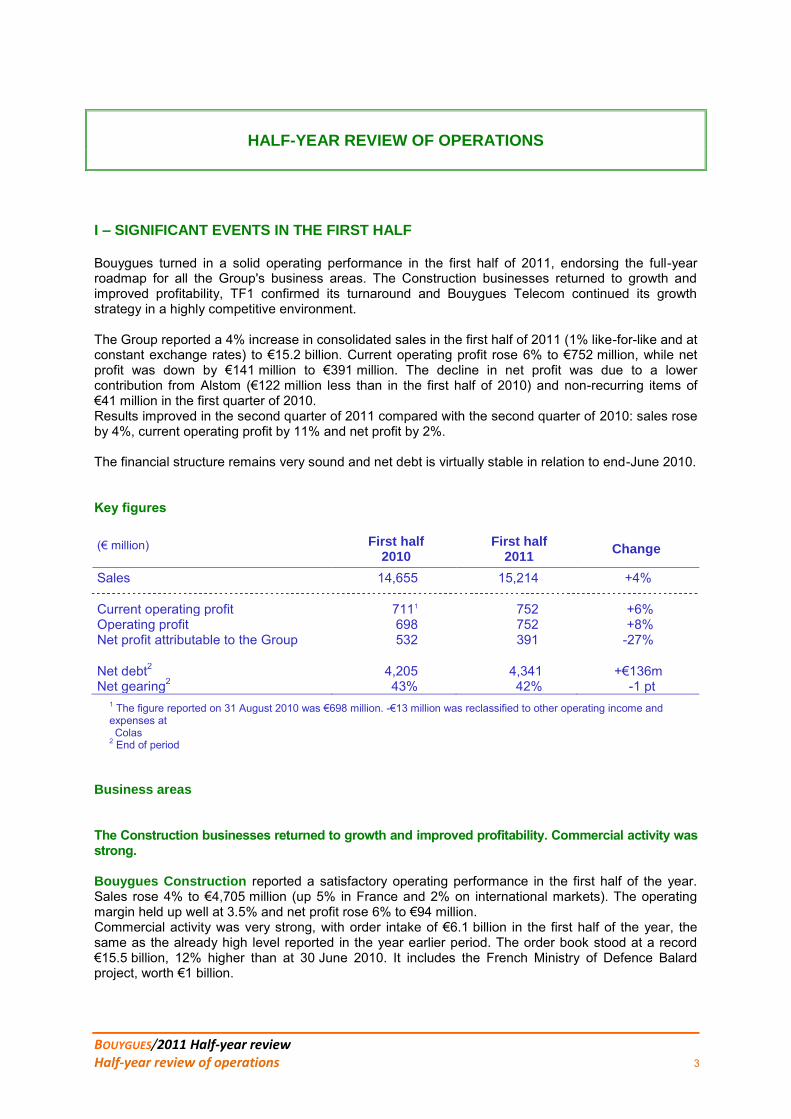

I – SIGNIFICANT EVENTS IN THE FIRST HALF Bouygues turned in a solid operating performance in the first half of 2011, endorsing the full-year roadmap for all the Group's business areas. The Construction businesses returned to growth and improved profitability, TF1 confirmed its turnaround and Bouygues Telecom continued its growth strategy in a highly competitive environment. The Group reported a 4% increase in consolidated sales in the first half of 2011 (1% like-for-like and at constant exchange rates) to €15.2 billion. Current operating profit rose 6% to €752 million, while net profit was down by €141 million to €391 million. The decline in net profit was due to a lower contribution from Alstom (€122 million less than in the first half of 2010) and non-recurring items of €41 million in the first quarter of 2010. Results improved in the second quarter of 2011 compared with the second quarter of 2010: sales rose by 4%, current operating profit by 11% and net profit by 2%. The financial structure remains very sound and net debt is virtually stable in relation to end-June 2010. Key figures

(€ million)

First half 2010

First half 2011

Change

Sales 14,655 15,214 +4%

Current operating profit 7111 752 +6% Operating profit 698 752 +8% Net profit attributable to the Group 532 391 -27%

Net debt2 4,205 4,341 +€136m Net gearing2 43% 42% -1 pt

1 The figure reported on 31 August 2010 was €698 million. -€13 million was reclassified to other operating income and expenses at Colas

2 End of period Business areas The Construction businesses returned to growth and improved profitability. Commercial activity was strong. Bouygues Construction reported a satisfactory operating performance in the first half of the year. Sales rose 4% to €4,705 million (up 5% in France and 2% on international markets). The operating margin held up well at 3.5% and net profit rose 6% to €94 million. Commercial activity was very strong, with order intake of €6.1 billion in the first half of the year, the same as the already high level reported in the year earlier period. The order book stood at a record €15.5 billion, 12% higher than at 30 June 2010. It includes the French Ministry of Defence Balard project, worth €1 billion.

BOUYGUES/2011 Half-year review Half-year review of operations

First-half results at Bouygues Immobilier were in line with the company's full-year roadmap. Sales declined 16% to €1,098 million. Commercial property sales were down 47% squeezed by a tough comparative with the first half of 2010. Residential property sales dropped 6% overall in the first six months but started to rise again in the second quarter. The current operating margin and net profit remained stable at 8.3% and €56 million respectively. After a record year in 2010, residential property reservations remained high at €990 million. Commercial property reservations rose sharply to €324 million in a still hesitant market. Overall, reservations were up 6% on the first half of 2010 at €1,314 million. The order book was 18% higher than at end-June 2010 at €2.5 billion.

At Colas, the gradual improvement in profitability was confirmed in the first half of 2011. Sales were up 8% to €5,400 million (up 15% in France and down 3% on international markets). After benefiting from favourable weather conditions in France in the first quarter, sales remained robust in the second quarter. As expected, current operating profit improved – it was €34 million higher than in the first half of 2010 – as the positive effects of the action plan introduced in 2010 began to show. Net profit amounted to €2 million, €31 million up on the first half of 2010. Good business activity in the first half of 2011 kept the order book at a high level of €7.2 billion (the same as at end-June 2010), despite sales growth. TF1 put in a very good first half and confirmed its turnaround. Sales at TF1 were virtually stable at €1,278 million. The current operating margin improved substantially to 14.6%, 6.5 points more than in the first half of 2010, and net profit rose 61% to €119 million as TF1 confirmed its capacity to closely manage costs and adapt its business model. Standard & Poor’s raised TF1's credit rating to BBB+ with a stable outlook, reflecting the company's healthy financial structure. Bouygues Telecom continued its growth strategy in a highly competitive environment and performed in line with its expectations. Bouygues Telecom reported a 5% increase in first-half sales to €2,866 million and a 3% rise in sales from network to €2,575 million. As anticipated, EBITDA remained stable stripping out the effect of the cut in mobile termination rate differentials, despite fierce competitive pressure. EBITDA amounted to €665 million, down 9%, and net profit to €213 million, down 19%. In a very brisk mobile phone market, Bouygues Telecom signed up 206,000 new mobile contract customers in the first half of 2011, representing 21% of net market growth1. Bouygues Telecom had a total customer base of 11,187,000 at 30 June 2011, 80% of them on mobile call plans, a 1.3-point rise over a 12-month period. On 18 July 2011, the operator innovated once again by launching the new B&YOU service, a mobile plan that targets the “internet generation”. 215,000 new fixed broadband customers joined Bouygues Telecom in the first half of 20112, giving a total of 1,023,000 fixed broadband customers at 30 June 2011. 1 Arcep (French communications regulator) data 2 Including broadband and very-high-speed subscribers. Alstom Alstom contributed €94 million to the Group's first-half net profit, compared with €216 million in the first half of 2010. As announced, after a first quarter severely hit by non-recurring expenses taken by Alstom in the second half of FY2010/2011, Alstom contributed €71 million to Group net profit in the second quarter of 2011 (versus €101 million in the second quarter of 2010). Carrying on from the second half of FY2010/2011, Alstom recorded strong growth in its order intake in the first quarter of FY2011/2012 and confirmed its operating margin target of between 7% and 8% for FY2011/2012.

4

BOUYGUES/2011 Half-year review Half-year review of operations

Financial position Cash flow increased slightly to €1,502 million, in line with the rise in operating profit. As anticipated, net capital expenditure rose to €651 million, €150 million more than in the first half of 2010, generating free cash flow1 of €494 million. Group net debt was virtually stable in relation to end-June 2010 at €4.3 billion. 1 Before the change in working capital requirement Cancellation of shares The Board of Directors decided to cancel 9,973,287 shares, 5,153,093 of which were acquired in the first half of 2011. Following the cancellation, the number of shares stood at 356,307,709 and voting rights at 479,801,903. Sales target Sales by business area

(€ million)

2010 actual

2011 target

% change

Reported in March

Reported in May

Reported in August

Bouygues Construction 9,235 9,400 9,600 9,600 +4% Bouygues Immobilier 2,418 2,440 2,440 2,440 +1% Colas 11,661 11,800 11,800 11,900 +2% TF1 2,622 2,630 2,630 2,630 = Bouygues Telecom 5,636 5,730 5,730 5,730 +2% Holding company and other 132 120 120 120 nm

Intra-Group elimination (479) (420) (420) (420) nm

TOTAL 31,225 31,700 31,900 32,000 +2% o/w France 21,576

1 22,000 22,100 22,400 +4%

o/w international 9,6491 9,700 9,800 9,600 -1%

1 Following the change in status of Mayotte that has become a French department, sales were reclassified to France

5

BOUYGUES/2011 Half-year review Half-year review of operations

Condensed consolidated income statement

(€ million) First half %

change 2010 2011

Sales 14,655 15,214 +4% Current operating profit 7111 752 +6% Operating profit 698 752 +8% Cost of net debt (162) (134) -17% Other financial income and expenses 36 (2) nm Income tax expense (204) (223) +9% Share of profits and losses from associates 237 91 -62% Net profit 605 484 -20% Minority interests (73) (93) +27% Net profit attributable to the Group 532 391 -27%

1 The figure reported on 31 August 2010 was €698 million. -€13 million was reclassified to other operating income and expenses at Colas

First-quarter consolidated income statement

(€ million)

First quarter

% change

2010 2011 Sales 6,443 6,686 +4%

Current operating profit 1701 153 -10% Operating profit 162 153 -6%

Net profit attributable to the Group 181 34 -81%

1 The figure reported on 1 June 2010 was €162 million. -€8 million was reclassified to other operating income and expenses at Colas

Second-quarter consolidated income statement

(€ million)

Second quarter

% change

2010 2011 Sales 8,212 8,528 +4%

Current operating profit 5411 599 +11% Operating profit 536 599 +12%

Net profit attributable to the Group 351 357 +2%

1 The figure reported on 31 August 2010 was €536 million. -€5 million was reclassified to other operating income and expenses at Colas

6

BOUYGUES/2011 Half-year review Half-year review of operations

Sales by business area

(€ million)

First half

% change

Change like-for-like and at

constant exchange

rates

2010

2011

Bouygues Construction 4,530 4,705 +4% +1% Bouygues Immobilier 1,313 1,098 -16% -16% Colas 5,002 5,400 +8% +4% TF1 1,285 1,278 -1% -4% Bouygues Telecom 2,732 2,866 +5% +5% Holding company and other 70 64 nm nm

Intra-Group elimination (277) (197) nm nm

Total 14,655 15,214 +4% +1%

o/w France 10,4011 11,064 +6% +4% o/w international 4,2541 4,150 -2% -6%

1 Following the change in status of Mayotte that has become a French department, sales were reclassified to France Contribution of business areas to EBITDA

(€ million)

First half

% change

2010 2011

Bouygues Construction 307 252 -18% Bouygues Immobilier 91 86 -5% Colas 1481 190 +28% TF1 123 234 +90% Bouygues Telecom 734 665 -9% Holding company and other (19) (19) nm TOTAL 1,3841 1,408 +2%

1 The figure reported on 31 August 2010: €1,378 million for the Group and €142 million for Colas.-€6 million was reclassified to other operating income and expenses at Colas

Contribution of business areas to Current operating profit

(€ million)

First half

% change

2010 2011

Bouygues Construction 144 165 +15% Bouygues Immobilier 109 91 -17% Colas (34)1 0 nm TF1 104 187 +80% Bouygues Telecom 409 331 -19% Holding company and other (21) (22) nm TOTAL 7111 752 +6%

1 The figure reported on 31 August 2010: €698 million for the Group and -€47 million for Colas. -€13 million was reclassified to other operating income and expenses at Colas

7

BOUYGUES/2011 Half-year review Half-year review of operations

Contribution of business areas to Net profit attributable to the Group

(€ million)

First half

% change

2010 2011

Bouygues Construction 89 94 +6% Bouygues Immobilier 56 56 = Colas (28) 2 nm TF1 32 51 +59% Bouygues Telecom 237 191 -19% Alstom 216 94 -56% Holding company and other (70) (97) nm TOTAL 532 391 -27%

Net cash by business area

(€ million)

At end-June

Change €m

2010 2011

Bouygues Construction 2,922 2,236 -€686m Bouygues Immobilier 58 390 +€332m Colas (952) (1,046) -€94m TF1 (120) 11 +€131m Bouygues Telecom (505) (619) -€114m Holding company and other (5,608) (5,313) +€295m TOTAL (4,205) (4,341) -€136m

Contribution of business areas to Cash flow

(€ million)

First half

% change

2010 2011

Bouygues Construction 245 260 +6% Bouygues Immobilier 97 94 -3% Colas 164 220 +34% TF1 132 220 +67% Bouygues Telecom 715 659 -8% Holding company and other 104 49 nm TOTAL 1,457 1,502 +3%

8

BOUYGUES/2011 Half-year review Half-year review of operations

Contribution of business areas to Net capital expenditure

(€ million)

First half

% change

2010 2011

Bouygues Construction 114 121 +6% Bouygues Immobilier 1 4 x4 Colas 135 159 +18% TF1 21 18 -14% Bouygues Telecom 227 348 +53% Holding company and other 3 1 nm TOTAL 501 651 +30%

9

BOUYGUES/2011 Half-year review Half-year review of operations

Bouygues share ownership structure at 30 June 2011 Capital

Voting rights

10

BOUYGUES/2011 Half-year review Half-year review of operations

Bouygues Construction

Bouygues Construction is a world leader in building, civil works, energy and services. Combining the strength of a large group with the responsiveness of a network of companies, its know-how includes project financing, design, construction, operation and maintenance. Key figures

(€ million) H1

Change 2010 2011

Sales o/w France o/w International

4,530 2,538 1,992

4,705 2,665 2,040

+4% +5% +2%

Operating profit 144 165 +15% Net profit attributable to the Group 89 94 +6%

Half-year highlights Bouygues Construction took orders worth a very satisfactory €6,134 million in the first half of 2011, stable in relation to the same period of the previous year (€6,105 million, i.e. an increase of €29 million). The order intake in France, up €864 million to €3,744 million, includes the Balard project, which involves the financing, design and construction of a new Defence Ministry complex in Paris, plus a 30-year operation and maintenance contract. International orders, down €835 million at €2,390 million, include the €464-million order book of Leadbitter, a British building firm acquired at the end of 2010. For information, the international order intake in the first half of 2010 included five projects worth over €300 million each. The order intake in the first half of 2011 includes long-term contracts (more than five years) worth €676 million for ETDE, compared with €568 million in the first half of 2010. The order book at 30 June 2011 amounted to €15.5 billion, another record and 12% higher than at end-June 2010. 52% of orders are on international markets, compared with 54% at 30 June 2010. The order book gives increasing visibility, since the share of orders at more than two years rose by 19% over the preceding 12 months to €5.6 billion. Overall sales in the first half of 2011 increased 4% to €4,705 million, rising by 5% in France to €2,665 million and by 2% on international markets to €2,040 million. Like-for-like and at constant exchange rates, the increase was 1%, taking account of the inclusion of Leadbitter and a positive exchange-rate effect mainly due to the appreciation of the Swiss franc. Operating profit rose €21 million to €165 million, representing 3.5% of sales compared with 3.2% in the first half of 2010. Although interest rates on surplus cash remained very low, net financial income rose by €4 million to €20 million. The net margin at end-June 2011 was 2.0%, the same as at end-June 2010, giving a net profit of €94 million. After the financing of capital expenditure and payment of the dividend in April 2011, the cash position net of financial debt stood at €2,236 million, down €620 million on end-December 2010.

11

BOUYGUES/2011 Half-year review Half-year review of operations

BUILDING AND CIVIL WORKS The Building and Civil Works activity generated €3,959 million, including €2,145 million in France and €1,814 million on international markets. France Sales in France in the first half of 2011 amounted to €2,145 million, 5% more than in the first half of 2010. Bouygues Bâtiment Ile-de-France, the leader on its market, is involved in numerous renovation and construction projects, including public buildings such as the Paris Philharmonic Hall in La Villette and the National Archives in Pierrefitte to the north of Paris, residential complexes and office buildings. Two major projects were delivered in the first half of the year: Tour First in La Défense, the biggest renovation project in France with HQE® High Environmental Quality certification, and a new shopping centre in Aubervilliers, to the north of Paris. The five regional subsidiaries of Bouygues Entreprises France Europe operate in both the building and civil works sectors in France. They are particularly involved in the construction of public infrastructure for healthcare (Amiens-Picardie hospital and the new regional hospital at Orléans), justice (a new prison in Réau, near Lille, is scheduled for delivery in the second half of the year), education and leisure (reconfiguration of the existing Stade Vélodrome in Marseille which will remain in operation throughout the works). Bouygues Travaux Publics and DTP Terrassement are involved in civil engineering work for the Flamanville EPR nuclear power plant, the largest ongoing construction project in Europe. Europe (except France) Sales in Europe (except France) amounted to €797 million in the first half of 2011, 1% down on the previous year. In the United Kingdom, Bouygues UK is involved in PFI (Private Finance Initiative) and Design & Build projects in the London area. Warings, which operates in the south of England, benefits from a diversified portfolio of activities. Bouygues Construction strengthened its regional coverage at the end of 2010 with the acquisition of an interest in Leadbitter, an Oxford-based building firm with operations throughout the south of England. Bouygues Travaux Publics is completing a new tunnel under the River Tyne at Newcastle in the framework of a concession agreement. In Switzerland, Bouygues Construction is taking advantage of its expertise in putting together complex property development projects. Losinger Construction is basing its expansion in the German-speaking part of the country on its subsidiary Marazzi. In Croatia, Bouygues Travaux Publics in partnership with DTP Terrassement is completing the widening of the Istria motorway. In Ukraine, Bouygues Travaux Publics, with other partners, is building the new Chernobyl confinement shelter, which will ultimately enable the damaged reactor to be dismantled. In Eastern Europe, subsidiaries in Poland and the Czech Republic are continuing to expand their building activities.

12

BOUYGUES/2011 Half-year review Half-year review of operations

In Finland, Bouygues Travaux Publics has completed civil engineering work on the Olkiluoto EPR nuclear power plant for Areva. Bouygues Construction also has smaller-scale operations in Hungary, Russia, Spain and Portugal. International (except Europe) Sales on international markets (except Europe) in the first half of 2011 amounted to €1,017 million, up 9% on the previous year. In Asia-Pacific, Bouygues Construction has strong local operations in Hong Kong, Singapore, Turkmenistan and Thailand. Dragages Hong Kong is involved in building projects including the civil aviation headquarters and Kai Tak Cruise Terminal, civil works (two sections of tunnel for the future high-speed rail link between Hong Kong and Canton) and electrical and HVAC engineering through a specialist subsidiary, BYME. In Singapore, work has started on the Sports Hub, the world's largest sports PPP project. In South Korea, Bouygues Travaux Publics is completing work on the port at Pusan under a concession agreement. In Africa, Bouygues Construction has operations in several countries. In South Africa, Bouygues Travaux Publics is finishing work on the Gautrain, an 80-km railway link between Johannesburg International Airport, Johannesburg and Pretoria. In Equatorial Guinea, Bouygues Bâtiment Guinée Equatoriale is involved in building, road construction and civil engineering, especially the major Bata motorway project. In Morocco, Bouygues Construction is continuing work on a second container port for Tangiers, Tanger Med 2. In Egypt, Bouygues Travaux Publics is helping to build Cairo's third subway line. In the Middle East, Bouygues Bâtiment International, in partnership with two local firms, is building the QP District in Doha (Qatar), a vast 700,000-sq metre real-estate complex. In Abu Dhabi, VSL is building the first cable-stayed bridge in the United Arab Emirates, linking Hodariyat Island to Abu Dhabi. In the Americas/Caribbean zone, Bouygues Bâtiment International is involved in two PPP projects in Canada: work is nearing completion on Surrey Hospital and has recently started on a headquarters building for the Royal Canadian Mounted Police. In the United States, Bouygues Travaux Publics is continuing work on a tunnel for the port of Miami under a 35-year PPP contract. In Cuba, Bouygues Bâtiment International builds turnkey luxury hotel projects and is currently working on a major tourist complex around a marina at Varadero. ENERGY AND SERVICES ETDE contributed €746 million to Bouygues Construction's consolidated first-half sales, virtually the same as in the first half of 2010. Sales in France amounted to €520 million, compared with €490 million at end-June 2010. A major street-lighting contract in Paris with an energy performance commitment was booked. ETDE also started three new contracts concluded in 2010, including a 20-year contract in Thiais, near Paris, that includes a commitment to reduce electricity consumption by a third. Exprimm, ETDE's facility management subsidiary, is also involved in PPP contracts in partnership with the group's construction subsidiaries. In the first half of the year, with Bouygues Bâtiment Île-de-France, it concluded a maintenance contract for the French Ministry of Defence Balard project. ETDE is the electrical and HVAC engineering contractor

13

BOUYGUES/2011 Half-year review Half-year review of operations

for hospitals in Metz and Amiens. Axione, another ETDE subsidiary specialising in network infrastructure, is involved in 14 public service delegations, representing 7,600 km of optical fibre serving six million people, making it a leading player in the development of broadband and digital networks in France. International sales at end-June 2011 amounted to €226 million, compared with €257 million at end-June 2010. ETDE operates through local subsidiaries that are well-established on their markets in Europe (mainly the UK and Switzerland) and Africa (mainly the Republic of the Congo and Gabon). In Canada, Ecovert FM has a 30-year FM contract for Surrey Hospital and a 25-year contract for the RCMP headquarters. ETDE is also involved in other major international projects, such as the ongoing construction and renovation of 500 km of power lines and substations in the Republic of the Congo for an international oil company. Outlook for 2011 Bouygues Construction's sales target for 2011 is €9.6 billion, up 4% on 2010. With several major projects getting under way, especially in Asia, Bouygues Construction has a relatively clear view of the future and can count on:

secured sales at 30 June 2011 to be executed in the year worth €9.1 billion, covering

95% of forecast sales; sustained activity on international markets (outside Europe), especially in countries

less affected by the economic crisis, such as Hong Kong, Singapore and Qatar;

a long-term order book (more than five years) worth €2.3 billion at 30 June 2011;

a sound financial structure, with a net cash position of €2.2 billion;

an expanding range of sustainable construction products and services, in many cases involving energy and environmental performance commitments.

Tight control over the execution of major projects and a high-quality order intake in a context of fierce competitive pressure will continue to be central priorities for Bouygues Construction. Sales target 2011

(€ million) 2010 2011 target Change

Sales 9,235 9,600 +4%

14

BOUYGUES/2011 Half-year review Half-year review of operations

Bouygues Immobilier Bouygues Immobilier is France's leading property developer, with 34 branches around the country and four subsidiaries elsewhere in Europe. A standard-setter in the ecocity movement, the company develops urban, residential, serviced residence and commercial projects. Key figures

(€ million) H1 Change

2010 2011

Sales 1,313 1,098 -16% o/w Residential 981 923 -6%

o/w Commercial 332 175 -47%

Current operating profit 109 91 -17% Current operating margin 8.3% 8.3% = Net profit attributable to the Group 56 56 = Net cash at end of period1 58 390 +332

1Net cash minus current and non-current financial debt and corresponding financial instruments. Context The housing market slowed in the first half of 2011 after an excellent year in 2010, sustained by historically low interest rates and government stimulus measures, including a doubling of zero-interest loans, the Pass-foncier® scheme for first-time owner-occupiers and tax incentives for investors in buy-to-let properties. The slowdown was attributable to economic uncertainty, a rise (albeit slight) in interest rates and waning interest from investors. The commercial property market was still hesitant despite some signs of picking up again. In this context, Bouygues Immobilier recorded a 6% increase in its order intake to €1,314 million. Sales amounted to €1,098 million, 16% down on the same period in 2010, mainly due to the completion of major commercial property projects. Residential property sales started to rise again in the second quarter. The operating margin remained stable at 8.3% due to good profitability in the residential segment. Sales and results were in line with the roadmap for the year.

15

BOUYGUES/2011 Half-year review Half-year review of operations

Half-year highlights Business performance Reservations

H1 Change 2010 2011

Total in €m Residential

1,243 1,314 +6%

Units 7,320 5,769 -21% Value (€m) 1,175 990 -16%

Commercial Surface area (sq. m) 28,000 83,000 x 3 Value (€m) 68 324 x 5

Residential property Residential property reservations fell back 21% in unit terms, consistent with the overall market trend. However, they remained at a high level after an exceptional year in 2010. In response to falling demand from private investors, Bouygues Immobilier is targeting owner-occupiers, especially first-time buyers, rolling out products at affordable prices. A number of competitively priced projects have been marketed in urban development zones, where the lower 5.5% rate of VAT applies. Benefiting from the leverage generated by enhanced zero-interest loans, these products have proved highly successful. Commercial property In a still-sticky market, commercial property reservations jumped sharply in the first half of 2011 to €324 million. This figure includes the sale to Scor of Green Office® Meudon, the first large-scale positive-energy office building in France, and the conclusion of two property development contracts, one for the co-development with Sogeprom of the D² tower in La Défense and one for the Paris Bar Law School in Issy-les-Moulineaux that will accommodate 1,500 students on completion. Bouygues Immobilier is also pursuing its strategy of becoming a flagship player in sustainable urban development and has recently been named developer of the Wacken eco-community in Strasbourg, France's first positive-energy neighbourhood. Order book

(€ million) End-December 2010

End-June 2011

Order book 2,280 2,537 o/w Residential 2,216 2,337 o/w Commercial 64 200

The order book rose substantially to €2,537 million, including €2,337 million in the residential segment representing 14 months of sales.

16

BOUYGUES/2011 Half-year review Half-year review of operations

Outlook and strategy Bouygues Immobilier expects the residential property market to pick up in the second half of 2011, sustained by stronger demand from private investors who, as in the latter part of 2010, will want to take advantage of the 22% tax break on low-energy buildings before the changes to the scheme announced by the government for 2012, and by the ongoing success of the enhanced zero-interest loan scheme for first-time buyers. With low-energy certification for all its products and its entry-level to mid-range positioning, well-suited to first-time buyers, Bouygues Immobilier intends to continue to increase its share of the residential property market in France over the year as a whole. In the commercial property segment, Bouygues Immobilier is continuing its strategy of controlling risk by developing projects for clearly identified operators. Bouygues Immobilier's objective of preserving a solid financial structure remains unchanged. 2011 sales target

(€ million) 2010 2011 target Change

Sales 2,418 2,440 +1%

17

BOUYGUES/2011 Half-year review Half-year review of operations

Colas

With more than 800 profit centres and 1,400 production units in 40 countries around the world, Colas is a leading player in the roadbuilding and maintenance sectors. Operating in all transport infrastructure markets, the firm offers complementary services including the manufacture and installation of road safety and signalling equipment, civil engineering, pipes and mains, the manufacture and laying of waterproofing membranes, building, and the construction and maintenance of railway infrastructure. Colas also operates infrastructure concessions, especially for motorways. Key figures

(€ million) H1

Change 2010 2010 2011

Sales o/w France o/w International

5,002 3,069 1,933

5,400 3,522 1,878

+8.0% +14.8%

-2.8%

11,661 6,731 4,930

Operating profit/(loss) (47) 0 47 313 Net profit/(loss) attributable to the Group (29) 2 31 224

Contribution to Bouygues' consolidated net profit (28) 2 30 216

Consolidated sales at 30 June 2011 amounted to €5.4 billion compared with €5.0 billion at end-June 2010, an increase of 8.0% (4.1% like-for-like and at constant exchange rates), boosted by a significant increase in business in mainland France and, to a lesser extent, in northern Europe. Half-year highlights

Acquisition of a 50% stake in Gamma Materials Ltd, a Mauritian producer of aggregates, ready-mixed concrete and blocks.

Award of a concession for a 105-km section of the A63 motorway in southwest France.

Good order intake in the first half of the year, with the renewal of railway renovation

contracts in France for the period 2013-2015, a tramway in Tours and airport extensions at Mauritius and Fort McMurray in Canada and Anchorage in Alaska.

€47 million increase in operating profit in comparison with H1 2010, due to:

- better weather conditions than in the first half of 2010, except in North America,

- the first effects of the rightsizing and cost control plans introduced in 2010,

- the stemming of losses in central Europe,

- the absence of non-current operating charges (€13 million in the first half of 2010). France

18

BOUYGUES/2011 Half-year review Half-year review of operations

Sales in France at end-June 2011 were up 14.8% on the same period in the previous year to €3.5 billion. Sales in mainland France in the first half of the year amounted to €3.3 billion, 15.4% higher than at end-June 2010 (9.6% like-for-like). Sales by roads subsidiaries were up 12% on the figure at end-June 2010 due to mild

winter weather which favoured activity in the first quarter, unlike in the previous year. Taking higher construction costs into account, the increase in constant euro terms may be estimated at 7%. Considerable disparities remain in local authority investment, both between regions and between urban and rural areas, and the roads market showed little change from the previous year, with no real sense of direction despite a slight upturn in private investment and numerous public transport projects in urban areas. In this context, and with prices remaining low, there was no let-up in the pressure on margins.

Sales at all non-road subsidiaries were 6.5% higher than at end-June 2010, driven by a

rise in the waterproofing business that offset a decline in the pipes and mains and building segments, with the railway and road safety/signalling businesses remaining stable.

Sales to third parties of refined oil products (basic oils, paraffin and fuel oils) generated

an additional €162 million in relation to end-June 2010 (SRD was acquired on 30 June 2010). Sales to roadbuilding subsidiaries of bitumen produced by SRD are eliminated on consolidation.

In French overseas departments (including Mayotte), sales rose 5% on the back of steady activity in French Guiana and Mayotte and a slight upturn on Réunion, though the market in the Caribbean remained depressed. International International sales amounted to €1.9 billion at 30 June 2011, down 2.8% on 30 June 2010 (-3.6% like-for-like and at constant exchange rates). Sales in North America amounted to €664 million, down slightly by 1.6% on end-June 2010 (-1.2% like-for-like and at constant exchange rates). Adverse weather conditions, especially in Canada but also in the United States, delayed the pickup in activity and affected worksite productivity until May. Sales in northern Europe rose 3% to €548 million. Higher sales in Belgium, Denmark and Switzerland offset a decline in activity in Ireland and the United Kingdom. As expected, sales in central Europe fell by around 20%, with Slovakia, Hungary and Romania the worst affected. Subsidiaries in the rest of the world reported sales of €435 million, the same level as at end-June 2010. Growth in Asia and Australia offset a slight fall in Africa and the Indian Ocean (Madagascar).

19

BOUYGUES/2011 Half-year review Half-year review of operations

Production of materials A significant proportion of Colas' activity, both in France and elsewhere, consists in the production of construction materials, especially aggregates. 46.4 million tonnes of aggregates (-3%), 17.5 million tonnes of asphalt mixes (+1%) and 716,000 tonnes of binders and emulsions (-5%) were produced in the six months to 30 June 2011. Outlook The order book at end-June 2011 amounted to €7.2 billion, practically the same as at end-June 2010. Orders in mainland France amounted to €3.6 billion, 1% higher than at end-June 2010. Orders in French overseas departments and on international markets remained stable, also at €3.6 billion. The high level of orders, despite robust activity in the first six months, bodes well for the second half of the year. For 2011 as a whole: activity in mainland France is expected to increase by over 5%, with sales in overseas

departments remaining close to last year's figure; in North America, the high level of orders at end-June points to a bright outlook for the

year as a whole, as long as the weather is better than in the first six months, enabling orders to be executed;

in central Europe, the planned scaling-back of activity to the expected market level over the coming years is going ahead in accordance with the strategy defined in 2010;

in northern Europe, due to a tough comparison base in 2010, activity could decline by around 10% because of budget cuts in the UK and Ireland; in the rest of the world, activity could be very slightly lower due to less buoyant markets in Africa.

On the basis of currently available data, the sales target for 2011 has been adjusted up from €11.8 billion at the start of the year to €11.9 billion. The first effects of the rightsizing measures taken since mid-2010 have confirmed an improvement in profitability in 2011. 2011 sales target

(€ million) 2010 2011 target Change

Sales 11,661 11,900 +2.0%

20

BOUYGUES/2011 Half-year review Half-year review of operations

TF1

The TF1 group's mission is to inform and entertain. While continuing to strengthen its position in its core television business with free and pay channels, it has diversified into the internet, audiovisual rights, production and licences. Key figures

(€ million) H1 Change

2010 2011

Sales TF1 channel advertising Other activities

1,284.6 764.6 520.0

1,277.6 757.8 519.8

-0.5% -0.9%

= Operating profit 104.4 186.5 +78.6%

Net profit attributable to the Group 74.2 118.6 +59.8%

The TF1 group's consolidated sales over the first six months of the year remained virtually stable at €1,287 million (down 0.5%). This figure comprises: revenue from advertising on the TF1 channel of €758 million, very slightly lower

(-0.9%) than in the first half of 2010. TF1 did not show any major sporting events in the first half of 2011, unlike in the previous year (2010 FIFA World Cup). Nevertheless, advertising revenue in the second quarter of 2011 was up 0.7% year-on-year and up 14% on the first quarter of 2011;

revenue from other activities of €520 million, stable year-on-year. Higher sales resulting

from the acquisition of TMC and NT1 were offset to a considerable extent by the absence of sporting rights sales.

Operating profit in the first half of 2011 amounted to €186.5 million, €82.1 million more than in the first half of 2010, a rise of 78.6%. The current operating margin rose to 14.6%, compared with 8.1% in the first half of 2010 and 8.8% over the whole of the year. The second-quarter operating margin rose to 18.8%, compared with 8.8% in the second quarter of 2010. Net profit attributable to the Group in the first half of 2011 amounted to €119 million, compared with €74 million in the first half of 2010. Half-year highlights The TF1 group kept its unrivalled position in free-to-air television in France, with TF1,

TMC and NT1 gaining an aggregate audience share of 29.1% among individuals aged four years and over and 32.9% among women under 50 who are purchasing decision-makers.

21

BOUYGUES/2011 Half-year review Half-year review of operations

The TF1 group had a cash surplus of €11 million at end-June 2011. The strength of its financial position was underlined when Standard & Poor's upgraded its rating from BBB with positive outlook to BBB+ with stable outlook.

1. French broadcasting

a. TF1 core channel

In the first half of the year, the TF1 core channel won an audience share of 23.8% among individuals aged four years and over and 26.8% among women under 50 who are purchasing decision-makers. It also achieved the top 50 audience ratings. The cost of programmes shown on TF1 amounted to €424 million in the first half of 2011, compared with €483 million in the same period of the previous year. The €59-million drop (12.2%) was due to the absence of the 2010 FIFA World Cup, which represented a saving of €49 million on rights net of replacement programme costs, and savings of €10 million on other programmes. Sales by the TF1 core channel fell 1.2% in the first six months of 2011 to €761 million, including €758 million of net advertising revenue, down 0.9%. Television remained the top medium for advertising spend in the first half of 2011 and TF1 confirmed its status as France's leading mass media outlet. The advertising sales department continued its value-recovery strategy even without any major sporting event, like the FIFA World Cup in 2010. With a €75-million increase in operating profit to €132 million, the operating margin in the first half of the year jumped 9.9 points from 7.4% in the first half of 2010 to 17.3%. b. Other activities Téléshopping generated sales of €54 million in the first half of 2011 compared with €58 million in same period of the previous year, a drop of 7%. This was mainly due to a decline in its core business and in the infomercials business, where the number of orders rose but the average value fell. This decline was partly offset by the success of Place des Tendances, an online fashion shopping site that now has a catalogue of 200 brands. Operating profit fell €3 million to €1 million. Theme channel sales jumped 48.4% to €160 million, due partly to full consolidation of TMC and NT1 from 1 July 2010 but also to an excellent increase in audience share by TMC, TV Breizh and LCI. Operating profit rose €16 million to €28 million, giving an operating margin of 17.4%. TF1 Entreprises reported a 5.1% rise in half-year sales to €17 million on the back of successes in the music business, including productions like the Prêtres I and II CDs, coproductions like the Black Eyed Peas, the musical Mozart Rock Opera, and the division's trade-mark and licence agency business. Operating profit amounted to €2.6 million compared with €0.3 million in the first half of 2010, giving an operating margin of 15.7%. At e-TF1, the sale of videos over the internet and the rollout by new operators of MyTF1, an enhanced television portal, drove revenue growth to €39 million, a rise of 3.5%. Profitability improved to €3.1 million, a €3-million increase over one year.

22

BOUYGUES/2011 Half-year review Half-year review of operations

2. Audiovisual rights The Catalogue division reported half-year sales of €12 million compared with €24 million in the first half of 2010. This decline was due to less successful cinema releases than in the first half of 2010 and the restatement of sales with TMC and NT1 as intragroup sales. Against a background of tumbling DVD prices, sales by TF1 Vidéo rose 7.9% to €38 million as a result of higher volume sales and the expansion of video on demand (VOD). The division incurred an operating loss of €11 million, which includes a provision for the Miracle at St Anna dispute. 3. International broadcasting

Sales at the international broadcasting division (Eurosport International) fell back 4.1% despite a steady rise in subscription revenue, due to the uncertain economic climate, the lack of major sporting events in the first half of 2011 and the corresponding impact on advertising revenue. Operating profit rose €1 million to €28 million. Eurosport International achieved an operating margin of 15.9%, a 1.2-point improvement attributable to reductions in and close management of programme costs by the TF1 group, which is not showing any major events this year. Outlook In a low-visibility economic environment, the TF1 group confirms that it expects sales to remain stable in 2011. The group is keener than ever to consolidate its position as France's leading provider of news and entertainment on television. Having rationalised its business portfolio, the TF1 group is continuing to expand its diversification activities, which are becoming more successful again. Source: Médiamétrie

23

BOUYGUES/2011 Half-year review Half-year review of operations

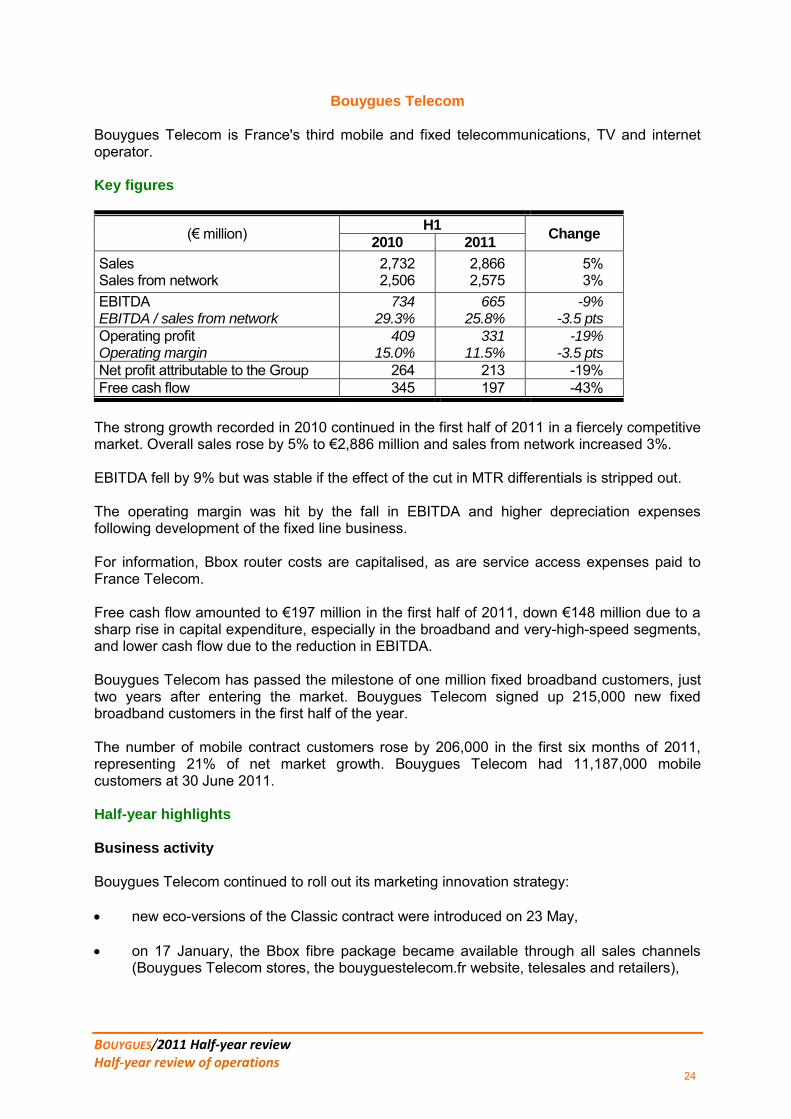

Bouygues Telecom Bouygues Telecom is France's third mobile and fixed telecommunications, TV and internet operator. Key figures

(€ million) H1 Change

2010 2011

Sales Sales from network

2,732 2,506

2,866 2,575

5% 3%

EBITDA EBITDA / sales from network

734 29.3%

665 25.8%

-9% -3.5 pts

Operating profit Operating margin

409 15.0%

331 11.5%

-19% -3.5 pts

Net profit attributable to the Group 264 213 -19%

Free cash flow 345 197 -43% The strong growth recorded in 2010 continued in the first half of 2011 in a fiercely competitive market. Overall sales rose by 5% to €2,886 million and sales from network increased 3%. EBITDA fell by 9% but was stable if the effect of the cut in MTR differentials is stripped out. The operating margin was hit by the fall in EBITDA and higher depreciation expenses following development of the fixed line business. For information, Bbox router costs are capitalised, as are service access expenses paid to France Telecom. Free cash flow amounted to €197 million in the first half of 2011, down €148 million due to a sharp rise in capital expenditure, especially in the broadband and very-high-speed segments, and lower cash flow due to the reduction in EBITDA. Bouygues Telecom has passed the milestone of one million fixed broadband customers, just two years after entering the market. Bouygues Telecom signed up 215,000 new fixed broadband customers in the first half of the year. The number of mobile contract customers rose by 206,000 in the first six months of 2011, representing 21% of net market growth. Bouygues Telecom had 11,187,000 mobile customers at 30 June 2011. Half-year highlights Business activity Bouygues Telecom continued to roll out its marketing innovation strategy: new eco-versions of the Classic contract were introduced on 23 May, on 17 January, the Bbox fibre package became available through all sales channels

(Bouygues Telecom stores, the bouyguestelecom.fr website, telesales and retailers),

24

BOUYGUES/2011 Half-year review Half-year review of operations

the new Neo Pro 24/24 Platinum contract for professionals was launched, including unlimited calls in France, unlimited text messages, 3G+ and 3 hours of international calls.

Bouygues Telecom is continuing its policy of putting customers first. Following the rise in VAT on mobile and fixed services including TV services, Bouygues

Telecom decided not to pass on the higher rate of VAT to its prices. As well as enhancing its brand image, the initiative enabled Bouygues Telecom to lead the market in terms of net growth on the mobile phone segment in the first quarter of 2011.

Bouygues Telecom, Orange, SFR and Atos Origin have cooperated on an innovative

payment solution called “Buyster”, which offers a secure link between a customer's bank card and mobile phone number.

High-quality customer relations continue to be a priority for Bouygues Telecom, which pulled off a historic double by coming top of the customer relations league table for both the mobile phone sector, for the fifth year running, and the fixed line internet sector, after just two years on the market. The quality of the company's HR policy was recognised by the award of the Top Employer label for the second year running. Networks Bouygues Telecom's 3G HSPA network covered 87% of the French population at end-June 2011, thus meeting the requirement under the terms of its licence to cover 75% of the population by the end of 2010. Bouygues Telecom covers all the major towns and cities in France and strives to continually improve its network.

On 4 April, the company extended the ADSL unbundling zone and now has access to over 3,700 subscriber connection nodes. Bouygues Telecom's fixed line network is now comparable to that of its rivals and gives the company a level playing-field on the fixed phone market.

A decision was taken with SFR to jointly build an optical fibre network to the home with 3 million FTTH connections.

A partnership agreement was concluded with Numericable under which Bouygues Telecom can use its optical fibre network to the last amplifier (FTTLA), giving access to a potential market of 7 million households in France.

Regulatory context The voice termination rate was cut by 41% on 1 July 2011 to €0.02 per minute, thus ending the differential with Orange and SFR. The SMS termination rate was also cut by 31% to €0.015. Environment

25

BOUYGUES/2011 Half-year review Half-year review of operations

The Technical Centre in Meudon, near Paris, was awarded HQE Operation certification, recognising the high environmental quality not only of the building but also of the monitoring and maintenance processes for the benefit of users. Outlook Voice and SMS termination rates were cut again on 1 July 2011. Bouygues Telecom considers that the impact of the cut in voice and SMS termination rates is likely to be at least €330 million on 2011 sales and a minimum of €120 million on EBITDA. However, strong organic growth means that sales are expected to rise by 2% over the year as a whole. EBITDA is likely to remain stable in 2011, stripping out the effect of the cut in termination rate differentials. 2011 sales target

(€ million) 2010 2011 target Change

Sales 5,636 5,730 2%

26

BOUYGUES/2011 Half-year review Half-year review of operations

Alstom

Alstom, in which Bouygues has a 30.7% stake, is a world leader in power generation and transmission and rail transport infrastructure and sets the standard in innovative technologies for the protection of the environment. It makes the world's fastest trains and highest-capacity automatic metros. Alstom also provides turnkey power plants, equipment and related services for the production of electricity from all sources, including hydropower, nuclear, gas, coal and wind. It offers a vast range of electricity transmission solutions, especially smart grids. The group has about 93,500 employees in a hundred or so countries and generated sales of €20.9 billion in FY2010/11, ended on 31 March 2011. Operating results in FY2010/11 in line with forecasts, a sharp rise in orders in the second half of the year Alstom published its financial statements for the year ended 31 March 2011 on 4 May 2011. During FY2010/11, Alstom recorded sales of €20.9 billion and an operating profit of €1,570 million, giving an operating margin of 7.5%. Net profit amounted to €462 million, severely hit by non-recurring expenses. The order intake amounted to €19.1 billion, higher than the low level recorded in the previous year. After bottoming out in the first half, orders bounced back in the second half. Free cash flow also improved substantially in the second half of FY2010/11, rising to €447 million, compared with -€963 million in the first half. Results in FY2010/11 reflected an operating performance in line with forecasts. After three consecutive half-years of low orders, the order intake jumped sharply in the second half of FY2010/11, with a stronger fourth than third quarter, as announced. This upturn in the commercial situation generated a substantial improvement in cash flow in the second half of the year. The upturn in orders was driven by numerous successes in emerging countries, where demand is likely to carry on growing, whereas business in developed countries remains sluggish. This geographical shift in demand opens up a new phase for Alstom. In order to grasp future opportunities while remaining competitive, the group plans to adapt the geographical scope of its operations and step up its innovative products and services. Consequently, Alstom continued to expand in the BRICs and concluded several partnership agreements in these key zones. At the same time, rightsizing plans were introduced for certain sites in Europe and North America. Research and development spending was maintained at a high level to enable Alstom to remain at the cutting edge of technology. On 15 June 2011, on a proposal from the Chairman and CEO, Alstom's board of directors approved major changes to the group's organisation, which took effect on 4 July 2011. They included the appointment of a Deputy CEO, the reshaping of operational activities into four sectors (Thermal Power, Renewable Power, Transport, Grid) and a complete overhaul of the Executive Committee. The new organisation is intended to allow the group to better anticipate the structural changes in its businesses, accelerate its development and achieve its performance objectives. Splitting the Power sector into two sectors, Thermal and Renewable, is designed to simplify the working of each entity and to take better account of the specific features of their markets. The shareholders' meeting on 28 June 2011 approved the payment of a dividend of €0.62 per share, compared with €1.24 in the previous financial year.

27

BOUYGUES/2011 Half-year review Half-year review of operations

Recent events

Alstom published its sales for the first quarter of FY2011/12 (1 April to 30 June 2011) on 20 July 2011. Alstom took orders worth €5 billion over the period, 44% more (34% excluding Grid) than in the same period of the previous year. Sales, at €4.5 billion, were down 12% (-23% excluding Grid). The newly created sectors, Thermal Power and Renewable Power, received orders of €2.8 billion and €0.3 billion respectively in the first quarter. Transport booked contracts for small and medium-sized projects worth €1 billion. Grid orders amounted to €0.9 billion. The geographical shift of orders towards emerging countries seen over the previous six months was confirmed, since they accounted for 63% of new orders booked. Thermal Power and Transport saw sales drop sharply in the first quarter of FY2011/12 in relation to the first quarter of FY2010/11, hitting a low that was the consequence of the previous low order intake. The total order book amounted to €47 billion at 30 June 2011, representing 28 months of sales. Outlook

Alstom's financial structure is solid and an improvement is expected in the second half as a result of the combined effect of the recent upturn in orders and the benefits of the restructuring plan. On that basis, Alstom confirmed that it expects an operating margin of between 7% and 8% for FY2011/12, as already announced.

28

BOUYGUES/2011 Half-year review Half-year review of operations

II – MAIN RISKS AND UNCERTAINTIES IN H2 2011 This report contains forward-looking statements. Those statements, which express targets based on current assessments and estimates, are subject to the risks and uncertainties described below. The main risks and uncertainties that the Group could face in the second half of 2011 are similar to those described in the 2010 Registration Document (pages 139-159). III – RELATED-PARTY TRANSACTIONS

No related-party transactions liable to materially affect Bouygues' financial situation or results were concluded in the first half of 2011. Likewise, no change to related-party transactions liable to materially affect Bouygues' financial situation or results occurred during that period. Under the terms of agreements approved by the Board of Directors and the Shareholders' Meeting, Bouygues provided services to its sub-groups, mainly in the areas of management, human resources, information systems and finance. More detailed information about related-party transactions is given in Note 13 of the notes to the condensed consolidated first-half financial statements. IV – RECENT EVENTS A number of significant events occurred in July and August 2011. Most of the Gautrain transport system linking Pretoria, Johannesburg and Johannesburg International Airport was brought into service on 2 August 2011. Bouygues Construction has started work on redeveloping the site of the old Laënnec Hospital in the 7th arrondissement of Paris, a project worth a total of around €150 million. On 28 July, TF1 finalised the acquisition of Metro International's 65.7% stake in Metro France, a free newspaper, making TF1 the sole owner. TF1 Droits Audiovisuels, the producer and the authors/directors of the film Miracle at St Anna ended the dispute as a result of which the Paris civil court of first instance, on 21 June 2011, ordered TF1 to pay €32 million in compensation. The calls for tender for the allocation of frequencies in the 800 MHz and 2.6 GHz bands were published on 15 June 2011. The frequencies will be allocated in late 2011 and early 2012. During the summer Bouygues Telecom launched B&You in the form of three no-commitment plans designed to meet the needs of new, more autonomous users at ease with new technologies. The new initiative is based on a new model: The creation of value from data traffic, Low marketing costs, mainly due to the absence of handset subsidies Increased customer participation via the use of Web 2.0 tools (social networks,

community help forums etc.) and the involvement of customers in the development of the service

Alstom has won a number of major contracts, including a €330-million contract to operate and maintain a gas-fired power station in Israel, an order worth €200 million for 66 trainsets for the

29

BOUYGUES/2011 Half-year review Half-year review of operations

Paris metro, electricity transmission contracts worth €100 million in Australia, an €80-million contract as part of the programme to rebuild the energy network in Iraq and a €90-million contract for a turnkey rail system in Indonesia.

30

BOUYGUES/2011 Half-year review Condensed consolidated first-half financial statements

CONDENSED CONSOLIDATED FIRST-HALF FINANCIAL STATEMENTS

31

CONSOLIDATED BALANCE SHEET AT 30 JUNE 2011 € million

ASSETS30/06/2011

Net

31/12/2010

Net

30/06/2010

Net

Property, plant and equipment 6,144 6,159 5,945

Intangible assets 966 990 988

Goodwill (1) 5,552 5,531 5,197

Investments in associates (2) 5,062 5,020 5,234

Other non-current financial assets 801 659 773

Deferred tax assets and non-current tax receivable 235 261 273

Non-current assets 18,760 18,620 18,410

Inventories, programmes and broadcasting rights 2,811 2,680 2,686

Advances and down-payments on orders 441 396 430

Trade receivables 7,532 6,167 7,173

Tax asset (receivable) 137 134 82

Other current receivables and prepaid expenses 2,257 1,982 2,231

Cash and equivalents 3,303 5,576 4,144

Financial instruments (3) 10 13 19

Other current financial assets 24 18 44

Current assets 16,515 16,966 16,809

Assets held for sale and discontinued operations

Total assets 35,275 35,586 35,219

LIABILITIES AND SHAREHOLDERS' EQUITY 30/06/2011 31/12/2010 30/06/2010

Shareholders' equity

- Share capital 366 366 356

- Share premium and reserves 8,591 8,027 7,785

- Translation reserve (24) 8 62

- Treasury shares (324) (155) (45)

- Consolidated net profit for the period 391 1,071 532

Shareholders' equity attributable to the Group 9,000 9,317 8,690

Minority interests 1,253 1,290 1,163

Shareholders' equity 10,253 10,607 9,853

Non-current debt 6,835 6,750 6,295

Non-current provisions 1,872 1,870 1,816

Deferred tax liabilities and non-current tax liabilities 130 112 92

Non-current liabilities 8,837 8,732 8,203

Advances and down-payments received 1,452 1,413 1,415

Current debt 268 994 1,538

Current taxes payable 111 137 118

Trade payables 6,629 6,347 6,479

Current provisions 853 930 873

Other current liabilities 6,306 6,089 6,156

Overdrafts and short-term bank borrowings 530 294 504

Financial instruments (3) 21 24 31

Other current financial liabilities 15 19 49

Current liabilities 16,185 16,247 17,163

Liabilities on held-for-sale assets and discontinued operations

Total liabilities and shareholders' equity 35,275 35,586 35,219

Net surplus cash/(net debt) (4,341) (2,473) (4,205)

(1) Goodwill of consolidated entities(2) Associates (including goodwill on associates)(3) Fair value hedges of financial liabilities

BOUYGUES GROUP - CONSOLIDATED FINANCIAL STATEMENTS

32

CONSOLIDATED INCOME STATEMENT

1st half

2011 2010

2nd quarter

2011 2010

Full year

2010

SALES (1) 15,214 14,655 8,528 8,212 31,225

Other revenues from operations 58 76 19 47 144

Purchases used in production (6,624) (6,313) (3,755) (3,610) (13,886)

Personnel costs (3,398) (3,274) (1,753) (1,706) (6,504)

External charges (3,554) (3,371) (1,869) (1,801) (7,091)

Taxes other than income tax (320) (303) (162) (147) (633)

Net depreciation and amortisation expense (664) (653) (355) (348) (1,392)

Net charges to provisions and impairment losses (157) (178) (69) (122) (549)

Changes in production and property development inventories (47) (166) (101) (111) (116)

Other income from operations (2) 576 576 304 296 1,250

Other expenses on operations (332) (338) (188) (169) (688)

CURRENT OPERATING PROFIT 752 711 599 541 1,760

Other operating income 0 0 0 108

Other operating expenses (13) 0 (5) (77)

OPERATING PROFIT 752 698 599 536 1,791

Financial income 42 34 25 21 64

Financial expenses (176) (196) (85) (101) (394)

COST OF NET DEBT (134) (162) (60) (80) (330)

Other financial income 35 92 25 30 101

Other financial expenses (37) (56) (22) (27) (95)

Income tax expense (223) (204) (194) (180) (482)

Share of profits and losses of associates 91 237 67 116 278

NET PROFIT FROM CONTINUING OPERATIONS 484 605 415 395 1,263

Net profit from discontinued and held-for-sale operations 0 0 0

NET PROFIT 484 605 415 395 1,263

Net profit attributable to the Group 391 532 357 351 1,071

Net profit attributable to minority interests 93 73 58 44 192

BASIC EARNINGS PER SHARE FROM CONTINUING OPERATIONS (€) 1.10 1.50 1.00 0.99 3.03

DILUTED EARNINGS PER SHARE FROM CONTINUING OPERATIONS (€) 1.09 1.49 1.00 0.98 3.02

(1) Of which sales generated abroad (including export sales) 4,150 4,254 2,501 2,529 9,649(2) Of which reversals of unutilised provisions and impairment losses/other items 165 158 72 61 371

BOUYGUES GROUP - CONSOLIDATED FINANCIAL STATEMENTS

€ million

33

BOUYGUES GROUP - CONSOLIDATED FINANCIAL STATEMENTS

STATEMENT OF RECOGNISED INCOME AND EXPENSE € million

Net profit for the period 484 605 1,263

Change in cumulative translation adjustment of controlled entities (18) 92 38Net change in fair value of financial instruments used for hedging purposes and of 12 (12)other financial assets (including available-for-sale financial assets) 23Actuarial gains/(losses) on employee benefits (amendment to IAS 19) (1) (15) (11)Share of income and expense recognised directly in equity by associates (1) 34 47 (16)Net tax effect of items recognised directly in equity 0 7 (5)

Income and expense recognised directly in equity 27 119 29

Total recognised income and expense 511 724 1,292

Attributable to the Group 423 640 1,092

Attributable to minority interests 88 84 200

(1) Relates primarily to Alstom (accounted for by the equity method)

Full year

2010

1st half

2011 2010

34

BOUYGUES GROUP - CONSOLIDATED FINANCIAL STATEMENTS

CHANGES IN CONSOLIDATED SHAREHOLDERS' EQUITY - PERIOD ENDED 30 JUNE 2011 € million

POSITION AT 1 JANUARY 2010 2,423 1,823 4,485 (56) (139) 8,536 1,190 9,726

MOVEMENTS IN FIRST HALF OF 2010

Capital and reserves transactions, net 27 451 (451) 27 27

Acquisitions/disposals of treasury shares (45) 83 38 38

Acquisitions/disposals without loss of control 1 1 1

Dividend paid (566) (566) (108) (674)

Other transactions with shareholders 1 (1) 14 14 1 15

Net profit for the period 532 532 73 605

Other recognised income and expense (b) 118 (10) 108 11 119

Total recognised income and expense 0 0 532 118 0 (10) 640 84 724

Changes in scope of consolidation 0 (4) (4)

POSITION AT 30 JUNE 2010 2,451 2,273 4,014 62 (45) (65) 8,690 1,163 9,853

MOVEMENTS IN SECOND HALF OF 2010

Capital and reserves transactions, net 261 7 268 268

Acquisitions/disposals of treasury shares (110) (110) (110)

Acquisitions/disposals without loss of control (3) (3) (3)

Dividend paid 0 0

Other transactions with shareholders (1) 20 19 19

Net profit for the period 539 539 119 658

Other recognised income and expense (b) (54) (33) (87) (3) (90)

Total recognised income and expense 0 0 539 (54) 0 (33) 452 116 568

Changes in accounting policy/scope of consolidation and other items 1 1 11 12

POSITION AT 31 DECEMBER 2010 2,711 2,273 4,574 8 (155) (94) 9,317 1,290 10,607

MOVEMENTS IN FIRST HALF OF 2011

Capital and reserves transactions, net 10 294 (294) 10 1 11

Acquisitions/disposals of treasury shares (169) (3) (172) (172)

Acquisitions/disposals without loss of control (19) (19) (19)

Dividend paid (570) (570) (123) (693)

Net profit for the period 391 391 93 484

Other recognised income and expense (b) (32) 64 32 (5) 27

Total recognised income and expense 0 0 391 (32) 0 64 423 88 511

Other transactions (changes in accounting policy/scope of consolidation and other items) (1) 12 11 (3) 8

POSITION AT 30 JUNE 2011 2,721 2,567 4,100 (24) (324) (40) 9,000 1,253 10,253

(a) Translation reserveAttributable to: Group Minority interests Total

Controlled entities (15) (3) (18)

Associates (17) (17)

(32) (3) (35)

(b) See the statement of recognised income and expense

Minority

interestsTOTAL

Translation

reserve

Treasury

shares

Share

capital &

share

premium

Reserves related

to capital/

retained earnings

Consolidate

d reserves

and profit

for the

period

Items

recognised

directly in

equity

TOTAL

ATTRIBUTABLE

TO THE GROUP

(a)

35

BOUYGUES GROUP - CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED CASH FLOW STATEMENT € million

1st half

2011 2010

Full year

2010

I - CASH FLOW FROM CONTINUING OPERATIONS

A - NET CASH GENERATED BY/(USED IN) OPERATING ACTIVITIES

Net profit from continuing operations 484 605 1,263

Share of profits effectively reverting to associates (1) (110) (124)

Elimination of dividends (non-consolidated companies) (9) (4) (8)

Charges to/(reversals of) depreciation, amortisation, impairment & non-current provisions 683 657 1,481

Gains and losses on asset disposals (15) (56) (91)

Miscellaneous non-cash charges 3 (1) (89)

sub-total 1,145 1,091 2,432

Cost of net debt 134 162 330

Income tax expense for the period 223 204 482

Cash flow 1,502 1,457 3,244

Income taxes paid during the period (189) (244) (501)

Changes in working capital related to operating activities (1)

(1,305) (1,163) (52)

NET CASH GENERATED BY/(USED IN) OPERATING ACTIVITIES 8 50 2,691

Tous

B - NET CASH GENERATED BY/(USED IN) INVESTING ACTIVITIES

Purchase price of property, plant and equipment and intangible assets (695) (532) (1,507)

Proceeds from disposals of property, plant and equipment and intangible assets 44 31 84

Net liabilities related to property, plant and equipment and intangible assets (101) (154) 28

Purchase price of non-consolidated companies and other investments (41) (214) (24)

Proceeds from disposals of non-consolidated companies and other investments 0 218 219

Net liabilities related to non-consolidated companies and other investments 0 5 6

Effects of changes in scope of consolidationPurchase price of investments in consolidated activities (43) (254) (470)

Proceeds from disposals of investments in consolidated activities 20 4 20

Net liabilities related to consolidated activities 0 0 1

Other cash effects of changes in scope of consolidation 1 (25) (51)TousOther cash flows related to investing activities (changes in loans, dividends received from

non-consolidated companies)(104) 12 (47)

NET CASH GENERATED BY/(USED IN) INVESTING ACTIVITIES (919) (909) (1,741)

C - NET CASH GENERATED BY/(USED IN) FINANCING ACTIVITIES

Capital increases paid, movements in treasury shares and other transactions with shareholders (104) (15) 78

Dividends paid during the period: Dividends paid to shareholders of the parent company (570) (566) (566)

Dividends paid to minority shareholders of consolidated companies (123) (108) (108)

Change in debt (639) 690 565

Cost of net debt (134) (162) (330)

Other cash flows related to financing activities 1 84 133

NET CASH GENERATED BY/(USED IN) FINANCING ACTIVITIES (1,569) (77) (228)

D - EFFECT OF FOREIGN EXCHANGE FLUCTUATIONS (29) 121 105

CHANGE IN NET CASH POSITION (A+B+C+D) (2,509) (815) 827

Net cash position at 1 January 5,282 4,455 4,455

Net cash flows during the period (2,509) (815) 827

Other non-monetary flows

Net cash position at end of period 2,773 3,640 5,282

II - CASH FLOWS FROM DISCONTINUED AND HELD-FOR-SALE OPERATIONS

Net cash position at 1 January 0 0 0

Net cash flows during the period 0 0 0

Net cash position at end of period 0 0 0

(1) Definition of change in working capital related to operating activities:

Current assets - current liabilities (excluding income taxes paid, which are reported separately)

36

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS FOR THE SIX MONTHS ENDED 30 JUNE 2011

30 August 2011

37

NOTES

CONTENTS

(Figures in millions of euros unless otherwise indicated)

NOTES

1. Significant events of the period

2. Accounting policies

3. Non-current assets

4. Current assets

5. Consolidated equity

6. Non-current and current provisions

7. Non-current and current debt

8. Main components of change in net debt

9. Analysis of sales and other revenues from operations

10. Operating profit

11. Income tax expense

12. Segment information

13. Related-party information

14. Principal exchange rates

38

Declaration of compliance:

The condensed consolidated financial statements for the six months ended 30 June 2011 have been prepared in accordance with IAS 34, “Interim Financial Reporting”, a standard issued by the IASB and endorsed by the European Union, using the historical cost convention (except for certain financial assets and liabilities measured at fair value). They include comparatives as at and for the periods ended 30 June 2010 and 31 December 2010. The Bouygues group has not early adopted as of 30 June 2011 any standard or interpretation not endorsed by the European Union.

The financial statements are prepared in millions of euros (unless otherwise indicated) and comprise:

the balance sheet;

the income statement and statement of recognised income and expense;

the statement of changes in equity;

the cash flow statement;

the notes to the financial statements.

39

1.0. SIGNIFICANT EVENTS OF THE PERIOD

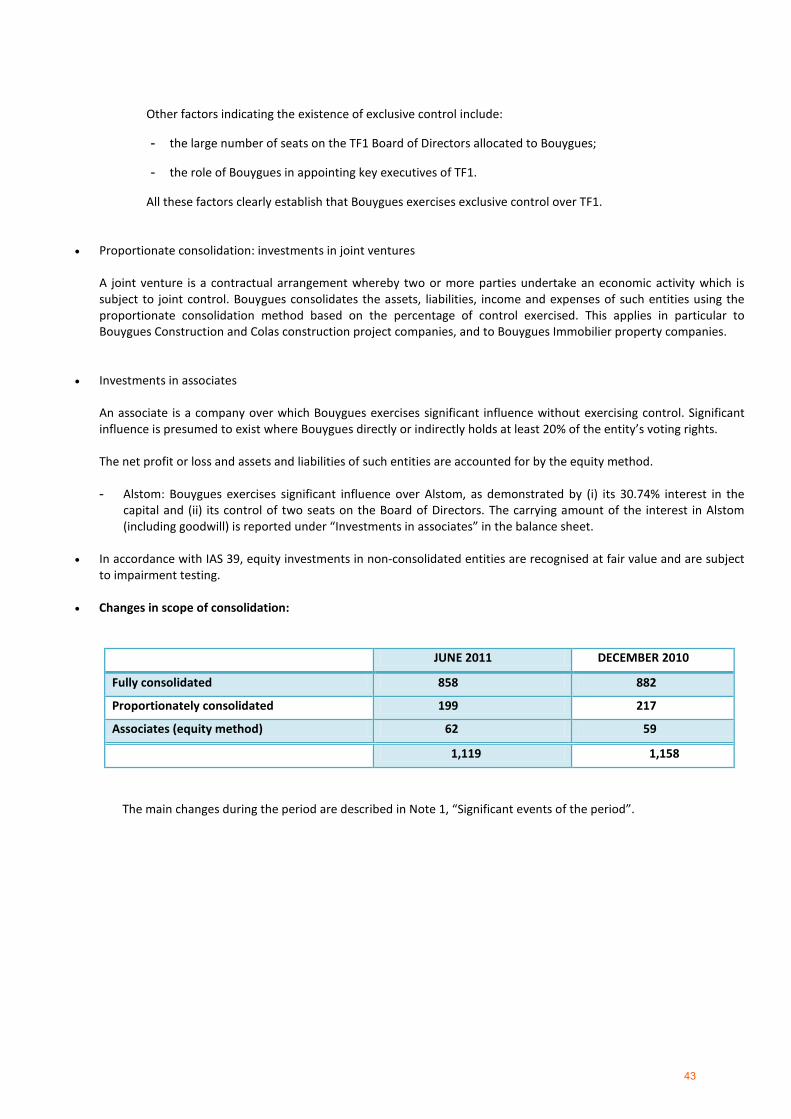

1.1. SCOPE OF CONSOLIDATION AS AT 30 JUNE 2011 1,119 entities were consolidated as at 30 June 2011, against 1,158 at the end of 2010. The net reduction of 39 mainly relates to Colas (various proportionately-consolidated asphalt companies) and to Bouygues Immobilier (deconsolidation of real estate partnerships and property companies on project completion, etc).

Principal acquisitions and other transactions during the period:

• LEADBITTER GROUP (BOUYGUES CONSTRUCTION):

After receiving clearance from the European Commission competition authorities in March 2011, the Bouygues Construction group acquired 51% of the Leadbitter group via the holding company Leadbitter Bouygues H. Ltd. The remaining 49% is held by the Leadbitter management team and is to be acquired within no more than 4 years. The Leadbitter group, which has a construction and house-building business in the United Kingdom, has been fully consolidated in the Bouygues Construction group financial statements with effect from 31 March 2011. The €38 million investment in Leadbitter was recognised in the first half of 2011. The commitment to buy out the minority shareholders in the holding company, amounting to €19 million, has been recognised in non-current debt.

• GAMMA MATERIALS LTD (COLAS): At the end of June 2011, Colas acquired a 50% interest in Gamma Materials Ltd (Mauritius) for €33 million. As at 30 June 2011, this interest is reported in “Investments in non-consolidated companies” pending accounting and financial data. Gamma Materials will be accounted for by the proportionate consolidation method in the second half of 2011. ALSTOM: Alstom is accounted for by the equity method, and is carried at net acquisition cost plus Bouygues’ share of Alstom’s net profit since the acquisition date. On 4 May 2011, Alstom published its results for the financial year ended 31 March 2011. Given the time-lag between the financial year-end of Alstom (31 March) and Bouygues (31 December), the financial contribution of Alstom to the Bouygues group’s net profit for the first quarter of 2011 was €23 million, while the estimate for the second quarter (after eliminating non-recurring charges booked in 2011) is €71 million. This gives a total contribution of €94 million for the first half of 2011. Amortisation of fair value remeasurements of identifiable intangible assets and other items had a negative impact of €8 million on the Bouygues group consolidated income statement in the period (portion attributable to the Bouygues group).

The investment in Alstom is reported under “Investments in associates” in the balance sheet, at a carrying amount of €4,425 million, including goodwill of €2,593 million.

1.2. CONSOLIDATED SALES FOR THE FIRST HALF OF 2011

Consolidated sales were €15,214 million, 3.8% higher than in the first half of 2010.

1.3. SIGNIFICANT EVENTS AND CHANGES IN SCOPE OF CONSOLIDATION SUBSEQUENT TO 30 JUNE 2011

None.

40

2.0. ACCOUNTING POLICIES

2.1. BUSINESS AREAS

The Bouygues group is a diversified industrial group with operations in more than 80 countries. The Group’s activities are organised into a number of business areas: a) Construction:

- Bouygues Construction (building & civil works, energy and services) - Bouygues Immobilier (property) - Colas (roads)

b) Telecoms/Media: - TF1 (television) - Bouygues Telecom (mobile, fixed, TV and internet services)

c) The Bouygues group also holds a 30.74% interest in Alstom (Power, Transport and Transmission).

2.2. BASIS OF PREPARATION

The consolidated financial statements of the Bouygues group include the financial statements of Bouygues and its subsidiaries, and investments in associates. They are presented in millions of euros, the currency in which the majority of the Group’s transactions are denominated, and take account of the recommendations on presentation (Recommendation 2009-R-03) issued on 2 July 2009 by the Conseil National de la Comptabilité (CNC), now the Autorité des Normes Comptables (ANC), the French national accounting standard-setter.

They were approved by the Board of Directors on 30 August 2011. The Bouygues group has applied the same standards, interpretations and accounting policies for the six months ended 30 June 2011 as those disclosed in its consolidated financial statements for the year ended 31 December 2010, except for new IFRS requirements applicable from 1 January 2011 (see below). Consequently, Note 2 to the consolidated financial statements for the six months ended 30 June 2011 does not include detailed disclosures of these accounting policies, and these financial statements should be read in conjunction with the consolidated financial statements for the year ended 31 December 2010. • Principal new standards, amendments and interpretations effective within the European Union and mandatorily

applicable to periods beginning on or after 1 January 2011:

- IFRIC 14, “The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction” (no impact on the financial statements).

- IFRIC 19, “Extinguishing Financial Liabilities with Equity Instruments” (no impact on the financial

statements).

• Other key standards, amendments and interpretations issued by the IASB but not yet endorsed by the European

Union, for which early adoption effective 1 January 2011 is permitted.

- Bouygues has not early adopted any standards, amendments or interpretations as of 30 June 2011.

41

• Elective accounting treatments and estimates used in the valuation of certain assets, liabilities, income and expenses: