h-1. h-2 appendix h other significant liabilities learning objectives after studying this chapter,...

TRANSCRIPT

H-1

H-2

Appendix HOther Significant Liabilities

Learning Objectives

After studying this chapter, you should be able to:

1. Describe the accounting and disclosure requirements for provisions and contingent liabilities.

2. Contrast the accounting for operating and finance leases.

3. Identify additional fringe benefits associated with employee compensation.

H-3

IFRS Guidelines:

Provision – if a loss is probable (> 50% chance) and if

a reasonable estimate can be made of the amount, then

a liability should be recorded.

Contingent Liability – if a loss is not probable a

liability should not be recorded and the details of

situation should be disclosed in the notes to the financial

statements.

Remote Possibility (< 10%) – no disclosure.

LO 1 Describe the accounting and disclosure requirements for provisions and contingent liabilities.

Provisions and Contingent Liabilities

H-4

AccountingProbability

Accrue

Footnote

Need not record or disclose

Probable

ReasonablyPossible

Remote

Provisions and Contingent Liabilities

LO 1 Describe the accounting and disclosure requirements for provisions and contingent liabilities.

H-5

A provision should be recorded in the accounts when:

a. it is probable an outflow of assets will happen but the

amount cannot be reasonably estimated.

b. it is reasonably possible an outflow of assets will happen

and the amount can be reasonably estimated.

c. it is reasonably possible an outflow of assets will happen

but the amount cannot be reasonably estimated.

d. it is probable an outflow of assets will happen and the

amount can be reasonably estimated.

Question

Provisions and Contingent Liabilities

LO 1 Describe the accounting and disclosure requirements for provisions and contingent liabilities.

H-6

Recording a Provision

Product Warranties

Future costs that companies may incur in replacing defective

units or repairing malfunctioning units.

Estimated cost of honoring product warranty contracts should

be recognized as an expense in the period in which the sale

occurs.

Provisions and Contingent Liabilities

LO 1 Describe the accounting and disclosure requirements for provisions and contingent liabilities.

H-7

Illustration: In 2014, Denson Manufacturing Company sells 10,000 washers and dryers at an average price of $600 each. The selling price includes a one-year warranty on parts. Denson expects that 500 units (5%) will be defective and that warranty repair costs will average $80 per unit. In 2014, the company honors warranty contracts on 300 units, at a total cost of $24,000. At December 31, compute the estimated warranty liability.

LO 1

Illustration H-1Computation of estimatedproduct warranty liability

Provisions and Contingent Liabilities

H-8

Warranty expense 40,000

Warranty liability 40,000

Illustration: In 2014, Denson Manufacturing Company sells 10,000 washers and dryers at an average price of $600 each. The selling price includes a one-year warranty on parts. Denson expects that 500 units (5%) will be defective and that warranty repair costs will average $80 per unit. In 2014, the company honors warranty contracts on 300 units, at a total cost of $24,000. At December 31, compute the estimated warranty liability. Make the required adjusting entry.

Provisions and Contingent Liabilities

LO 1 Describe the accounting and disclosure requirements for provisions and contingent liabilities.

H-9

Illustration: Prepare the entry to record the repair costs incurred in 2014 to honor warranty contracts on 2014 sales.

Warranty liability 24,000

Repair parts 24,000

Assume that the company replaces 20 defective units in January 2015, at an average cost of $80 in parts and labor.

Warranty liability 1,600

Repair parts 1,600

Provisions and Contingent Liabilities

LO 1 Describe the accounting and disclosure requirements for provisions and contingent liabilities.

H-10

Disclosure of Contingent Liabilities

Disclosure should identify the:

Nature of the item.

Amount of the contingency, if known.

Expected outcome of the future event.

Provisions and Contingent Liabilities

LO 1 Describe the accounting and disclosure requirements for provisions and contingent liabilities.

H-11

A lease is a contractual arrangement between a lessor (owner

of the property) and a lessee (renter of the property).

LO 2 Contrast the accounting for operating and finance leases.

Illustration H-3Types of leases

Lease Liabilities

H-12

Operating LeaseOperating Lease Finance LeaseFinance Lease

Journal Entry:Journal Entry:

Rent ExpenseRent Expense xxx xxx

CashCash xxx xxx

Journal Entry:Journal Entry:

Leased Equipment xxxLeased Equipment xxx

Lease Liability xxxLease Liability xxx

A lease that transfers substantially all of the benefits and risks of A lease that transfers substantially all of the benefits and risks of property ownership should be capitalized.property ownership should be capitalized.

LO 2 Contrast the accounting for operating and finance leases.

Lease Liabilities

H-13

IFRS does not prescribe criteria for determining classification,

however if any one of the following conditions exists, the

lessee should record a lease as a finance lease:

1. The lease transfers ownership of the property to the lessee.

2. The lease contains a bargain purchase option.

3. The lease term is a major portion of the economic life of the

leased property.

4. The present value of the lease payments represents

substantially all of the fair value of the leased property.

LO 2 Contrast the accounting for operating and finance leases.

Lease Liabilities

H-14

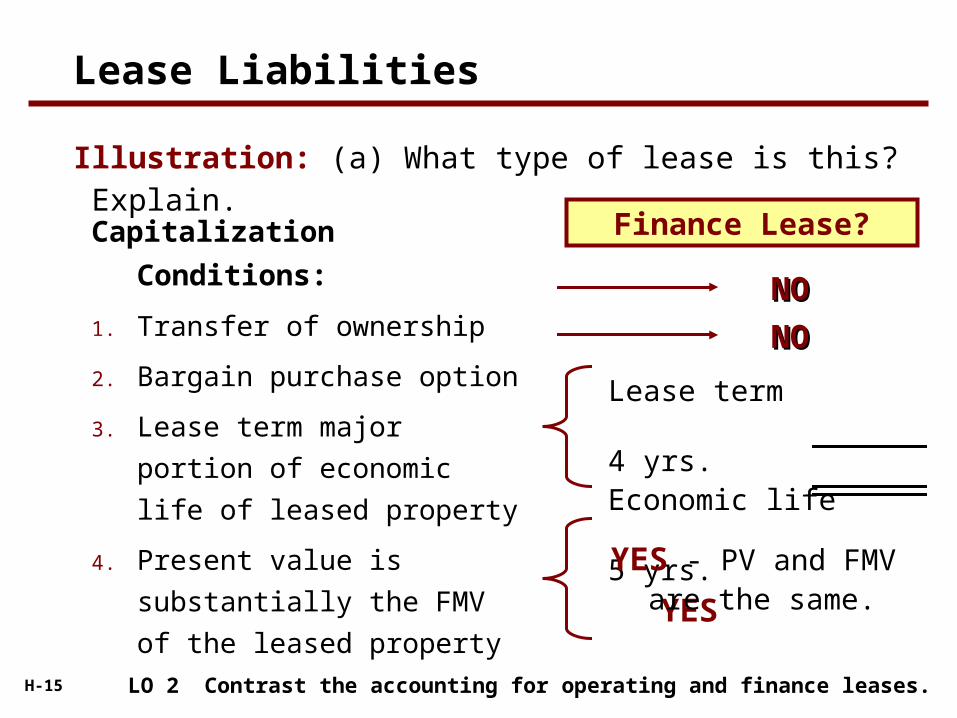

Illustration: Gonzalez Company decides to lease new equipment. The lease period is four years; the economic life of the leased equipment is estimated to be five years. The present value of the lease payments is $190,000, which is equal to the fair market value of the equipment. There is no transfer of ownership during the lease term, nor is there any bargain purchase option.

Instructions

(a) What type of lease is this? Explain.

(b) Prepare the journal entry to record the lease.

LO 2 Contrast the accounting for operating and finance leases.

Lease Liabilities

H-15

Illustration: (a) What type of lease is this? Explain.

Capitalization Conditions:

1. Transfer of ownership

2. Bargain purchase option

3. Lease term major portion of

economic life of leased

property

4. Present value is substantially

the FMV of the leased

property

NONO

NONO

Lease term

4 yrs.Economic life

5 yrs.

YES

80%

YES - PV and FMV are the same.

Finance Lease?

LO 2 Contrast the accounting for operating and finance leases.

Lease Liabilities

H-16

Illustration: (b) Prepare the journal entry to record the lease.

Leased Asset - Equipment 190,000

Lease Liability

190,000

The portion of the lease liability expected to be paid in the next year The portion of the lease liability expected to be paid in the next year is a current liability. The remainder is classified as a non-current is a current liability. The remainder is classified as a non-current liability.liability.

LO 2 Contrast the accounting for operating and finance leases.

Lease Liabilities

H-17

Paid absences for vacation, illness, and holidays.

Accrue a liability if:

Payment of the compensation is probable.

The amount can be reasonably estimated.

Paid Absences

Employee Fringe Benefits

LO 3 Identify additional fringe benefits associated with employee compensation.

H-18

Vacation benefits expense 3,300

Vacation benefits liability3,300

Illustration: Academy Company employees are entitled to one

day’s vacation for each month worked. If 30 employees earn an

average of $110 per day in a given month.

Vacation benefits liability 1,100

Cash1,100

Academy pays vacation benefits for 10 employees.

Employee Fringe Benefits

LO 3 Identify additional fringe benefits associated with employee compensation.

H-19

Postretirement Benefits

Employee Fringe Benefits

Post-retirement benefits are benefits that employers

provide to retired employees for

1. health care and life insurance

2. pensions.

Companies account for post-retirement benefits on the

accrual basis.

LO 3 Identify additional fringe benefits associated with employee compensation.

H-20

Postretirement Health-Care and Life Insurance Benefits

Employee Fringe Benefits

Companies estimate and expense postretirement costs

during the working years of the employee.

Companies rarely sets up funds to meet the cost of the

future benefits.

► Pay-as-you-go basis for these costs.

► Major reason is that the company does not receive a tax

deduction until it actually pays the medical bill.

LO 3 Identify additional fringe benefits associated with employee compensation.

H-21

An arrangement whereby an employer provides benefits to employees

after they retire for services they provided while they were working.

Pension PlanAdministrator

Pension PlanAdministrator

ContributionsEmployerEmployer

Retired Employees Benefit Payments Assets &

Liabilities

Employee Fringe Benefits Pension Plans

LO 3 Identify additional fringe benefits associated with employee compensation.

H-22

Defined-Contribution Plan Defined-Benefit Plan Employer contribution

determined by plan (fixed)

Risk borne by employees

Benefits based on plan value

Benefit determined by plan

Employer contribution varies

(determined by Actuaries)

Risk borne by employer

Companies record pension costs as an expense.

Actuaries estimate the employer contribution by considering

mortality rates, employee turnover, interest and earning rates, early

retirement frequency, future salaries, etc.

Employee Fringe Benefits Pension Plans

LO 3 Identify additional fringe benefits associated with employee compensation.

H-23

“Copyright © 2013 John Wiley & Sons, Inc. All rights reserved.

Reproduction or translation of this work beyond that permitted in

Section 117 of the 1976 United States Copyright Act without the

express written permission of the copyright owner is unlawful. Request

for further information should be addressed to the Permissions

Department, John Wiley & Sons, Inc. The purchaser may make back-

up copies for his/her own use only and not for distribution or resale.

The Publisher assumes no responsibility for errors, omissions, or

damages, caused by the use of these programs or from the use of the

information contained herein.”

Copyright