gujarat state petronet ltd | initiating...

TRANSCRIPT

1

Gujarat State Petronet Ltd | Initiating Coverage December 21st, 2009

Wealth Research, Unicon Securities Private Limited, 285 – Princess Street, Marine Lines, Mumbai -400002

Contact: +91-22- 4359 1200 | E-Mail: [email protected]

UNICON WEALTH

Year Revenue EBIDTA EBIDTA (%) PAT PAT (%) EPS P/E (x) RoE (%) RoCE (%)

FY08 4179 3645 87 999 23.9 1.8 52.0 8.8 8.6

FY09 4875 4249 87 1234 25.3 2.2 42.8 10.2 8.9

FY10E 9936 8875 89 3704 37.3 6.6 14.3 25.8 18.6

FY11E 15840 14398 91 6876 43.4 12.2 7.7 37.4 25.3

FY12E 16601 15139 91 7191 43.3 12.8 7.4 31.8 22.9

Source: Unicon Research

Industry Gas Transmission

Recommendation Accumulate

CMP (INR) 94

Target Price (INR) 105

Upside / (Downside) % 11.5%

Market Cap (INR in Mn) 52971

52 week High/Low (INR) 105 / 26

3M Average Daily Volume

3629187

Sensex / Nifty 16601 / 4953

Bloomberg Code GUJS IN

Reuters Code GSPT.BO

Shareholding Pattern (%)

(As on September 30

th, 2009)

Stock Performance (One Year Chart)

0

25

50

75

100

Dec-08 Feb-09 Apr-09 Jun-09 Aug-09 Oct-09

Company NIFTY

Performance (%)

1M 3M 12M

Company 3.6 25.8 224.2

NIFTY 0.9 4.2 63.5

Source: Unicon Research

Analyst: Arvind Rana

Accumulate Pure Gas Transmission – Strong Growth

Incorporated in December 1998, Gujarat State Petronet Ltd (GSPL)

is a gas distribution subsidiary of state-owned Gujarat State

Petroleum Corporation (GSPC). With its leadership position in

India’s fast-growing gas market, GSPL strongly claims its

perceptible volume-led growth.

INVESTMENT RATIONALE

Major beneficiary from Gujarat’s huge demand potential:

GSPL is strategically located in the Industrial clusters of Gujarat

(largest gas consuming state) driving volume growth through pre-

eminent pipeline connectivity, favourable regulation policies, and its

reach within Gujarat.

High supply volumes giving edge to GSPL growth:

With increase in gas supplies from Reliance KG basin D6 and

Petronet LNG, gas transmission volumes are expected to reach

55% CAGR over FY09-FY12E. Impact of this increase will be

reflected as growth from FY09-10 onwards for GSPL.

Focus on expansion of network outside Gujarat:

Mounting market potential beyond Gujarat drove GSPL to file

Expression of Interest (EOI) with regulator for four new routes to

grab more pipelines in its pocket. The decision on this is expected

in January-February 2010. Thus stronger growth scenario outside

Gujarat may appear for GSPL before the end of FY10E.

Benefit by bidding through SPVs:

To extract benefit from Sec 35AD, GSPL is expected to bid for the

new pipeline outside Gujarat through special purpose vehicles

(SPV), which ensures, capex on pipelines could be charged as

deductible expense. This would contribute to the bottom line

through lower taxes.

Advantage from Price Economics of Naphtha:

Naphtha prices have risen lately, rendering Regassified Liquefied

Natural Gas (RLNG) competitive, which enable the volumes to pick

up from Q4 FY09, with a visible improvement from Q1 FY10.

Valuation & Recommendation

GSPL is expected to see a huge jump in its EPS of INR 2.2 for

FY09 to INR 12.6 for FY12. Revenues are expected to grow at a

CAGR of 51% over FY09-FY12. Based on DCF calculations, stock

has an intrinsic value of INR 105. At current market price of INR 94,

we give “Accumulate” rating to the stock, with a time horizon of 12

months.

2

Gujarat State Petronet Ltd | Initiating Coverage December 21st, 2009

Wealth Research, Unicon Securities Private Limited, 285 – Princess Street, Marine Lines, Mumbai -400002

Contact: +91-22- 4359 1200 | E-Mail: [email protected]

UNICON WEALTH

CONTENTS Company Background 03 Business Model / Manufacturing Process 04 Management Brief 05 Industry Overview 05 Investment Rationale and recommendation 06

� Major beneficiary from Gujarat’s huge demand potential 06 � High supply volumes giving edge to GSPL growth 06

� GSPL looking forward to grab new pipelines by bidding through SPVs 06 � Operation & Maintenances Activities 06

� Price Economics of Naphtha 06

� Growing Demand Of Natural gas in India 07 � Tariff Regulations 07 � Favourable Gas Pipeline Policy for GSPL 08

Concerns 09 Financial analysis 09 Peer Analysis 10 Valuations & Outlook 10 Financial Tables & Ratios 11

3

Gujarat State Petronet Ltd | Initiating Coverage December 21st, 2009

Wealth Research, Unicon Securities Private Limited, 285 – Princess Street, Marine Lines, Mumbai -400002

Contact: +91-22- 4359 1200 | E-Mail: [email protected]

UNICON WEALTH

Company Background

Gujarat State Petronet Ltd (GSPL), a subsidiary of Gujarat State

Petroleum Corporation (GSPC), is the first pure transmission player in the

gas sector. It is the largest gas transmission player with outstanding

connectivity and reach in the largest gas consuming state of India, i.e.

Gujarat.

GSPL is well-known as an “open access / contract carrier” gas

transmission pipeline operator, which means that it offers the service of

transporting gas to customers who have the demand and have tied up the

supply source for a transportation fee. Thus commodity price risk does not

impact GSPL and its revenue growth mainly comes from Volume game.

GSPL is going to increase its pipeline from 1,420 km to 1,870 km by 2011.

Current capacity – 45 mmscmd (million metric standard cubic meters per

day)

Current utilization – 35 mmscmd

It has signed a 15 year agreement with Reliance Industries Ltd (RIL) to

transport 11 mmscmd. It also signed a 20 year agreement with Torrent

Power (Torrent) to transport – 4.5 mmscmd.

GSPC (Parent co) is expected to start production in KG Basin by 2010

with a volume of 10-15 mmscmd.

The Company has signed firm Gas Transmission Agreements (GTA) for

transporting 31.99 mmscmd of gas to various customers and interruptible /

short term GTA for 11.17 mmscmd. Also boost in re-gasification capacity

at Dahej & Hazira, and commissioning of the new R-LNG terminal at

Dabhol are expected to provide an opportunity to GSPL to transmit

additional R-LNG volumes going ahead.

The major customers of GSPL include RIL, Essar group, Torrent Power,

Shell, Petronet LNG, Cairn India and GSPC.

GSPL has acquired strategic stakes in Krishna Godavari Gas Network

Limited (planning to develop gas transmission) CGD (Compressed Gas

Distribution) network in Andhra Pradesh & Gujarat.

GSPL has successfully commissioned various pipeline projects like

Bhadbhut- Gana, Rajkot-Jamnagar, Padmala Halol, and Suzlon Spur.

Further, the company also continues to develop several spur lines to

connect industrial clusters and medium size customers along the pipeline

network, which include regions like Tarapur, Vilayat, Dahej, Silvasa,

Bhavnagar, Amreli, Veraval, Gandhidham, Anjar, Mundra, Jafrabad region.

GSPL has expanded its gas pipeline network beyond the traditional

markets of South Gujarat and extended it to the Central and Northern

parts of Gujarat. It is currently building a pipeline to Mundra and Pipavav

ports, which will improve its presence in the Western parts of the State.

GSPL Gas Transmission Network- Gujarat

Source: Company, Unicon Research

Previous year: GSPL GTAs - 29.27 MMSCMD &

interruptible GTAs – 7.53 MMSCMD.

Gas transmission volumes

-

10

20

30

40

50

60

FY06 FY07 FY08 FY09 FY10EFY11EFY12E

11 14 17 15

31

50 54

Gas Transportaion Volumes (MMSCMD)

Source: Company, Unicon Research

4

Gujarat State Petronet Ltd | Initiating Coverage December 21st, 2009

Wealth Research, Unicon Securities Private Limited, 285 – Princess Street, Marine Lines, Mumbai -400002

Contact: +91-22- 4359 1200 | E-Mail: [email protected]

UNICON WEALTH

Business Model

Marketers Producers LNG Terminals

Bulk Customers Local Distribution

Companies

(GSPL)

GTA GTA

Overview: GSPL’s customer space includes both suppliers as well as users of natural gas. Suppliers of natural gas include marketers,

producers of natural gas and LNG terminals. Producers/suppliers of gas have direct Gas Sale Agreements (GSA) with the

buyers and either of the parties can enter the Gas Transmission Agreement (GTA) with GSPL to use its network for gas

shipment.

Users of natural gas comprise bulk customers (power and fertilizer companies) and local distribution companies. GSPL

operates as a pure natural gas transmission company and as such does not own any natural gas transported through its

network which insulates it from the fluctuations of the prices in natural gas.

GTA

The GTA designates the entry and exit points for the natural gas as it travels through the gas transmission network. GTA also

lays down the terms including the tariffs, tenure and capacity reserved in the gas transmission network.

A typical contract period varies between 5 and 25 years. Long term agreement accounts for major portion of revenue for

GSPL. GSPL's GTAs include "ship or pay" provisions, which require its customers to pay the capacity charges for the capacity

reserved by them, regardless of the amount of natural gas they transport. GTAs also include provisions for payment security

mechanisms, such as bank guarantees and letters of credit.

5

Gujarat State Petronet Ltd | Initiating Coverage December 21st, 2009

Wealth Research, Unicon Securities Private Limited, 285 – Princess Street, Marine Lines, Mumbai -400002

Contact: +91-22- 4359 1200 | E-Mail: [email protected]

UNICON WEALTH

Prominent Demand – Supply Gap

Huge Demand in Gujarat itself

Rising oil prices and pressure / incentives to shift to

Natural Gas

Management Brief

GSPL being the subsidiary of state-owned GSPC, its management is

monitored by Government. Shri D Rajagopalan, IAS, the Chairman holds

Master Degree in Science. He is a senior IAS officer having

administrative and corporate experience spanning 25 years. During his

tenure with the Central Government, he has served as the Import and

Export Secretary with the Commerce and Industry Ministry, Government

of India. Presently he is Additional Chief Secretary, Industry and Mines

Department, Government of Gujarat.

Industry Overview

Growing Indian Economy requires higher energy consumption, and thereby triggers development of Indian Energy Sector, and Gas sector in particular. The Supply-Demand gap for natural gas is becoming prominent in India. In the XI Plan, demand for natural gas in India is estimated to increase 36.07% lifting the mark from 179 million cubic meters per day in 2007-08 to 280 million cubic meters per day in the year 2011-12. Gujarat itself has huge demand potential. With its large industrial base, growing energy needs and proactive government approach, it has emerged as a Vibrant Hub for gas industry. As per CRISIL’s report, natural gas demand in the State is expected to increase from 54.1 mmscmd in 2005 to 94.5 mmscmd by 2010. According to EIA International Energy Outlook Report 2009, Global Natural Gas consumption is estimated to increase @ 1.6% per annum from about 104 trillion cubic feet in 2006 to 153 trillion cubic feet by 2030. The Natural gas transmission industry is primarily being driven by the level of demand for natural gas and other fossil fuels in regions that lack energy resources and assets. Main factor that boosts the demand of Natural Gas is skyrocket rise in spot price of Oil from 2003 to 2008 hitting mark of $147 per barrel during mid July 2008 and its rebound trend from early 2009. Also governments across the world encourage Industrial consumers, especially power industry and fertiliser industry players to make a move towards environment friendly fuels, such as Natural gas which is more efficient, cost effective and environment friendly over other fossil fuels Growth plans for Natural gas sector are being laid by Indian Government. Several gas pipelines are planned for development across the world in coming few years, including cross country pipelines like Iran-Pakistan- India Pipeline, Myanmar India Pipeline, Trans-Afghan Pipeline, Central Asia Gas Pipeline, Nabucco Gas Pipeline, etc. Supply mark of natural gas has taken a hike with the commencement of Reliance KG (D-6) basin natural gas production in March 2009, expansion of capacity of LNG terminals by Petronet LNG, and Hazira LNG being completed, opening doors of volume growth for transmission players. Moreover, focus on Power / fertiliser companies coming on stream in Gujarat would drive the growth for transmission players in the state. Thus with substantial demand estimated for natural gas, future of Gas Transmission Industry players, which play on volume metrics, is supposed to be bright.

6

Gujarat State Petronet Ltd | Initiating Coverage December 21st, 2009

Wealth Research, Unicon Securities Private Limited, 285 – Princess Street, Marine Lines, Mumbai -400002

Contact: +91-22- 4359 1200 | E-Mail: [email protected]

UNICON WEALTH

Investment Rationale

Major beneficiary from Gujarat’s huge demand potential

Gujarat is the largest gas consuming state in India. GSPL, the largest gas

transmission player in Gujarat, stands to benefit from the increasing

demand due to its pre-eminent pipeline connectivity and reach within

Gujarat.

As per CRISIL’s report, natural gas demand in the State is expected to

increase from 54.1 mmscmd in 2005 to more than 100 mmscmd by 2012

and ~ 146 mmscmd by 2020.

Albeit expansion of the gas grid in state, expansion of capacities of

existing projects, setting up of new Industries and development of CGD

networks in Gujarat has resulted in increase in demand but overall trend

of industrial players moving towards natural gas to satisfy their fuel and

feedstock requirements has also played its part.

High supply volumes giving growth opportunity to GSPL:

GSPL being pure gas transmission is not subjected to any commodity

price risk or marketing margins and revenue growth comes only from

increasing transportation volume.

Boost in re-gasification capacity at Dahej, Hazira and commissioning of

the new R-LNG terminal at Dabhol are expected to provide an

opportunity to GSPL to transmit additional R-LNG volumes going ahead.

For instance increase in gas supplies from Reliance KG basin D6 and

Petronet LNG gas transmission volumes are expected to reach 61.8%

CAGR over FY09-FY11E. Impact of this increase will be reflected as

growth from FY09-10 for GSPL.

GSPL looking forward to grab new pipelines by bidding through

SPVs

Under Sec 35AD, capex incurred on pipelines under SPVs can be

charged as deductible expense. This can give the tax benefits to the

company, thereby increasing the cash inflows in the initial phases of the

projects. GSPL is expected to bid for the new pipelines outside Gujarat

through special purpose vehicles (SPV), which can enable it to get the

tax benefits and can improve the bottom line.

Operation & Maintenances Activities

The Company has transported 5428.48 MMSCM (Previous year: 6144.91

MMSCM) of gas during the FY 08-09. The Company will be benefited by

transmission of additional volumes available on account of increase in

supply of natural gas in the State

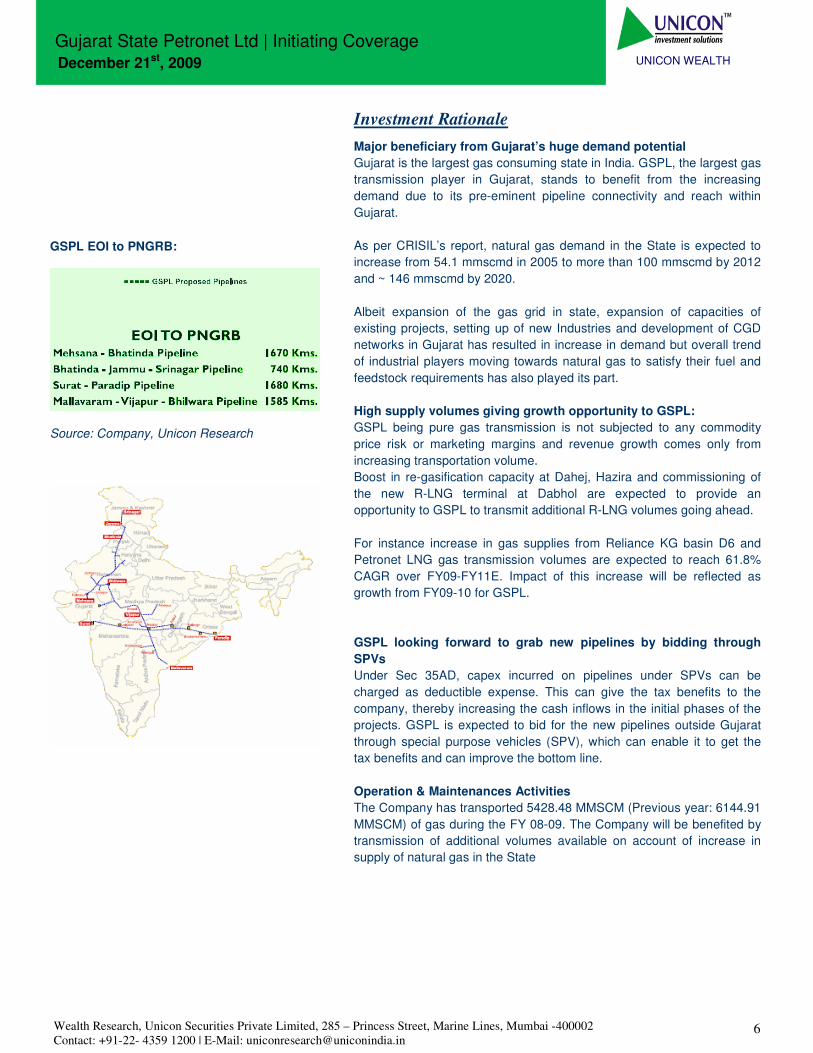

GSPL EOI to PNGRB:

Source: Company, Unicon Research

Every possible care taken to adhere to high and

7

Gujarat State Petronet Ltd | Initiating Coverage December 21st, 2009

Wealth Research, Unicon Securities Private Limited, 285 – Princess Street, Marine Lines, Mumbai -400002

Contact: +91-22- 4359 1200 | E-Mail: [email protected]

UNICON WEALTH

Price Economics of Naphtha:

In the recent past, price of alternative feedstock like Naphtha had fallen

sharply due to a weak demand outlook. These competitive Naphtha

prices led to some customers (with dual-feedstock capabilities) opting for

the alternative feedstock, and thus, the decline in GSPL’s volumes of

spot RLNG in Q3 FY09. Volumes declined to 13.1mmscmd, de-growth of

25.8% YoY.

Unlike impact in Q3FY09 price economics now started tilting towards gas

again Naphtha prices have risen lately, rendering RLNG competitive

enabling the volumes to pick up in Q4 FY09 with a visible improvement

from Q1 FY10.

Growing Demand of Natural gas in India

The macro outlook is favorable given India’s huge appetite for cleaner

fuels like natural gas, which should get a boost from new discoveries by

RIL, ONGC, GSPC and others, going ahead.

Apart from power and fertilizer sector, Growth plans of compressed gas

distribution (CGD) sector in India boosts the growth of Gas transmission

industry. CGD sector in India currently consumes 5-6% of the total

available gas, or 5-6 mmscmd, but the consumption is expected to

quadruple in a few years. Petroleum and Natural Gas Regulatory Board

(PNGRB) is targeting CGD bidding in 200 cities by 2012.

Cities covered in the first phase of CGD were Kakinada (Andhra

Pradesh), Kota (Rajasthan), Sonipat (Haryana), Mathura and Meerut

(Uttar Pradesh), and Dewas (Madhya Pradesh). As of now the CGD work

in progress cities toll has crossed the number 77.

The company recognized the mounting market potential beyond Gujarat.

GSPL has filed EOI with regulator for four new Pipelines to grab more

pipelines in its pocket. A decision is expected in January-February 2010.

Company expects to win Mehsana – Bhatinda pipeline, as the pipeline

originates in Gujarat and GSPL will be maintaining and operating the

feeder pipelines to the main trunk line. Thus stronger growth scenario

outside Gujarat may appear for GSPL before end of FY10E.

Benefits from Take or Pay Agreements:

GSPL typically goes for fixed tariff component (especially in high volume

gas transmission agreements) based on pipeline distance and utilization,

duration of contract, tariff offered by competing pipelines and the

comparative cost of alternate fuels.

This tariff is there on account of the reservation of the network capacity

and typically covers 90% of the customer's tariff commitment. Balance

10% is commodity charges linked to the actual transportation of natural

gas through the gas transmission network. This means that if the second

party fails to meet the commitments for transmission, GSPL can claim

capacity charge from it (generally 90%).

Naphtha getting less attractive is pushing the demand

for natural gas further up

Huge appetite for cleaner fuels in India

Demand from CGD growing in multiples

GSPL bids for Interstate Pipelines:

Pipeline Distance (kms)

Mehsana - Bhatinda 900

Bhatinda - Jammu & Srinagar 300

Mallavaram - Bhilwara - Vijaipur 1585

Surat - Paradip 1600

Source: Company, Unicon Research

Limited downside risk from new tariff regulations

8

Gujarat State Petronet Ltd | Initiating Coverage December 21st, 2009

Wealth Research, Unicon Securities Private Limited, 285 – Princess Street, Marine Lines, Mumbai -400002

Contact: +91-22- 4359 1200 | E-Mail: [email protected]

UNICON WEALTH

Favourable Gas Pipeline Policy for GSPL

Sole Operator Rights Recent Petroleum and Natural Gas Regulatory Board (PNGRB) Regulations have provided pipeline operators exclusivity (from the date of commencement of respective pipeline) for 25 years. GSPL is benefited from early mover's advantage in Gujarat and after undergoing process of authorisation will be the sole operator in its current areas of operation for the next around 20-25 years as most of its assets are not too old. 12% post-tax RoCE With PNGRB allowing 12% post-tax RoCE on gas transportation pipelines. GSPL’s tariffs jumped from around INR 0.7 per scm (FY09) to INR 0.9 per scm (Q1FY10) and INR 0.89 (Q2 FY10). GSPL ROE will increase on account of it being benefited from higher leveraging to fund its expansion plans. Act corresponding to Depreciation leads to Benefits: Schedule VI of The Companies Act, 1956 is in place for the calculation of capital employed. The same is applicable to GSPL. According to current figures stated GSPL currently depreciates its plant & machinery at a rate of 8.33%. This being high implies that GSPL would benefit from higher capital employed and earn higher returns in the initial years of operation. Benefit from Tariff Computation Policy: According to PNGRB Gas Pipeline Policy pipeline tariffs are computed on the basis of lower volumes in the initial four years of operations. The volumes for the first year shall be taken as 60% of the firmed-up contracted capacity, increasing 10% every year to reach 100% in the fifth year for computing the tariffs. This would benefit company in terms of higher returns in the initial years of operation. Benefit from Regulation Return Computation Policy According to PNGRB policy contracted volumes should be used for computing pipeline tariffs/regulated returns. Also, the additional returns from spot volumes will not be used for determination of regulated returns the spot volumes is considered in contracted volumes only after the initial tariff period of five years. This way there is possibility GSPL to generate more than 11% returns after two years.

0

5

10

15

20

25

30

35

40

FY08 FY09 FY10E FY11E FY12E

ROE (%)

ROCE (%)

Source: Company, Unicon Investment Solutions

Higher returns in Initial years of operation

9

Gujarat State Petronet Ltd | Initiating Coverage December 21st, 2009

Wealth Research, Unicon Securities Private Limited, 285 – Princess Street, Marine Lines, Mumbai -400002

Contact: +91-22- 4359 1200 | E-Mail: [email protected]

UNICON WEALTH

Concerns

Regulatory risk:

Board appointed for the determination of transmission tariffs and authorisation of gas transportation pipelines is Petroleum and Natural Gas Regulatory Board (PNGRB). It also dictates technical operating parameters for gas transporting companies. GSPL’s failure to abide by the dictations would lead to heavy fine and it would come under the scanner of the regulator. Competitive prices of substitute products:

In the recent past, price of alternative feedstock like Naphtha had fallen sharply due to a weak demand outlook. These competitive Naphtha prices could have led to some customers (with dual-feedstock capabilities) opting for the alternative feedstock, and thus, the decline in GSPL’s volumes of spot RLNG in Q3 FY09. Although price economics now started tilting towards gas again Naphtha prices have risen lately but any reduction in prices of Naphtha in future would impact the demand of Natural Gas adversely. Social contribution:

In July 2008, Government of Gujarat directed all the profit making state PSUs to contribute 30% of pre-tax profit to newly formed Gujarat Socio-Economic Development Society (GSEDS) for welfare activities. In case of GSPL, on February 2, 2009, shareholders approved the contribution of INR 644 mn for FY09 to GSEDS. However, there have been no eligible projects this year to entail a meaningful contribution out of profits. Any hit on the bottom line this year is escaped but the risk of such contributions from the future earnings will still be there.

Financial Analysis For H1FY10, GSPL generated net revenue of INR 4.7 bn, showing a growth of 95.56% on YoY basis, as a result of increasing gas transportation volumes. During the period under review, the operating profit jumped from INR 2.2 bn in H1FY09 to INR 4.5 bn in H1FY10. Net income jumped even higher INR 1.9 bn for H1FY10 from INR 610 mn in H1FY09, showing the effect of rise in volumes and better capacity utilisation. The transportation charges are not dependent on natural gas prices and company is expected to maintain the EBIDTA margins at ~ 91% going forward. During FY09-12, gas transmission volumes are expected to increase from 15 mmscmd for FY09 to 54 mmscmd for FY12 at a CAGR of 53%. Over FY09-12, revenue is expected to grow at a CAGR of ~50%, operating profit is expected to grow at a CAGR of ~53% and Net Profit is expected to grow at a CAGR of 72%. Going forward we expect the company to continue to maintain the momentum seen over the last two quarters. We expect the company to achieve revenues of INR 15.8 bn and INR 16.6 bn in FY11 and FY12 respectively. The net margins of the company are expected to improve from 25.3% (INR 1.2 bn) in FY09 to 43% (INR 7.1 bn) by FY12.

Regulatory delays can slow the growth plans

-

5,000

10,000

15,000

20,000

FY08 FY09 FY10E FY11E FY12E

Revenue (INR Million)

Source: Company, Unicon Research

85%

86%

87%

88%

89%

90%

91%

92%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

FY08 FY09 FY10E FY11E FY12E

EB

IDT

A M

arg

ins

EB

IDT

A (

INR

Milli

on

)

Source: Company, Unicon Research

0 5 10 15

FY08

FY09

FY10E

FY11E

FY12E

EPS (INR)

Source: Company, Unicon Research

10

Gujarat State Petronet Ltd | Initiating Coverage December 21st, 2009

Wealth Research, Unicon Securities Private Limited, 285 – Princess Street, Marine Lines, Mumbai -400002

Contact: +91-22- 4359 1200 | E-Mail: [email protected]

UNICON WEALTH

One Year forward Earning P/E Graph

0

100

200

300

400

Feb-06 Feb-07 Feb-08 Feb-09

Price 5x 10x 20x 30x 42x

Source: Company, Unicon Investment Solutions

Peer Analysis

Being a pure gas transmission player, GSPL is not comparable to other

companies in natural gas transmission / distribution business. The closest peers

to GSPL are Gujarat Gas Company Ltd (GGCL) and Indraprastha Gas Ltd

(IGL).

GGCL is India’s largest private sector player in the natural gas transmission and

distribution segment and supplies gas to more than 230000 domestic,

commercial, industrial customers and serve over 80000 compressed natural

gas users. IGL is the sole supplier of Compressed Natural Gas (CNG) and

Piped Natural Gas (PNG) in the National Capital Region of Delhi and supplies

CNG to automotive, PNG to domestic and commercial sectors.

At current market price (CMP) of INR 94.2, GSPL is trading at 13.9x its

annualised EPS (INR 6.8) of H1FY10, as compared to 17.1x for GGCL, and

12.4x for IGL. On P/BV basis, GSPL (4.4x) seems to be expensive as

compared to its peers, GGCL (4.3x), GAIL (3.4x), IGL (3.8x) and RIL (2.9x).

As compared to peers, GSPL has more visibility of future revenues as well as

margins, due to mix of long term and short term gas supply agreements, make it

worthy of higher valuations than its peers.

Peer Group Comparison

Company CMP Mkt. Cap EPS (INR) PE(x) P/BV(x) EV/EBIDTA(x) EV/Sales(x) Dividend Yield

INR in Mn FY09 FY10E* FY09 FY10E* (%)

GSPL 94 52972 2.2 6.8 42.8 13.9 4.4 8.1 7.5 0.8

GGCL 228 29100 6.1 13.3 37.1 17.1 4.3 11.8 2.2 0.7

GAIL 400 506160 22.1 21.6 18.1 18.5 3.4 14.0 2.0 1.7

IGL 187 26103 12.3 15.0 15.2 12.4 3.8 8.4 2.9 2.1

RIL 1017 3337124 48.4 45.8 21.0 22.2 2.9 14.1 2.4 0.6

*Annualised figures on stand alone basis

Valuations & Outlook

With more pipelines (450 km) coming on-stream by the end of FY11

and demand for natural gas increasing rapidly in the Gujarat region,

GSPL would experience exponential growth. The company would

improve its Return on Equity to 36.6% in FY11 from the 8.8% in FY09. On

an equity base of INR 12.2 billion, its EPS would jump from INR 2.2 for

FY09 to INR 12.2 and INR 12.6 by FY11E and FY12E respectively.

As per DCF* calculations, the intrinsic value of the stock works out to INR

105, implying an upside of ~ 11.5% from the current level. We have

assumed a discount rate for equity of 16.2%, tax rate of 35% and terminal

growth rate of 3%.

At the current market price, the stock can be Accumulated for 12 months

time horizon.

* Refer Appendix

Sensitivity Analysis

DCF

Discount Rate for Equity

14% 15% 16% 17% 18%

2.0% 127 114 102 93 84

2.5% 130 116 105 95 86

3.0% 134 119 107 96 87

3.5% 138 123 109 98 89

Term

ina

l G

row

th R

ate

4.0% 143 126 112 101 91

Source: Unicon Investment Solutions

11

Gujarat State Petronet Ltd | Initiating Coverage December 21st, 2009

Wealth Research, Unicon Securities Private Limited, 285 – Princess Street, Marine Lines, Mumbai -400002

Contact: +91-22- 4359 1200 | E-Mail: [email protected]

UNICON WEALTH

Company Financials and Ratios (INR in Mn)

Income Statement FY08 FY09 FY10E FY11E FY12E Balance-sheet FY08 FY09 FY10E FY11E FY12E

Net Sales 4179 4875 9936 15840 16601 Net Assets 15,371 17,686 23,407 28,207 30,073

Operating Expenses 534 626 1061 1442 1462 CWIP 5,888 6,446 4,500 4,500 4,500

EBITDA 3645 4249 8875 14398 15139 Investments 356 356 356 356 356

EBITDA Margin (%) 87% 87% 89% 91% 91% C. Assets & Loans & Adv

5,497 5,615 5,522 9,370 11,316

Depreciation 1632 1705 2568 3200 3634 Inventories 397 926 1,000 1,000 450

EBIT 2013 2544 6307 11198 11505 Sundry Debtors 416 544 1,089 1,736 1,819

Interest Expenses 815 870 1013 1080 1215 Cash & Bank Balances

2,569 975 1,240 2,163 1,918

Other Income 294 243 403 460 773 Loans and Advances 1,880 3,018 1,852 3,776 6,019

PBT 1491 1914 5698 10579 11062 Total assets 21,070 23,661 25,339 31,399 36,645

Tax Provision 492 679 1994 3702 3872 Shareholders' Fund 11,410 12,152 14,339 18,399 22,646

PAT 999 1234 3704 6876 7191 Share Capital 5,620 5,621 5,621 5,621 5,621

Reserves 5,789 6,531 8,718 12,778 17,024

Minority Interest 0 0 0 0 0

Total Debt 9,660 11,509 11,000 13,000 14,000

Current Liab. & Provisions

5,106 5,331 7,306 9,889 8,455

Current Liabilities 4,199 3,742 4,745 6,030 4,467

Provisions 907 1,590 2,561 3,860 3,988

Def. Tax Liabilities 1,002 1,144 1,144 1,144 1,144

Total Equities & Liabilities

21,070 23,661 25,339 31,399 36,645

Cash flow Statement FY08 FY09 FY10E FY11E FY12E Key Ratios FY08 FY09 FY10E FY11E FY12E

PBT 1491 1914 5698 10579 11062 Profitability & Return (%)

Add: Depreciation 1632 1705 2568 3200 3634 EBITDA (%) 87% 87% 89% 91% 91%

Interest 815 637 648 658 480 EBIT (%) 48% 52% 63% 71% 69%

Less: Direct Taxes Paid -410 -535 -1994 -3702 -3872 Pre-tax (%) 36% 39% 57% 67% 67%

Change in Working Capital 2449 -1652 1309 -1640 -3753 PAT (%) 24% 25% 37% 43% 43%

Other Miscellaneous -267 -202 -335 -419 -735 Basic EPS 1.8 2.2 6.6 12.2 12.8

CF from Operations 5710 2100 8258 9097 7552 Growth % 10% 22% 199% 86% 5%

(Pur) / Sale of Fixed Assets

-5821 -4579 -6342 -8000 -5500 RoE 8.8 10.2 25.8 37.4 31.8

(Pur.) / Sale of Investments

-356 0 0 0 0 RoCE 8.6 8.9 18.6 25.3 22.9

Other Miscellaneous 256 233 365 422 735

CF from Investments -5921 -4346 -5977 -7578 -4765 Leverage (x)

Change in Net worth 1080 1 0 0 0 Debt / Equity 0.8 0.9 0.8 0.7 0.6

Change in Loan Fund 1022 1849 -509 2000 1000 Interest Coverage 2.5 2.9 6.2 10.4 9.5

Less: Interest Paid -815 -870 -1013 -1080 -1215 Current Ratio 1.1 1.1 0.8 0.9 1.3

Dividend Paid -318 -329 -493 -1517 -2816

Other Miscellaneous 0 0 0 0 0 Valuations (x)

CF from Fin. activities 969 652 -2016 -597 -3031 EV/Sales 14.7 13.0 6.3 4.1 4.0

Net Change in Cash 758 -1595 265 923 -244 EV/EBITDA 16.8 14.9 7.1 4.5 4.3

P/E (Standalone) 52.0 42.8 14.3 7.7 7.4

P/BV 4.5 4.2 3.6 2.8 2.3

(Source: Company, Unicon Investment Solutions)

12

Gujarat State Petronet Ltd | Initiating Coverage December 21st, 2009

Wealth Research, Unicon Securities Private Limited, 285 – Princess Street, Marine Lines, Mumbai -400002

Contact: +91-22- 4359 1200 | E-Mail: [email protected]

UNICON WEALTH

Disclaimer This document has been issued by Unicon Securities Private Limited (“UNICON”) for the information of its customers only. UNICON is governed by the Securities and Exchange

Board of India. This document is not for public distribution and has been furnished to you solely for your information and must not be reproduced or redistributed to any other person.

Persons into whose possession this document may come are required to observe these restrictions. The information and opinions contained herein have been compiled or arrived at

based upon information obtained in good faith from public sources believed to be reliable. Such information has not been independently verified and no guarantee, representation or

warranty, express or implied is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. This document has

been produced independently of any company or companies mentioned herein, and forward looking statements; opinions and expectations contained herein are subject to change

without notice. This document is for information purposes only and is provided on an “as is” basis. Descriptions of any company or companies or their securities mentioned herein

are not intended to be complete and this document is not, and should not be construed as an offer, or solicitation of an offer, to buy or sell or subscribe to any securities or other

financial instruments. We are not soliciting any action based on this document. UNICON, its associate and group companies its directors or employees do not take any responsibility,

financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this document, including but not restricted to, fluctuation

in the prices of the shares and bonds, reduction in the dividend or income, etc. This document is not directed to or intended for display, downloading, printing, reproducing or for

distribution to or use by any person or entity who is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction,

availability or use would be contrary to law or regulation or would subject UNICON or its associates or group companies to any registration or licensing requirement within such

jurisdiction. If this document is inadvertently sent or has reached any individual in such country, the same may be ignored and brought to the attention of the sender. This document

may not be reproduced, distributed or published for any purpose without prior written approval of UNICON. This document is for the general information and does not take into

account the particular investment objectives, financial situation or needs of any individual customer, and it does not constitute a personalised recommendation of any particular

security or investment strategy. Before acting on any advice or recommendation in this document, a customer should consider whether it is suitable given the customer’s particular

circumstances and, if necessary, seek professional advice. Certain transactions, including those involving futures, options, and high yield securities, give rise to substantial risk and

are not suitable for all investors. UNICON, its associates or group companies do not represent or endorse the accuracy or reliability of any of the information or content of the

document and reliance upon it is at your own risk.

UNICON, its associates or group companies, expressly disclaims any and all warranties, express or implied, including without limitation warranties of merchantability and fitness for a

particular purpose with respect to the document and any information in it. UNICON, its associates or group companies, shall not be liable for any direct, indirect, incidental, punitive

or consequential damages of any kind with respect to the document. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any

means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of Unicon Securities Private Limited.

Unicon Investment Ranking Methodology

Rating Buy Accumulate Hold Reduce Sell

Return Range >= 20% 10% to 20% -10% to 10% -10% to -20% <= -20%

Appendix

DCF Discounted cash flow (DCF) is a method of valuing a company using the concept of time value of money. All future cash flows are estimated and discounted to give their present values. The discount rate used is generally a weighted average cost of capital (WACC) that reflects the risk of the cash flows. Cash flows after the projected period are estimated using the Terminal value equation. This equation uses a geometric series to determine the value of a series of growing future cash flows into perpetuity.