h1 2017 interim results - thomascookgroup.com · germany ›interest costs ... consolidate finance...

TRANSCRIPT

H1 2017 Interim Results 18 May 2017

Agenda

Page 2

› Highlights - Peter Fankhauser | CEO

› Financial results

› Strategic progress

› Current trading and outlook

Strategic actions leading to improved performance

Page 3 1 HIGHLIGHTS

› Growing top line Revenue up 3% reflecting expanded Winter Sun programme

› Improved profit performance Seasonal underlying EBIT loss improved by £2 million; loss after tax better by £27 million

› Delivering on our customer promises Net Promoter Score up by 8 points

› More unique holidays Sales of holidays to higher margin own-brand hotels up 10%

› Good demand for the Summer On track to meet full year expectations

Agenda

Page 4

› Highlights

› Financial results - Michael Healy | Group CFO

› Strategic progress

› Current trading and outlook

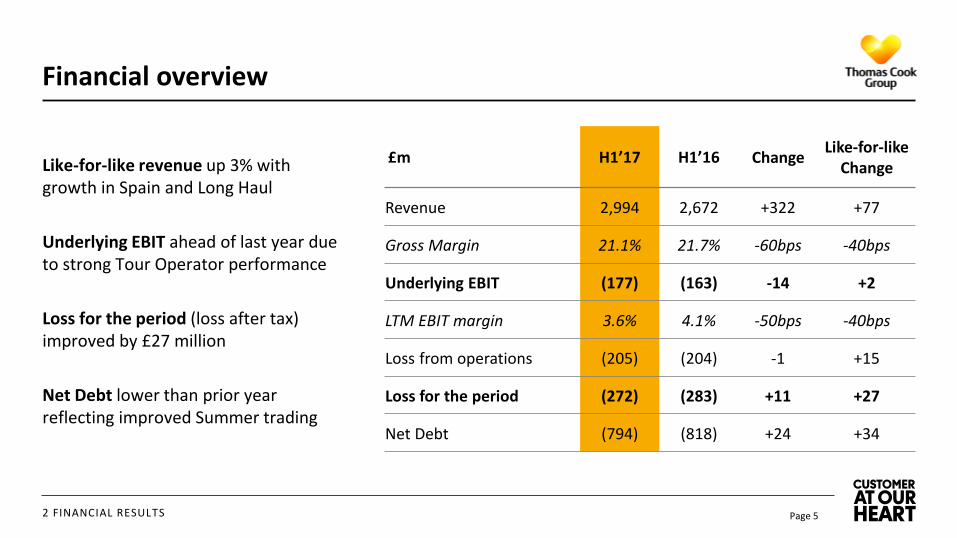

Financial overview

2 FINANCIAL RESULTS Page 5

£m H1’17 H1’16 Change Like-for-like

Change

Revenue 2,994 2,672 +322 +77

Gross Margin 21.1% 21.7% -60bps -40bps

Underlying EBIT (177) (163) -14 +2

LTM EBIT margin 3.6% 4.1% -50bps -40bps

Loss from operations (205) (204) -1 +15

Loss for the period (272) (283) +11 +27

Net Debt (794) (818) +24 +34

Like-for-like revenue up 3% with growth in Spain and Long Haul

Underlying EBIT ahead of last year due to strong Tour Operator performance

Loss for the period (loss after tax) improved by £27 million

Net Debt lower than prior year reflecting improved Summer trading

Group revenue bridge

Page 6 2 FINANCIAL RESULTS

Continued expansion of our Western Med and Long Haul programmes

65

56

326

2,917

Easter timing

(55)

Fuel

(26)

FX H1’16

2,672

H1’17 LfL Spain

18

Greece Long Haul

18

2,994

Other

(80)

Turkey

Like-for-like change +£77m (+3%)

H1’17

-41%

+5%

+36% +6%

+3%

Gross margin by business

Group gross margin slightly below last year, mainly due to weaker trading at Condor

Page 7

UK Continental Europe

Northern Europe

Condor Group

21.1% 21.5% 21.2% 23.3%

24.5%

27.9% 25.8% 26.4%

22.7% 23.1% 22.7% 21.2%

13.7% 14.2% 13.9%

2 FINANCIAL RESULTS

H1’15 LfL

H1’16 LfL

H1‘17 H1’15 LfL

H1’16 LfL

H1‘17 H1’15 LfL

H1’16 LfL

H1‘17

H1’15 LfL

H1’16 LfL

H1‘17 H1’15 LfL

H1’16 LfL

H1‘17

+40bp -20bp -60bp -120bp -40bp

Group EBIT bridge

Page 8 2 FINANCIAL RESULTS

New Operating Model continues to benefit the UK and Continental Europe

(19)

(10)

(6)

14

8

Continental Europe

UK

(179)

H1’16 LfL Easter timing FX H1’16

(163)

Like-for-like change +£2m

H1’17

(177)

Corporate

(1)

Condor Northern Europe

0

Includes net New Operating Model

Benefits of £15m

EBIT by business

Page 9 2 FINANCIAL RESULTS

(176)

324

(58)

(129)

(179)

(22)

42

(58)

(128)(177)

(41)

42

(50)

(114)

H1’15 LfL

H1’16 LfL

H1‘17

UK Continental

Europe Condor Group(i)

+£14m +£8m -£19m +£2m

Northern Europe

Same

H1’15 LfL

H1’16 LfL

H1‘17 H1’15 LfL

H1’16 LfL

H1‘17 H1’15 LfL

H1’16 LfL

H1‘17 H1’15 LfL

H1’16 LfL

H1‘17

(i) Group includes Corporate costs of £14m in H1’17 (H1’16 LfL: £13m; H1’15 LfL: £17m)

Challenging H1 for Condor but on track to meet full year improvement plans

4.9% 6.8% 10.2% 10.4% 3.0% -2.5% 4.0% 3.6% LTM EBIT Margin % 4.5% 4.9% 3.9% 7.3% 2.4% 1.9% 2.5%

Condor H1 performance

Page 10 2 FINANCIAL RESULTS

Profitability actions starting to improve performance

(8)

(18)

Yield Profitability actions

7 (41)

H1’17

Like-for-like change -£19m

FX FX

(1)

H1’16

(18)

H1’16 LfL

(22) (3)

Easter timing

(38) (13) (6)

Q4'16LfL

Q1'17LfL

Q2'17

Page 11

Improving trend for Condor profitability through implementation of improvement measures

Reroute capacity

Cost reduction initiatives

Fuel hedging benefit

More flexible planning

Improving trend of Condor’s performance

Condor year-on-year EBIT change (£m)

Targeting £35m of annualised profit improvement1 – full impact in FY18

Profit improvement measures

2 FINANCIAL RESULTS

1. Versus FY16 baseline

Group cash flow

2 FINANCIAL RESULTS Page 12

£m H1’17 H1’16 Change

EBITDA (66) (66) -

Working Capital (335) (407) +72

Tax (30) (6) -24

Pensions & Other (8) (6) -2

Operating Cashflow (439) (485) +46

Bond refinancing costs (10) - -10

Exceptional items (41) (35) -6

Capital Expenditure(i) (91) (84) -7

Net Interest Paid (67) (42) -25

Free Cash Flow (648) (646) -2

Co-op payment (32) (4) -28

Net Cash Flow (680) (650) -30

Improvement in operating cash flow of £46 million offset by bond refinancing costs and Co-op payment

› Working capital boosted by strong Summer bookings

› Higher tax due to timing of tax payments in Germany

› Interest costs higher due to timing of interest payments in relation to bond refinancing

› £32 million paid to Co-op in respect of UK retail joint venture

(i) Capex shown net of disposal proceeds (£1m in H1’17 and £1m in H1’16)

Net debt

Page 13 2 FINANCIAL RESULTS

Net Debt of £794 million represents a reduction of £34 million on a like-for-like basis

Operating Cashflow

Mar-16 LfL

£539m

£(155)m

£(32)m

Net Interest Paid

£(794)m

Like-for-like reduction £34m

Mar-17 Co-op payment

£(208)m

£(828)m

Bond refinancing

£(25)m

FX

£15m

Mar-16

£(818)m

Exceptionals Capex

£(110)m

Includes timing impact of £24m of interest paid in connection with

bond refinancing in December 2016 Includes £10m cash and £15m non-cash costs

Page 14

Financing review

› Target to reduce fixed-term debt by further £200 million Lower interest costs remains a key priority for Group

› Strengthened financial position New €750m 2022 bond extends debt maturities at a lower interest rate

› Improving credit outlook Outlook revised from ‘Stable’ to ‘Positive’ by Fitch and Standard & Poor’s

› Expect to declare dividend with full year results Policy targets distribution of 20% to 30% of reported net profit

2 FINANCIAL RESULTS

Agenda

Page 15

› Highlights

› Financial results

› Strategic progress - Peter Fankhauser | CEO

› Current trading and outlook

Our strategy for profitable growth – a recap

Page 16 3 STRATEGIC PROGRESS

Benefits from our strategic progress – 1

Page 17 3 STRATEGIC PROGRESS

CARE

CONTACT

More satisfied customers

› UK web sales up 15% and Germany up 35%

› Enriched online content for greater inspiration

› Growing direct distribution in Germany through more franchise retail and improved web distribution

More effective customer engagement

› Focus on service and quality drives up Group Net Promoter Score by 8 points

› 24-hour hotel promise extended to reach 80% of sun & beach customers in core hotels

Benefits from our strategic progress – 2

Page 18 3 STRATEGIC PROGRESS

HOLIDAYS

SERVICES

PARTNER- SHIPS

› Own-brand hotel sales up 10% for the Summer

› Moving towards fewer, better quality differentiated hotels

More focused, higher quality hotel offering

› Ancillary sales up 14%, reflecting more personalised offers

› New business unit to focus on holiday money

Added value from personalised services

› Webjet partnership in complementary hotels leading to efficiencies across the Group

› Thomas Cook China growing rapidly

Acceleration of strategic progress

Progress towards a more focused holiday offering

Page 19 3 STRATEGIC PROGRESS

Number of Customers

Number of Hotels Own-brand hotels (part of differentiated hotel offering)

Differentiated hotels

› Focus on added value to our customers

› Greater influence on hotel quality

› Leverage scale across Group

› Automated low-cost production

› Source electronically

› Expands choice for customer

Differentiated Hotels Complementary Hotels

1/3 of holiday customers

2/3 of holiday customers

Developing and growing own-brand hotels

Page 20

› Own-brand hotels are key to our holiday offering:

- Higher NPS than other hotels

- More control

- Higher returns

› Pipeline of 11 new hotels for Summer 17, and a further 11 by Summer 18

› Focus on quality and sharpening brands

3 STRATEGIC PROGRESS

Sunwing Sandy Bay, Cyprus Casa Cook, Kos

Sunprime Miramare, Rhodes SENTIDO Flora Garden, Antalya

Developing our airline business

Page 21 3 STRATEGIC PROGRESS

Opening new routes

› 15 new destinations added this year

› Long-haul growth – S17 bookings +9%

› Short-haul flexibility to match demand changes

Leveraging distribution Customer focus Cost control

› 50% of passengers from TC tour operator

› Growing direct-to-customer and 3rd party tour operator channels

› Entire fleet new or refurbished

› Significant reduction in 3-hour delays

› New in-flight entertainment

› Rigorous cost discipline to maintain competitive edge

› Improved reliability

› Increased productivity

Benefits from our strategic progress – 2

Page 22 3 STRATEGIC PROGRESS

HOLIDAYS

SERVICES

PARTNER- SHIPS

› Own-brand hotel sales up 10% for the Summer

› Moving towards fewer, better quality differentiated hotels

More focused, higher quality hotel offering

› Ancillary sales up 14%, reflecting more personalised offers

› New business unit to focus on holiday money

Added value from personalised services

› Webjet partnership in complementary hotels leading to efficiencies across the Group

› Thomas Cook China growing rapidly

Acceleration of strategic progress

Benefits from our strategic progress – 3

Page 23 3 STRATEGIC PROGRESS

OPERATIONAL EFFICIENCIES AND STREAMLINED ORGANISATION STRUCTURE

› Cost initiatives underway to align and integrate our tour operator processes

› Reducing duplication and sharing best practice in Continental Europe

› Further restructuring in France

› New shared service centre in Palma to consolidate finance support across Group

£60m of cost efficiencies targeted

through New Operating Model

Agenda

Page 24

› Highlights

› Financial results

› Strategic progress

› Current trading and outlook - Peter Fankhauser | CEO

Current trading – Summer bookings up 12%

Page 25

Based on cumulative bookings to 6th May 2017

Winter 2017/18

Summer 2017

• Very early in cycle with around 10% sold

• Bookings slightly higher than last year; average selling prices up 5%

• Strong trading with bookings up 12%, pricing broadly in line

• High demand for Greece and smaller European destinations

• Double-digit bookings growth for Continental and Northern Europe

• Condor bookings up 18%

• UK focus on quality and margin due to more competitive market to Spain

4 CURRENT TRADING AND OUTLOOK

Page 26

Summary and outlook

› Strategic progress is delivering results

› Putting the customer first

› Improving our holiday offering

› On track to deliver market expectations for the full year

4 CURRENT TRADING AND OUTLOOK

Page 27

Q&A

Financial calendar

› Q3 2017 Results - 27 July 2017

› Pre-close Trading Update – 26 September 2017

› 2017 Full Year Results – 22 November 2017

› Q1 2018 Results – 8 February 2018

› Pre-close Trading Update – 27 March 2018

› H1 2018 Interim Results – 17 May 2018

Page 28 APPENDIX

331

(127)(54)

488

24

343

(129)(50)

498

24

294

(128)(49)

469

2

8.6

1.41.6

3.52.1

8.4

1.31.6

3.52.0

8.1

1.41.63.3

1.8

Revenue & EBIT by quarter

Page 29 APPENDIX

Q4 40%

Q1 20%

H1 LTM(1)

Q3 23%

Revenue £bn

EBIT £m

Share of revenue

-£0.2bn -£0.2bn Same +£0.1bn

-£0.3bn

H1’16 LTM LfL

H1’17 LTM

H1’15 LTM LfL

Q2’16 LfL

Q2’17 Q2’15 LfL

Q1’16 LfL

Q1’17

Q1’15 LfL

Q4’15 LfL

Q4’16

Q4’14 LfL

Q3’15 LfL

Q3’16

Q3’14 LfL

-£22m -£29m +£1m +£1m

-£49m

(1) LTM refers to last twelve months

Q2 17%

Group income statement

Page 30

£m H1’17 H1’16 LfL H1’15 LfL H1’17 to H1’16

LfL Change

Revenue 2,994 2,917 2,993 +77

Gross Profit 633 627 635 +6

Overheads (810) (806) (811) -4

EBIT (177) (179) (176) +2

Separately Disclosed Items (EBIT) (28) (41) (47) +13

Loss from Operations (205) (220) (223) +15

Associated Undertakings - - 8 -

Net Finance costs (74) (73) (79) -1

Separately Disclosed Items (Finance Charges) (35) (7) (12) -28

Loss before Tax (314) (300) (306) -14

Tax 42 1 (11) +41

Loss for the period (272) (299) (317) +27

APPENDIX

Revenue by business

Page 31

H1’17 vs. H1’16

£m H1’17 H1’16 H1’16 LfL Headline variance

Like-for-like variance

UK & Ireland 707 700 664 +1% +6%

Continental Europe 1,206 1,036 1,201 +16% Flat

Northern Europe 617 536 583 +15% +6%

Condor 609 546 616 +12% -1%

Corporate (145) (146) (147) n/a n/a

Group Revenue 2,994 2,672 2,917 +12% +3%

APPENDIX

Gross margin by business

Page 32

H1’17 vs. H1’16

£m H1’17 H1’16 H1’16 LfL Headline variance

Like-for-like variance

UK & Ireland 23.1% 22.4% 22.7% +70bps +40bps

Continental Europe 13.7% 13.8% 13.9% -10bps -20bps

Northern Europe 25.8% 26.7% 26.4% -90bps -60bps

Condor 23.3% 24.2% 24.5% -90bps -120bps

Corporate n/a n/a n/a n/a n/a

Group Gross Margin 21.1% 21.7% 21.5% -60bps -40bps

APPENDIX

EBIT by business

Page 33

H1’17 vs. H1’16

£m H1’17 H1’16 H1’16 LfL Headline variance

Like-for-like variance

UK & Ireland (114) (124) (128) +8% +11%

Continental Europe (50) (48) (58) -4% +14%

Northern Europe 42 40 42 +5% Flat

Condor (41) (18) (22) -128% -86%

Corporate (14) (13) (13) n/a n/a

Group EBIT (177) (163) (179) -9% +1%

APPENDIX

Page 34

Supplementary information – Tour Operators

APPENDIX

H1’17 vs. H1’16

£m H1’17 H1’16 H1’16 LfL Headline variance

Like-for-like variance

Revenue 2,284 2,056 2,264 +228 +20

Gross Margin 15.0% 15.0% 14.9% Flat +10bps

Underlying EBIT (81) (93) (100) +12 +19

Underlying LTM EBIT margin (%) 4.0% 3.6% 3.5% +40bps +50bps

Average Selling Price (ASP) (£) 723 611 685 +112 +38

Page 35

Supplementary information - Airlines

APPENDIX

H1’17 vs. H1’16

£m H1’17 H1’16 H1’16 LfL Headline variance

Like-for-like variance

Revenue 1,202 1,098 1,163 +104 +39

Gross Margin 23.8% 24.3% 24.7% -50bps -90bps

Underlying EBIT (82) (57) (66) -25 -16

Underlying EBITDAR 67 64 75 +3 -8

Underlying LTM EBIT margin (%) 2.0% 4.5% 4.4% -250bps -240bps

Available Seat Kilometre (ASK) (‘m) 22,148 21,675 21,675 +473 +473

Seat Load Factor (SLF) (%) 88.6% 88.3% 88.3% +0.3% +0.3%

Long Haul Yields per seat (£) 307 291 324 +16 -17

Short Haul Yields per seat (£) 116 108 121 +8 -5

Separately disclosed items

Page 36

P&L (£m) H1’17 H1’16

New Operating Model implementation costs (18) (20)

Restructuring costs (9) (4)

Reassessment of provisions 32 4

Store closures (16) (13)

Other (17) (8)

EBIT related items (28) (41)

Finance related charges (35) (7)

Total (63) (48)

Of which:

- Cash(i) (57) (23)

- Non-Cash (6) (25)

(i) Items classified as ”Cash” represent both current year cash flows, and cash effects which are yet to be realised

Cash (£m) H1’17 H1’16

Cash related exceptionals (57) (23)

Of which will be paid in future years 22 -

Prior year cash exceptionals paid in financial year (13) (8)

Prior year EU261 (paid in financial year) (3) (4)

Total (51) (35)

APPENDIX

Underlying finance costs

Page 37 APPENDIX

Pro Forma P&L

£m Coupon H1’17 H1’16 2017 2018 2019 2020 2021 2022

Interest on bank facilities LIBOR

+3.50% 2 0 - - - - - -

Interest on 2017 £300m bond 7.75% 4 12 4 - - - - -

Interest on 2020 €525 bond (inc. IRS) 7.75% 6 14 7 - - - - -

Interest on 2021 €400m bond 6.75% 12 10 23 23 23 23 17 -

Interest on 2022 €750m bond 6.25% 13 - 33 40 40 40 40 30

Bank and bond interest and related charges 37 36 67 63 63 63 57 30

Commitment fees 3 4

Assumed at c.£70m (same level as 2016)

Letters of credit & bonding 9 8

Other interest costs 7 10

Interest & finance costs before aircraft financing

56 58

Interest income (2) (3)

Net interest & finance costs before aircraft financing

54 55

Aircraft financing 9 8

Fee amortisation and other non-cash 11 10

Net Interest Expense (excl.

exceptionals) 74 73 137 133 133 133 127 100

Assumes all bonds are paid on maturity

Net debt composition

Page 38 APPENDIX

Maturity profile – 31 March 2017

800

342

641

2017 2022 2018 2019 2021 2020

Bank facility

€400m senior notes

€750m senior notes

£m H1’17 H1’16 Variance

2017 GBP Bond Jun-17 - (299) +299

2020 Euro Bond Jun-20 - (415) +415

2021 Euro Bond Jun-21 (342) (316) -26

2022 Euro Bond Jun-22 (642) - -642

Commercial Paper Various (140) (134) -6

Revolving Credit Facility May-19 (50) - -50

Finance Leases Various (167) (183) +16

Aircraft related borrowings Various (47) (69) +22

Other external debt Various (33) (25) -8

Arrangement fees & other n/a 18 16 +2

Total Debt (1,403) (1,425) +22

Cash 609 607 +2

Net Debt (794) (818) +24

£m

Cash conversion

Page 39 APPENDIX

Cash conversion (£m) H1’17 LTM

H1’16 LTM

FY16

Underlying EBIT 294 321 308

Net interest (141) (135) (140)

Underlying PBT 153 186 168

Free cash flow 56 (51) 56

Cash conversion 36% n/m 33%

H1’17 LTM

FY16 H1’16 LTM

33% 36%

Not meaningful

Reconciliation of ‘like for like’ to underlying numbers

Page 40

“Underlying” refers to trading results after adjusting for separately disclosed items that are significant in understanding the on-going results. “Like for like” reflects the comparison in the underlying results after removing identifiable non-recurring items in the prior year.

Revenue Gross Margin EBIT

£m H1’17 £m

H1’16 £m

Change £m

H1’17 %

H1’16 %

Change %

H1’17 £m

H1’16 £m

Change £m

Underlying 2,994 £2,672 +322 21.1% 21.7% -60bps (177) (163) -14

Easter timing (55) +55 0.1% -10bps (10) +10

Impact of Currency Movements and other(i) 326 -326 (0.5)% +50bps (6) +6

Reduced fuel costs (26) +26 0.2% -20bps - -

Like-for-Like 2,994 2,917 +77 21.1% 21.5% -40bps (177) (179) +2

APPENDIX

(i) Other includes alignment of comparatives to reallocate per diem costs associated with airline crew from operating costs to cost of sales

Page 41

Capital expenditure

H1’16 H1’17

3

30

6 4

41 Hotels

IT

Airlines

Other

Store refits

£84m

5

31

7

45

3

£91m

APPENDIX

FX and fuel hedging (30 April 2017)

Page 42 APPENDIX

Winter

2016/17 Price Summer

2017 Price 2017 Price Winter

2017/18 Price Summer

2018 Price 2018 Price

EUR 99% 95% 96% 76% 41% 51%

USD 97% 94% 95% 84% 43% 62%

Jet Fuel(i) 95% $587 90% $485 92% $536 98% $519 51% $528 72% $521

Overall Fuel Rate(ii)

£466 £468

((iii) Spot rates as at 30 April 2017

FY17 overall fuel rate £466/Mt represents a projected saving of £30m versus FY16 (£505/Mt)

Transactional USD exposures against EUR, GBP and DKK have been hedged in line with Fuel hedges. A 1% variance in 2017 would have an annualised £0.7m impact

Transactional EUR exposures against GBP and SEK hedged in line with policies. A 1% variance in 2017 would have an annualised £0.4m impact

It is our policy not to hedge EUR and SEK profits and so FY16 profits will not be hedged. At current rates(iii), the impacts of fluctuations in those currencies can be summarised as:

Every 1% move in Euro has a £1.3m impact on EBIT

Every 1% SEK movement has a £0.6m impact on EBIT

(i) Jet Fuel Price [$/Mt] incorporates achieved hedge rates per season with market forward rates applied to unhedged portion.(ii) Based on estimated Jet Fuel costs & Intoplane costs, converted at $ blended hedged rates into functional CCY equivalents and then translated into GBP, either at blended rates for partially completed years or latest spot rates [£/Mt]