group 6 -monetqary policy transmission mechanism

TRANSCRIPT

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 1/42

{

Monetary Policy

Transmission MechanismGroup 6Adarsh N ( PGP/16/060)

Deepak Jangid(PGP/16/080)

Eshnna V P Ekka ( PGP/16/081)

Gaurav Chand (PGP/16/082)

Hemant Kumar (PGP/16/083)

Nishant S (PGP/16/096)

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 2/42

To meet the policy targets set by Central Bank

Exert systematic influence on the economy in aforward looking sense

To reflect the desired effect in desired time frame

Objective

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 3/42

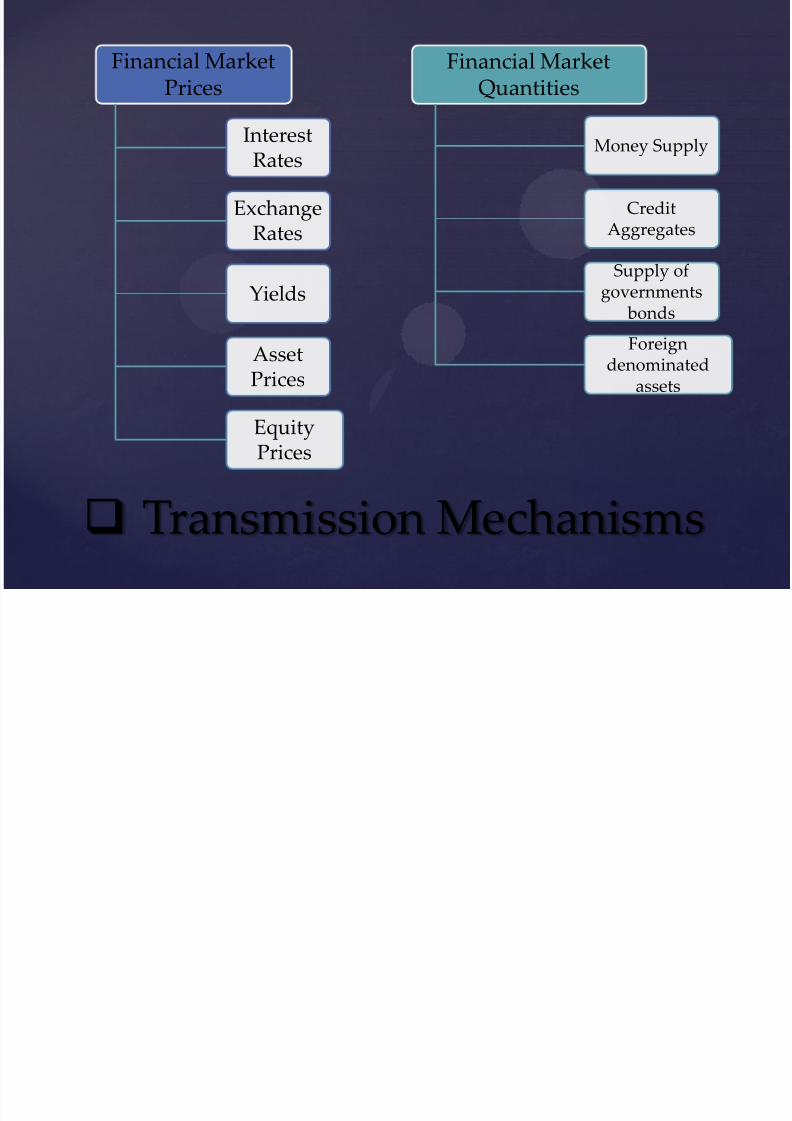

Transmission Mechanisms

Financial MarketPrices

InterestRates

ExchangeRates

Yields

AssetPrices

EquityPrices

Financial MarketQuantities

Money Supply

CreditAggregates

Supply ofgovernments bonds

Foreigndenominated

assets

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 4/42

Major channels are :

1. Interest rate

2. Credit aggregates

3. Asset prices

4. Exchange rate

Interest rate channel is dominant transmission mechanism

Credit channel amplify and propagate interest rate effects

Fifth channel – expectations

Transmission Channels

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 5/42

Transmission Channels

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 6/42

1) Objectives of Monetary policy2) Framework and instruments of monetary

policy guiding monetary policy transmission

3) Monetary policy transmission channels and

operating Procedures4) Assessment of monetary transmission

5) Challenges and dilemmas of monetary policy

Key points to be discussed

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 7/42

Reserve Bank of India Act, 1934 sets out theobjectives

‚To regulate the issue of Bank notes and thekeeping of reserves with a view to securingmonetary stability in India and generally tooperate the currency and credit system of thecountry to its advantage‛.

1) Objectives of Monetary Policy

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 8/42

Twin objectives :A) Price stability

B) Provision of adequate credit to productivesectors of the economy to support the

aggregate demand Underlying philosophy- to establish the low and

stable inflation environment that economic growthcan sustain.

1) Objectives of Monetary Policy

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 9/42

Prior to Mid-1980s No formal enunciation of

Objectives

Instruments

Other than Administering the supply/allocation of and

demand for credit

2) Framework and Instruments

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 10/42

1985-1997 Implementation of loose and flexible monetary

targeting with feedback

Growth in broad money supply (M3) was

projected in a manner consistent with expectedGDP growth and a tolerable level of inflation

Operating target – Reserve Money

Operating Instrument – Bank Reserves

2) Framework and Instruments

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 11/42

But..

Market deregulation increased the role of marketforces

Capital flows led to : increased liquidity

Upward pressure on the money supply, prices andexchange rates

Result: Interest rates gained relative influence onthe decision to hold money.

2) Framework and Instruments

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 12/42

Post 1998-99

Broad-based multiple indicator approach

Policy objectives obtained by the combination of

interest rate and other market rates Central objective - High economic growth

Inflation targeting was made secondary

2) Framework and Instruments

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 13/42

Reasons for inflation being second concern

Record moderate inflation until the downturn of 2008

Absence of efficient financial market

Interest rate distortions Supply shocks arising from Monsoon on agriculture

Market imperfections with regional differences

2) Framework and Instruments

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 14/42

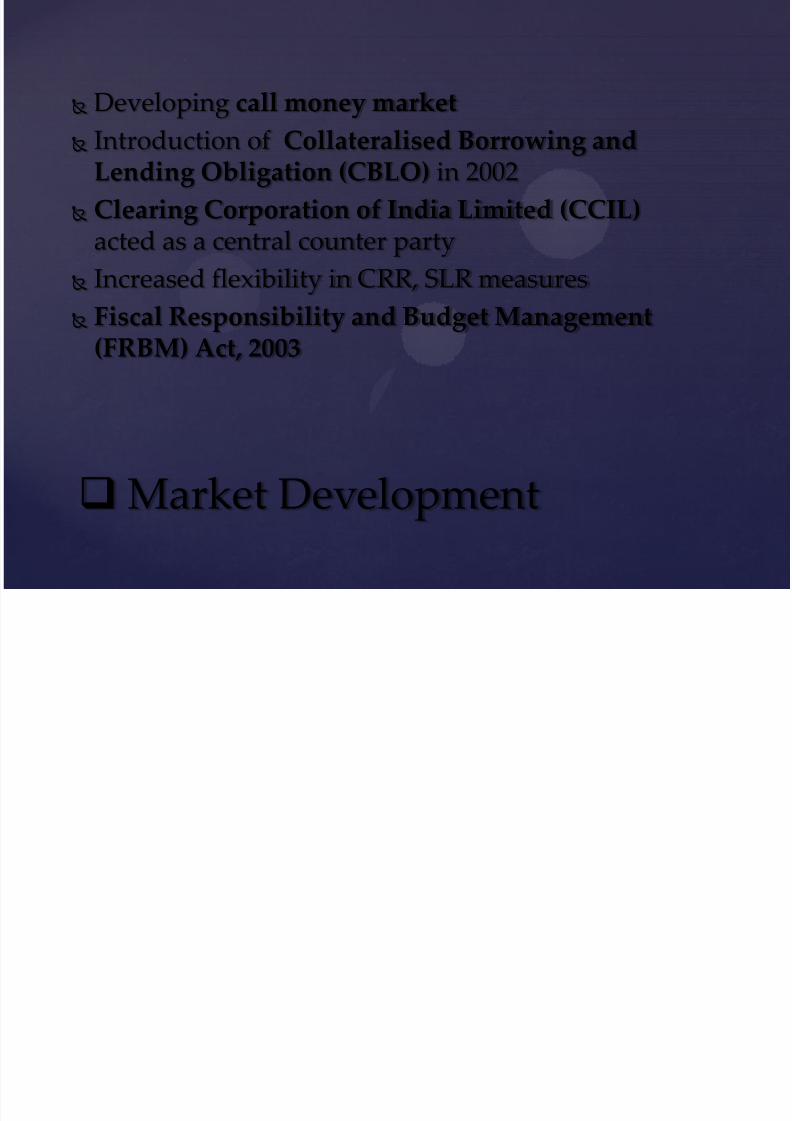

Need for efficient price discovery w.r.t. to interestrates and exchange rates

Growing need for full financial market spectrum Pivotal in transmission of policies

Market Development

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 15/42

Developing call money market

Introduction of Collateralised Borrowing andLending Obligation (CBLO) in 2002

Clearing Corporation of India Limited (CCIL)acted as a central counter party

Increased flexibility in CRR, SLR measures Fiscal Responsibility and Budget Management

(FRBM) Act, 2003

Market Development

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 16/42

Fiscal Responsibility and Budget Management(FRBM) Act, 2003

Reserve Bank not allowed to subscribe G-Secs inPrimary market

Completed the transition to a fully market based

system for Government securities Raising of funds by State Governments was

made market driven

Market Development

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 17/42

Key indicators – short term interest rates

Use of instruments directly under control of central banklike – Interest rate, CRR

Sterilization of exchange rates through OMO etc. Monetary policy is implemented by fixing operating

target and policy instruments for short time horizon.

3) Operating Procedures

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 18/42

3) Operating Procedures

Variant Example Operating Procedure

First US Federal

Reserve

Estimates the demand for bank reserves and

then carry out openmarket operations to target short-terminterest rates;

Second Bank of Japan Estimate market liquidity andcarry out open market operations to target bank reserves, while allowing interest rates

to adjust

Third Bank of England Modulates monetary conditions in terms of both quantum and price of liquidity, througha mix of OMOs, standing facilities andminimum reserve

requirement and changes in the policy rate.

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 19/42

3) Operating Procedures

1. Money Markets and LAF

2. Market Stabilization scheme

3. Bank Credit and Lending rate channels

4. Debt Market Channel

5. Exchange Rate Channel

6. Communication and Expectationchannel

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 20/42

LAF - Liquidity Adjustment Facility, 2000

Reserve Bank

Sets its policy rates i.e. Repo/Reverse Repo rates

Carries out Repo/Reverse Repo Operations

3.1 Money Market and LAF

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 21/42

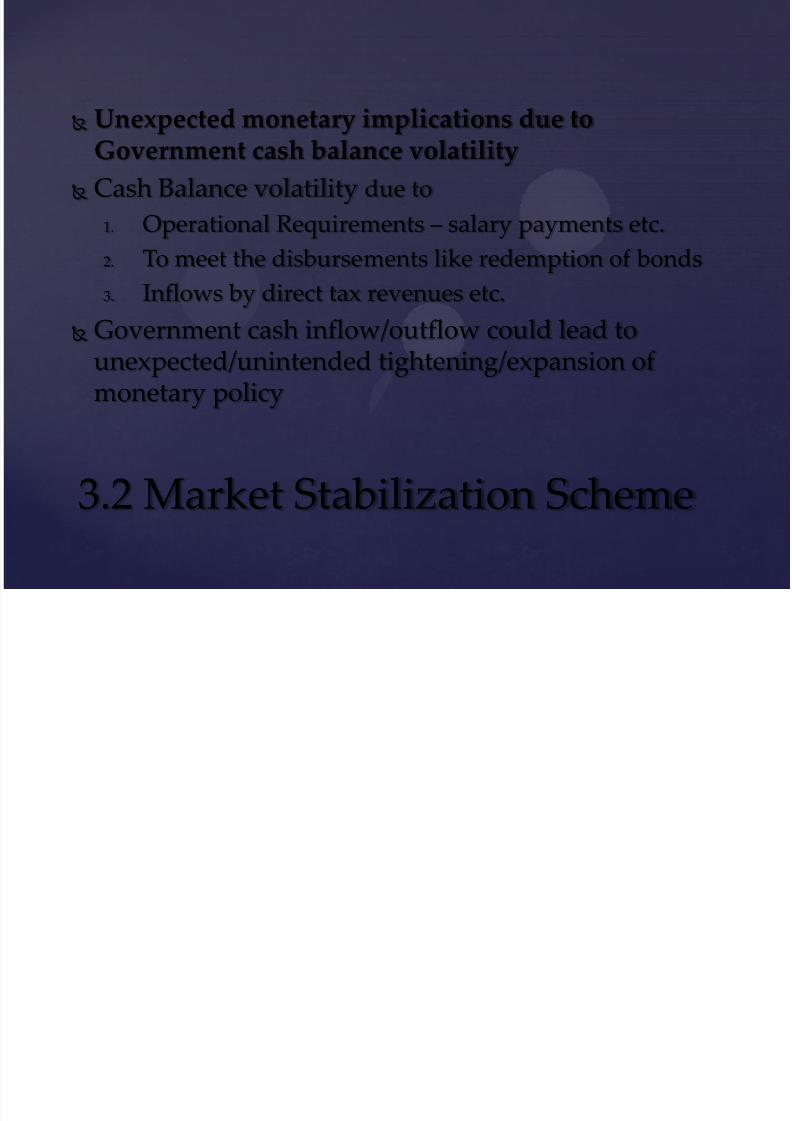

Market Stabilization Scheme March, 2004

Needed to sterilize the large capital inflows

RBI issues additional T-bills and securities to absorbthe liquidity

Money goes into the Market Stabilization schemeAccount

The RBI cannot use this account for paying anyinterest or discounts and cannot credit anypremiums to this account

3.2 Market Stabilization Scheme

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 22/42

Unexpected monetary implications due to

Government cash balance volatility

Cash Balance volatility due to

1. Operational Requirements – salary payments etc.

2. To meet the disbursements like redemption of bonds

3. Inflows by direct tax revenues etc.

Government cash inflow/outflow could lead tounexpected/unintended tightening/expansion ofmonetary policy

3.2 Market Stabilization Scheme

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 23/42

Gaining strength due to increasing share of retailcredit, household credit etc.

A better tool of price discovery

Highly important for RBI to ensure

Availability of bank credit to agriculture, exports, SSI,infrastructure, housing etc.

Increasing share

Depends upon Interest pass-through ratio

3.3 Bank Credit & Lending Ratechannels

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 24/42

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 25/42

Factors affecting pass-through ratio: Policy efforts to impart greater flexibility to interest

rate structure

Guidance by RBI to introduce flexibility in new

deposits Competition – High competition will lead to higher

pass-through ratio

3.3 Bank Credit & Lending Ratechannels

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 26/42

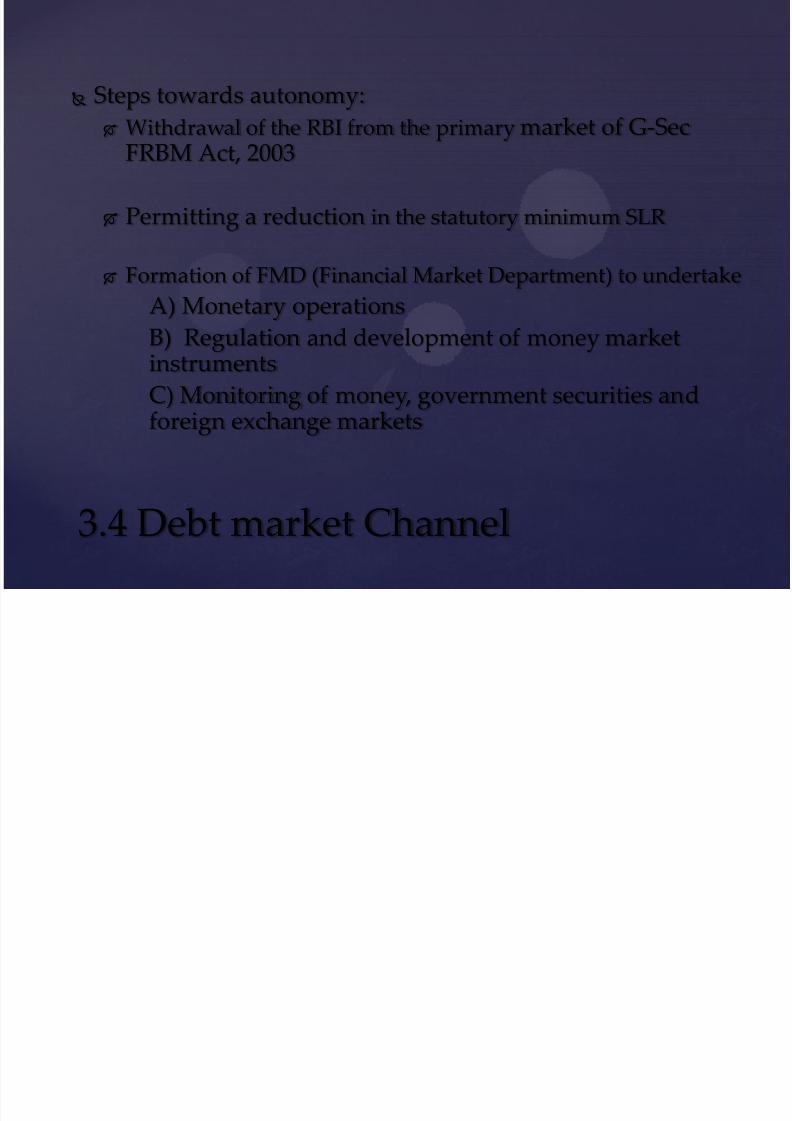

Two functions – Monetary Policy & Debt Management

Pre-conditions for separation of both requires:

Fuller development of financial markets

Reasonable control over the fiscal deficit Necessary legislative changes

Greater autonomy for the monetary policies

3.4 Debt market Channel

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 27/42

Steps towards autonomy:

Withdrawal of the RBI from the primary market of G-SecFRBM Act, 2003

Permitting a reduction in the statutory minimum SLR

Formation of FMD (Financial Market Department) to undertakeA) Monetary operations

B) Regulation and development of money marketinstruments

C) Monitoring of money, government securities and

foreign exchange markets

3.4 Debt market Channel

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 28/42

While the government securities market is fairly welldeveloped now

Corporate debt market remains to be developed forfacilitating monetary signalling across various marketsegments.

3.4 Debt market Channel

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 29/42

Guided by the broad principles of careful monitoring andmanagement of exchange rates with flexibility, without a

fixed target or a pre-announced target or a band, coupledwith the ability to intervene, if and when necessary.

3.5 Exchange Rate Channel

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 30/42

3.5 Exchange Rate Channel

InterestRate

Arbitrage

Net Inflowuntil interest

parity isachieved

Appreciatingexchange rate

Dampeningeffect on

Aggregatedemand

Inflationarypressure

Restrictedexchange rateadjustments

due to market

volatility

Need to carry outforex operations forstabilizing the market

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 31/42

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 32/42

Dilemma faced by RBI about communication What and to what degree of disaggregation?

What stage of evolution of internal thinking and debate shouldthere be dissemination

timing of communication with reference to its market impact quality of information and the possible ways in which it could be

perceived

3.6 Communication and ExpectationChannel

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 33/42

More complex is the mandate for the central bank, themore is the necessity of communication

Three kinds of communication

policy measures reasons behind such policy measures and

analysis of the economy

3.6 Communication and ExpectationChannel

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 34/42

Quarterly policy statement Governor explains the rationale behind the policy

measures

Technical Advisory Committees (TACs)

External experts Reviews macroeconomic and monetary developments

Advises the Reserve Bank

3.6 Communication andExpectation Channel

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 35/42

Inflation statistics (Excel)

Spreadsheet Analysis

4) How well do these channelsdo?

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 36/42

1. Volatility in agriculture sector2. Challenges in liquidity management

3. Volatility in global financial market

4. Evolving challenges:1. Evolving Demography

2. Financial innovations : e-banking

5. Challenges in efficient transmission

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 37/42

Caused by dependence on monsoon rainfall

Volatility in share to GDP

Supply shock impacts food inflation

Since food items form part of price indices it resultvolatility in headline inflation

5.1 Volatility in agriculture sector

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 38/42

Buffer cash reserves kept by banks with RBI

Government‘s surplus cash balances in RBI

5.2 Challenges in liquidity management

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 39/42

Withdrawal of funds from Indian equity markets

Dollar liquidity in the domestic foreign exchangemarket

Adverse expectations on the balance of payments

Increased volatility in the foreign exchange market

5.3 Volatility in global financial market

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 40/42

As the proportion of elderly population to the total

increases, the pattern of global savings will change Tends to reduce the natural rate of interest

Elderly population richer in financial and real capitalwhile young are richer in human capital

With growing share of elderly population, the role ofthe wealth channel in monetary transmission mightassume greater importance

5.4.1 Evolving Demography

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 41/42

7/28/2019 Group 6 -Monetqary Policy Transmission Mechanism

http://slidepdf.com/reader/full/group-6-monetqary-policy-transmission-mechanism 42/42

Thank You