half-year report 2013

TRANSCRIPT

www.ivsgroup.it

Half-yearReport2013

+5ACQUISITIONS

VENDS (million)

325.6334.1SALES / BUSINESS DAY

(€ ‘000’ s)

H1 2012

H1 2012

H1 2012

H1 2013

H1 2013

H1 2013

1,11

7

1,19

4AVERAGE PRICE (€ cents/vend)

COIN DIVISIONREVENUES

42.1

43.4

+15.6%59BRANCHESItaly / France / Spain

2,040EMPLOYEES

COST OF SALESPER VENDS (€ cents/vend)

11.0

11.4

GROSS PROFIT(€ cents/vend)

31.1

32.1

65%Automatic Vending Machines

35%

VENDING MACHINES

Highlights

O� ce Co� ee

System

~147KH1 2012

H1 2012

H1 2013

H1 2013

In

dex

In

dex

2

Con

dens

ed in

terim

con

solid

ated

repo

rt a

s of

Mar

ch 3

1,

Con

dens

ed in

terim

con

solid

ated

repo

rt a

s of

Mar

ch 3

1,

Con

dens

ed in

terim

con

solid

ated

repo

rt a

s of

Mar

ch 3

1, 2

013

2013

2013

•••Ind

exIn

dex

Inde

x

3

Hal

f-yea

r Rep

ort 2

013

• C

onte

nts

COMPANY OFFICERS 5Board of Directors 5Independent auditors 5

GROUP STRUCTURE 7

INTERIM MANAGEMENT REPORT 9Purpose and Accounting principles 10Company overview 10Signi� cant events in the � rst six months of 2013 12Business overview 14Changes in the consolidation 14Information on acquisitions carried out in previous years 14Group performance 15Related party transactions 20Principal Risks and uncertainties 20

MANAGEMENT CERTIFICATION 23

CONDENSED INTERIM CONSOLIDATED FINANCIAL STATEMENTS 25Indipendent Auditor’s Report on Interim Consolidated Financial Statements 27Financial Statements Schedules 31 Consolidated Statements of � nancial position 32 Consolidated Income Statements 33 Consolidated Statements of Comprehensive Income 34 Consolidated Statements of changes in Shareholders’ equity during the � rst six months of 2013 35 Consolidated Statements of changes in Shareholders’ equity during the � rst six months of 2012 36 Consolidated Statements of Cash Flows 37

Explanatory Notes to the Financial Statements 39 1 – Corporate information 40 2 – Basis of preparation and changes to the Group’s accounting policies 40 3 – Seasonal factors 42 4 – Business combinations 42 5 – Operating segments 43 6 – Intangible assets 45 7 – Goodwill 45 8 – Property, plant and equipment 46 9 – Borrowings 46 10 – Net Financial Indebtedness 47 11 – Financial Instruments 47 12 – Shareholders’ equity 48 13 – Commitments and guarantees 49 14 – Other non-recurring income and expenses 50 15 – Financial income and expenses 50 16 – Income tax for the period 51 17 – Earnings per share 51 18 – Related party transactions 52 19 – Subsequent events 53 20 – Consolidation 53

Contents

Inte

rim m

anag

emen

t rep

ort

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

4

IVS GROUP S.A.Registered o� ces: 2A Rue Jean-Baptiste Esch L-1473 Luxembourg R.C.S. Luxembourg B155 294 VAT No. LU 24379120Share capital Euro 386,892.00 fully paid up

Operational headquarters: I-24068 Seriate (BG) via dell’Artigianato, 25VAT No. IT 03840650166 – Tax code 97602500155

www.ivsgroup.lu

5

Hal

f-yea

r Rep

ort 2

013

• Co

mpa

ny O

� ce

rs

Company Offi cers

BOARD OF DIRECTORS

Cesare Cerea Chairman

Massimo Paravisi Chief Executive O� cer (CEO)

Massimo Trapletti Chief Executive O� cer (CEO)

Antonio Tartaro Chief Financial O� cer (CFO)

Paolo Covre Vice Chairman

Vito Alfonso Gamberale Vice Chairman

Adriana Cerea Director

Monica Cerea Director

Carlo Giovanni Mammola Non-executive director

Mariella Trapletti Non-executive director

Luigi De Puppi Independent non-executive director

Mariano Frey Independent non-executive director

Francesco Tatò Independent non-executive director

INDEPENDENT AUDITORS

Ernst & Young S.A. Luxembourg

IVS GROUP S.A.Registered o� ces: 2A Rue Jean-Baptiste Esch L-1473 Luxembourg R.C.S. Luxembourg B155 294 VAT No. LU 24379120Share capital Euro 386,892.00 fully paid up

Operational headquarters: I-24068 Seriate (BG) via dell’Artigianato, 25VAT No. IT 03840650166 – Tax code 97602500155

www.ivsgroup.lu

7

Hal

f-yea

r Rep

ort 2

013

• G

roup

Str

uctu

re

Group Structure

ESP S.A.(J.V. con Lavazza e DB)

Vending SystemItalia S.p.A.

IVS Italia S.p.A.

IVS F. S.p.A.

Metroshopping S.r.L.IVS France S.a.S. Emmedi S.A.

SCI+39Maquina Automaticas

Blasco S.L.

D.A.V. S.A.

CaYbe 2 S.L.

Eur Co� ee S.r.L. Mr. Vending S.r.L. Time Vending S.r.L.(J.V. con Cremonini)

S. Italia S.p.A. Fast ServiceItalia S.p.A.

The IVS Group presents the following structure as of June 30, 2013:

20.10 Vending S.r.L. D.D.S. S.p.A. Eurovending S.r.L. EVS S.r.L. Liguria Ca� è Automatico S.r.l.

IVS GROUP S.A.

ItalianCompanies

FrenchComapanies

SpanishCompanies Associates Joint

VenturesSociété Civile

Immobilière (France)

Universo Vending S.r.L.

CoFraDis Sud S.a.S.

Ristora System S.r.L.

Ciesse Ca� é S.r.L.

CoinPartecipazioni

S.p.A.

Coin Service Empoli S.p.A.

Coin Service Nord S.p.A.

CSH S.r.L.

Coin Service business division

(Italy)

Inte

rim m

anag

emen

t rep

ort

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

8

Inte

rim m

anag

emen

t rep

ort

Inte

rim m

anag

emen

t rep

ort

9

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

tInterim

management report

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

10

Interim management report

PURPOSE AND ACCOUNTING PRINCIPLES

This half-year report for the six-month period ended June 30, 2013 has been prepared in compliance with Article 4 of the Luxembourg Transparency Law of January 11, 2008, and should be read in conjunction with the annual report for the year ended December 31, 2012 (including the � nancial statements included therein) and the unaudited consolidated condensed interim � nancial statements included in this half-year report.

These condensed interim consolidated � nancial statements has been prepared in conformity with IFRS, the International Financial Reporting Standards, as issued by the International Accounting Standards Board and as adopted by the European Union.

Our consolidated � nancial statements are expressed in Euro. The unaudited condensed interim consolidated � nancial statements included in this half-year report have been prepared in accordance with IAS 34, “Interim Financial Reporting”. These unaudited condensed interim consolidated � nancial statements should be read in conjunction with the audited consolidated � nancial statements for the year ended December 31, 2012, which have been prepared in accordance with IFRS. See Note 2, “Basis of preparation and changes to the Group’s accounting policies” to our unaudited condensed interim consolidated � nancial statements included in this half-year report.

COMPANY OVERVIEW1

IVS Group S.A. resulted from the merger by incorporation of IVS Group Holding S.p.A. into Italy1 Investment S.A.Italy1 Investment S.A. (“Italy1”) was the � rst SPAC (Special Purpose Acquisition Company) to be listed on the Italian Stock Exchange. The merger between Italy1 Investment S.A. and its target IVS Group Holding S.p.A. was approved on April 12, 2012 by the shareholders and on May 16, 2012 the merger � nally came into force and Company assumed the corporate name of IVS Group S.A., proceeding, in the meantime, as per company statute and regulations, to buy-back the shares held by those Italy1’s shareholders who exercised the redemption option in view of the realization of the Business Combination.

1. Cautionary Statement Concerning Forward-looking statements This half-year report and any other oral or written statements made by us to the public may contain “forward-looking statements”. Forward looking statements

are based on management’s current views and assumptions and involve known and unknown risks that could cause actual results, performance or events to di� er materially from those expressed or implied by those statements.

We use words such as “aim”, “will likely result”, “will continue”, “contemplate”, “seek to”, “future”, “objective”, “goal”, “should”, “will pursue”, “anticipate”, “estimate”, “expect”, “project”, “intend”, “plan”, “believe” and words and terms of similar substance to identify forward-looking statements, but they are not the only way we identify such statements. All forward-looking statements are management’s present expectations of future events and are subject to a number of factors and uncertainties that could cause actual results to di� er materially from those described in the forward-looking statements. These factors include the risks related to our business discussed under “Principal Risks and Uncertainties”, among them, the following:

- our ability to implement our business strategy or to grow through acquisitions, joint ventures and other investments; - the competitive environment in our business and our industry; - our ability to price our products and services in accordance with our strategy; - general macroeconomic and political conditions and developments in the countries in which we operate; - � uctuations in costs related to fuel and transportation inputs, food, co� ee and other commodity prices; - impact of seasonal variation and abnormal weather; - loss of major customers and/or inability to establish new customer relationships; By their nature, certain disclosures relating to these and other risks are only estimates and could be materially di� erent from what actually occurs in the future. As

a result, actual future gains or losses that may a� ect our � nancial condition and results of operations could di� er materially from those that have been estimated. You should not place undue reliance on the forward-looking statements, which speak only as of the date of this half-year report.

Except as required by law, we are not under any obligation, and expressly disclaim any obligation, to update or alter any forward-looking statements, whether as a result of new information, future events or else.

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

11

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

12

SIGNIFICANT EVENTS IN THE FIRST SIX MONTHS OF 2013SENIOR SECURED NOTES DUE 2020On March 12, 2013 the Parent company, IVS Group S.A., incorporated the Italian company IVS F. S.p.A., under its direction and control, with share capital of EUR 2,050,000. On March 20, 2013 IVS F. S.p.A. announced the plan to issue EUR 200,000,000 of senior secured notes due on April 1, 2020, to be o� ered to quali� ed investors, principally to re� nance some of its credit facilities, to extend the maturity pro� le of its debt, and for other more general corporate purposes. On March 26, 2013 IVS F. S.p.A. set the price of the senior secured bond, and issued the Notes listed on the ExtraMOT Market of Borsa Italiana S.p.A. and on the EUR MTF Market of the Luxembourg Stock Exchange, publishing the O� ering Memorandum and setting the interest rate on the bonds at 7.125% per annum. The rating of these notes is BB- (S&P).

With regards to the issue procedure, pursuant to the laws of the State of New York, a purchase agreement was signed by the initial purchasers – who are also quali� ed institutional buyers – the issuer and the underwriters. The notes may be resold by the initial purchasers exclusively as follows:• in the United States of America only to quali� ed investors, in compliance with Rule 144A of the U.S.

Securities Act; • outside the United States of America to quali� ed investors as de� ned by Regulation S of the U.S. Securities

Act, and• in Europe to European investors speci� ed in the O� ering Memorandum.

Subsequently, a global bond certi� cate was published pursuant to Rule 144A and a global bond certi� cate was published pursuant to Regulation S (collectively “Global Notes”).The Notes are guaranteed by the following shares owned by IVS Group S.A.:• Pledge on IVS F. S.p.A. shares,• Pledge on Fast Service Italia S.p.A. shares,• Pledge on S.Italia S.p.A. shares, and• Pledge on IVS Italia S.p.A. shares;as well as by:• Pledge on IVS F. S.p.A. receivables arising from intragroup loans, and by • Note Guarantees issued by each underwriter for the amounts indicated in the O� ering Memorandum.

On April 4, 2013 IVS F. S.p.A signed an Indenture between certain Group companies (as guarantors - IVS Group S.A., IVS Italia S.p.A., Fast Service S.p.A. and S.Italia S.p.A.), The Law Debenture Trust Corporation p.l.c.(as trustee) and BNP Paribas Securities Services (as security agent).The Notes were issued under the laws of New York (Rule 144A and Regulation S of Securities Act as of 1933), Securities Act as of 1933), Securities Actand the placement was led by BNP Paribas and Banca IMI as Joint Lead Bookrunners and MPS Capital Services, as Co-Manager.During April and May 2013 the subsidiaries of the Group made certain early repayments of loans and other � nancial liabilities in accordance with the speci� c instructions set out in the Senior Secured Notes issued by IVS F. S.p.A..

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

13

Share

Recent trading of IVS Securities

Contracts in €

Jan2013

Feb2013

Mar2013

Apr2013

May2013

Jun2013

Jul2013

Aug2013

3,000K

2,500K

2,000K

1,500K

1,000K

500K

0K

Warrants Contracts in €

Jan2013

Feb2013

Mar2013

Apr2013

May2013

Jun2013

Jul2013

Aug2013

100K

50K

0K

Senior Secure Notes Contracts in €

Apr2013

Jun2013

Jul2013

2,000K

1,500K

1,000K

500K

0K

Feb2013

Mar2013

May2013

Jun2013

Aug2013

6.300

6.700

7.100

Feb2013

Mar2013

May2013

Jun2013

Aug2013

0.2259

0.2980

0.3700

Source: Borsa italiana

Feb2013

Mar2013

May2013

Jun2013

Aug2013

96.00

98.25

100.50

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

14

TRANSLISTING FROM MIV TO MTA SEGMENT OF BORSA ITALIANA On April 30, 2013 IVS Group S.A. � led with Borsa Italiana a request to list its shares (Class A shares) and warrants on the MTA-Mercato Telematico Azionario managed by Borsa Italiana S.p.A.. On May 30, 2013 Borsa Italiana approved the transfer. The starting date of trading on the MTA and the simultaneous end of trading on the MIV was June 3, 2013.

DIVIDEND DISTRIBUTIONThe shareholders’ meeting of IVS Group S.A., held in Luxembourg on May 14, 2013, in addition to approving the � nancial statements and the consolidated � nancial statements as of December 31, 2012 and related documents, resolved the distribution of a dividend amounting to EUR 0.125 per share, for a total amount of EUR 4,824,745.38, by using distributable reserves. The ex-dividend date was set to be June 3, 2013, the record date June 5, 2013, and the payment date June 6, 2013.

BUY-BACKThe General Meeting held in Luxembourg on May 14, 2013 also resolved to authorise the Board of Directors to purchase the company’s own shares, to be used as consideration for possible acquisitions, for a total amount of up to EUR 5 million over a period of 10 months from the date of the General Meeting, and indicated, pursuant to the applicable Luxembourg laws, a purchase price between a minimum of EUR 1 per share and a maximum of EUR 10 per share.

BUSINESS OVERVIEW

The IVS Group is one of the leading vending machine operators in Europe (a highly fragmented market), as detailed in the Company’s annual report and as re� ected in the � gures published by the EVA (European Vending Association). According to the latest report of CONFIDA, the Italian association of vending sector companies (based on 2012 � gures), IVS is the most important operator in Italy, with a market share of 11.3%. Italy represents IVS’s principal market; nevertheless, IVS is also present in the French and Spanish markets, where sales for the half year ended June 30, 2013 represented, respectively, approximately 7.9% and 4.8% of the Group’s total turnover, net of the Coin business. With over 40 years of experience in the industry, the IVS Group is the only operator to cover the entire territory of Italy.The Company owns more than 147,000 automatic and semiautomatic vending machines of various sizes, located in o� ces, institutions, and areas open to the public.

CHANGES IN THE CONSOLIDATION

The main change in the composition of the IVS Group with respect to December 31, 2012 is the acquisition on February 6, 2013 of Liguria Ca� è Automatico S.r.l., an Italian company operating in the vending sector.

INFORMATION ON ACQUISITIONS CARRIED OUT IN PREVIOUS YEARS

In March and April 2012, the Group acquired Fast Service Italia S.r.l. and Selecta Italia S.p.A. (now Fast Service Italia S.p.A. and S.Italia S.p.A., respectively) and the related purchase price allocations were completed on December 31, 2012. Accordingly, following the provisions of IFRS 3, the Company has retrospectively adjusted the reported � gures as of June 30, 2012. Further details are provided in Note 7 of the explanatory notes to the consolidated � nancial statements of IVS Group S.A. as of December 31, 2012.

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

15

GROUP PERFORMANCE2

The interim consolidated � nancial statements of the IVS Group as of June 30, 2013 show a net pro� t ofEUR 4,947 thousand.This result, without giving e� ect to non-recurring expenses related to the translisting (EUR 576 thousand) and the issuance of Senior Secure Notes (EUR 2,776 thousand), would have amounted to Euro 8,299 thousand.

Six Months Ended June 30, 2013

(thousands of Euro) Italy France Spain Coin GroupInter-sector

eliminations Total

Value of production 135,915 12,549 7,651 6,498 (4,229) 158,384

Operating costs (107,820) (10,077) (5,924) (5,027) 4,229 (124,619)

Ebitda Adjusted 28,095 2,472 1,727 1,471 - 33,765 Other non-recurring income/(expenses) (1,940) (47) (87) (47) - (2,121)

EBITDA 26,155 2,425 1,640 1,424 - 31,644 % Ebitda Adj / Value of production 21% 20% 23% 23% - 21%

Depreciation and amortisation (17,235) (1,177) (1,060) (297) - (19,770)

Ebit 8,920 1,248 580 1,127 - 11,873

% Ebit/ Value of production 7% 10% 8% 17% - 7%

Six Months Ended June 30, 2012

(thousands of Euro) Italy France Spain Coin GroupInter-sector

eliminations Total

Value of production 125,831 12,485 7,781 5,621 (4,289) 147,429

Operating costs (99,908) (10,808) (6,300) (4,147) 4,289 (116,874)

Ebitda Adjusted 25,923 1,677 1,481 1,474 - 30,555Other non-recurring income/(expenses) (*) (1,555) 232 - 16 - (1,307)

EBITDA (*) 24,368 1,909 1,481 1,490 - 29,248 % Ebitda Adj / Value of production 21% 13% 19% 26% - 21%

Depreciation and amortisation (16,281) (1,301) (750) (192) 24 (18,500)

Ebit (*) 8,087 608 731 1,298 24 10,748

% Ebit (*)/ Value of production 6% 5% 9% 23% - 7%

2. In this document, we present certain non-IFRS measures, including EBITDA, Adjusted EBITDA, Operating pro� t, Net � nancial position/ indebtedness and Financial indebtedness.

We de� ne “EBITDA” as operating pro� t before interest and income taxes (“EBIT”) plus amortisation and depreciation. “Adjusted EBITDA” refers to EBITDA as adjusted to remove accounting e� ects and costs associated with the Merger and some other non-recurring income and expenses considered by our management to be non-recurring and exceptional in nature.

It uses similar indicators for its net � nancial indebtedness, the components of which are described in the relative section of the notes. This document also includes a number of � nancial ratios which are helpful to better understand the Group’s performance, especially with respect to di� erences

compared to previous years. We believe that EBITDA is a useful indicator of our ability to incur and service our indebtedness and can assist certain shareholders, certain investors, security

analysts and other interested parties in evaluating us. We believe that Adjusted EBITDA is a relevant measure for assessing our performance because it is adjusted for certain charges which, we believe, are not indicative of our underlying operating performance and thus aid in an understanding of EBITDA.

EBITDA and Adjusted EBITDA and similar measures are used by di� erent companies for di� ering purposes and are often calculated in ways that re� ect the circumstances of those companies. Reader should exercise caution in comparing EBITDA and Adjusted EBITDA as reported by us to EBITDA and Adjusted EBITDA of other companies. The information presented by each of EBITDA and Adjusted EBITDA is unaudited and has not been prepared in accordance with IFRS or any other accounting standards. None of EBITDA or Adjusted EBITDA is a measurement of performance under IFRS and you should not consider EBITDA or Adjusted EBITDA as an alternative to net income or operating pro� t determined in accordance with IFRS, as the case may be, or to cash � ows from operations, investing activities or � nancing activities. EBITDA and Adjusted EBITDA have limitations as analytical tools, and you should not consider them in isolation. Some of these limitations are:

- they do not re� ect our cash expenditures or future requirements for capital expenditures or contractual commitments; - they do not re� ect changes in, or cash requirements for, our working capital needs; - they do not re� ect the signi� cant interest expense, or the cash requirements necessary, to service interest or principal payments on our debt; - although depreciation and amortisation are non-cash charges, the assets being depreciated and amortised will often need to be replaced in the future and

EBITDA and Adjusted EBITDA do not re� ect any cash requirements that would be required for such replacements; and - the fact that other companies in our industry may calculate EBITDA and Adjusted EBITDA di� erently than we do. which limits their usefulness as comparative measures.

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

16

Vending sector

Vending business overview

First six months of 2013 First six months of 2012 Italy France Spain Consolidated Italy France Spain Consolidated

Business days 122.0 118.5 118.0 121.5 123.0 122.0 119.0 122.7Units sold (thousands) 287,691 27,139 19,294 334,124 277,483 28,033 20,133 325,649Units sold per business day (thousands) 2,358 229 164 2,751 2,256 230 169 2,653Sales (€ thousand) 125,475 12,072 7,589 145,136 118,141 11,165 7,733 137,039Sales per business day(€ thousand) 1,028 102 64 1,194 960 92 65 1,117Average price (€ cents) 43.61 44.48 39.34 43.44 42.58 39.83 38.41 42.08Cost of sales per unit sold(€ cents) (11.20) (13.12) (11.73) (11.38) (10.81) (12.59) (11.75) (11.02)Gross pro� t per unit sold(€ cents) 32.41 31.36 27.61 32.06 31.77 27.24 26.66 31.07Operating pro� t from continuing operations per unit sold (€ cents) 9.24 9.11 8.95 9.21 8.97 5.98 7.35 8.47

Italy France Spain Consolidated

Δ% Business days -0.8% -2.9% -0.8% -1.0%Δ% Units sold 3.7% -3.2% -4.2% 2.6%Δ% Units sold per business day 4.5% -0.3% -3.4% 3.6%Δ% Sales 6.2% 8.1% -1.9% 5.9%Δ% Sales per business day 7.1% 11.3% -1.0% 6.9%Δ% Average price 2.4% 11.7% 2.4% 3.2%Δ% Cost of sales per unit sold 3.6% 4.3% -0.2% 3.3%Δ% Gross pro� t per unit sold 2.0% 15.1% 3.5% 3.2%Δ% Operating pro� t from continuing operations per unit sold 3.1% 52.3% 21.6% 8.8%

During the � rst six months of the year 2013, the Group recorded an increase in the turnover from distribution and sale of food, drinks and other goods through automatic vending machines, with respect to the corresponding period of the previous year (EUR 145,136 thousand, compared to EUR 137,039 thousand).The signi� cant increase in sales is corroborated by the increase in volumes registered during the � rst part of 2013 with respect to the corresponding period of the previous year. This change is largely due to the improvement of the acquisitions completed during all the 2012 that also contributed to P&L since January 1, 2013.

June 30, 2013 Sales and vends breakdown by product type

57Hot34

Mix

9OCS

%

Vends (Thousands)

Hot Mix OCS Total

2013 2012 2013 2012 2013 2012 2013 2012

Italy 161,743 154,087 103,637 102,161 22,311 21,235 287,691 277,483France 16,408 16,275 3,504 3,514 7,227 8,245 27,139 28,033Spain 13,179 13,381 5,565 6,031 550 721 19,294 20,133Total 191,330 183,743 112,706 111,706 30,088 30,201 334,124 325,649

Sales (Thousands) (€)

Hot Mix OCS Total

2013 2012 2013 2012 2013 2012 2013 2012

Italy 57,785 52,828 58,433 56,749 9,257 8,565 125,475 118,141France 6,454 5,222 2,816 2,768 2,802 3,174 12,072 11,165Spain 4,416 4,506 2,947 2,922 227 305 7,589 7,733Total 68,654 62,556 64,196 62,439 12,286 12,044 145,136 137,039

9OCS

44Mix

47Hot%

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

17

Vending activity during the � rst six months of the year 2013 has been negatively a� ected by unfavourable meteorological conditions. In particular, the second quarter – where normally a temperature increase favours the consumption of items with higher margin in absolute terms sold through our vending machines – was colder than the previous year. In Rome, the number of 2013 2Q days where the average temperature was higher than 20˚ C were 17 (vs. 25 in 2012); in Nice 10 (vs. 24 in 2012) and in Madrid 19 (vs. 40 in 2012) (Source: wunderground.com).

The raising of the average sales price – from 42.08 to 43.44 EUR cents – was therefore particularly incisive, although the sales price of our main product (co� ee) remains far below the average price in traditional bars, which in certain cases reaches three-times our price. Our observation of the Italian vending operators’ market suggest a decrease in overall vends in the region of 4%. The decrease is closely correlated to corporate market segment trend, which is driven by working hours. (Source: ISTAT). However, our commercial e� ort in 1H 2013 resulted in a positive gain of vends coming from new clients, which exceeded the churn rate for the � fth quarter in raw.

First Quarter Second Quarter

2013 2012 2013 2012

Thousands % €cent Thousands % €cent Thousands % €cent Thousands % €cent

Vends 167,071 161,329 167,052 164,320Value of production 74,364 100.0% 44.51 65,016 100.0% 40.30 78,929 100.0% 47.25 73,267 100.0% 44.59Operating costs (58,582) 78.8% 35.06 (50,843) 78.2% 31.52 (62,418) 79.1% 37.36 (58,359) 79.7% 35.52Ebitda Adjusted 15,782 21.2% 9.45 14,172 21.8% 8.78 16,511 20.9% 9.88 14,908 20.3% 9.07Other non-recurring income/(expenses)* (1,023) 1.4% 0.61 (849) 1.3% 0.53 (1,051) 1.3% 0.63 (474) 0.6% 0.29Ebitda* 14,759 19.8% 8.83 13,323 20.5% 8.26 15,460 19.6% 9.25 14,434 19.7% 8.78Depreciation and amortisation (9,790) 13.2% 5.86 (8,934) 13.7% 5.54 (9,683) 12.3% 5.80 (9,399) 12.8% 5.72Ebit* 4,969 6.7% 2.97 4,389 6.8% 2.72 5,777 7.3% 3.46 5,035 6.9% 3.06Δ% Vends 3.6% 1.7%Δ% Value of production 14.4% 10.4% 7.7% 6.0%Δ% Operating costs 15.2% 11.3% 7.0% 5.2%Δ% Ebitda Adjusted 11.4% 7.5% 10.8% 8.9%Δ% Other non-recurring income/(expences)* 20.5% 16.3% 121.7% 118.1%Δ% Ebitda* 10.8% 7.0% 7.1% 5.4%Δ% Depreciation and amortisation 9.6% 5.8% 3.0% 1.3%Δ% Ebit* 13.2% 9.3% 14.7% 12.9%

(*) Adjusted by IT1-IVSG 2012 merger cost (Euro 26,827 thousand).

COIN SECTORThe Coin Service division (which carries out coin management activities) recorded revenues of Euro 6,498thousand during the � rst six months of 2013, registering an increase of 15.6% with respect to the corresponding period of the previous year, meanwhile the decrease in the unitary margins generated from bank’s coin managing business a� ected level of pro� tability. Consequently the EBITDA Adjusted remained stable despite the above mentioned increase in the turnover. However the new plants of Alessandria and Messina are not yet at full capacity and they have enough space to increase the activity.In the � rst months of 2013, a new activity, regarding managing of special electronic money acceptance system for Vending industry was started. The initial cost of the start-up has slightly diluted the overall margin of the division, although the performance of the core metallic coin business remains in line with the past.

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

18

Coin Sector June 30, 2013 June 30, 2012

Value of production 6,498 5,621 Operating costs (5,027) (4,147)Ebitda Adjusted 1,471 1,474 Other non-recurring income/(expenses) (47) 16EBITDA 1,424 1,490 % Ebitda Adj / Value of production 23% 26%Depreciation and amortisation (297) (192)Ebit 1,127 1,298 % Ebit / Value of production 17% 23%

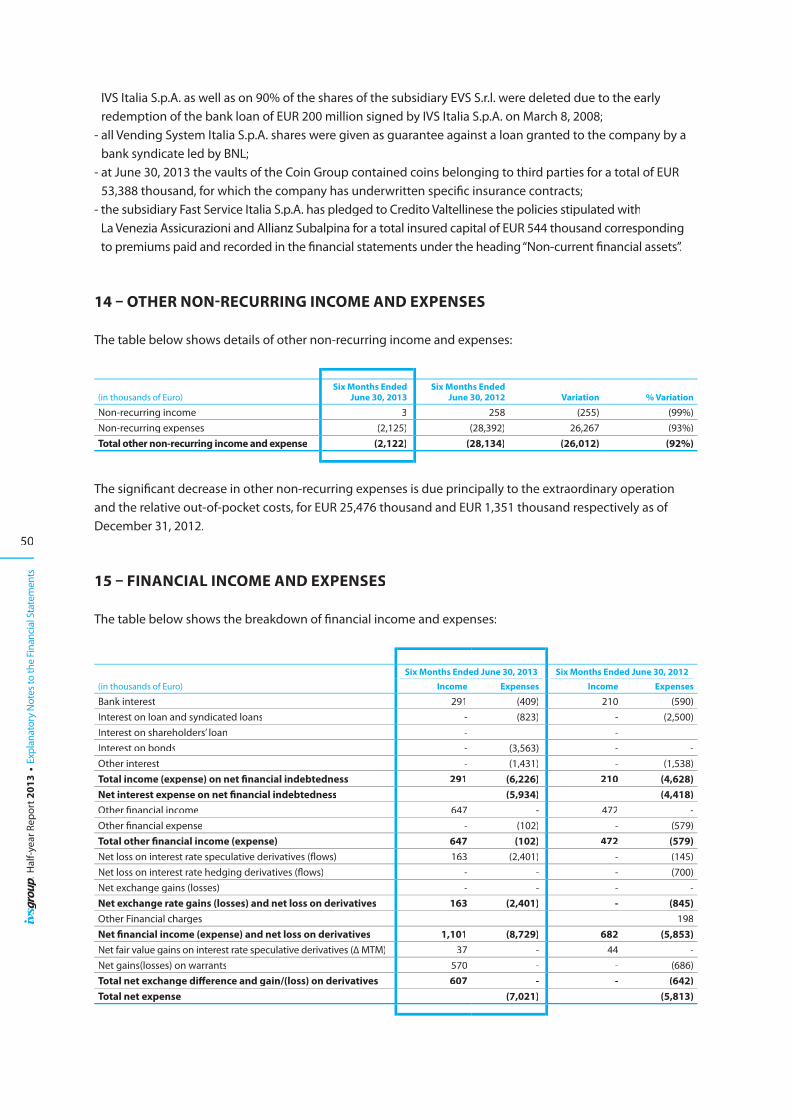

FINANCIALS COST, NETNet � nance costs amounted to EUR 7,008 thousand against EUR 5,762 thousand in the corresponding period of the previous year. This increase is due to the non-recurring expenses for an amount equal to EUR 2,776 thousand, as described in the table below.This table shows the detail of � nancials P&L:

Financial P&L June 30, 2013

Interest income 939 Result of companies valued at net equity 13 Interest on loans (1,237) Interest on � nancial leases (321) Interest on bond (3,563) Interest cost of employee bene� ts (102) Income on derivatives, net 90 Income on fair value warrant 570 Change of put option (326) Other charges (295) Total ordinary result (4,232) MTM hedging derivatives (2,291) Amortised cost fees (485) Total extraordinary result (2,776)Grand Total (7,008)

In the � rst part of 2013, the Italian tax authorities did not increase their delay in refund VAT3 and partially recovered the lag accumulated in 2012. Accordingly, our VAT credit decreased of EUR 5,078 thousand during the � rst six months of the year 2013.In addition to that, EUR 8,445 thousand have been refunded in July 2013. The Italian tax authority is committed to normalise the timing of VAT refunds.

INVESTMENTSDuring the period the principal investments carried out by Group companies regarded the purchase of assets to be used in the exercise of its commercial activities: vending machines, token dispensers and payment systems, motor vehicles and trucks; these investments were made to upgrade and renew the existing machinery and equipment in order to meet customers’ changing requirements, to improve customer service and, accordingly, strengthen and develop the Group’s position in its relevant market.

In August 2013 the Italian Parliament approved the conversion in law of the Government’s decree June 4, 2013, no.63 that increased from 4% to 10% the VAT rate applicable to items sold through vending business. In order to allow vending operators to modify their machines on the � eld and to inform the clients of this law

3. VAT credit deriving from the di� erence in the VAT rate between the one applied to sales and the one applied to purchases of the principal Italian operating company (IVS Italia S.p.A.).

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

19

change, the increase will take e� ect from the beginning of the year 2014. Considering that the largest part of our Italian technical structure will be involved during the second part of 2013 in this activity, we concentrated the largest part of our capital expenditure (“capex”) during the second quarter of the year 2013.

In the � rst part of year 2013 we paid Euro 7,968 for acquiring new participations and pay part of the deferred consideration agreed with the acquisition of Fast Service Italia S.p.A., completed in the year 2012.Despite the amounts paid in the � rst half of the year 2013 in connection with the Senior Notes issuance and an aggressive payment policy adopted with some selected suppliers to obtain some reductions in COGS, the cash � ows generated in the � rst half of year 2013 from the operating activity (EUR 20,007 thousand) were comparable to the amount generated in the whole year 2012 (EUR 20,151 thousand).

March 31, 2013

Type

New Refurbishment Total Capex

Operative Capex:Vending machines and payment systems 4,882 1,886 6,768 Vehicles 804 - 804 Other assets 1,522 - 1,522

7,208 1,886 9,094 Extraordinary CapexNew Barcelona facility 3,657 - 3,657 Operating Assets from Acquisitions 903 - 903

4,560 - 4,560

June 30, 2013 (Cumulated 1Q + 2Q)

Type

New Refurbishment Total Capex

Operative Capex:Vending machines and payment systems 9,127 3,364 12,491 Vehicles 1,500 - 1,500 Other assets 3,971 - 3,971

14,598 3,364 17,962 Extraordinary CapexNew Barcelona facility 4,232 - 4,232 Operating Assets from Acquisitions 3,157 - 3,157

7,389 - 7,389

PRINCIPAL EQUITY, FINANCIAL AND EARNINGS RATIOSThe IVS Group closed the � rst six months of the year 2013 with a net pro� t of Euro 4,947 thousand and with a consolidated shareholders’ equity attributable to the owner of the parent company of Euro 298,454 thousand, (+1.6% compared to December 31, 2012). In addition, at June 30, 2013, the Group shows a net � nancial indebtedness of Euro 177,770 thousand (+5,5% compared to December 31, 2012).

(thousands of Euro) Italy % France % Spain % Coin %Intra-sector adjustment

June 30, 2013 %

Capital structure composition analysisFixed Assets 508,338 79% 34,140 88% 19,672 87% 14,811 31% (38,281) 538,680 76%Current Assets 73,314 11% 3,087 8% 1,672 7% 17,939 37% (6,158) 89,855 13%Liquidity 63,602 10% 1,424 4% 1,220 6% 15,328 32% - 81,574 11%Invested Capital 645,254 100% 38,651 100% 22,564 100% 48,078 100% (44,439) 710,109 100%Consolidated Liabilities 237,352 37% 14,089 36% 3,486 16% 11,248 23% (8,996) 257,178 36%Current Liabilities 112,847 17% 7,060 18% 3,240 14% 32,979 69% (6,404) 149,722 21%Equity 295,056 46% 17,502 46% 15,839 70% 3,851 8% (29,039) 303,209 43%Finance Capital 645,254 100% 38,651 100% 22,564 100% 48,078 100% (44,439) 710,109 100%

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

20

(thousands of Euro) Italy % France % Spain % Coin %Intra-sector adjustment

December 31, 2012 %

Capital structure composition analysisFixed Assets 508,098 85% 33,118 90% 17,547 86% 19,222 40% (37,996) 539,989 82%Current Assets 78,599 13% 2,911 8% 1,946 10% 9,896 21% (6,407) 86,945 13%Liquidity 11,812 2% 719 2% 886 4% 18,400 39% (3,001) 28,817 5%Invested Capital 598,509 100% 36,749 100% 20,380 100% 47,518 100% (47,404) 655,751 100%Consolidated Liabilities 142,604 24% 14,240 38% 797 4% 14,928 32% (20,907) 151,662 23%Current Liabilities 163,613 28% 7,157 20% 4,137 20% 29,630 62% 1,479 206,016 31%Equity 292,292 48% 15,352 42% 15,446 76% 2,961 6% (27,976) 298,074 46%Finance Capital 598,509 100% 36,749 100% 20,380 100% 47,518 100% (47,404) 655,751 100%

RELATED PARTY TRANSACTIONS

The transactions with related parties shown in the interim consolidated � nancial statements regarded the associated companies and other related parties as de� ned by IAS 24. A summary of transactions and balances with related parties as of June 30, 2013 is provided in the Explanatory notes (Note 18).The operations with related parties were carried out for the purposes of consolidating existing synergies within the Group in terms of production, commercial and logistics integration, of the e� cient use of expertise and skills and streamlining of centralised structures and of � nancial resources. All transactions with related parties, both those related to the exchange of goods and services and those of a � nancial nature, take place at normal market conditions.

TRANSACTIONS WITH SUBSIDIARIES AND ASSOCIATESThese transactions are of a commercial (exchange of goods and/or services) and � nancial nature. For more detailed information reference should be made to the explanatory notes regarding transactions with subsidiaries and associates.

TRANSACTIONS WITH OTHER RELATED PARTIES:Transactions with other related parties are mainly of a commercial nature and mostly consist of the exchange of goods and/or services such as management fees, fees and consideration for services, rental/leasing charges, etc..For further information reference should be made to the explanatory notes about transactions with other related parties.

OWN SHARES AND SHARES/QUOTAS IN PARENT COMPANIESThe Company holds 2,854,528 own shares following the re-acquisition thereof as a result of the exercise of the redemption option by certain shareholders during the business combination completed on May 16, 2012.

PRINCIPAL RISKS AND UNCERTAINTIES

Risk management (which involves management of internal and external, social, industrial, political and � nancial risks) is an integrated part of the Group’s growth strategy and is essential to the on-going development of its corporate governance system. Its aim is to protect both stakeholders (employees, customers, suppliers and shareholders) and the Group’s assets by improving codes of conduct.

GENERAL AND BUSINESS RISKS:The Group constantly monitors its � nancial risks in order to assess in advance the potential e� ects thereof and undertake the necessary actions to mitigate or o� set them.Our business, � nancial condition and results of operations may be adversely a� ected by the current unfavourable economic conditions in our primary markets of Italy, France and Spain and by market perceptions concerning Italy in particular.

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

21

The global � nancial and credit markets continue to be volatile in many markets and non-� nancial sectors of the world economy have also su� ered in recent years, resulting in a general contraction in consumer spending that varies by market. The international crisis, unprecedented in its scope and rapid spread, has steadily damaged the global economy in the last few years and constituted a risk for the Group. This di� cult situation was worsened by the � nancial scenario characterised by rising uncertainty and a rigidity which has made it very di� cult to operate.The Group has faced this situation by adjusting its equity and � nancial structure and introducing policies to contain costs, rethink its commercial policies and increase prices. The e� ects of the crisis would seem to be more or less stabilised, although demand continues to � uctuate.

The food and beverage industry is highly regulated and our business could be materially adversely a� ected by changes in governmental regulation and legislation or by associated compliance costs. Moreover, failure to comply with governmental regulations could result in the imposition of � nes or restrictions on operations and remedial liabilities.The restrictions placed in the past on the French market in relation to vending machines in schools may become more widespread, even in Italy, for instance, some discussions on this matter took place in the last months. Such restrictions could require us to stock less pro� table products in our vending machines and/or products that are less appealing to consumers and generate less revenue. If this were to occur in Italy or Spain, then it may have a material adverse e� ect on our business, � nancial condition and results of operations.

We operate in highly competitive industries, and if we do not compete e� ectively, we may lose market share or be unable to maintain or increase prices for our services. We face constraints on our ability to increase prices in response to competitive pressures or otherwise. Additionally, increasing operating costs, including redevance4 cost arrangements with certain customers, may o� set improvements on margins that rising prices might otherwise produce.

Our Coin Service Business involves the movement of large sums of money, and, as a result, our business is particularly dependent on our ability to process and settle transactions securely, accurately and e� ciently.

Our operations could be adversely a� ected if we are unable to retain key employees.We may face labour disruptions that could interfere with our operations and have a material adverse e� ect on our business, � nancial condition and results of operations.

The concentration of credit risk of a commercial nature is limited given its vast and diversi� ed customer base. For this reason, the current provisions for bad and doubtful debts are considered to be adequate.

FINANCIAL RISKS:The Group is exposed to normal � nancial risks as part of its business related mainly to interest rate.The Group did not made any investments in non-current � nancial assets nor in current � nancial assets (shares, bonds or other securities) such as to require particular prudence on how to measure the impact the economic recession and collapse of the � nancial markets in having thereon.

CREDIT RISK:We are exposed to credit risk related to our customers who may cause us to make larger allowances for doubtful trade receivables or incur write-o� s related to impaired receivables.

As of June 30, 2013, we had approximately Euro 18.6 million in trade receivables from customers resulting from sales hot beverage single-use drink pods (mostly co� ee), cups and stirrers which we provide to our O� ce Co� ee Services customers and typically invoice our customers at the time of each delivery.

4. We name Redavance any cost, fees or expenses paid to exercise vending activity at third parties premises or spaces.

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

22

If the macroeconomic conditions in Italy, France and Spain continue to deteriorate, we cannot assure that we will not have to increase our provisions for impaired debts relating to debts owed to us, which could have a material adverse e� ect on our business, � nancial condition and results of operations.

LIQUIDITY RISK:This is the risk that the Group will not be able to generate su� cient cash � ows from its operations to cover investments and third party debt. Each group company is free to negotiate credit facilities (in accordance with corporate management) and to agree diversi� ed sources of funding (e.g., loans, � nance leases, bank credit facilities, etc.) as long as the incurrence covenants of the Indenture of the Senior Notes are respected.

INTEREST RATE RISK:This is the risk related to future cash � ows from � nancing operations at � oating interest rates. A change in interest rates a� ects the fair value of � oating rate � nancial assets and liabilities and may impact a company’s future results. However as of June 30, 2013 only 26% of IVS Group’s � nancial indebtedness is at � oating rate.

The Group is also exposed to the following non-� nancial risks:

LEGAL RISKS:The Group is not involved in any signi� cant legal disputes relative to products sold, unfair competition or market practices, nor does it have any related � nancial obligations.

FISCAL RISKS:No new relevant � scal disputes have arisen as a result of tax assessments carried out by the � scal authorities.

While not constituting a risk in itself, we would point out that IVS Group S.A. has registered o� ces in Luxembourg, while its operational headquarters and centre of main operations are located in Italy. Consequently, for 2012, but also for 2011, in accordance with the prevailing OECD doctrine, the directors believe that the Company is resident for � scal purposes in Italy. The Company has therefore presented a request for interpretation to the Italian tax authorities (Agenzia delle Entrate – Direzione Centrale Normativa) regarding the application of the regulations contained in Article 83, D.P.R. No. 917 of 22 December 1986 and by Article 1, Legislative Decree No. 201 of 6 December 2011. After receiving the answer from the Italian tax authorities, the company has decided to calculate its tax charge in accordance with Italian tax legislation applicable to Italian resident companies.

SUBSEQUENT EVENTS AND OUTLOOK FOR THE REMAINDER OF THE YEAR No signi� cant events have occurred after June 30, 2013 except the above mentioned enact of the law concerning the VAT rate increase applicable to items sold through vending machines. All available steps are being taken to increase average sales prices to compensate this VAT rate increase., We are managing an adequate pricing policy to minimise the e� ect of such law on our margins, but we estimate that the extraordinary commercial e� ort to implement such strategy will bare an extraordinary cost of between EUR 500 thousand and EUR 900 thousand.Nevertheless, volumes will be a� ected by the new regime. In addition, it is reasonable to expect that, due to the current economic condition, like-for-like sale volumes will continue to stagnate, which is being taken into consideration by the IVS Group management team.

Lastly, we continue the research of targets to acquire in order to increase the customer base and service in those areas and branches which � xed structures would permit an increase in volumes without a proportional increase in the relative costs.

Luxembourg, 28 August 2013 On behalf of the Board of Directors,

Cesare Cerea Chairman

23

Management Certifi cation

On the basis of the information currently available to us, we con� rm that:

1. the unaudited condensed interim consolidated � nancial statements, prepared in conformity with the International Financial Reporting Standards adopted by the European Union, included in this Half-year Report, give a true and fair view of the equity and � nancial situation, the economic result and the cash � ows of IVS Group S.A., and of its consolidated subsidiaries; and

2. the Interim management’s report included in this Half-year Report, contains a reliable analysis of the signi� cant events which took place during the � rst six months of the year 2013, of the impact thereof on the unaudited condensed interim consolidated � nancial statements, of the signi� cant transactions with related parties, as well as a description of the principal risks and uncertainties to which the IVS Group is exposed.

Massimo Paravisi Chief Executive O� cer August 28, 2013

Antonio Tartaro Chief Financial O� cer August 28, 2013

Hal

f-yea

r Rep

ort 2

013

• M

anag

emen

t Cer

ti� c

atio

n

Inte

rim m

anag

emen

t rep

ort

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

24

Inte

rim m

anag

emen

t rep

ort

Inte

rim m

anag

emen

t rep

ort

25

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

tCondensed Interim

Consolidated Financial Statements

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

26

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

27

IndependentAuditor’s Report

Indi

pend

ent A

udito

r’s R

epor

t

29

Hal

f-yea

r Rep

ort 2

013

• In

dipe

nden

t Aud

itor’s

Rep

ort

Hal

f-yea

r Rep

ort 2

013

• F

inan

cial

Sta

tem

ents

Sch

edul

es

30

H

alf-y

ear R

epor

t 201

3 •

Fin

anci

al S

tate

men

ts S

ched

ules

31

Financial StatementsSchedules

Hal

f-yea

r Rep

ort 2

013

• F

inan

cial

Sta

tem

ents

Sch

edul

es

32

Financial Statements SchedulesCONSOLIDATED STATEMENTS OF FINANCIAL POSITION

(in thousands of Euro) Note June 30, 2013 December 31, 2012

ASSETSNon-current assetsIntangible assets 6 46,487 48,337Goodwill 7 317,067 314,794Property, plant and equipment 8 154,739 150,588Equity Investments 5,564 5,552Non-current � nancial assets 2,813 9,487Deferred tax assets 11,807 10,956Other non-current assets 203 274TOTAL NON-CURRENT ASSETS A 538,680 539,988Current assetsInventories 18,943 19,194Trade receivables 18,616 19,047Tax assets 2,316 2,498Other current assets 38,661 41,397Current � nancial assets 11,319 4,810Cash and cash equivalents 81,574 28,817TOTAL CURRENT ASSETS B 171,429 115,763TOTAL ASSETS A+B 710,109 655,751SHAREHOLDERS’ EQUITY AND LIABILITIESShareholders’ equityShare capital 11 387 387Share premium reserve 349,825 354,650Other reserves 9,401 7,740Treasury shares (28,303) (31,720)Retained earnings / (losses) (37,151) (21,746)Net pro� t (loss) for the period 4,295 (15,422)SHAREHOLDERS’ EQUITY ATTRIBUTABLE TO THE OWNERS OF THE PARENT 298,454 293,889Share capital and reserves attributable to non-controlling interests 4,103 2,913Net pro� t/(loss) for the year attributable to non-controlling interests 652 1,272SHAREHOLDERS’ EQUITY ATTRIBUTABLE TO NON-CONTROLLING INTERESTS 4,755 4,185TOTAL SHAREHOLDERS’ EQUITY C 303,209 298,074Non-current liabilitiesDue to Bond holders 9 195,161 - Non-current � nancial liabilities 9 34,777 113,682Employee bene� ts 6,477 6,729Provisions for risks and charges 830 814Deferred tax liabilities 19,933 20,906Other non-current liabilities 0 9,531TOTAL NON-CURRENT LIABILITIES D 257,178 151,662Current liabilitiesDue to Bond holders 9 3,852 8,083Current � nancial liabilities 9 33,260 79,906Derivative � nancial instruments 9, 11 6,629 10,245Trade payables 65,663 68,608Tax liabilities 2,046 2,580Other current liabilities 38,272 36,593TOTAL CURRENT LIABILITIES E 149,722 206,016TOTAL LIABILITIES F=D+E 406,900 357,677TOTAL SHAREHOLDERS’ EQUITY AND LIABILITIES C+F 710,109 655,751

H

alf-y

ear R

epor

t 201

3 •

Fin

anci

al S

tate

men

ts S

ched

ules

33

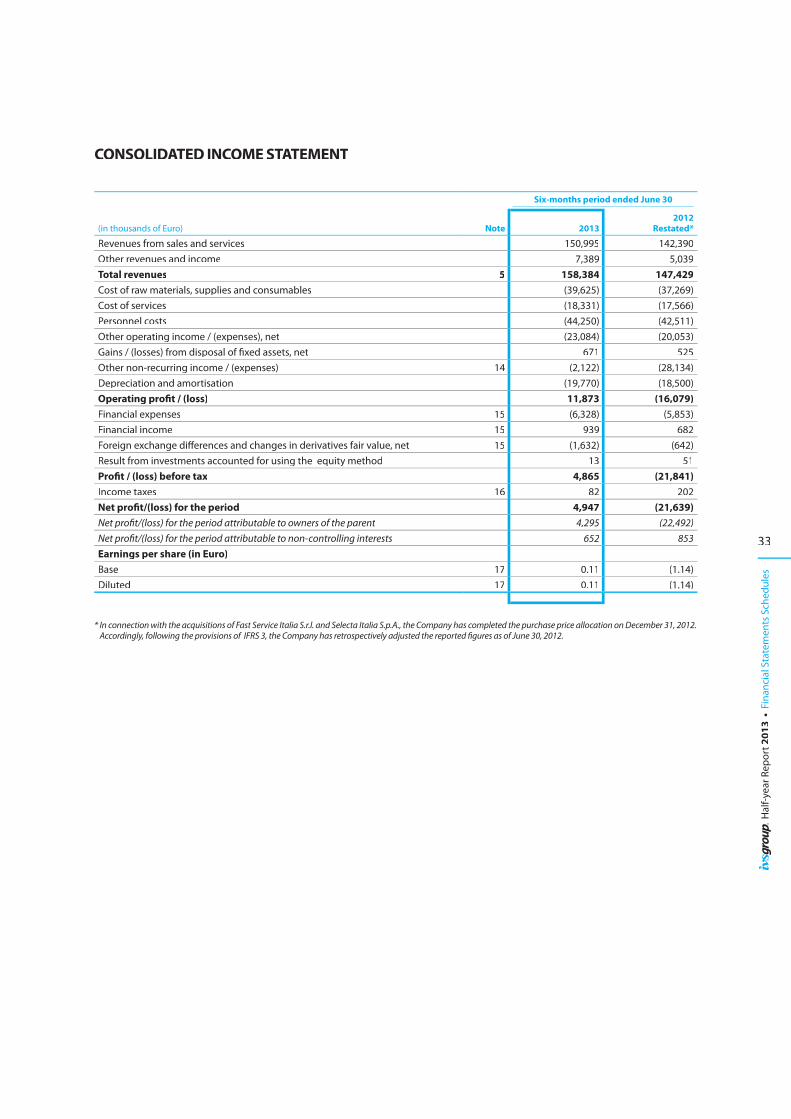

CONSOLIDATED INCOME STATEMENT

(in thousands of Euro) Note

Six-months period ended June 30

20132012

Restated*

Revenues from sales and services 150,995 142,390Other revenues and income 7,389 5,039Total revenues 5 158,384 147,429Cost of raw materials, supplies and consumables (39,625) (37,269)Cost of services (18,331) (17,566)Personnel costs (44,250) (42,511)Other operating income / (expenses), net (23,084) (20,053)Gains / (losses) from disposal of � xed assets, net 671 525Other non-recurring income / (expenses) 14 (2,122) (28,134)Depreciation and amortisation (19,770) (18,500)Operating pro� t / (loss) 11,873 (16,079)Financial expenses 15 (6,328) (5,853)Financial income 15 939 682Foreign exchange di� erences and changes in derivatives fair value, net 15 (1,632) (642)Result from investments accounted for using the equity method 13 51Pro� t / (loss) before tax 4,865 (21,841)Income taxes 16 82 202Net pro� t/(loss) for the period 4,947 (21,639)Net pro� t/(loss) for the period attributable to owners of the parent 4,295 (22,492)Net pro� t/(loss) for the period attributable to non-controlling interests 652 853Earnings per share (in Euro)Base 17 0.11 (1.14)Diluted 17 0.11 (1.14)

* In connection with the acquisitions of Fast Service Italia S.r.l. and Selecta Italia S.p.A., the Company has completed the purchase price allocation on December 31, 2012.Accordingly, following the provisions of IFRS 3, the Company has retrospectively adjusted the reported � gures as of June 30, 2012.

Hal

f-yea

r Rep

ort 2

013

• F

inan

cial

Sta

tem

ents

Sch

edul

es

34

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

(in thousands of Euro)

Six-months period ended June 30,

20132012

Restated*

Net pro� t/(loss) for the period 4,947 (21,639)Other comprehensive income to be reclassi� ed to pro� t or loss in subsequent periodsNet (loss)/gain on cash � ow hedges 2,291 268Income tax e� ect (630) (74)Net other comprehensive income to be reclassi� ed to pro� t or loss in subsequent periods 1,661 194Items not to be reclassi� ed to pro� t or loss in subsequent periodsActuarial gains/(losses) on de� ned bene� t plans 137 (198)Income tax e� ect (32) 54Net other comprehensive income not being reclassi� ed to pro� t or loss in subsequent periods 105 (144)Total income/(loss) in the statements of comprehensive income, net of taxes 6,713 (21,589)Attributable to:Owners of the Parent 6,049 (22,442)Non-controlling interests 664 853

* In connection with the acquisitions of Fast Service Italia S.r.l. and Selecta Italia S.p.A., the Company has completed the purchase price allocation on December 31, 2012Accordingly, following the provisions of IFRS 3, the Company has retrospectively adjusted the reported � gures as of June 30, 2012.

H

alf-y

ear R

epor

t 201

3 •

Fin

anci

al S

tate

men

ts S

ched

ules

35

CON

SOLI

DAT

ED S

TATE

MEN

T O

F CH

AN

GES

IN S

HA

REH

OLD

ERS’

EQ

UIT

Y D

URI

NG

TH

E FI

RST

SIX

MO

NTH

S O

F 20

13

(in th

ousa

nds

of E

uro)

Shar

ehol

ders

’equ

ity

of th

e IV

S G

roup

S.A

.

Att

ribu

tabl

e to

non

-co

ntro

lling

in

tere

sts

Tota

l Sh

areh

olde

rs’

equi

tySh

are

capi

tal

Shar

e pr

emiu

m

rese

rve

Trea

sury

sh

ares

Oth

erca

pita

l re

serv

es

Reta

ined

ea

rnin

gs/

(loss

es

brou

ght

forw

ard)

Rese

rve

for

cash

� ow

he

dges

Net

inco

me/

(loss

) for

the

peri

odTo

tal

Bal

ance

as

of Ja

nuar

y 1,

201

3 38

735

4,65

0(3

1,72

0)9,

401

(21,

746)

(1,6

61)

(15,

422)

293,

889

4,18

529

8,07

4 A

lloca

tion

of n

et in

com

e (lo

ss)

(15,

422)

15,4

22 -

0 N

et re

sult

for t

he p

erio

d 4,

295

4,29

565

24,

947

Oth

er c

ompr

ehen

sive

inco

me

941,

661

1,75

512

1,76

6 T

otal

com

preh

ensi

ve in

com

e/(lo

ss)

- -

- -

941,

661

4,29

56,

050

664

6,71

3 T

reas

ury

shar

es s

old:

-

to IV

S Pa

rtec

ipaz

ioni

S.p

.A.

3,41

7(1

96)

3,22

13,

221

Tot

al e

� ec

t of T

reas

ury

shar

es s

old

- -

3,41

7 -

(196

) -

- 3,

221

- 3,

221

Oth

er m

ovem

ents

: R

ecla

ssi�

catio

n 11

8 1

18

(118

)0

Wai

ver c

redi

t min

ority

sha

reho

lder

s of

CSH

Srl

- 24

24

Rou

ndin

gs

11

2 T

otal

oth

er m

ovem

ents

-

- -

- 11

9 -

- 11

9(9

4)25

Pay

men

t of d

ivid

ends

(4

,825

)(4

,825

)(4

,825

) B

alan

ce a

s of

June

30,

201

3 38

734

9,82

5(2

8,30

3)9,

401

(37,

151)

- 4,

295

298,

454

4,75

530

3,20

9

Hal

f-yea

r Rep

ort 2

013

• F

inan

cial

Sta

tem

ents

Sch

edul

es

36

CON

SOLI

DAT

ED S

TATE

MEN

TS O

F CH

AN

GES

IN S

HA

REH

OLD

ERS’

EQ

UIT

Y D

URI

NG

TH

E FI

RST

SIX

MO

NTH

S O

F 20

12 (R

ESTA

TED

)*

(in th

ousa

nds

of E

uro)

Shar

ehol

ders

’equ

ity

of th

e IV

S G

roup

S.A

.

Att

ribu

tabl

e to

non

-co

ntro

lling

in

tere

sts

Tota

l Sh

areh

olde

rs’

equi

tySh

are

capi

tal

Shar

e pr

emiu

m

rese

rve

Trea

sury

sh

ares

Oth

erca

pita

l re

serv

es

Reta

ined

ea

rnin

gs/

(loss

es

brou

ght

forw

ard)

Rese

rve

for

cash

� ow

he

dges

Net

inco

me/

(loss

) for

the

peri

odTo

tal

Bala

nce

as o

f Jan

uary

1, 2

012

64,0

022,

498

5,23

1(1

9,88

4)(2

,216

)2,

684

52,3

157,

403

59,7

18A

lloca

tion

of n

et in

com

e (lo

ss)

2,68

4(2

,684

)-

-N

et lo

ss fo

r the

per

iod

(22,

492)

(22,

492)

853

(21,

639)

Oth

er c

ompr

ehen

sive

inco

me

(143

)19

451

51To

tal c

ompr

ehen

sive

inco

me/

(loss

) -

--

-(1

43)

194

(22,

492)

(22,

441)

853

(21,

588)

E� e

cts

of a

cqui

sitio

n of

non

-con

trol

ling

inte

rest

s-

-- I

VS F

ranc

e S.

a.S.

(366

)(3

66)

(2,0

30)

(2,3

96)

- EM

MED

I S.A

.(1

,715

)(1

,715

)(9

92)

(2,7

07)

- DAV

S.A

.(1

,856

)(1

,856

)(1

,222

)(3

,078

)- M

ETRO

SHO

PPIN

G(2

7)(2

7)(2

)(2

9)To

tal e

� ec

t of A

cqui

siti

on o

f non

-con

trol

ling

inte

rest

s -

--

-(3

,964

)-

-(3

,964

)(4

,246

)(8

,210

)E�

ect

s of

sha

re c

apita

l inc

reas

es c

arrie

d ou

t:- S

hare

cap

ital i

ncre

ase

of 2

1-03

-12

128,

227

(5,2

31)

122,

996

122,

996

- Sha

re c

apita

l inc

reas

e of

04-

04-1

21,

938

285

2,22

32,

223

- Sha

re c

apita

l inc

reas

e of

03-

05-1

24,

310

945

5,25

55,

255

Tota

l e�

ect o

f Sha

re c

apit

al in

crea

ses

134,

475

1,23

0-

(5,2

31)

--

-13

0,47

4-

130,

474

E� e

cts

from

Bus

ines

s Co

mbi

natio

ns:

- Bus

ines

s co

mbi

natio

n Fa

st S

ervi

ce It

alia

S.r.

l.90

890

8To

tal e

� ec

t of B

usin

ess

Com

bina

tion

s-

--

--

--

-90

890

8E�

ect

s of

reve

rse

asse

t acq

uisi

tion

Shar

e ca

pita

l inc

reas

e (F

air V

alue

Ital

y1 In

vest

men

t S.A

. 16/

5/12

)13

0,51

013

0,51

013

0,51

0Ac

quis

ition

of o

wn

shar

es(3

1,72

0)31

,720

--

Exis

ting

shar

es It

aly1

Inve

stm

ent S

.A.

175

134,

860

(135

,035

)-

-Sh

are

capi

tal in

crea

se in

favo

ur o

f the

shar

ehol

ders

of I

VS G

roup

Hol

ding

S.p

.A.

212

219,

788

(220

,000

)-

-Re

clas

si� c

atio

n of

the

shar

e ca

pita

l of I

VS G

roup

Hol

ding

S.p

.A.

(198

,477

)(3

,728

)20

2,20

5-

-To

tal e

� ec

t fro

m re

vers

e as

set a

cqui

siti

on(1

98,0

90)

350,

920

(31,

720)

9,40

0-

--

130,

510

-13

0,51

0Pa

ymen

t of d

ivid

ends

-(1

88)

(188

)Ba

lanc

e as

of J

une

30, 2

012

387

354,

648

(31,

720)

9,40

0(2

1,30

7)(2

,022

)(2

2,49

2)28

6,89

44,

730

291,

624

* In

conn

ectio

n w

ith th

e ac

quis

ition

s of F

ast S

ervi

ce It

alia

S.r.

l. an

d Se

lect

a Ita

lia S

.p.A

., th

e Co

mpa

ny h

as co

mpl

eted

the

purc

hase

pric

e al

loca

tion

on D

ecem

ber 3

1, 2

012.

Acc

ordi

ngly

, fol

low

ing

the

prov

isio

ns o

f IF

RS 3

, the

Com

pany

has

retr

ospe

ctiv

ely

adju

sted

th

e re

port

ed �

gure

s as o

f Jun

e 30

, 201

2.

H

alf-y

ear R

epor

t 201

3 •

Fin

anci

al S

tate

men

ts S

ched

ules

37

CONSOLIDATED STATEMENT OF CASH FLOWS

Six Months EndedJune 30, 2013

Six Months EndedJune 30, 2012

Restated*

A) Cash � ows from operating activities Pro� t (Loss) before tax 4,865 (21,841)Adjustments for:Undistributed pro� t/(loss) of associates valued at net equity (13) (51)Amortisation, depreciation and impairment losses 20,111 18,385Non-recurring costs of reverse asset acquisition - 25,476(Gains)/losses on disposal of non-current assets (670) (525)Changes in employee bene� ts and other provisions (374) 270Reversal of � nancial expense 4,005 5,813 Cash � ows from operating activities before tax, � nancial income/expense and changes in

working capital: 27,924 27,527Changes in working capital 4,934 (13,164) Cash � ows from operating activities before tax and � nancial income/expense: 32,858 14,363Net � nancial expense paid (10,184) (5,859)Tax paid (2,667) (1,612)

Total A) 20,007 6,892B) Cash � ows from investing activities:Investments in non-current assets:Intangible assets (273) (618)Property, plant and equipment (21,943) (14,312)Payments for property, plant and equipment acquired in previous years (1,495) 664Business acquired (2,670) (1,932)Acquisition of subsidiaries, net of cash (7,968) (23,242)

Total investments (34,349) (39,440)Proceeds from disposal of net non-current assets 1,667 1,272

Total divestitures 1,667 1,272Total B) (32,682) (38,168)

C) Cash � ows from � nancing activities:Proceeds from non-current loan 205,386 9,903Repayment of non-current loan liabilities (120,054) (191,107)Changes in current � nancial liabilities (15,553) 516Changes in � nancial assets 165 13,000Changes in a Parent’s ownership interests - (7,679)Share capital increase - 130,705Share capital increase realised by means of reverse asset acquisition - 119,066Dividend distribution (4,512) -

Total C) 65,432 74,404Total D) - -

D) Exchange rate di� erences and other variations:E) Change in cash and cash equivalents (A+B+C+D): 52,757 43,128F) Cash and cash equivalents as of January 1: 28,817 36,127Cash and cash equivalents as of June 30 (E+F) 81,574 79,255

* In connection with the acquisitions of Fast Service Italia S.r.l. and Selecta Italia S.p.A., the Company has completed the purchase price allocation on December 31, 2012.Accordingly, following the provisions of IFRS 3, the Company has retrospectively adjusted the reported � gures as of June 30, 2012.

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

38

Hal

f-yea

r Rep

ort 2

013

• In

terim

man

agem

ent r

epor

t

39

Explanatory Notes to the Financial Statements

Hal

f-yea

r Rep

ort 2

013

• E

xpla

nato

ry N

otes

to th

e Fi

nanc

ial S

tate

men

ts

40

Explanatory Notes to the Financial Statements

1 – CORPORATE INFORMATION

IVS Group S.A. is a public limited company incorporated under the Luxembourg law on August 26, 2010 and registered on the Luxembourg Companies Register with the number B155.294. The company has its registered o� ces at 2A, Rue Jean-Baptiste Esch, L-1473 Luxembourg, where it is currently based. The shares of IVS Group S.A. are listed on the Italian stock market (“MTA” segment). The name of the Company was changed on May 16, 2012, from Italy1 Investment S.A..The publication of the Condensed Interim Consolidated Financial Statements for the period ended on June 30, 2013 was authorised by the Board of Directors’ resolution of August 28, 2013.

IVS Group S.A. controls, directly and indirectly, a number of companies that operate in the vending market, i.e., in the sale of products through automated and semi-automated vending machines installed at unattended points of sale (businesses, schools, hospitals, railway stations, and other public places). These machines operate 24 hours a day and allow consumers to purchase products with coins, banknotes, prepaid cards and other means of payment. The Group also controls the Coin Group, whose core business is the counting of coins for third parties, cash-in-transit services, collection and distribution of coins (coin management).

2 – BASIS OF PREPARATION AND CHANGES TO THE GROUP’S ACCOUNTING POLICIES

BASIS OF PREPARATIONThe condensed interim consolidated � nancial statements for the six months ended June 30, 2013 have been prepared in accordance with IAS 34 Interim Financial Reporting. The condensed interim consolidated � nancial statements do not include all the information and disclosures required in the annual � nancial statements, and should be read in conjunction with the Group’s annual consolidated � nancial statements as at December 31, 2012.

NEW STANDARDS, INTERPRETATIONS AND AMENDMENTS ADOPTED BY THE GROUPThe accounting policies adopted in the preparation of the condensed interim consolidated � nancial statements are consistent with those followed in the preparation of the Group’s annual consolidated � nancial statements for the year ended December 31, 2012, except for the adoption of new standards and interpretations e� ective as of January 1, 2013.

The Group applied, for the � rst time, some standards and amendments that require restatement of previous � nancial statements. These include amendments to IAS 1 Presentation of Financial Statements. As required by IAS 34, the nature and the e� ect of these changes are disclosed below.

IAS 1 Presentation of Items of Other Comprehensive Income – Amendments to IAS 1 The amendments to IAS 1 introduce a grouping of items presented in other comprehensive income (OCI). Items that could be reclassi� ed (or recycled) to pro� t or loss at a future point in time (e.g., net gain on hedge of net investment, exchange di� erences on translation of foreign operations, net movement on cash � ow hedges and net loss or gain on available-for-sale � nancial assets) now have to be presented separately from items that will never be reclassi� ed (e.g., actuarial gains and losses on de� ned bene� t plans and revaluation of land and buildings). The amendment a� ected presentation only and had no impact on the Group’s � nancial position or performance.

Hal

f-yea

r Rep

ort 2

013

• E

xpla

nato

ry N

otes

to th

e Fi

nanc

ial S

tate

men

ts

41

IFRS 7 Financial Instruments: Disclosures O� setting Financial Assets and Financial Liabilities – Amendments to IFRS 7 The amendment requires an entity to disclose information about rights to o� set � nancial instruments and related arrangements (e.g., collateral agreements). The disclosures would provide investors with information relevant to the evaluation of the e� ect of netting arrangements on an entity’s � nancial position. The new disclosures are required for all recognised � nancial instruments that are o� set in accordance with IAS 32.The disclosures also apply to recognised � nancial instruments that are subject to an enforceable master netting arrangement or similar agreement, irrespective of whether the � nancial instruments are o� set in accordance with IAS 32. As the Group is not o� setting � nancial instruments in accordance with IAS 32 and does not have relevant o� setting arrangements, the amendment does not have an impact on the Group.

IFRS 13 Fair Value Measurement IFRS 13 establishes a single IFRS framework for all fair value measurements. IFRS 13 does not determine when an entity is required to use fair value, but rather provides guidance on how to measure fair value under IFRS when fair value is required or permitted. The application of IFRS 13 has not materially impacted the fair value measurements carried out by the Group. IFRS 13 also requires speci� c disclosures on fair values, some of which replace existing disclosure requirements set by other standards, including IFRS 7 Financial Instruments: Disclosures. Some of these disclosures are speci� cally required for � nancial instruments by IAS 34.16A(j), thereby a� ecting the interim condensed consolidated � nancial statements period. The Group provides these disclosures in Note 11.

In addition to the above-mentioned amendments and new standards, IFRS 1 First-time Adoption of International Financial Reporting Standards was amended with e� ect on reporting periods starting on or after January 1, 2013. The Group is not a � rst-time adopter of IFRS, therefore, this amendment is not relevant to the Group.

Standards and interpretations issued but not yet e� ective up to the date of preparation of the Group’s consolidated financial statements are listed below. The Group intends to adopt these standards when they become e� ective.

IFRS 10 Consolidated Financial Statements and IAS 27 Separate Financial Statements IFRS 10 establishes a single control model that applies to all entities including special purpose entities. IFRS 10 replaces the parts of previously existing IAS 27 Consolidated and Separate Financial Statements that dealt with consolidated � nancial statements and SIC-12 Consolidation – Special Purpose Entities. IFRS 10 changes the de� nition of control such that an investor controls an investee when it is exposed, or has rights, to variable returns from its involvement with the investee and has the ability to a� ect those returns through its power over the investee. To meet the de� nition of control in IFRS 10, all three criteria must be met, including: (a) an investor has power over an investee; (b) the investor has exposure, or rights, to variable returns from its involvement with the investee; and (c) the investor has the ability to use its power over the investee to a� ect the amount of the investor’s returns. IFRS 10 had no impact on the consolidation of investments held by the Group. This Standard becomes e� ective for annual periods beginning on or after January 1, 2014.

IFRS 11 “Joint arrangements”It replaces IAS 31 “Interests in joint ventures” and SIC-13 “Jointly-controlled entities - non-monetary contributions by venturers”. IFRS 11 removes the option to account for jointly controlled entities (JCEs) using proportionate consolidation. Instead, JCEs that meet the definition of a joint venture must be accounted for using the equity method. This Standard becomes e� ective for annual periods beginning on or after January 1, 2014.

IFRS 12 “Disclosure of interests in other entities”It includes all of the disclosure requirements about consolidated financial statements that were previously covered by IAS 27, as well as all those that were previously included in IAS 31 and IAS 28. These disclosures

Hal

f-yea

r Rep

ort 2

013

• E

xpla

nato

ry N

otes

to th

e Fi

nanc

ial S

tate

men

ts

42

relate to an entity’s interests in subsidiaries, joint ventures, associates and structured entities. A number of new disclosures are also required. The Standard will have no impact on the Group’s financial position or its results for the period. This Standard becomes e� ective for annual periods beginning on or after January 1, 2014.

3 – SEASONAL FACTORS

In the vending sector the seasons have a signi� cant impact on the sales mix: in warmer months the consumption of cold drinks increases, while in colder months the consumption of co� ee is most important. However, the e� ect on economic result in terms of margin between the � rst and the second half of the calendar year is insigni� cant, as the abovementioned seasonal e� ects o� set each other. On the other hand, the volume of the Coin division business increases signi� cantly in the summer months, and therefore the � gures shown for the � rst six months of the year are not representative of the trend for the entire year.

4 – BUSINESS COMBINATIONS

During the � rst six months of 2013, the subsidiary IVS Italia S.p.A. � nalised the following:- on February 6, 2013 the acquisition of 100% of the share capital of Liguria Ca� è Automatico S.r.l., an Italian

company operating in the vending sector;- the acquisition of four business segments of Italian companies (Danmatic, D’Andrea, DAG and Til Ca� ).

All these acquisitions were recorded using the acquisition method of accounting. Consequently, the condensed interim consolidated � nancial statements as of June 30, 2013 include the results of Liguria Ca� è Automatico S.r.l. from the date of acquisition of control.

The fair values of the identi� able assets acquired and liabilities assumed of these companies as at the date of acquisition were the following:

(in thousands of Euro)Liguria Ca� è

Automatico S.r.l.Acquisition of business units