granules india

TRANSCRIPT

Granules India Ltd(GIL) -An Emerging Business

Content Index

•Granules India Limited – Investment Snapshot :- Slide #3

• Pharma Industry – An Overview:- Slide #5

• Investment Arguments :- Slide #14

•P&L - Slide #27

• Concerns & Reasoning :- Slide #28

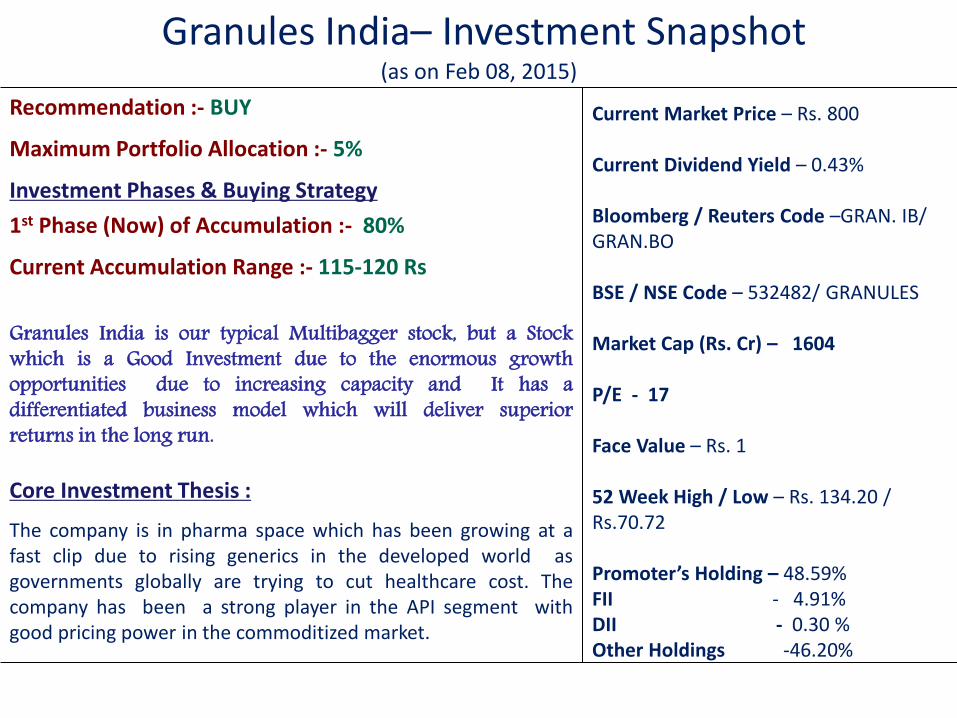

Granules India– Investment Snapshot (as on Feb 08, 2015)

Recommendation :- BUY

Maximum Portfolio Allocation :- 5%

Investment Phases & Buying Strategy

1st Phase (Now) of Accumulation :- 80%

Current Accumulation Range :- 115-120 Rs

Granules India is our typical Multibagger stock, but a Stock

which is a Good Investment due to the enormous growth

opportunities due to increasing capacity and It has a

differentiated business model which will deliver superior

returns in the long run.

Core Investment Thesis :

The company is in pharma space which has been growing at a

fast clip due to rising generics in the developed world as

governments globally are trying to cut healthcare cost. The

company has been a strong player in the API segment with

good pricing power in the commoditized market.

Current Market Price – Rs. 800

Current Dividend Yield – 0.43%

Bloomberg / Reuters Code –GRAN. IB/

GRAN.BO

BSE / NSE Code – 532482/ GRANULES

Market Cap (Rs. Cr) – 1604

P/E - 17

Face Value – Rs. 1

52 Week High / Low – Rs. 134.20 /

Rs.70.72

Pro oter’s Holdi g – 48.59%

FII - 4.91%

DII - 0.30 %

Other Holdings -46.20%

Key Investment Highlights

1.) Presence in a growing segment :- Company caters to the API space which has been growing rapidly

which provides immense opportunities to the companies in the sector.

2)M&A , JV to drive growth- Company has been consistently looking for inorganic growth opportunities. And

has been actively concluded several M&A,JV opportunities which are bound to drive growth.

3.) Strong Pricing Power :- Despite being a API dominant company where the business is commoditized the

company has been able t command strong pricing power due to the quality and service .

4.) Pass on higher raw material cost :- The company enters into a 3-5 year contracts with major customers

which also enables the company to pass on any increase n raw material cost.

5) No adverse FDA Issues :- The companies plants had been recently inspected by USFDA and no issues had

cropped up.

6.) Presence in key markets :- Company has been predominantly an export player and is present in key

markets across Europe, US etc which has enabled the company to grow faster.

7.) Increasing share of Formulations:- Company although was a API player is focusing on formulations

development from Auctus API s which would enhance share of formulations.

8) Increasing manufacturing capacity:- The company has expanded its PFI capacity from 9840 TPA to

14,400 TPA and its formulations capacity from 6bn to 18bn per annum which will drive growth .

9.) Management/ Corporate Governance :- The company has a good management and adhere to strong

corporate governance norms. The company is run professionally by a team of professionals who have a

strong understanding of the business and have a strong vision about its business.

10.) Compelling Valuations :- In spite of so many advantages, the company is quoting at very attractive

Valuations. The company is quoting at 16X its trailing FY14 Earnings which is reasonable for the Quality of

this stock which has a strong operating performance and provides revenue visibility.

Industry Opportunity & Potential

- An Overview

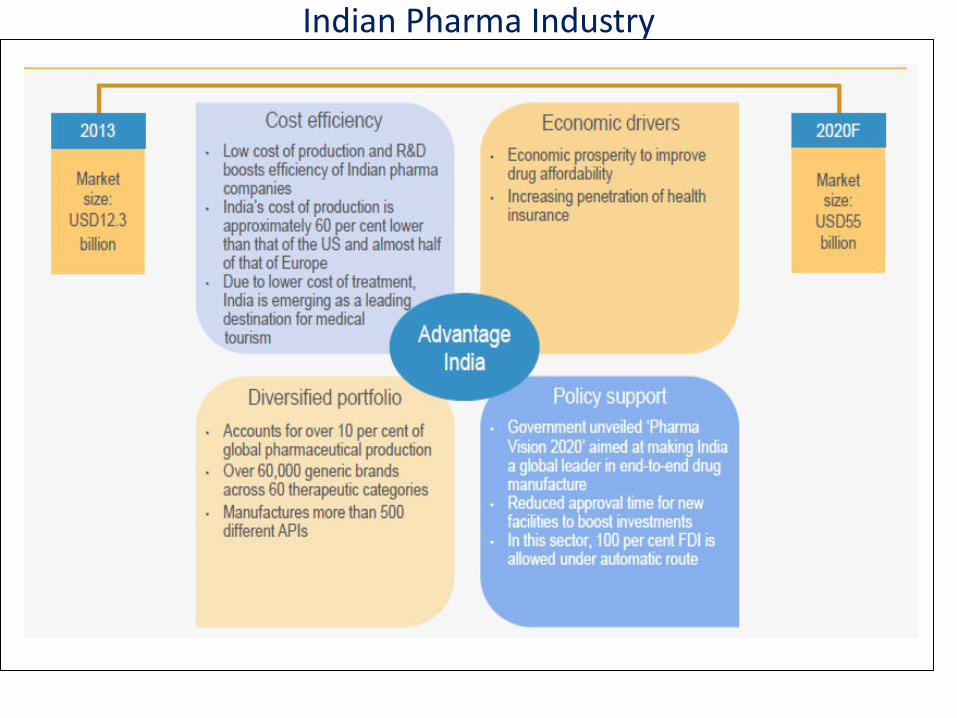

Indian Pharma Industry

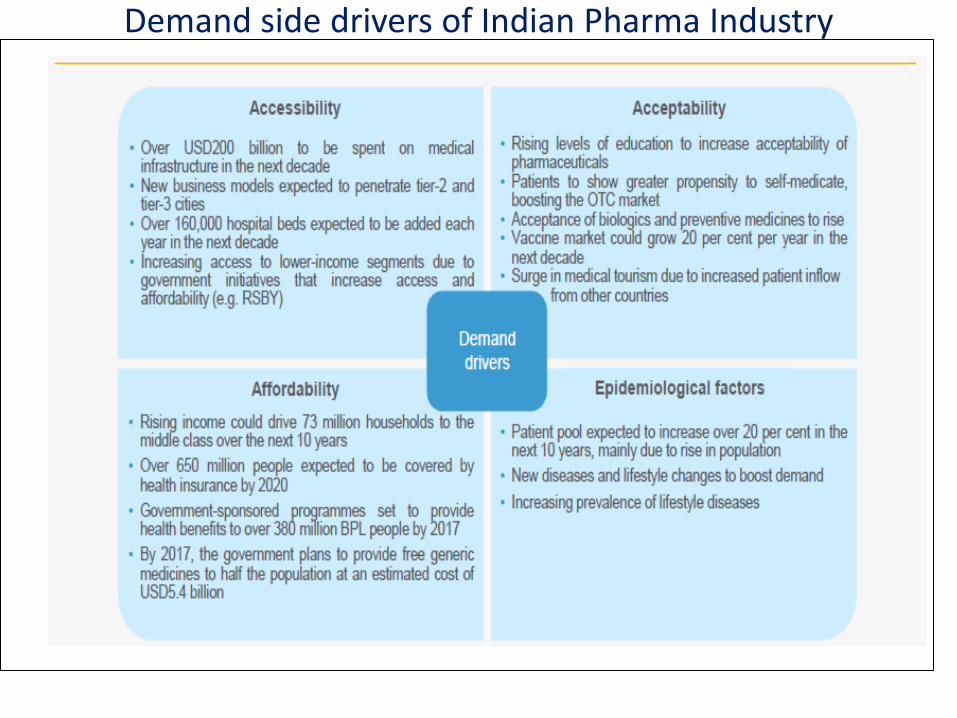

Demand side drivers of Indian Pharma Industry

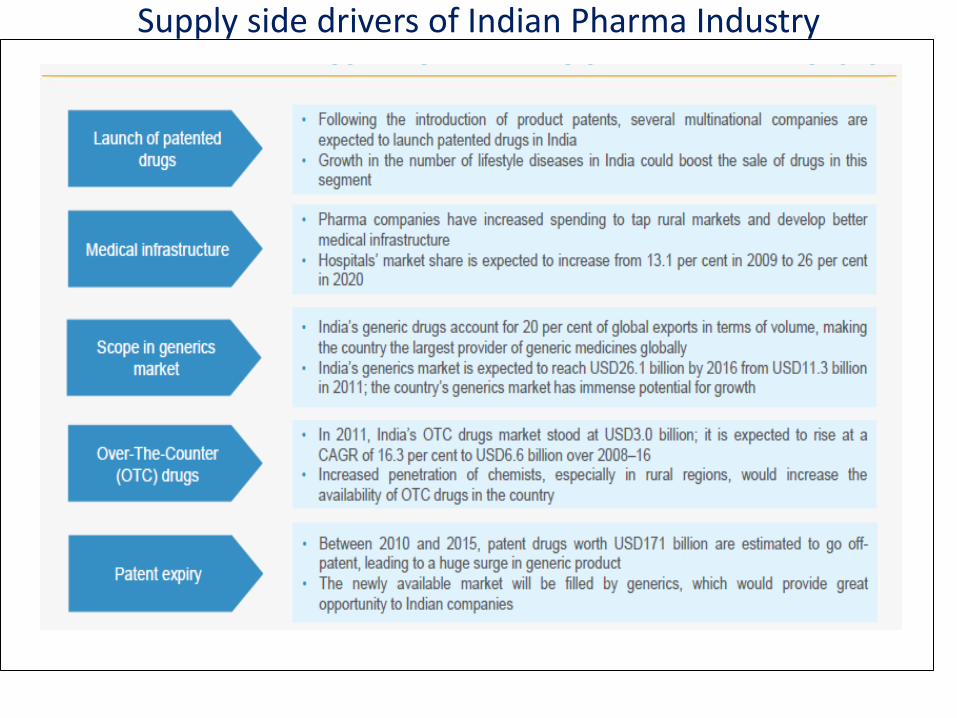

Supply side drivers of Indian Pharma Industry

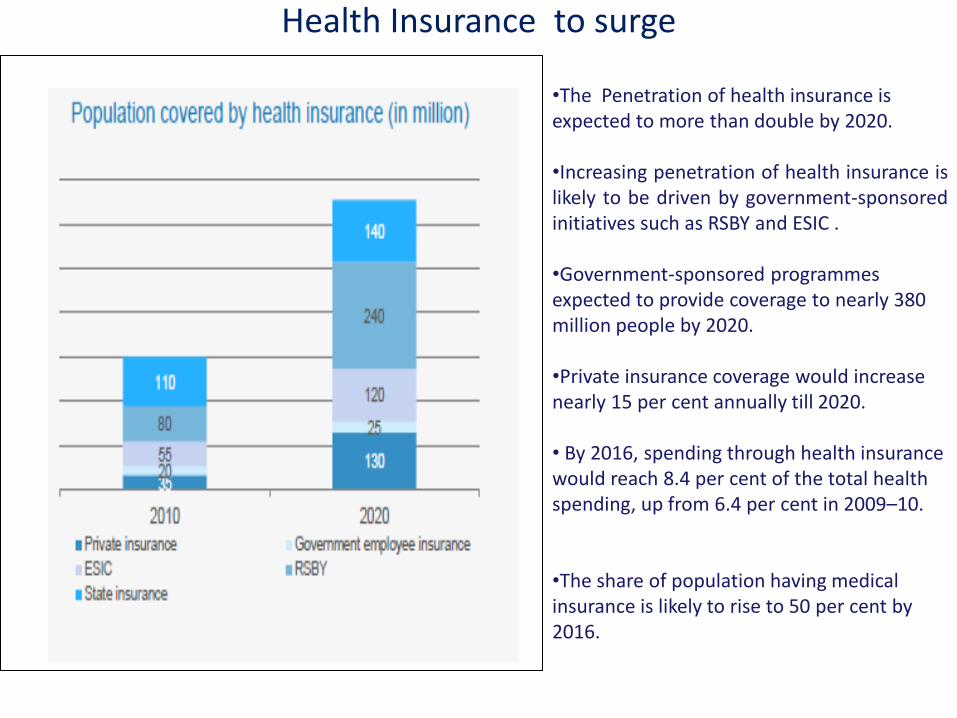

Health Insurance to surge

•The Penetration of health insurance is

expected to more than double by 2020.

•Increasing penetration of health insurance is

likely to be driven by government-sponsored

initiatives such as RSBY and ESIC .

•Government-sponsored programmes

expected to provide coverage to nearly 380

million people by 2020.

•Private insurance coverage would increase

nearly 15 per cent annually till 2020.

• By 2016, spending through health insurance

would reach 8.4 per cent of the total health

spending, up from 6.4 per cent in 2009–10.

•The share of population having medical

insurance is likely to rise to 50 per cent by

2016.

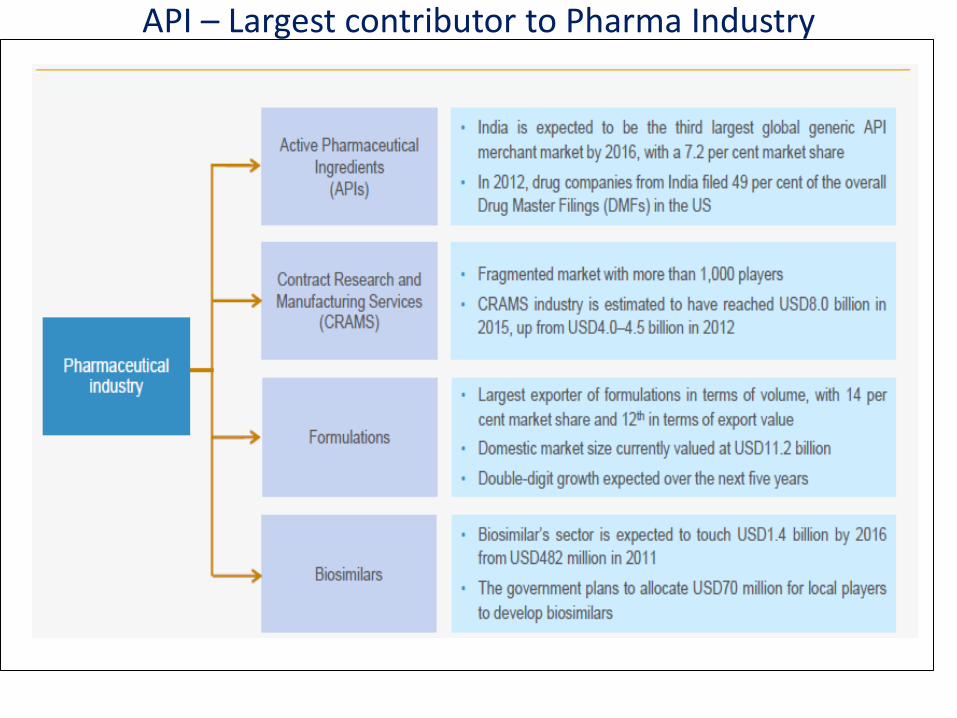

API – Largest contributor to Pharma Industry

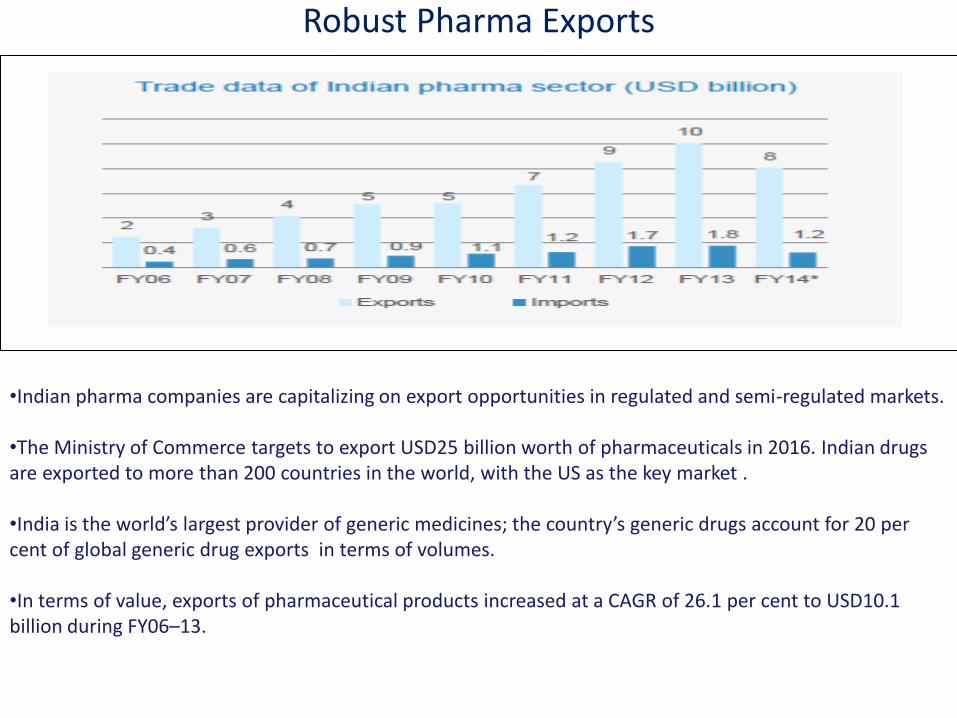

Robust Pharma Exports

•Indian pharma companies are capitalizing on export opportunities in regulated and semi-regulated markets.

•The Ministry of Commerce targets to export USD25 billion worth of pharmaceuticals in 2016. Indian drugs

are exported to more than 200 countries in the world, with the US as the key market .

•I dia is the o ld s la gest p o ide of ge e i edi i es; the ou t s ge e i d ugs a ou t fo pe cent of global generic drug exports in terms of volumes.

•In terms of value, exports of pharmaceutical products increased at a CAGR of 26.1 per cent to USD10.1

billion during FY06–13.

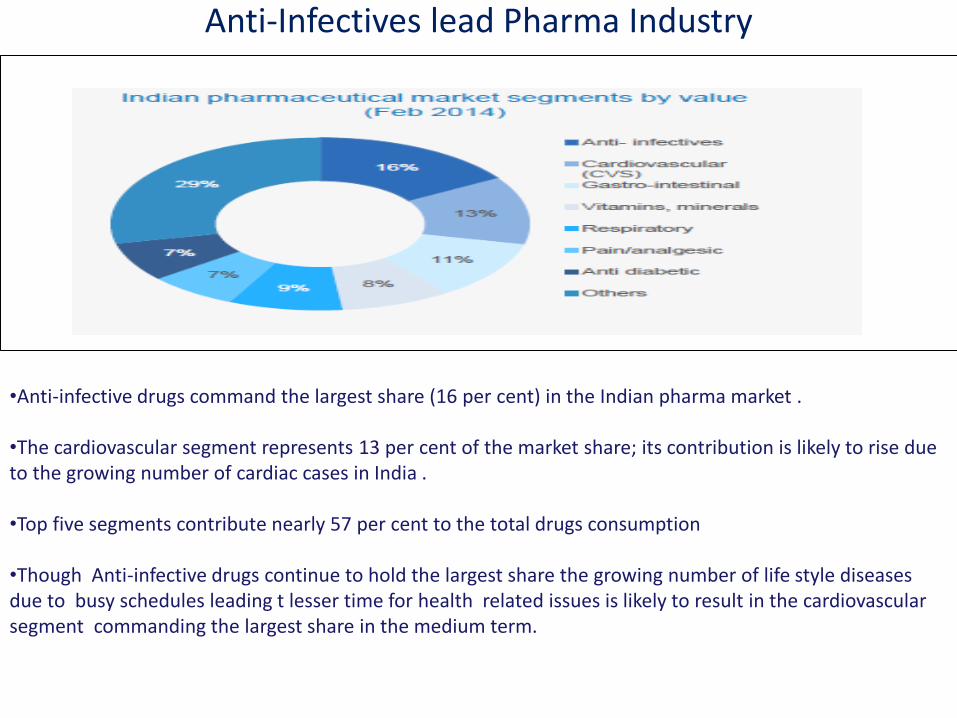

Anti-Infectives lead Pharma Industry

•Anti-infective drugs command the largest share (16 per cent) in the Indian pharma market .

•The cardiovascular segment represents 13 per cent of the market share; its contribution is likely to rise due

to the growing number of cardiac cases in India .

•Top five segments contribute nearly 57 per cent to the total drugs consumption

•Though Anti-infective drugs continue to hold the largest share the growing number of life style diseases

due to busy schedules leading t lesser time for health related issues is likely to result in the cardiovascular

segment commanding the largest share in the medium term.

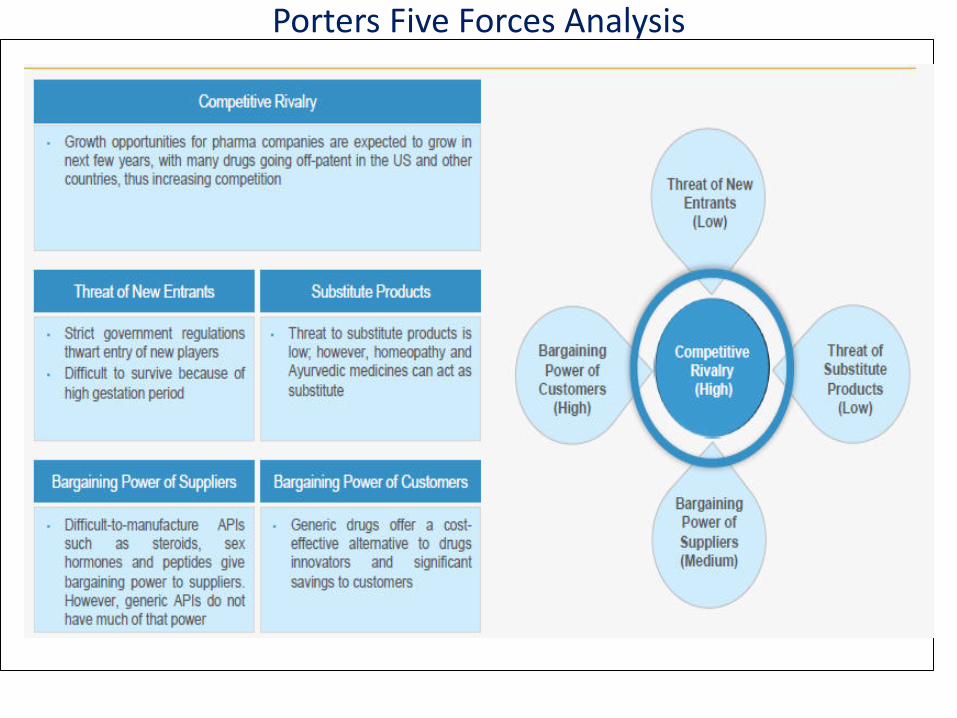

Porters Five Forces Analysis

GIL – Investment Arguments

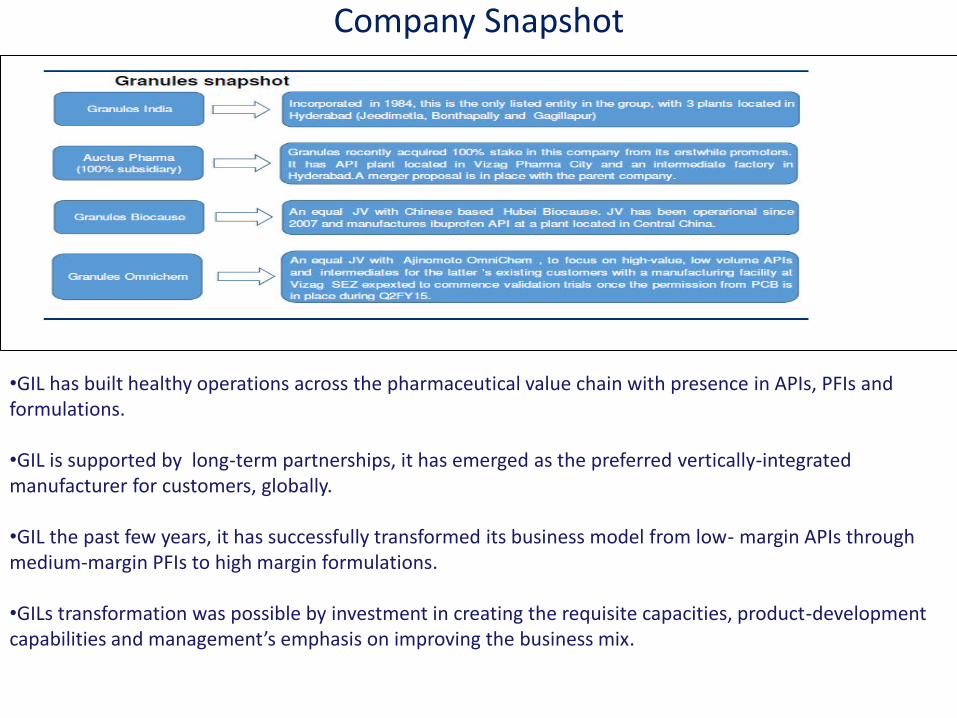

Company Snapshot

•GIL has built healthy operations across the pharmaceutical value chain with presence in APIs, PFIs and

formulations.

•GIL is supported by long-term partnerships, it has emerged as the preferred vertically-integrated

manufacturer for customers, globally.

•GIL the past few years, it has successfully transformed its business model from low- margin APIs through

medium-margin PFIs to high margin formulations.

•GILs transformation was possible by investment in creating the requisite capacities, product-development

apa ilities a d a age e t s e phasis o i p o i g the usi ess i .

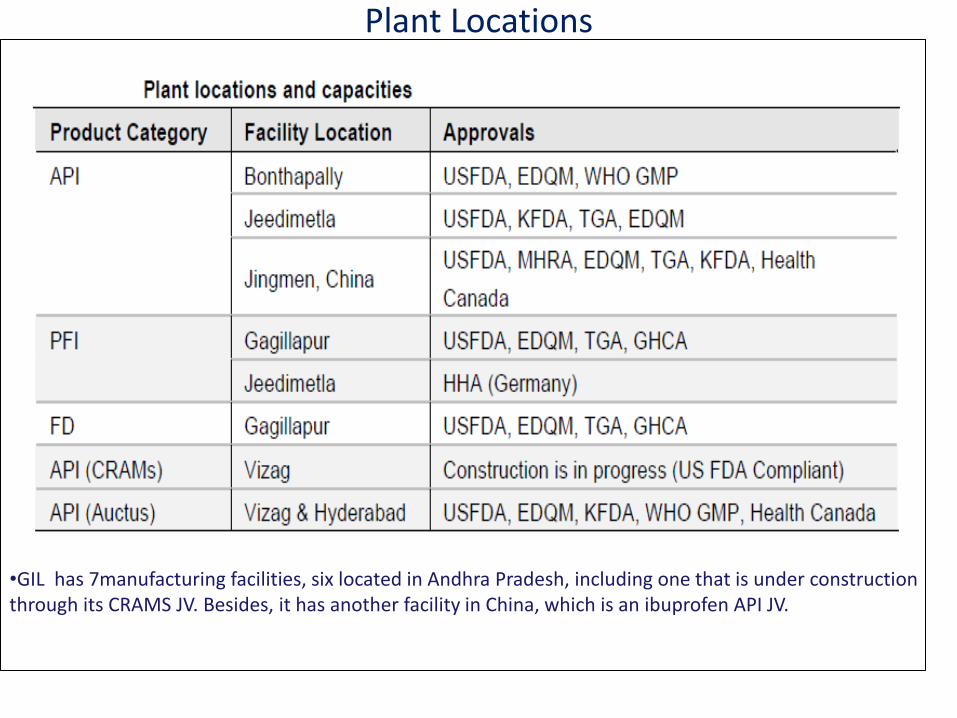

Plant Locations

•GIL has 7manufacturing facilities, six located in Andhra Pradesh, including one that is under construction

through its CRAMS JV. Besides, it has another facility in China, which is an ibuprofen API JV.

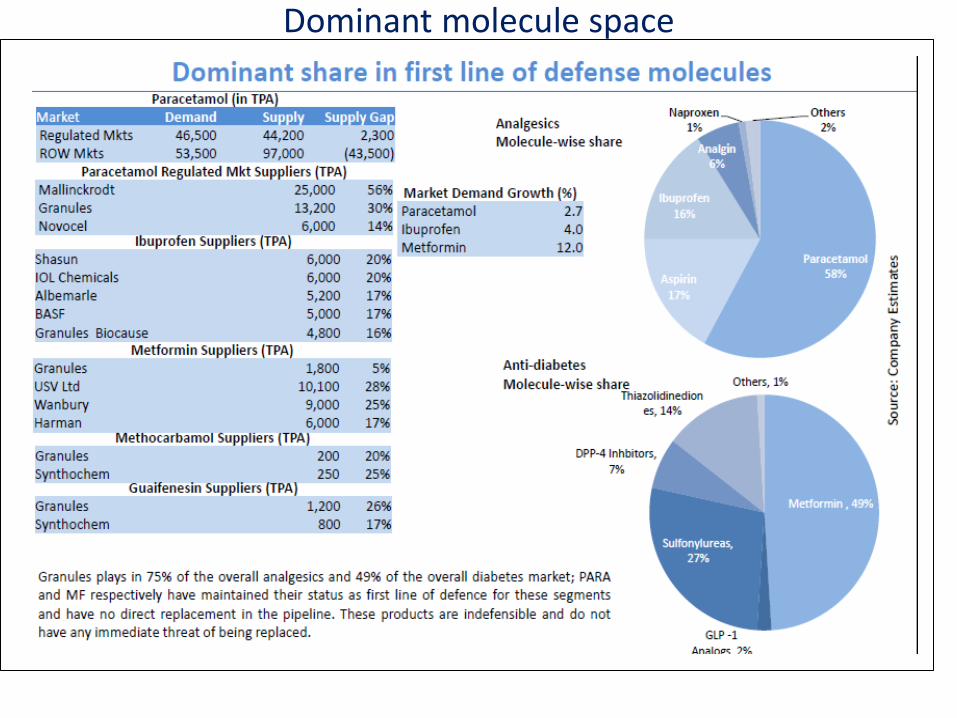

Dominant molecule space

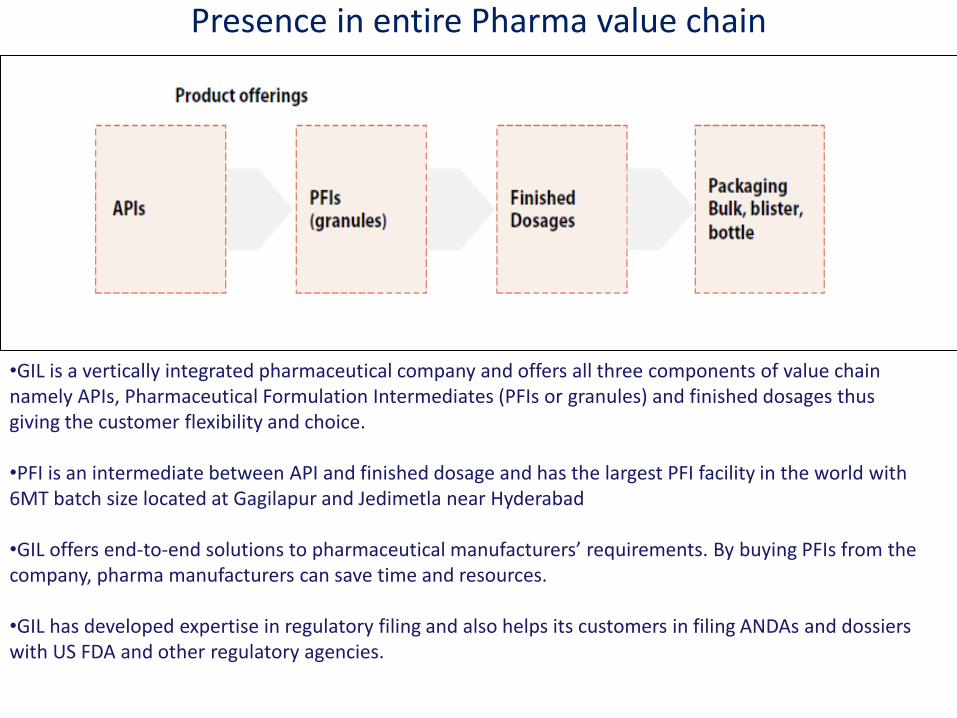

Presence in entire Pharma value chain

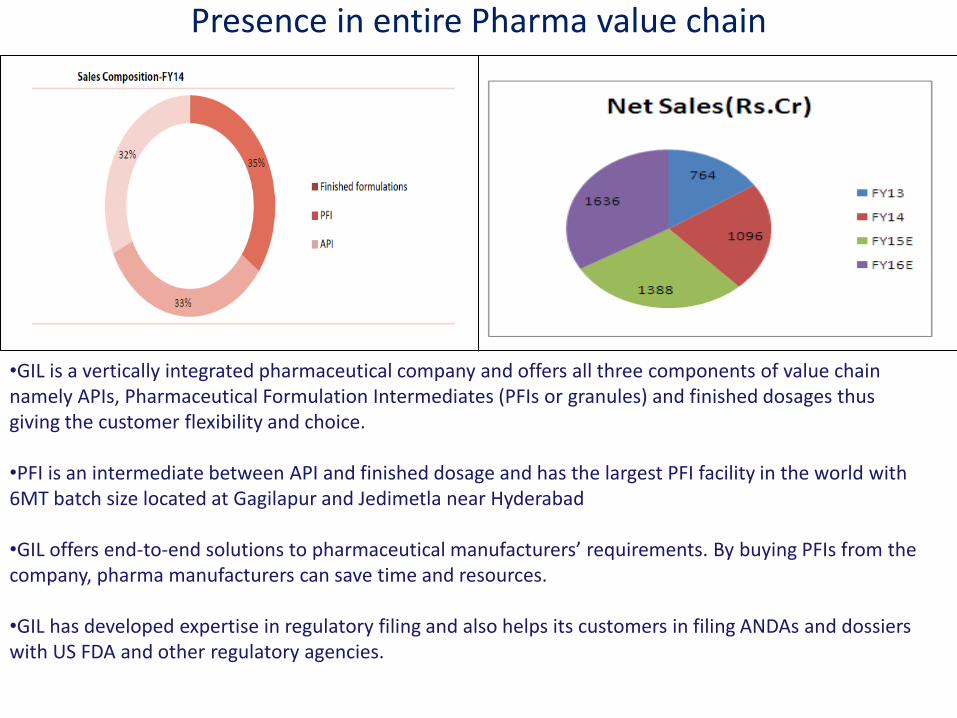

•GIL is a vertically integrated pharmaceutical company and offers all three components of value chain

namely APIs, Pharmaceutical Formulation Intermediates (PFIs or granules) and finished dosages thus

giving the customer flexibility and choice.

•PFI is an intermediate between API and finished dosage and has the largest PFI facility in the world with

6MT batch size located at Gagilapur and Jedimetla near Hyderabad

•GIL offers end-to-e d solutio s to pha a euti al a ufa tu e s e ui e e ts. B u i g PFIs f o the company, pharma manufacturers can save time and resources.

•GIL has developed expertise in regulatory filing and also helps its customers in filing ANDAs and dossiers

with US FDA and other regulatory agencies.

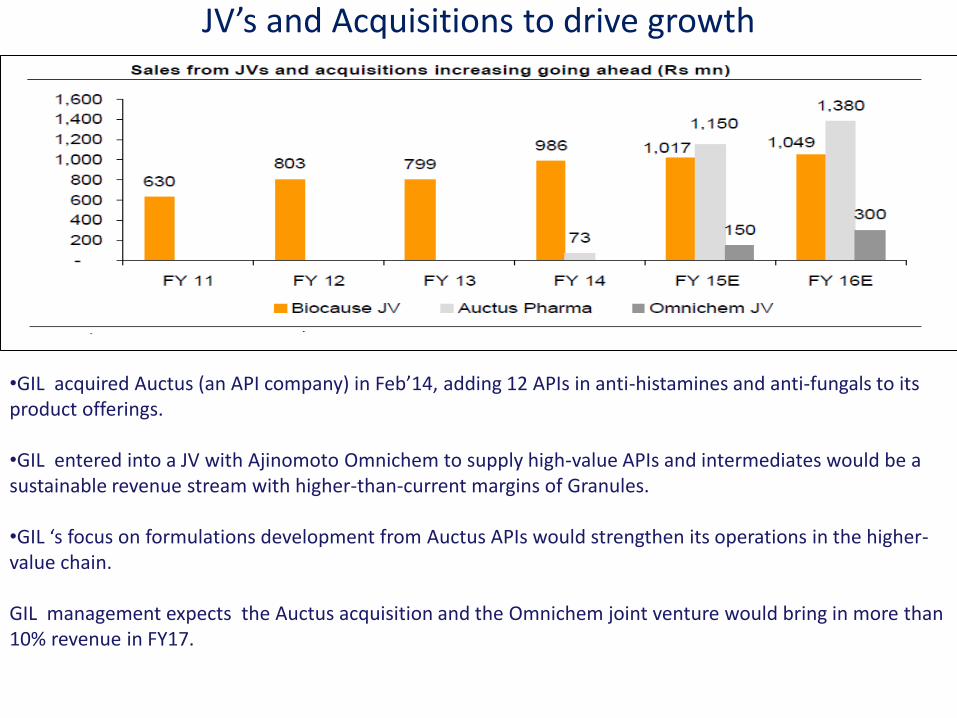

JV s a d A uisitio s to d i e g o th

•GIL acquired Auctus a API o pa i Fe 4, addi g APIs i a ti-histamines and anti-fungals to its

product offerings.

•GIL entered into a JV with Ajinomoto Omnichem to supply high-value APIs and intermediates would be a

sustainable revenue stream with higher-than-current margins of Granules.

•GIL s fo us o fo ulatio s de elop e t f o Auctus APIs would strengthen its operations in the higher-

value chain.

GIL management expects the Auctus acquisition and the Omnichem joint venture would bring in more than

10% revenue in FY17.

Leading global player in key products

•GIL is a vertically integrated pharmaceutical company and offers all three components of value chain

namely APIs, Pharmaceutical Formulation Intermediates (PFIs or granules) and finished dosages thus

giving the customer flexibility and choice.

•PFI is an intermediate between API and finished dosage and has the largest PFI facility in the world with

6MT batch size located at Gagilapur and Jedimetla near Hyderabad

•GIL offers end-to-e d solutio s to pha a euti al a ufa tu e s e ui e e ts. B u i g PFIs f o the company, pharma manufacturers can save time and resources.

•GIL has developed expertise in regulatory filing and also helps its customers in filing ANDAs and dossiers

with US FDA and other regulatory agencies.

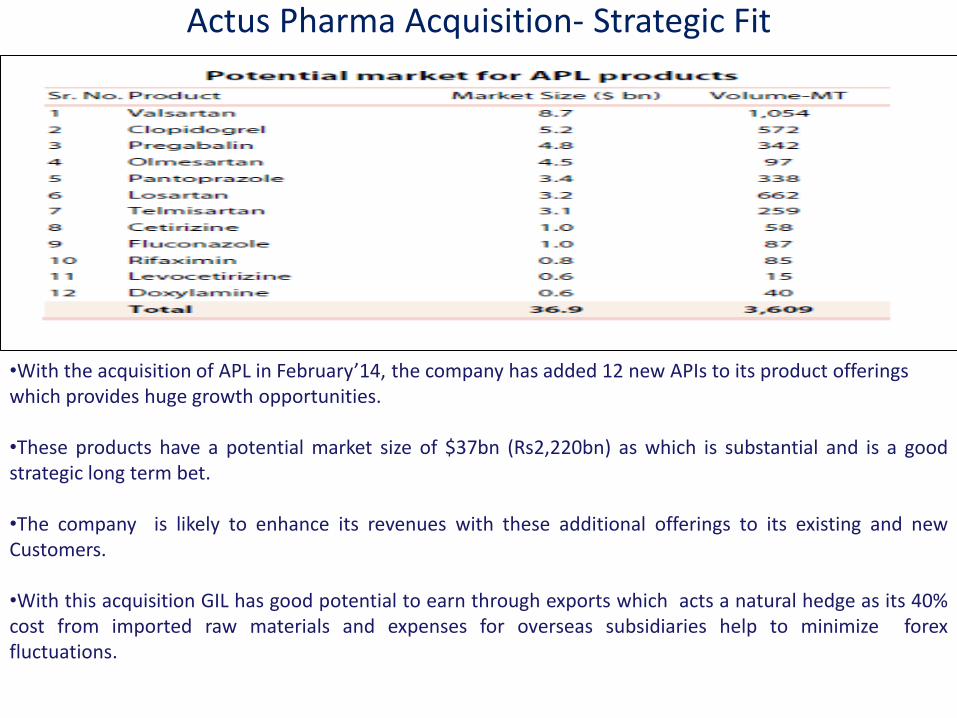

Actus Pharma Acquisition- Strategic Fit

•With the a uisitio of APL i Fe ua 4, the o pa has added e APIs to its p odu t offe i gs which provides huge growth opportunities.

•These products have a potential market size of $37bn (Rs2,220bn) as which is substantial and is a good

strategic long term bet.

•The company is likely to enhance its revenues with these additional offerings to its existing and new

Customers.

•With this acquisition GIL has good potential to earn through exports which acts a natural hedge as its 40%

cost from imported raw materials and expenses for overseas subsidiaries help to minimize forex

fluctuations.

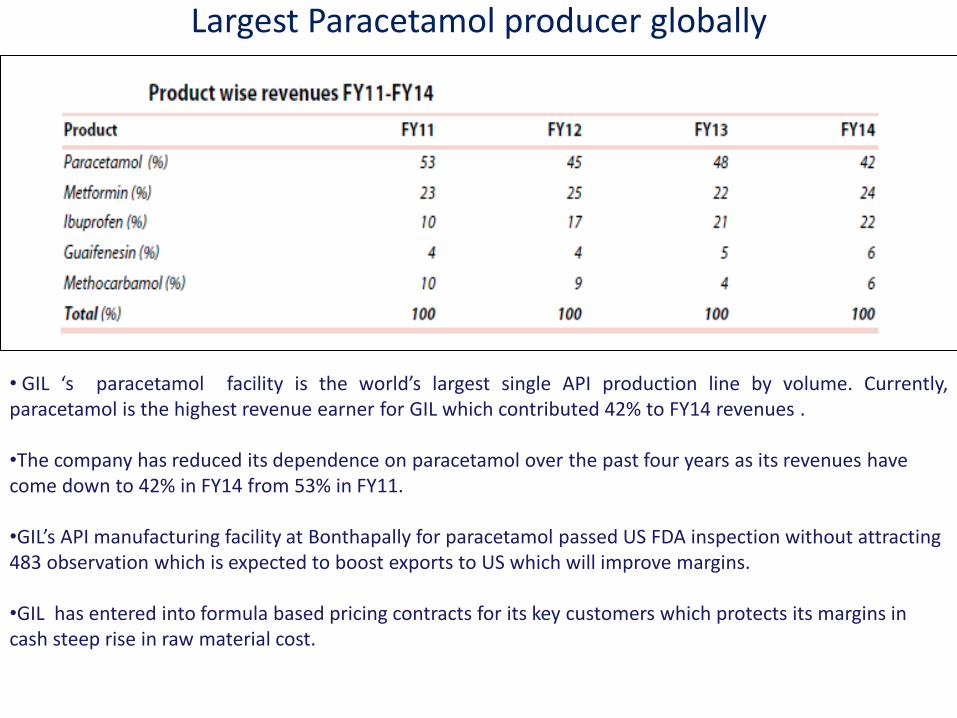

Largest Paracetamol producer globally

• GIL s paracetamol facility is the o ld s largest single API production line by volume. Currently,

paracetamol is the highest revenue earner for GIL which contributed 42% to FY14 revenues..

•The company has reduced its dependence on paracetamol over the past four years as its revenues have

come down to 42% in FY14 from 53% in FY11.

•GIL s API a ufa tu i g fa ilit at Bonthapally for paracetamol passed US FDA inspection without attracting

483 observation which is expected to boost exports to US which will improve margins.

•GIL has entered into formula based pricing contracts for its key customers which protects its margins in

cash steep rise in raw material cost.

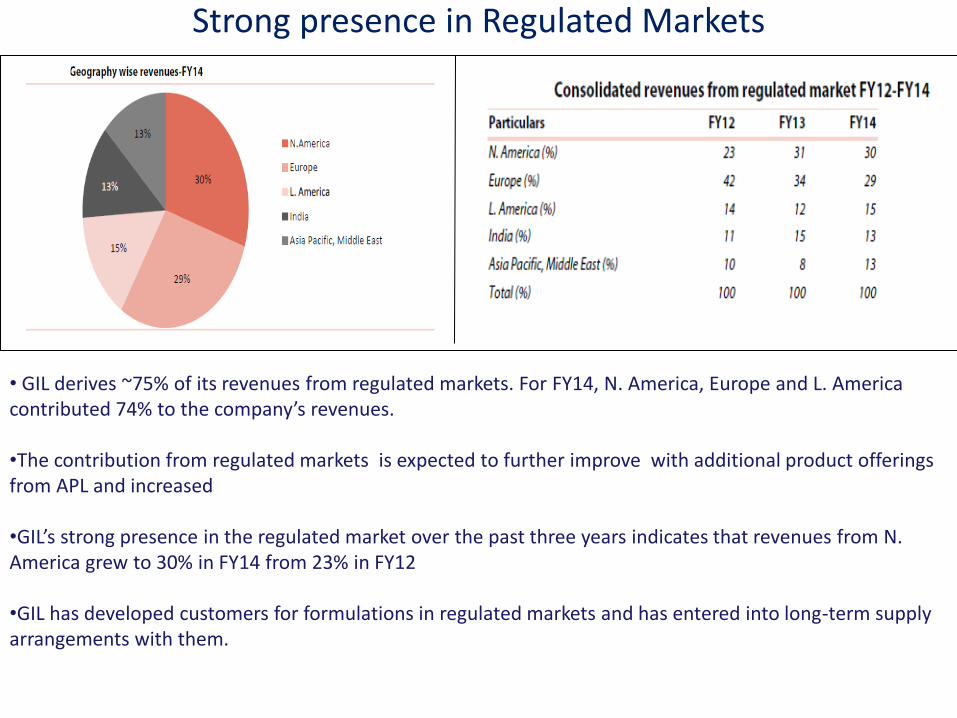

Strong presence in Regulated Markets

• GIL derives ~75% of its revenues from regulated markets. For FY14, N. America, Europe and L. America

o t i uted 74% to the o pa s e e ues.

•The contribution from regulated markets is expected to further improve with additional product offerings

from APL and increased

requirements from its existing customers

•GIL s st o g p ese e i the egulated a ket o e the past th ee ea s i di ates that e e ues f o N. America grew to 30% in FY14 from 23% in FY12

•GIL has developed customers for formulations in regulated markets and has entered into long-term supply

arrangements with them.

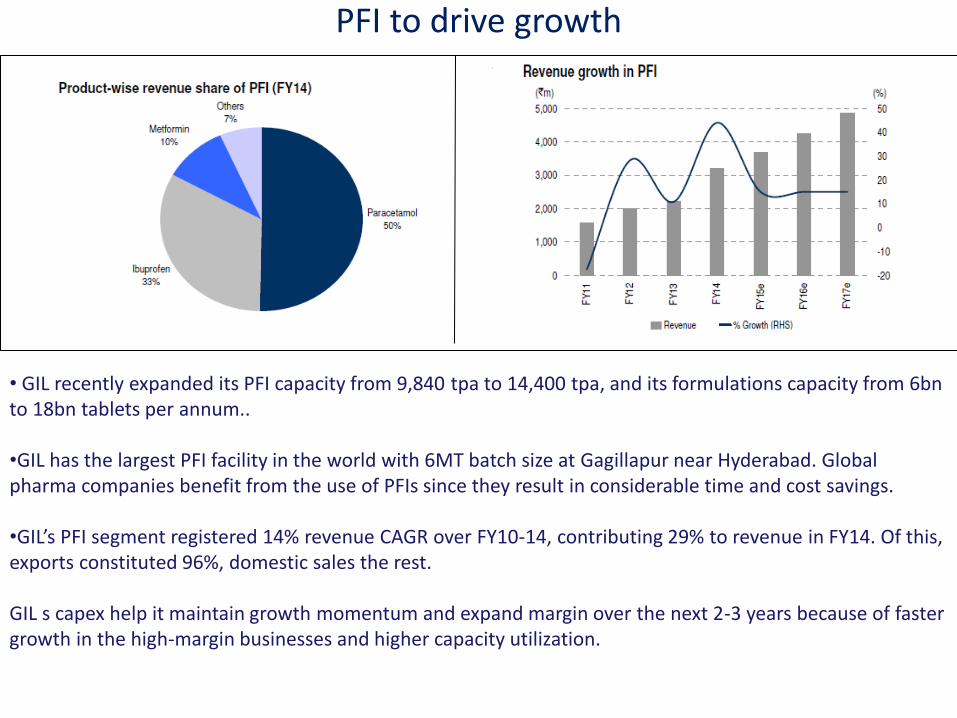

PFI to drive growth

• GIL recently expanded its PFI capacity from 9,840 tpa to 14,400 tpa, and its formulations capacity from 6bn

to 18bn tablets per annum..

•GIL has the largest PFI facility in the world with 6MT batch size at Gagillapur near Hyderabad. Global

pharma companies benefit from the use of PFIs since they result in considerable time and cost savings.

requirements from its existing customers

•GIL s PFI seg e t egiste ed 4% e e ue CAG‘ o e FY -14, contributing 29% to revenue in FY14. Of this,

exports constituted 96%, domestic sales the rest.

GIL s capex help it maintain growth momentum and expand margin over the next 2-3 years because of faster

growth in the high-margin businesses and higher capacity utilization.

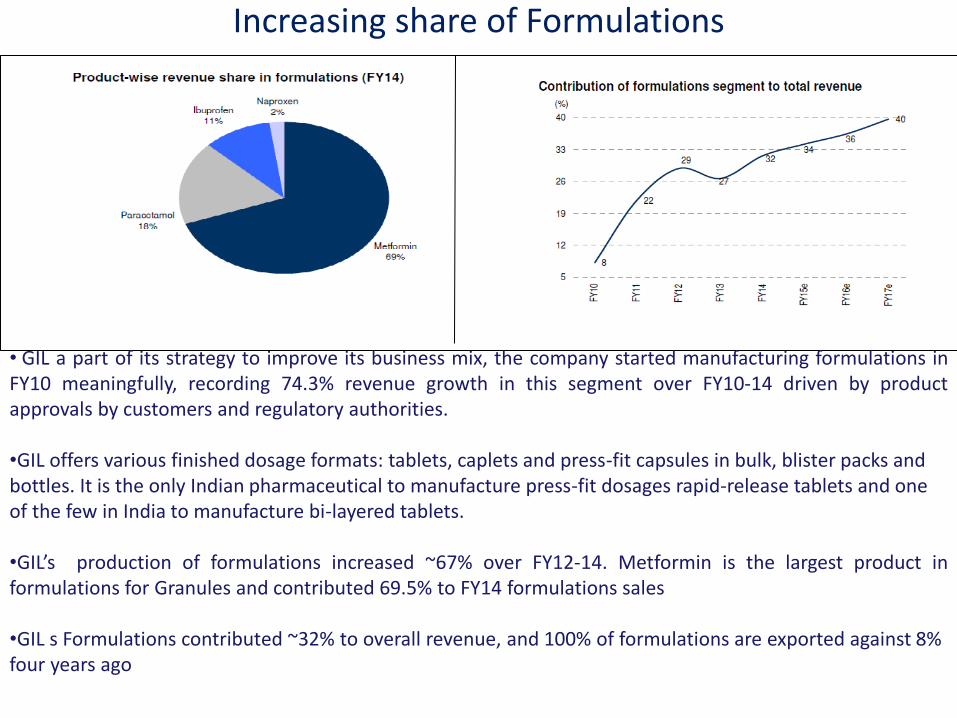

Increasing share of Formulations

• GIL a part of its strategy to improve its business mix, the company started manufacturing formulations in

FY10 meaningfully, recording 74.3% revenue growth in this segment over FY10-14 driven by product

approvals by customers and regulatory authorities.

•GIL offers various finished dosage formats: tablets, caplets and press-fit capsules in bulk, blister packs and

bottles. It is the only Indian pharmaceutical to manufacture press-fit dosages rapid-release tablets and one

of the few in India to manufacture bi-layered tablets.

requirements from its existing customers

•GIL s production of formulations increased ~67% over FY12-14. Metformin is the largest product in

formulations for Granules and contributed 69.5% to FY14 formulations sales

•GIL s Formulations contributed ~32% to overall revenue, and 100% of formulations are exported against 8%

four years ago

Presence in entire Pharma value chain

•GIL is a vertically integrated pharmaceutical company and offers all three components of value chain

namely APIs, Pharmaceutical Formulation Intermediates (PFIs or granules) and finished dosages thus

giving the customer flexibility and choice.

•PFI is an intermediate between API and finished dosage and has the largest PFI facility in the world with

6MT batch size located at Gagilapur and Jedimetla near Hyderabad

•GIL offers end-to-e d solutio s to pha a euti al a ufa tu e s e ui e e ts. B u i g PFIs f o the company, pharma manufacturers can save time and resources.

•GIL has developed expertise in regulatory filing and also helps its customers in filing ANDAs and dossiers

with US FDA and other regulatory agencies.

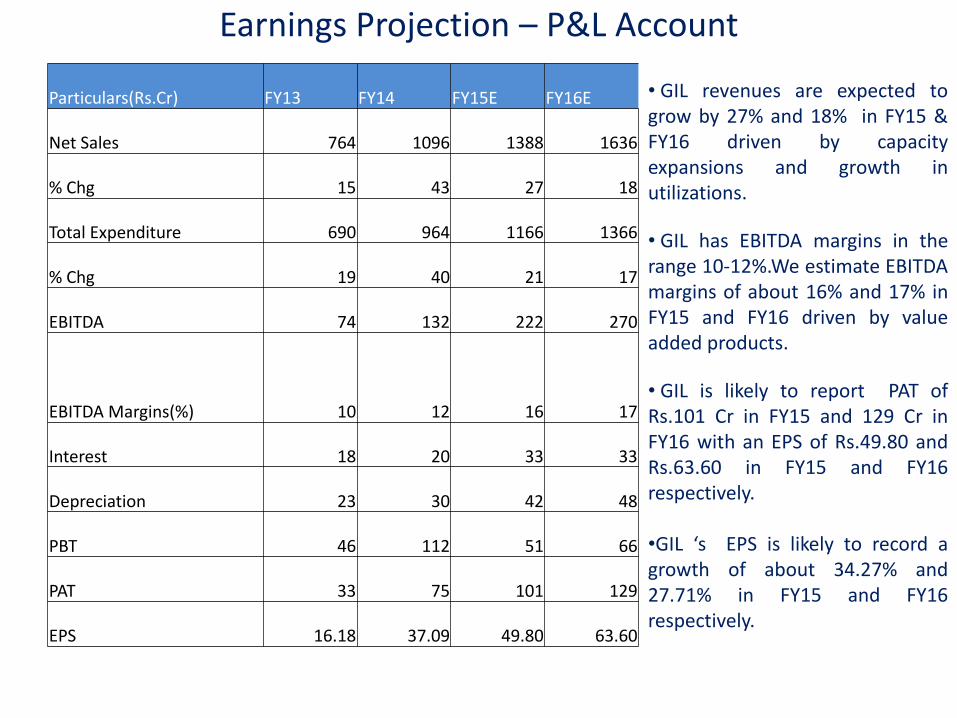

Earnings Projection – P&L Account

• GIL revenues are expected to

grow by 27% and 18% in FY15 &

FY16 driven by capacity

expansions and growth in

utilizations.

• GIL has EBITDA margins in the

range 10-12%.We estimate EBITDA

margins of about 16% and 17% in

FY15 and FY16 driven by value

added products.

• GIL is likely to report PAT of

Rs.101 Cr in FY15 and 129 Cr in

FY16 with an EPS of Rs.49.80 and

Rs.63.60 in FY15 and FY16

respectively.

•GIL s EPS is likely to record a

growth of about 34.27% and

27.71% in FY15 and FY16

respectively.

Particulars(Rs.Cr) FY13 FY14 FY15E FY16E

Net Sales 764 1096 1388 1636

% Chg 15 43 27 18

Total Expenditure 690 964 1166 1366

% Chg 19 40 21 17

EBITDA 74 132 222 270

EBITDA Margins(%) 10 12 16 17

Interest 18 20 33 33

Depreciation 23 30 42 48

PBT 46 112 51 66

PAT 33 75 101 129

EPS 16.18 37.09 49.80 63.60

Concerns & Reasoning

1.) Regulatory Risk :

Granules supplies to export markets, and hence being a pharma player it is mandatory that it secures

approvals from several regulatory bodies across the globe. Granules has approved facilities from several

regulatory bodies across the globe like USFDA, UK-MHRA, EDQM, KFDA, WHO GMP, Health Canada, TGA etc.

The recent increase in scrutiny and adverse outcome for several players in the industry continues to be the

biggest risk in the pharma sector and implies to Granules too.

2.) Foreign Exchange Risk :

Most of G a ules revenue accrues from exports roughly 87% FY14, but at the same time a large component

(around 60%) of its raw material requirements is imported. Hence, it enjoys a natural hedge. The company

also has most of its debt in foreign currency. Granules also has clauses in most of its contracts, wherein it

adjusts the selling price based on the Forex rate.

3.) Limited disclosure Risk :

Agreements between Granules and its partners/customers are confidential in nature and is bound t be so.

The estimates are based on information which is believed to be accurate and any major deviations may

adversely impact the company.

4.) Concentration Risk :

In the generics and API business, the companies have high dependency on select products. Hence, they face

the risk of low diversity in products. Incidentally, Granules derives around 90% of its revenue from top-4

products.

THANK YOU