guide to business in spain

TRANSCRIPT

2004/CAP 1-a4 28/4/04 17:03 Página 1

2004/CAP 1-a4 28/4/04 17:03 Página 2

This guide was researched and written by Garrigues Abogados y Asesores Tributarios on behalfof the Spanish Institute for Foreign Trade (ICEX) and the General Directorate for Trade and Investment(DGCI).

This guide is correct to the best of our knowledge and belief at the time of going to press. It is, however,written as a general guide so it is recommended thatspecific professional advice be sought before any actionis taken, and therefore no responsibility whatsoever is assumed for the contents, including opinions, contained in this guide or for any actions based on such contents.

Madrid, January, 2004

© Spanish Institute for Foreign Trade (ICEX)

Instituto Español de Comercio Exterior (ICEX)

Paseo de la Castellana, 14-16, 28046 Madrid

Ph: 00 (34) 91 349 61 00

Fax: 00 (34) 91 431 61 28

E-mail: [email protected]

Web: www.icex.es

Creación y realización: Bravo Lofish, S.L.

Imprime:

ISBN: 84-7811-513-7

ISSN: 1137-2907

N.I.P.O.: 381-04-024-0

Depósito Legal:

2004/CAP 1-a4 28/4/04 16:29 Página 1

This publication has been edited with thetechnical advice of the General Directorate forTrade and Investment. The Directorate withinSpain’s Ministry of Economy is in charge ofpromoting foreign investment in Spain.

Acknowledgements:

General Subdirectorate of Regional Incentives

2004/CAP 1-a4 28/4/04 16:29 Página 2

Spain: a profile

The Spanish financial system

Company andcommercial law

Tax system

Investment aidand incentives in Spain

Accounting and auditingrequirements

Labor and social securityregulations

Useful addresses

Practical guidelines

Legal framework and tax implicationsof e-commerce in Spain

2004/CAP 1-a4 28/4/04 16:29 Página 4

S p a i n : a p r o f i l e

7

Spain:a profileI. Introduction 9

II. The country, its people and its institutions 101. Geography, climate

and living conditions 102. Population and

human resources 103. Political institutions 12

III. Spain and the European Union 14

IV. Infrastructure 15

V. Economic overview 17

VI. Domestic market 19

VII. Foreign trade and investment 20

Spain: a profile1

2004/CAP 1-a4 28/4/04 16:29 Página 7

S p a i n : a p r o f i l e

9

Spain is, at the beginning of the twenty-firstcentury, one of the world’s most developedcountries, with a very important role in theinternational political and economic arenas.The country has well proved its capacity toeffectively translate consistent economicgrowth into significant investments, includingcommunication networks comprisingthousands of kilometers of highways, high-speed train services and satellite facilities.This capacity and the constant effort madeto ensure the competitiveness of itseconomic structure have enabled Spain to beplaced among the world’s main economicplayers.

The process of development andenlargement of the EU has led to thedecision of including in May 2004 ten newcountries in the Union, the biggestenlargement ever in terms of scope anddiversity. This enlargement will boosteconomic growth in Spain, thereforeenhancing the opportunities of the Spanishmarket.

The single currency introduced in 2002 intwelve countries of the EU, the Euro Zone,has proved to be a success. The Euro Zoneis a monetary zone comparable to theUnited States and a consolidated, tariff-freemarket of more than 379 million consumers.With the euro, the opportunities of growthand development for Spain have been furtherincreased.

The effective economic performance of Spainis the result of the legislative reformsundertaken and of the heavy investmentsmade by Spanish enterprises to ensurecompetitiveness, develop foreign networksand join multinational projects.

I. Introduction

2004/CAP 1-a4 28/4/04 16:29 Página 9

S p a i n : a p r o f i l e

10

I. Geography, climate andliving conditionsThe Kingdom of Spain occupies an area of506,013 square kilometers in the southwestof Europe, and is the second largest countryin the EU. The territory of Spain coversmost of the Iberian Peninsula, which it shareswith Portugal, and also includes the BalearicIslands in the Mediterranean, the CanaryIslands in the Atlantic Ocean, the NorthAfrican cities of Ceuta and Melilla and somesurrounding rocky islands.

Despite the differences among the variousregions of Spain, the country can be said tohave mainly a typical Mediterranean climate.The weather in the northern coastal region(looking onto the Atlantic and the Bay ofBiscay) is mild and generally rainy throughoutthe year, with temperatures neither very lowin the winter nor very high in the summer.The climate on the Mediterranean coastline,including the Balearic Islands, Ceuta andMelilla, is mild in the winter and hot and dryin the summer. The most extremedifferences occur in the interior of thePeninsula, where the climate is rather dry,with cold winters and hot summers. TheCanary Islands have a climate of their own,with temperatures constantly around 20Celsius degrees and only minor variations intemperature between seasons or betweenday and night.

Spain has an excellent quality of life and isvery open to foreigners. Over four thousandkilometers of beaches, abundant sportingfacilities and events and social opportunitiesare crowned by the diversity of the country’scultural heritage as a crossroads ofcivilizations (Celts, Romans, Visigoths, Arabs,Jews, etc.).

2. Population and humanresourcesThe population of Spain in 2002 was 41.838million people, with a population density ofnearly 83 inhabitants per square kilometer.The last forecast offered by the “InstitutoNacional de Estadística” (National StatisticsInstitute) is the figure for the Spanishpopulation for year 2003, which will increaseto 42.8 million people.

Spain is a markedly urban society (see Table1), as evidenced by the fact that more than34% of the population lives in the capitals ofthe provinces of Spain.

The official national language is Spanish,which is used jointly with other officialregional languages (Catalan, Basque, Galicianand Valencian) in specific AutonomousCommunities. Education is compulsory untilthe age of 16 and English is the main foreignlanguage studied at school.

Compared with other OECD countries,Spain’s population is relatively young:approximately 21% is under 19 years old, 62%

II. The country, its people and its institutions

Table 1

The biggest cities in Spain*

Population

Madrid 3,016,788Barcelona 1,527,190Valencia 761,871Seville 704,114Saragossa 620,419Malaga 535,686Murcia 377,888The Palms of Great Canary 370,649Majorca 358,462Bilbao 353,950

* Figures refer only to the municipal district of each city.Source: Revised registered population in Spanish cities

as of January 1, 2002. Instituto Nacional de Estadística (National Statistics Institute).

2004/CAP 1-a4 28/4/04 16:29 Página 10

S p a i n : a p r o f i l e

11

is between 19 and 65 years old, and only 17%is over 65 according to year 2002 figures.

Spain has a labor force of around 18.9 millionpeople, representing 55.31% of the country’spopulation over 16 years old. The workingpopulation is generally middle-aged.Additionally, as seen in Table 2 below, Spainis also experiencing in recent years a relevantinflow of immigrants which is beginning tooffset the consequences of an agingpopulation.

The structure of the labor force byeconomic sector has also changedsignificantly in recent years, with a notableincrease in the number of those employed inthe services sector and a decrease in thenumber of farmworkers (see Table 3 andChart 1).

Table 2

Foreigners resident in Spain by continent of origin

1999 2000 2001 2002 2003*

Europe 353,556 361,437 414,555 473,514 506,745America 166,709 199,964 298,798 380,305 432,428Asia 66,340 71,015 89,519 101,621 110,968Africa 213,012 261,385 304,149 366,518 397,516Oceania 1,013 902 944 1,024 1,014Unknown 699 1,017 1,095 1,019 0Total 801,329 895,720 1,109,060 1,324,001 1,448,671

*January-June. Figures released by the “Ministerio del Interior” (Home Office).Source: Instituto Nacional de Estadística (National Statistics Institute).

Chart 1

Labor force structure by economicsector in 2003

Source: Instituto Nacional de Estadística (National Statistics Institute).

5%

19%

12%

64%

Agriculture Construction

Industry Services

2004/CAP 1-a4 28/4/04 16:29 Página 11

S p a i n : a p r o f i l e

12

The labor force is very qualified, productiveand capable of adapting to technologicalchanges, productivity growth being as aconsequence among the highest in Europe.

Lastly, in line with the existing commitmentwithin the European Union to fosteremployment, since the mid-nineties theGovernment implemented wide-rangingreforms of the labor market regulations,introducing a high degree of flexibility in theuse of the labor force by companies. Thesuccess of the reforms undertaken isattested by the fact that from 1996 to 2003,Spain has generated one third of theemployment in the Euro Zone.

3. Political institutionsSpain is a parliamentary monarchy. The Kingis the Head of State; and his primary missionis to arbitrate and moderate the regularfunctioning of the country’s institutions inaccordance with the Constitution. He alsoformally ratifies the appointment ordesignation of the highest holders of publicoffice in the legislative, executive and judicialbranches.

The Constitution of 1978 enshrined thefundamental civil rights and public freedomsand assigned legislative power to the “CortesGenerales” (Parliament), executive power to

the Government of the nation, and judicialpowers to independent judges andmagistrates.

The responsibility for enacting laws isentrusted to the “Cortes Generales”,comprising the “Congreso de los Diputados”(Lower House of Parliament) and the“Senado” (Senate), the members of whichare elected by universal suffrage every fouryears.

The “Cortes Generales” exercise thelegislative power of the nation, approve theannual State budgets, control the actions ofthe Government and ratify internationaltreaties.

The Government is headed by the“Presidente del Gobierno” (President of theGovernment) who is elected by the “CortesGenerales” and is, in turn, in charge ofelecting the members of the “Consejo deMinistros” (Council of Ministers).

The members of the Council of Ministers areappointed and removed by the President ofthe Goverment at his or her discretion.

For administrative purposes, Spain isorganised into 17 Autonomous Communities(Regions) each containing generally one ormore provinces, plus the Autonomous Citiesof Ceuta and Melilla in Northern Africa; thetotal number of provinces is 50.

Table 3

Evolution of labor force structure by economic sector(Percentages)

1985 1990 1995 2000 2001 2002 2003

Agriculture 18.2 11.8 9.3 6.6 6.2 5.5 5.4Industry 24.5 23.8 20.1 19.8 19.7 19.6 18.7Construction 7.3 9.7 10.4 11.1 11.5 11.7 11.8Services 50.0 54.7 60.2 62.5 62.6 63.2 64.1

Source: Instituto Nacional de Estadística (National Statistics Institute), Labor Force Survey, 2003.

2004/CAP 1-a4 28/4/04 16:29 Página 12

S p a i n : a p r o f i l e

13

Each Autonomous Community (Region)exercises the powers assigned to it by theConstitution as specified in its “Statute ofAutonomy”. These Statutes also stipulate theinstitutional organization of the Communityconcerned, consisting generally of: alegislative assembly elected by universalsuffrage, which enacts legislation applicable inthe Community; a Government withexecutive and administrative functions,headed by a President elected by theAssembly, who is the Community’s supremerepresentative; and a Superior Court ofJustice, in which judicial power in theCommunity’s territory is vested. A Delegateappointed by the Central Governmentdirects the Administration of the State in theAutonomous Community (Region), and co-ordinates it with the Community’sadministration.

The Autonomous Communities (Regions)are financially autonomous and also receiveallocations from the general State budgets.

As a result of the structure above describedSpain has become one of the mostdecentralized countries in Europe.

2004/CAP 1-a4 28/4/04 16:29 Página 13

S p a i n : a p r o f i l e

14

Spain became a full member of the EuropeanEconomic Community in 1986. Therefore, EUlegislation is fully applicable in Spain. In thisconnection and according to figures publishedby the European Commission, Spain fullycomplies with the objectives established bythe European Council and has implemented2,364 Directives into national law.

A major impact of European Unionmembership for Spain, and for the otherMember States, came in the mid-nineties withthe advent of the European Single Market andthe European Economic Area, which createda genuine barrier-free trading space. Sincethen, the EU has advanced significantly in theprocess of unification by strengthening thepolitical and social ties among its citizens.Spain, throughout all this process, has alwaysstood out as one of the leaders in theimplementation of liberalization measures.

Spain has a strong responsibility in the EU,evidenced by the fact that it is the fifth countryin terms of voting power in the Council ofMinisters. During 2002, it held its thirdPresidency of the Council of the EuropeanUnion with the overall intention of culminatingthe integration process and the historicalchanges which began over a decade ago.

This process has reached one of its mostimportant milestones, as the draft Treatyestablishing a Constitution for Europe is beingdiscussed within the European Commission.The Constitution will incorporate the mainreforms to improve the decision-makingprocess within the Union, to strengthen itsmeans of action and to provide its citizenswith a Charter of Fundamental Rights.

The introduction of the euro (January 1st,2002) in twelve countries marked thebeginning of the third Spanish Presidency,representing the culmination of a lengthyprocess and a whole deal of growth

opportunities for the Spanish and Europeanmarkets.

With the euro in the European Union, amonetary zone has been established to formthe world’s number one trading power,triggering the integration of the financialmarkets and economic policies of theMember States adopting it. Such changes havealso fostered the coordination of the taxsystems of the Euro Zone Member States,thus further increasing the stability of the EU.

The euro has yielded clear results at theinternational level, promoting the visibility ofthe Euro Zone both in international andfinancial fora (the G-7 group meetings) andin multilateral organizations. The economicand commercial stability provided by theeuro has further bolstered Spain’s currenteconomic growth along with additionalinternational political presence.

The European Union approved the joining of10 new countries for May 1, 2004 (Cyprus,the Czech Republic, Estonia, Hungary, Latvia,Lithuania, Malta, Poland, the Slovak Republicand Slovenia). Such enlargement of the EUposes a unique challenge since it is withoutprecedent in terms of scope and diversity: anextension of land area of 23% and apopulation increase of 75 million people.

Spain is the EU Member State that in the lastyears has received the most EU structuraland cohesion funds —used to financeinfrastructure and development projects. Infact, Spain is expected to receive in totalaround 45 billion euros in various EUstructural funds in the 2000-2006 period andover 11 billion euros in cohesion funds (62%of the total budget agreed by the EuropeanCouncil of Berlin). With these funds, theGovernment has undertaken actions in thisarea, with the cooperation of privateinitiatives financing infrastructures.

III. Spain and the European Union

2004/CAP 1-a4 28/4/04 16:29 Página 14

S p a i n : a p r o f i l e

15

Over the last decade Spain has undergone aprocess of modernization that has includedan extensive renewal of its infrastructure.

The Government plans to continue investingheavily in the future. This is reflected in theOverall Infrastructure Plan for 2000-2010,which provided for investment totalling over102 billion euros. Intercity transport is themain item in the Infrastructure Plan, followedby urban transport. There will also beaccompanying measures in hydraulic worksand environmental infrastructure.

The motorway network, totalling nearly11,000 km, has more than tripled in lengthsince 1982 and has undergone continuousrenovation to enhance efficiency andconvenience. The Government investmentplan will result in over 13,000 km ofmotorway network by year 2010, with totalinvestment expected to surpass 25 billioneuros between 2000 and 2006, thusbecoming one of the most modern networksin the world.

As far as rail transport is concerned, Spainhas a network of over 15,000 km of track,and in 1992 introduced a 471-km high-speedtrain line from Madrid to Seville. High-speedtrain lines have become a priority for theGovernment infrastructure plans (theforeseen network of high-speed trains willtotal 7,200 km), and as a consequence ofthem, by December 2004, Madrid will beconnected by high-speed train to the Frenchborder via Zaragoza (Aragón) and Barcelona(Catalonia) and additionally via Vitoria andIrún (Basque Country). In fact, the sectionMadrid-Guadalajara-Zaragoza-Lérida openedin October 2003. Furthermore, Madrid willbe soon connected to the Mediterraneancoast via Malaga and, by 2005, via Valencia. Inconnection with the Northern route(Madrid-Valladolid-La Coruña), completion of

works for the Madrid-Segovia-Valladolidsection is expected for 2007. Additionally, anagreement has been entered into betweenSpain and Portugal; Madrid and Lisbon will beconnected in less than 3 hours by 2010. Theinvestment forecast for railroads totalsalmost 40.9 billion euros between 2000 and2007.

There are air transport services between themain cities. The approximately 250 airlineswith scheduled flights operating out of thecountry’s 33 international airports ensurecomplete service abroad. Spain is animportant intermediate stop in the linesbetween Latin America and Europe and liesin a crucial position in the network toAmerica and Africa from Europe. Spain alsohas excellent sea communications, with 53international ports on the Atlantic andMediterranean coasts.

Spain is also well equipped with industrialland and technological and industrialinfrastructure. In the last few years,technology parks have proliferated in themain industrial areas and near universitiesand R&D centers. There are currently 41technology parks (12 fully operational, 29 ina development stage). In these technologyparks there are 1,080 companies, 108 R&Dcenters and 12 incubators operating. R&Dexpenditure has risen significantly in recentyears. The new national R&D Plan (2004-2007) forecasts to achieve the objective of aR&D expenditure amounting to 1.4% of GDPby 2007.

Lastly, Spain has a good telecommunicationsnetwork. In addition to the extensive fiberoptic network which covers almost all theterritory, Spain manages one of the largestinternational undersea cable networks andhas satellite connections with the fivecontinents. In this respect, it is worthwhile

IV. Infrastructure

2004/CAP 1-a4 28/4/04 16:29 Página 15

S p a i n : a p r o f i l e

16

mentioning the strong liberalization processundertaken in most industries, including thetelecommunications sector, well within theEuropean schedule. Among other benefits,this implies a more competitive and costeffective offering of this type of services,essential for an appropriate economicdevelopment.

2004/CAP 1-a4 28/4/04 16:29 Página 16

S p a i n : a p r o f i l e

17

Spain’s GDP increased by 2.0% in 2002totalling around US$ 583 billions making itthe eighth largest in the OECD. Growth ofthe GDP for 2003 is estimated to reach2.3%.

The structure of the Spanish economy is thatof an industrialized country, with the servicessector being the main contributor to GDP,followed by industry. These two sectorsrepresent almost 90% of Spain’s GDP withagriculture’s share today representing less

than 4% of GDP, and declining sharply as aresult of the country’s intense economicgrowth (see Table 4).

Spain is a fairly dynamic country, and hasconsistently achieved high economic growthrates, clearly above the average for otherindustrialized countries. The growth in Spaincontinues to be much greater than theaggregate growth of the EU (see Chart 2).

V. Economic overview

4.5

4

3.5

3

2.5

2

1.5

1

0.5

01999 2000 2001 2002 2003*

* January-June.Source: Banco de España (Bank of Spain).

Table 4

Structure of GDP(% of total, in 1995 constant pesetas)

Sector 1998 1999 2000 2001 2002 2003*

Agriculture and fishery 4.7 4.3 4.5 4.3 4.05 3.79Industry 30.2 29.6 24.1 23.1 22.93 23.71Construction 7.0 7.1 8.1 8.5 8.71 8.16Services 58.1 59.0 63.3 64.1 64.31 64.34

* January-March.Source: Instituto Nacional de Estadística (National Statistics Institute).

Chart 2

GDP growth(% growth rate)

Spain

EU

4.2

2.8

4.2

3.42.7

1.5

2.0

1.0

2.3

1.2

2004/CAP 1-a4 28/4/04 16:29 Página 17

S p a i n : a p r o f i l e

18

The prospects, taking into account that theworld economic situation is beginning torecover, are that Spain will have growth ratesof 3% in 2004, once again exceeding theaverage for the EU (see Table 5). In fact, theSpanish economy is accomplishing theprojections given last year by the OECD,which it already foresaw a recovery for 2003and achievement of real GDP growth ratesover 3% in 2004.

Inflation in Spain has fallen steadily since thelate 1980’s. The average inflation rate for 1987through 1992 was 5.8%. The rate of inflationwas kept under 5% for the first time in 1993,and has been further reduced in subsequentyears. Year 2003 will end with an annual rate

of inflation of 2.6%, clearly improving lastyear’s figure, which amounted to 4%.

Also, in 1999 Spain engaged in an earnesteffort to reduce the budget deficit, includinga successful program of major privatizationsand of contention of public expenditure. Theactions taken by the Government have onceagain proved the flexibility of the Spanisheconomy and according to OECDprojections, a deficit of close to 0.5% of GDPis likely to be recorded in 2003, implying aneutral fiscal stance.

Very noteworthy is the impressive reductionin the official interest rates in Spain from10% in 1993 to the current 2.0%.

Table 5

Growth and inflation forecasts for OECD countries(Percentages)

Real GDP Growth Inflation

2003 2004 2003 2004

EU countriesAustria 1.1 2.0 1.4 1.1Belgium 1.3 2.3 1.7 1.2Denmark 1.6 2.6 2.3 2.3Finland 2.2 3.4 2.3 1.5France 1.2 2.6 1.4 1.4Germany 0.3 1.7 0.8 0.4Greece 3.6 3.9 3.3 3.4Ireland 3.2 4.2 4.2 3.2Italy 1.0 2.4 2.4 1.9Luxembourg 0.3 2.7 2.2 1.4Netherlands 0.7 1.9 2.3 1.3Portugal 0.3 2.3 3.1 2.2Spain 2.1 3.1 2.9 2.4Sweden 1.5 2.8 2.3 1.7United Kingdom 2.1 2.6 0.9 1.0Other countriesUnited States 2.5 4.0 2.0 1.2Japan 1.0 1.1 -1.6 -1.6Total EU 1.2 2.4 1.6 1.4Total Euro Zone 1.0 2.4 1.7 1.4Total OECD 1.9 3.0 2.0 1.3

Source: OECD Economic Outlook (projections). June 2003.

2004/CAP 1-a4 28/4/04 16:29 Página 18

S p a i n : a p r o f i l e

19

The growth of the Spanish economy inrecent years has been driven by a strongdemand and a substantial expansion ofproduction in the context of an increasinglyopen economy.

Today Spain has a domestic market of almost42 million people with a per capita income ofmore than 20,000 US$1 and an additionalinjection of demand coming from the 51.7million tourists who visit the country everyyear. The close links (economic, cultural,political) with Latin America and NorthAfrica and the obvious advantages of usingSpain as a gateway to those countries areworthy of mention.

Table 6 reflects the evolution of basicproduction and demand components since1999. Recent indicators show a sustainedrecovery of industrial production. The

general recovery trend shown by allcomponents is also worthy of mention. Ingeneral, the potential for growth is still veryhigh in many industrial sectors due to therelatively lower level of per capitaconsumption as compared to otherEuropean countries. This is the case, forinstance, in the telecommunications and,among others, environmental equipmentindustries.

VI. Domestic market

Table 6

Growth of production and demand components(Percentages)

1999 2000 2001 2002 2003*

Production components

Agriculture and fishery -3.1 1.5 -3.1 1.0 -0.2Industry 3.0 4.0 1.2 0.7 1.9Energy ** ** 2.8 0.3 2.1Construction 8.7 6.3 5.4 4.8 3.8Services 4.0 3.9 3.2 2.2 2.0

Demand components

Private consumption 4.7 4.0 2.5 2.6 3.1Public consumption 2.9 4.0 3.1 4.4 3.8Gross fixed capital formation 8.9 5.7 3.2 1.0 3.2Domestic demand 5.5 4.3 2.8 2.6 3.4Exports of goods and services 6.6 9.6 3.4 0 5.0Imports of goods and services 11.9 9.8 3.5 -0.6 8.2

* January-September. ** For these years, Industry and Energy were added under the Industry heading.Source: Instituto Nacional de Estadística (National Statistics Institute).

1 Figure based on current purchasing power parities.

2004/CAP 1-a4 28/4/04 16:29 Página 19

S p a i n : a p r o f i l e

20

In recent years, Spain’s exports and importshave grown rapidly, as has incoming foreigninvestment. As can be seen in Table 7, thebasic features of the country’s balance ofpayments today include a trade deficit whichis being completely financed by the surplus inthe services account (driven by tourism) and

in the capital and financial accounts.However, it should be noted that despite thestrong volume of foreign direct investmentthat Spain receives, Spanish direct investmentabroad is since 1997 larger than foreigndirect investment in Spain.

VII. Foreign trade and investment

Table 7

Spain’s balance of payments(Millions of euros)

2000 2001 2002 2003*

I. Current account -18,959 -18,346 -16,627 -9,600

Trade Balance -35,643 -36,396 -34,712 -16,292Services Balance 24,216 27,131 26,128 11,680Income -9,055 -10,878 -10,466 -6,192Net Current Transfers 1,523 1,798 2,424 1,205

II. Capital Account 5,217 5,556 7,498 4,035

III. Financial Account 21,509 20,072 16,179 8,604

Total (excluding Bank of Spain) 27,652 2,597 12,618 12,910Direct investment 18,561 -5,686 2,909 6,333Portfolio investment -2,919 -19,813 6,510 -17,004Other investment 46,961 28,498 7,912 26,380Financial derivatives 2,172 -401 -4,712 -2,800Bank of Spain -6,143 17,475 3,561 -4,305Reserves 3,302 1,581 -3,630 4,552Claims with the Eurosystem -9,250 16,122 6,506 -4,116Other net assets -195 -228 685 -4,742

IV. Net errors & omissions -7,768 -7,293 -7,050 -3,039

*January-June.N.B.: A positive sign in the current and capital accounts means a surplus (receipts greater than payments) and represents a net loan from Spain tothe rest of the world (increase in assets or decrease in liabilities), whereas in the financial account a positive sign means a net inflow of capital andrepresents a net loan from the rest of the world to Spain. A negative sign in reserves means an increase.Source: Banco de España (Bank of Spain).

The main products traded by Spain in 2003are shown in Table 8. The sophistication ofthe main products exported clearly showsthe degree of technology and capability ofSpanish economy.

2004/CAP 1-a4 28/4/04 16:29 Página 20

S p a i n : a p r o f i l e

21

Spain’s main trading partners are EUcountries, with 72% of total exports and 64%of total imports. Latin American countriesrepresent 6% of Spanish exports and 5% ofimports, the U.S. accounts for 5% of exportsand 5% of imports and Japan accounts for 1%of exports and 3% of imports.

Perhaps the most striking feature of theSpanish balance of payments is the net inflowof foreign investment, consistently receivedby Spain since 1996, with the exception of2001 and 2002, due to the internationalcrisis (see Chart 3).

Table 8

Distribution of exports and imports 2003*(Percentages)

Exports Imports

Transport vehicles 23.8 Transport vehicles 16.5Boilers, machinery and equipment 8.3 Nuclear reactors, boilers 11.9Electronic machinery 6.7 Fuels and mineral oils 10.5Plastics and plastic products 3.4 Electronic machinery 8.3Fuels and mineral oils 3.1 Cast iron and steel 3.5Fresh fruits 3.0 Plastics and plastic products 3.3Pharmaceutical products 2.5 Pharmaceutical products 3.3Fresh vegetables 2.3 Organic chemical products 3.0Cast iron and steel 2.3 Optical machinery 2.4Organic chemical products 2.1 Fishery products 2.2Cast iron and steel products 1.9 Wood and cardboard products 1.8Wood and cardboard products 1.7 Clothing products 1.7

* January-October.Source: Ministry of Economy.

Chart 3

Foreign investment in Spain (1999-2003)(Billions of euros)

120

100

80

60

40

20

01999 2000 2001 2002 2003*

■ Direct ■ Portfolio ■ Total* January-August.Source: Banco de España (Bank of Spain).

14.79

42.69

57.48

40.73

63.64

104.37

31.3030.47

61.77

22.52

37.04

59.56

11.2714.21

25.48

2004/CAP 1-a4 28/4/04 16:29 Página 21

S p a i n : a p r o f i l e

22

According to the Annual World InvestmentReport released by the United NationsConference on Trade and Development,global foreign direct investment declinedsharply in 2001 (59% in developedcountries). Spain did not escape thisinternational trend, but it is one of the EUcountries with lowest decreases.

Foreign direct investment is mainly routed toservices (77.5% between 1997 and 2000) andindustry (22.5%). The industrial sectors thatreceived most investment were, amongothers, the chemicals, pharmaceutical,automobile, food and beverage andelectronic subsectors.

However, other sectors such as electronics,aeronautics, environment, healthcare andleisure offer attractive investmentopportunities for foreign investors.

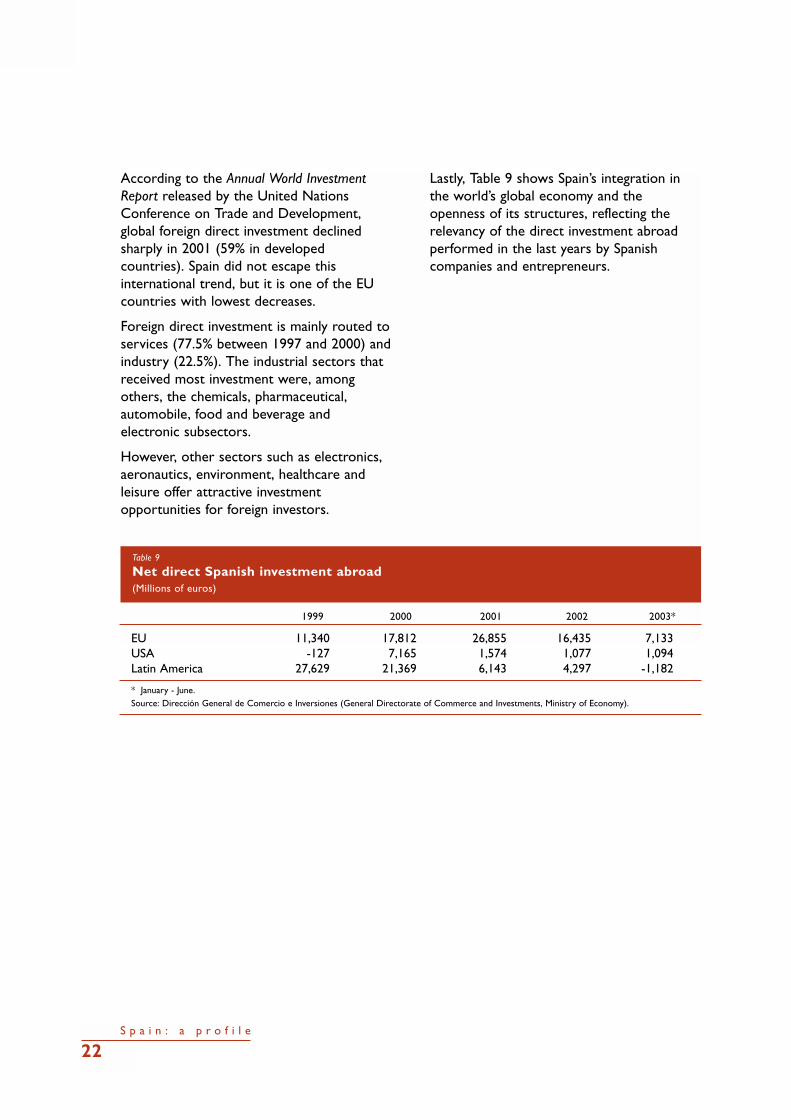

Lastly, Table 9 shows Spain’s integration inthe world’s global economy and theopenness of its structures, reflecting therelevancy of the direct investment abroadperformed in the last years by Spanishcompanies and entrepreneurs.

Table 9

Net direct Spanish investment abroad(Millions of euros)

1999 2000 2001 2002 2003*

EU 11,340 17,812 26,855 16,435 7,133USA -127 7,165 1,574 1,077 1,094Latin America 27,629 21,369 6,143 4,297 -1,182

* January - June.Source: Dirección General de Comercio e Inversiones (General Directorate of Commerce and Investments, Ministry of Economy).

2004/CAP 1-a4 28/4/04 16:29 Página 22

T h e S p a n i s h f i n a n c i a l s y s t e m

25

financialSpanish

system

The

I. Introduction 27II. Financial institutions 28

1. Credit institutions 282. Collective investment

entities 303. Credit market 324. Stock market 32

a) Equity market 34b) Options and futures

market 37c) Fixed-income market 37d) New Market 39

5. Money market 406. Credit finance

establishments 427. Venture capital

institutions 428. Asset securitization 439. Mutual guarantee

societies 4310. Pension plans and

insurance companies 44

III. Law 44/2002 on financialsystem reform measures 46

IV. Taxation of financial products 48

The Spanish financial system

2

2004/CAP 2-a4 28/4/04 16:27 Página 25

T h e S p a n i s h f i n a n c i a l s y s t e m

27

From the institutional standpoint, a financialsystem can be defined as the group ofentities which generates, gathers, administersand manages saving and investment in apolitical and economic system.

Spain has a diversified modern financialsystem, which is fully integrated withinternational financial markets.

The system comprises credit, stock andmoney markets, and specific markets forderivatives (options and futures based ondifferent assets, e.g. a share index called Ibex 35).

I. Introduction

2004/CAP 2-a4 28/4/04 16:27 Página 27

T h e S p a n i s h f i n a n c i a l s y s t e m

28

The operators in the Spanish financial systemcan be classified as follows:

• The central bank: Bank of Spain

• Credit institutions:

– Spanish and foreign banks

– Savings banks

– Credit cooperatives - Rural savings banks

• Other credit entities:

– Credit Financial Establishments(introduced by Law 3/94, implementingthe Second EC Directive on bankingcoordination). These are credit entitiesspecialized in certain asset products –e.g., leasing, financing, mortgage loans,etc.– which cannot take public deposits.

– Instituto de Crédito Oficial, ICO (acts asthe State’s finance agency and investmentbank).

• Investment institutions:

– Collective investment entities:

- Investment companies dealing in:

Marketable securities

Property assets

- Investment funds:

Marketable securities

Property assets

- Money market assets:

Mortgage securities

Pension plans and funds

Other

– Venture capital funds and companies

– Other investment entities

• Brokers:

– Stock market:

- Stockbroker companies and agencies

– General:

- Banks

- Security management and depositcompanies

• Insurance and reinsurance companiesand insurance brokers

1. Credit institutionsBanks and savings banks are of particularimportance in the financial sector in Spain,because of the volume of their business andbecause they are active in all segments of theeconomy.

In Spain, since the European System ofCentral Banks (ESCB) and the EuropeanCentral Bank were set up, the functions ofthe Bank of Spain have been redefined. Theynow consist of participating in the followingbasic functions attributed to the ESCB:

– Defining and implementing the Euro Zone’smonetary policy, with the aim ofmaintaining price stability within it.

– Conducting currency exchange operationsand holding and managing the SpanishState’s official foreign exchange reserves.

– Promoting the sound working of paymentsystems in the Euro Zone.

– Issuing legal tender banknotes.

Also, pursuant to its Law of Autonomy, theBank of Spain will have the followingfunctions:

– Supervising the solvency and behavior ofcredit institutions and financial markets.

II. Financial institutions

2004/CAP 2-a4 28/4/04 16:27 Página 28

T h e S p a n i s h f i n a n c i a l s y s t e m

29

– Promoting the sound working and stabilityof the financial system and of Spain’spayment systems.

– Preparing and publishing statistics relatingto its functions.

– Providing treasury services and acting as afinancial agent for government debt.

– Advising the Government and preparingthe appropriate reports and studies.

The banks operating in Spain are financialinstitutions authorized as such which engagein intermediation transactions using fundsobtained from customers and provide otherservices of a financial nature.

At November 21, 2003 there were 80officially registered Spanish banks, manysubsidiaries, branches, representative officesand correspondents abroad.1 Some 58foreign banks also have offices in Spain. Of these foreign banks, 49 have theirheadquarters in another EU Member State.

Savings banks are credit institutions with thesame freedoms as and full operationalequality with the other members of theSpanish financial system. They have the legalform of private foundations and acommunity-welfare purpose and operate inthe open market, although they reinvest aconsiderable portion of the earningsobtained by them in community welfarework.

These long-standing institutions with deeproots in Spain attract a substantial portion ofprivate savings and their lending businesscharacteristically focuses on the privatesector (through mortgage loans, etc.). Theyare also very active in financing major publicworks and private-sector projects by

subscribing and purchasing fixed-incomesecurities.

The Spanish savings banks are members ofthe Spanish Confederation of Savings Banks(Confederación Española de Cajas deAhorro-CECA), a credit institution formedin 1928 to act as the national association andfinancial institution of the Spanish savingsbanks and which today groups together 47confederated savings banks.

In recent years, savings banks and certainother banks have been involved in a majorprocess aimed at optimizing their positionvis-à-vis the EU single market for bankingservices. As part of this, a process ofintegration took place involving the largestSpanish banks and the creation of twobanking groups (SCH and BBVA) on aEuropean scale and with a major presence inLatin America.

The network of branches in the bankingindustry enjoyed very moderate andconstant growth until 1999. However, sincethen banks have begun to reduce the numberof branches and increase the number ofpersonnel per branch in order to offer amore personalized service and a wider rangeof high value-added financial services,meaning the redeployment of personnel fromheadquarters to the commercial network.Savings banks, on the other hand, opened507 more branches in 2002, representing agrowth of 2.6%.

A noteworthy development in the regulatoryarea is Law 26/2003 amending the SecuritiesMarket Law and the Corporations Law witha view to reinforcing the transparency oflisted corporations.

1 Bank of Spain.

2004/CAP 2-a4 28/4/04 16:27 Página 29

T h e S p a n i s h f i n a n c i a l s y s t e m

30

Under this Law, savings banks that issuesecurities admitted to trading on officialsecurities markets must annually publish acorporate governance report, which must befiled with the Spanish National SecuritiesMarket Commission (CNMV) and mustaddress, among other aspects:

– The entity’s management structure withexhaustive information on thecompensation of the managing bodies.

– Transactions with members of the boardand oversight committee of the savingsbank and with political groups.

– Compensation received by directors andexecutives for services to the savings bank.

– Structure of the business and of therelationships within its economic group.

– Risk control systems.

2. Collective investmententitiesProspective investors planning investments atany term on the Spanish money or stockmarkets can call on the expert services ofnumerous investment and brokerage entitiesthat ensure ease and flexibility in makingtheir investments, offering risk profilessuitable for each investor’s requirements.

The regulations governing investment entitieslay down complete and stringentrequirements for financial reporting in thisfield, and also introduce a favourable taxregime permitting the elimination ofadditional tax costs that may occur oninvesting through these institutions.

In general, Spanish collective investmentinstitutions are of two types:

– Financial: Their main activity is the investmentin or management of marketable securities.

They include securities investmentcompanies and securities mutual funds,money market mutual funds and otherinstitutions whose purpose is to invest inor manage financial assets.

– Nonfinancial: Their main activity is theexploitation of real estate assets.

They include real estate investmentcompanies and trusts.

These tax relief measures have led to anotable increase in the number of theseinstitutions and in the volume of theirinvestments (see Table 1). The soundnessof the markets in Spain and of theparticipating entities is evidenced by the8.309.839 shareholders and investmentinstitution participants in Spain at October31, 20032.

Table 1

Growth of investment institutions

Investment Volume Institutions(million euros)

1990 9,030 5501991 25,510 6621992 39,831 7321993 64,365 8221994 69,996 9291995 75,791 1,0241996 115,642 1,2581997 167,267 1,8401998 211,903 2,4771999 219,453 3,2612000 201,507 4,1372001 204,458 4,8732002 199,272 5,1052003* 226,229 5,719

* October.Sources: Inverco and CNMV.

2 Spanish National Securities Market Commission (CNMV).

2004/CAP 2-a4 28/4/04 16:27 Página 30

T h e S p a n i s h f i n a n c i a l s y s t e m

31

However, it is notable that although the netassets of mutual funds declined in 2002, thistrend was gradually reversed by constantgrowth throughout 2003.

Charts 1 and 2 below show the variations inthe aforementioned figures.

7,000

6,000

5,000

4,000

3,000

2,000

1,000

01994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Source: Spanish Stock Market.

Chart 1

Number of Investment Institutions

250,000

200,000

150,000

100,000

50,000

01994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Source: Spanish Stock Market.

Chart 2

Negotiation volume

2004/CAP 2-a4 28/4/04 16:27 Página 31

T h e S p a n i s h f i n a n c i a l s y s t e m

32

On November 5, 2003, the new CollectiveInvestment Institutions Law (Law 35/2003)was published. The purpose of this Law is toregulate business in the collective investmentindustry through the adoption of three basicprinciples:

a) The deregulation of investment policy.

b)The protection of investors through newinstruments.

c) The perfection of the administrativecontrol system.

Among the new developments, it is worthhighlighting that the types of collectiveinvestment institutions have been narroweddown to two (companies and mutual funds),the management and marketing powers ofthe managers of collective investmentinstitutions have been expanded, andregulations have been introduced for theEuropean passport. Likewise, the legalregulation of the procedure enables unit-holders to transfer their investments fromone collective investment institution toanother at no tax cost.

3. Credit marketAs noted earlier, the Spanish credit market isstructured around banks, which attract mostsavings and use their funds to providefinancing for the private sector.

The banks also operate as investors andunderwriters in the stock market, and adjusttheir liquidity by interbank and moneymarket transactions.

The parallel growth in deposits from andlending to the private sector indicates thelack of any serious problems in obtainingbusiness financing.

The liberalization of capital movements inthe EU has also made it easier for Spanishcompanies to obtain financing from abroad.

The regulation of non-mortgagesecuritization procedures should also bementioned. These will contribute tofurthering the generation of additionalresources by credit institutions, enablingthem to grant new credit facilities.

4. Stock marketThe Spanish stock market consists of thefixed-income and equity markets and theregulated options and futures market.

The issuers are mainly Spanish privatecompanies and banks. However, the sharesof some foreign companies are also listed onthe Spanish stock exchanges. Certain non-resident entities may also issue bondsdenominated in euros in the Spanish market(“matador” bonds), subject to certainconditions.

Market regulation has established a marketbased on the British/US model, aimed atprotecting small investors and the marketitself. A single computerized and centralizedcontinuous stock market (“mercadocontinuo”) exists, on which “insider trading”is penalized. The obligatory involvement ofpublic authenticating officers in stock markettransactions was abolished, and a publicagency (the “Comisión Nacional del Mercadode Valores” –CNMV– National SecuritiesMarket Commission) regulates the systemand supervises its satisfactory operation.

The CNMV is the agency entrusted withsupervising and inspecting the Spanish stockmarkets and the activities of all entitiesoperating in them.

2004/CAP 2-a4 28/4/04 16:27 Página 32

T h e S p a n i s h f i n a n c i a l s y s t e m

33

The CNMV’s objectives include:

– Overseeing the transparency of the Spanishstock markets and proper price formation.

– Overseeing investor protection.

The CNMV’s action impinges on thecompanies which issue securities for publicofferings, the secondary securities marketsand the companies which provide investmentservices.

Crossed trading on the market is cleared inthree days, trading on credit is permitted andnew hedging instruments (i.e. index andwarrant options) are available. The modernregulations for takeover bids and publicofferings should be noted.

On April 12, 2003, Royal Decree 432/2003amending the current regulations on tenderoffers was published. This Royal Decreeoffers broader protection to small investorsby introducing the changes detailed below:

The reform adds new situations in which atender offer must be made, namely:

– A tender offer must be made for 10% ofthe capital of the target company, wherethe intention is to reach a percentagelower than 25% of its capital, provided thatit permits the acquiror, and the acquirorintends, to appoint a number of boardmembers (together with any the acquirorhas already appointed) representing morethan one third and less than one half plusone of the members of the board ofdirectors of the target company.

– A tender offer must be made for 100% ofthe capital of the target company, wherethe intention is to reach a percentagelower than 50% of its capital, provided thatit permits the acquiror, and the acquirorintends, to appoint a number of board

members (together with any the acquirorhas already appointed) representing morethan half of the members of the board ofdirectors of the target company.

The reform now expressly permits thepossibility of making conditional tenderoffers effective subject to conditions thefulfillment of which must be approved by thecorporate bodies of the target company.

Lastly, the reform improves the rules oncompeting tender offers:

– It eliminates the requirement that theprices in competing offers must bebettered by at least 5%.

– Once the period for accepting the last ofthe authorized competing tender offers hascommenced, an auction period starts.Accordingly, the tender offerors maymodify the terms of their offers bybettering the price or widening the scopeof their offers to a greater number ofsecurities. The bettered price must besubmitted in a sealed envelope to theCNMV within five days of thecommencement of the period for acceptingthe last of the authorized competingtender offers.

2002 saw the formation of Bolsas yMercados Españoles, Sociedad Holding deMercados y Sistemas Financieros, S.A., whichgroups together the following companies:

– FC & M, Sociedad Rectora del Mercado deFuturos y Opciones sobre Cítricos, S.A.

– MEFF-AIAF-SENAF Holding de MercadosFinancieros, S.A.

– Iberclear (Servicio de Compensación yLiquidación de Valores, S.A.).

– The Madrid, Barcelona, Valencia and BilbaoStock Exchange Governing Companies.

2004/CAP 2-a4 28/4/04 16:27 Página 33

T h e S p a n i s h f i n a n c i a l s y s t e m

34

The purpose of this holding company is toact as the integrating force behind thevarious Spanish stock markets and as thekey instrument of their internationalprojection.

Also noteworthy within the statutoryframework is the approval of Law 19/2003regulating the legal regime for movements ofcapital and economic transactions withforeign countries and concerning certainmoney laundering prevention measures, asthe Law overhauls the previous legal regimeof exchange control.

One of the highlights of the new Law is thetreatment afforded to preferredparticipations, which must satisfy thefollowing requirements:

– They must be issued by a credit institutionresident in Spain or in another EU MemberState, the voting rights of which mustwholly correspond, directly or indirectly, tothe parent credit institution of aconsolidable group or subgroup of creditinstitutions and the sole business of whichis to issue preferred participations.

– The issuer must furnish the tax authoritieswith information on the businesses andidentities of the holders of theparticipations issued.

– They must be listed on organizedsecondary markets.

– They must not grant preemptivesubscription rights with respect to futureissues.

– They must be perpetual in nature, althoughearly redemption may be agreed on asfrom the fifth year following the date ofdisbursement, with the prior authorizationof the Bank of Spain.

– In cases of dissolution or liquidation,preferred participations must guaranteeonly the reimbursement of the par valuetogether with the remuneration accruedand outstanding.

– For the purposes of issuing preferredparticipations, the outstanding par valuemay not exceed 30% of the core capital ofthe consolidable group or subgroup,including the amount of the issue itself.

All these advances have made the securitiesmarket in Spain more transparent and safer.

a) Equity market

The activity of the Spanish stock marketcan be gauged by the trading volume of the Madrid Stock Exchange, which was g 100,670 million in October, 2003, withthe number of transactions amounting to2.33 million.

The total market capitalization of equitiesin 2002 was g 419,450 million, down 20%from 2001.

Foreign investment also made a significantcontribution to growth in the Spanishstock market. As of December 2002,foreign investment amounted to g 218,726million of listed shares, representing anincrease of 49.8% of the total market.

Chart 3 shows the high volume of foreigninvestment in the Spanish stock market.

2004/CAP 2-a4 28/4/04 16:27 Página 34

T h e S p a n i s h f i n a n c i a l s y s t e m

35

Stock exchange markets had very difficultmoments during year 2002. Despite the2002 losses and from a historicalperspective, Spanish Stock ExchangeMarket has supported a high profitabilityduring the last ten years. The accumulativeannual profitability in the last ten years hasbeen 15,2%; meanwhile the US StockExchange rose a 9.4% and the LondonStock Exchange rose a 6.4%.

The importance of foreign investment inlisted shares, market capitalization andshare index variations in the majorEuropean stock exchanges is shown inTables 2 and 3, and Chart 4.

Chart 3

Madrid Stock Exchange tradingvolume by type of investor(December 2002)

Source: Madrid Stock Exchange.

Foreign Retail operators

Proprietary Proprietary (banks)(brokers)

Collective investment and other

62.91%

5.43%5.88%

9.13%

16.65%

Table 2

Foreign investment in shares of listed companies (transactions on the secondary market)(Millions of euros)

Year Purchases Sales Net Investment

1987 8,941.42 6,415.29 2,526.131988 6,546.35 5,219.17 1,327.181989 10,194.97 6,011.55 4,183.431990 10,023.94 6,640.99 3,382.951991 9,922.43 8,059.56 1,862.871992 11,026.16 8,877.07 2,149.091993 18,211.90 12,647.96 5,563.951994 20,784.85 20,051.53 733.321995 20,766.93 18,037.82 2,729.111996 30,789.29 31,059.69 -270.401997 61,571.63 62,027.41 -455.781998 115,765.75 110,594.74 5,171.011999 136,165.00 131,825.00 4,340.002000 260,721.60 275,505.66 -14,784.052001 227,730.00 251,070.00 -23,340.002002 218,726.00 239,734.00 -21,008.002003* 151,110.00 161,640.00 -10,530.00

* Data at July, 2003.Source: Madrid Stock Exchange.

2004/CAP 2-a4 28/4/04 16:27 Página 35

T h e S p a n i s h f i n a n c i a l s y s t e m

36

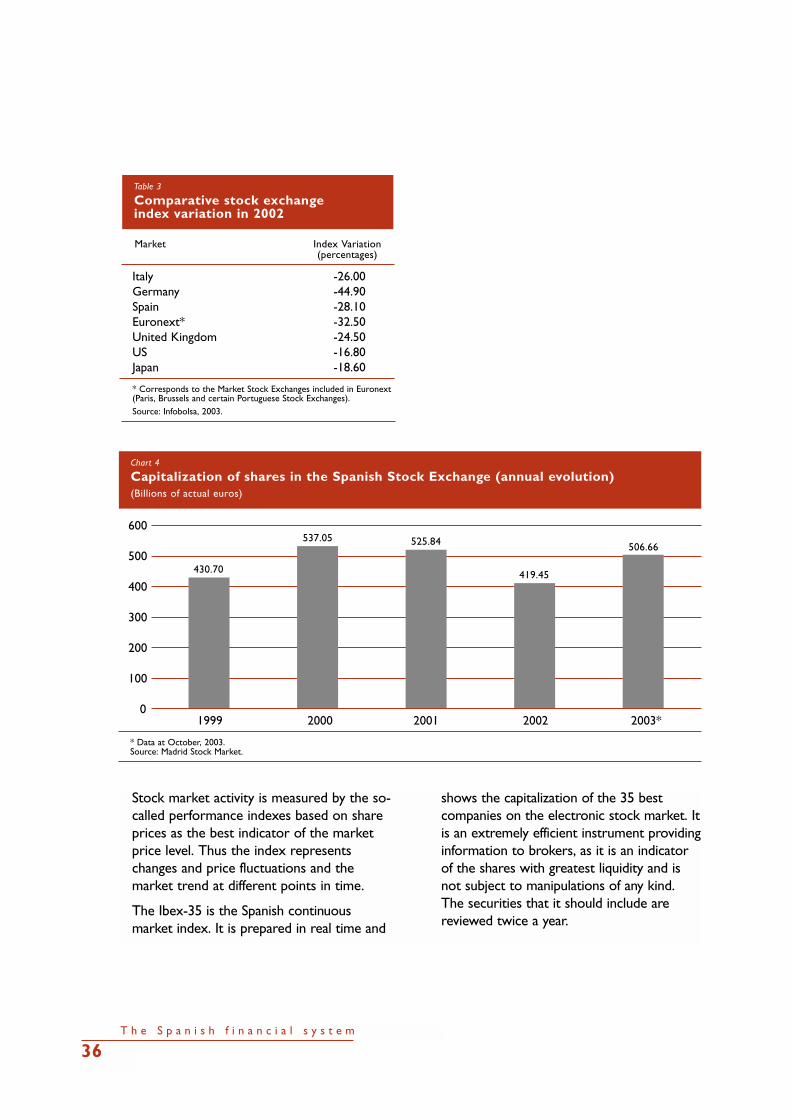

Stock market activity is measured by the so-called performance indexes based on shareprices as the best indicator of the marketprice level. Thus the index representschanges and price fluctuations and themarket trend at different points in time.

The Ibex-35 is the Spanish continuousmarket index. It is prepared in real time and

shows the capitalization of the 35 bestcompanies on the electronic stock market. Itis an extremely efficient instrument providinginformation to brokers, as it is an indicatorof the shares with greatest liquidity and isnot subject to manipulations of any kind.The securities that it should include arereviewed twice a year.

Table 3

Comparative stock exchange index variation in 2002

Market Index Variation(percentages)

Italy -26.00Germany -44.90Spain -28.10Euronext* -32.50United Kingdom -24.50US -16.80Japan -18.60

* Corresponds to the Market Stock Exchanges included in Euronext(Paris, Brussels and certain Portuguese Stock Exchanges).Source: Infobolsa, 2003.

Chart 4

Capitalization of shares in the Spanish Stock Exchange (annual evolution)(Billions of actual euros)

600

500

400

300

200

100

01999 2000 2001 2002 2003*

* Data at October, 2003.Source: Madrid Stock Market.

506.66

419.45

525.84537.05

430.70

2004/CAP 2-a4 28/4/04 16:27 Página 36

12,820

11,576

10,333

9,090

7,846

6,603

5,360Jan. Apr. Jul. Oct. Jan. Apr. Jul. Oct. Jan. Apr. Jul. Oct. Jan. Apr. Jul. Oct. Jan. Apr. Jul. Oct.

1999 2000 2001 2002 2003

Source: Spanish Stock Exchange.

T h e S p a n i s h f i n a n c i a l s y s t e m

37

To be included in the index, certainguidelines must be observed such as:

– Trading on the continuous market for atleast six months.

– Companies with stock exchangecapitalization of less than 0.3% of theaverage capitalization of the Ibex-35 maynot be included.

– Rules on the weighing of companiesaccording to their free float must beobserved.

Chart 5 shows the performance of thisindex in the last few years.

b) Options and futures market

The regulated Spanish options and futuresmarket is the MEFF (“Mercado Español deFuturos Financieros”). MEFF is an officialmarket and therefore entirely regulated,controlled and supervised by the financialauthorities (CNMV and the Ministry ofEconomy) performing the functions fortrading and those of clearance and

settlement, fully integrated in theelectronic market developed for thepurpose.

There are options and futures marketsrelated to citrus fruits and olive oil.

c) Fixed-income market

The fixed-income markets in Spain arecharacterized by:

– The establishment of a predeterminedsecurity redemption plan at the maturitydate.

– The yield provided to investors in theform of interest or the differencebetween the redemption price and thesubscription price.

The Spanish market for the trading offixed-income securities and assets ofprivate companies and private institutionsis the AIAF, “Asociación de Intermediariosde Activos Financieros”, which forms apart of the official organized financialmarket in this country.

Chart 5

Average value of Ibex-35, 1999-2003

2004/CAP 2-a4 28/4/04 16:27 Página 37

T h e S p a n i s h f i n a n c i a l s y s t e m

38

The AIAF market has developed swiftly inrecent years because of the expansion offixed-income securities in Spain. It wascreated in 1987 through an initiative of theBank of Spain, which wished to put newmechanisms in place to encourage businessinnovations with funds procured throughfixed-income assets.

Subsequently, taking the AIAF as a base,the regulatory and supervisory authoritiesprovided it with the attributes necessary tocompete in its surroundings until equatingit in legal terms with the financial markets.

Therefore AIAF “Mercado de Renta Fija”can be described as an organized marketwith ninety-four members, including theleading banks, savings banks andstockbroker companies and agencies in theSpanish financial system.

At October 2001, AIAF held a 60.1%interest in SENAF, (“Sistema Electrónico de Negociación de Activos Financieros”),an electronic financial assets trading system created in 1999 by Infomedas (a stockbroker agency acting as a tradingplatform for the blind market). SENAF wasorganized as the electronic platform fortrading Spanish government notes andbonds, and it acts neutrally towards thebond market, since its legal statuteprevents it from taking positions. It issubject to supervision by the CNMV andby the Bank of Spain.

The SENAF develops and operates a blindelectronic system for bond trading, inwhich the traders do not know thecounter party in their transactions. Thispromotes the efficiency of the market andgenerates great liquidity.

On February 23, 2001, the Governmentauthorized the creation of SENAF as anorganized trading system. This means thatall the members of any official fixed-incomesecond market may join the system,including the members of fixed-incomemarkets in other countries, provided thatthey meet certain conditions.

The aim of this interest held by AIAF inSENAF was to begin to support theintegration of fixed-income trading systemsin Spain. This has now materialized withthe creation of the MEFF-AIAF-SENAFHolding de Mercados Financieros, S.A. onOctober 4, 2001.

With the creation of this holding company,the first group of financial markets by totaltrading volume has been set up. It is alsothe first initiative for the interconnectionof all Spanish financial markets, with a jointprojection of domestic and internationalscope. It also means the provision of anintegrated service and the offer of newproducts and services, under unbeatableconditions of quality and cost.

Also, the incorporation of this companyaims to strengthen the three entities’competitive position, signifies the provisionof an integrated service, enables newproducts and services to be offered andoffers the possibility of sharing technicalsolutions and harnessing economies ofscale, which will result in lower operatingcosts for market members.

2004/CAP 2-a4 28/4/04 16:27 Página 38

T h e S p a n i s h f i n a n c i a l s y s t e m

39

d) New Market

As a noteworthy new feature of thesecurities market, the “New Market” wascreated in 2000 by CNMV Circular 1/2000,implementing the Ministerial Order ofDecember 22, 1999, as a special tradingsegment in the Spanish stock exchanges.The New Market is used to tradesecurities of companies in state-of-the-artsectors as regards their final products,their production processes or theirperformance of business with high growthpotential.

The New Market (“Nuevo Mercado”) wascreated essentially because of the presenceon the Spanish stock market of companiesassociated with the new communicationstechnologies and particularly with theInternet, and it was thus based onexperiences of a similar kind in themarkets of other countries.

Among the special features of the NewMarket, note the exception made, at theregulatory level, with regard to theperiod for obtaining profits and theprovision of reports on businessprospects and potential futuredevelopment. This is considered of greatimportance for new-economy companies,since many of them, organized recentlyon the base on future expectations, donot have a positive profit and lossaccount at the present time.

To protect investors, the “Sociedad deBolsas” has laid down specific rules fortrading, considering the higher volatilityand risk of the securities. Thus, for thespecific case of New Market securities, themaximum percentage of price variationsfor each session has been increased to 25%(it is 15% for traditional securities), and

this percentage may be further increased ifthe circumstances of the market or of thesecurity make this advisable.

However, the investor’s safety in connectionwith these securities is based on reportingobligations additional to the traditional ones(relevant events, quarterly, six-monthly andyearly information), since at least once ayear these companies must publishexplanatory information on the evolutionand prospects of their businesses at theshort term or in the next financial year.

The New Market started up on April 10,2000 with ten companies being listed,although there are currently eleven,following the delisting of Puleva BIOTECHand Serv. POINT.SOL during 2003. To helpmonitor the New Market, the IBEX NMindex was created. Its value of 1,754 onNovember 21, 2003 shows a increase of27.35% in relation to its levels in late 2002.

The market capitalization of the companieslisted in the New Market on December 31,2002 is shown in Table 4:

Table 4

Capitalization of New Marketcompanies at Dec. 31, 2002

New Market Euro capitalizationIBEX Securities (euros)

Terra 2,438,722,638.59Amadeus 1,739,025,000.00TPI 1,115,750,022.93Zeltia 1,082,449,283.80Indra 958,398,765.12Abengoa 303,978,124.80Jazztel 274,110,999.98Tecnocom 54,648,345.10Amper 50,236,498.80Avanzit 20,824,754.50Natraceutical 18,443,934.18

Source: Invertia.

2004/CAP 2-a4 28/4/04 16:27 Página 39

T h e S p a n i s h f i n a n c i a l s y s t e m

40

5. Money marketThe money market in Spain is basedfundamentally on the issuance of short-termsecurities by the Bank of Spain, which aretaken up by banks, finance companies andmoney market operators that subsequentlyplace a portion of them with individuals andbusinesses.

In a broader sense, the money market isdeemed to encompass also interbankdeposits (the interest rates for which areused as benchmarks for other transactions)and trading in short-term corporatesecurities.

The money market has become increasinglyimportant as a result of the liberalization andgreater flexibility of the Spanish financialsystem as a whole in past years. This isevident from the fact that interest rates areordinarily higher than the rate of inflationand from the substantial volume of trading inmoney market securities.

The government debt market is of specialimportance in Spain and is very often usedby both resident and foreign investors. Thefavorable tax arrangements for investmentsby nonresidents in these securities is makingthis market particularly attractive.Noteworthy developments were thestructuring of money market operationsthrough a book-entry system and thecreation of the options and futures markets,both linked to the book-entry system oftrading in government debt securities.

Following the merger of the Bank of SpainBook-Entry Center and the SecuritiesClearing and Settlement Service, Iberclear isnow in charge of recording, clearing andsettling transactions in the Book-EntryGovernment Debt Securities Market.

The globalization of the securities markets isalso being demonstrated, since 1999, bymergers and alliances among depositories ofthe Euro Zone, such as the trans-bordermergers of Euroclear with the CentralDepositories of France, Belgium and Holland,or that of Cedel with the Deutsche BörseClearing (DBC).

The combination of these factors has had animportant effect on the fixed-incomemarkets, demonstrated by:

– Increased interaction between theefficiency of the channels for issues andtrading and the appraisal of fixed-incomeassets.

– Increased interchangeability betweenproducts issued by the public treasures inthe Euro Zone. The enhanced transparencyof markets facilitates comparison of thevarious assets and therefore increasescompetition among issuers.

– Liquidity and spread in lending, togetherwith the expectations of agents concerningthe future evaluation of variables, havebecome decisive factors for the price ofthe assets and their relative valuecompared with other fixed-income issues.

In 2002, trading in the Spanish governmentdebt market, including bond and debenturesmarket trading and considering single anddouble transactions, increased up to g 18.9trillion, 16.4% higher than 2001 levels.

Thus the level of bond and debenture markettrading was higher in 2002 than in 2001. Thisrise was due to the increase in operationsbetween accountholders (up 21% year-on-year) and in double transactions, according tothe up of 25% year-on-year increase in thetrading with third parties and single-transaction trades.

2004/CAP 2-a4 28/4/04 16:27 Página 40

T h e S p a n i s h f i n a n c i a l s y s t e m

41

Overall, the total volume of bonds anddebentures traded in 2002 was g 16.7trillion, up 23.2% on the g 15.4 trilliontraded in 2001.

Also noteworthy was the sharp increase inthe debt securities held by nonresidents,since the introduction of the euro. Their debtportfolio consisted mainly of governmentbonds and debentures and included scantlysignificant Treasury bill holdings.

Analysis of this market showed most notablythat until 1999 the unstripped bonds anddebentures held by nonresidents represented24% of the outstanding total, although in

2002 there was a surge in this segment,which now accounts for 41.4% of the totalamount of these products.

The reasons for this sharp rise in the growthof government debt securities held bynonresidents are as follows:

– Spain’s accession to Economic andMonetary Union (EMU) eliminatedexchange risk, which made Spanishgovernment debt more attractive.

– The strong performance of the Spanisheconomy in 2002 and its healthy growthled to a higher rating of Spanish debt.

Chart 6

Public Debt Negotiation Volume(Millions of euros)

40,000

35,000

30,000

25,000

20,000

15,000

10,000

5,000

0Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

■ 2002 ■ 2003

Source: AIAF 2003.

2004/CAP 2-a4 28/4/04 16:27 Página 41

T h e S p a n i s h f i n a n c i a l s y s t e m

42

– The significant contribution by nonresidentmarket makers who entered the Spanishgovernment debt market in 1999 and havemoved significant volumes of debt, therebymaking for an active market.

6. Credit financeestablishmentsThese institutions are regulated by RoyalDecree 692/1996, which characterizes themas subject to the legal regime of creditinstitutions, although with certain changesregarding their financing possibilities andoperating capacity.

They may engage in the following activities:

– Lending and credit, including consumercredit, mortgage loans and the financing ofcommercial transactions.

– Factoring, with and without recourse, andother supplementary transactions.

– Financial leasing.

– Provision of guarantees.

These institutions include most notablyfinancial lease and factoring companies.

Financial lease companies engage in leasingand renting.

Leasing is a transaction of a financial naturegoverned by commercial law whereby acustomer acquires an asset previouslychosen by him and its use is assigned to himin exchange for certain periodic (normallymonthly) payments; on completion of thecontract term, the customer can opt toexercise a purchase option on the asset andpay its residual value.

Renting is a manner of medium- and long-term leasing of assets. Under this contractthe customer undertakes to pay a fixed

amount, generally monthly, for a certain timeand the credit institution undertakes tofurnish the use of the asset for thecontractual period, assure that the asset ismaintained in good condition and arrangecomprehensive insurance on the asset. Onexpiration of the contract the customer canopt to replace the assets with others orrenew the contract for a certain period.

Factoring is a transaction whereby acompany assigns the trade accountsreceivable from its customers to aspecialized financial institution in exchangefor a consideration. This enables companiesto transfer their cash management tasks toanother party.

There are two types of factoring:

– With recourse: The factor does notassume liability for any factored receivableswhich cannot be collected. Accordingly, ifthe debtor fails to pay, the factor can claimpayment from its customer, which assumesliability for nonpayment.

– Without recourse: The factor accepts thecredit risk arising from the receivablesfactored by the customer.

7. Venture capitalinstitutionsVenture capital is defined as a financialactivity which consists of routing investmentsto unlisted nonfinancial companies andassuming the risk arising from their activitythrough the acquisition of a temporaryholding in their capital stock.

Venture capital institutions can take the legalform of a corporation or a fund and, inaddition to their main corporate purpose,can grant participating loans and providecounseling services to the investees.

2004/CAP 2-a4 28/4/04 16:27 Página 42

T h e S p a n i s h f i n a n c i a l s y s t e m

43

8. Asset securitizationSecuritization consists basically of thetransformation of securities acquired fromcredit institutions into standardized fixed-income securities for subsequent trading inorganized markets, where they can bepurchased by investors.

Two types of securitization can bedistinguished:

– Mortgage-backed securitization: This isperformed through mortgagesecuritization funds, which are separateasset pools lacking legal personality whoseassets are the mortgage loans pooled bythem and whose liabilities are thesecurities issued, such that their net assetvalue is zero.

– Asset-backed securitization: Assetsecuritization funds are separate assetpools lacking legal personality whose assetsare their financial assets and othercollection rights, including assignments ofpresent and future receivables, and whoseliabilities are the fixed-income securitiesissued, loans from credit institutions andany contributions from institutionalinvestors.

9. Mutual guaranteesocietiesThese companies were first introduced in1978 and since then have operated in thearea of medium- and long-term financing ofsmall and medium-sized enterprises, towhich they provide guarantees.

Accordingly, their corporate purpose is asfollows:

– To provide their members with access tocredit and to credit-related services.

– To improve the financial conditions of theirmembers.

– To provide personal guarantees in anylawful form.

– To provide assistance and financial adviceto their members.

– To take holdings in companies andassociations whose sole purpose is toengage in activities for small and medium-sized companies. To this end, they musthave the required reserves and obligatoryprovisions.

The following members of mutual guaranteesocieties should be distinguished:

– Participating members: Also known asmutual members. They are the individualsor legal entities eligible to obtainguarantees from the society. Therefore,they are required to belong to the industryspecified in their bylaws.

– Protector members: These cannot requestguarantees from the society and thereforeare not subject to limitations on theindustry to which they belong. Theprotector members are usually publicauthorities, public-law entities and thecompanies majority-owned by them.

Working together with these societies are“sociedades de reafianzamiento” (supporting-guarantee companies), whose purpose is toprovide sufficient coverage and assurance forthe risk assumed by the mutual guaranteesocieties and, in addition, furnish the cost ofthe guarantee for the members.

2004/CAP 2-a4 28/4/04 16:27 Página 43

T h e S p a n i s h f i n a n c i a l s y s t e m

44

10. Pension plans andinsurance companiesIn 1987 the Pension Plans and Funds Lawintroduced a form of saving in Spain that hascreated a sound instrument for long-termfinancing. This legislation envisages theexistence of pension plans promoted byemployers, certain associations and financialentities.

Pension plans are collective investmentproducts which invest a principal sum with aview to obtaining periodic income or capitalgains in the future in order to provide forretirement, death or disability.

Pension funds are asset pools set up for thesole purpose of implementing pension plans.A pension fund may include one or morepension plans.

Inherent features of pension plans are theirfavorable tax treatment and restrictions onuse of the accumulated savings until theoccurrence of the event for which they wereintended.

Also, the Law provides for the possibility ofwithdrawing the savings accumulated inpension plan in the event of long-termunemployment or serious illness.

The Private Insurance Law (Law 30/1995)required all Spanish companies (exceptfinancial institutions) to instrument beforeNovember 15, 2002, their pensioncommitments to employees through anexternal arrangement (pension plan orinsurance policy), which rose significantly thefunds managed by these entities.

Pension funds performed very well in 2002,and this was reflected by an increase in thenumber of plan participants, up 12.55% from2001. This is due especially to theexternalization process by various employersthat has taken place in the employmentsystem.

The volume managed by occupationalpension funds rose to g 22,728 million at theend of September, 2003, up 22.94% from thesame period in 2002. See Table 5.

The personal pension system, with assets ofg 28,169 million, grew more moderately inthe same period (by 20.44%).

In contrast, the performance of theassociation system has not been so strong,with more than g 772 million of assets and87,854 participants.

Table 5

Variation of assets of pension funds (Millions of euros)

Personal System Occupational System Association System

1999 18,989 11,834 8402000 21,494 15,553 8122001 24,214 18,837 7772002 26,284 21,278 760Sep. 30, 2003 28,169 22,728 772

Source: Inverco.

2004/CAP 2-a4 28/4/04 16:27 Página 44

The Spanish life insurance market has grownsubstantially in recent years, mainly becauseof the similarity between survivorship lifeinsurance policies and traditional savingsinstruments and because of the morefavorable tax treatment than in the past.Although the economic crisis due to theSeptember 11 atacks slowed insuranceindustry growth in 2001, in 2002 the processof employers externalizing their pensioncommitments fueled insurance growth wellabove general growth levels.

In this connection, it is noteworthy that,effective 2002, the tax treatment of savingsplaced in pension funds has again beenimproved.

The Spanish insurance industry will facemajor challenges in the next few years, whichmay be beneficial for it insofar as thetheoretically foreseeable growth in the sizeof companies will bring its ratios closer tothose in countries with similar economies.

Also noteworthy is the trend towardsconsolidation in the Spanish insurancemarket, with mergers, spin-offs, andassignments of books of business leading tothe disappearance of 7 companies in 2002.

In 2002, the Spanish insurance industry sawthe volume of its premiums increase by14.53%.

The revenue collected by the insuranceindustry in 2002 was approximately g 50,000million, of which 55.5% were in life and45.5% in nonlife.

Chart 7 shows the importance of investmentin pension funds and life insurance productscompared with other forms of investments,such as mutual funds.

In 2002, technical results for the nonlifeinsurance business as a whole increased byalmost 450%, yielding the first technicalincome in many years. For the life insurancebusiness, technical income amounted to g 644 million, representing growth of only4.38% due to the decline in value ofinvestments, offset largely by the realizationof capital gains. Growth in the other classesof insurance was 157%, which accounts for6.2% of gross premiums earned, almostdouble the figure in 2001.

T h e S p a n i s h f i n a n c i a l s y s t e m

45

Chart 7

Savings distribution(Millions of euros)

200,000

180,000

160,000

140,000

120,000

100,000

80,000

60,000

40,000

20,000

01999 2000 2001 2002

■ Investment Funds■ Life Insurance■ Pension Funds

Source: General Directorate of Insurance and Pension Funds.

2004/CAP 2-a4 28/4/04 16:27 Página 45

T h e S p a n i s h f i n a n c i a l s y s t e m

46

Law 44/2002, (“the Financial Law”), approvedby the Lower House of Parliament onNovember 22, 2002, includes major changesto the Spanish financial system.

First of all, a securities Registration, Clearingand Settlement System ManagementCompany (“Systems Company”) has been setup through the merger of the SecuritiesSettlement and Clearing Service (SCLV) andthe Spanish Government Debt Book-EntryTrading Central Office (CADE).

This company has included other systemsalready existing in Spain, such as those forfinancial derivatives or those managed by theValencia, Bilbao or Barcelona stockexchanges, and will enable the managementof interconnections and alliances with othercountries’ stock markets.

One or more Central Counterparty Entitieswill foreseeably be set up and interposedbetween the purchaser and the seller toeliminate counterparty risk in transactionsand ensure that they are duly completed.

The Settlement and Clearing Systems will bedemutualized and a portion of their capitalwill be placed in the hands of shareholdersthat do not trade in the market.

Also, changes have been made to the systemset up to control the cross-holdingsbetween the companies administeringsecondary markets and their counterpartsoutside Spain. This will permit a moreflexible system conducive to the integrationof crossborder markets while simultaneouslyensuring a certain control over theappropriateness of shareholders in theSpanish markets.

As regards insurance, securities andcollective investment institutions, theexchange of information has been mademore fluid by facilitating these procedures

between the EU supervisors and those inother countries, while ensuring dueconfidentiality.

Extensive regulation of the organized tradingsystems has been introduced in matters suchas the authorization system, the obligation toform governing companies with the legalform of corporations (Spanish “S.A.”companies) and the supervision and penaltysystem.

In the credit market, a more flexibleinvestment regime for credit cooperativeshas been introduced to make it more similarto that of banks and savings banks. Thepurpose of this change is to:

– Enable these entities to achieve a largersize, thereby paving the way for increasesin their industrial portfolios.

– Facilitate management of their liabilitiesand equity by means of recourse tosubordinated debt financing.

As regards the equity of credit institutions,the regulation of the participation certificatesof savings banks, which are treated asmarketable securities representing monetarycontributions for an indefinite term, standsout. Participation certificates cannot beissued for a value below their par value andwill be listed on organized secondarymarkets.