gst update brent murray cga cch tax update webinar march 5, 2008 brent murray cga cch tax update...

Post on 20-Dec-2015

213 views

TRANSCRIPT

GST UpdateGST UpdateBrent MurrayCGA CCH Tax Update WebinarMarch 5, 2008

Brent MurrayCGA CCH Tax Update WebinarMarch 5, 2008

2

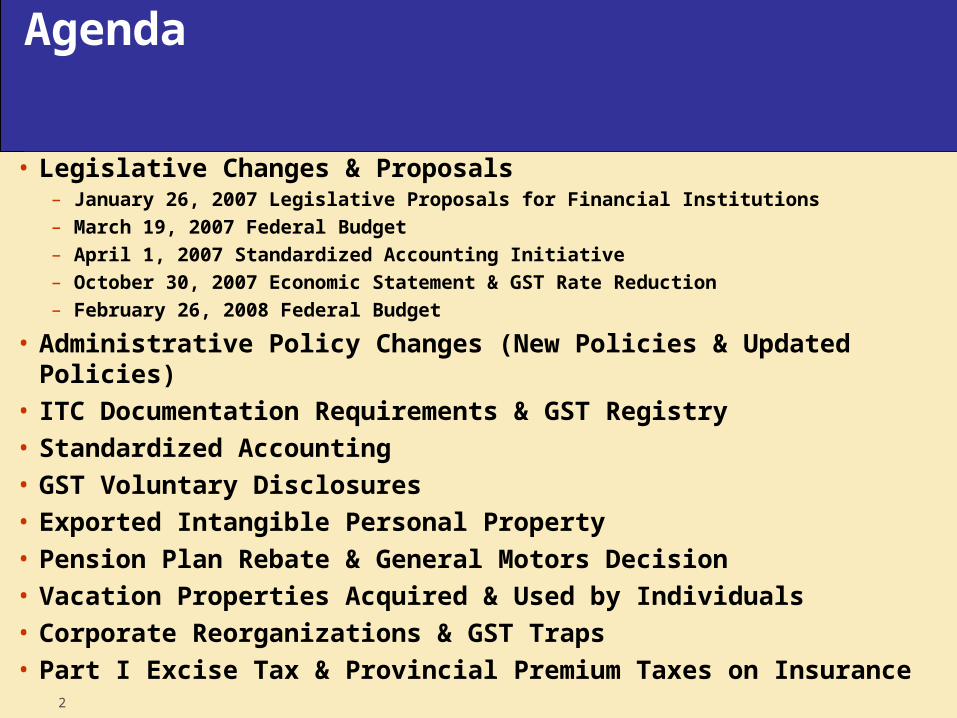

Agenda

• Legislative Changes & Proposals– January 26, 2007 Legislative Proposals for Financial Institutions– March 19, 2007 Federal Budget– April 1, 2007 Standardized Accounting Initiative– October 30, 2007 Economic Statement & GST Rate Reduction– February 26, 2008 Federal Budget

• Administrative Policy Changes (New Policies & Updated Policies)• ITC Documentation Requirements & GST Registry• Standardized Accounting • GST Voluntary Disclosures• Exported Intangible Personal Property• Pension Plan Rebate & General Motors Decision• Vacation Properties Acquired & Used by Individuals• Corporate Reorganizations & GST Traps• Part I Excise Tax & Provincial Premium Taxes on Insurance

3

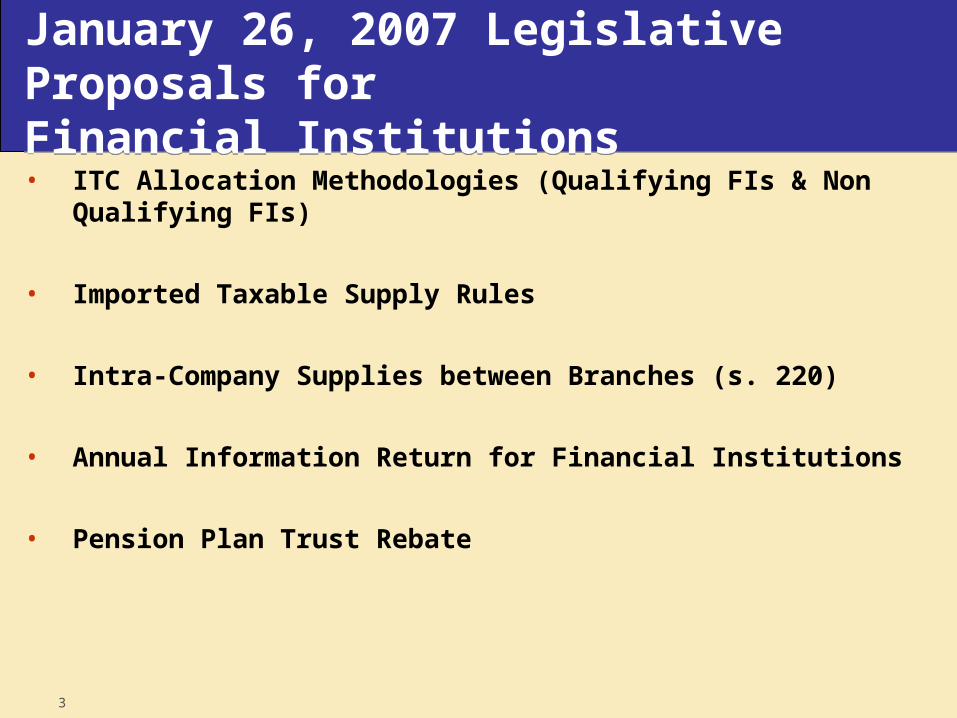

January 26, 2007 Legislative Proposals forFinancial InstitutionsJanuary 26, 2007 Legislative Proposals forFinancial Institutions

• ITC Allocation Methodologies (Qualifying FIs & Non Qualifying FIs)

• Imported Taxable Supply Rules

• Intra-Company Supplies between Branches (s. 220)

• Annual Information Return for Financial Institutions

• Pension Plan Trust Rebate

4

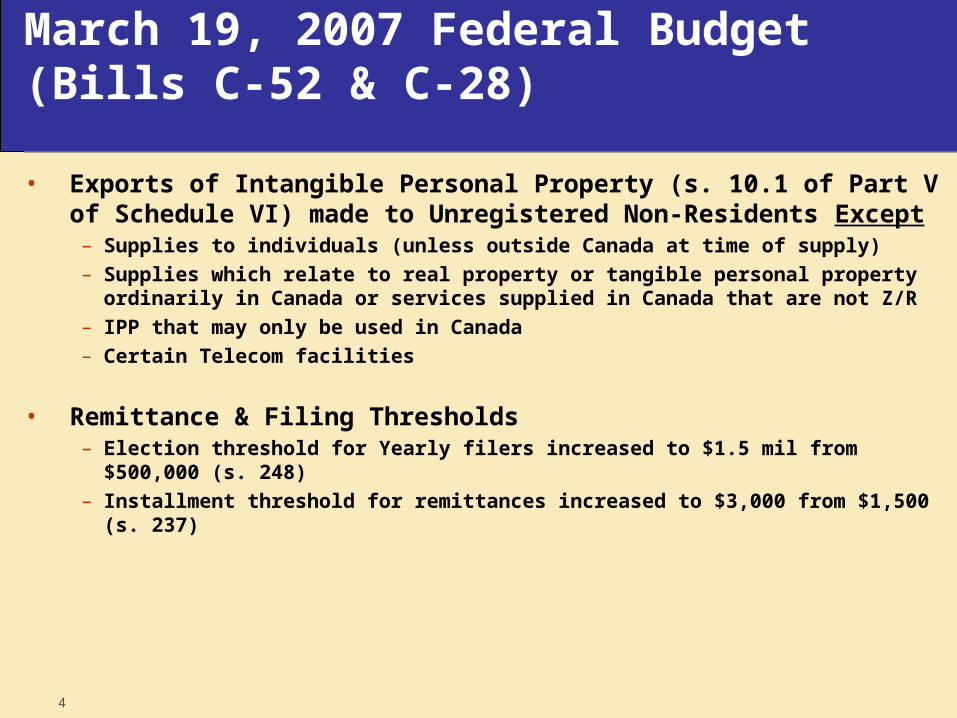

March 19, 2007 Federal Budget (Bills C-52 & C-28)March 19, 2007 Federal Budget (Bills C-52 & C-28)

• Exports of Intangible Personal Property (s. 10.1 of Part V of Schedule VI) made to Unregistered Non-Residents Except– Supplies to individuals (unless outside Canada at time of supply) – Supplies which relate to real property or tangible personal property ordinarily in

Canada or services supplied in Canada that are not Z/R– IPP that may only be used in Canada– Certain Telecom facilities

• Remittance & Filing Thresholds– Election threshold for Yearly filers increased to $1.5 mil from $500,000 (s. 248)– Installment threshold for remittances increased to $3,000 from $1,500 (s. 237)

5

March 19, 2007 Federal Budget (Bills C-52 & C-28)March 19, 2007 Federal Budget (Bills C-52 & C-28)

• Foreign Convention & Tour Incentive Program (s. 167.2 & s. 252.1 through 252.4)

• Green Levy on Fuel-Inefficient Vehicles (s. 6 of Schedule I to ETA)– Taxes of $1,000 to $4,000 per passenger vehicle based on fuel consumption rating

• End-User Refunds for Excise Tax on Diesel Fuel (s. 68.01)

• ITCs for Meal Expenses of Truck Drivers (s. 236(1))

6

April 1, 2007 Standardized Accounting Initiative (Bill C-13 Budget Implementation Act, 2006)April 1, 2007 Standardized Accounting Initiative (Bill C-13 Budget Implementation Act, 2006)

• Replaced 6% yearly penalty with higher interest rate (T-bill, rounded up plus 4%)

• New late filing penalties (280.1): 1% plus 0.25% per month (maximum 12 months)

• Interest payable by CRA equals T-bill, rounded up plus 2%

• Non-deductibility for Income Tax– S.18 (i)(t) of ITA (interest)– S.67.6 of ITA & Reg. 7309(GST penalties)

7

October 2, 2007 Legislative Proposals & November 13, 2007 NWM Motion (Bill C-28)October 2, 2007 Legislative Proposals & November 13, 2007 NWM Motion (Bill C-28)

• Imported Taxable Supply of Zero-Rated IPP (paragraph 217(c.1) & 218.1)

• Meal Expenses for Truck Drivers

• Filing Frequency & Installment Threshold

• Minor amendments to Non-Taxable Importation Schedule resulting from increase in 48-hour exemption to $400

• Repealing Excise Tax Exemption for Renewable Fuels

8

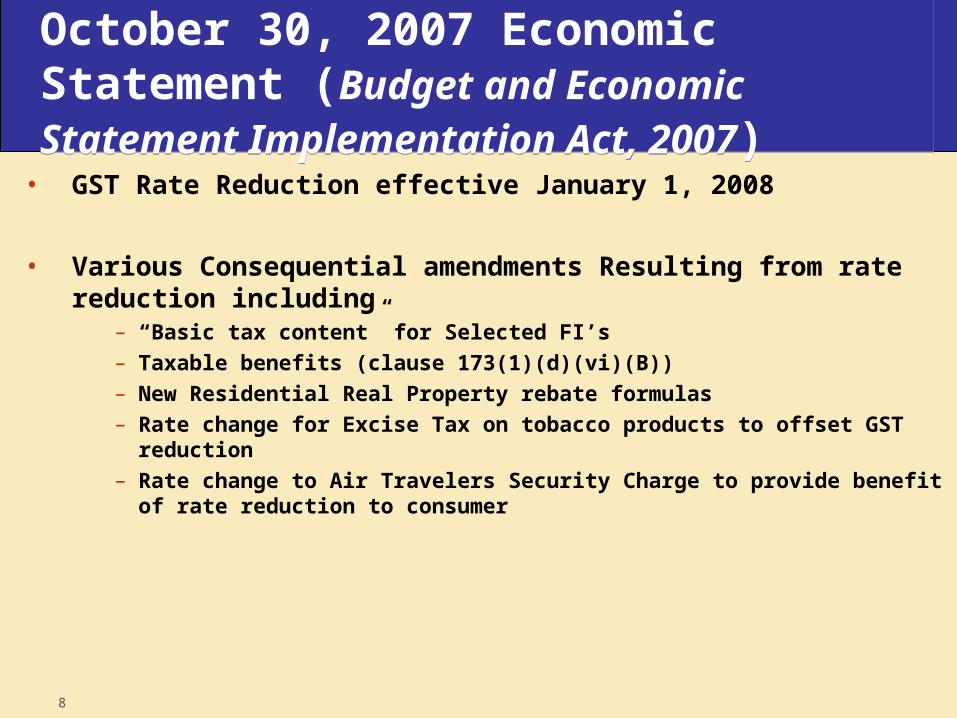

October 30, 2007 Economic Statement (Budget and Economic Statement Implementation Act, 2007)October 30, 2007 Economic Statement (Budget and Economic Statement Implementation Act, 2007)

• GST Rate Reduction effective January 1, 2008

• Various Consequential amendments Resulting from rate reduction including

– “Basic tax content” for Selected FI’s– Taxable benefits (clause 173(1)(d)(vi)(B))– New Residential Real Property rebate formulas– Rate change for Excise Tax on tobacco products to offset GST reduction– Rate change to Air Travelers Security Charge to provide benefit of rate

reduction to consumer

9

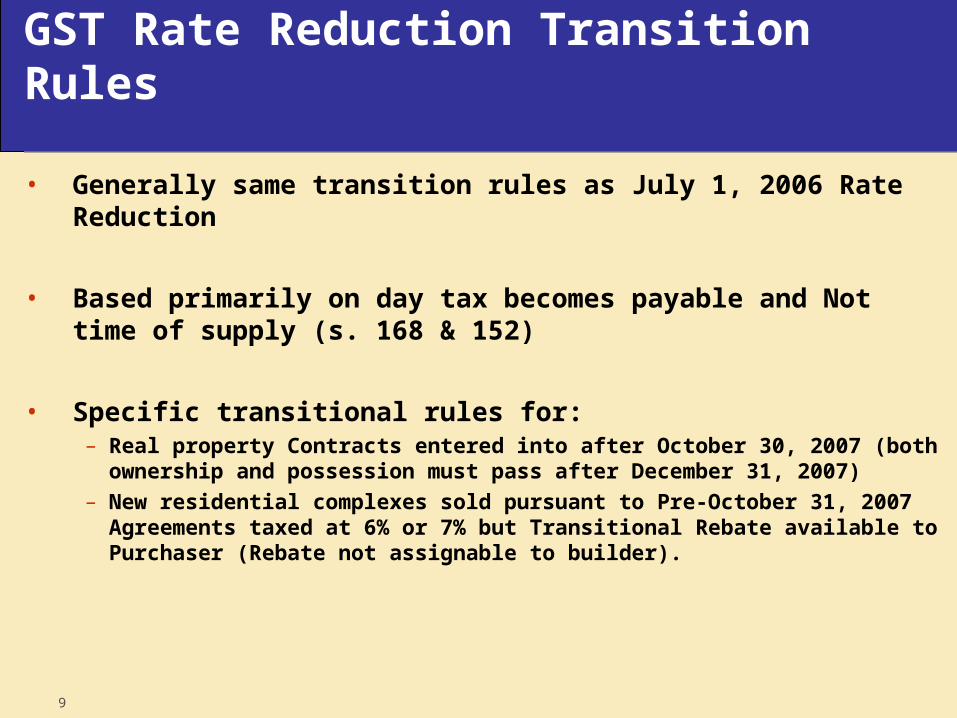

GST Rate Reduction Transition RulesGST Rate Reduction Transition Rules

• Generally same transition rules as July 1, 2006 Rate Reduction

• Based primarily on day tax becomes payable and Not time of supply (s. 168 & 152)

• Specific transitional rules for:– Real property Contracts entered into after October 30, 2007 (both ownership and

possession must pass after December 31, 2007)– New residential complexes sold pursuant to Pre-October 31, 2007 Agreements

taxed at 6% or 7% but Transitional Rebate available to Purchaser (Rebate not assignable to builder).

10

GST Rate Reduction Transition RulesGST Rate Reduction Transition Rules

• Specific transitional rules for:– Imported Goods (date of importation)– Imported Taxable Services & Intangibles (date tax is paid or payable) but special

rules for FIs based on fiscal year-end and percentage of days in 2007

• New Quick Method Remittance Formulas

• No Changes to PSB Rebate Percentages

11

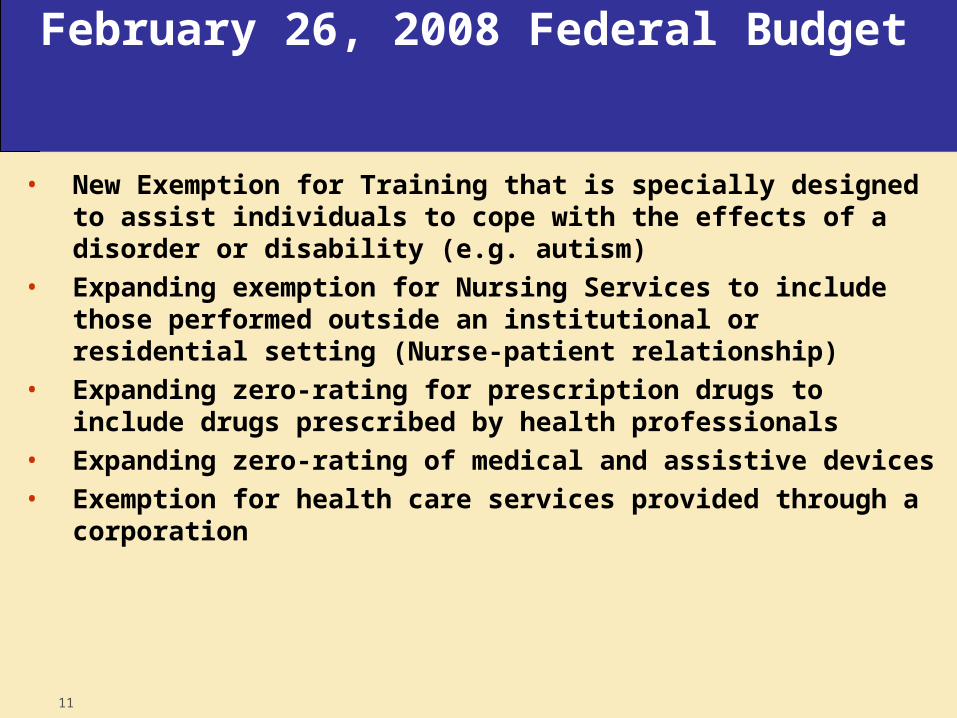

February 26, 2008 Federal BudgetFebruary 26, 2008 Federal Budget

• New Exemption for Training that is specially designed to assist individuals to cope with the effects of a disorder or disability (e.g. autism)

• Expanding exemption for Nursing Services to include those performed outside an institutional or residential setting (Nurse-patient relationship)

• Expanding zero-rating for prescription drugs to include drugs prescribed by health professionals

• Expanding zero-rating of medical and assistive devices• Exemption for health care services provided through a corporation

12

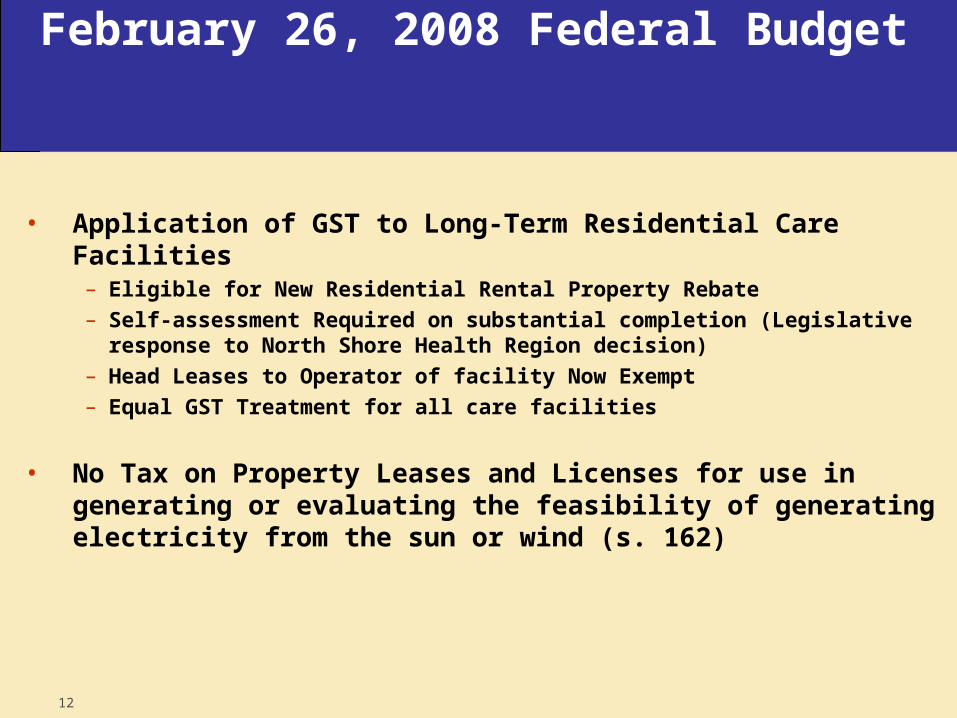

February 26, 2008 Federal BudgetFebruary 26, 2008 Federal Budget

• Application of GST to Long-Term Residential Care Facilities– Eligible for New Residential Rental Property Rebate– Self-assessment Required on substantial completion (Legislative response to

North Shore Health Region decision)– Head Leases to Operator of facility Now Exempt– Equal GST Treatment for all care facilities

• No Tax on Property Leases and Licenses for use in generating or evaluating the feasibility of generating electricity from the sun or wind (s. 162)

13

Administrative Policy UpdateAdministrative Policy Update

GST Rate Reduction Policies• Notice 226 - Proposed GST/HST Rate Reduction in 2008 (Nov. 13, 2007)• GI-043 - The 2008 GST/HST Rate Reduction and Purchases of New Housing • GI-042 - Applying the 2008 GST/HST Rate Reduction to Price Adjustments, Adjustments for

GST/HST Overcharged, and Returned Goods • GI-041 - The 2008 GST/HST Rate Reduction and Streamlined Methods of Accounting for Small

Businesses • GI-040 - Applying the 2008 GST/HST Rate Reduction to Prepaid Funeral and Cemetery

Arrangements • GI-039 - Applying the 2008 GST/HST Rate Reduction to Allowances and Reimbursements

- Tax is deemed to have been paid on day Allowance is paid (s. 174)

- Tax is deemed to have been paid on day of Reimbursement (s. 175)

- Administrative Formula of 4/104ths for reimbursements paid on or after January 1, 2008

• GI-038 - The 2008 GST/HST Rate Reduction

14

Administrative Policy Update

Newly Published Policies• TIB-100 — Standardized Accounting • TIB-099 — Application of Section 141.02 to Financial Institutions That Are Not Qualifying

Institutions• TIB-098 — Application of Section 141.02 to Financial Institutions That Are Qualifying

Institutions • TIB-097 — Determining Whether a Financial Institution is a Qualifying Institution for

Purposes of Section 141.02 • TIB-095 — Import Rules for Financial Institutions Under Section 217.1 and Dealings

Between Permanent Establishments Under Section 220 • GST Form 59E GST/HST Return for Imported Taxable Supplies and Qualifying Consideration

[non-registrants]

15

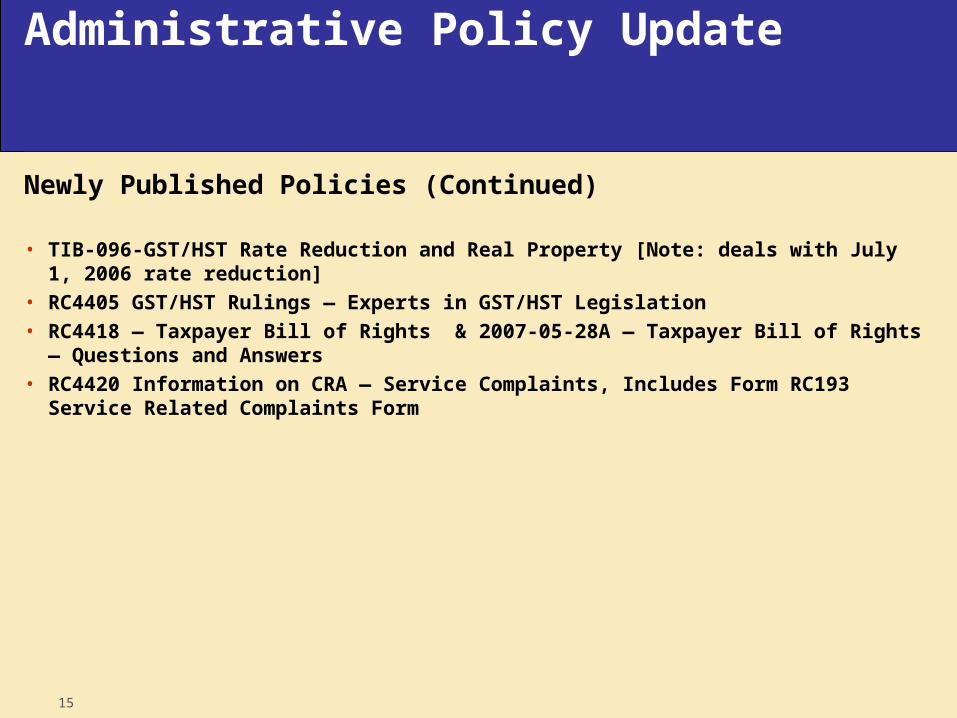

Administrative Policy Update

Newly Published Policies (Continued)

• TIB-096-GST/HST Rate Reduction and Real Property [Note: deals with July 1, 2006 rate reduction]

• RC4405 GST/HST Rulings — Experts in GST/HST Legislation• RC4418 — Taxpayer Bill of Rights & 2007-05-28A — Taxpayer Bill of Rights — Questions

and Answers • RC4420 Information on CRA — Service Complaints, Includes Form RC193 Service Related

Complaints Form

16

Administrative Policy Update

Newly Published Policies (Continued)• GI-025 The GST/HST and the Purchase, Use and Sale of Vacation Properties by Individuals• GI-026 Visitor Rebate Program — Accommodation Rebate for Non-Residents • GI-027 — GI-033: Foreign Convention and Tour Incentive Programs• GI-044 Foreign Convention & Tour Incentive Program Tour Packages: What is an Eligible

Package • Notice 221 Questions and Answers on the Cancellation of the Visitor Rebate Program and

the New Foreign Convention and Tour Incentive Program (August 31, 2007)• GI-034 Exports of Intangible Personal Property • GI-035 Annual Information Schedule for Financial Institutions • GI-036 Beverages • GI-037 Children's Camps Operated by Public Sector Bodies

17

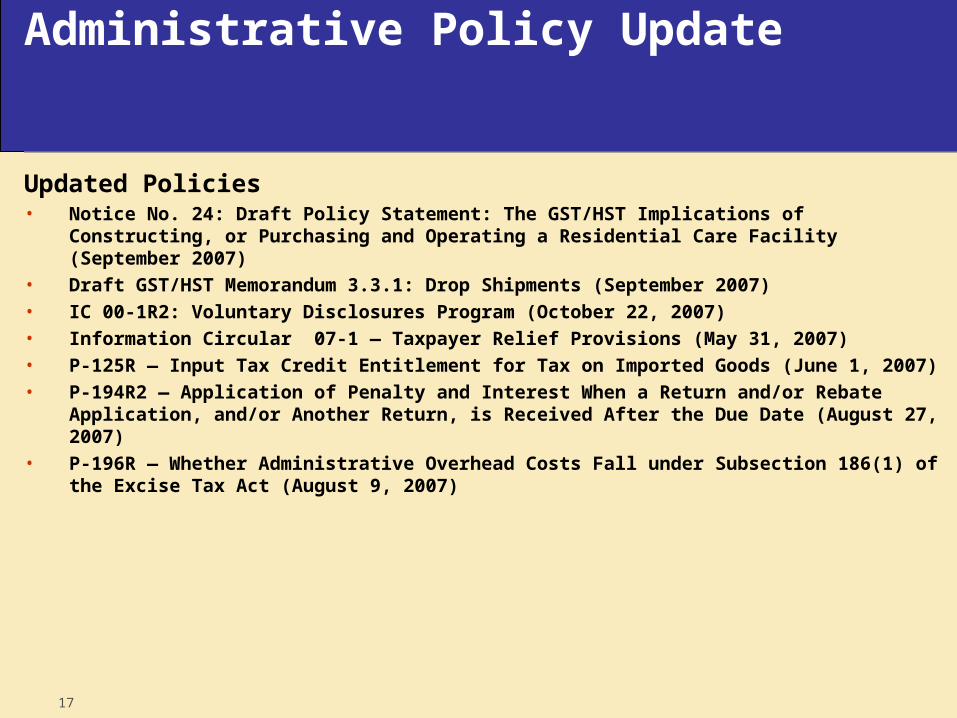

Administrative Policy UpdateAdministrative Policy Update

Updated Policies• Notice No. 24: Draft Policy Statement: The GST/HST Implications of Constructing, or

Purchasing and Operating a Residential Care Facility (September 2007)• Draft GST/HST Memorandum 3.3.1: Drop Shipments (September 2007)• IC 00-1R2: Voluntary Disclosures Program (October 22, 2007) • Information Circular 07-1 — Taxpayer Relief Provisions (May 31, 2007) • P-125R — Input Tax Credit Entitlement for Tax on Imported Goods (June 1, 2007)• P-194R2 — Application of Penalty and Interest When a Return and/or Rebate Application,

and/or Another Return, is Received After the Due Date (August 27, 2007)• P-196R — Whether Administrative Overhead Costs Fall under Subsection 186(1) of the

Excise Tax Act (August 9, 2007)

18

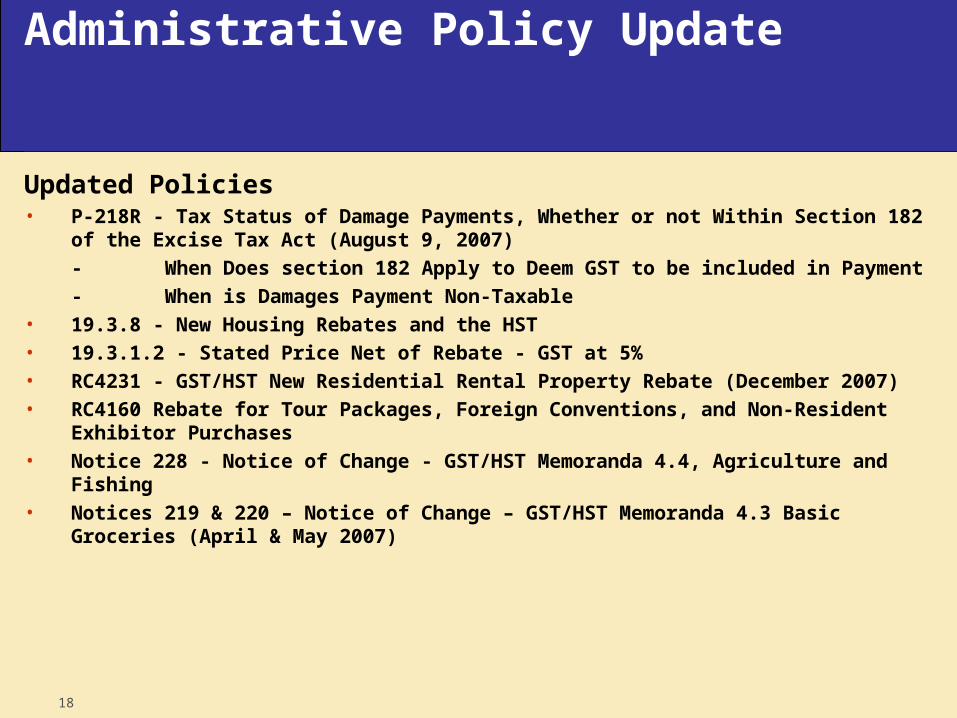

Administrative Policy Update

Updated Policies• P-218R - Tax Status of Damage Payments, Whether or not Within Section 182 of the

Excise Tax Act (August 9, 2007)

- When Does section 182 Apply to Deem GST to be included in Payment

- When is Damages Payment Non-Taxable• 19.3.8 - New Housing Rebates and the HST • 19.3.1.2 - Stated Price Net of Rebate - GST at 5% • RC4231 - GST/HST New Residential Rental Property Rebate (December 2007)• RC4160 Rebate for Tour Packages, Foreign Conventions, and Non-Resident Exhibitor

Purchases • Notice 228 - Notice of Change - GST/HST Memoranda 4.4, Agriculture and Fishing• Notices 219 & 220 – Notice of Change – GST/HST Memoranda 4.3 Basic Groceries (April &

May 2007)

19

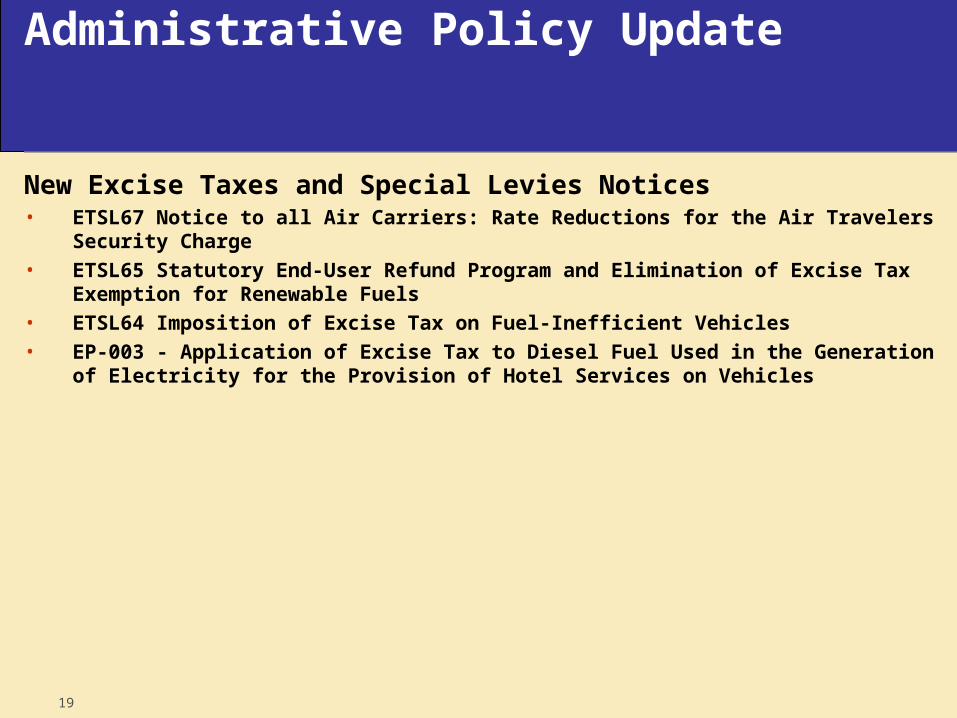

Administrative Policy UpdateAdministrative Policy Update

New Excise Taxes and Special Levies Notices• ETSL67 Notice to all Air Carriers: Rate Reductions for the Air Travelers Security Charge• ETSL65 Statutory End-User Refund Program and Elimination of Excise Tax Exemption for

Renewable Fuels• ETSL64 Imposition of Excise Tax on Fuel-Inefficient Vehicles• EP-003 - Application of Excise Tax to Diesel Fuel Used in the Generation of Electricity for

the Provision of Hotel Services on Vehicles

20

Administrative Policy Update

New Excise Taxes and Special Levies Notices - (Continued)• Form E638A: Statement of Availability or Declination From Authorized Insurers – Tax on

Insurance Premiums (Part I of the Excise Tax Act)• Form E638: Application for Exemption from Insurance Premium Taxes Imposed Under

Excise Tax Act – Part 1

• News 2008/02 - CRA - ETSL-068 — Frequently Asked Questions Regarding Part I of the Excise Tax Act

21

Most Common GST Audit Issues (GST Rulings)

1. Year End ITC Adjustments (s. 236 Meals & Entertainment)

2. Bad debts (s. 231)

3. ITC Documentation

4. ITC Allocation Methods (Financial Service Providers)

5. Proof of Exports to Non-Residents

6. Inter-Company Transactions & ITCs being claimed by Wrong Entity

7. Clerical Errors & Accounting System Errors (Failure to Add)

8. GST on Additional Rent Paid by Tenants

9. Foreign Currency Translations

22

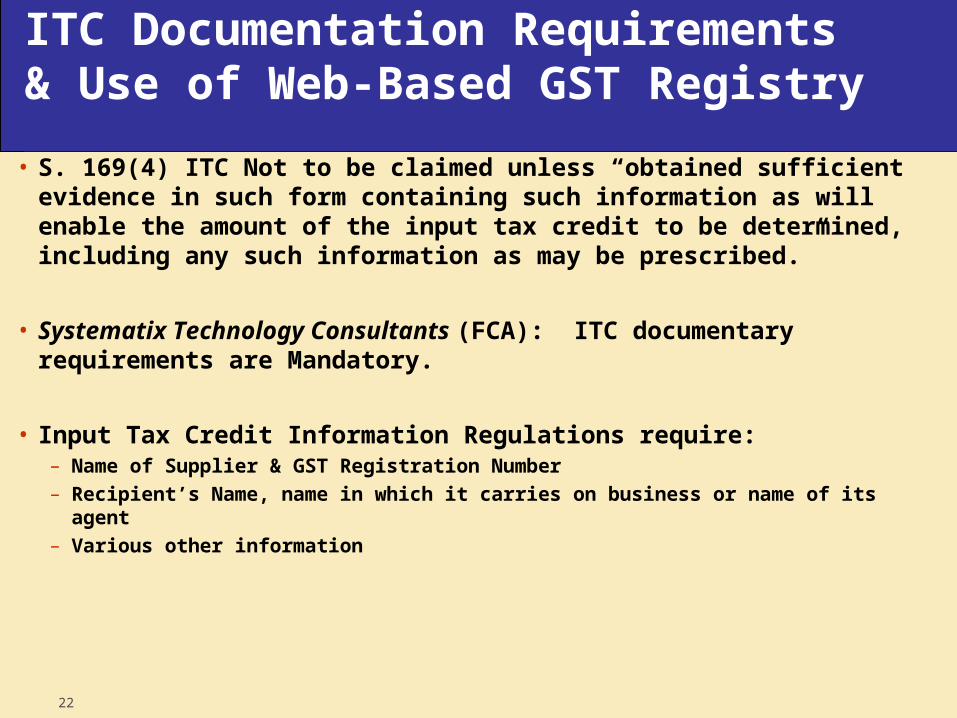

ITC Documentation Requirements & Use of Web-Based GST Registry

• S. 169(4) ITC Not to be claimed unless “obtained sufficient evidence in such form containing such information as will enable the amount of the input tax credit to be determined, including any such information as may be prescribed.”

• Systematix Technology Consultants (FCA): ITC documentary requirements are Mandatory.

• Input Tax Credit Information Regulations require:– Name of Supplier & GST Registration Number– Recipient’s Name, name in which it carries on business or name of its agent– Various other information

23

ITC Documentation Requirements & Use of Web-Based GST Registry

• GST Web-based GST Registry enables you to confirm supplier’s GST registration number

• Confirmation should be maintained on file & Periodically Verified

• GST should not be paid if supplier not registered & has not provided sufficient ITC Documentation

• Prior to GST Registry– Ribkoff: ITC available Registration Number Seemingly Belongs to Supplier– Pointe Claire: Unless CRA provides Verification Mechanism ITC is valid where GST Number is

Invalid

• Owraki Decision: Relevant time for documentation is at time of claiming, Not at time of Audit (but onus is on ITC Claimant)

24

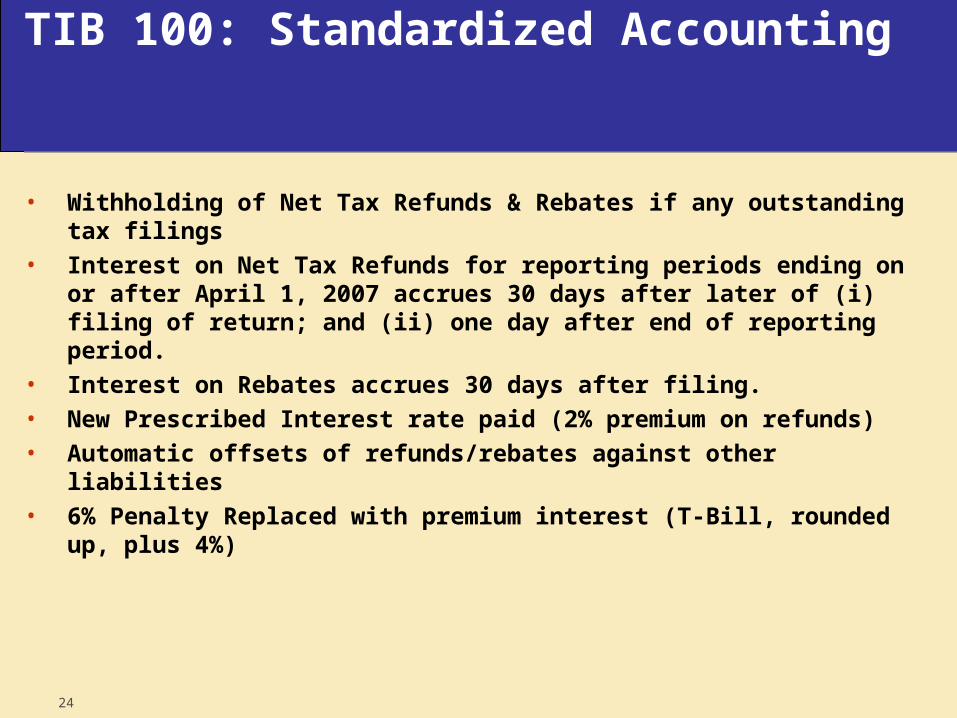

TIB 100: Standardized AccountingTIB 100: Standardized Accounting

• Withholding of Net Tax Refunds & Rebates if any outstanding tax filings

• Interest on Net Tax Refunds for reporting periods ending on or after April 1, 2007 accrues 30 days after later of (i) filing of return; and (ii) one day after end of reporting period.

• Interest on Rebates accrues 30 days after filing.• New Prescribed Interest rate paid (2% premium on refunds)• Automatic offsets of refunds/rebates against other liabilities• 6% Penalty Replaced with premium interest (T-Bill, rounded up, plus

4%)

25

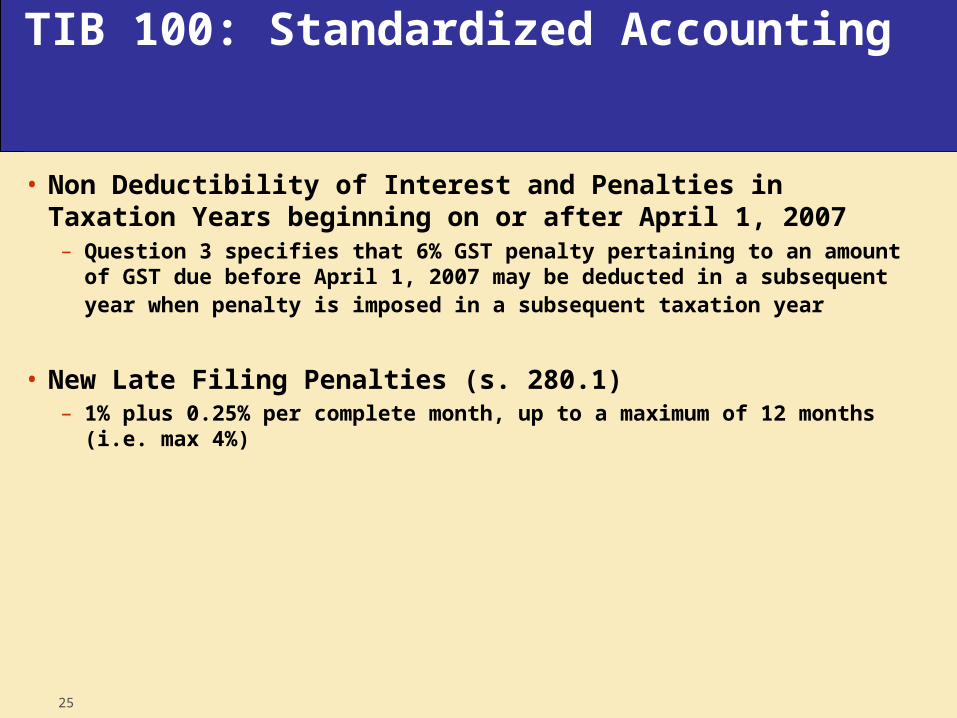

TIB 100: Standardized Accounting

• Non Deductibility of Interest and Penalties in Taxation Years beginning on or after April 1, 2007– Question 3 specifies that 6% GST penalty pertaining to an amount of GST due

before April 1, 2007 may be deducted in a subsequent year when penalty is imposed in a subsequent taxation year

• New Late Filing Penalties (s. 280.1)– 1% plus 0.25% per complete month, up to a maximum of 12 months (i.e. max 4%)

26

TIB 100: Standardized Accounting

• Wash Transaction Policy (Waive interest in excess of 4% of tax amount)

• Due Diligence for New Late Filing Penalty but not premium interest

• 12 Frequently Asked Questions– Notice of Assessment issued when refunds withheld– Intentionally filing Nil returns to avoid late filing penalties may result in gross

negligence penalties

27

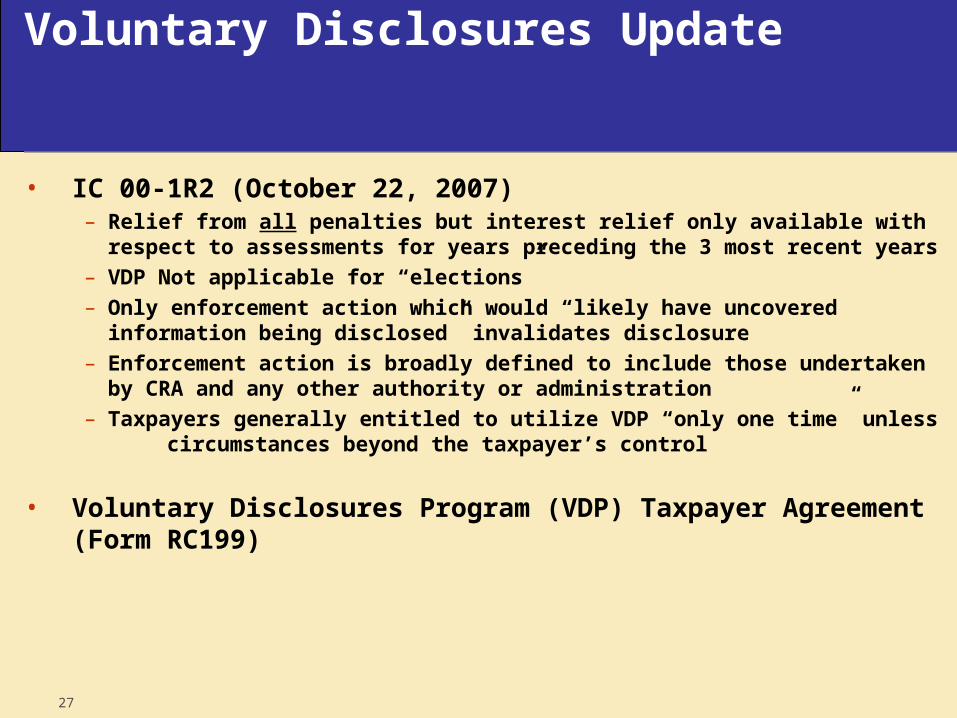

Voluntary Disclosures UpdateVoluntary Disclosures Update

• IC 00-1R2 (October 22, 2007)– Relief from all penalties but interest relief only available with respect to

assessments for years preceding the 3 most recent years– VDP Not applicable for “elections”– Only enforcement action which would “likely have uncovered information being

disclosed” invalidates disclosure– Enforcement action is broadly defined to include those undertaken by CRA and

any other authority or administration– Taxpayers generally entitled to utilize VDP “only one time” unless

circumstances beyond the taxpayer’s control

• Voluntary Disclosures Program (VDP) Taxpayer Agreement (Form RC199)

28

Voluntary Disclosures Update

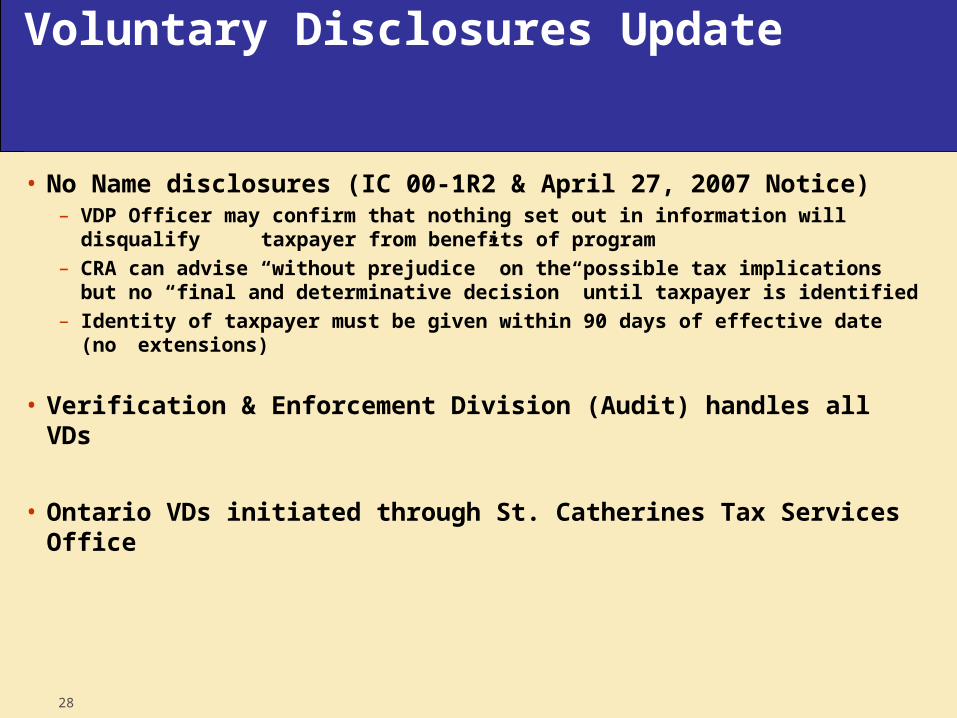

• No Name disclosures (IC 00-1R2 & April 27, 2007 Notice)– VDP Officer may confirm that nothing set out in information will disqualify

taxpayer from benefits of program– CRA can advise “without prejudice” on the possible tax implications but no “final

and determinative decision” until taxpayer is identified– Identity of taxpayer must be given within 90 days of effective date (no

extensions)

• Verification & Enforcement Division (Audit) handles all VDs

• Ontario VDs initiated through St. Catherines Tax Services Office

29

Voluntary Disclosures Update

• Standardized Accounting will significantly reduce number of VDs– No 6% Penalty post April 1, 2007– Penalty must be payable to initiate valid disclosure– CRA’s refusal to waive premium interest and 4% interest for wash transactions

• Assessments should be Requested where Recipient entitled to claim ITCs & period covered by disclosure extends beyond 4 years (extends ITC claim period

• No Positive Obligation to initiate Voluntary Disclosure

• VD Jurisprudence of Note:- Karia 2005 FC 639; Wong 2007 FC 628 & Palonek 2007 FCA 281

30

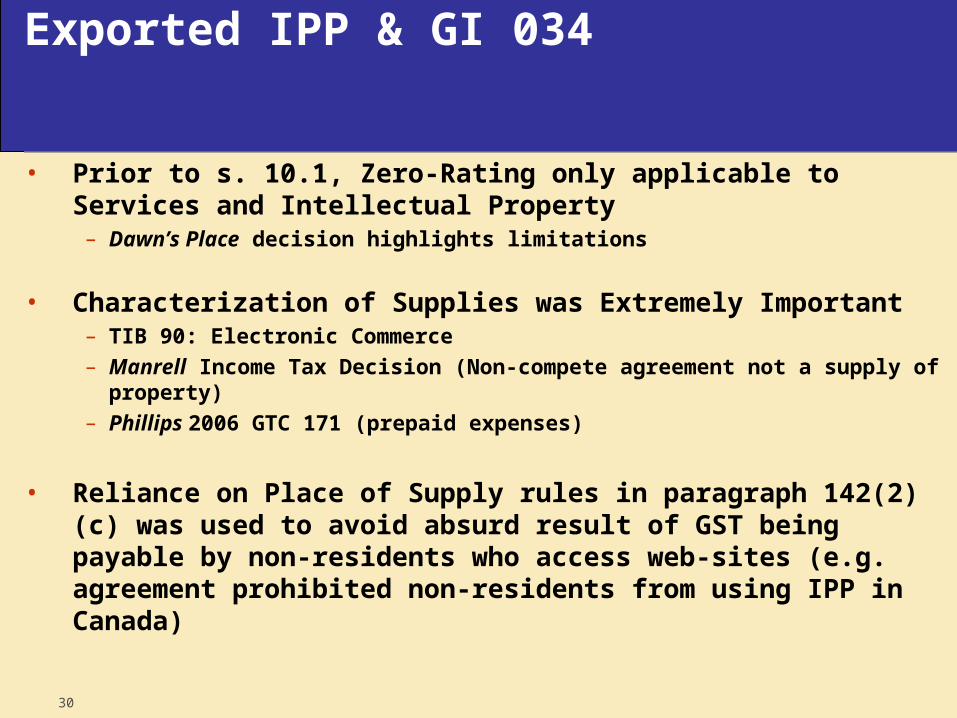

Exported IPP & GI 034Exported IPP & GI 034

• Prior to s. 10.1, Zero-Rating only applicable to Services and Intellectual Property – Dawn’s Place decision highlights limitations

• Characterization of Supplies was Extremely Important– TIB 90: Electronic Commerce– Manrell Income Tax Decision (Non-compete agreement not a supply of property)– Phillips 2006 GTC 171 (prepaid expenses)

• Reliance on Place of Supply rules in paragraph 142(2)(c) was used to avoid absurd result of GST being payable by non-residents who access web-sites (e.g. agreement prohibited non-residents from using IPP in Canada)

31

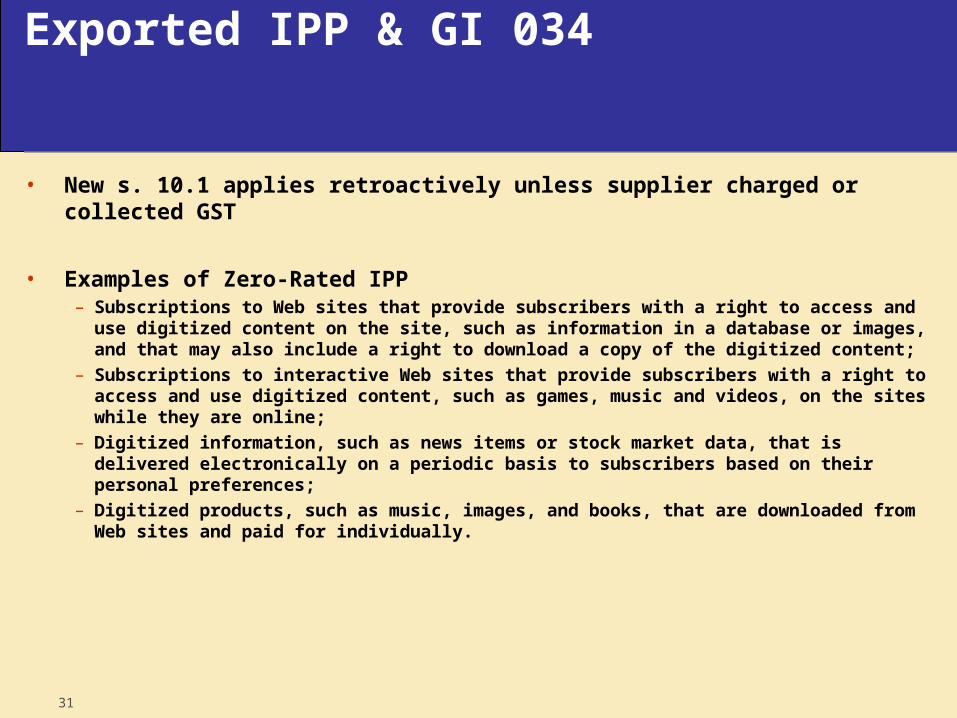

Exported IPP & GI 034Exported IPP & GI 034

• New s. 10.1 applies retroactively unless supplier charged or collected GST

• Examples of Zero-Rated IPP– Subscriptions to Web sites that provide subscribers with a right to access and use

digitized content on the site, such as information in a database or images, and that may also include a right to download a copy of the digitized content;

– Subscriptions to interactive Web sites that provide subscribers with a right to access and use digitized content, such as games, music and videos, on the sites while they are online;

– Digitized information, such as news items or stock market data, that is delivered electronically on a periodic basis to subscribers based on their personal preferences;

– Digitized products, such as music, images, and books, that are downloaded from Web sites and paid for individually.

32

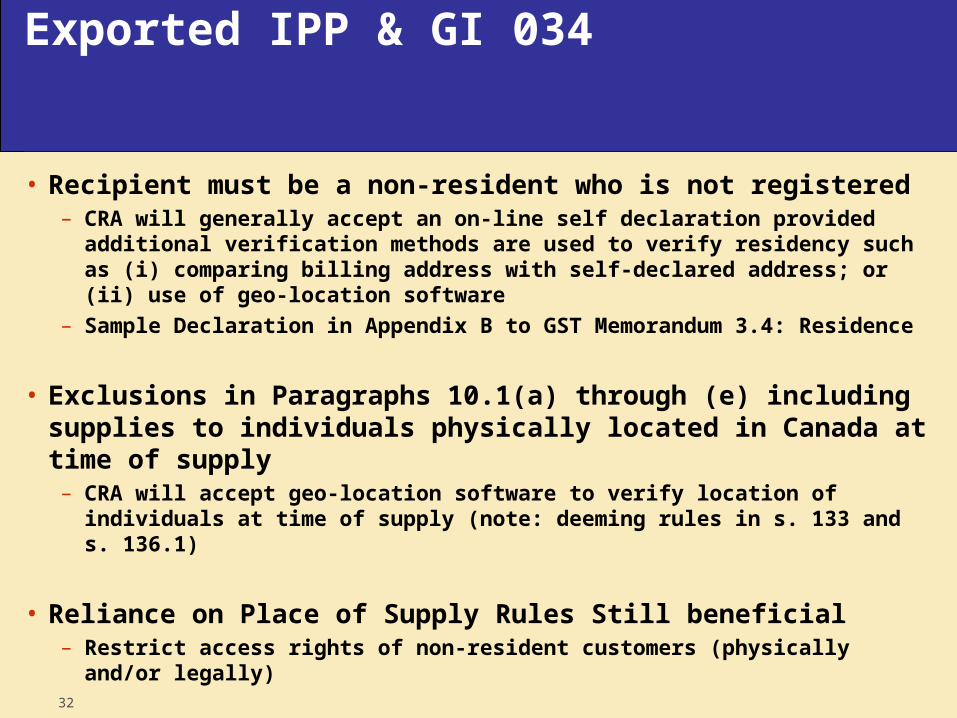

Exported IPP & GI 034

• Recipient must be a non-resident who is not registered– CRA will generally accept an on-line self declaration provided additional verification

methods are used to verify residency such as (i) comparing billing address with self-declared address; or (ii) use of geo-location software

– Sample Declaration in Appendix B to GST Memorandum 3.4: Residence

• Exclusions in Paragraphs 10.1(a) through (e) including supplies to individuals physically located in Canada at time of supply – CRA will accept geo-location software to verify location of individuals at time of

supply (note: deeming rules in s. 133 and s. 136.1)

• Reliance on Place of Supply Rules Still beneficial– Restrict access rights of non-resident customers (physically and/or legally)

33

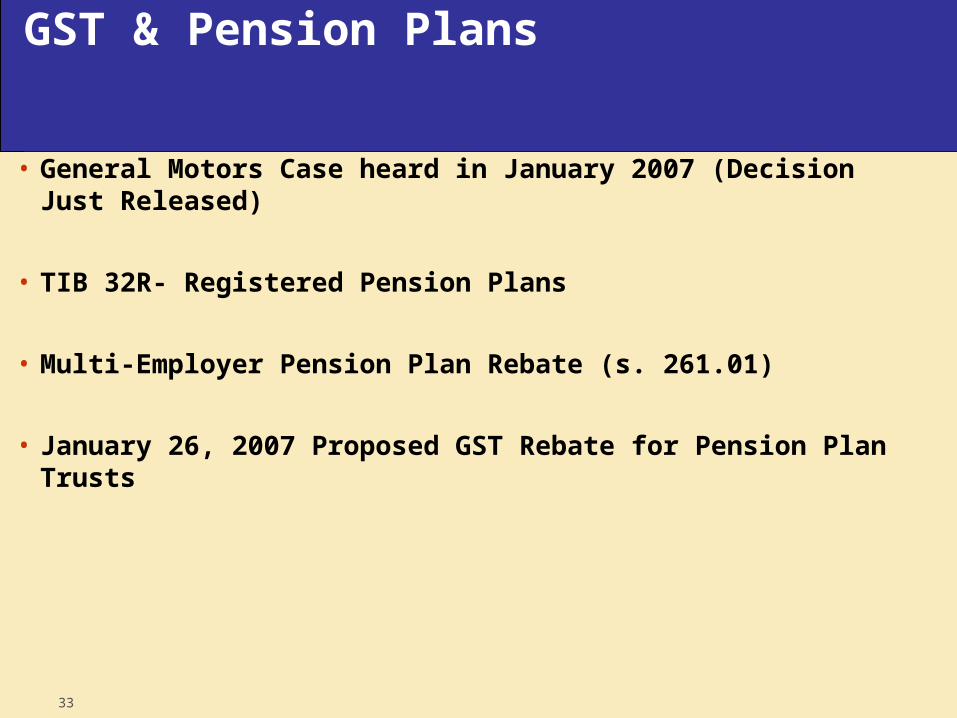

GST & Pension Plans

• General Motors Case heard in January 2007 (Decision Just Released)

• TIB 32R- Registered Pension Plans

• Multi-Employer Pension Plan Rebate (s. 261.01)

• January 26, 2007 Proposed GST Rebate for Pension Plan Trusts

34

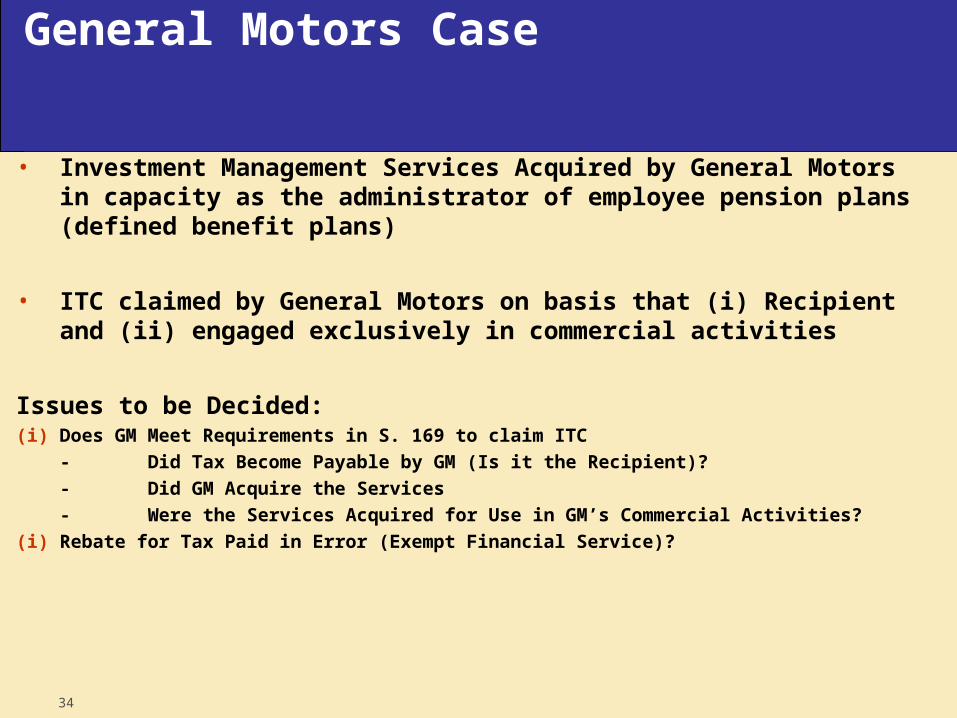

General Motors Case

• Investment Management Services Acquired by General Motors in capacity as the administrator of employee pension plans (defined benefit plans)

• ITC claimed by General Motors on basis that (i) Recipient and (ii) engaged exclusively in commercial activities

Issues to be Decided:(i) Does GM Meet Requirements in S. 169 to claim ITC

- Did Tax Become Payable by GM (Is it the Recipient)?

- Did GM Acquire the Services

- Were the Services Acquired for Use in GM’s Commercial Activities?

(i) Rebate for Tax Paid in Error (Exempt Financial Service)?

35

General Motors Case

• General Motors Entitled to Claim ITCs– GM acquired Investment management Services (s.267.1 not applicable)– GM is recipient (person contractually liable to pay tax)– Services acquired for use “in the Course of Commercial Activities of” GM.

• “In the Course of” only requires the Smallest Connection• Defined Benefit Plan so GM liable for any pension plan financial short

falls “and the only person that can use the services”• Profitable Pension Plan furthers GM’s Capacity to complete in the

Market• Obiter Comments on GST Status of Discretionary Investment

Management & Services– Not an Exempt Financial Service

36

TIB 32R: Registered Pension Plans

• Pension Plan (Plan Trust) eligible to register if a listed FI

• Limited ITCs available to Plan Trust (Only if engaged in Commercial activity)

• Pension Plan Expenses to be Categorized into 2 Buckets:(i) Employer Expenses (establishment and administrative expenses); and

(ii) Plan Trust Expenses (investment expenses)

• ITCs available for Employer on Employer Expenses provided employer engaged in commercial activities

37

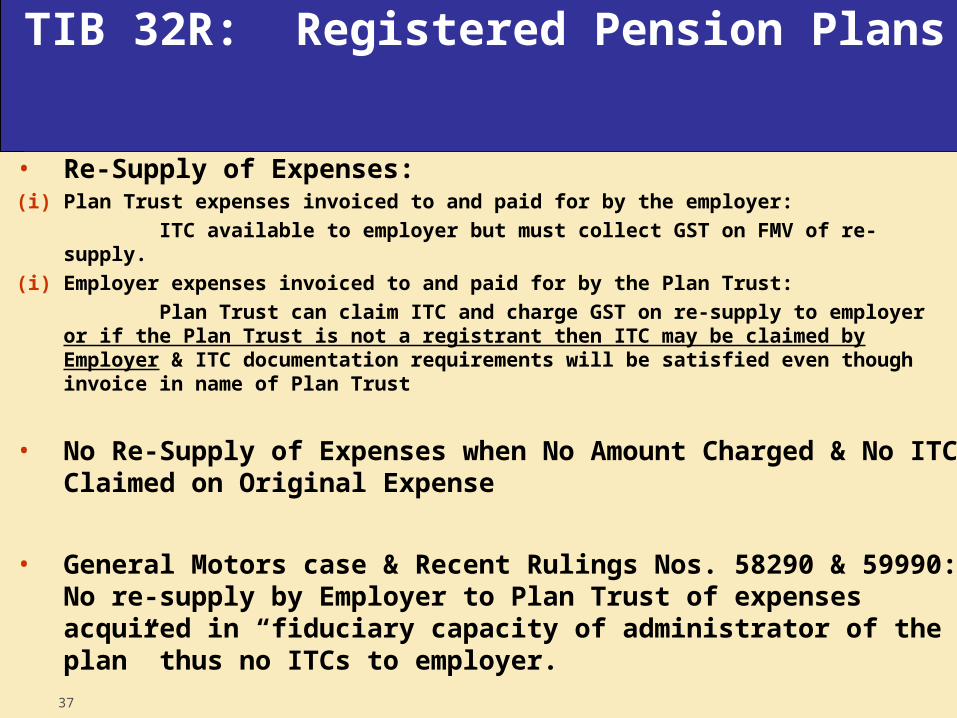

TIB 32R: Registered Pension Plans

• Re-Supply of Expenses:(i) Plan Trust expenses invoiced to and paid for by the employer:

ITC available to employer but must collect GST on FMV of re-supply.

(i) Employer expenses invoiced to and paid for by the Plan Trust:

Plan Trust can claim ITC and charge GST on re-supply to employer or if the Plan Trust is not a registrant then ITC may be claimed by Employer & ITC documentation requirements will be satisfied even though invoice in name of Plan Trust

• No Re-Supply of Expenses when No Amount Charged & No ITC Claimed on Original Expense

• General Motors case & Recent Rulings Nos. 58290 & 59990: No re-supply by Employer to Plan Trust of expenses acquired in “fiduciary capacity of administrator of the plan” thus no ITCs to employer.

38

Proposed New Rebate for Pension Plan Trusts

• Current Rules for Single Employer Pension Plans (TIB 32R) “Not Clear and may not provide Equitable Results”

• Multi-Employer Pension Plans entitled to 33% Rebate (s. 261.01) on supplies acquired “in respect of the plan”

• Single Rebate System to be implemented for all employer - sponsored pension trusts: – No requirement for Pension Plan to be registrant

– Not available if 10% of contributions are made by listed Fls

– Applies to all pension related expenses (administrative & investment)

– 33% rebate for all expenses

– ITCs available to employer for all pension related expenses but deemed resupply and collection of GST

39

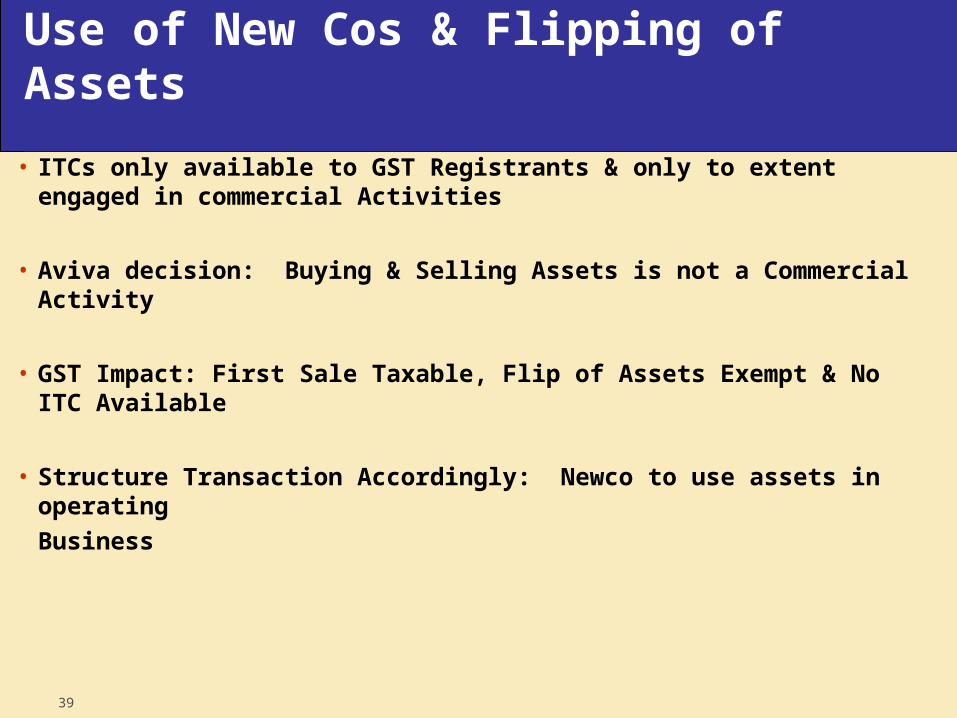

Use of New Cos & Flipping of Assets

• ITCs only available to GST Registrants & only to extent engaged in commercial Activities

• Aviva decision: Buying & Selling Assets is not a Commercial Activity

• GST Impact: First Sale Taxable, Flip of Assets Exempt & No ITC Available

• Structure Transaction Accordingly: Newco to use assets in operating

Business

40

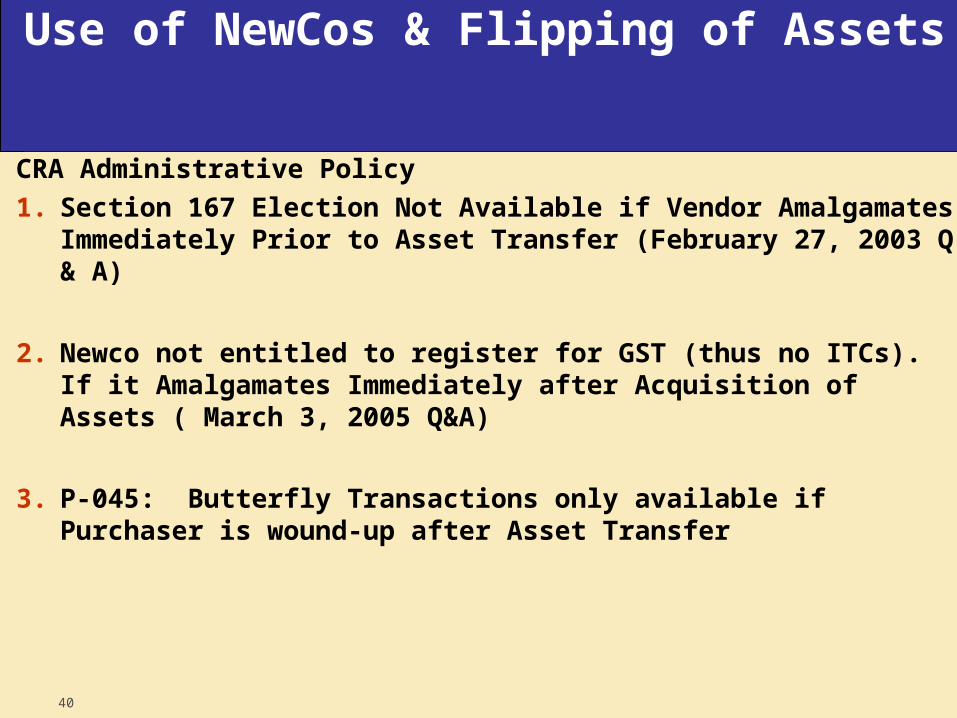

Use of NewCos & Flipping of Assets

CRA Administrative Policy

1. Section 167 Election Not Available if Vendor Amalgamates Immediately Prior to Asset Transfer (February 27, 2003 Q & A)

2. Newco not entitled to register for GST (thus no ITCs). If it Amalgamates Immediately after Acquisition of Assets ( March 3, 2005 Q&A)

3. P-045: Butterfly Transactions only available if Purchaser is wound-up after Asset Transfer

41

Special Remittance Rule for Real Property• s. 221(2) - Vendor not to collect GST where supply is sale and

either:a) The vendor is a non-resident; or

b) The purchaser is registered and the property is not a residential complex supplied to an individual (i.e., most business acquisitions)

• s. 228 (4) Purchaser's obligationsa) Self-assess on regular return, or

b) File form GST 60

• Risks to Vendor if Purchaser not registered

42

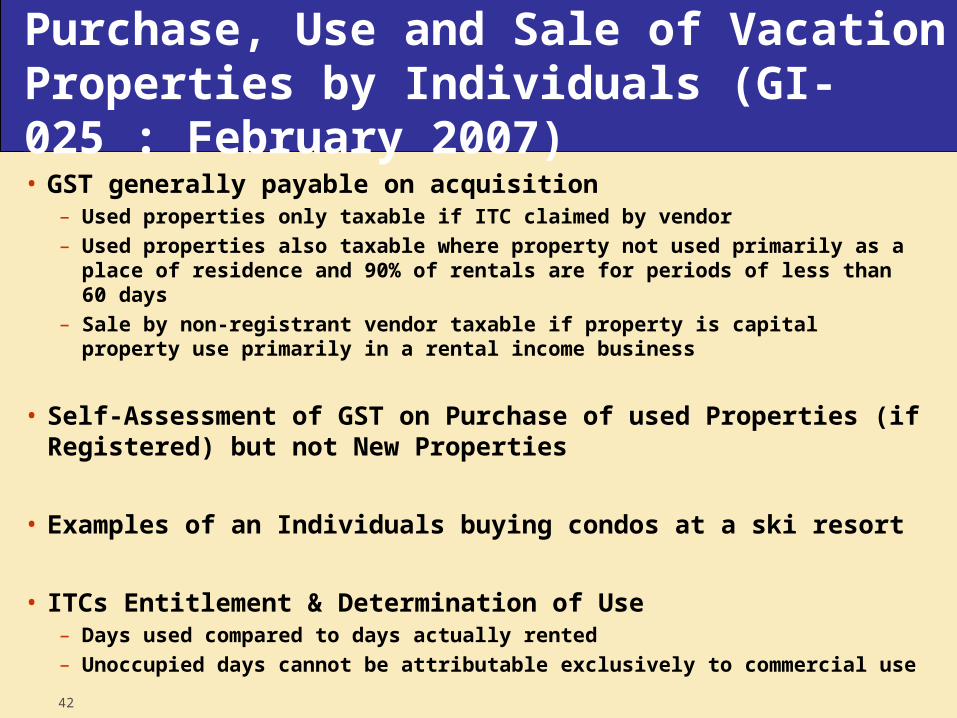

Purchase, Use and Sale of Vacation Properties by Individuals (GI-025 : February 2007)

• GST generally payable on acquisition– Used properties only taxable if ITC claimed by vendor– Used properties also taxable where property not used primarily as a place of

residence and 90% of rentals are for periods of less than 60 days– Sale by non-registrant vendor taxable if property is capital property use primarily

in a rental income business

• Self-Assessment of GST on Purchase of used Properties (if Registered) but not New Properties

• Examples of an Individuals buying condos at a ski resort

• ITCs Entitlement & Determination of Use– Days used compared to days actually rented– Unoccupied days cannot be attributable exclusively to commercial use

43

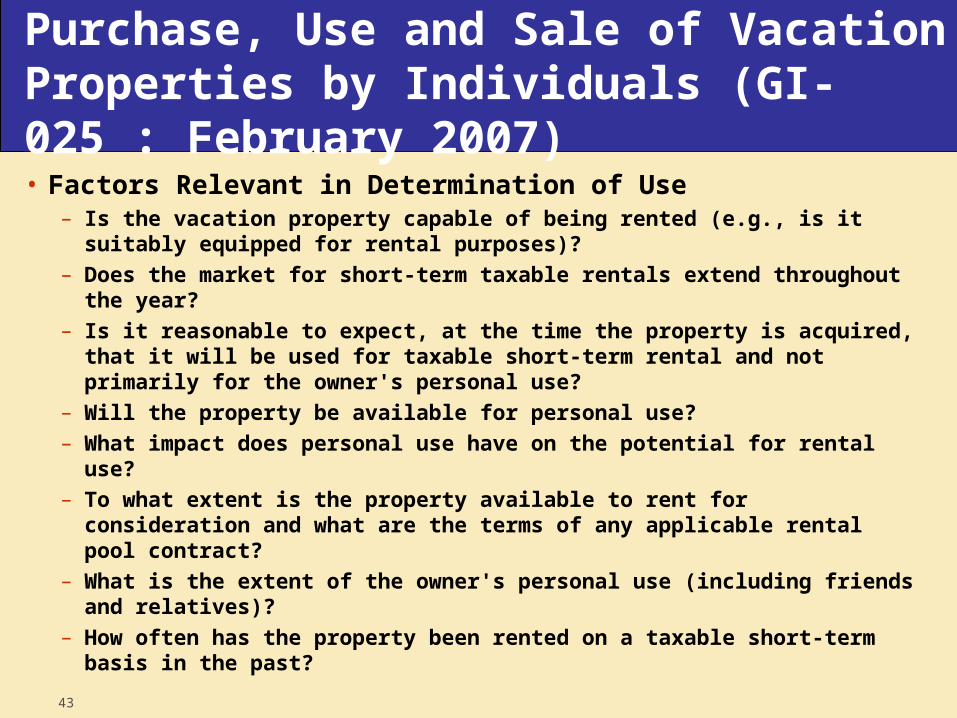

Purchase, Use and Sale of Vacation Properties by Individuals (GI-025 : February 2007)

• Factors Relevant in Determination of Use– Is the vacation property capable of being rented (e.g., is it suitably equipped for

rental purposes)?– Does the market for short-term taxable rentals extend throughout the year?– Is it reasonable to expect, at the time the property is acquired, that it will be used

for taxable short-term rental and not primarily for the owner's personal use?– Will the property be available for personal use?– What impact does personal use have on the potential for rental use?– To what extent is the property available to rent for consideration and what are the

terms of any applicable rental pool contract?– What is the extent of the owner's personal use (including friends and relatives)?– How often has the property been rented on a taxable short-term basis in the past?

44

Part I Excise Tax on Insurance Premiums from Unlicensed Insurers

• Old Tax with Increasing CRA Focus

• 10% Tax Levied on Canadian Residents by whom or on whose behalf Insurance is placed with Unlicensed Insurers (e.g. Global Parent obtaining insurance for Group of Companies from U.S. Insurer)

• Insured to File Return by April 30th of following year

• Broker/Agent assisting in placing insurance to file return by March 15th

• Exemption “to the extent that the insurance is not, in the opinion of the Commissioner, available within Canada” – To be supported by 5 letters of declination and/or Form E638A

45

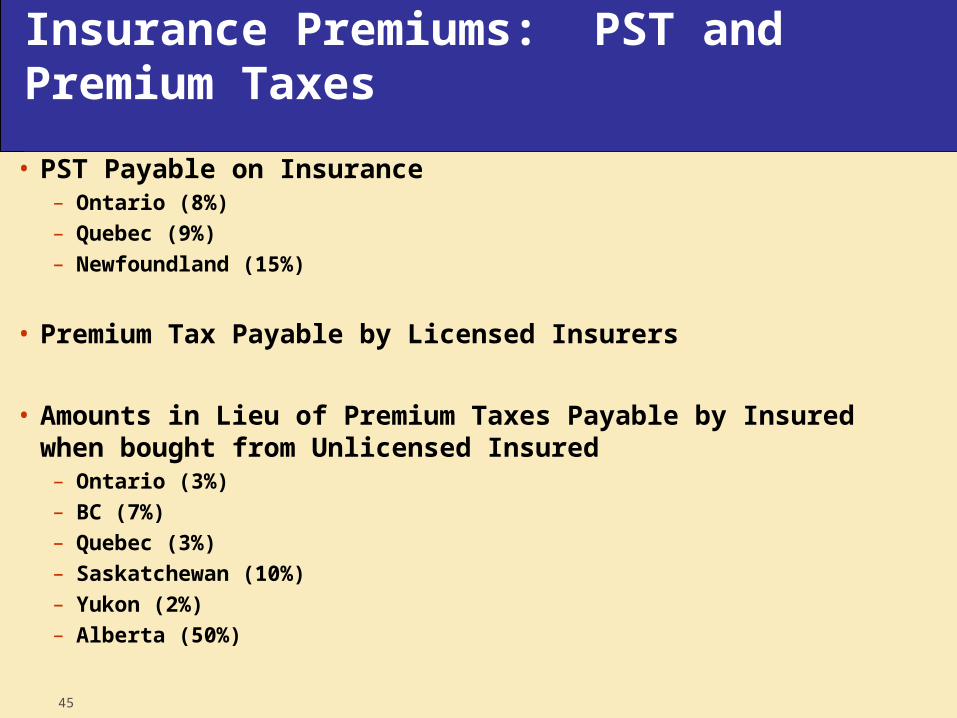

Insurance Premiums: PST and Premium Taxes

• PST Payable on Insurance– Ontario (8%)– Quebec (9%)– Newfoundland (15%)

• Premium Tax Payable by Licensed Insurers

• Amounts in Lieu of Premium Taxes Payable by Insured when bought from Unlicensed Insured– Ontario (3%)– BC (7%)– Quebec (3%)– Saskatchewan (10%)– Yukon (2%)– Alberta (50%)