gs report ofs jan 2010

TRANSCRIPT

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 1/37

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 2/37

January 7, 2010 Americas: Energy: Oil Services

Goldman Sachs Global Investment Research 2

Table of contents

2010 outlook: firing on all cylinders; favor structural winners, both “oily” and “gassy” 3

(1) Drilling activity is on an upswing globally – budgets suggest +10% growth with $70 oil 7(2) Pricing power (and growth) passes to the service companies from the offshore drillers 11

(3) Increasing service intensity is key – advantage goes to diversified service companies 13

North America – Increased activity in the shales will drive service intensity 13

International – Service intensity on the rise driven by increased offshore and reservoir complexity 17

Views on the stocks: Favor structural winners, both “oily” and “gassy” 19

Halliburton: Upgrading to Conviction Buy from Neutral 19

Cameron International: Downgrading to Neutral from Conviction Buy 21

Basic Energy: Downgrading to Sell from Neutral: Well-servicing is structurally disadvantaged 24

Nabors: Upgrading to Neutral from Sell 24

Tenaris (CL Buy) remains a Conviction List favorite 25

Schlumberger (Buy) continues to be a leading international franchise 26

Offshore Drillers: Ensco, Noble and Transocean are Buy-rated favorites 26

Appendix 1: E&P capex announcements 28

Appendix 2: Stock performance 29

Appendix 3: Stock price performance while on Investment Lists 31

Disclosures 34

The prices in the body of this report are based on the market close of January 6, 2010.

We would like to thank Kapil Chauhan for his contribution to this report.

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 3/37

January 7, 2010 Americas: Energy: Oil Services

Goldman Sachs Global Investment Research 3

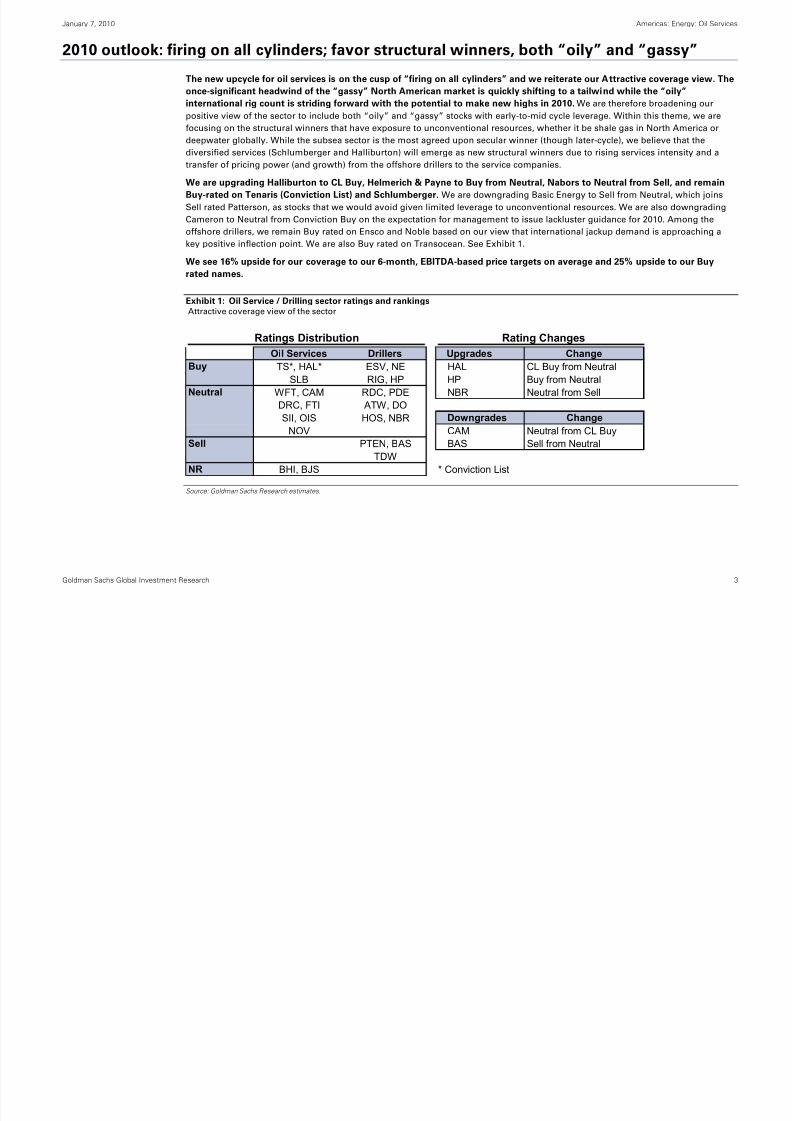

2010 outlook: firing on all cylinders; favor structural winners, both “oily” and “gassy”

The new upcycle for oil services is on the cusp of “firing on all cylinders” and we reiterate our Attractive coverage view. The

once-significant headwind of the “gassy” North American market is quickly shifting to a tailwind while the “oily”

international rig count is striding forward with the potential to make new highs in 2010. We are therefore broadening ourpositive view of the sector to include both “oily” and “gassy” stocks with early-to-mid cycle leverage. Within this theme, we are

focusing on the structural winners that have exposure to unconventional resources, whether it be shale gas in North America or

deepwater globally. While the subsea sector is the most agreed upon secular winner (though later-cycle), we believe that the

diversified services (Schlumberger and Halliburton) will emerge as new structural winners due to rising services intensity and a

transfer of pricing power (and growth) from the offshore drillers to the service companies.

We are upgrading Halliburton to CL Buy, Helmerich & Payne to Buy from Neutral, Nabors to Neutral from Sell, and remain

Buy-rated on Tenaris (Conviction List) and Schlumberger. We are downgrading Basic Energy to Sell from Neutral, which joins

Sell rated Patterson, as stocks that we would avoid given limited leverage to unconventional resources. We are also downgradingCameron to Neutral from Conviction Buy on the expectation for management to issue lackluster guidance for 2010. Among the

offshore drillers, we remain Buy rated on Ensco and Noble based on our view that international jackup demand is approaching a

key positive inflection point. We are also Buy rated on Transocean. See Exhibit 1.

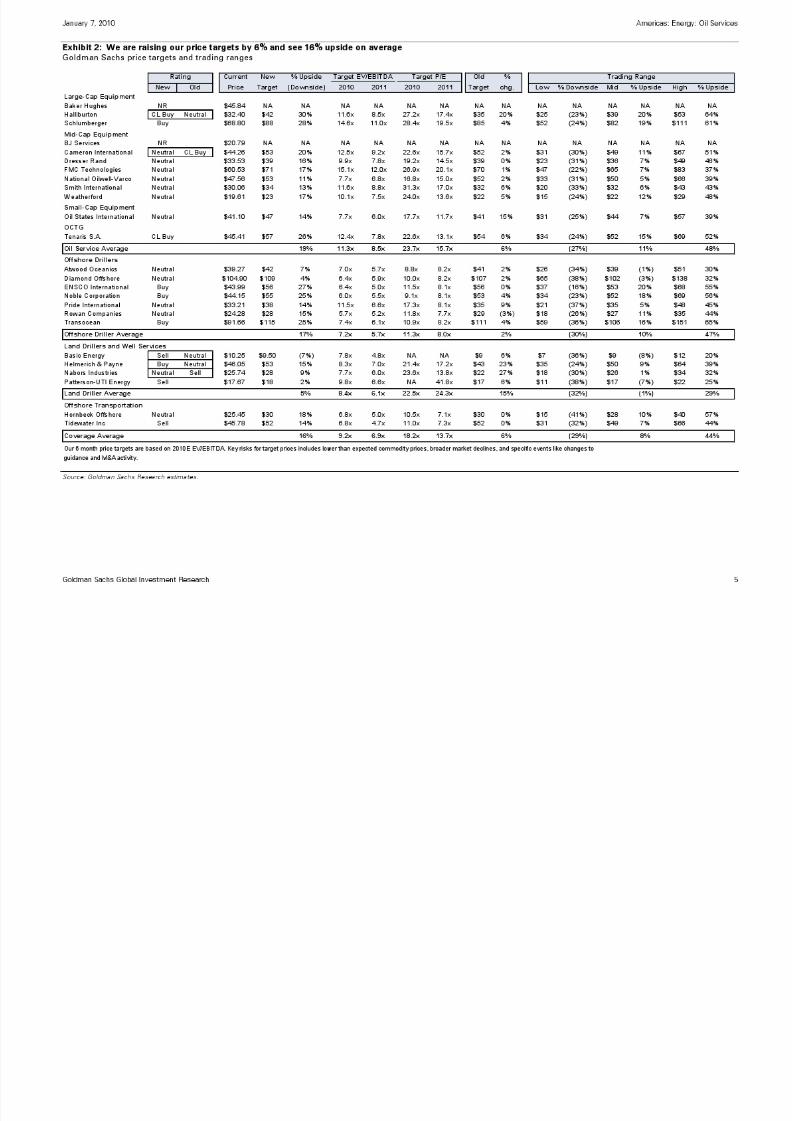

We see 16% upside for our coverage to our 6-month, EBITDA-based price targets on average and 25% upside to our Buy

rated names.

Exhibit 1: Oil Service / Drilling sector ratings and rankings

Attractive coverage view of the sector

Ratings Distribution Rating Changes

Oil Services Drillers Upgrades Change

Buy TS*, HAL* ESV, NE HAL CL Buy from Neutral

SLB RIG, HP HP Buy from Neutral

Neutral WFT, CAM RDC, PDE NBR Neutral from Sell

DRC, FTI ATW, DO

SII, OIS HOS, NBR Downgrades ChangeNOV CAM Neutral from CL Buy

Sell PTEN, BAS BAS Sell from Neutral

TDW

NR BHI, BJS * Conviction List

Source: Goldman Sachs Research estimates.

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 4/37

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 5/37

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 6/37

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 7/37

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 8/37

January 7, 2010 Americas: Energy: Oil Services

Goldman Sachs Global Investment Research 8

Exhibit 4: Accelerating activity should lead to the return of pricing power…International and US horizontal rig count months after the peak

Exhibit 5: …as higher budgets continue to call for more drillingRecently announced 2010 spending plans for select companies ($ in mm)

(45%)

(40%)

(35%)

(30%)

(25%)

(20%)

(15%)

(10%)

(5%)

0%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

Months after the peak (% change in rig count)

US horizontal rig count International rig count

… while the

horizontal drilling inthe US is only 12%

below the peak...

The international rig count isapproaching peak drilling

activity...

…which indicates higher E&P

capex and the return of pricingpower to oil service companiesstarting with the international

markets as service capacitytightens

+ 53%

+ 8%

Announced International E&P Capex Budgets

2009E 2010E % Chg.

Chevron(1)

$11,600 $13,200 14%

ConocoPhillips(2)

6,950 5,600 (19%)Ecopetrol 3,764 4,509 20%Pemex 16,177 17,197 6%TNK-BP 3,000 3,400 13%All others that annouced budgets thus far 7,285 9,809 35%Total $48,776 $53,715 10%

Announced North America E&P Capex Budgets

2009E 2010E % Chg.

Chesapeake(3)

$3,388 $4,688 38%Chevron 3,600 4,100 14%

ConocoPhillips 3,300 4,100 24%Devon 3,300 3,925 19%All others that annouced budgets thus far 7,774 9,616 24%Total $21,362 $26,429 24%

(1) 2009 CVX international capex excludes $2.3 billion extenstion of concession payment which we view to be

non-activity related.

(2) ConocoPhillips is in the process of divesting a portion of its international assets making year-on-year comparisons difficult.

(3) Drilling and geophysical capex only.

Source: Baker Hughes, Goldman Sachs Research. Source: Company data, Platts, Goldman Sachs Research.

Exhibit 6: The industry is set to increase major project sanctioning

Top230 oil and gas reserves that maturing to the FID each year

Exhibit 7: We expect continued reacceleration in the rig count

Goldman Sachs Baker Hughes North America and International rig count forecast

0

5,000

10,000

15,000

20,000

25,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

mn b

oe

$0

$20

$40

$60

$80

$100

$120

US$/

bbl

Oil Gas Oil price (GS estimates post 2008)

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

1

Q07A

2

Q07A

3

Q07A

4

Q07A

1

Q08A

2

Q08A

3

Q08A

4

Q08A

1

Q09A

2

Q09A

3

Q09A

4

Q09E

1

Q10E

2

Q10E

3

Q10E

4

Q10E

1

Q11E

2

Q11E

3

Q11E

4

Q11E

North America rig count

900

950

1,000

1,050

1,100

1,150

1,200

1,250

1,300

International rig count

North America InternationalForecast

Source: Goldman Sachs Research Top230 Projects report. Source: Baker Hughes, Goldman Sachs Research.

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 9/37

January 7, 2010 Americas: Energy: Oil Services

Goldman Sachs Global Investment Research 9

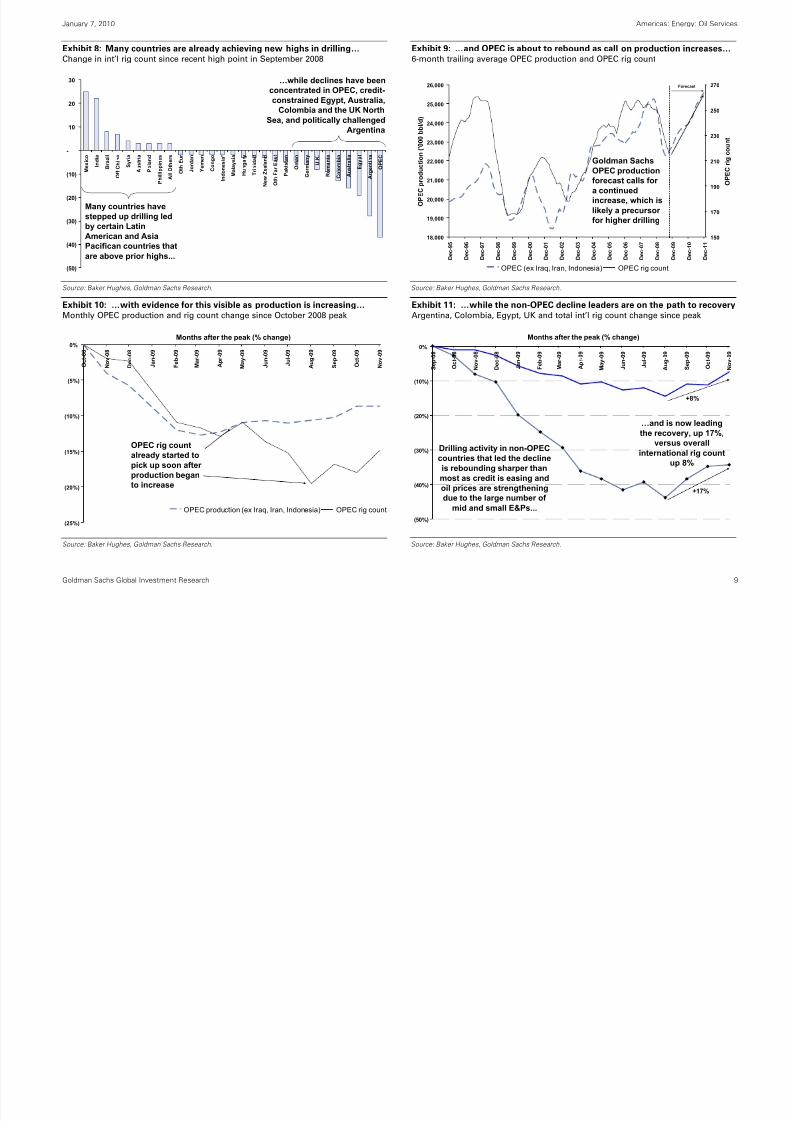

Exhibit 8: Many countries are already achieving new highs in drilling…Change in int’l rig count since recent high point in September 2008

Exhibit 9: …and OPEC is about to rebound as call on production increases…6-month trailing average OPEC production and OPEC rig count

(50)

(40)

(30)

(20)

(10)

-

10

20

30

Mexico

India

Brazil

Off China

Syria

Austria

Poland

Phillippines

All Others

Oth Eur

Jordan

Yemen

Congo

Indonesia*

Malaysia

Hungary

Trinidad

New Zealand

Oth Far East

Pakistan

Oman

Germany

U.K.

Romania

Colombia

Australia

Egypt

Argentina

OPEC

Many countries havestepped up drilling ledby certain LatinAmerican and AsiaPacifican countries thatare above prior highs...

…while declines have beenconcentrated in OPEC, credit-constrained Egypt, Australia,

Colombia and the UK NorthSea, and politically challenged

Argentina

18,000

19,000

20,000

21,000

22,000

23,000

24,000

25,000

26,000

Dec-95

Dec-96

Dec-97

Dec-98

Dec-99

Dec-00

Dec-01

Dec-02

Dec-03

Dec-04

Dec-05

Dec-06

Dec-07

Dec-08

Dec-09

Dec-10

Dec-11

OPEC production ('000 bbl/d)

150

170

190

210

230

250

270

OPEC rig count

OPEC (ex Iraq, Iran, Indonesia) OPEC rig count

Goldman SachsOPEC productionforecast calls for a continuedincrease, which is

likely a precursor for higher drilling

Forecast

Source: Baker Hughes, Goldman Sachs Research. Source: Baker Hughes, Goldman Sachs Research.

Exhibit 10: …with evidence for this visible as production is increasing…

Monthly OPEC production and rig count change since October 2008 peak

Exhibit 11: …while the non-OPEC decline leaders are on the path to recovery

Argentina, Colombia, Egypt, UK and total int’l rig count change since peak

(25%)

(20%)

(15%)

(10%)

(5%)

0%

Oct-08

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

Sep-09

Oct-09

Nov-09

Months after the peak (% change)

OPEC production (ex Iraq, Iran, Indonesia) OPEC rig count

OPEC rig countalready started topick up soon after production beganto increase

(50%)

(40%)

(30%)

(20%)

(10%)

0%

Sep-08

Oct-08

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

Sep-09

Oct-09

Nov-09

Months after the peak (% change)

…and is now leadingthe recovery, up 17%,

versus overallinternational rig count

up 8%

+17%

Drilling activity in non-OPECcountries that led the declineis rebounding sharper thanmost as credit is easing andoil prices are strengtheningdue to the large number of

mid and small E&Ps...

+8%

Source: Baker Hughes, Goldman Sachs Research. Source: Baker Hughes, Goldman Sachs Research.

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 10/37

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 11/37

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 12/37

January 7, 2010 Americas: Energy: Oil Services

Goldman Sachs Global Investment Research 12

Exhibit 16: Offshore rig spending will lag global spending growth in 2010/11Global Offshore spending versus strip oil prices

Exhibit 17: Offshore rig revenues have massively outpaced service growthyoy revenue growth for service and offshore rig revenue

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Globa

l Offshore rig spending ($ millions)

$0

$20

$40

$60

$80

$100

$120

Strip oil price ($bbl)

Global offshore rig spending growth:

2006A +52%2007A +53%

2008A +31%2009E +8%2010E +0% (vs. global E&P capex growth of 10%)2011E +12% (vs. global E&P capex growth of 20%)

Strip Oil Price

Offshore rigspending

6%

14%

-9%

9%

18%

-7%

31%

52% 53%

31%

8%

0%

21%

26% 27%

20%

12%

1%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

2003A 2004A 2005A 2006A 2007A 2008A 2009E 2010E 2011E

YOY change in revenue

Big 3 - International service revenue

Offshore rig revenue, ex US GOM

Offshore rig revenues havemassively outpaced service

company growth 2005-2009

due to capacityconstraints

Service companies are

now in a better position to

out grow the "market" dueto increased rig supply

Source: Company data, ODS-Petrodata, Goldman Sachs Research estimates.

Exhibit 18: Rig shortages led to greater pricing power for offshore drillers

Offshore driller and oil service EBIT margins

Exhibit 19: Rising offshore exploration suggests higher demand for services

Tenders for seismic vessels by month in square kilometers

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

1997A 1998A 1999A 2000A 2001A 2002A 2003A 2004A 2005A 2006A 2007A 2008A 2009E 2010E 2011E

Operating M

argin

Offshore Driller

Oil Service

Oil Service: SLB, HAL, BHI

Offshore Driller: ATW, DO, ESV, NE, PDE, RDC, RIG

January

February

March

April

May

June

July

August

S

eptember

October

November

December

S

i

ze

i

n

SQ

KM

The spike in offshore seismic tendersover the past several months indicates

increased exploration activity andultimately higher demand for services

Source: Company data, Goldman Sachs Research estimates. Source: Polarcus, Goldman Sachs Research estimates.

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 13/37

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 14/37

January 7, 2010 Americas: Energy: Oil Services

Goldman Sachs Global Investment Research 14

supply, we expect the market to become OCTG constrained by mid-2010 as demand recovers, supply declines and much of the low-

end Chinese inventory is deemed unusable. This is still our favorite way to gain exposure to the recovery in North America and

Tenaris is the most compelling vehicle to gain leverage to this theme, in our view. See Exhibits 24-25.

Exhibit 20: Service intensity rig count is down just 24% from the prior high

versus 41% for the overall rig count suggesting service capacity is tighterthan initially appearsBHI rig count and BHI rig count adjusted for service intensity

Exhibit 21: Halliburton’s service intensity is driven by the growing horizontal

rig countNorth America horizontal rig count as percentage of total and HAL’s revenue perrig

500

1,000

1,500

2,000

2,500

3,000

3,500

1Q07A

2Q07A

3Q07A

4Q07A

1Q08A

2Q08A

3Q08A

4Q08A

1Q09A

2Q09A

3Q09A

4Q09E

Current

US rig count

50

150

250

350

450

550

650

750

Horizontal rig count

US rig count US rig count - Service intensity adjusted Horizontal

BHI rig count isdown 41% fromthe peak ...

... But the service intensityadjusted rig count is down

just 24% - driven by theincrease in horizontals

Horizontal

US rig count -service intensityadjusted

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

$4.5

$5.0

2001A

2002A

2003A

2004A

2005A

2006A

2007A

2008A

2009E

2010E

2011E

HAL's revenue per

rig

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Horizontal as a % of US rig count

HAL's NorthAmericarevenue/rig

Horizontalrig count

Source: Baker Hughes, Goldman Sachs Research. Source: Baker Hughes, company data, Goldman Sachs Research.

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 15/37

January 7, 2010 Americas: Energy: Oil Services

Goldman Sachs Global Investment Research 15

Exhibit 22: Barnett Shale is losing share to more service intensive shalesPercentage of horizontal rig count

Exhibit 23: “newer” shale plays can be up to 1.6X more service intensiveAnnual services opportunity per rig in each basin ($ in mm)

0%

10%

20%

30%

40%

50%

60%

Oct-08

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

Sep-09

Oct-09

Nov-09

Dec-09

Barnett Haynesville (La.) Marcellus

$18$22 $23

$25

$58$18

$24 $25

$32

$-

$10

$20

$30

$40

$50

$60

$70

Barnett- CHK Haynesvillle - CHK Fayetteville- CHK Haynesvillle - XCO Marcellus- CHK

Annual Spend ($'000,000s)

Annual Completion Spend

Annual Dilling Spend (ex rig dayrate)

1.3X more

service intensity

than the Barnett

1.3X more

service intensity

than the Barnett

1.6X more

service intensity

than the Barnett

1.6X more

service intensity

than the Barnett

Source: Land rig newsletter, Goldman Sachs Research. Source: Company data, Goldman Sachs Research.

Exhibit 24: We think consumption troughed in 3Q09 and should rise sharply

Quarterly US OCTG consumption (tons in ‘000s)

Exhibit 25: We expect inventories to enter bullish territory in late 2010

OCTG inventories vs. price ($/ton); assumes 15% of inventory is scrapped

400

600

800

1,000

1,200

1,400

1,600

1,800

1Q02

3Q02

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

Forecast

Average = ~900

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

1Q01

3Q01

1Q02

3Q02

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Prices tend to increasewhen inventories decline

below 5 months of supply,which we expect to see in

late 2010 & 2011

PipeLogix

price

Months of

supply

inventory

Source: OCTG Situation Report, Goldman Sachs Research estimates. Source: OCTG Situation Report, PipeLogix, Goldman Sachs Research estimates.

J 20 0 A i E Oil S i

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 16/37

January 7, 2010 Americas: Energy: Oil Services

Goldman Sachs Global Investment Research 16

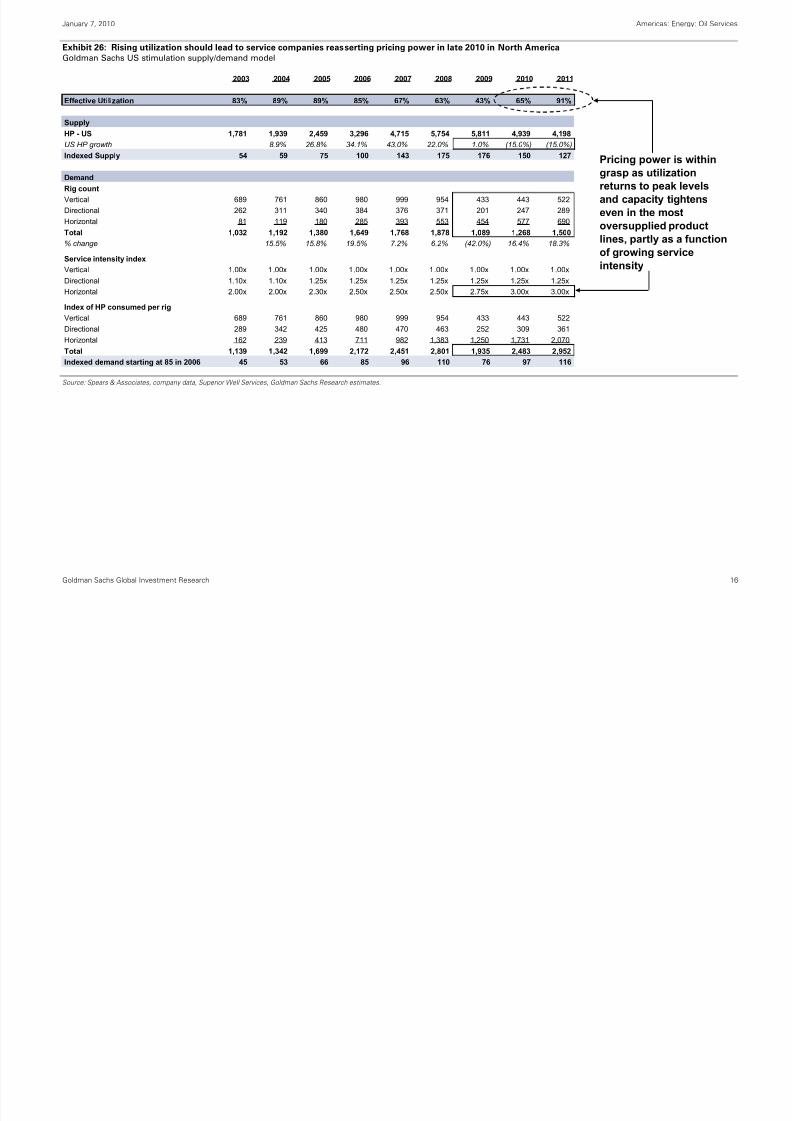

Exhibit 26: Rising utilization should lead to service companies reasserting pricing power in late 2010 in North AmericaGoldman Sachs US stimulation supply/demand model

2003 2004 2005 2006 2007 2008 2009 2010 2011

Effective Utilization 83% 89% 89% 85% 67% 63% 43% 65% 91%

Supply

HP - US 1,781 1,939 2,459 3,296 4,715 5,754 5,811 4,939 4,198

US HP growth 8.9% 26.8% 34.1% 43.0% 22.0% 1.0% (15.0%) (15.0%)

Indexed Supply 54 59 75 100 143 175 176 150 127

Demand

Rig count

Vertical 689 761 860 980 999 954 433 443 522

Directional 262 311 340 384 376 371 201 247 289Horizontal 81 119 180 285 393 553 454 577 690

Total 1,032 1,192 1,380 1,649 1,768 1,878 1,089 1,268 1,500

% change 15.5% 15.8% 19.5% 7.2% 6.2% (42.0%) 16.4% 18.3%

Service intensity index

Vertical 1.00x 1.00x 1.00x 1.00x 1.00x 1.00x 1.00x 1.00x 1.00x

Directional 1.10x 1.10x 1.25x 1.25x 1.25x 1.25x 1.25x 1.25x 1.25x

Horizontal 2.00x 2.00x 2.30x 2.50x 2.50x 2.50x 2.75x 3.00x 3.00x

Index of HP consumed per rig

Vertical 689 761 860 980 999 954 433 443 522Directional 289 342 425 480 470 463 252 309 361

Horizontal 162 239 413 711 982 1,383 1,250 1,731 2,070

Total 1,139 1,342 1,699 2,172 2,451 2,801 1,935 2,483 2,952

Indexed demand starting at 85 in 2006 45 53 66 85 96 110 76 97 116

Pricing power is within

grasp as utilizationreturns to peak levels

and capacity tightens

even in the mostoversupplied product

lines, partly as a function

of growing service

intensity

Source: Spears & Associates, company data, Superior Well Services, Goldman Sachs Research estimates.

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 17/37

January 7 2010 Americas: Energy: Oil Services

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 18/37

January 7, 2010 Americas: Energy: Oil Services

Goldman Sachs Global Investment Research 18

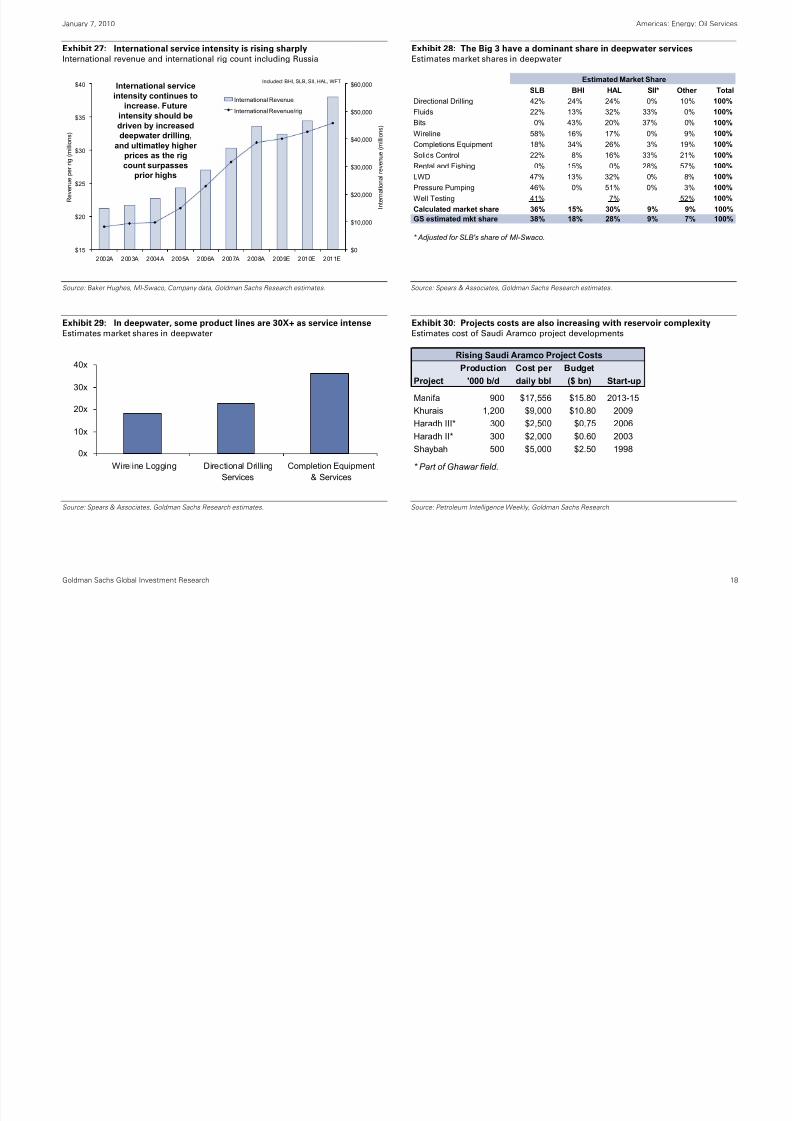

Exhibit 27: International service intensity is rising sharplyInternational revenue and international rig count including Russia

Exhibit 28: The Big 3 have a dominant share in deepwater servicesEstimates market shares in deepwater

$15

$20

$25

$30

$35

$40

2002A 2003A 2004A 2005A 2006A 2007A 2008A 2009E 2010E 2011E

Revenue per rig (millions)

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

International revenue (millions)

International Revenue

International Revenue/rig

International serviceintensity continues to

increase. Futureintensity should bedriven by increaseddeepwater drilling,

and ultimatley higher prices as the rigcount surpasses

prior highs

Included: BHI, SLB, SII, HAL, WFT Estimated Market Share

SLB BHI HAL SII* Other Total

Directional Drilling 42% 24% 24% 0% 10% 100%

Fluids 22% 13% 32% 33% 0% 100%

Bits 0% 43% 20% 37% 0% 100%

Wireline 58% 16% 17% 0% 9% 100%

Completions Equipment 18% 34% 26% 3% 19% 100%

Solids Control 22% 8% 16% 33% 21% 100%

Rental and Fishing 0% 15% 0% 28% 57% 100%

LWD 47% 13% 32% 0% 8% 100%

Pressure Pumping 46% 0% 51% 0% 3% 100%

Well Testing 41% 7% 52% 100%

Calculated market share 36% 15% 30% 9% 9% 100%

GS estimated mkt share 38% 18% 28% 9% 7% 100%

* Adjusted for SLB's share of MI-Swaco.

Source: Baker Hughes, MI-Swaco, Company data, Goldman Sachs Research estimates. Source: Spears & Associates, Goldman Sachs Research estimates.

Exhibit 29: In deepwater, some product lines are 30X+ as service intenseEstimates market shares in deepwater

Exhibit 30: Projects costs are also increasing with reservoir complexityEstimates cost of Saudi Aramco project developments

0x

10x

20x

30x

40x

Wireline Logging Directional Drilling

Services

Completion Equipment

& Services

Rising Saudi Aramco Project Costs

Production Cost per Budget

Project '000 b/d daily bbl ($ bn) Start-up

Manifa 900 $17,556 $15.80 2013-15

Khurais 1,200 $9,000 $10.80 2009

Haradh III* 300 $2,500 $0.75 2006Haradh II* 300 $2,000 $0.60 2003

Shaybah 500 $5,000 $2.50 1998

* Part of Ghawar field.

Source: Spears & Associates, Goldman Sachs Research estimates. Source: Petroleum Intelligence Weekly, Goldman Sachs Research.

January 7 2010 Americas: Energy: Oil Services

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 19/37

January 7, 2010 Americas: Energy: Oil Services

Goldman Sachs Global Investment Research 19

Views on the stocks: Favor structural winners, both “oily” and “gassy”

We are positioned in traditional early-to-mid cycle stocks which we deem to be structural winners over the course of the

cycle due to the industry’s inability to grow crude oil supply and shift towards more complex reservoirs such as shale gas.

We see 25% upside on average in our Buy-rated stocks.

Halliburton: Upgrading to Conviction Buy from Neutral

With North America finally becoming a tailwind for oil service stocks at the same time that the deepwater market is heating

up, we are upgrading Halliburton to Conviction Buy from Neutral and see 30% upside to our $42, 6-month EBITDA-based

target. Halliburton has one of the strongest franchises in North America due to its market expertise, solid execution and diverse

product lines that allow it to effectively bundle products and services. Internationally, the company is growing and executing well

with the second highest market share in the lucrative deepwater market.

As the North American market recovers, Halliburton is among the best companies to own due to its large and high quality

pressure pumping fleet which complements its other product offerings. The company’s ability to bundle these offering and to

take share has resulted in growing revenue per rig in North America and one of the best growth rates in among peers. See Exhibits

31 and 32. As the market recovers, service intensity grows, utilizations increase, and pricing power returns, Halliburton’s margins

are set to rise sharply. See Exhibit 33. In an upside case scenario, Halliburton could also continue to gain share due to its ability to

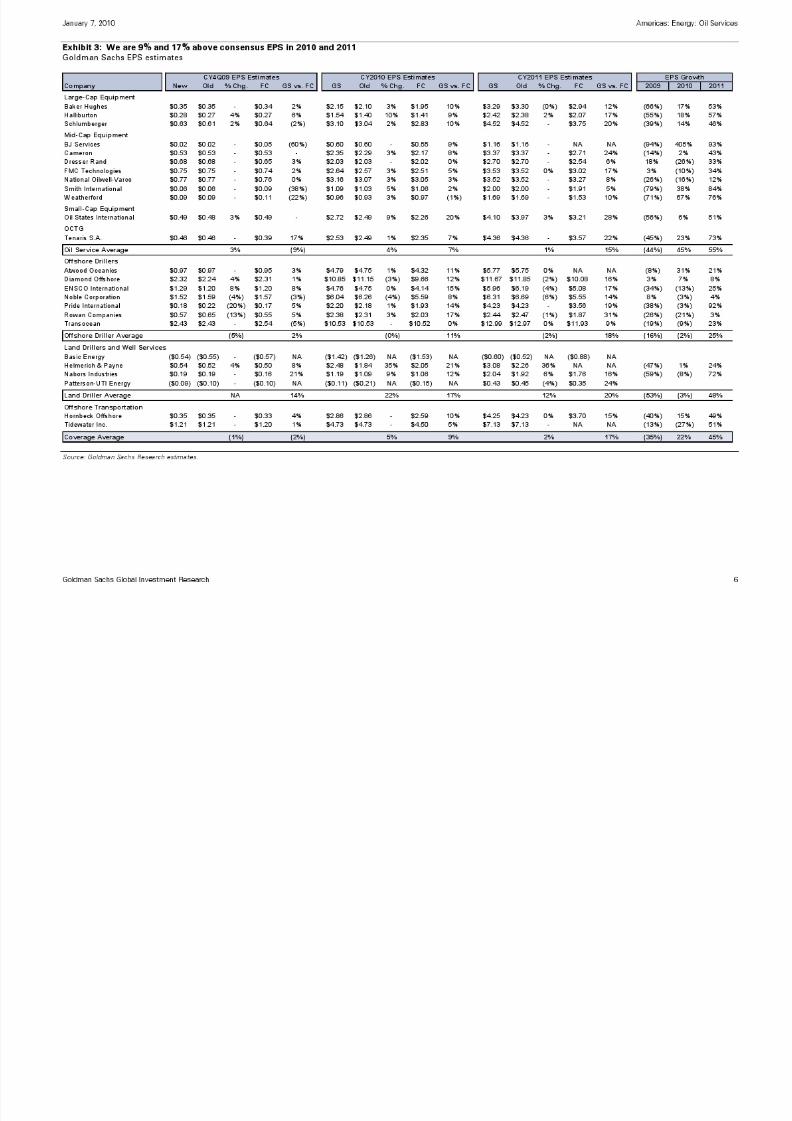

bundle, but we are currently not assuming this in our estimates. We are 9% and 17% above consensus in 2010 and 2011 and think

that EPS revisions will drive the shares higher. We have raised estimates in 2010 and 2011 by 10% and 2% to $1.54 and $2.42,

respectively.

Halliburton’s balance sheet also gives it significant fire power to buy back stock and to do accretive acquisitions. With $3.2 billion

cash on the balance sheet, there is significant flexibility to complement shareholder value creation.

On valuation, the shares are trading at 2010/2011 P/E of 21.0X/13.4X and EV/EBITDA of 9.1X/6.8X versus full cycle average multiples

of 19.2X/10.1X suggesting that there is upside on 2011 estimate as we move though the cycle.

January 7, 2010 Americas: Energy: Oil Services

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 20/37

y , gy

Goldman Sachs Global Investment Research 20

Exhibit 31: HAL has growth revenue per rig in N.A. the fastest…Revenue per rig in North America for HAL and SLB, and US/Mexico PP for BJS

Exhibit 32: …as ability to bundle has helped it grow the fastestY-o-Y revenue growth in North America

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

$4.5

$5.0

2002A 2003A 2004A 2005A 2006A 2007A 2008A 2009E 2010E 2011E

($ in mm)

BJS HAL SLB

2004-2009E CAGR:HAL = 13%

SLB = 7%BJS = 4%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

2002A 2003A 2004A 2005A 2006A 2007A 2008A 2009E 2010E 2011E

BJS HAL SLB

HAL is a marketshare "winner"

A strong pressurepumping market

helped BJS

A weak pressure pumpingmarket and inability to bundle

has since hurt BJS

Source: Company data, Baker Hughes, Goldman Sachs Research. Source: Company data, Goldman Sachs Research estimates.

Exhibit 33: …as ability to bundle has helped it grow the fastestYoY revenue growth in North America

40%

50%

60%

70%

80%

90%

100%

2003 2004 2005 2006 2007 2008 2009 2010 2011

US stimulation utilization

0%

5%

10%

15%

20%

25%

30%

35%

40%

HAL N.A C&

P margin

US stimulation utilization (lhs)

HAL N.A. C&P margin (rhs)

Expect pricingpower to return inlate 2010/early 2011as capacity tightens

Source: Spears & Associates, company data, Goldman Sachs Research estimates.

January 7, 2010 Americas: Energy: Oil Services

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 21/37

Goldman Sachs Global Investment Research 21

Cameron International: Downgrading to Neutral from Conviction Buy

We are tactically downgrading Cameron International to Neutral from Conviction Buy as we expect management to issue its typical

overly conservative guidance for 2010 when the company reports 4Q2009 results. We note that historically, the shares struggle to

outperform the oil service index at the onset of the year as management has historically set conservative guidance that tends to

disappoint investors on the day of the announcement. We do not expect this year to be any different based on recent conversations

with management. See Exhibits 34 and 35. While we continue to like the company’s strong leverage to all segments of the energy

value chain and its strong subsea franchise, we prefer to tactically shift away from the stock as the company prepares to give

guidance. As we continue to like the stock for the longer term, we will look to revisit the story post 1Q results and as we get closer

to potential large subsea projects awards which we do not expect to see until later in 2010. We now see 20% upside to our $53 6-

month price target, which is similar to group average upside of 16%.

Since being added to the Conviction Buy list on June 25, 2009, Cameron is +53% versus +31% for OSX and +24% for S&P500. Over

the last 12 months, Cameron is +74% versus +49% for OSX and +22% for S&P500.

Exhibit 34: Cameron management tends to give disappointing guidancewhich causes shares to trade in-line with the OSX initially…CAM annual EPS guidance versus consensus and stock performance over the next3 months

Exhibit 35: …but the stock outperforms meaningfully as guidance proves tobe conservative; this suggest that one should revisit the stock in 2Q10CAM annual EPS guidance versus reported EPS in each year and shareperformance month 3 though 6 after initial guidance

(30%)

(25%)

(20%)

(15%)

(10%)

(5%)

0%

5%

10%

2004 2005 2006 2007 2008 2009

Guidance vs. consensus expectations

3 months post guidance performance vs. OSX

(10%)

0%

10%

20%

30%

40%

50%

60%

2004 2005 2006 2007 2008 2009

Reported EPS vs. initial guidance

Month 3-6 post guidance performance vs. OSX

Source: FactSet, Company data, Goldman Sachs Research. Source: FactSet, Company data, Goldman Sachs Research.

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 22/37

January 7, 2010 Americas: Energy: Oil Services

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 23/37

Goldman Sachs Global Investment Research 23

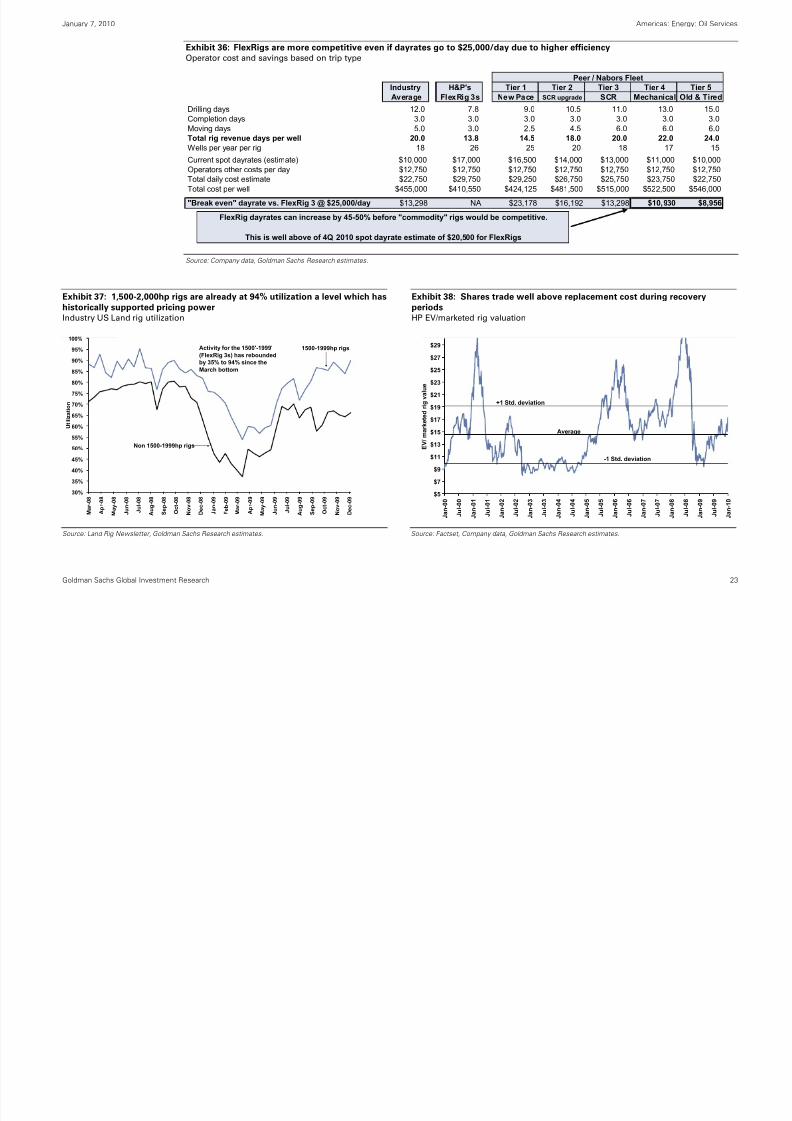

Exhibit 36: FlexRigs are more competitive even if dayrates go to $25,000/day due to higher efficiencyOperator cost and savings based on trip type

Peer / Nabors FleetIndustry H&P's Tier 1 Tier 2 Tier 3 Tier 4 Tier 5

Average FlexRig 3s New Pace SCR upgrade SCR Mechanical Old & Tired

Drilling days 12.0 7.8 9.0 10.5 11.0 13.0 15.0 Completion days 3.0 3.0 3.0 3.0 3.0 3.0 3.0 Moving days 5.0 3.0 2.5 4.5 6.0 6.0 6.0 Total rig revenue days per well 20.0 13.8 14.5 18.0 20.0 22.0 24.0 Wells per year per rig 18 26 25 20 18 17 15

Current spot dayrates (estimate) $10,000 $17,000 $16,500 $14,000 $13,000 $11,000 $10,000Operators other costs per day $12,750 $12,750 $12,750 $12,750 $12,750 $12,750 $12,750Total daily cost estimate $22,750 $29,750 $29,250 $26,750 $25,750 $23,750 $22,750

Total cost per well $455,000 $410,550 $424,125 $481,500 $515,000 $522,500 $546,000

"Break even" dayrate vs. FlexRig 3 @ $25,000/day $13,298 NA $23,178 $16,192 $13,298 $10,930 $8,956

FlexRig dayrates can increase by 45-50% before "commodity" rigs would be competitive.

This is well above of 4Q 2010 spot dayrate estimate of $20,500 for FlexRigs

Source: Company data, Goldman Sachs Research estimates.

Exhibit 37: 1,500-2,000hp rigs are already at 94% utilization a level which hashistorically supported pricing power

Industry US Land rig utilization

Exhibit 38: Shares trade well above replacement cost during recoveryperiods

HP EV/marketed rig valuation

30%

35%

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

Mar-08

Apr-08

May-08

Jun-08

Jul-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

Sep-09

Oct-09

Nov-09

Dec-09

Utilization

Non 1500-1999hp rigs

1500-1999hp rigsActivity for the 1500'-1999'

(FlexRig 3s) has reboundedby 35% to 94% since the

March bottom

$5

$7

$9

$11

$13

$15

$17

$19

$21

$23

$25

$27

$29

Jan-00

Jul-00

Jan-01

Jul-01

Jan-02

Jul-02

Jan-03

Jul-03

Jan-04

Jul-04

Jan-05

Jul-05

Jan-06

Jul-06

Jan-07

Jul-07

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

EV/ mark

eted rig value

+1 Std. deviation

Average

-1 Std. deviation

Source: Land Rig Newsletter, Goldman Sachs Research estimates. Source: Factset, Company data, Goldman Sachs Research estimates.

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 24/37

January 7, 2010 Americas: Energy: Oil Services

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 25/37

Goldman Sachs Global Investment Research 25

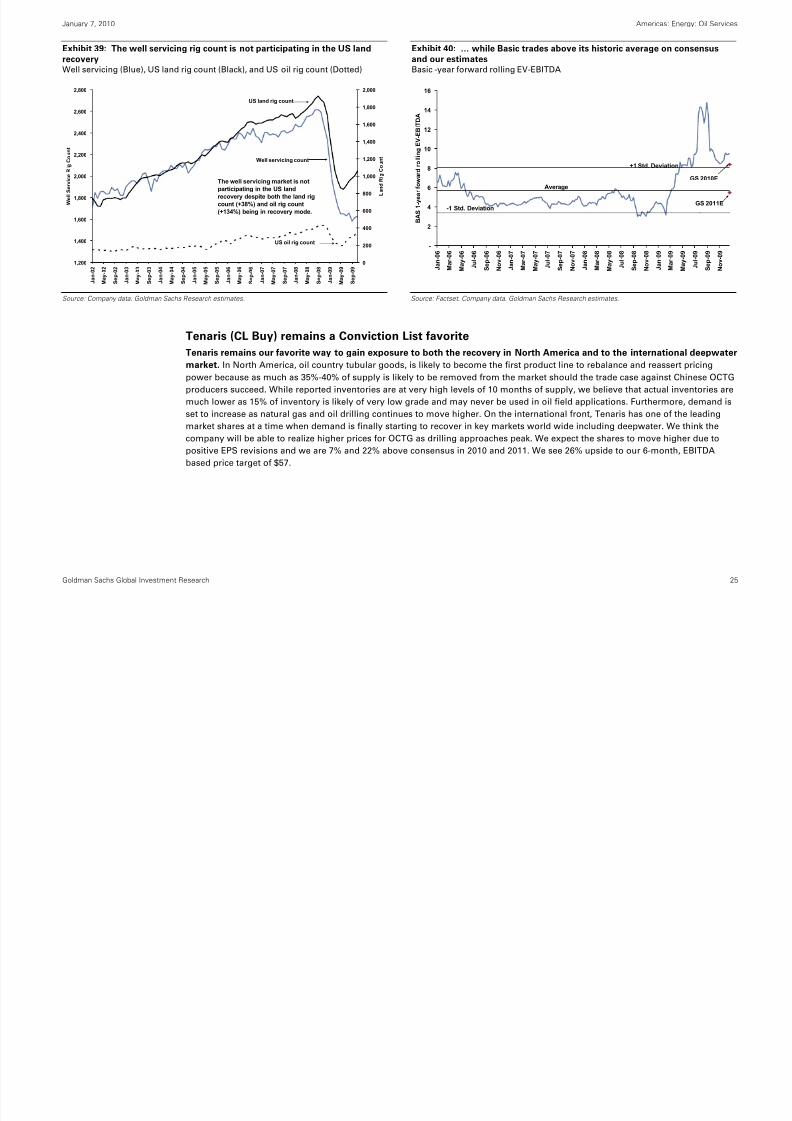

Exhibit 39: The well servicing rig count is not participating in the US landrecoveryWell servicing (Blue), US land rig count (Black), and US oil rig count (Dotted)

Exhibit 40: … while Basic trades above its historic average on consensusand our estimatesBasic -year forward rolling EV-EBITDA

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

2,800

Jan-02

May-02

Sep-02

Jan-03

May-03

Sep-03

Jan-04

May-04

Sep-04

Jan-05

May-05

Sep-05

Jan-06

May-06

Sep-06

Jan-07

May-07

Sep-07

Jan-08

May-08

Sep-08

Jan-09

May-09

Sep-09

Well Service Rig Count

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Land Rig Count

Well servicing count

US land rig count

The well servicing market is notparticipating in the US landrecovery despite both the land rigcount (+38%) and oil rig count(+134%) being in recovery mode.

US oil rig count

-

2

4

6

8

10

12

14

16

Jan-06

Mar-06

May-06

Jul-06

Sep-06

Nov-06

Jan-07

Mar-07

May-07

Jul-07

Sep-07

Nov-07

Jan-08

Mar-08

May-08

Jul-08

Sep-08

Nov-08

Jan-09

Mar-09

May-09

Jul-09

Sep-09

Nov-09

BA

S 1-year foward rolling EV-EBITDA

GS 2010E

GS 2011E

+1 Std. Deviation

-1 Std. Deviation

Average

Source: Company data, Goldman Sachs Research estimates. Source: Factset, Company data, Goldman Sachs Research estimates.

Tenaris (CL Buy) remains a Conviction List favorite

Tenaris remains our favorite way to gain exposure to both the recovery in North America and to the international deepwater

market. In North America, oil country tubular goods, is likely to become the first product line to rebalance and reassert pricing

power because as much as 35%-40% of supply is likely to be removed from the market should the trade case against Chinese OCTG

producers succeed. While reported inventories are at very high levels of 10 months of supply, we believe that actual inventories are

much lower as 15% of inventory is likely of very low grade and may never be used in oil field applications. Furthermore, demand is

set to increase as natural gas and oil drilling continues to move higher. On the international front, Tenaris has one of the leading

market shares at a time when demand is finally starting to recover in key markets world wide including deepwater. We think thecompany will be able to realize higher prices for OCTG as drilling approaches peak. We expect the shares to move higher due to

positive EPS revisions and we are 7% and 22% above consensus in 2010 and 2011. We see 26% upside to our 6-month, EBITDA

based price target of $57.

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 26/37

January 7, 2010 Americas: Energy: Oil Services

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 27/37

Goldman Sachs Global Investment Research 27

Exhibit 41: International jackup tendering (bidding) is up 30%....International jackup outstanding tenders

Exhibit 42: … suggesting that demand is at an inflection pointInternational jackup supply/demand forecast

85

90

95

100

105

110

115

120

7/28/09

8/4/09

8/11/09

8/18/09

8/25/09

9/1/09

9/8/09

9/15/09

9/22/09

9/29/09

10/6/09

10/13/09

10/20/09

10/27/09

11/3/09

11/10/09

11/17/09

11/24/09

12/1/09

12/8/09

12/15/09

12/22/09

12/29/09

Outstanding international jackup tend

ers

International jackuptendering activity hasincreased 30% since mid-summer.

250

265

280

295

310

325

340

355

370

385

400

Jan-07

Mar-07

May-07

Jul-07

Sep-07

Nov-07

Jan-08

Mar-08

May-08

Jul-08

Sep-08

Nov-08

Jan-09

Mar-09

May-09

Jul-09

Sep-09

Nov-09

Jan-10

Mar-10

May-10

Jul-10

Sep-10

Nov-10

Jan-11

Mar-11

May-11

Jul-11

Sep-11

Nov-11

International jackup supply/demand

75%

80%

85%

90%

95%

100%

International jackup utilization

Demand forecast(Left)

Utilization(Right)

Supply forecast (Left)(based on planned

newbuilds)

Source: ODS-Petrodata, Goldman Sachs Research estimates. Source: ODS-Petrodata, Company data, Goldman Sachs Research estimates.

January 7, 2010 Americas: Energy: Oil Services

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 28/37

Goldman Sachs Global Investment Research 28

Appendix 1: E&P capex announcements

Exhibit 43: Global E&P capex announcements suggest 14% growth in 2010, which is in excess of our 10% forecast2010 capex budgets announced up to date

E&P capex budget announcements thus far

2009E 2010E % Chg.

North America E&P Capex

Berry Petroleum $132 $240 82%

Chesapeake(1) 3,388 4,688 38%

Cabot Oil & Gas 600 585 (3%)

Chevron 3,600 4,100 14%

ConocoPhillips 3,300 4,100 24%

Devon 3,300 3,925 19%

EXCO Resources 400 471 18%

Frontier Oil 190 100 (47%)

Hess 1,125 1,700 51%

Husky Energy 1,485 1,770 19%

Mariner Energy 575 660 15%

Pioneer Natural Resources 300 850 183%

SandRidge Energy 767 750 (2%)

Southwestern Energy 1,800 2,100 17%

Quicksilver Resources 400 390 (3%)

Total North American E&P capex $21,362 $26,429 24%

International E&P Capex

Chevron(2) $11,600 $13,200 14%

ConocoPhillips(3) 6,950 5,600 (19%)

Devon 1,300 1,325 2%

Ecopetrol 3,764 4,509 20%

Hess 1,935 2,150 11%

Husky Energy(4) 458 626 37%

Nexen(4) 1,458 1,501 3%

Pemex(4) 16,177 17,197 6%

Pertamina

(4) (5) 2,134 4,207 97%

TNK-BP 3,000 3,400 13%

Total International E&P capex $48,776 $53,715 10%

Total International E&P capex (ex-Conoco) $41,826 $48,115 15%

Global E&P capex $70,137 $80,144 14%

(1) Drilling and geophysical capex only.

(2) 2009 CVX international capex excludes $2.3 billion extenstion of concession payment which we view to be

non-activity related.

(3) ConocoPhillips is in the process of divesting a portion of its international assets making year-on-year comparisons difficult.

(4) 2009 based on average exchange rate that year and 2010 is based on spot exchange rate.

(5) Includes non-E&P capex.

Source: Company data, Platts, Goldman Sachs Research.

January 7, 2010 Americas: Energy: Oil Services

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 29/37

Goldman Sachs Global Investment Research 29

Appendix 2: Stock performance

Exhibit 44: Oil services sub-sector performance for 2009 Exhibit 45: Individual stock performance for 2009

104%

94%

64%

56%

46%

31%

0%

20%

40%

60%

80%

100%

120%

Equipment Deepwater Land Dril lers Jackups Diversif iedServices

OSV

2009 Sub-sector Performance

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%140%

150%

FTI

ATW

OIS

CAM T

S

PDE

DRC

NBR

NOV

HP

RIG D

O

WFT

HAL

BJS

SLB

HOS

RDC

ESV

PTEN

BHI

TDW S

II

2009 Stock Price Performance

Source: FactSet Source: FactSet

Exhibit 46: Oil Services sub-sector performance since trough (Mar 9, 2009) Exhibit 47: Stock performance since individual trough (Jan – Mar 2009)

134%

123%

108%

90%86%

71%

0%

20%

40%

60%

80%

100%

120%

140%

160%

Equipment Land Drillers Deepwater Jackups OSV DiversifiedServices

Performance since recent trough

0%

65%

130%

195%

260%

OIS T

S

ATW

CAM

PDE

BJS

FTI

NBR

PTEN

HOS

HAL

WFT

HP

SLB

RIG

RDC

ESV

DO

DRC

NOV

BHI

TDW S

II

Stock Performance since trough

Source: FactSet. Source: FactSet.

January 7, 2010 Americas: Energy: Oil Services

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 30/37

Goldman Sachs Global Investment Research 30

Exhibit 48: Oil Services sub-sector performance since peak (July 2008) Exhibit 49: Stock performance since individual peak (May – Jul 2009)

(30%)

(35%)

(39%)

(44%)

(50%)(51%)

(60%)

(50%)

(40%)

(30%)

(20%)

(10%)

0%

Equipment Deepwater OSV Jackups Land Drillers Diversif iedServices

Performance since prior peak

(70%)

(60%)

(50%)

(40%)

(30%)

(20%)

(10%)

0%

TDW

DRC

CAM

FTI

DO

PDE

OIS

SLB

ATW T

S

HAL

BJS

HP

RIG

ESV

NOV

RDC

NBR

BHI

PTEN

HOS

WFT

SII

Stock Performance since prior p

eak

Source: FactSet. Source: FactSet.

Exhibit 50: Oil Services sub-sector upside to prior high (July 2008) Exhibit 51: Stock performance to individual highs (May – Jul 2008)

102%

81% 79%

57%

47%

118%

0%

20%

40%

60%

80%

100%

120%

DiversifiedServices

Land Drillers OSV Jackups Deepwater Equipment

Upside to prior peak

0%

40%

80%

120%

160%

200%

SII

WFT

HOS

PTEN

BHI

NBR

RDC

NOV

ESV

RIG H

P

BJS

HAL

TS

ATW

SLB

OIS

PDE

DO

FTI

CAM

DRC

TDW

Upside to prior peak

Source: FactSet. Source: FactSet.

January 7, 2010 Americas: Energy: Oil Services

A di S k i f hil I Li

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 31/37

Goldman Sachs Global Investment Research 31

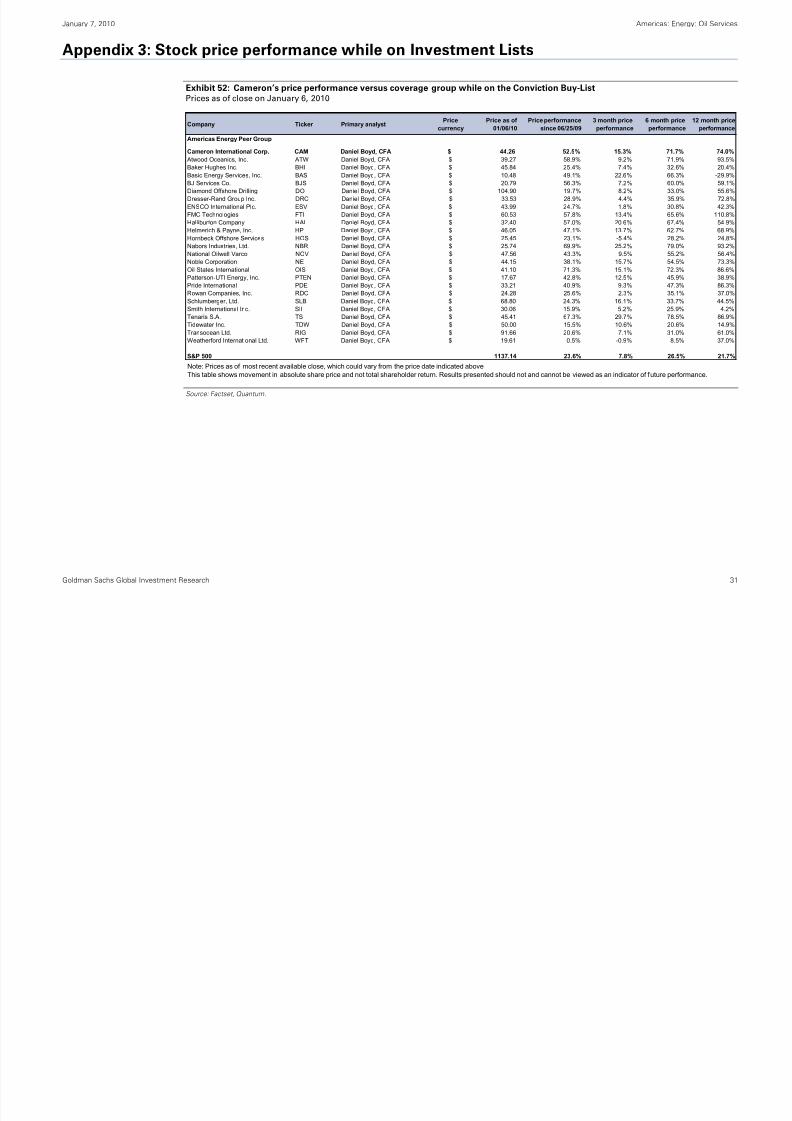

Appendix 3: Stock price performance while on Investment Lists

Exhibit 52: Cameron’s price performance versus coverage group while on the Conviction Buy-ListPrices as of close on January 6, 2010

Company Ticker Primary analystPrice

currency

Price as of

01/06/10

Price performance

since 06/25/09

3 month price

performance

6 month price

performance

12 month price

performance

Americas Energy Peer Group

Cameron International Corp. CAM Daniel Boyd, CFA $ 44.26 52.5% 15.3% 71.7% 74.0%

Atwood Oceanics, Inc. ATW Daniel Boyd, CFA $ 39.27 58.9% 9.2% 71.9% 93.5%

Baker Hughes Inc. BHI Daniel Boyd, CFA $ 45.84 25.4% 7.4% 32.6% 20.4%

Basic Energy Services, Inc. BAS Daniel Boyd, CFA $ 10.48 49.1% 22.6% 66.3% -29.9%

BJ Services Co. BJS Daniel Boyd, CFA $ 20.79 56.3% 7.2% 60.0% 59.1%

Diamond Offshore Drilling DO Daniel Boyd, CFA $ 104.90 19.7% 8.2% 33.0% 55.6%

Dresser-Rand Group Inc. DRC Daniel Boyd, CFA $ 33.53 28.9% 4.4% 35.9% 72.8%

ENSCO International Plc. ESV Daniel Boyd, CFA $ 43.99 24.7% 1.8% 30.8% 42.3%

FMC Technologies FTI Daniel Boyd, CFA $ 60.53 57.8% 13.4% 65.6% 110.8%Halliburton Company HAL Daniel Boyd, CFA $ 32.40 57.0% 20.6% 67.4% 54.9%

Helmerich & Payne, Inc. HP Daniel Boyd, CFA $ 46.05 47.1% 13.7% 62.7% 68.9%

Hornbeck Offshore Services HOS Daniel Boyd, CFA $ 25.45 23.1% -5.4% 28.2% 24.8%

Nabors Industries, Ltd. NBR Daniel Boyd, CFA $ 25.74 69.9% 25.2% 79.0% 93.2%

National Oilwell Varco NOV Daniel Boyd, CFA $ 47.56 43.3% 9.5% 55.2% 56.4%

Noble Corporation NE Daniel Boyd, CFA $ 44.15 38.1% 15.7% 54.5% 73.3%

Oil States International OIS Daniel Boyd, CFA $ 41.10 71.3% 15.1% 72.3% 86.6%

Patterson-UTI Energy, Inc. PTEN Daniel Boyd, CFA $ 17.67 42.8% 12.5% 45.9% 38.9%

Pride International PDE Daniel Boyd, CFA $ 33.21 40.9% 9.3% 47.3% 86.3%

Rowan Companies, Inc. RDC Daniel Boyd, CFA $ 24.28 25.6% 2.3% 35.1% 37.0%

Schlumberger, Ltd. SLB Daniel Boyd, CFA $ 68.80 24.3% 16.1% 33.7% 44.5%

Smith International Inc. SII Daniel Boyd, CFA $ 30.06 15.9% 5.2% 25.9% 4.2%

Tenaris S.A. TS Daniel Boyd, CFA $ 45.41 67.3% 29.7% 78.5% 86.9%

Tidewater Inc. TDW Daniel Boyd, CFA $ 50.00 15.5% 10.6% 20.6% 14.9%Transocean Ltd. RIG Daniel Boyd, CFA $ 91.66 20.6% 7.1% 31.0% 61.0%

Weatherford International Ltd. WFT Daniel Boyd, CFA $ 19.61 0.5% -0.9% 8.5% 37.0%

S&P 500 1137.14 23.6% 7.8% 26.5% 21.7%

Note: Prices as of most recent available close, which could vary from the price date indicated aboveThis table shows movement in absolute share price and not total shareholder return. Results presented should not and cannot be viewed as an indicator of future performance.

Source: Factset, Quantum.

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 32/37

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 33/37

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 34/37

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 35/37

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 36/37

8/7/2019 GS Report OFS Jan 2010

http://slidepdf.com/reader/full/gs-report-ofs-jan-2010 37/37